Intraday Advance-Decline vs. SPY; SPY Daily With Comparative

SPY Daily Chart with comparative (middle graph of relative volume versus its 50-day moving average)

BY Doug Kass · Dec 27, 2024, 4:40 PM EST

SPY Daily Chart with comparative (middle graph of relative volume versus its 50-day moving average)

BY Doug Kass · Dec 27, 2024, 4:40 PM EST

BY Doug Kass · Dec 27, 2024, 4:23 PM EST

I am leaving early today.

Thanks for reading my Diary today and all week.

And all year.

Enjoy the weekend.

Be safe.

BY Doug Kass · Dec 27, 2024, 2:50 PM EST

From SoCalGary:

For fun, I asked I asked ChatGPT what to invest in with a couple of Doug's Surprises.

#7: AI related equities are adversely impacted by two factors - the inadequacy of supply of electricity and the absence of a killer app or related income stream:

Natural Gas and Infrastructure: As natural gas prices surge, producers like EOG Resources EOG and Chesapeake Energy CHK, as well as midstream players like Kinder Morgan KMI and Williams Companies WMB, are positioned to thrive. The demand for new power stations and reliable energy sources will further bolster these industries.

Renewable Energy and Grid Modernization: With public pressure for sustainable solutions, companies like NextEra Energy NEE, Itron ITRI, and Siemens SIEGY, which focus on renewables and modernizing the grid, are poised for growth.

Power Storage and Backup Solutions: Rising power outages make companies like Generac GNRC, Tesla TSLA, Enphase Energy ENPH, and Fluence Energy FLNC, which specialize in energy storage and backup systems, critical players in maintaining reliability.

AI-Adjacent Sectors: Software-focused AI firms like Palantir Technologies PLTR and ServiceNow NOW, less reliant on energy-intensive data centers, may outperform as the industry adapts to regulatory pressures.

Utilities and Dividends: Utilities such as Duke Energy DUK and Dominion Energy D could see higher revenues from rate increases, while dividend-paying companies like Southern Company (SO) and Consolidated Edison ED offer income stability.

Infrastructure and Engineering: Firms like Quanta Services PWR, General Electric Vernova GEV, Fluor Corporation FLR, and Jacobs Engineering J, which specialize in grid modernization and energy infrastructure, are well-positioned to benefit from increased investment in energy reliability.

Surprise #8: AI headlines are replaced with quantum computing headlines

Quantum Computing Hardware Providers: Leaders like IBM IBM, IonQ IONQ, and Rigetti Computing RGTI are pioneering quantum hardware, with systems that offer unprecedented computing power for specific problems.

Semiconductor and Chipmakers: Companies like NVIDIA NVDA, Intel INTC, and Advanced Micro Devices AMD are developing the specialized chips needed for quantum-compatible and hybrid systems.

Quantum Software and Algorithms: Firms like D-Wave Quantum QBTS, Alphabet GOOGL, and Microsoft MSFT are innovating in quantum algorithms and creating platforms to harness quantum power for optimization, AI, and more.

Cloud Computing Providers: Platforms such as Amazon AMZN with AWS Braket, Microsoft MSFT with Azure Quantum, and Google GOOGL via Google Cloud enable quantum experimentation and application development.

Companies Exploring Quantum Applications: Quantum breakthroughs are being applied in industries like aerospace (Boeing BA), pharmaceuticals (Pfizer PFE), and automotive optimization (Volkswagen VWAGY).

Cybersecurity Companies: Quantum computing could revolutionize encryption, boosting demand for quantum-resistant solutions. Companies like Quantinuum (backed by Honeywell HON), Palo Alto Networks PANW, and Arqit Quantum ARQQ are leading in this area.

Venture Capital and ETFs: Diversified investment options like Defiance Quantum ETF QTUM and ARK Innovation ETF ARKK offer exposure to a broad array of companies in the quantum and disruptive technology space.

Quantum Networking and Infrastructure: Supporting technologies, such as quantum-safe networks and communication, are advanced by companies like Lumen Technologies LUMN and Ciena CIEN.

BY Doug Kass · Dec 27, 2024, 1:51 PM EST

BY Doug Kass · Dec 27, 2024, 1:11 PM EST

At $87.29 moved to large TLT.

