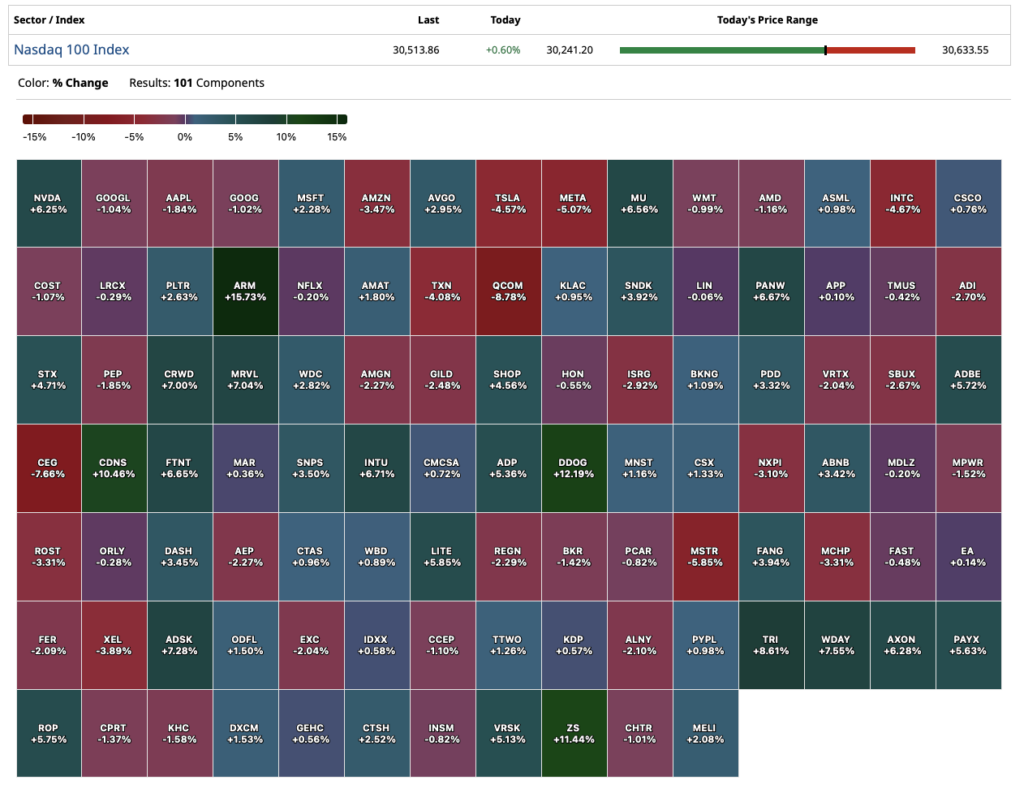

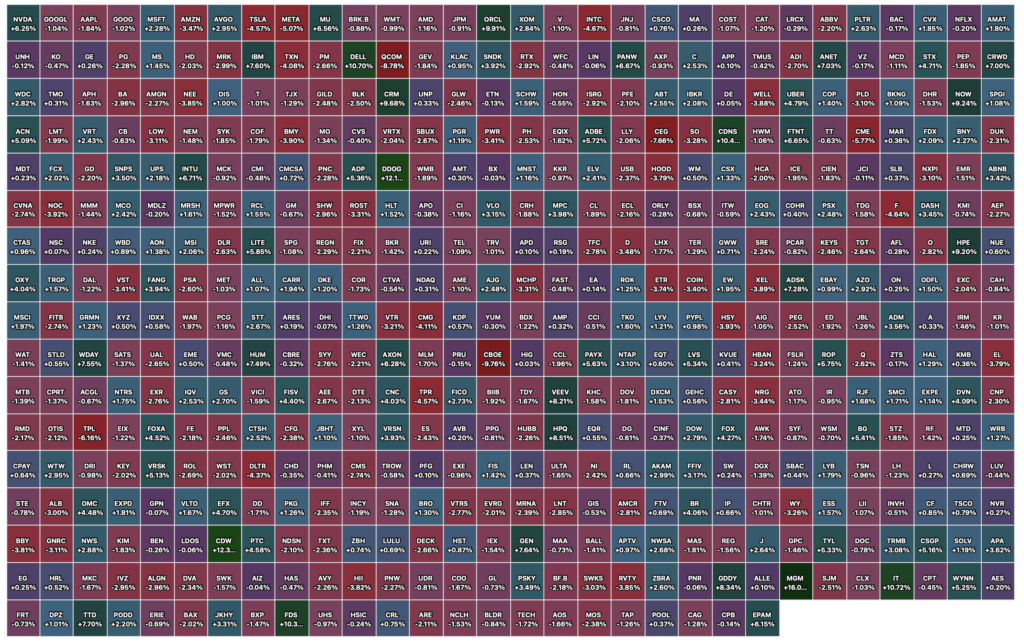

Equal-weight S&P is at its most extreme underperformance vs. cap-weight in decades@CarterBWorth says it can only be one of two things: a major market bottom or a major market top… pic.twitter.com/HmrWaPEwkX

Manufacturing continuing to benefit from order pull forwards, along with the obvious

