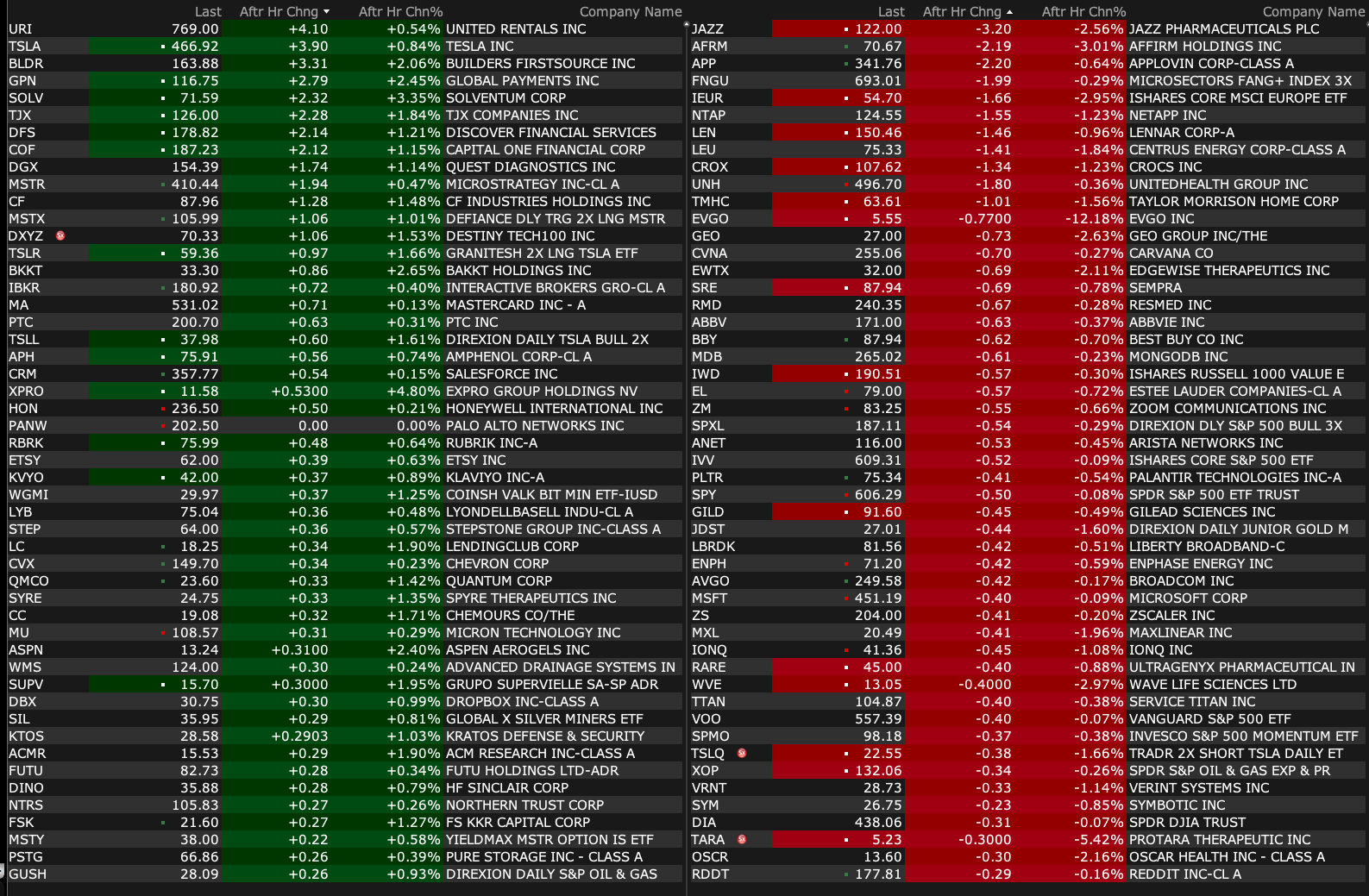

Monday's After-Hours Movers

As of 4:19 p.m. ET:

BY Doug Kass · Dec 16, 2024, 4:35 PM EST

As of 4:19 p.m. ET:

