Quoth the Raven on Bitcoin

Position: None

BY Doug Kass · Jun 2, 2026, 4:40 PM EDT

Position: None

BY Doug Kass · Jun 2, 2026, 4:40 PM EDT

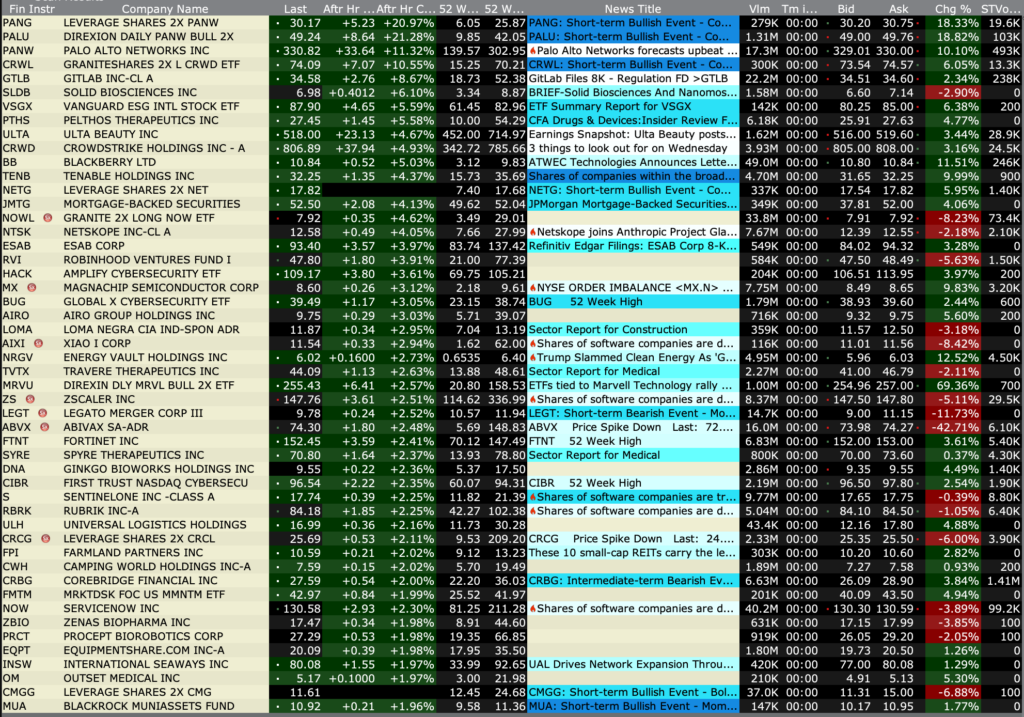

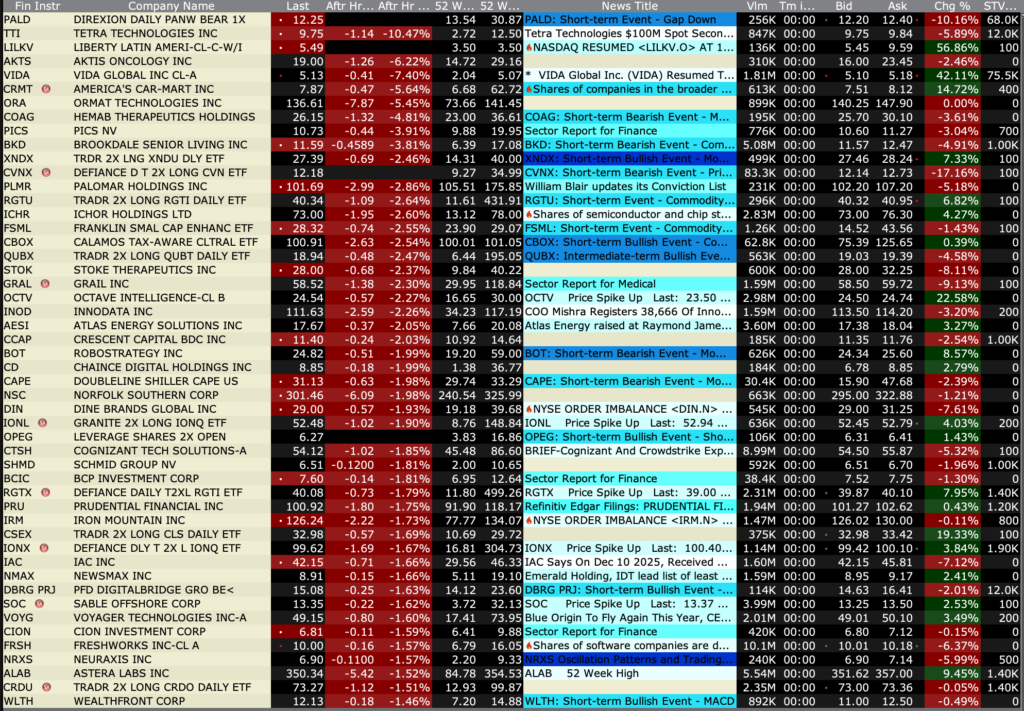

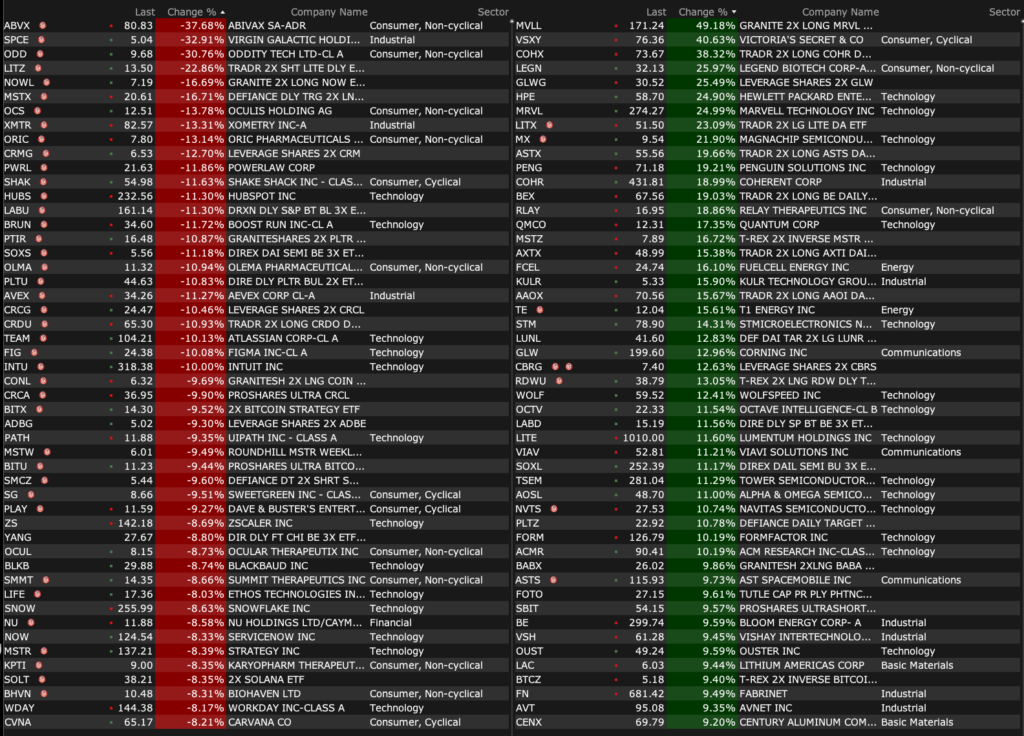

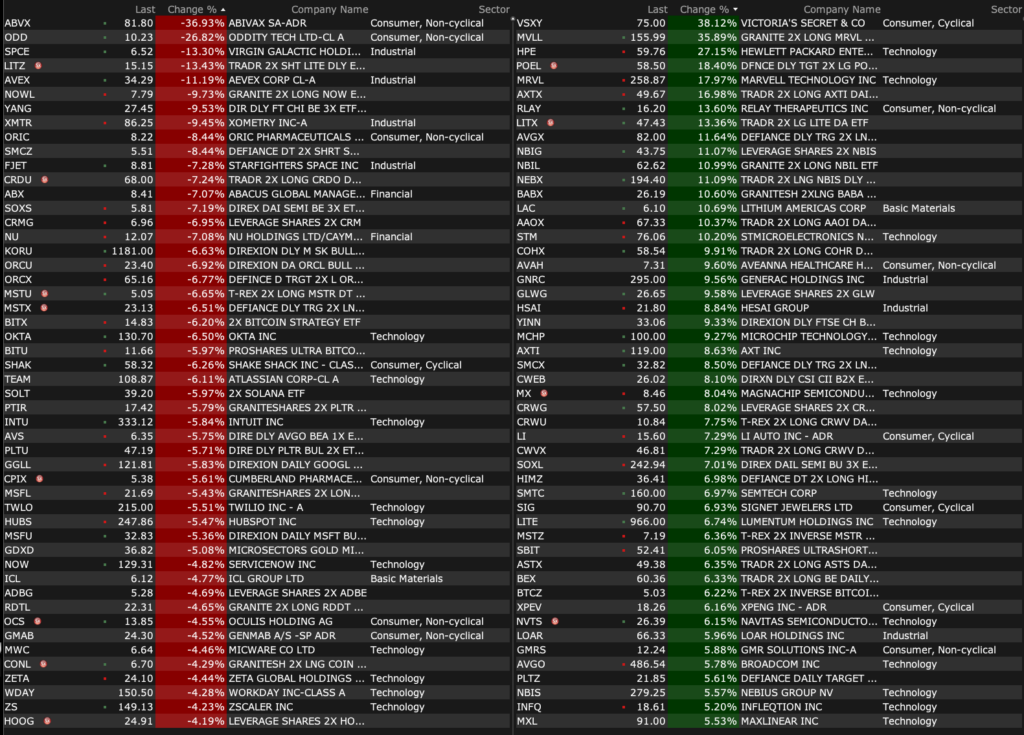

After-Hours % Advancers

After-Hours % Advancers

Position: None

BY Doug Kass · Jun 2, 2026, 4:35 PM EDT

Closing Volume

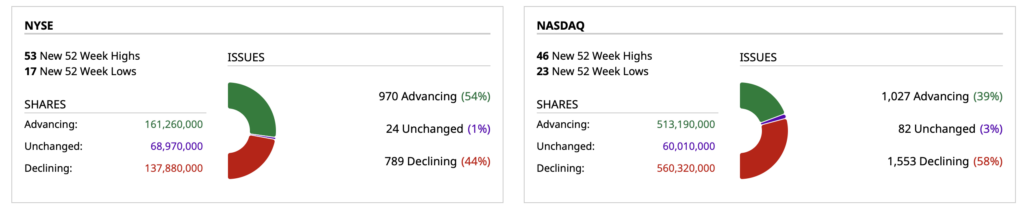

– NYSE volume 2% above its one-month average