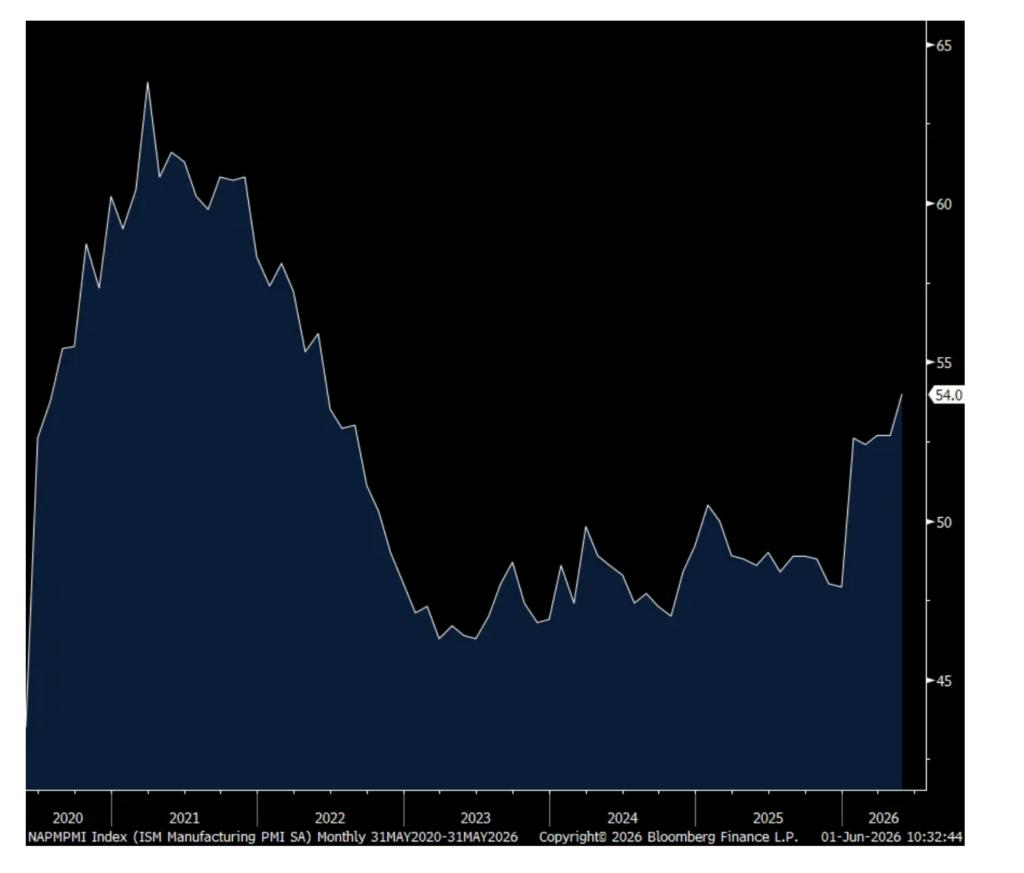

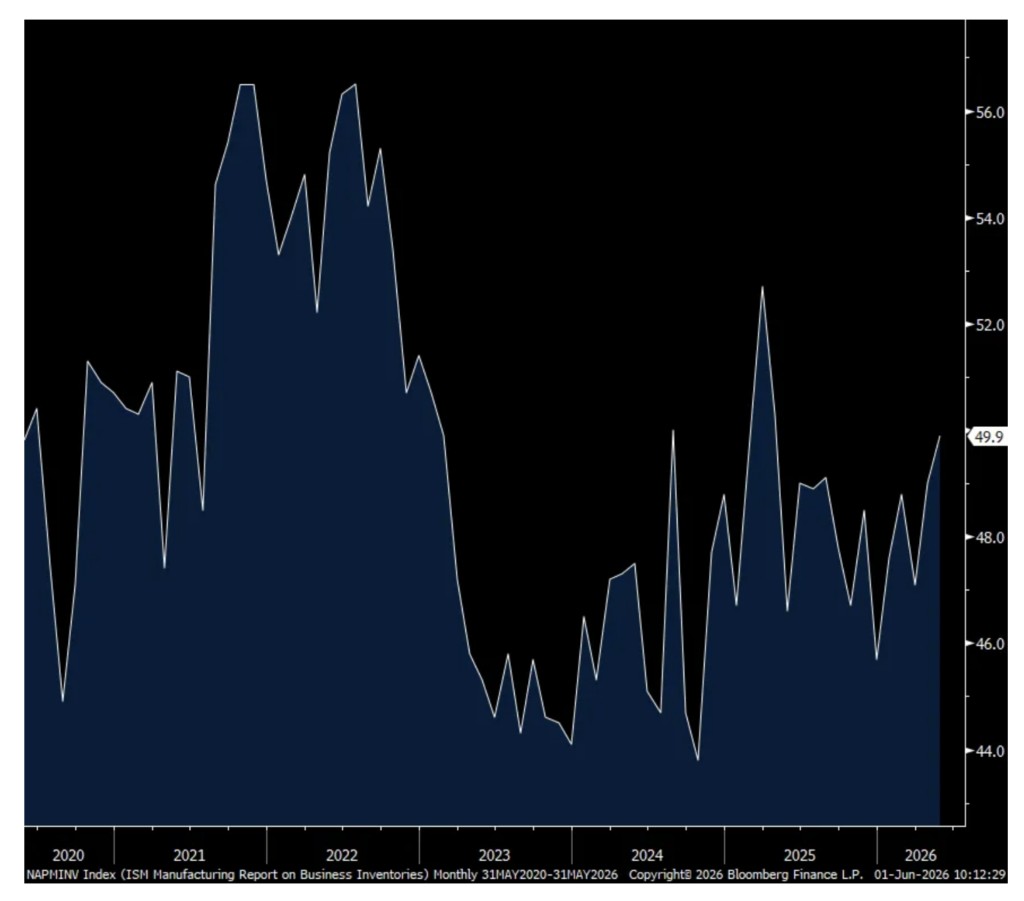

The May ISM manufacturing index rose to 54 from 52.7 and was 1 pt above the estimate. Strength in new orders helped again, rising by 2.7 pts m/o/m to 56.8 and backlogs were above 50 for the 5th month in a row at 52.2. Inventories got to 49.9, around the flat line but that is the highest since April 2025. Customer inventories remain well below 50 at 42.7 but that is the highest in 5 months.