BY Doug Kass · Dec 16, 2024, 4:35 PM EST

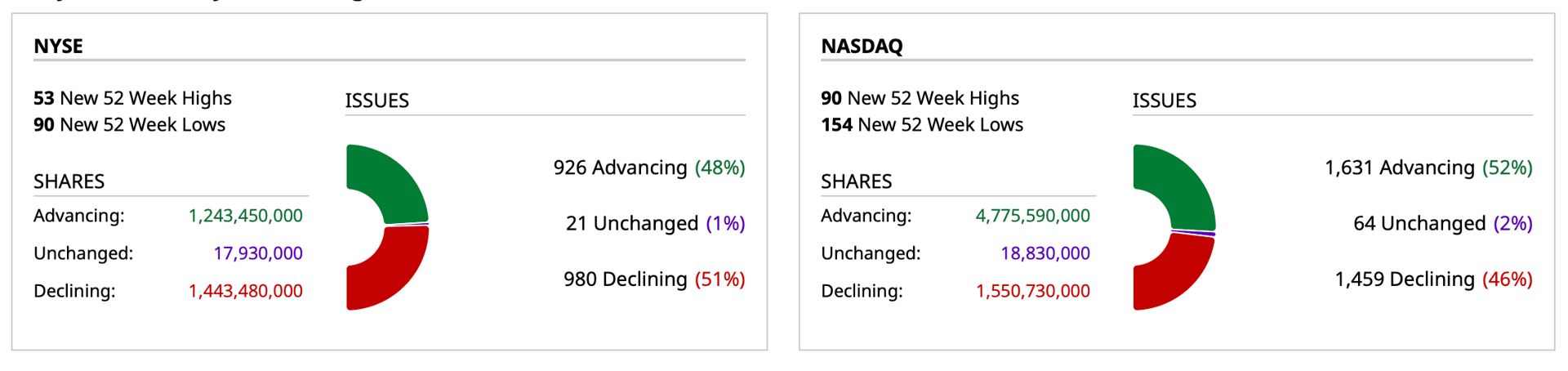

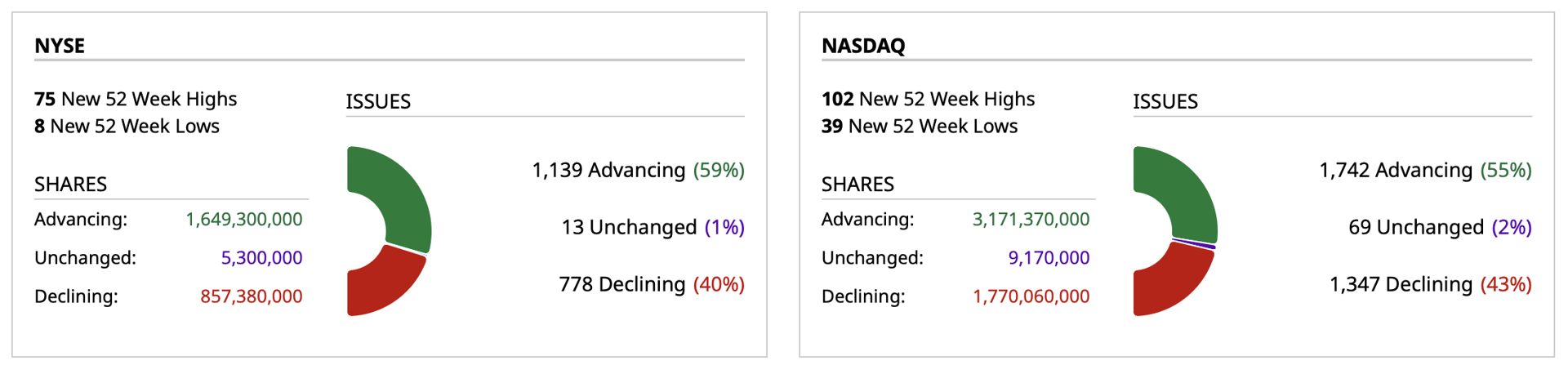

Closing Breadth

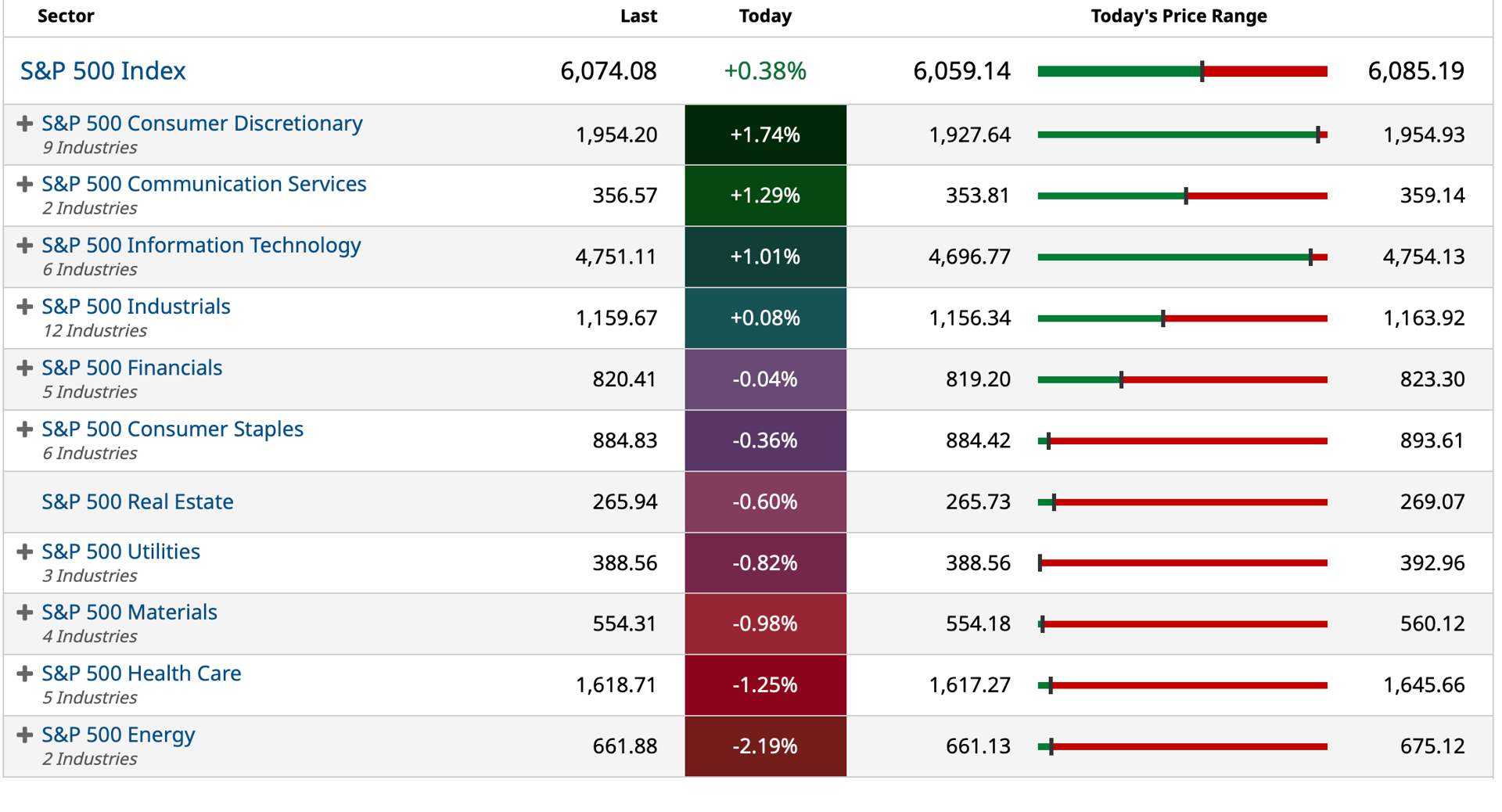

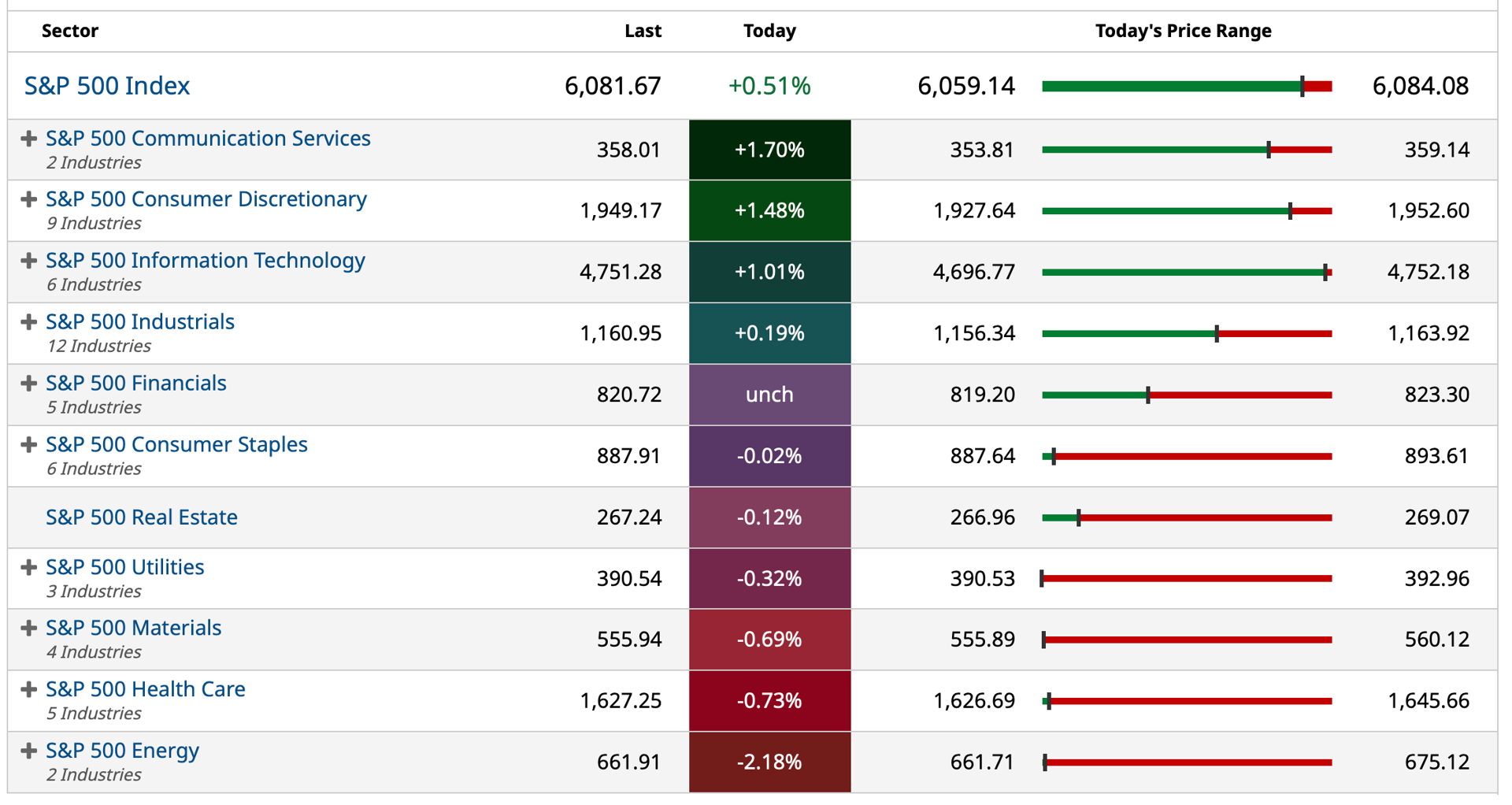

S&P Sectors