– NASDAQ volume flat to its one-month average

– VIX index: down 1.62% to 15.79

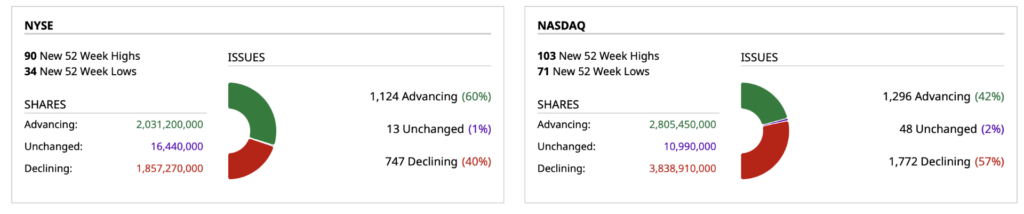

Breadth

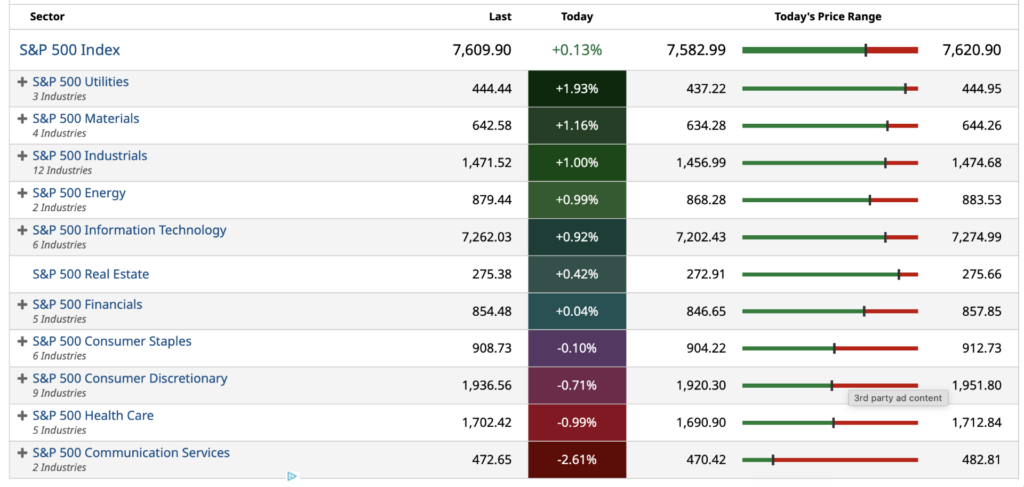

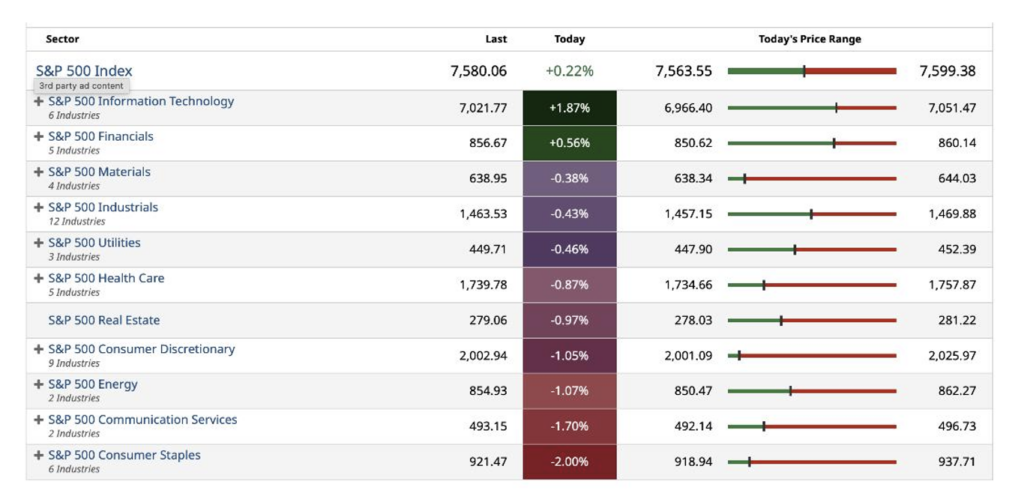

S&P 500 Sectors

% Movers

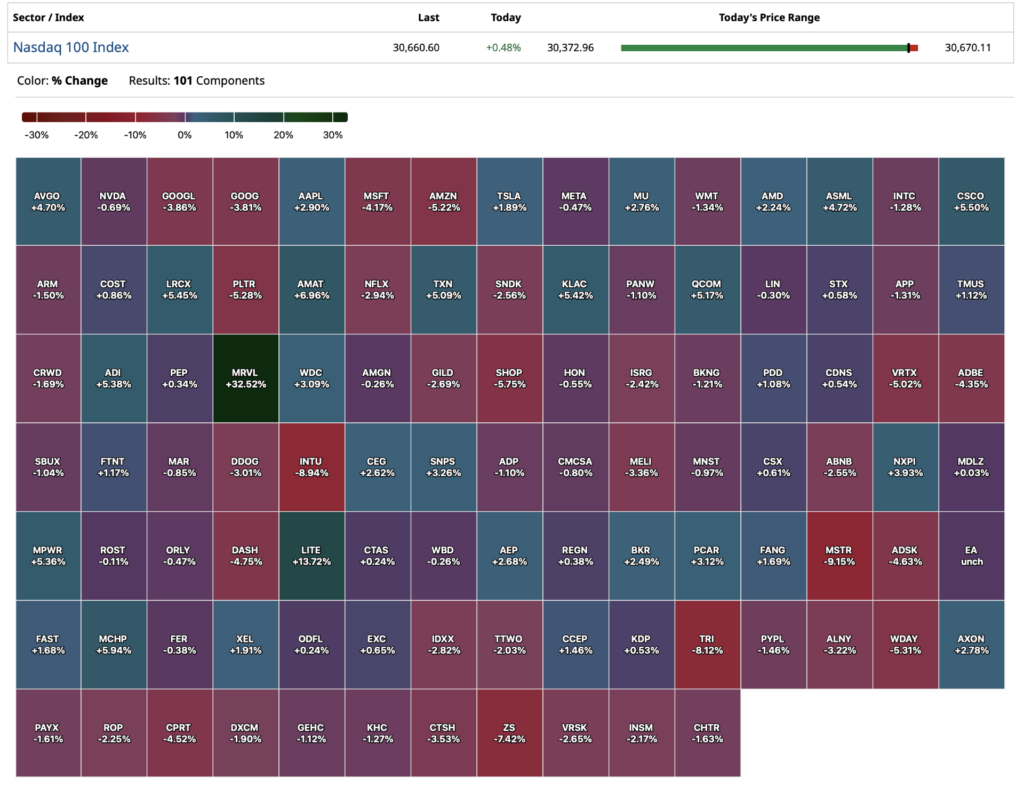

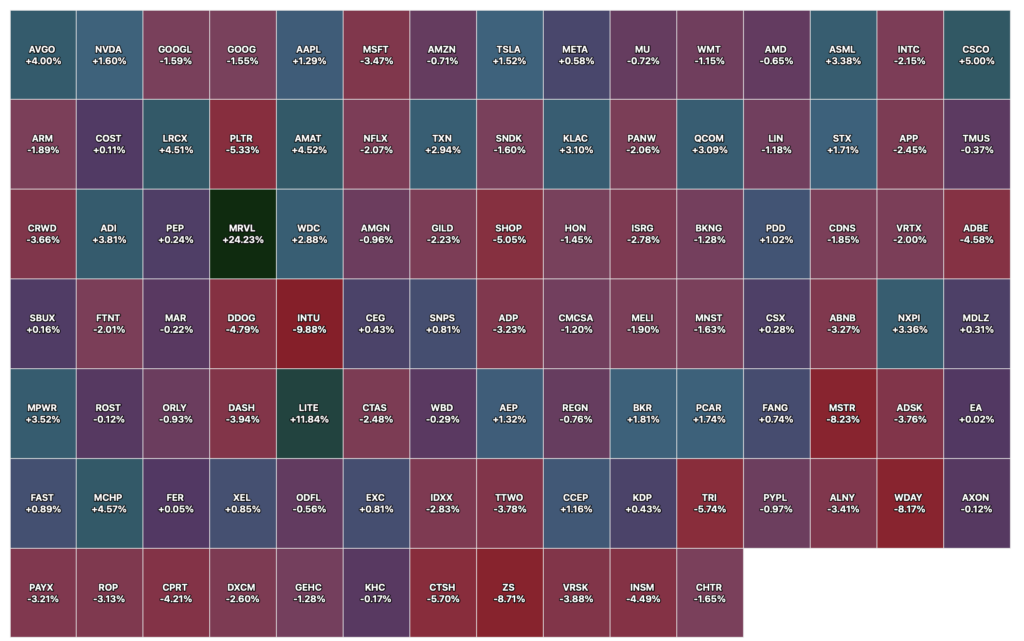

Nasdaq 100 Heat Map

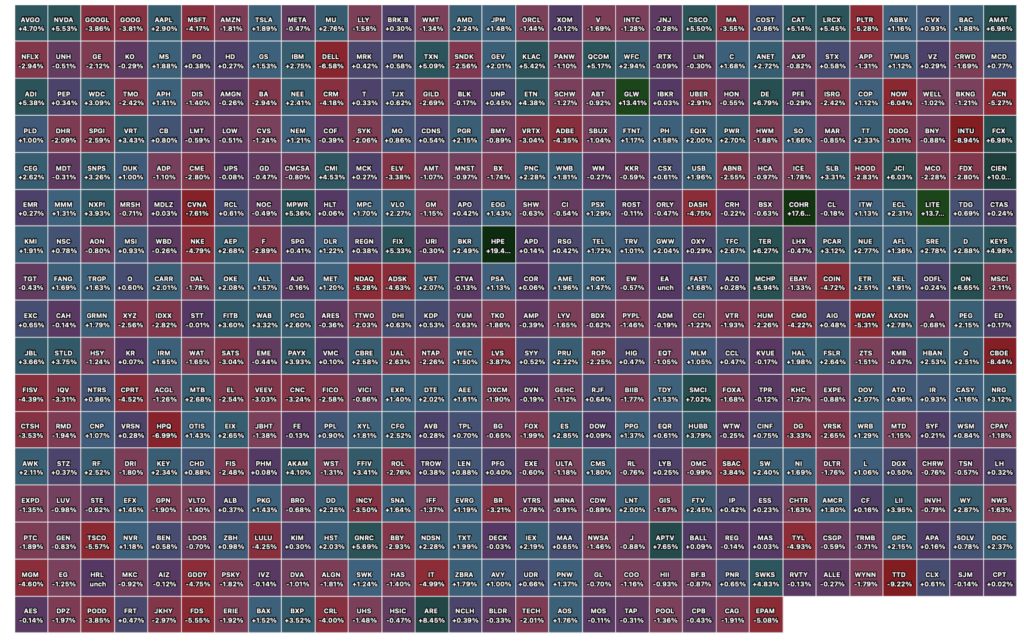

Closing S&P 500 Heat Map

Position: None

BY Doug Kass · Jun 2, 2026, 4:27 PM EDT

Verano Holdings (VRNO) management is on the Trade to Black podcast from The Dales Report.