Employment was in contraction again at 48.6 but up 2.2 pts m/o/m.

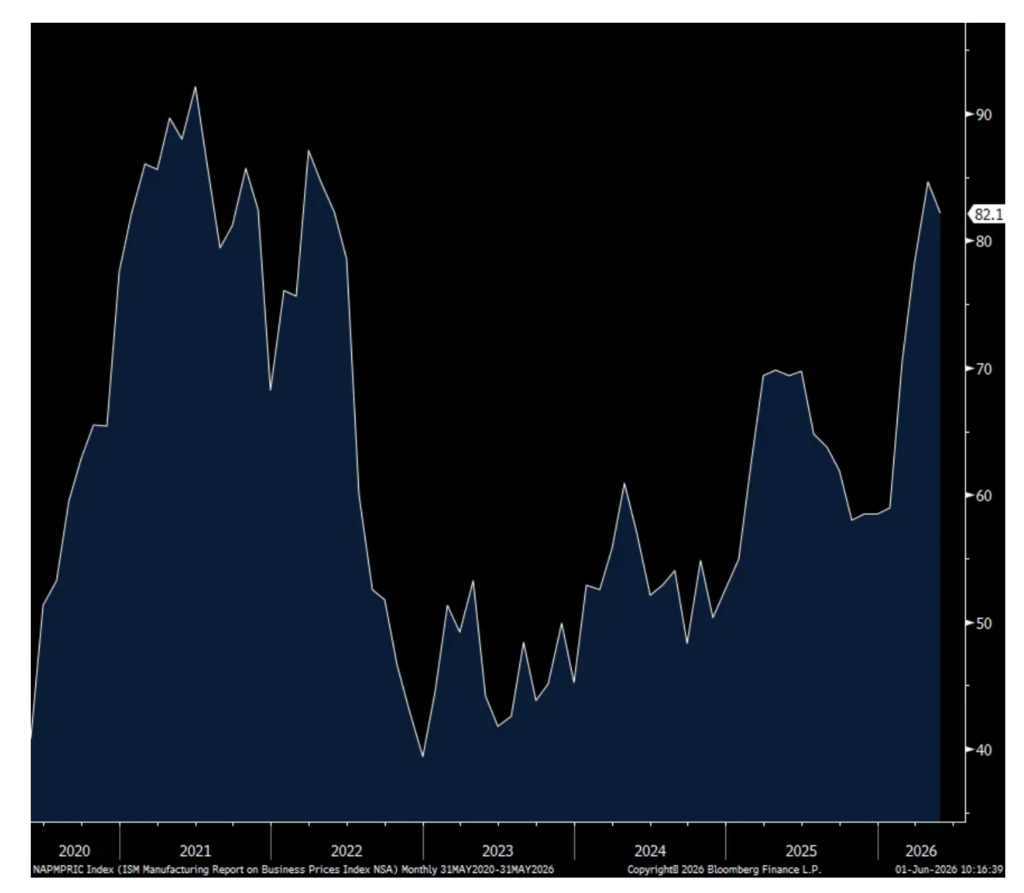

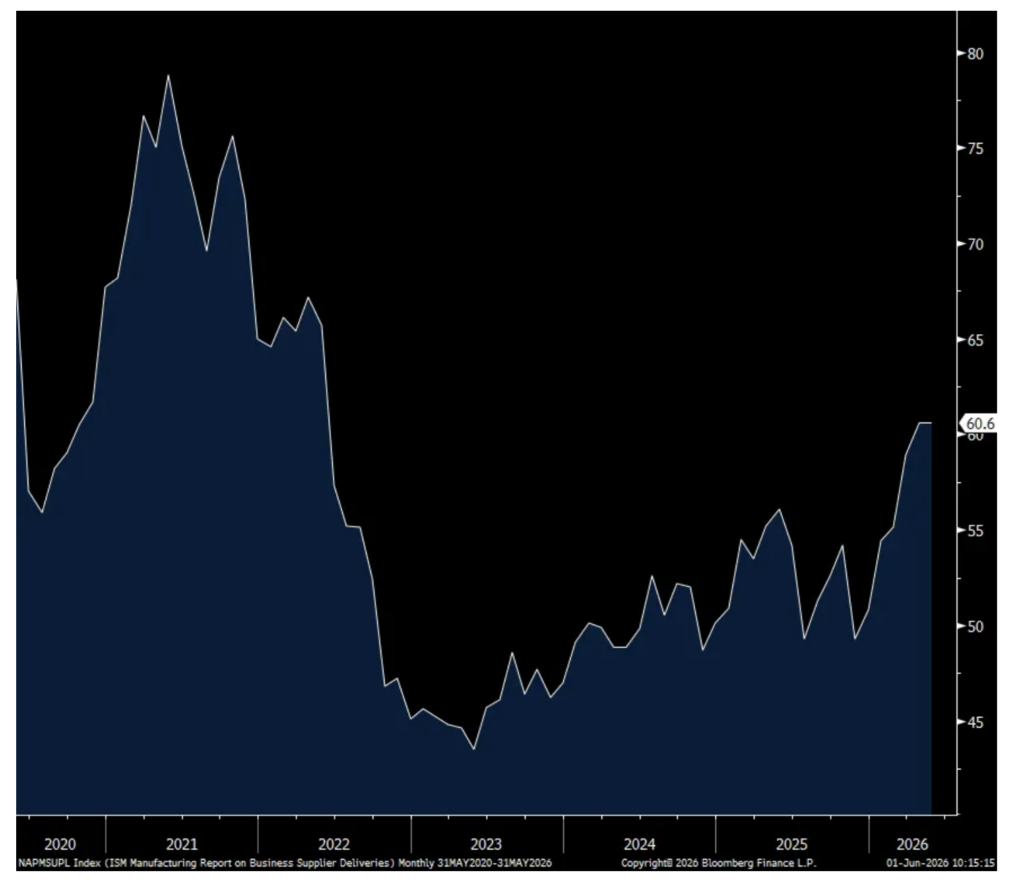

With respect to the supply chain, Supplier Deliveries were unchanged at 60.6 but remaining at the highest level since May 2022 and the higher it is, the slower the lead times. Prices paid slipped back by 2.5 pts to a still very high 82.1 and after rising by 6.3 pts in April to the highest since March 2022. ISM said this on prices, “The Prices Index reading is still being driven by (1) increases in steel and aluminum prices that impact the entire value chain, (2) tariffs applied to many imported goods and (3) increases in petroleum-based products as a result of the Middle East conflict.”

Export orders lifted by 2.7 pts to 50.6 as I’m sure everyone around the world scrambles to front run orders with the US a key supplier.

Industry breadth further improved with 16 of 18 industries seeing growth vs 13 in the two prior months. In December it was at just 2. One saw a contraction, ‘wood products’, vs 3 in April.

I’m going to steal the bottom line from today’s S&P Global US manufacturing PMI because I believe it helps best to describe what has contributed to the improvement in global manufacturing over the past few months:

“At first glance, the manufacturing sector seems to be firing on all cylinders but lift the hood and the picture is not so clear…since the outbreak of war in the Middle East we have seen production and demand buoyed by stock building as companies worry over rising prices and supply difficulties. This stockpiling was again widely evident in May and makes it hard to take an accurate reading on the underlying health of the manufacturing economy, as growth will cool once this stock build has run its course.”

I’ll add to this, not mentioned but obvious, anyone making anything going into the date center construction is benefiting hugely of course.

And, “The incidence of supply chain delays is the highest since August 2022, with the buying of safety stocks not only adding to the supply squeeze from the closure of the Strait of Hormuz but also pushing prices higher for a wide variety of inputs…Manufacturers’ own charges rose to the greatest extent since September 2022 as they sought to pass through their own higher expenses to clients wherever possible.”

The respondent comments in the ISM are filled with worries about supply chains and rising costs:

“Impact of Iran conflict starting to directly and negatively impact cost of supply chain. Oil and related commodities are escalating in price.” [Transportation Equipment]

“The Middle East conflict is triggering shipment delays and uncertainties. Elevated gas prices and inflation will surely impact our purchases. However, over the last quarter, we’ve seen increased demand that was unexpected.” [Machinery]