BY Doug Kass · Dec 27, 2024, 12:22 PM EST

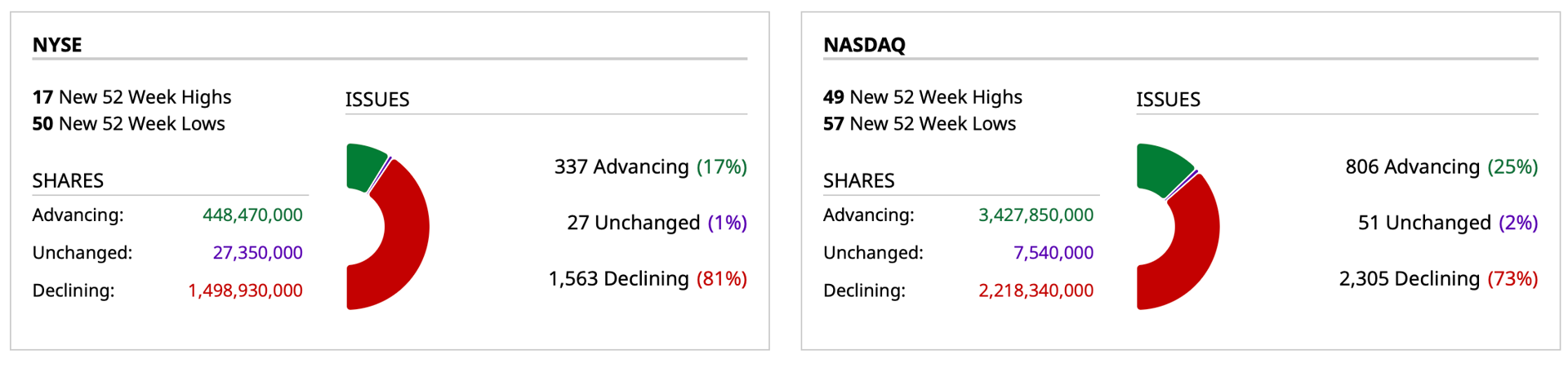

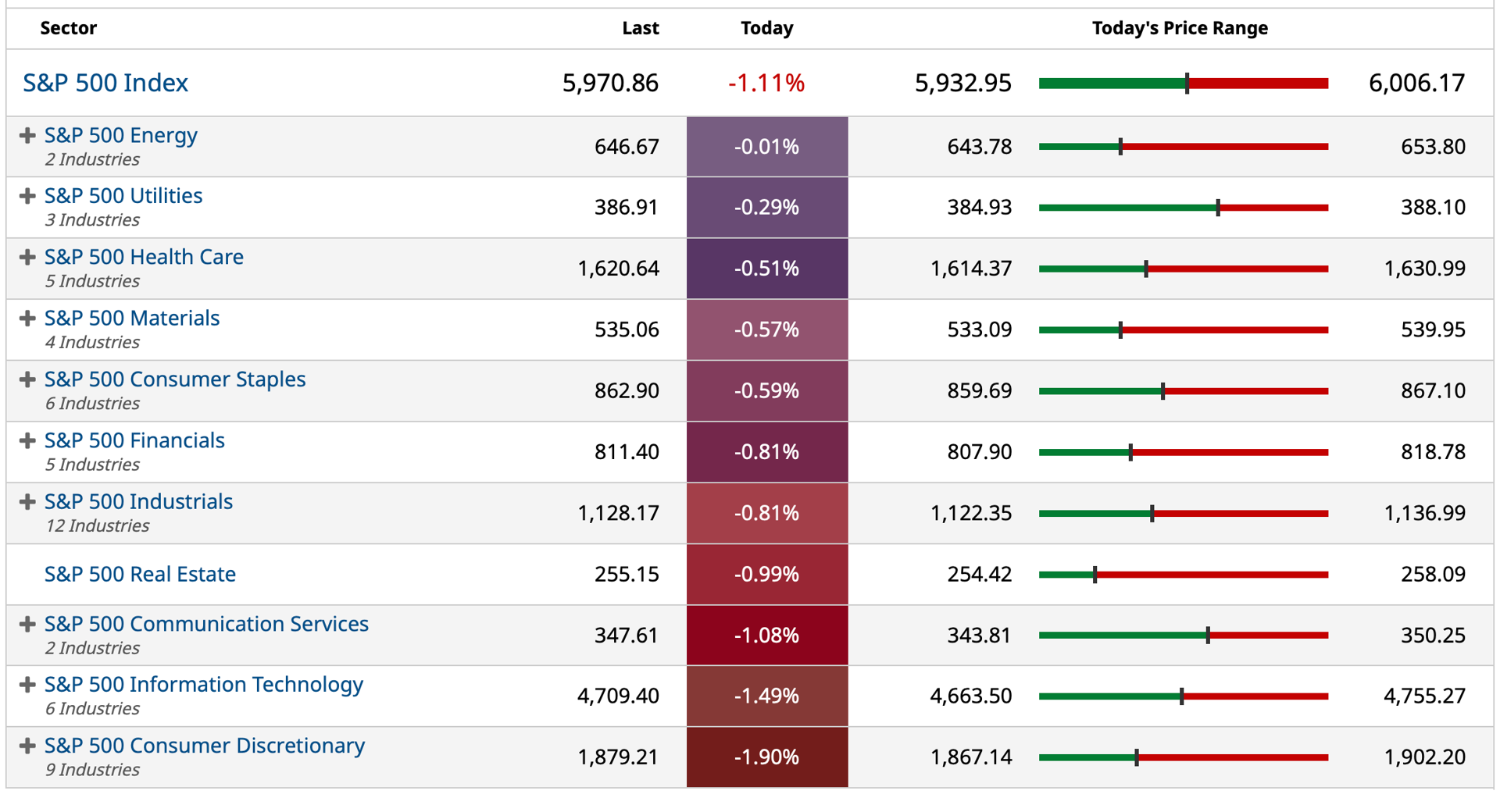

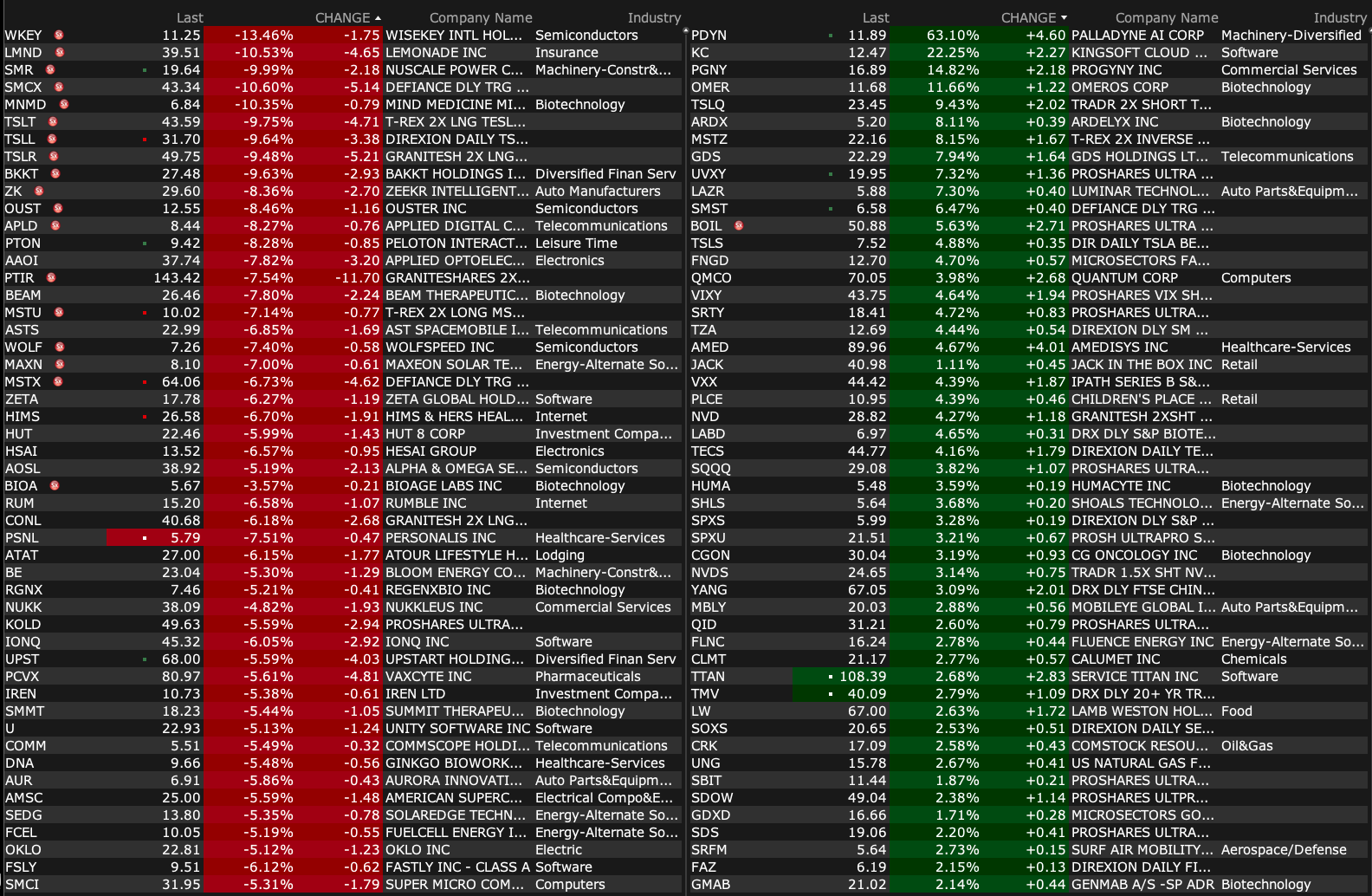