Position: Long VRNO (M)

BY Doug Kass · Jun 2, 2026, 4:19 PM EDT

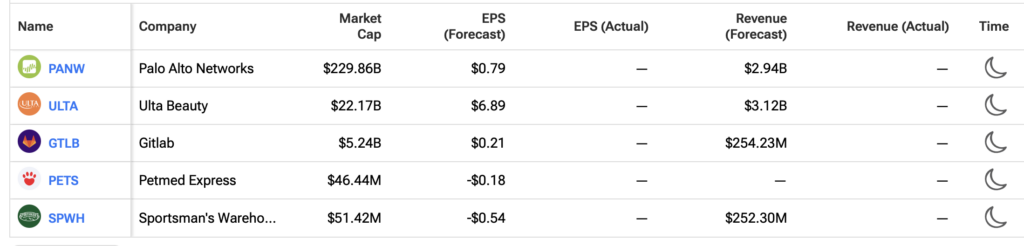

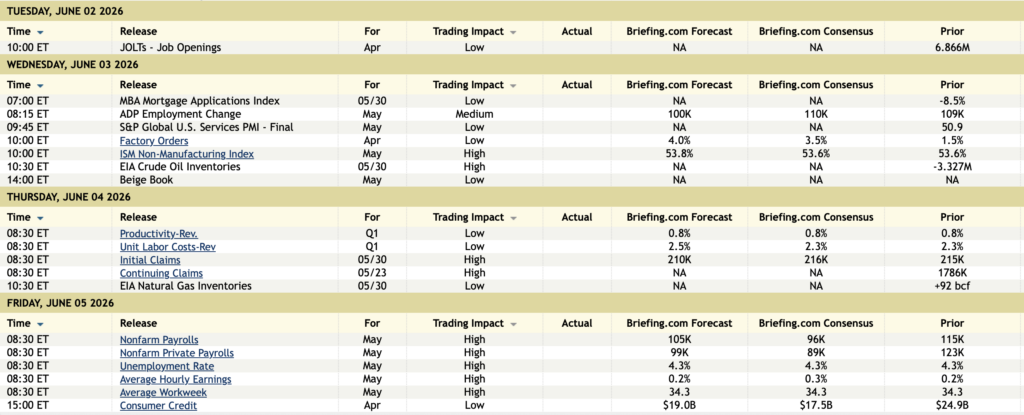

Earnings Calendar After the Close Tuesday, June 2

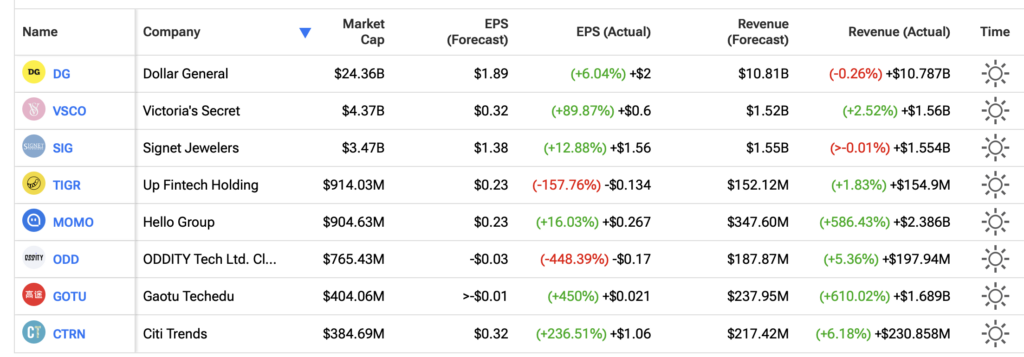

Earnings Calendar Before the Open Wednesday, June 3

Position: None

BY Doug Kass · Jun 2, 2026, 3:45 PM EDT

Position: None

BY Doug Kass · Jun 2, 2026, 2:40 PM EDT

* A Key Observation

“Maybe not today, maybe not tomorrow, but soon and for the rest of your life.”

– Casablanca (Rick telling Ilsa why she has to board the plane)

Everyone is playing the same game on the long side (AI).

* The Likely Memeification of Cannabis Stocks

“I never make plans that far ahead.”

– Casablanca (Rick’s response when Ilsa asks, “Will I see you tonight?”)

The animal spirits are on overload.

Market participants are grabbing at anything AI, space, memory, semis, etc. Parabolic moves have become common place. In the extreme, Jensen Huang mentions Marvell (MRVL) favorably and the shares rally by nearly +$70.

With the likely rescheduling of weed, likely uplistings (on major U.S. exchanges), settling of custody issues and emergence of institutional buyers (unleashing an abundance of buying power), I am increasingly of the camp that cannabis stocks could be memeified with such powerful changes ahead in the reasonably near term.

I add daily to VRNO — my favorite on a risk/reward basis.

Position: Long MSOS (VS), TSNDF (S), GTBIF (VS), TCNNF (VS), GLASF (S), CURLF (VS) VRNO (M)

BY Doug Kass · Jun 2, 2026, 2:30 PM EDT

It has been 15 years since my friend, CNBC’s Mark Haines passed away.

Here is a repost of my tribute to him written a few years ago.

I wanted to end today’s posts by paying homage to someone we lost this week, nine years ago: CNBC’s Mark Haines.

CNBC’s Mark Haines passed away on May 24, 2011.

I still miss him. His death was a great loss to his family, friends and CNBC.

I probably guest hosted Squawk Box with Mark on over 35 to 45 occasions from 2003 to the time of his death (in those days guest hosts were allotted a full three hours).

Here is a column I wrote on the fifth anniversary of Mark’s death — check out the great video of the match race I had with him at The Meadowlands Racetrack(!): https://www.cnbc.com/video/2011/05/25/fast-money-tribute-mark-haines.html

But it’s just a box of rain, It’s just a box of rain,

I don’t know who put it there.

Believe it if you need it,

Or leave it if you dare.

Or a ribbon for your hair.

Such a long long time to be gone,

And a short time to be there.

— The Grateful Dead, Box of Rain

My friend Mark Haines of CNBC passed away five years ago today, and it still stings.

I appeared via telephone on CNBC’s Fast Money with Mel and the gang shortly after Mark’s death and offered my teary-eyed thoughts, which I wanted to share with everyone again this morning.

Below is what I wrote about Mark upon his death five years ago:

“I have known Mark for about eight years, starting when I began to guest-host Squawk Box with him, Joe and David in 2003.

A lot has been said this morning on CNBC about Mark — his broadcasting techniques and strengths, as well has his personal idiosyncrasies.

What I most remembered about Mark was his strength of broadcasting during a crisis — whether it was a financial, geopolitical or social crisis.

But today, I will write about something this morning that most don’t know — his hobby was betting on thoroughbred horses. And for many years, he was proud to tell me that he had computerized the entire Hialeah Racetrack’s meet.

His favorite page in the newspaper wasn’t the business section. His favorite page was the racetrack entries at Aqueduct, Belmont, Saratoga, Gulfstream and Hialeah in the New York Post and Daily News. And, again, what few know, is that during commercial breaks he could be seen handicapping the horse races.

My fondest memory and funniest story about Mark Haines was about six years ago during a guest-host gig I had on Squawk Box. It was the week of the Hambletonian race at the Meadowlands racetrack (the harness-racing equivalent of the Kentucky Derby).

Two days before I was on Squawk, CNBC taped a match race between Mark and myself at The Meadowlands. https://www.cnbc.com/video/2011/05/25/fast-money-tribute-mark-haines.html Mark had never driven a standardbred, but he loved the racetrack and said to me, ‘What the heck, I will take a shot.’

I had so much fun in that race. (I beat him by a nose!) And after we went over the finish line, I asked him did he have fun, too?

Mark’s reply: “Dougie, I would rather put a needle in my eye than do this again.”

That was Mark — ever so honest and truthful.

Here’s a 2011 clip of Carl Quintanilla announcing Mark’s death on CNBC.

R.I.P. my friend.

Position: None

BY Doug Kass · Jun 2, 2026, 2:20 PM EDT

Wolf Street howls about the labor data.

Position: None

BY Doug Kass · Jun 2, 2026, 1:58 PM EDT

From Peter Boockvar:

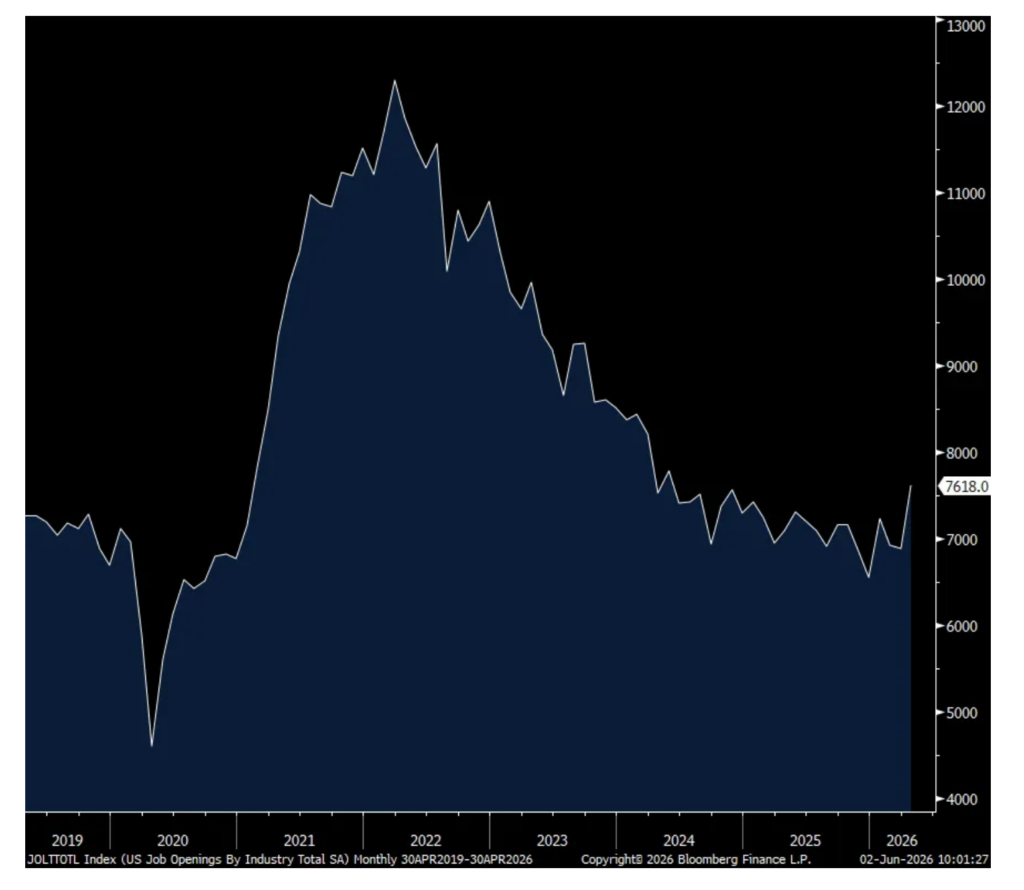

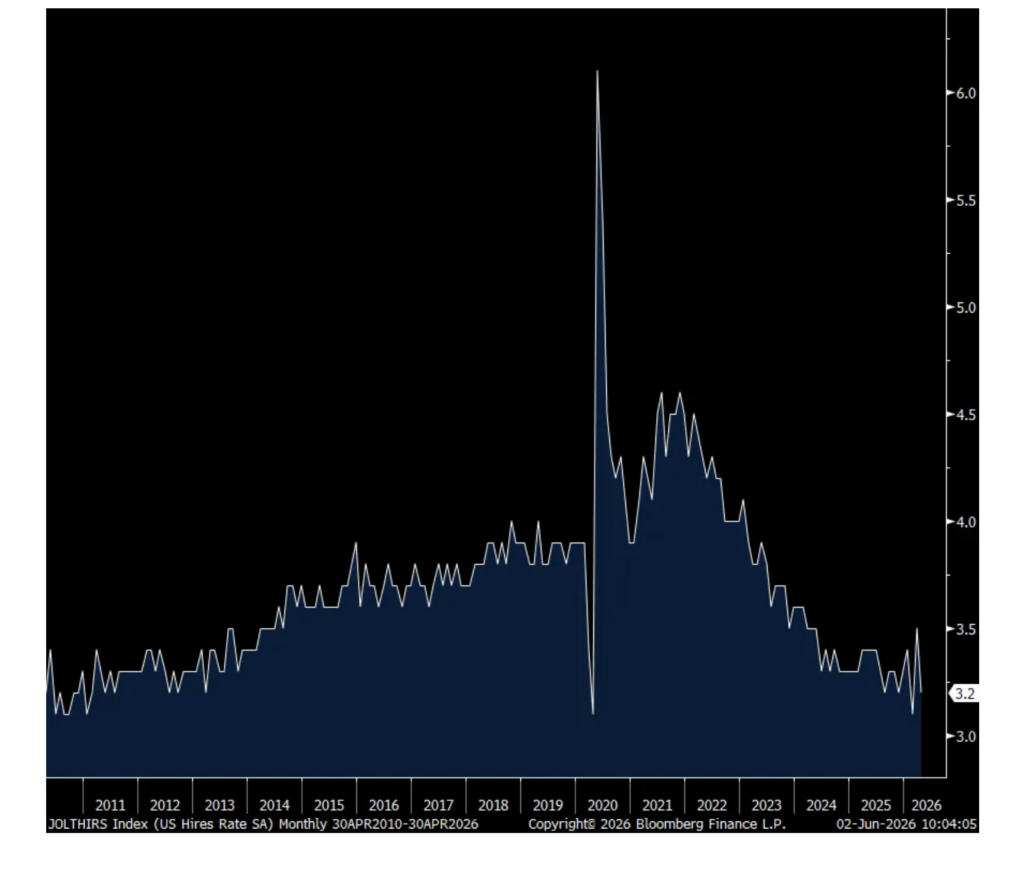

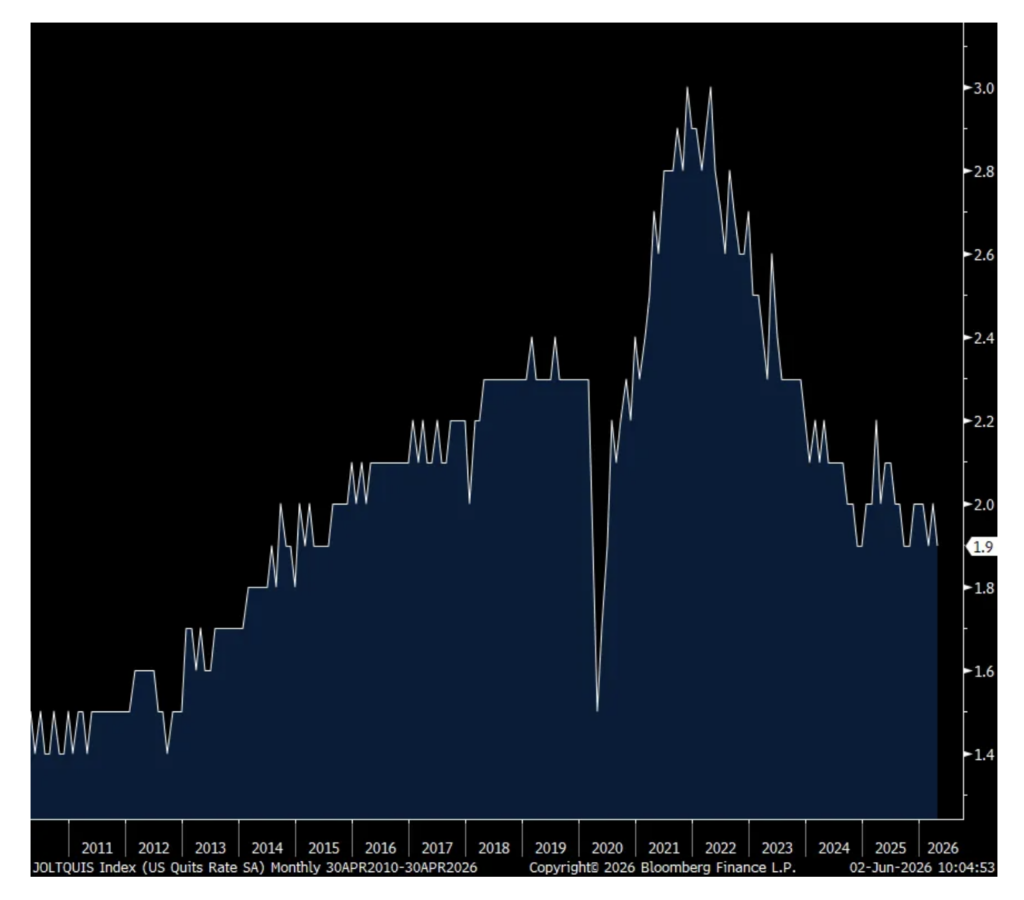

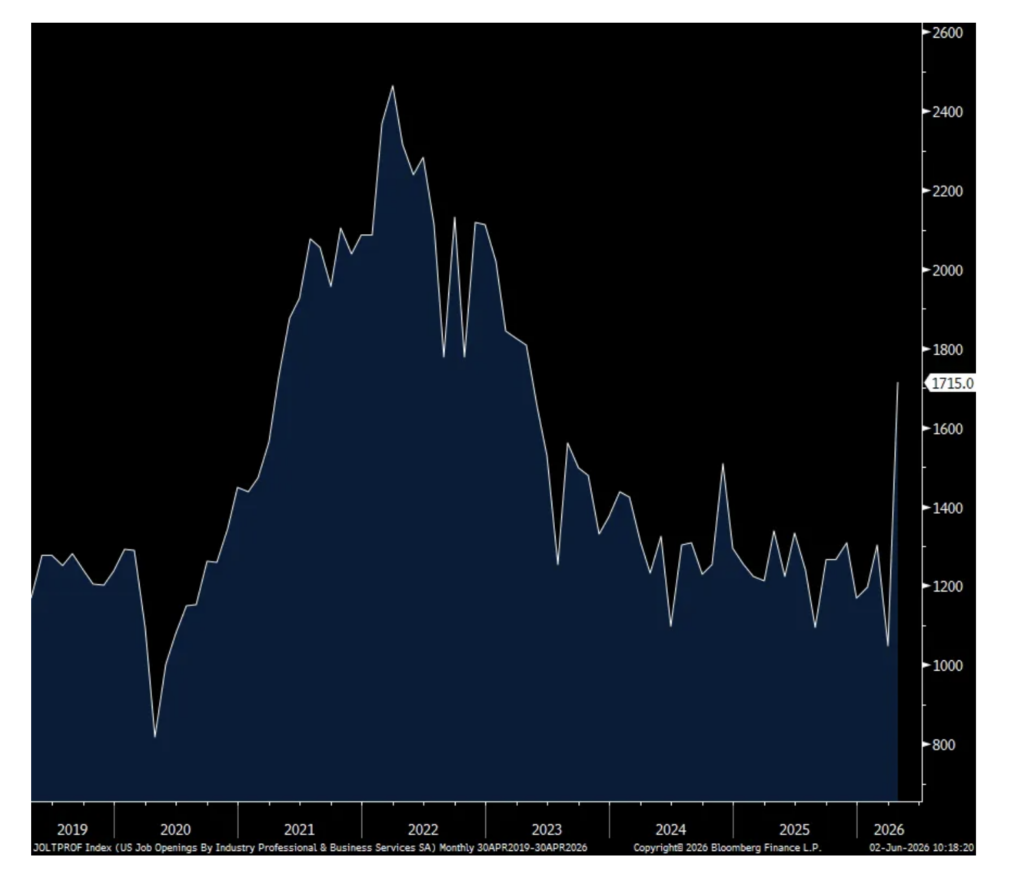

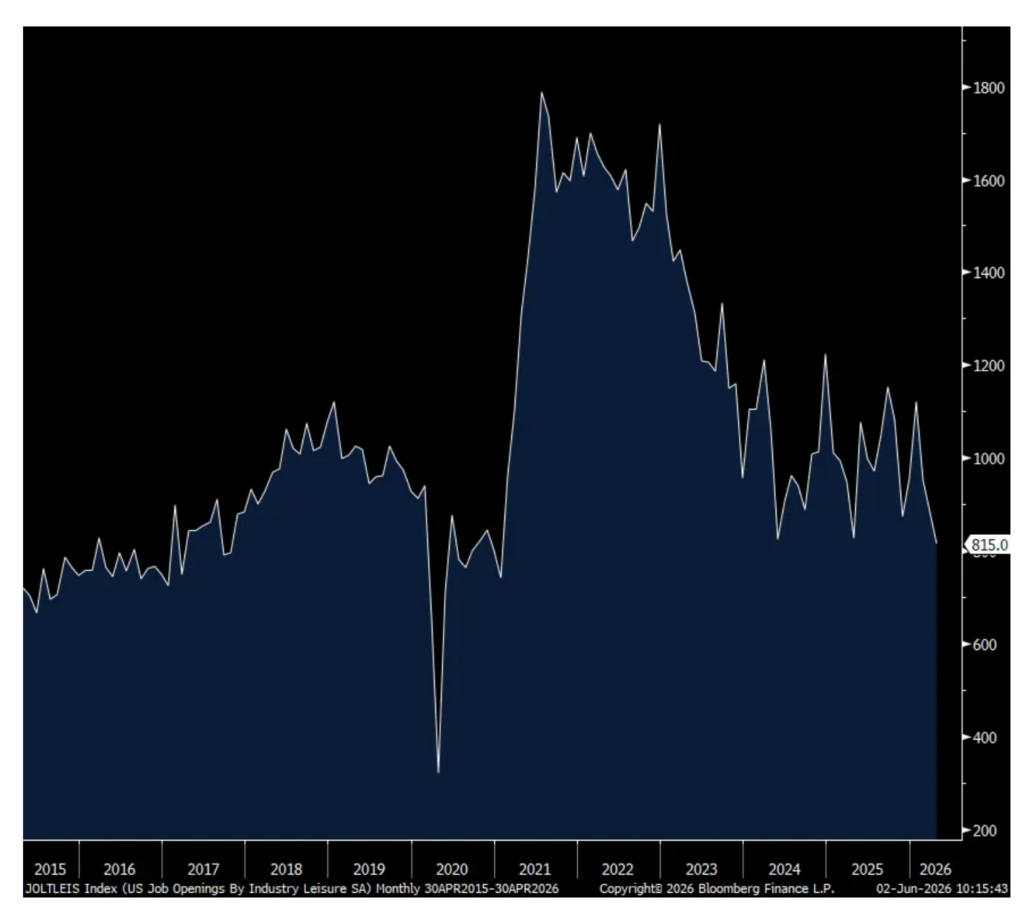

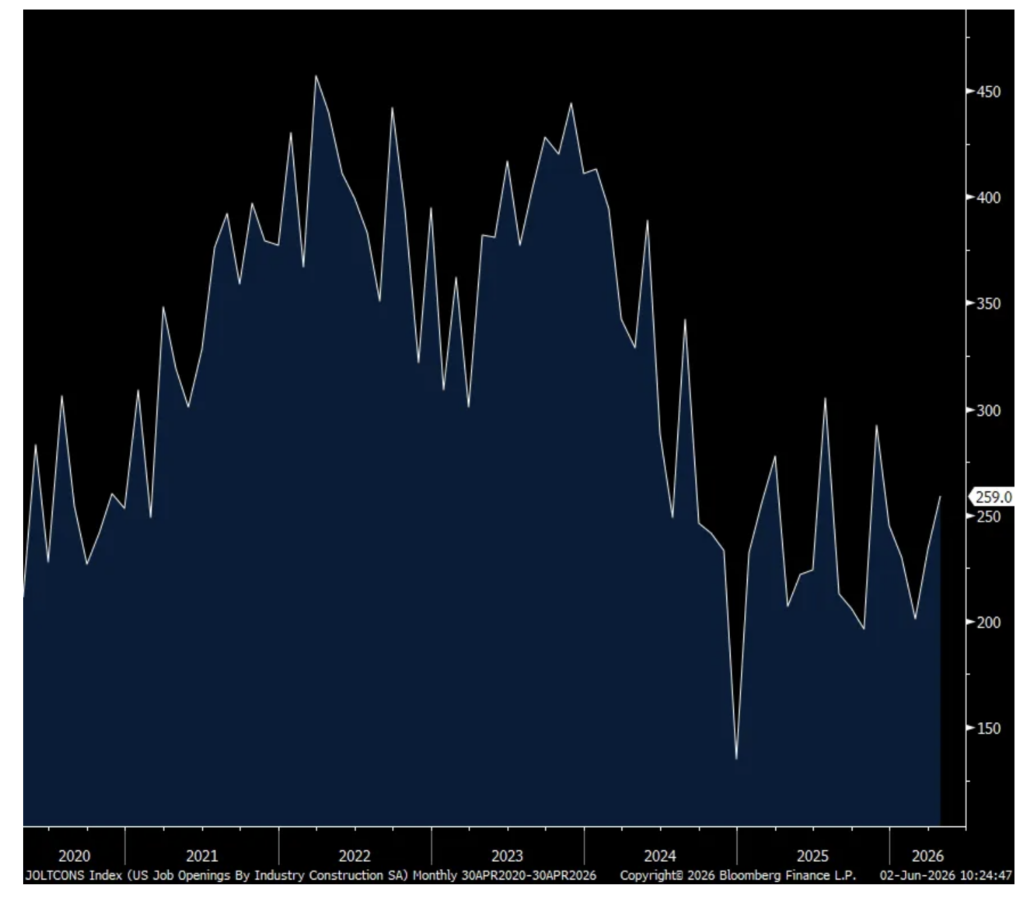

The number of job openings in April jumped to 7.618mm, an increase of 752k from March and to the most since May 2024. The hiring rate though fell back to 3.2% after rising to 3.5% in March vs 3.1% in February. Outside of Covid, 3.1% was the lowest since 2011 for perspective. The quit rate fell to 1.9% which matches the smallest print since 2014, also not including Covid.