“As with all companies, we have felt the effects of fuel-related inflation and general market uncertainty due to overall economic variability and geopolitical events that have impacted such markets as construction, automotive and agriculture, as well as the general industrial sector.” [Chemical Products]

“Continuing trends of 15-percent sales increase in April, cost increases on a majority of raw materials, and fuel charges on many inbound and outbound deliveries. We remain cautiously optimistic that if global economic factors stabilize and the Iran conflict ends, we can continue with increased sales and maintain acceptable margins.” [Chemical Products]

“Cost of diesel is having huge impacts on our profitability. Confusion abounds around tariff refunds. We purchase many imported goods but in most cases are not the importer of record, so it is currently unclear to what we may be entitled.” [Food, Beverage & Tobacco Products]

“Prices continue to rise for many products — some due to increase in data center creation for electronic components, others as a result of the Iran war and reductions in availability of oil/petroleum.” [Computer & Electronic Products]

“Supply constraints continue to propagate and are a key headwind to supporting increased aerospace and defense demand. Semiconductors, critical minerals and certain types of raw materials are illustrative examples of sales plans at risk. Corporate risk mitigation actions are underway to secure supply in the midst of constraints.” [Transportation Equipment]

“The current atmosphere is one of extreme uncertainty and concern for the future in terms of both price stability and longer-term supply continuity related to the Iran conflict and Strait of Hormuz closure. We have a lot of negotiations in process related to requested price increases, some related to oil prices and some still fallout from the 2025 tariff/geopolitical climate.” [Miscellaneous Manufacturing]

“Continued dynamic random-access memory (DRAM) volatility, increased gas prices and tariffs are causing long lead constraints and price hikes that customers are not willing to bear. Panic is starting within our industry.” [Electrical Equipment, Appliances & Components]

“Business appears to be weakening — uncertainty surrounding the Iran war, rising energy prices and customers unwilling to commit to expenditures beyond a very short term.” [Fabricated Metal Products]

Treasury yields are rising but all related to the jump in oil prices.

Some perspective from Michael Burry on X posted last week, that I first saw over the weekend, on the size of the upcoming major IPOs relative to the size and pace we saw in the late 1990’s.