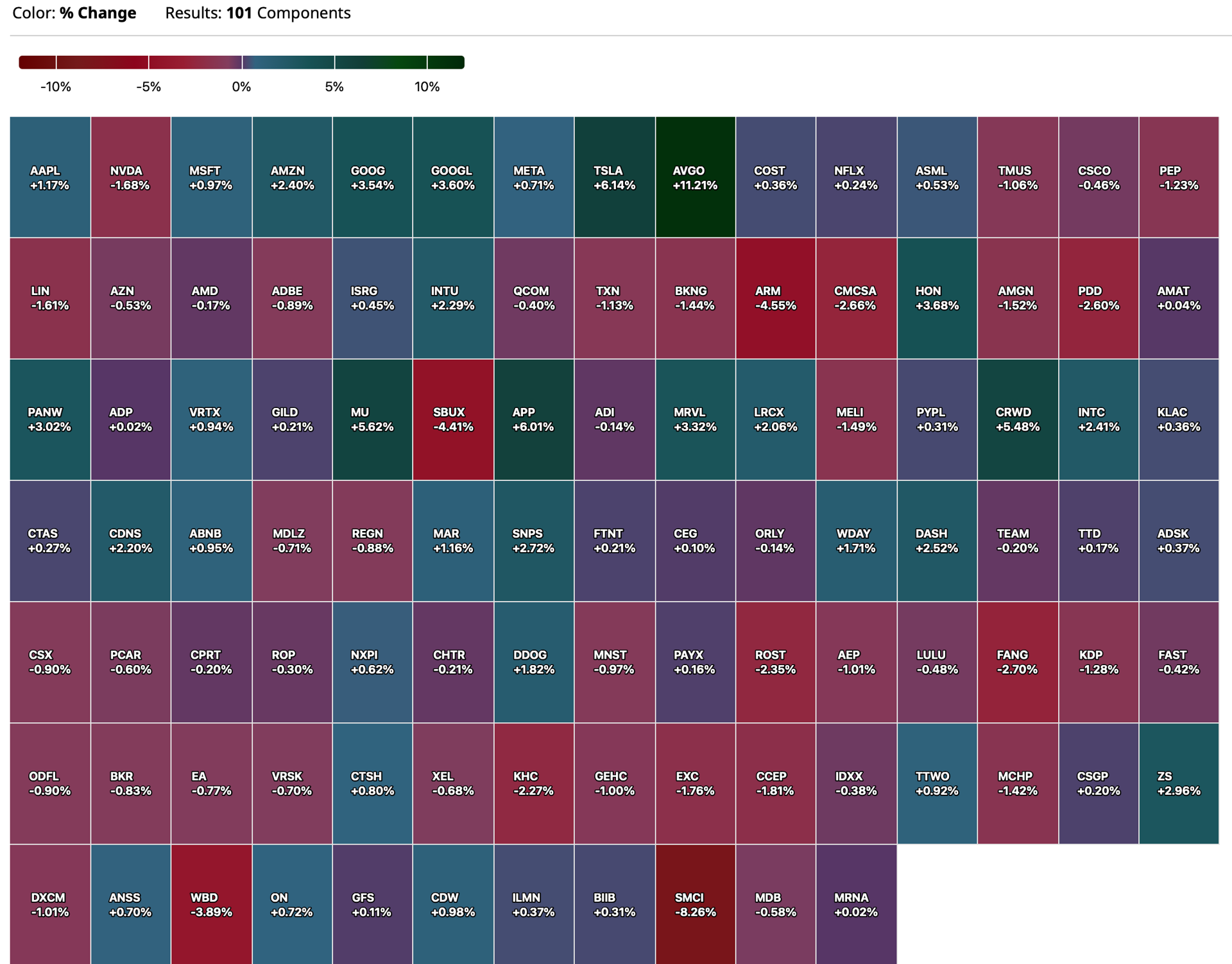

Nasdaq 100 Heat Map

BY Doug Kass · Dec 16, 2024, 4:23 PM EST

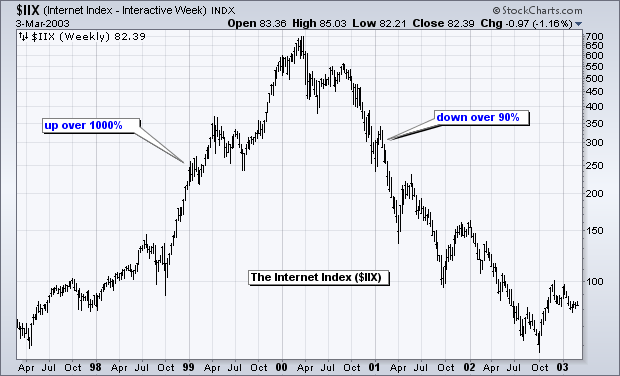

* "There are no new eras; excess moves are never permanent"

* I am starting to get a Wired Magazine feeling (circa late 1990)....

I am starting to get a Wired Magazine feeling (late 1990s)... Remember Peter Schwartz and Peter Leyden's "The Long Boom: A History of the Future (1980-2020)"? "We're Facing 25 Years of Prosperity, Freedom and a Better Environment for the Whole World. You Got a Problem With That?"

Unfortunately, during the next 25 years, we faced not only an 80% drawdown starting in 2000 (as the dot-com boom fizzled) but also "The Great Decession" of 2007-09 (in which the S&P Index fell to 666).