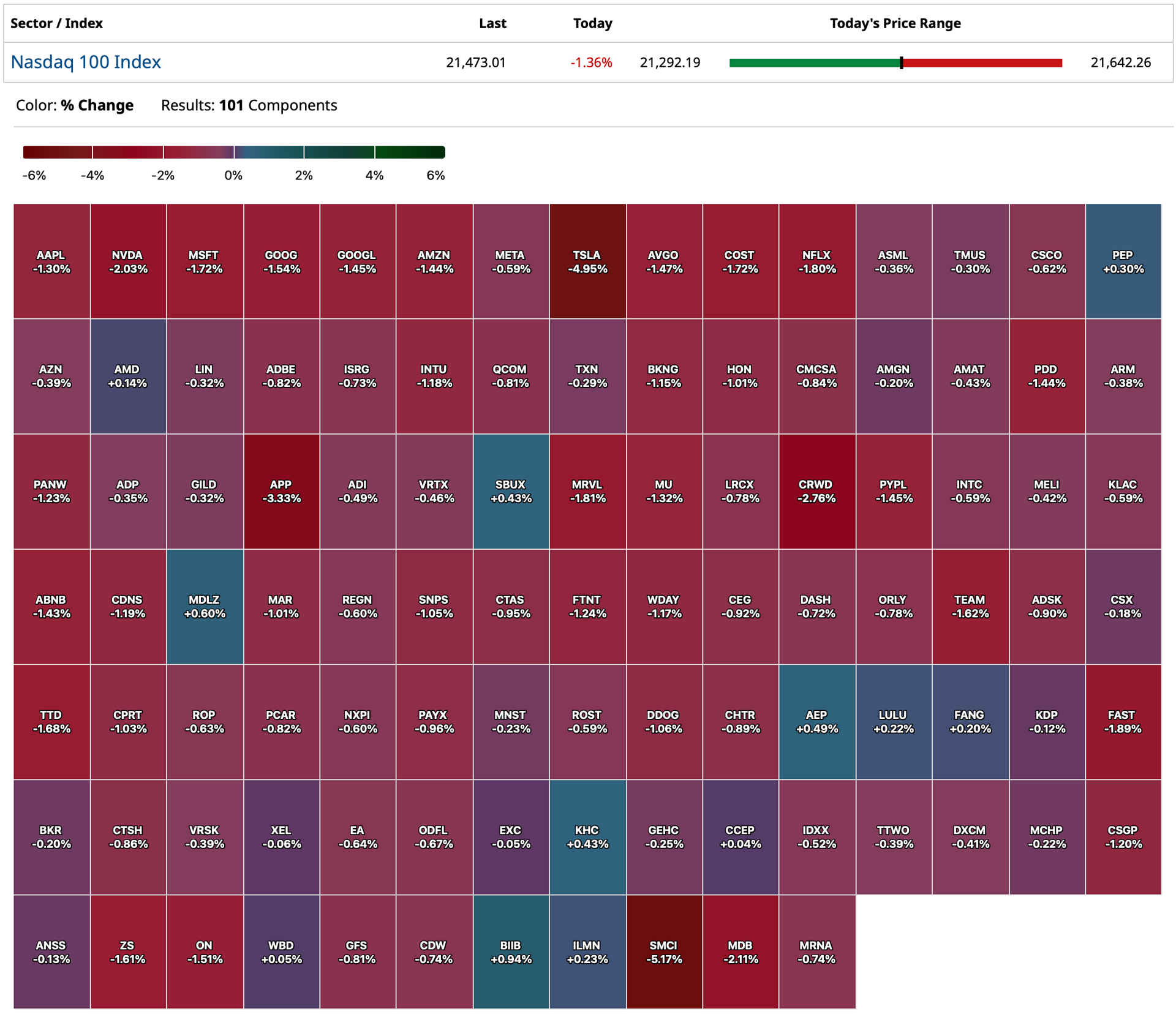

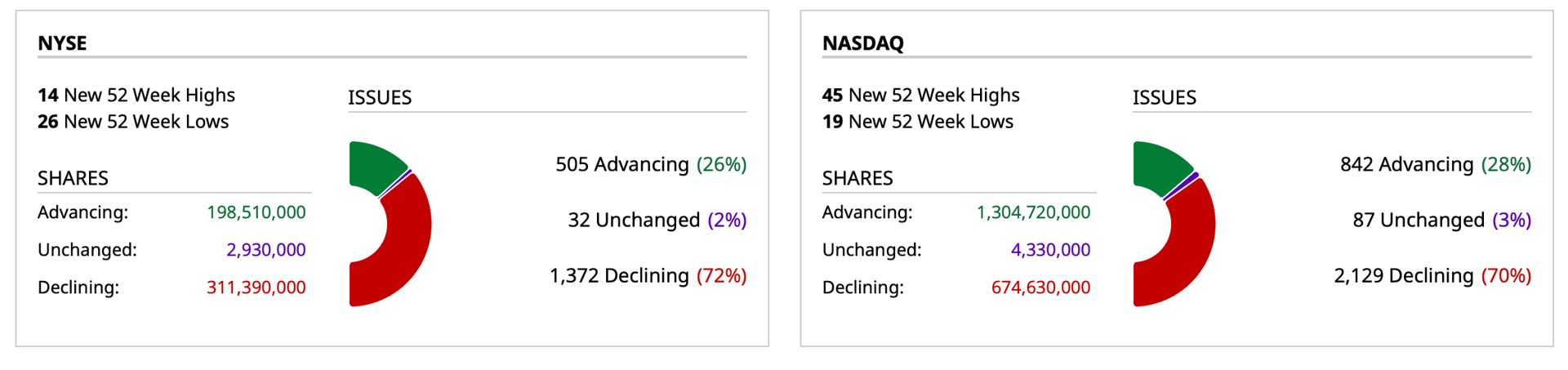

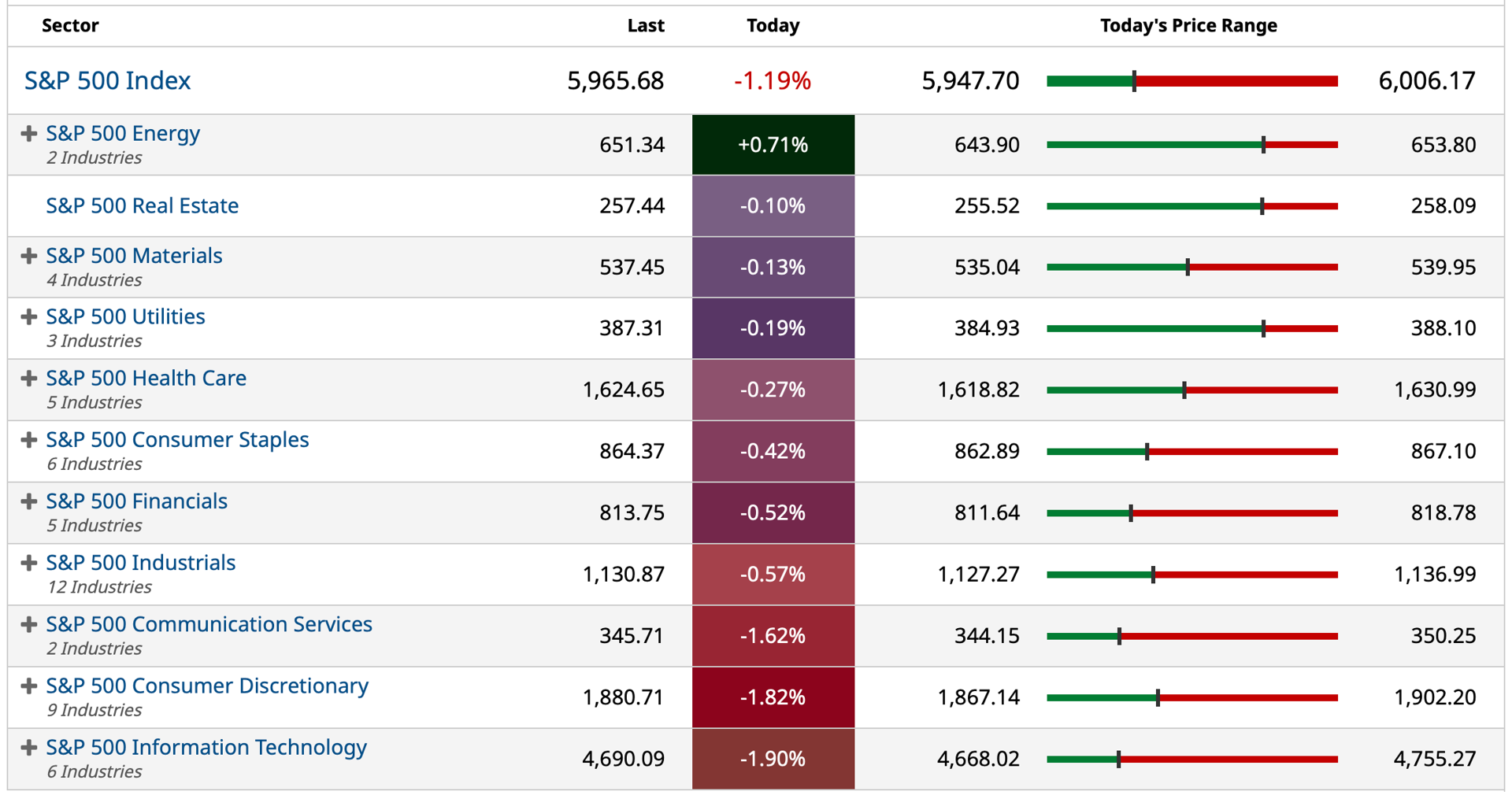

