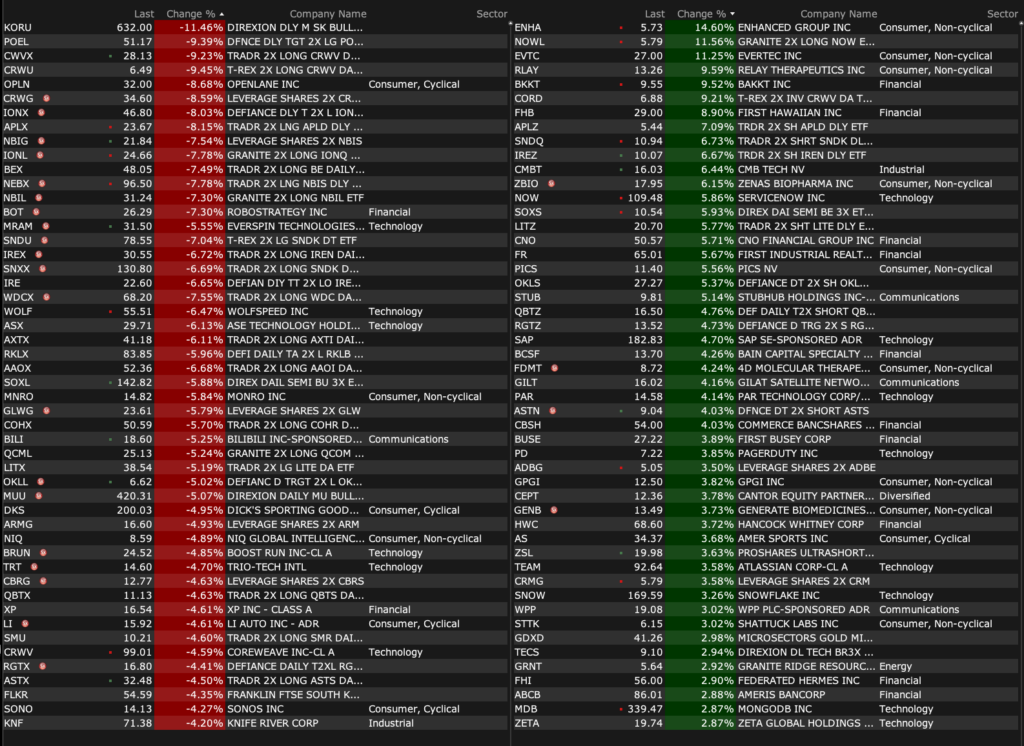

Tuesday’s After-Hours Advancers and Decliners

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · May 19, 2026, 4:35 PM EDT

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · May 19, 2026, 4:35 PM EDT

Closing Volume

– NYSE volume 1% above its one-month average

– NASDAQ volume 12% above its one-month average

– VIX index: up 1.68% to 18.12

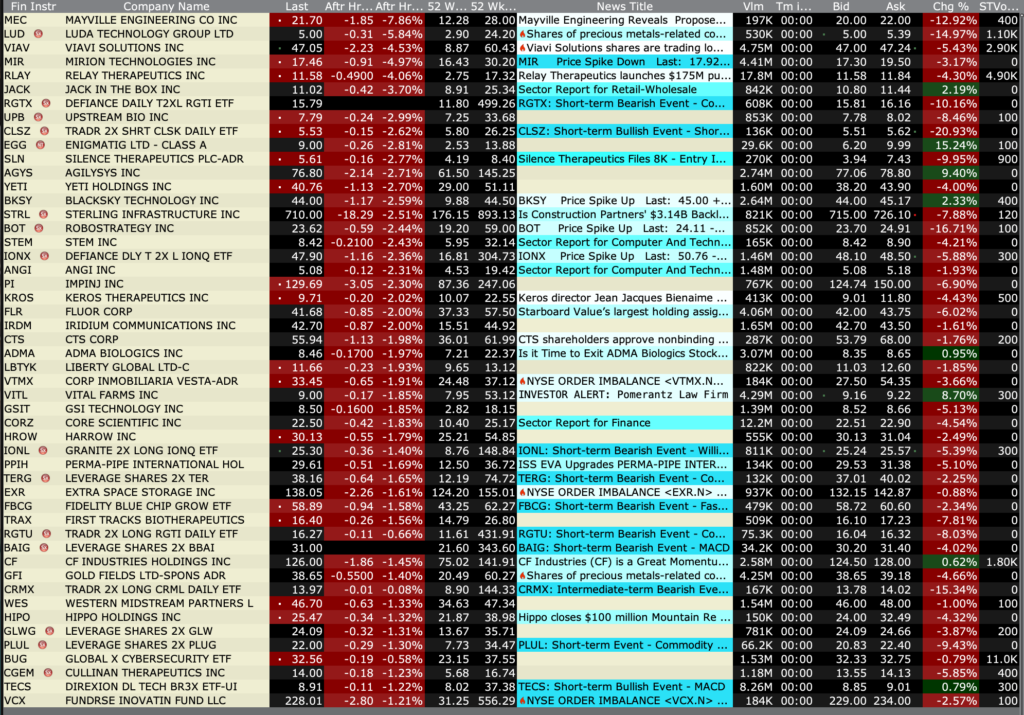