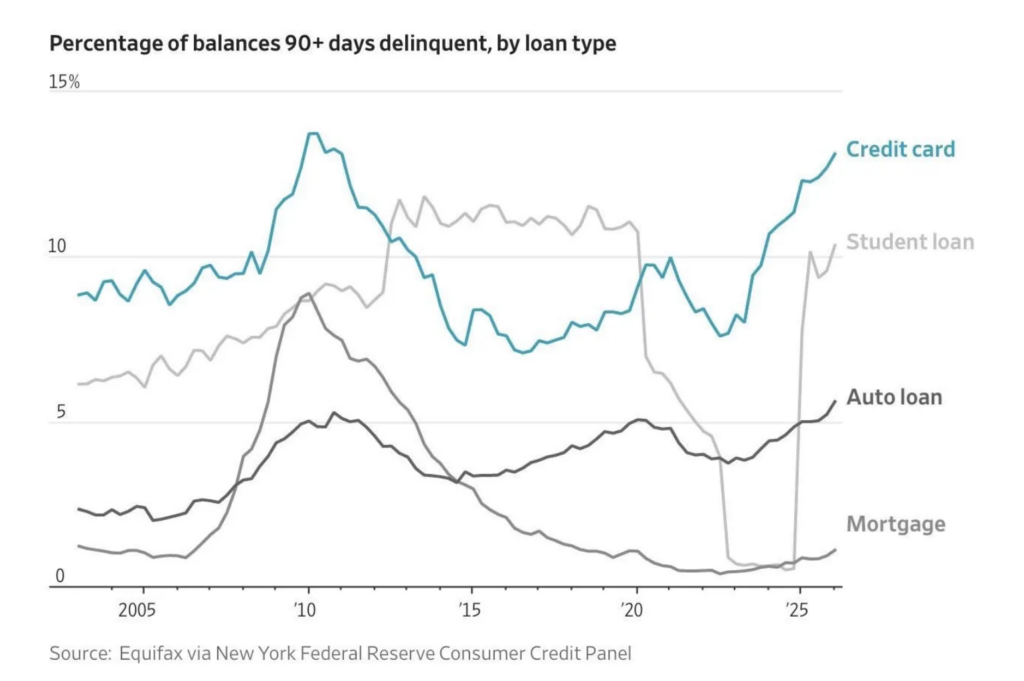

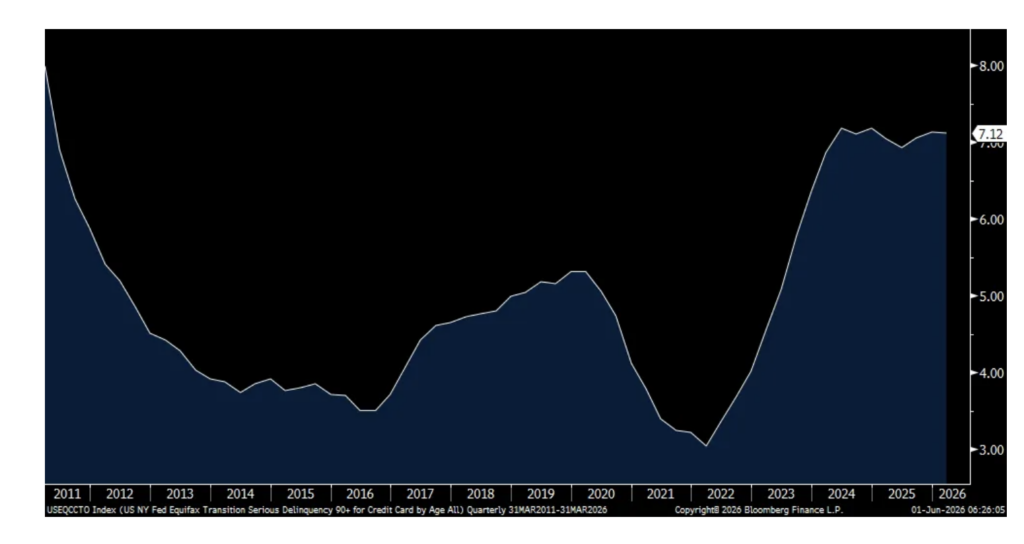

This is an updated chart from the WSJ a few days ago on the % of delinquencies that are 90+ days. What is considered delinquent is a bill that hasn’t been made in 30 days, so, the 13% is not an absolute delinquency figure but of those considered ‘delinquent’, the extent at which it’s 90 days or more. The actual 90 day delinquency rate according to the NY Fed for Q1 was 7.1%, steady over the past 2 years, though around the highest in 15 years. The 90+ day delinquency rate for autos is at 2.97%, just below a 15 yr high.

US oil drillers continue to respond to higher oil prices by putting more rigs to work. The Baker Hughes crude oil rig count rose by another 4 as of Friday. That’s the 5th week higher and by 22 over this time frame. We need it as we heard this warning last Thursday from Neil Chapman, a senior VP at Exxon last week speaking at the Bernstein conference.

“Commercial inventories of crude oil, of liquids, think petroleum, gasoline, diesel, jet fuel, they’ve all run down. And running down those inventories has mitigated or offset, supplemented by the release of strategic petroleum reserves, which most of the Western countries have done. All of that has mitigated the impact. You can model this. We’ve modeled it. I think a lot of people in the industry have modeled it. We’re approaching unheard of inventory levels. I mean, really, really low levels. You can debate whether that’s going to hit those really low levels in two weeks or three weeks. Once you get to that point, then you’ll see price shoot up. I mean, I think dated Brent, most people, well, a model would say dated Brent will shoot up. Once you get to that really low inventory level, up to $150, $160, the models would tell you that. And then what happens is when the price gets to a certain level, demand destruction brings it back into balance. Prices go so high, it becomes unaffordable and that’s what happens. And so we’re at that level right now.” I bolded to emphasize.