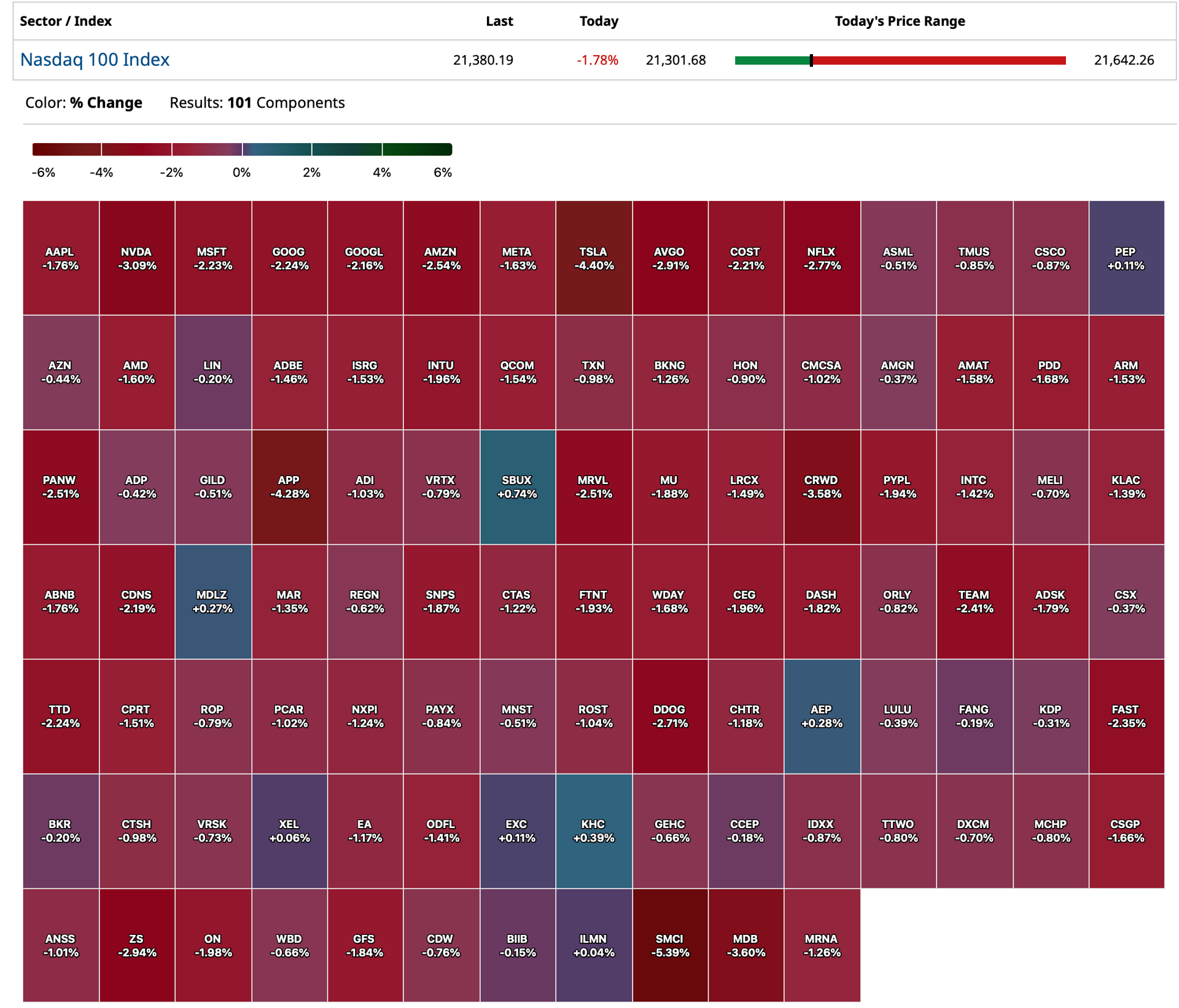

* Declining market but this time on large volume and during a usually quiet holiday week

* Nasdaq volume is 28% above its one-month average

* Volatility Index is up 20.77% to 17.79

BY Doug Kass · Dec 27, 2024, 11:45 AM EST

I bought a small position in TLT at $87.53.