Breadth

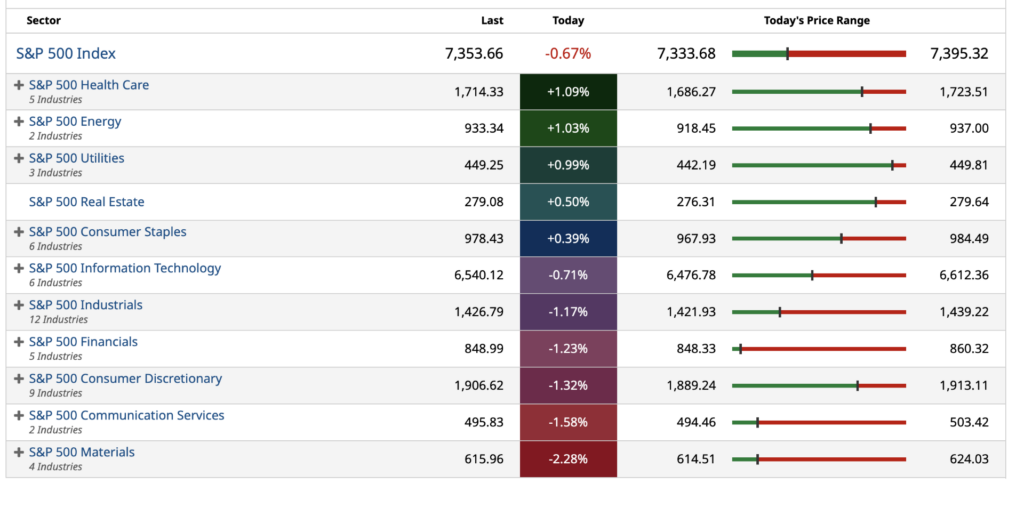

S&P 500 Sectors

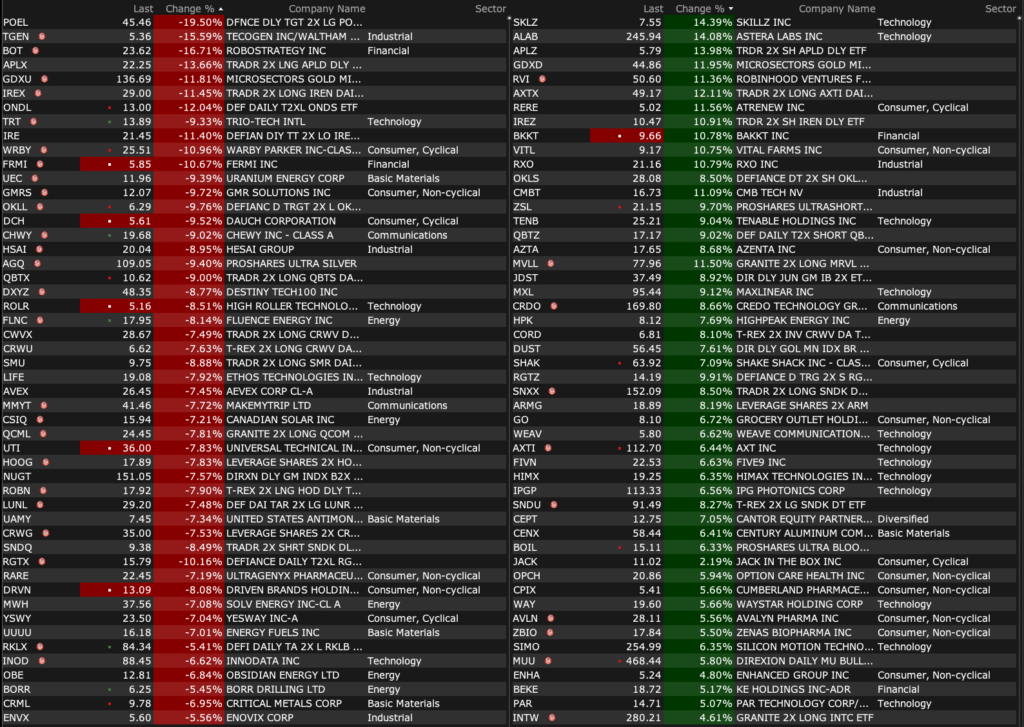

% Movers

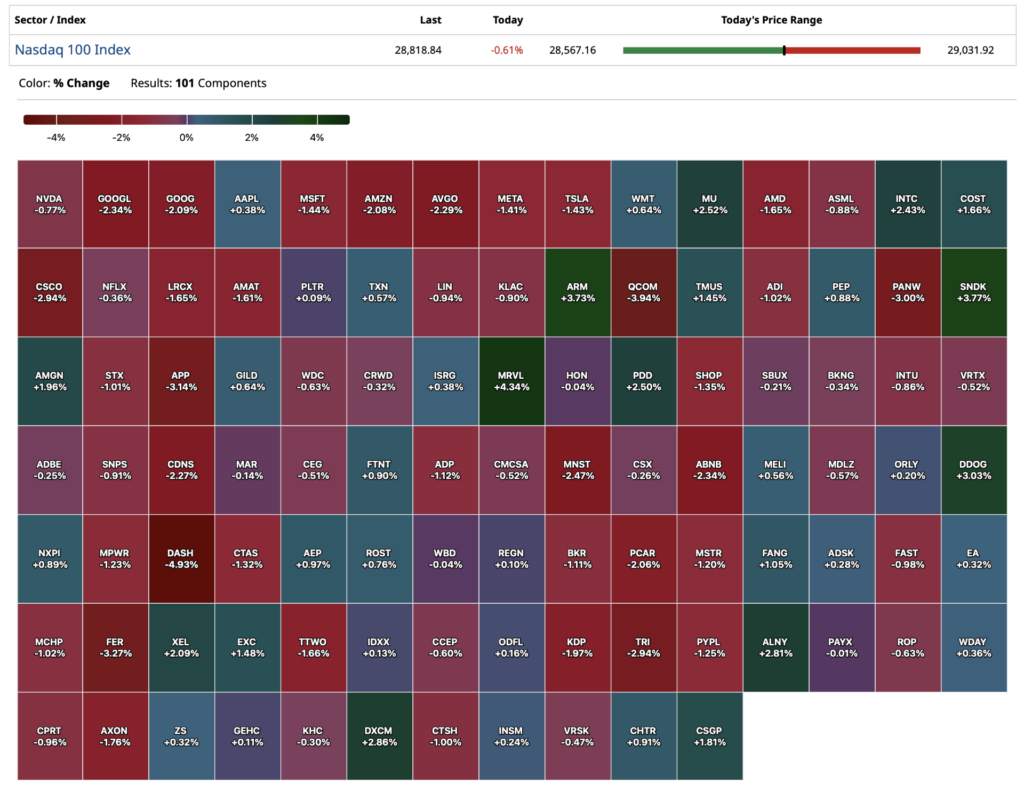

Nasdaq 100 Heat Map

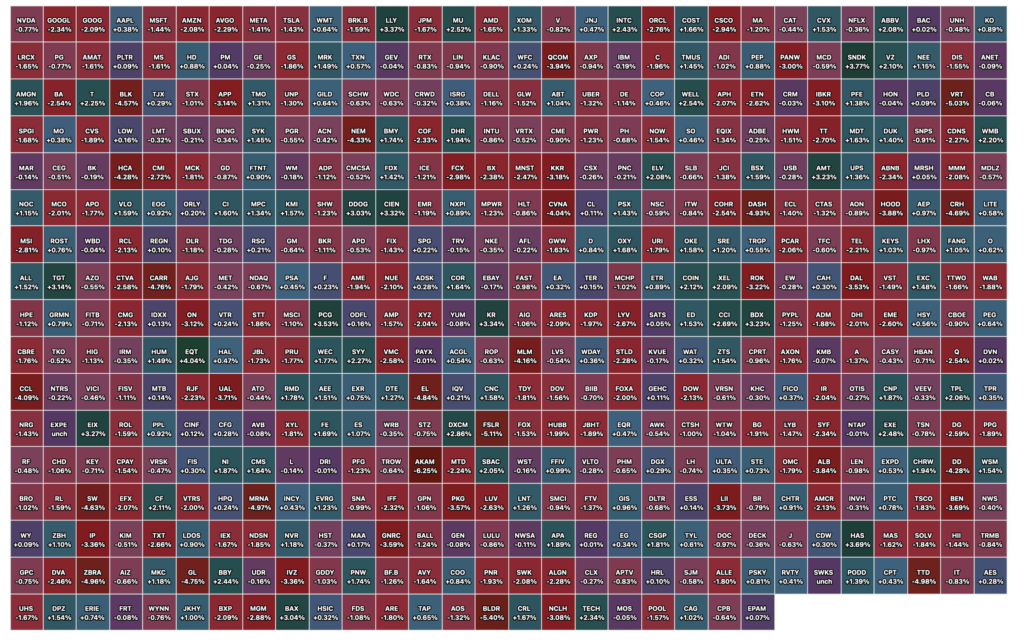

Closing S&P 500 Heat Map

Position: None

BY Doug Kass · May 19, 2026, 4:25 PM EDT

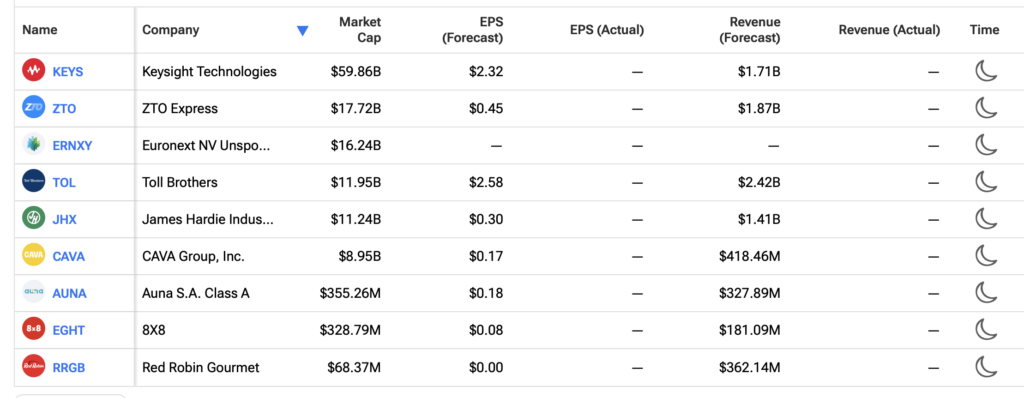

Earnings Calendar After the Close Tuesday

Earnings Calendar Pre-Open Wednesday

Position: None

BY Doug Kass · May 19, 2026, 3:44 PM EDT

Financials rolling over.

Never a good sign.

Position: None

BY Doug Kass · May 19, 2026, 3:37 PM EDT

Position: None

BY Doug Kass · May 19, 2026, 2:19 PM EDT

Good covers on NVDA, MU, AMD, INTC and SNDK yesterday:

I covered the balance of my individual technology shorts for some good profits:

* AMD $416.30 (-$6)

* NVDA $221.08

* MU $$680.95 (-$42)

* SNDK $1,291.61 (-$115)

* INTC $106.42 (-$2)

Position: None

BY Doug Kass · May 18, 2026, 1:37 PM EDT

I plan to re-short on strength but I am giving these volatile stocks a wide berth before I do so.

However, after the big rally off of the morning lows (and Nasdaq futures back in the green), I am back shorting the indices:

* SPY $737.44

* QQQ $706.28

Position: Short SPY (VS), QQQ (VS)