Just about all of the increase in job openings came from just the ‘professional/business services’ line item which spiked by 668k. I wish I had more detail of what this consists of specifically outside of the typical white collar desk job. Healthcare/social assistance also helped, rising by 89k. Construction openings as well as manufacturing rose a touch. Trade/transportation, which includes retail/wholesale trade, was little changed. Leisure and hospitality openings fell to the lowest since 2017 not including the 2020 and 2021 Covid distortions. Job openings in finance/insurance totaled 300k vs 435k in March and 330k in February.

Bottom line, that rise in ‘professional and business services’ accounts for just about all of the rise in job openings and maybe AI won’t be taking everyone’s white collar jobs after all? That said, the hiring rate remains muted as does the quit rate, all getting to a still mixed but strange labor market when we look at both hiring’s and firing’s.

Job Openings

Hiring Rate

Quit Rate

Professional/Business Services job openings

Leisure/hospitality job openings

Construction job openings

Positions: None.

BY Doug Kass · Jun 2, 2026, 12:30 PM EDT

* Market risks are greatly under appreciated in the current ‘Bull Market in Complacency’

* By my calculus there is 3-times or more downside than upside presently

Equities, contrary to our expectations, continued to ramp higher during the last month.

The last several weeks have felt like a battle in which I have felt much like the Greek mythological character Sisyphus who was punished by the gods for cheating death and who was condemned to eternally roll a boulder up a hill, only for it to roll back down each time. While the myth symbolizes the endless struggle and futility of human efforts, this morning’s opening missive incorporates what I believe to be a deteriorating fundamental economic and corporate profit proposition on top of stretched valuations – making me feel more like Elpis (the goddess of hope) than Sisyphus as I have growing confidence that my market expectations might be soon realized.

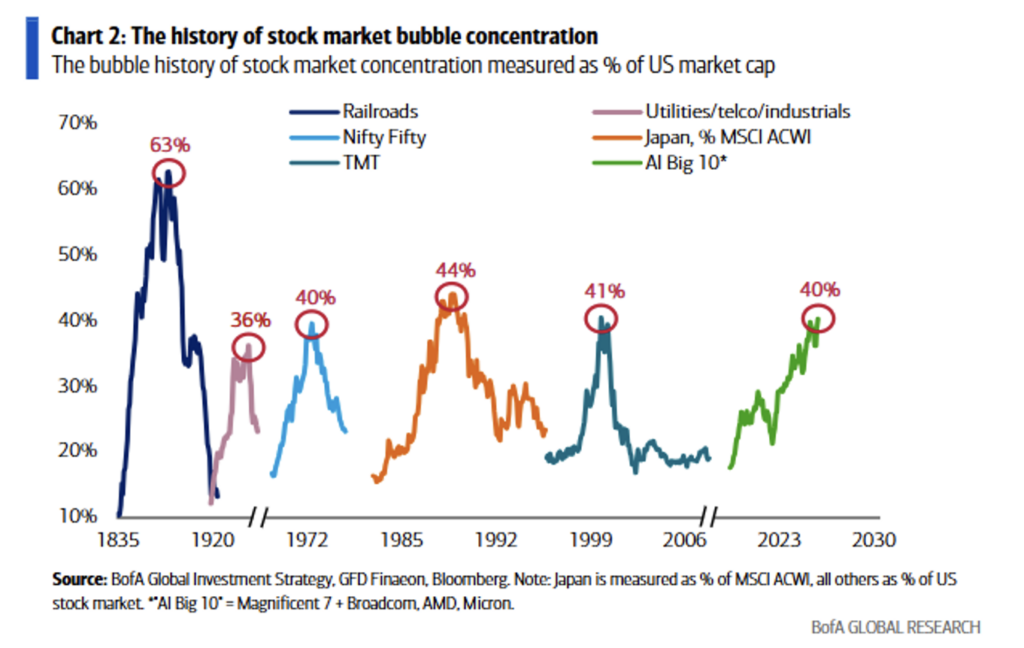

For the second month in a row, it was All Ai All The Time, with large-cap technology the dominant contributor to the market’s rise. Only ten companies contributed to 2/3 of the overall rally over the last eight weeks. (See our comments about the foul market breadth later in this commentary)

We have not seen a stock market this concentrated around a single theme in 150 years:

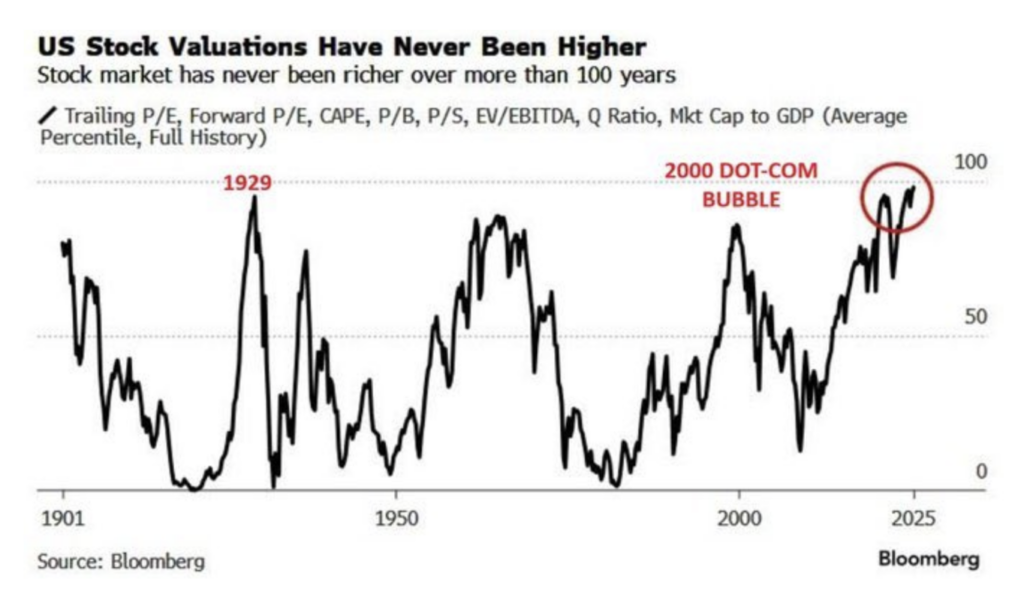

As the S&P Index made a new high last week, only 21 stocks also made record highs. By comparison, only 20 stocks made new highs at the March 2000 top. Beyond the aforementioned concentration levels, there has never been a more expensive market in history:

For these reasons and others, I continue to maintain a cautious investing posture in my investment partnership — sitting in a net short exposure.

As subscribers are aware, I have been defensively positioned for some time, in the belief that the reward vs. risk setup was unattractive. With the exception of the brief market dips in 2024 (April), 2025 (February) and 2026 (March) I have maintained my net short exposure. Disappointingly, that strategy did not allow us to take advantage of the opportunity set provided by the market advance over the last two years, which was a period in which caution became the most expensive position on Wall Street.

Despite the net short exposure and a wrong-footed investment view, on a positive note, through a combination of opportunistic trading, good risk control/management and some excellent shorts — we have had a long streak of positive monthly investment performance.

To me, the current AI-driven equity rally increasingly resembles a late-stage speculative bubble: extremely narrow market leadership, stretched valuations (in the 97% percentile), euphoric positioning (and absence of fear), collapsing volatility, massive IPO supply ahead and, of course, excessive concentration in mega-cap tech. Central banks still remain too loose globally, which is prolonging the bubble, but once policy tightening meaningfully bites, the unwind could resemble prior post-bubble rotations (with the historical analogs a combination of 1929, Japan 1989, Dotcom 2000 and China 2007 and The Great Recession (2008-09)).

As noted, I am increasingly confident that my concerns will be reflected in lower stock prices and in today’s commentary I will discuss the equity risk discount, a foundational part of my ursine market outlook.

An increasingly slender sector participation underscores the market’s narrowing leadership, as last Friday’s action demonstrated:

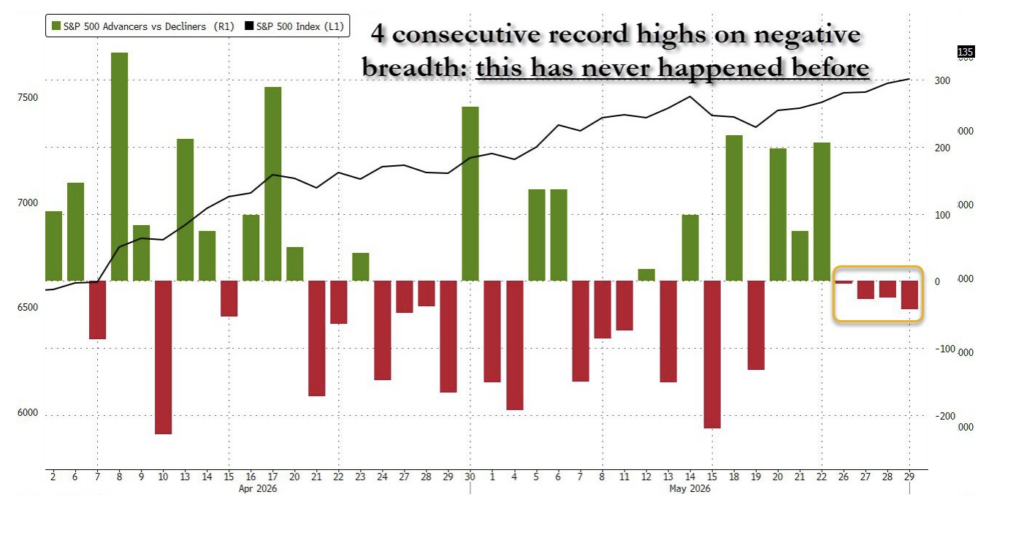

In this past week, the S&P has recorded four consecutive all-time highs while a majority of equities were actually falling. This has never happened before:

The S&P advance/decline line hasn’t made a new high since April 17, despite multiple all-time highs made by the Index. The last time we had such a divergence was November 2024 to February 2025 and that eventually led to a 20% drop:

Call me “old school,” but I continue to adhere to one of Bob Farrell’s 10 Lessons of Investing:

Lesson #7 Markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names.

Translation: Breadth is important. A rally on narrow breadth indicates limited participation and the chances of failure are above average. The market cannot continue to rally with just a few large-caps (generals) leading the way. Small- and mid-caps (troops) must also be on board to give the rally credibility. A rally that lifts all boats indicates far-reaching strength and increases the chances of further gains.

Last month I we wrote:

In our view, the markets have ignored the same conditions that set off the January-February selloff. None of the non-war issues that drove stocks lower have been resolved:

* Oil prices are off their highs but are likely to remain elevated because of the magnitude of the supply shock and continued uncertainties related to the Iran conflict.

* Inflation is now rising on a sequential monthly basis – and is higher than before the conflict in Iran.

* Interest rates will be higher for longer.

* The 2026 annual deficit will approach $2 trillion, neither political party show any signs of being fiscally responsible.

* The U.S. debt will hit $40 trillion this year – the cost of servicing the debt is over $1 trillion/year.

* With a burgeoning deficit, stiff debt load and persistent inflation, the Fed’s hands are tied.