BY Doug Kass · Dec 27, 2024, 11:31 AM EST

BY Doug Kass · Dec 27, 2024, 11:15 AM EST

douglas cassel

39 minutes ago

This article can be taken two ways. First, it reinforces the nefarious aspect of cypto, being used by criminals and other bad actors to evade the law. However, it also demonstrates that people in the USA have a very biased perspective on currencies because of the dominance of the dollar. In countries where currencies are weaker and even more manipulated, BTC represents a real alternative that is far more attractive then in the USA. I have long said that crypto uptake will be far sooner in countries with a lack of trust in the government and the currency, a factor really discounted by many crypto critics.

Russia's finance minister reveals bitcoin is being used to conduct foreign trade - SiliconANGLE

siliconangle.com

BY Doug Kass · Dec 27, 2024, 11:00 AM EST

Back to market neutral.

BY Doug Kass · Dec 27, 2024, 10:41 AM EST

BY Doug Kass · Dec 27, 2024, 10:28 AM EST

I have covered my TSLA short at $433.52.

BY Doug Kass · Dec 27, 2024, 10:12 AM EST

I have covered my Apple AAPL short at $255.94.

I will reshort strength.

BY Doug Kass · Dec 27, 2024, 10:09 AM EST

At $135.83 (-$4) I have covered my NVDA.

BY Doug Kass · Dec 27, 2024, 10:06 AM EST

With S&P cash -48 handles I have taken off my Index short calls for a profit.

I am also trading around my NVDA and AAPL shorts. Covering some, will reshort strength (which there usually appears to be).