BY Doug Kass · May 19, 2026, 1:40 PM EDT

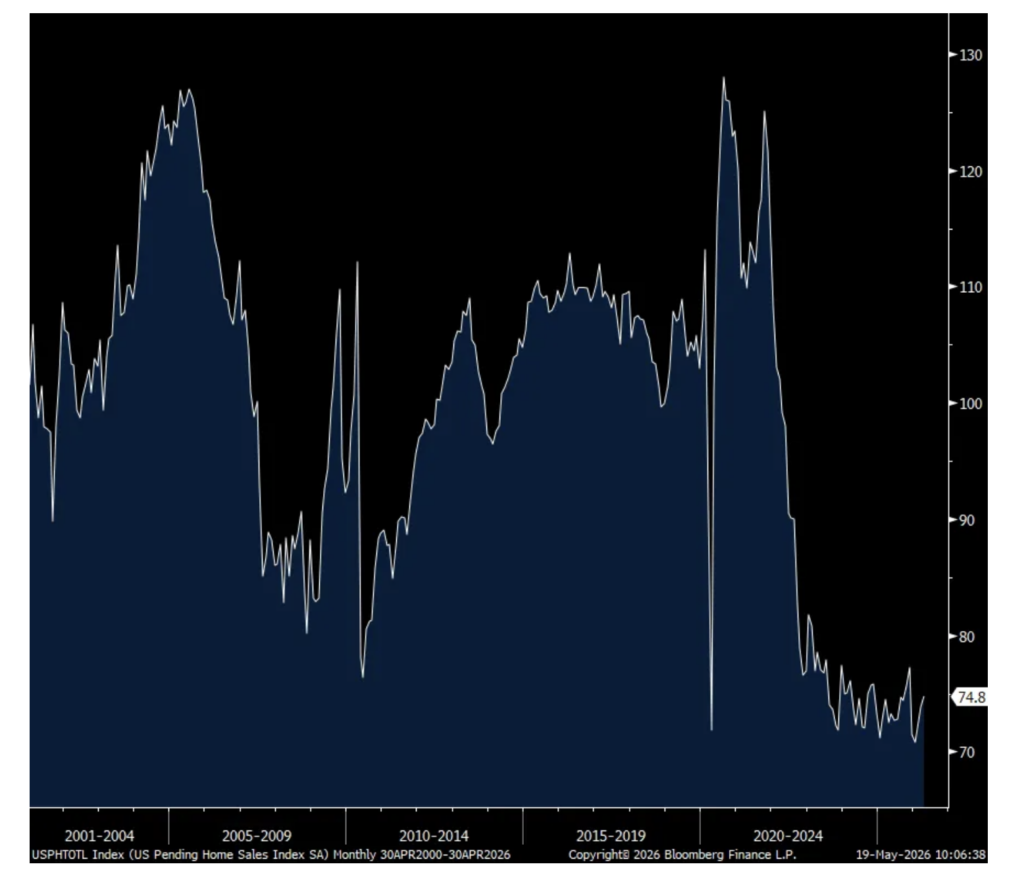

From Peter Boockvar:

Pending home sales lift for 3rd month but what happens next?

Pending home sales in April, when mortgage rates averaged 6.44% vs 6.26% in March, rose by 1.4% m/o/m, just above the estimate of up 1% and after a 1.7% increase in March and a 2.5% rise in February after a few months of declines. About all of the gain was seen in the Northeast and Midwest while there was little change in the South and West.

The NAR said “Buyers are coming out with cautious optimism despite increasing economic uncertainty and a slight rise in mortgage rates.”

Still limited inventory in some markets remains an issue in keeping prices elevated. The NAR added, “Unless supply meaningfully increases, home price growth could outpace wage growth and further erode the homeownership rate. All efforts need to be focused on boosting housing supply.”

Bottom line, as seen in the chart below, the pace of transactions continues to bounce along the multi decade bottom for reasons we all know and now we have higher mortgage rates again coincident with the rise in the 10 yr Treasury yield.

Pending Home Sales index

BY Doug Kass · May 19, 2026, 1:30 PM EDT

AI is, as it stands, not economically viable for anybody involved other than the construction firms, NVIDIA, and the surrounding hardware companies benefitting from the irrational exuberance of a data center buildout that doesn’t appear to be happening at the speed we believed.

Every AI startup loses millions or billions of dollars a year, and nobody appears to have worked out a way to stop hemorrhaging cash. Hyperscalers have invested over $800 billion in the last three years, with plans to add another $700 billion or so in 2026 and another $1 trillion in 2027, meaning that they need to make at least three trillion dollars in AI specific revenue just to break even, and $6 trillion or more for AI to be anything other than a wash. I went into detail about this (albeit at a lower, pre-2026/2027 capex number) in a premium piece last year.

– Ed Zitron

BY Doug Kass · May 19, 2026, 1:15 PM EDT

Position: None

BY Doug Kass · May 19, 2026, 12:55 PM EDT

Position: None

BY Doug Kass · May 19, 2026, 12:10 PM EDT

BY Doug Kass · May 19, 2026, 11:57 AM EDT

I’ve made no trade today.

Position: None

BY Doug Kass · May 19, 2026, 11:55 AM EDT

Positions: None.

BY Doug Kass · May 19, 2026, 9:55 AM EDT

From Peter Boockvar:

Fitch updated us with their April default figures yesterday for companies they follow in private credit. It rose to 6% which is the most since they started doing this in August 2024. That’s up from 5.7% in March. We know that there is so much focus on software but it wasn’t that at all that caused the rise. Fitch said they “recorded 10 private credit default events in April. Issuers in the industrial and manufacturing sector accounted for four events, followed by business services general with two. The consumer products, transportation and distribution, pharmaceuticals, and cable sectors each accounted for one event. Of the 10 private credit default events, six were new unique defaulters and four were serial defaulters.” Note, no mention of software.

Defining what qualified as a default, “Seven of the 10 default events involved maturity extensions under stress, while the remaining three involved the introduction of PIK interest in lieu of cash interest.”

Lastly on this, and to the point that software is not an issue here right now, “Healthcare providers remained the sector with the highest number of unique defaulters in the April TTM period. Twelve unique defaulters produced a 7% default rate, up from 6.9% in March 2026 and 5.8% in April 2025.”

Bottom line, private credit should still be a focus but as said, the software worries right now are not showing up in the data yet. Also, we have to differentiate the good underwriters from the not so good and not paint the whole sector with a broad brush. And finally, also differentiating a loan given to finance a private equity deal vs a loan lent to a borrower that wants to expand a business.