* While private equity’s problems are not systemic, the leverage they brought us remains in place. KKR Private-Credit Fund Takes $560 Million Loss – WSJ

* The enormous amount of money spent on AI will probably never see an adequate return on investment. As noted by Stan Druckenmiller (again!), AI’s societal and transformative impact could rival the internet’s life-changing influence – and so may the stock market consequences (rhyme) be similar:

“If we were all sitting here in 1999 talking about the Internet, I don’t think anybody would have estimated it would be as big as it got in 20 years. And yet, if you bought the Nasdaq in ’99, it went down 80% before that all came to fruition. That’s not going to happen with AI. But it could rhyme – AI could rhyme with the Internet as we go through all this capital spending we need to do. The big payoff might be four to five years from now. So AI might be a little overhyped now but under-hyped long term.”

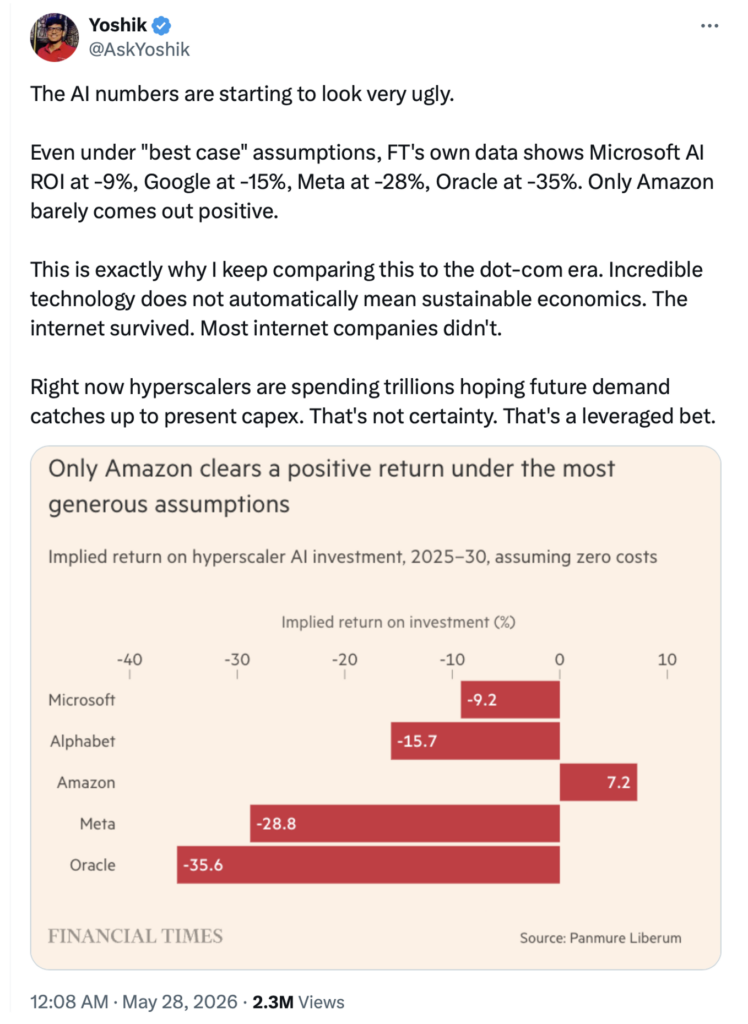

With 45% of the S&P Market Cap AI or AI-adjacent, What if the AI boom… goes in reverse? Panmure Liberum – Strategy

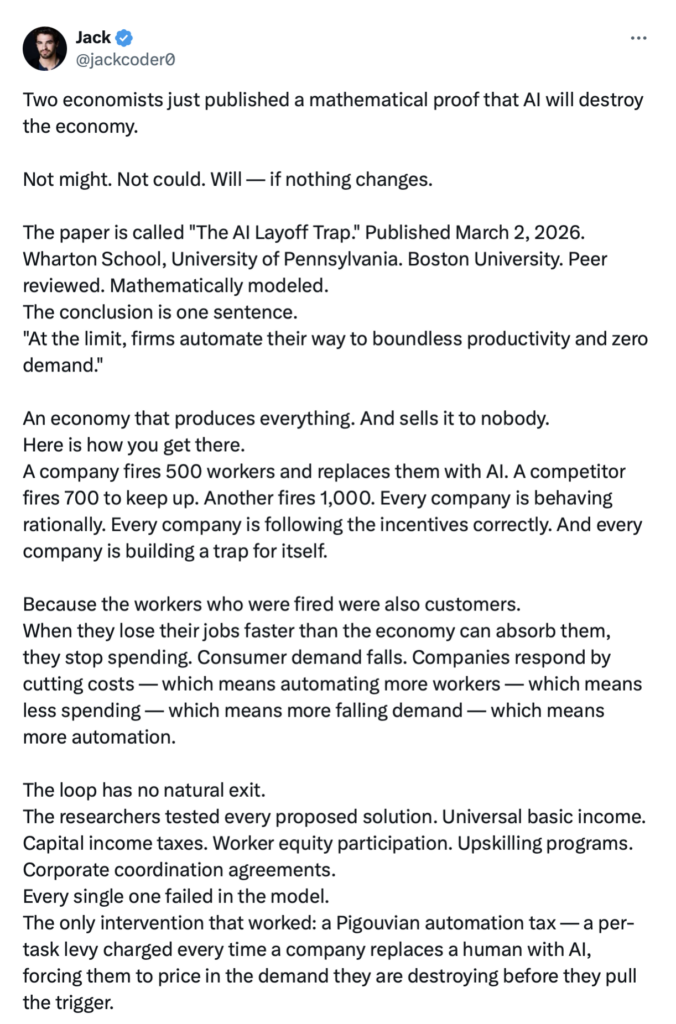

Or even worse, what happens if, at the limit (as two professors have recently written) companies “automate themselves to boundless productivity and zero demand – an economy that produces everything and sells it to nobody:

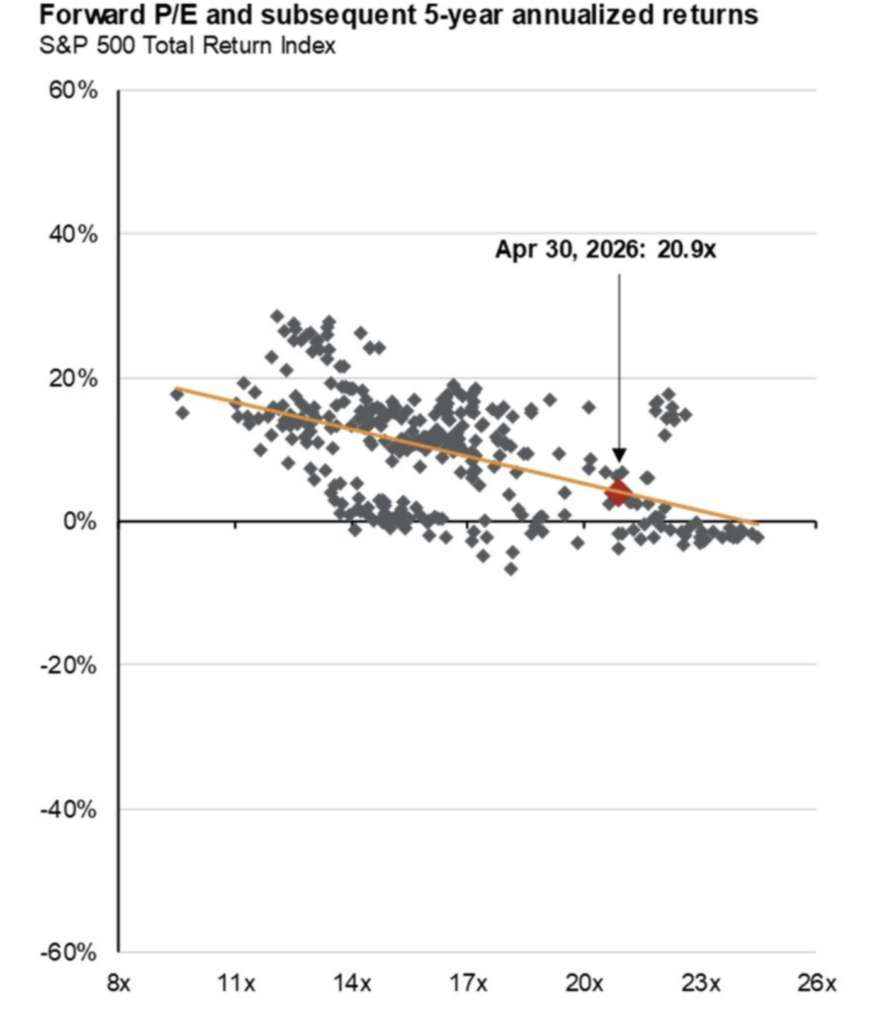

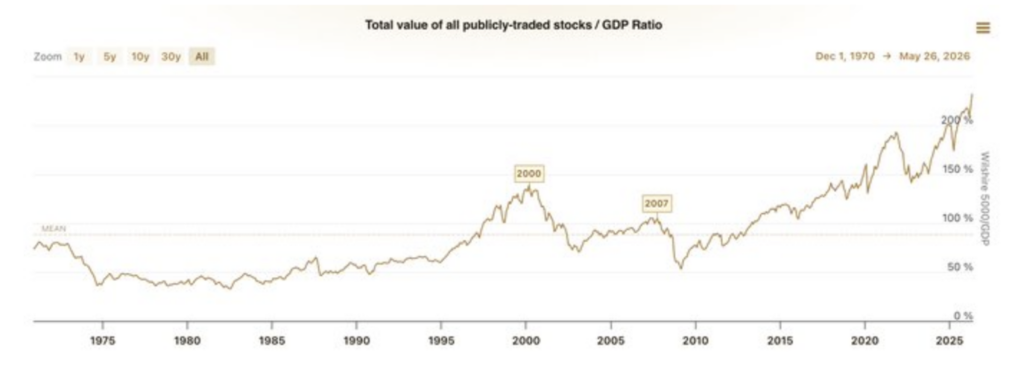

* Valuations are a terrible clock but a good weather forecast. That valuations are stretched is an understatement. See Cape Shiller above. The Buffett ratio (the total market capitalization divided by GDP) hit an all-time high this week). Most other traditional metrics indicate that equity valuations are in the 97 percentile.

* Many bulls highlight the improving strength in projected 2026 S&P EPS. They argue that this year’s robust growth in profits (at about +17%) – justify current valuations. However, if one takes out Nvidia (NVDA) and Micron (MU), 2026 S&P EPS growth falls to under +10%:

I am increasingly confident that our concerns (are multiplying and intensifying) will be reflected in lower stock prices and in today’s commentary, I will discuss one factor, the equity risk premium (now a discount), which incorporates some of the foundation of our ursine market outlook.

To borrow a phrase from Warren Buffett, the voting machine is overwhelming the weighing machine.

For nearly three years, the markets and its participants have ignored elevated valuations.

How much longer can the S&P 500 and the other major indices deliver upside when price-earnings multiples and equity risk premiums are in the 95th percentile or higher?

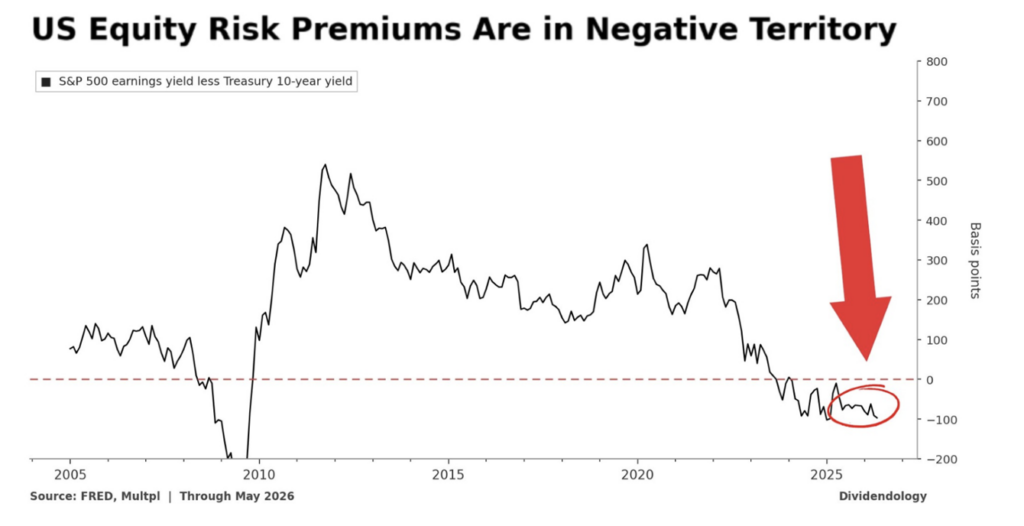

With consensus (I think overly optimistic!) 2026 S&P EPS at $330/share, the senior average trades at 23x and the equity risk premium is negative.