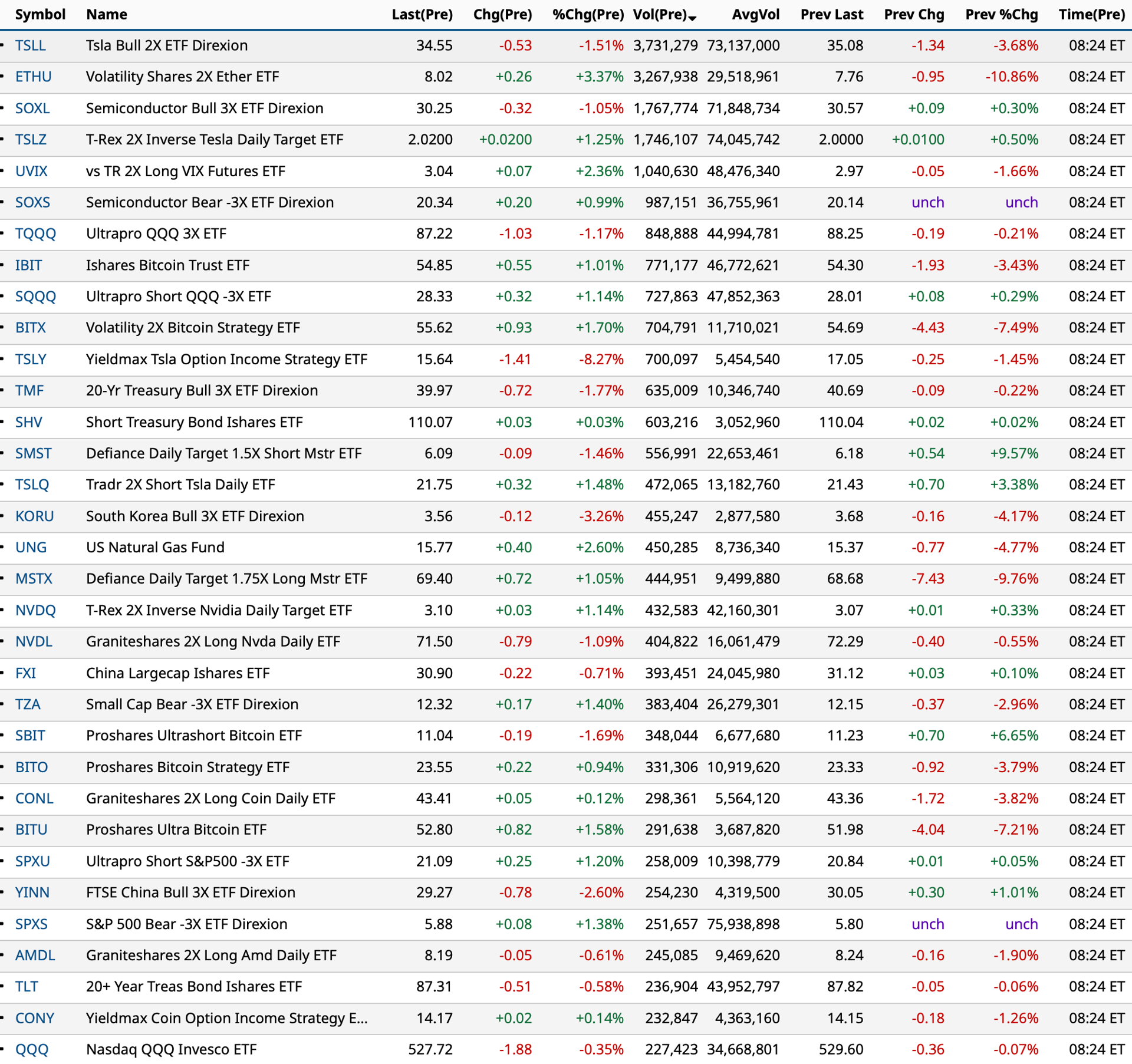

BY Doug Kass · Dec 27, 2024, 9:45 AM EST

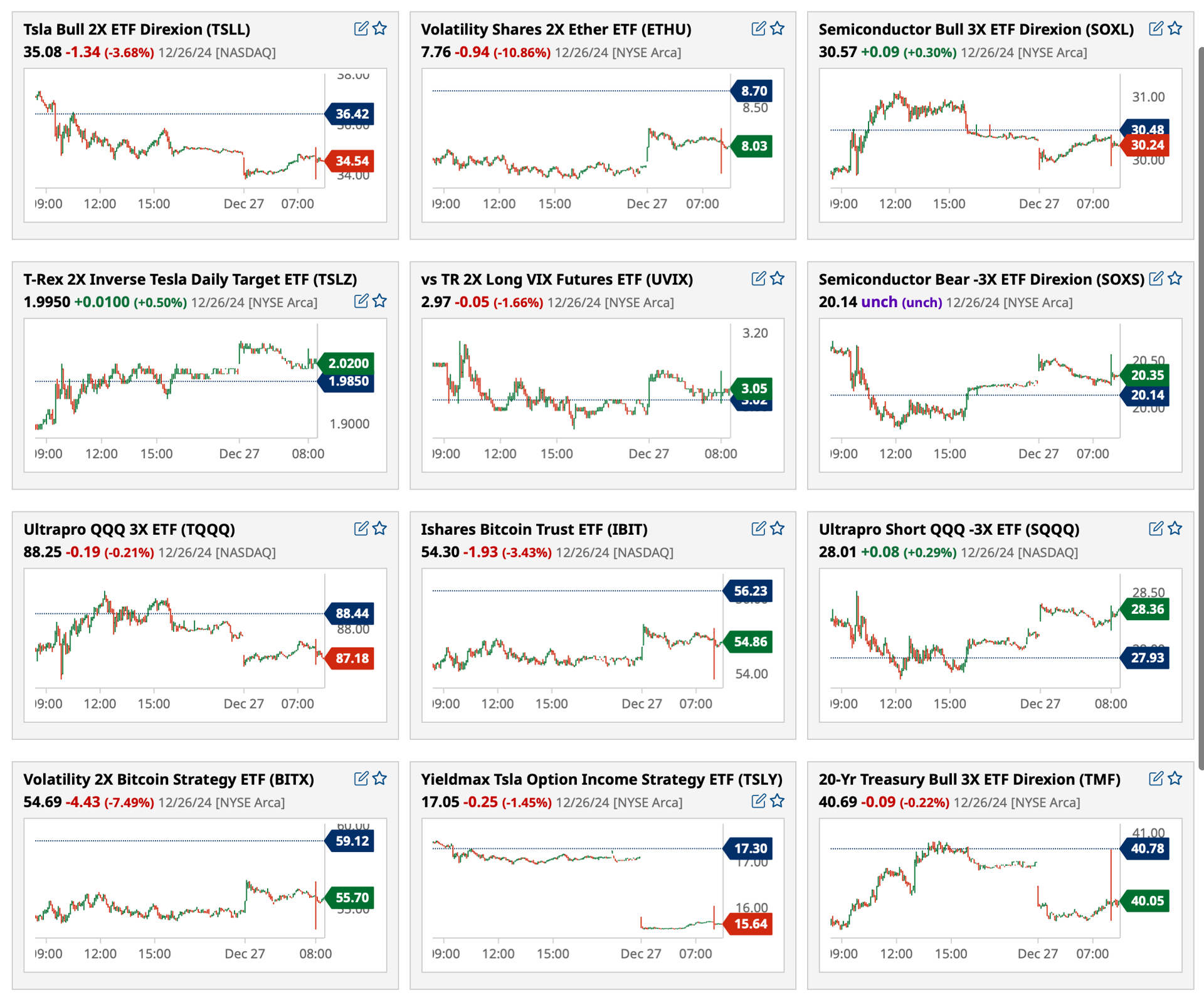

What happens when QQQ is only 33rd most active and SPY is 37th ranking in premarket volume?

Charts from 8:24 a.m. ET:

BY Doug Kass · Dec 27, 2024, 9:10 AM EST

Chart from 8:41 a.m. ET:

BY Doug Kass · Dec 27, 2024, 8:53 AM EST

I added to my Apple AAPL short at $259.36.

BY Doug Kass · Dec 27, 2024, 8:37 AM EST

-AMED +3% Amedisys and UnitedHealth Group each waived its right to terminate the Merger Agreement

-KULR +12% files to sell shares

-GDYN +7% to join S&P SmallCap 600 Index

-SRFM +32% Board purchases

-IMKTA +2% earnings

-BGNE -2% TEVIMBRA approved in U.S. for first-line treatment of Gastric and Gastroesophageal Junction Cancers i

-BNTX -1% discloses settlement agreement with NIH

BY Doug Kass · Dec 27, 2024, 8:05 AM EST

* The herd of the consensus has rarely been so crowded

* As the many prophets of prosperity battle (to defeat?) the few prophets of doom

* But, to me, the times may be a-changin' and investors might now be blinded by that bullish consensus

* In 2025, Minsky might have "his moment" and the bond vigilantes may be coming out of their cave of hibernation

* The Bottom Line: Reward vs. risk has grown ever more unattractive and the phrase, "margin of safety," has been eliminated from many investors' dictionaries

Come gather 'round people wherever you roam

And admit that the waters around you have grown

And accept it that soon you'll be drenched to the bone

If your time to you is worth savin'

Then you better start swimmin' or you'll sink like a stone

For the times, they are a-changin'

Come writers and critics who prophesize with your pen

And keep your eyes wide, the chance won't come again

And don't speak too soon for the wheel's still in spin

And there's no tellin' who that it's namin'

For the loser now will be later to win

-Bob Dylan, "Times They Are a Changin'" (Live in England, 1965)

Yesterday's opening missive, "Don't Think Twice," was stimulated and was the outgrowth of watching the movie, "A Complete Unknown" on Christmas Day. I made the case "to be on your own" with a non-consensus market view that December 2024 might resemble December 1972 (the start of an extended multi-year bear market):

"I have been on my own with an ursine market view.