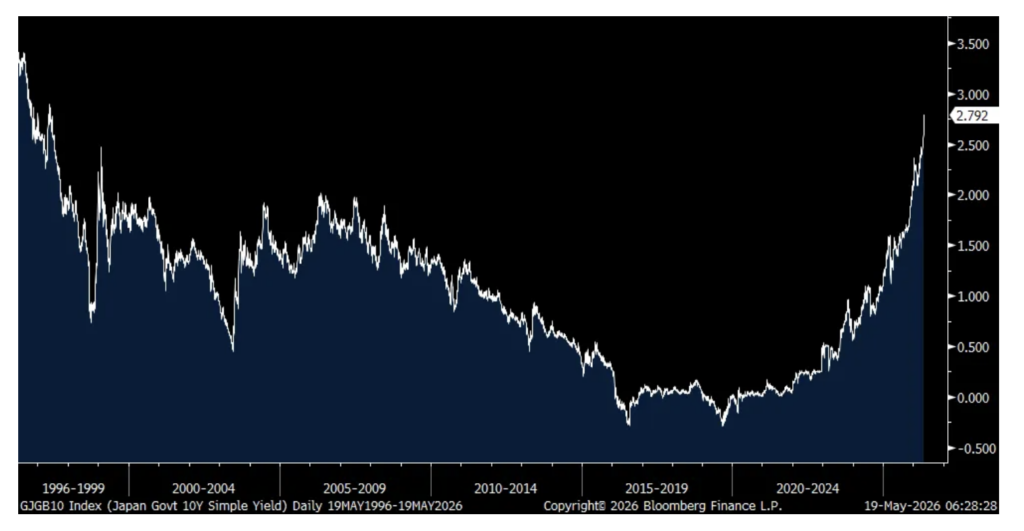

JGB yields jumped again overnight with the 10 yr yield up another 6 bps to 2.79% and we’re getting close to 30 yr highs. The chart is beginning to look vertical. I keep highlighting Japanese yields in particular because this was the original home of modern day interest rate suppression with ZIRP and QE and then they followed the Europeans into NIRP. And they remain the largest foreign holder of US Treasuries.

Speaking of those holdings of US Treasuries, Japan’s stock in Treasuries in March fell by $47.7b (including maturing T-bills not reinvested and changes in value). China’s holdings fell by $41b. Foreigners in the ‘foreign official’ category sold another $38b in total in notes/bonds. It was the $51.5b of ‘private’ buying that helped to offset that with ‘private’ including hedge funds in the Cayman Islands and their basis trades. UK holdings data are likely part of this too via UK banks.

If we include T-bills and those maturing and not reinvested, foreign holdings in total fell a large $138.4b worth with some of that due to falling values.

Bottom line, the US Treasury is relying more and more on US domestic savings and the basis trade to finance itself.

10 yr JGB Yield

Japanese holdings of US Treasuries, $1.192T

UK gilt yields are backing off a bit but not for good reason. In April, the ‘payrolled employee’ count fell by 100k, well worse than the estimate of down 10k. The caveat is that the ONS said there could be some beginning of the tax year distortions. Let’s hope so. The biggest job losses were seen in retail and leisure/hospitality. Also, jobless claims rose by another 26.5k. In the three months thru March, their unemployment rate rose one tenth m/o/m to 5%.

With respect to wages ex bonus, weekly earnings rose 3.4% y/o/y thru March which is not much above the rise in CPI. Tomorrow’s expected April CPI is expected to be up 3% y/o/y.

Home Depot had mixed results, beating top and line estimates but slightly missing Q1 comp forecasts. They said this in their earnings release of note ahead of their conference call:

“The underlying demand in our business was relatively similar to what we saw throughout fiscal 2025, despite greater consumer uncertainty and housing affordability pressure.”

In an interview, the CFO said that its customers “continue to defer large projects. They have told us that they have a higher degree of uncertainty.”

They reaffirmed its guidance with 2026 comps expected to be flat to up 2%.

Positions: None.

BY Doug Kass · May 19, 2026, 9:30 AM EDT

-AGYS +22% (earnings, guidance)

-RLAY +11% (intends to initiate Phase 3 zovegalisib + atirmociclib + aromatase inhibitor in early 2027, subject to regulatory feedback)

-NOW +5.9% (momentum)

-STUB +5.5% (Guggenheim Securities Raised STUB to Buy from Neutral, price target: $12.50 from $8.50)

-GILT +4.4% (announces milestone with Boeing for Sidewinder line-fit solution for in-flight connectivity)

-AS +3.4% (earnings, guidance)

-BILI -4.3% (earnings)

-CRWV -4.2% (pressure following BX deal with Google for AI data centers)

-XP -4.0% (earnings, guidance)

-RXO -2.7% (business update)

Positions: None.

BY Doug Kass · May 19, 2026, 9:01 AM EDT

Positions: None.

BY Doug Kass · May 19, 2026, 8:41 AM EDT

Positions: None.