“And I think crude being in this sort of $90 to $110 for the last whatever it is, six weeks, has really been mitigated by running down inventories. It can’t last forever. So we’ll see what happens. Predicting this and the exact timing, it’s always a challenge. But that’s the way we see the picture.”

Crude Oil Rig Count

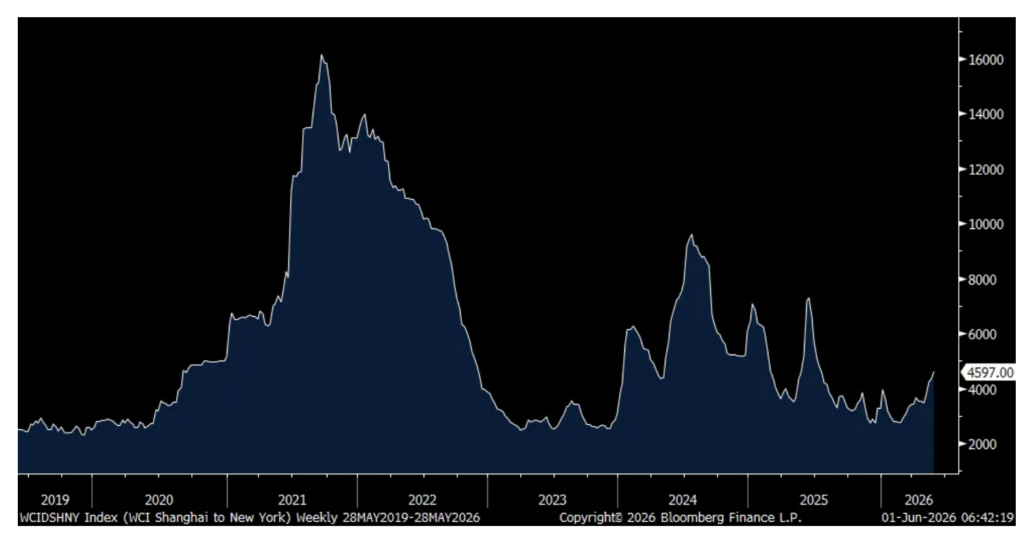

Seen last Thursday, container shipping prices continue to rise. The Shanghai to NY price rose another 6.5% w/o/w, up for the 11th week in the past 13 since the conflict started. Relative to the Covid spikes, we remain well below though. The Shanghai to LA chart looks similar and prices rose 2.6% w/o/w.

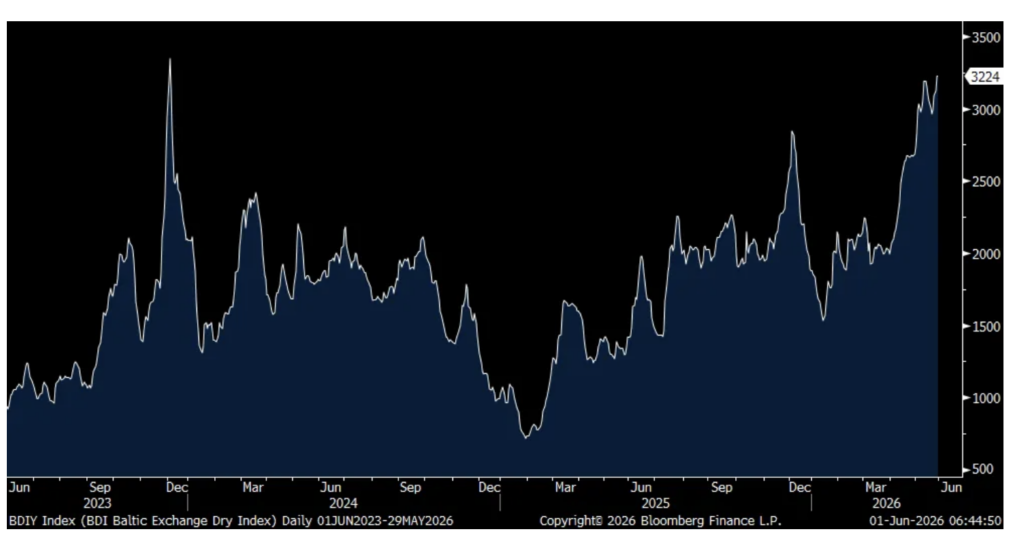

The Baltic Dry Index was flat on Friday but at the highest since late 2023. We know too that spot trucking prices have been rising to record highs. I highlight these transportation costs because we know these price changes flow through to the rest of us.