On projected 2027 S&P EPS consensus of $375/share (I think overly optimistic as well) the S&P trades at 20.5x and the equity risk premium is only at 50 basis points, both in the 93rd percentile.

The steady decline in the equity risk premium is a metric I pay very close because. Historically, it has been an excellent indicator future investment returns…

My focus on the ERP has contributed importantly to my incorrect market view and a missed opportunity set on the long side.

Let’s examine the equity risk premium, which is the difference between the S&P earnings yield (the inverse of the P/E ratio) and the risk-free rate (the 10-year Treasury note yield is typically used):

The equity risk premium tells us how much excess return investors are being paid to own stocks over a risk free Treasury bond.

Historically, equities typically offer a three-to-four percent premium over Treasuries. Such a premium makes sense because it compensates investors for volatility, drawdowns and uncertainty.

Right now, according to the chart above, the investor is being paid negative in equities vis a vis bonds. The ratio is saying that holding bonds is more risky than owning stocks — this is a radical notion, at an extreme! Again, this means:

1. Investors are not being paid extra to take on risk in stocks.

2. Stocks are offering similar or worse “yield” than bonds.

3. Valuations are materially stretched relative to interest rates.

Stated simply, this means that holders of equities are taking more risk for less reward (than bonds). When this has happened in the past (most notably during the dot-com bubble and leading up to The Great Recession in 2007-09), forward returns have been somewhere between non-existent and negative:

“What we learn from history is that we do not learn from history.”

– Benjamin Disraeli

As noted earlier in this opener and based on historical metrics, there has never been a more overvalued market in history.

It is hard to understand why stocks have been impervious to elevated valuations (a record high in overvaluation in both the Buffett Indicator and a near record in Shiller’s CAPE ratio), as well as an equity risk discount. As an example, the Buffett Indicator (the total value of all publicly traded stocks divided by GDP) is at 236%, making this the most expensive stock market in history:

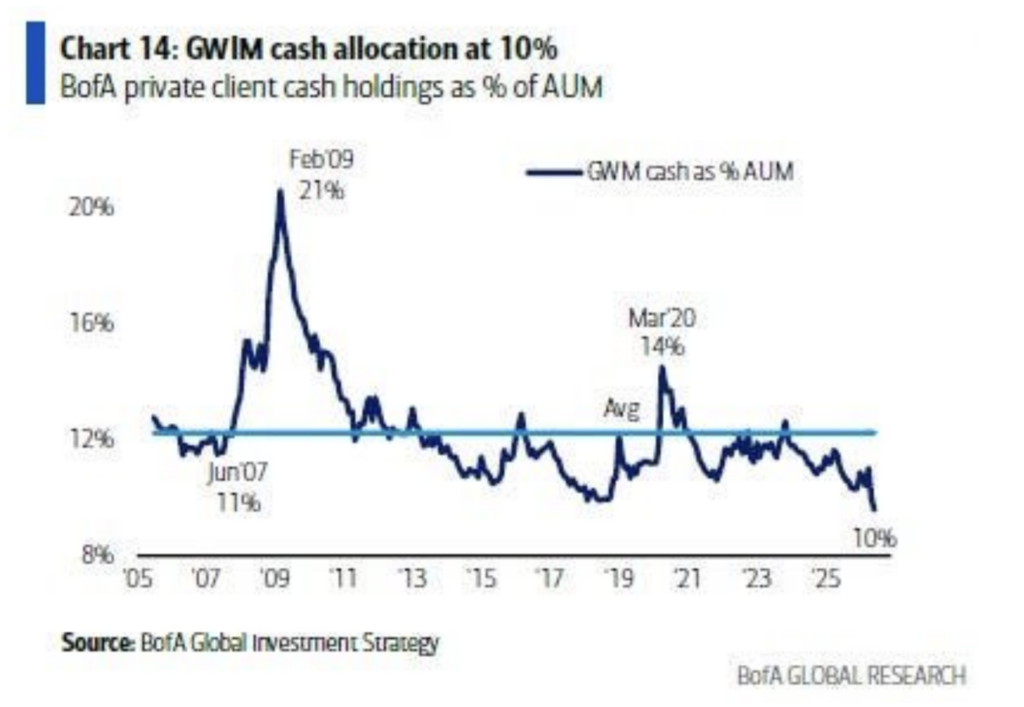

Investors are euphoric – BankAmerica’s private wealth clients hold the lowest amount of cash in two decades):

The market has become a casino – with more ETFs (many of them 2x leveraged) listed on the New York Stock Exchange than individual securities. ODTE (zero-day to expiration options) account for about 70% of total option activity.

Speculation is running amok:

Moreover, the markets are growing increasingly synthetic:

One answer for the recent market momentum is the dominance of passive products and strategies that worship at the altar of price. They know everything about price and nothing about value.

Other explanations are the euphoria in AI and the fear of missing out (FOMO).

Nonetheless, excessive valuations, excesses and the idea of a “new era” are nothing new — we have seen these at the top of other cycles (for reasons of overenthusiasm/heated speculation).

Finally, it is my strong view that the components of the equity risk premium suggest, at the very least, a mean reversion back towards the historical premium as 2027 EPS estimates come down and interest rates likely rise.

Let’s not forget when Berkshire Hathaway’s shares were suffering in late 1999 and many were questioning Warren Buffett’s investing philosophy (as they are currently with his near $400 billion cash hoard) — right before a more than -80% drawdown in the Nasdaq.

To me, it’s not different this time.

I continue to choose the weighing machine over the voting machine.

Positions: None.

BY Doug Kass · Jun 2, 2026, 11:30 AM EDT

“The next trillion dollar company, Ladies and Gentlemen…”

* Jensen Huang on Marvell Technology

Positions: None.

BY Doug Kass · Jun 2, 2026, 11:05 AM EDT

– NYSE volume 10% above its one-month average;

– Nasdaq volume 5% below its one-month average;

– VIX index: up 0.19% to 16.08

Positions: None.

BY Doug Kass · Jun 2, 2026, 11:02 AM EDT

From Peter Boockvar:

The data center buildout is keeping the US economy afloat, its beneficiaries are continuously taking the stock market to new highs, and the technological advancements are exciting but we are being reminded again how expensive and capital heavy it all is, especially for the major hyperscaler spenders.

Google/Alphabet seems to have all the building blocks to monetize its development of Gemini and further grow its cloud business but it sure is costly. This company generated about $73 billion of free cash flow in both 2024 and 2025, bought back $62 billion of stock in 2024 and $46 billion in 2025 and spent $52.5 billion on CapEx in 2024 and $91.4 billion in 2025. Now, they are raising $80 billion of equity, just the second equity raise since it went public in 2004, as they sold some shares in 2005, as they need help financing $186 billion of expected CapEx in 2026 and almost $250 billion forecasted for 2027 and as their free cash flow is expected to decline this year to ‘just’ $21 billion and $16 billion expected in 2027. Back in February, they raised $32 billion in debt sales which as of 3/31/26 took their long term debt to $90.5 billion when including lease liabilities, that is up from $22.5 billion on 3/31/25. Asset light no longer.

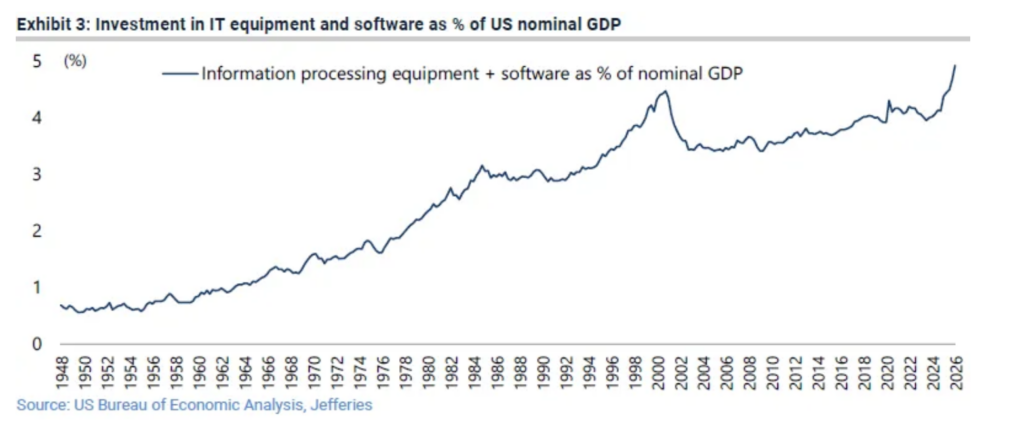

Further quantifying all the CapEx on the data center buildout, Chris Wood at Jefferies had this chart last week which dates back to post WWII. It speaks for itself the size at which companies are investing. None of this is to say it all doesn’t work out from a monetizable perspective for the builders and the technological wonders for its users, aka, the rest of us, but just to highlight, again, the ever-rising costs of it and its current tremendous economic contribution.

Competing with Dell, HP Enterprise reported a blowout quarter too and its stock is responding in kind to the upside. They said of note:

“Demand was even stronger than revenue growth. Orders more than doubled, significantly outpacing revenue, resulting in a record company backlog. Customer investments in agentic AI and AI inferencing accelerated. We also saw broad based demand strength across the portfolio, driven by ongoing investment in compute infrastructure modernization, unstructured storage data growth, and private cloud adoption for AI.”

“Sequentially, revenue grew 15%, reflecting higher average selling prices within our server business, driven by ongoing DRAM and NAND inflationary costs and supply constraints. We continue to work with our partners to secure long-term agreements while executing the pricing actions we discussed last quarter.”

While Dell talked about seeing some pull forward of ordering, HP is saying they don’t. “And customers, when you think about budgets, obviously they are challenged because of the price increases we have seen driven by the cost of commodities. But I can tell you, we have not seen any pull-in. We don’t see a cliff. And in many ways, I think customers are prioritizing getting access to technology now faster than ever before because nobody wants to be left behind when it comes down to deploying AI.”

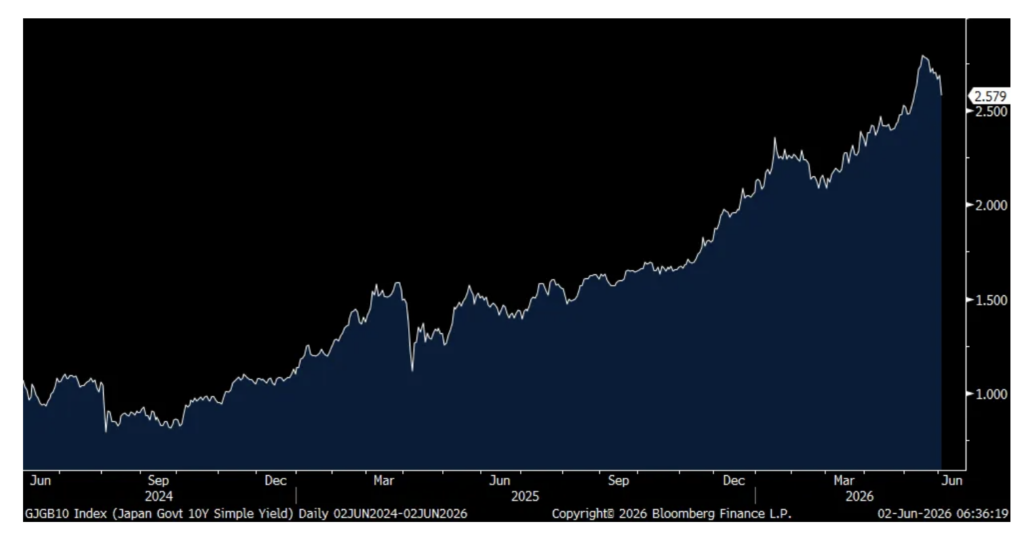

There was a big move lower in JGB yields overnight with the 10 yr in particular falling by 11 bps to 2.58% after a good 10 yr auction was conducted. The bid to cover of 3.53 was well above the previous 12 month average of 3.35, though down from 3.90 in May. With the yen back to 160 vs the US dollar, we watch to see if this market test will trigger another round of Japanese government intervention. I think all they need is another rate hike in a few weeks but we’ll see if it happens or not.