BY Doug Kass · May 19, 2026, 8:35 AM EDT

11:00 a.m.: Treasury Announces a 4, 8 and 17 Week Bill Auction;

11:30 a.m.: Treasury hosts a$85B 6-Week Bill Auction;

2:00 p.m.: Treasury buyback (liq support)

8:00 a.m.: Fed Board Governor Waller (Voter) speaks at the ECB Research Conference, Frankfurt Germany;

7:00 p.m.: Fed Bank of Philadelphia President Paulson (Voter) speaks on the economic outlook before a dinner at the Federal Reserve Bank of Atlanta 2026 Financial MarketsConference: “Technology’s Transformative Role in Finance and Central Banking,” Amelia Island, FL (Livestream and text available. Audience Q&A expected.No media Q&A. Event information: atlantafed.org);

7:45 p.m.: FedBank of Atlanta First Vice President Venable (Voter) gives closing remarks before the Federal Reserve Bank of Atlanta 2026 Financial Markets Confer-ence: “Technology’s Transformative Role in Finance and Central Banking,” Amelia Island, FL (Livestream available. Other details TBA. Event information: atlantafed.org/news-and-events/events/2026/05/17/financial-markets-conference/agenda)

BY Doug Kass · May 19, 2026, 8:27 AM EDT

How deep is your love, how deep is your love

How deep is your love?

I really mean to learn

‘Cause we’re living in a world of fools

Breaking us down when they all should let us be

We belong to you and me

– Bee Gees, How Deep is Your Love?

Under the influence of a prolonged conflict in Iran, the uncertainty of improvisational policy in Washington D.C., rising interest rates and an accelerating rate of inflation — equities have been heading lower since late last week.

Machines, that worship at the altar of price, have begun to mechanically sell. (A perma-bull panelist on CNBC blamed the market decline over the last several days on algo selling, but failed to highlight that algos likely contributed to the upside explosion in stocks since March 2026).

How deep is the market’s love?

We will likely find out in the next several weeks.

I remain bearish, as highlighted in my recent five-part missive.

Doug Kass: A Market Bacchanal Rages On, While I Remain Celibate

Position: None

BY Doug Kass · May 19, 2026, 7:20 AM EDT

Position: None

BY Doug Kass · May 19, 2026, 6:35 AM EDT

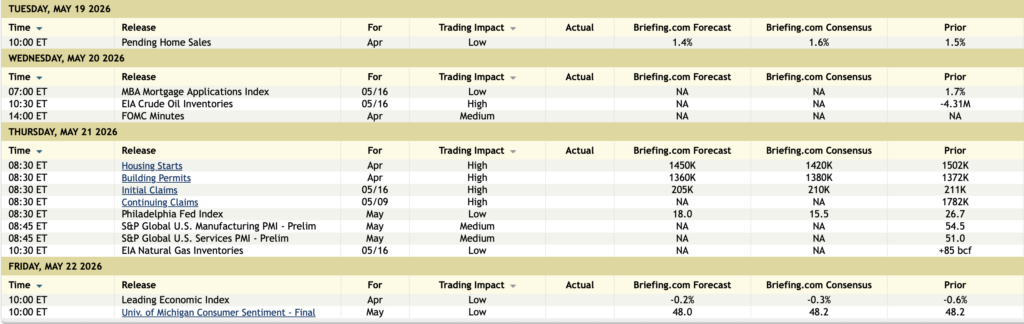

From Jazzy Jeff Hirsch:

As of today’s close, slower moving MACD indicators applied to both DJIA and S&P 500 are negative (arrows in the charts below point to a crossover or negative histogram). We are issuing our Best Six Months MACD Seasonal Sell signal for DJIA and S&P 500. NASDAQ’s “Best Eight Months” lasts until June.

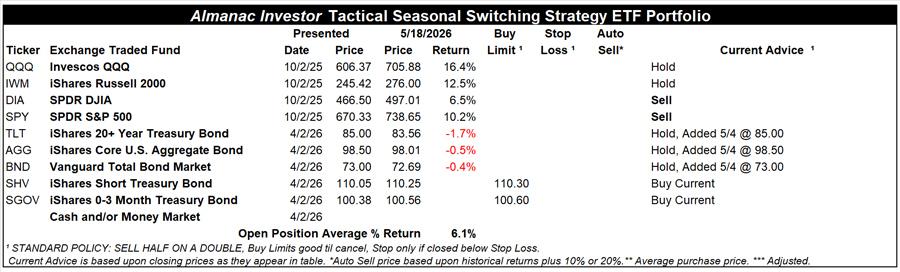

Almanac Investor Tactical Seasonal Switching ETF Portfolio Trades

SELL SPDR DJIA (DIA) and SPDR S&P 500 (SPY) positions. For tracking purposes these positions will be closed out of the portfolio using their respective average prices on May 19.

Continue to HOLD Invesco QQQ (QQQ) and iShares Russell 2000 (IWM) as NASDAQ’s “Best Eight Months” does not end until June.

For this “Worst Months” period we have presented some low-fee ETFs where cash from the positions that are being closed out can be used ranging from relatively low-risk/low-reward to higher-risk/potentially higher reward. Please, consider your individual risk tolerance and investment objectives when choosing.