Shanghai to NY

Baltic Dry Index

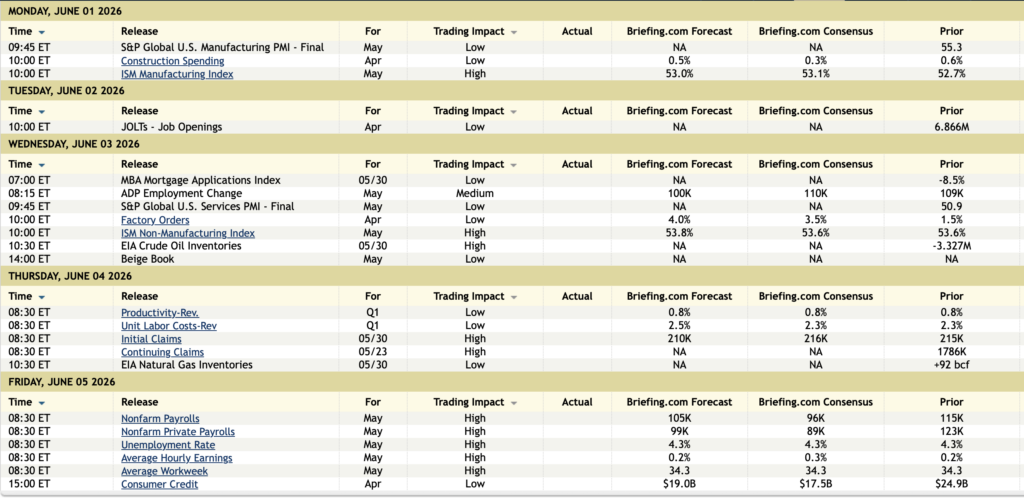

Ahead of the US ISM report at 10am est, here were the May PMI’s seen overseas and they mostly improved again, helped by tech and order pull forwards but with rising cost pressures:

South Korea 54.8 vs 53.6 (certainly helped by Samsung and SK Hynix)

Taiwan 56.1 vs 55.3 (certainly helped by TSMC)

Vietnam 52.8 vs 50.5

Japan 54.5 vs 55.1

Australia 50.7 vs 51.3

India 55 vs 54.7

Philippines 50.8 vs 48.3

The China state focused manufacturing was 50 vs 50.3 in April. The non-manufacturing PMI (including construction) was 50.1 vs 49.4.

“When effected, the Reverse Stock Split will reduce Verano’s total issued and outstanding shares of common stock and is expected to deliver an increase in the price per share. Management also believes the Reverse Stock Split may provide additional benefits, including increasing institutional investor interest and access as the Company pursues uplisting on a U.S. exchange in the future.”

More:

The history of price action has not been kind to the companies in this sector.

If Verano is doing a 1-5 and the share price to maintain is $4-$5 to meet exchange requirements. I would have to assume they are expecting some kind of positive catalysts in the short term. MSOS

— Anthony Varrell (@V_arrell)

This is starting to sound like Congress doesn’t need to pass SAFE… the theory grows. https://t.co/Ld2xREb6jC