South Korean bonds rallied too even after they reported May CPI that rose 3.1% headline y/o/y, two tenths more than expected and a core rate gain of 2.5% which was 3 tenths above the estimate.

10 yr JGB Yield

After seeing individual European country inflation stats over the past few trading days, the May Eurozone CPI was higher by 3.2% y/o/y and 2.5% at the core. The headline was as forecasted but the core rate was one tenth above and both compare with 3% and 2.2% in April. Of note, services inflation accelerated to a 3.5% y/o/y increase, matching the quickest since April 2025 while non-energy industrial goods prices rose .9% y/o/y, still benign but that is the fastest rate of change since Q1 2024. As the data was basically as expected and we saw the big JGB yield drop, European sovereign bonds are rallying across the board with yields lower which in turn is helping US Treasuries with yields down. The ECB is expected to raise rates this month as REAL rates are now well negative.

Eurozone CPI y/o/y

Positions: None.

BY Doug Kass · Jun 2, 2026, 10:53 AM EDT

With S&P cash -9 handles I am adding to Index, (GRNY) and (JOET) shorts.

Positions: Short SPY M QQQ M GRNY M JOET S

BY Doug Kass · Jun 2, 2026, 10:04 AM EDT

Chart from 9:37 a.m. ET.

BY Doug Kass · Jun 2, 2026, 9:58 AM EDT

… a bit late, but still here:

-BJDX +165% (partners with Argonaut Manufacturing Services to support Symphony platform)

-VSXY +32% (earnings, guidance)

-HPE +29% (earnings, guidance; appoints Christopher Hsu of Elliott Investment Management to Board of Directors)

-MRVL +18% (Nvidia’s CEO says Marvell could be next to join $1T market cap club)

-CTRN +15% (earnings, guidance)

-CAMT +11% (receives $55M multi-system order and $50M+ Hawk system orders for 2027 delivery)

-GNRC +10% (signs global supply agreement with leading hyperscale data center operator to provide backup generators)

-STM +9.9% (raises data center revenue ambition; now about $1B in 2026 (prior nicely above $500M), could double in 2027 (prior well above $1B))

-MCHP +8.9% (Data center solutions unit revenue expected to grow 65% in 2026 to about $500M; Announces price increases)

-SIG +5.8% (earnings, guidance)

-DG +5.5% (earnings, guidance)

-SMCI +4.1% (showcases next gen AMD Helios rack-scale platform at Computex)

-TRIP +2.2% (Wedbush, Inc. Assumed TRIP with Outperform, price target: $19)

-HKIT -62% (raises $8M in registered direct offering of 4.0M shares at $2.00/shr)

-FULC -51% (discontinues pociredir for sickle cell disease; explores strategic alternatives)

-ABVX -36% (reports Phase 3 ABTECT maintenance trial data in ulcerative colitis)

-CELC -24% (reports detailed efficacy and safety results in PIK3CA MT cohort for Phase 3 VIKTORIA-1 gedatolisib regimens vs alpelisib plus fulvestrant)

-ODD -23% (earnings, guidance)

-XMTR -9.8% (prices previously announced $225M sale of 2.65M shares at $85/share)

-LPTH -9.4% (prices registered direct primary and secondary offering of Class A common stock; 7,142,800 shares at $14.00/share)

-NU -7.1% (appoints Rob Livingston CFO)

-SHAK -6.8% (cuts guidance)

-INTU -6.4% (Goldman Sachs Cuts INTU to Sell from Neutral, price target: $276 from $519)

-SNOW -3.6% (profit taking)

-CRDO -3.3% (earnings, guidance)

-GOOGL -2.8% (authorizes proposed $80B equity capital raise to expand AI infrastructure and compute)

Positions: None.

BY Doug Kass · Jun 2, 2026, 9:35 AM EDT

Jaw4860

15m ago

Doug ,You quote Marcus and others ,What are their track records ?

DDougie Kass

just now

they are research analysts not running portfolios

i believe, unlike some, that my job is to provide contrarian views/analysis – ergo gary marcus tweets/columns

others feel differently

bullish views dominate the markets (wall street, fin tv ,etc.), thoughtful outside of consensus, provides food for thought for investors and traders considering sectors and weighting those sectors

warren buffett has done poorly in the last 5-10 years vs the markets – so should i stop quoting him?

druckenmiller, the goat, is on a bad streak – should we stop listening to him?

lee is having a rough year – are his views worthwhile?

considering pros and cons, creating a ledger on ideas is reasonable

if we confided the dialogue and discourse to those who are right… well, that is sub optimal

BY Doug Kass · Jun 2, 2026, 9:35 AM EDT

Positions: None.

BY Doug Kass · Jun 2, 2026, 9:14 AM EDT

11:00 a.m.: Treasury Announces a 4, 8 and 17 Week Bill Auction;

11:00 a.m.: Treasury buyback announcement (liq support); 1

1:30 a.m.: Treasury hosts a $75B 6-Week Bill Auction

8:30 a.m.: Fed Bank of Cleveland President Hammack (Voter) gives remarks and participates in conversation on monetary policy co-hosted by the Cleveland Fed, the City Club of Cleveland, the Greater Cleveland Partnership, and the 50 Club of Cleveland, Cleveland, OH

Positions: None.

BY Doug Kass · Jun 2, 2026, 8:51 AM EDT

Positions: None.

BY Doug Kass · Jun 2, 2026, 8:39 AM EDT

Positions: None.

BY Doug Kass · Jun 2, 2026, 8:33 AM EDT

Position: None

BY Doug Kass · Jun 2, 2026, 7:45 AM EDT

Position: None

BY Doug Kass · Jun 2, 2026, 7:30 AM EDT

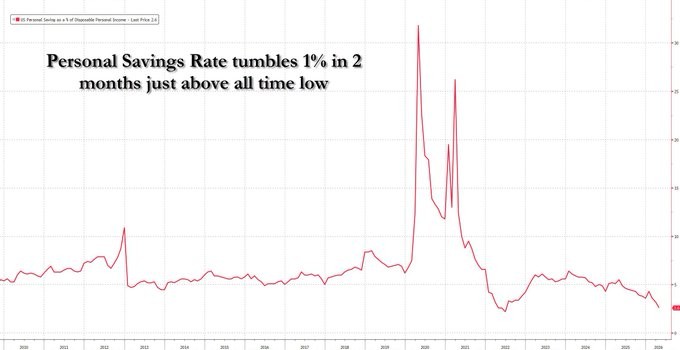

* The consumer is ‘spent up, not pent up’…

The same thing that has got into the shares of Walmart (just look at the sickly WMT chart) and other consumer staples — a weakening consumer.

The low-end and middle-end consumer has lived on borrowed time — the dwindling savings rate (now at about 2.6%%) suggests the consumer, plagued by a weak jobs market and an acceleration in the rate of inflation, is spent up and not pent up:

The consumer forms the core foundation of most banks.

While the K-shaped economy has buoyed the wealthy (with large balance sheets, invested in stocks and real estate) — a crack in equities could adversely impact the resilient and higher-end consumer.

Position: None

BY Doug Kass · Jun 2, 2026, 7:15 AM EDT

Position: None

BY Doug Kass · Jun 2, 2026, 7:05 AM EDT

Position: None

BY Doug Kass · Jun 2, 2026, 6:55 AM EDT

Position: None

BY Doug Kass · Jun 2, 2026, 6:45 AM EDT

Position: None

BY Doug Kass · Jun 2, 2026, 6:35 AM EDT

AI: The Biggest Capital Misallocation in History

Position: None

BY Doug Kass · Jun 2, 2026, 6:25 AM EDT

Position: None

BY Doug Kass · Jun 2, 2026, 6:15 AM EDT

Position: None

BY Doug Kass · Jun 2, 2026, 6:05 AM EDT

With S&P futures down by only -5 handles (they were -33 at the lows last night when I was covering), I am back shorting the indices:

Position: Short SPY (M), QQQ (M)

BY Doug Kass · Jun 2, 2026, 5:55 AM EDT

The S&P Short Range Oscillator moved into a greater overbought condition at 3.08% vs. 1.81%.

With S&P futures -29 handles last night at around 9 PM I covered some index shorts.

I plan to reup the short position on a rally.

Position: Short SPY (M) QQQ (M)

BY Doug Kass · Jun 2, 2026, 5:45 AM EDT

The embedded tweet could not be found…

I'm old enough to remember when mega-cap tech co's were capital-light cash printing monopolies Now they're raising record amounts of debt and equity to buy rapidly depreciating assets in a commoditized technology Probably ends well

🚨 S&P 500 MAX DRAWDOWN IN EVERY MIDTERM ELECTION YEAR: 1962: -28.0% 1966: -22.2% 1970: -36.1% 1974: -48.2% 1978: -14.1% 1982: -27.1% 1986: -9.4% 1990: -19.9% 1994: -8.9% 1998: -19.3% 2002: -33.8% 2006: -7.7% 2010: -16.0% 2014: -7.4% 2018: -10.2% 2022: -25.4% NOT A SINGLE Show more

Remember when shale companies would keep drilling negative ROIC wells and fund them with debt or equity or converts or literally any idiotic funding source. That’s why they’d trade at 3x EBITDA. $GOOG just told you that it’s basically a shale company. They cannot stop spending on Show more

Wow, Berkshire Hathaway investing $10 billion into $GOOGL

Drop everything and listen to this. This is the best AI discussion to be found ANYWHERE. This is crucial to not just the AI related stocks, but has important implications for the market and the economy. @GaryMarcus @JG_Nuke

Why things will eventually fall apart: 1. Everybody, even Google, seems to be treating AI as if it were some kind of winner take all competition like web search was, in which Google taking over 95% 2. But everybody is building essentially the same technical solution with Show more

Jensen Huang called Marvell “the next trillion-dollar company” during $MRVL CEO Matt Murphy’s Computex keynote in Taiwan.

THE DEFINITIVE AI CONVERSATION OF THE YEAR. MUST LISTEN. @JG_Nuke @GaryMarcus @MacrostrategyP open.substack.com/pub/georgenobl…

Alphabet generated over $160b in operating cash flow last year… yet it’s still issuing $40b+ in equity to fund AI compute (including a private placement to berkshire) One of the biggest cash generators in tech is diluting to keep up

John Hussman just published one of the most important pieces of market analysis I have read this year and every serious investor needs to read it. His warning flag system just triggered at levels only seen THREE other times since 1992. One of those times was March 24, 2000, Show more

Building Verano for Wall Street: A Capital Markets Breakdown with George Archos x.com/i/broadcasts/1…

I would argue Buffett and Munger have always preached the opposite. They've always focused on capital-efficient businesses, or those that can grow profits with minimal reinvestment back into the business. Think Sees Candies, American Express, Coca-Cola, etc. From Munger: Show more

Buffett described the *perfect* company as one that can reinvest huge amounts of money at high returns. He says the problem with companies like Mastercard is although they have high returns on invested capital, they just don’t have enough places to reinvest. Google prints $100