Consider establishing a position in iShares Short Treasury Bond (SHV) with a Buy Limit of $110.30.

Consider establishing a position in iShares 0-3 Month Treasury Bond (SGOV) with a Buy Limit of $100.60.

Although we would consider SHV and SGOV to be low-risk/low-reward options given their relatively stable prices, they have respectable yields. With longer-dated Treasury bond yields creeping higher (prices going down) due to rising inflation expectations brought on by higher energy costs, our preferred funds are SHV and SGOV at this time.

For tracking purposes, SHV and SGOV will be added to the portfolio on May 19, using their respective average prices.

Vanguard Total Bond Market (BND), iShares Core US Aggregate Bond (AGG), and iShares 20+ Year Treasury Bond (TLT) were all added to the portfolio on May 4, when they all dipped below their respective buy limits. BND, AGG, and TLT are on Hold.

Lastly, positions in cash and/or money market funds can also be considered. Choices yielding 3.5% are available. An allocation to cash or a money market fund will likely be the least nerve-racking position should market volatility spike during the “Worst Months.”

Traders/investors following the Best 6 + 4-Year Cycle switching strategy detailed on page 64 of the Stock Trader’s Almanac 2026 should heed this Seasonal Sell signal. Even if you are not actively trading the “Best Months” switching strategy, it is still a good reminder to review existing holdings and consider a cautious stance.

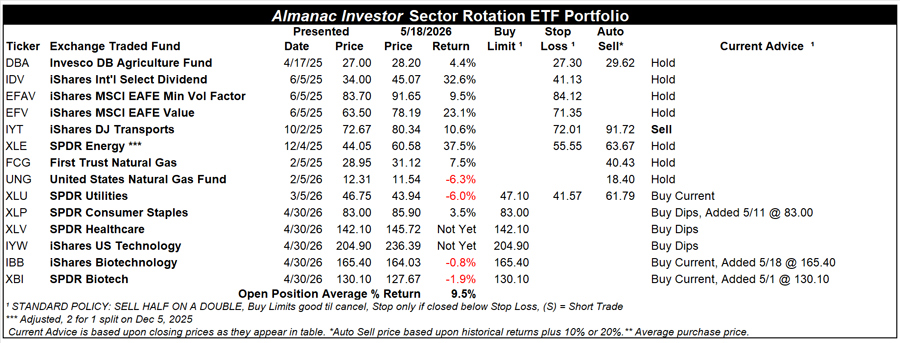

Almanac Investor Sector Rotation ETF Portfolio Trades

Sell iShares DJ Transports (IYT) as its correlating seasonality has historically ended in the beginning of May. For tracking purposes IYT will be closed out of the portfolio using its average price on May 19.

SPDR Healthcare (XLV) and iShares US Technology (IYW) can still be considered on dips below their respective buy limits.

SPDR Consumer Staples (XLP), iShares Biotechnology (IBB), and SPDR Biotech (XBI) have been added to the portfolio and can be considered on dips or at current prices up to their respective buy limits.

SPDR Utilities (XLU) can still be considered at current prices up to its buy limit.

XLU, XLP, XLV, IYW, IBB, and XBI are “Worst Months” defensive trades based upon their corresponding sectors’ historical tendency to outperform the S&P 500 from May through October.

All other holdings in the Sector Rotation Portfolio are on Hold.

Today’s Seasonal MACD Sell Signal for DJIA and S&P 500 marks the beginning of the “Worst Six Months” for DJIA and S&P 500. We do not simply sell and go away. Instead, today’s trades are the start of tactical adjustments that will be made in the portfolios. Between now and when NASDAQ’s Seasonal MACD Sell Signal triggers (earliest it can trigger is on June 1 this year), the portfolios will be shifted toward a neutral stance. Positions that have historically performed well during the “Worst Months” will be held along with positions that correlate to NASDAQ and Russell 2000.

All current stock and ETF holdings will be reevaluated in upcoming email Alerts. Weak or underperforming positions may be closed out, stop losses may be raised, new buying may be limited, and we will evaluate the timing of adding additional positions in sectors that perform well in the “Worst Six Months” and potentially a new basket of defensive stocks.

Position: None

BY Doug Kass · May 19, 2026, 6:17 AM EDT

The S&P Short Range Oscillator has shifted back to neutral from oversold at 0.04% vs. -1.35%.

Position: None

BY Doug Kass · May 19, 2026, 5:50 AM EDT

I am hearing on good authority a Virginia Adult Use veto is imminent.

Dario Amodei and Sam Altman have created the largest grift in history by manipulating growth-obsessed investors, brainless executives, and building a culture where skeptics are harassed and attacked for not bowing to the platonic form of capital. wheresyoured.at/ai-is-too-expe…