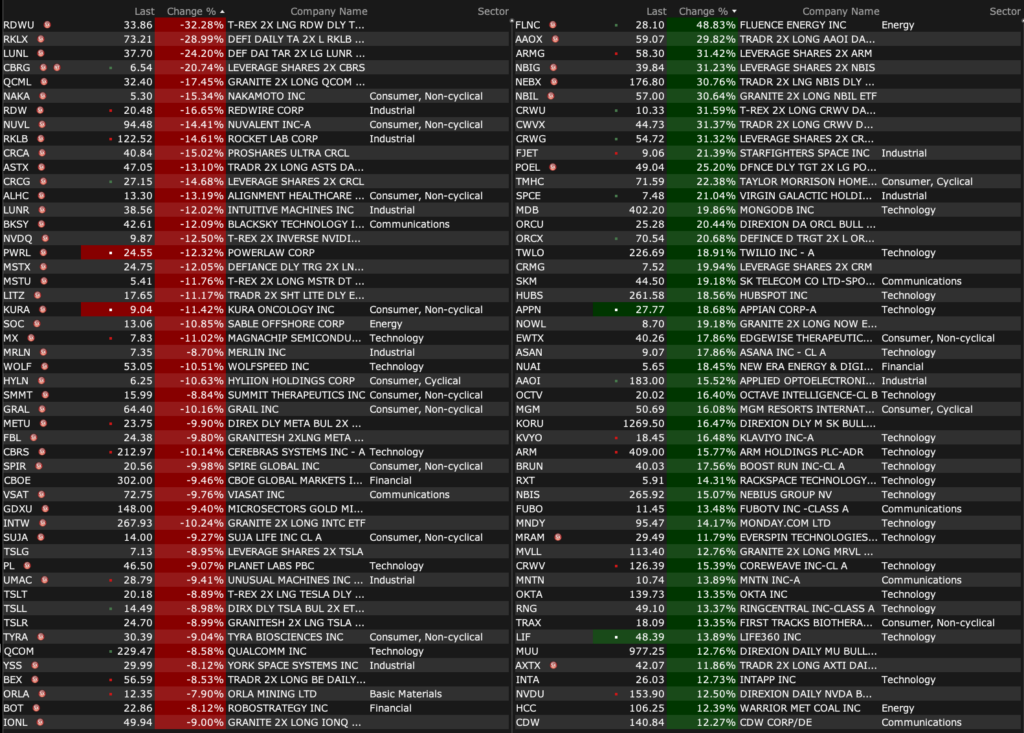

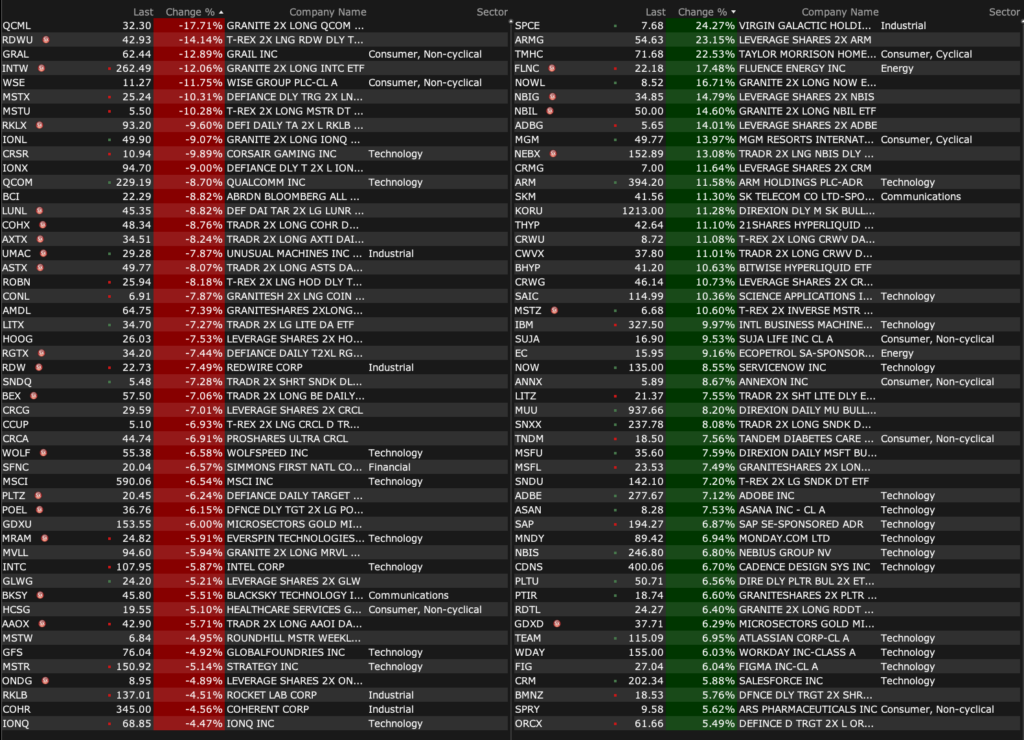

-EWTX +33% (sells sevasemten and muscular dystrophy business to Servier for up to $2.65B) -SPCE +24% (momentum) -TMHC +22% (to be acquired by Berkshire Hathaway for $72.50/share which equates to an equity value of $6.8B in cash and EV of $8.5B) -MGM +15% (Barry Diller’s business empire, People Inc., said to be planning to bid $48.30/shr in cash for the 73.9% of MGM Resorts that it doesn’t already own, valued at $18B) -IBM +9.4% (higher off re-circulation of video showing President Trump mentioning company) -CDNS +7.6% (advances ChipStack AI Super Agent to Level-5 autonomy) -VAC +4.8% (hearing Goldman Sachs Raised VAC to Buy from Sell, price target: $100) -MSFT +3.8% (Microsoft and Nvidia are expected to unveil the first Windows computer powered by chips from Nvidia) -HUM +3.6% (affirms FY26 guidance) -EQNR +3.2% (Chair to resign; To nominate Jarle Roth as new Board chair) -RVMD +2.8% (Oppenheimer Reiterates RVMD with Outperform, price target: $195 from $165) -NVDA +2.3% (Microsoft and Nvidia are expected to unveil the first Windows computer powered by chips from Nvidia ; Hearing added to ‘Best of Breed’ list at Davidson)

Downside:

-OCS -30% (Phase 3 DIAMOND-1 and DIAMOND-2 results did NOT meet primary endpoints) -QCOM -7.5% (weakness following NVDA launching PC chip) -RDW -6.9% (Jefferies Cuts RDW to Hold from Buy) -INTC -5.9% (weakness following NVDA launching PC chip) -MSTR -5.2% (sold 32 BTC for $2.5M during May 26-31st at an average sale price of $77,135) -AMD -3.9% (weakness following NVDA launching PC chip) -ASTS -3.7% (hearing Deutsche Bank Cuts ASTS to Hold from Buy, price target: $106)

AI-related companies have issued ~$140 billion in investment-grade bonds year-to-date, accounting for 49% of the total IG issuance.

AI-related companies have also attracted ~$220 billion in venture capital funding year-to-date, making up 87% of the total.… pic.twitter.com/dppFGbumH9

Equal-weight S&P is at its most extreme underperformance vs. cap-weight in decades

@CarterBWorth says it can only be one of two things: a major market bottom or a major market top...

S&P average single-stock 1m put-call skew has now collapsed to the lowest level in Goldman Sachs entire dataset.

Translation: Everyone is a bull.

Source: Goldman Sachs

The history of price action has not been kind to the companies in this sector.

If Verano is doing a 1-5 and the share price to maintain is $4-$5 to meet exchange requirements. I would have to assume they are expecting some kind of positive catalysts in the short term. $MSOS

FUN FACT 🚨: The Stock Market has never peaked in June Show more

Ryan Detrick, CMT

@RyanDetrick

As we head into June with the S&P 500 at the highest level it has ever traded at, just remember this is the only month to never see the ultimate peak for the year.

This is starting to sound like Congress doesn’t need to pass SAFE… the theory grows.

Anthony Martinelli

@AMartinelliWA

Verano Holdings Corp. has approved a 1-for-5 reverse stock split as the multistate marijuana operator prepares for a potential listing on a major U.S. stock exchange. themarijuanaherald.com/2026/06/verano…

This is incredible:

AI-related companies have issued ~$140 billion in investment-grade bonds year-to-date, accounting for 49% of the total IG issuance.

AI-related companies have also attracted ~$220 billion in venture capital funding year-to-date, making up 87% of the total.Show more