"My theory has been that the December 2024 investing backdrop may resemble that of December 1972.

"Let me explain.

"In both periods, we faced a combative President (Nixon/Trump), narrow leadership (it was the Nifty Fifty in the early 1970s and the Mag Seven in recent years), interest rates and inflation turned up (from the prior few decades) and public sector debt was climbing rapidly — like in 1972, we lack visibility today (and a sense of fiscal responsibility on the part of our political leaders with regard to future fiscal policy).

"In both periods the forward PE was extremely elevated (today, at nearly 23x), the market advance was not broadening out, the "animal spirits" took stock prices higher without a commensurate change in future profit forecasts and the equity risk premium was paper thin."

It is said that not everything that is faced can be changed, but nothing can be changed until it is faced.

Outlier market views are easily rejected in a market that is dominated by money managers, analysts and strategists who, like the very market structure that we operate in (dominated by passive products and strategies) — worship at the altar of price momentum.

A compliant business media routinely delivers up bullish opinions — it is calming chicken soup for their viewers' souls.

It is easy to listen to the "prophets of prosperity" — like Tom Lee and Dan Ives — because it is what their audience wants to hear and, well... stocks are climbing apace and those prophets are delivering profits.

It is easy to be entranced and even intoxicated about the heady market returns this year and easy to extrapolate those returns and to expect them to continue — of course, unless you look under the market's hood.

The prophets of doom, on the other hand, are readily dismissed in the face of the aforementioned prosperity — even if their analysis and rationale of their ursine views are (arguably) growing in possibility.

Adopting such a profitless and non-consensus view these days, feels much like the Fall of 2007, early 2000 or late 2021 — or, as I made the case yesterday, of December 1972. Those negative views looked supremely stupid... until they didn't.

So, for those that are ignoring persistent and stick inflation, climbing interest rates (that have produced a paper thin equity premium), extended valuations (in the 95 percentile) and following the crowd — mea culpa.

Here are some "Lessons Learned" about conventional wisdom from the "Prelude to My 2025 Surprise List" from last week:

"A second argument is made that there are just too many question marks about the near future; wouldn't it be better to wait until things clear up a bit? You know the prose: 'Maintain buying reserves until current uncertainties are resolved,' etc. Before reaching for that crutch, face up to two unpleasant facts: The future is never clear; you pay a very high price in the stock market for a cheery consensus. Uncertainty actually is the friend of the buyer of long-term values."

-Warren Buffett, Forbes (1979)

"The missing step in the standard Keynesian theory (is) the explicit consideration of capitalist finance within a cyclical and speculative context... finance sets the pace for the economy. As recovery approaches full employment... soothsayers will proclaim that the business cycle has been banished (and) debts can be taken on. But in truth neither the boom nor the debt deflation... and certainly not a recovery can go on forever. Each state nurtures forces that lead to its own destruction."

-Hyman Minsky

"Every new beginning comes from some other beginning's end."

-Seneca the Elder

"I'm astounded by people who want to 'know' the universe when it's hard enough to find your way around Chinatown."

-Woody Allen

"Let's face it: Bottom-up consensus earnings forecasts have a miserable track record. The traditional bias is well-known. And even when analysts, as a group, rein in their enthusiasm, they are typically the last ones to anticipate swings in margins."

-UBS (Top 10 Surprises for 2012)

There are five important and core lessons I have learned over the course of my investing career that form the foundation of my annual surprise lists:

Again, it's important to note that my surprises are not intended to be predictions, but rather events that have a reasonable chance of occurring despite being at odds with the consensus. I call these "possible-improbable events." In sports, betting my surprises would be called an "overlay," a term commonly used when the odds on a proposition are in favor of the bettor rather than the house.

The real purpose of this endeavor is a practical one — that is, to consider positioning a portion of my portfolio in accordance with outlier events, with the potential for large payoffs on small wagers/investments.

Since the mid-1990s, Wall Street research has deteriorated in quantity and quality due to competition for human capital at hedge funds, brokerage industry consolidation and a rapid decline in institutional commission rates. It remains, more than ever, maintenance-oriented, conventional and group-think — or "group-stink," as I prefer to call it. Mainstream and consensus expectations are just that and, in most cases, they are deeply embedded into today's stock prices.

It has been said that if life were predictable, it would cease to be life, so if I succeed in making you think, and possibly position, for outlier events, then my endeavor has been worthwhile.

Nothing is more obstinate than a fashionable consensus, and my annual exercise recognizes that, over the course of time, conventional wisdom is often wrong. As a society and as investors, we are consistently bamboozled by appearance and consensus.

Ayn Rand put it well:

"You can ignore reality, but you cannot ignore the consequences of ignoring reality."

Too often, we are played as suckers, as we just accept the trend, momentum and/or the superficial-as-certain truth without a shred of criticism. Just look at those who bought into:

The bottom line... as Bob Dylan wrote, "For the loser now may be later to win."

But enough of the rant — the weekend is almost upon us — and with it the New Year emerges next week.

BY Doug Kass · Dec 27, 2024, 7:37 AM EST

The S&P Short Range Oscillator slipped from -5.39% to -4.77%.

BY Doug Kass · Dec 27, 2024, 7:15 AM EST

Wolf Street howls about the housing recession on the West Coast: "San Francisco House Prices Drop Back to 2019, Condo Prices to 2015, as Tech Jobs in the City & Silicon Valley Evaporate after Drunken Hiring Binge"

BY Doug Kass · Dec 27, 2024, 7:00 AM EST