Which brings us to an interview with Merrill Lynch's Hyzy on CNBC (with Judge Wapner), in which Hyzy says he sees "a powerful new bull market and new paradigm lies ahead in 2025... as an asset light tech sector leads stocks higher."

I raise Merrill Lynch alum Hyzy one Bob Farrell (who also cut his teeth at Merrill Lynch):

Farrell's Lesson #3. There are no new eras—excesses are never permanent

Translation: There will be a hot group of stocks every few years, but speculation fads do not last forever. In fact, over the last 100 years, we have seen speculative bubbles involving various stock groups. Autos, radio and electricity powered the roaring '20s. The nifty-fifty powered the bull market in the early 70s. Biotechs bubble up every 10 years or so and there was the dot-com bubble in the late '90s. “This time it is different” is perhaps the most dangerous phrase in investing. As Jesse Livermore puts it:

A lesson I learned early is that there is nothing new in Wall Street. There can't be because speculation is as old as the hills. Whatever happens in the stock market today has happened before and will happen again.

BY Doug Kass · Dec 16, 2024, 4:00 PM EST

*Rates rise, breadth so-so and breathless technology

At 3:15 p.m. ET, S&P cash was +32 handles.

Here are today's "Things":

* Very early this morning, I sold SPY $605.79 and QQQ $532.62.

* Added to ELAN long at $12.12.

* Shorted more AAPL $250.47 and AXP $304.01.

BY Doug Kass · Dec 16, 2024, 3:45 PM EST

Only four sectors participating on the upside, the remainder not only negative but near day lows:

BY Doug Kass · Dec 16, 2024, 3:35 PM EST

BY Doug Kass · Dec 16, 2024, 3:25 PM EST

From my pal, Rosie:

Memo From the Chief Economist:

Risky Business

The Bottom Line: We are in this strange backdrop where investors believe that there is no recession risk, no risk of earnings disappointments, no risk of equity selling by anyone, and zero risk of any credit defaults. We are in a once-in-a-lifetime situation where the concept of risk has been totally distorted — an investment world where there is no more differentiation between what has traditionally been risky and what is riskless.

Heading into 2025, the question must be addressed: what is a razor-thin equity risk premium (ERP) telling us? Investors willingly investing in the market today, in this environment, can only rationally be doing so if they are in it for the long run; never to sell under any circumstances. If that is your belief, then go right ahead. This is your sort of market. But if you believe that the ERP should be positive or anywhere close to the long run mean of 300 or 400 basis points, then, arithmetically, only three things can happen: interest rates have to come down, the equity market will have to come down, or some combination thereof. The valuations in the S&P 500 are such that +20% average annualized earnings growth is now being embedded in the pricing of the index — that is nearly triple the historical norm over half-decade cycles based on a century of data. I know there are folks out there who believe +20% average annual profits growth is doable — even though it is a 1-in-20 event historically speaking (it did happen in the mid-to-late 1990s) — and who believe that the ERP is appropriate. Again, to believe that is to believe there will never be any sellers. That is what equity portfolio managers also believe, because they are running their funds with barely more than 1% cash ratios, unheard of in the annals of financial history.

Because I believe that earnings growth estimates are too lofty, even with the AI craze and how it will change the world, and because I believe that the ERP should be above zero (as risky assets should command a risk premium against riskless assets), I am still largely on the sidelines. There’s the rub. If you believe that it is appropriate that the ERP is zero, or close to zero, then you must believe, in the name of logic and consistency, that the S&P 500 has emerged as a “riskless asset” — treating it as one would a Treasury bill in terms of capital risk — and that the constituents in the index collectively have become zero-beta stocks. Sorry, but I am not there. There is new-era thinking and then there is wishful thinking.

I also believe that by the time the top is turned in, there will be a mad scramble to get out because the two extreme primal emotions of investing, fear and greed, never go out of style. Greed has been working, and may continue to work in 2025, but as Herb Stein famously posited, “If something can’t go on forever, it will stop.” The problem is that because there is so much overexposure to equities on household balance sheets, everyone is going to be trying to bail out together with precious few buyers on the other side, because there aren’t exactly a whole lot of folks out there with a cash position like mine (oh, save for Warren Buffett… the two of us will be there, rest assured, to be the providers of liquidity when the time comes). I don’t know when that time will be, but I do know it will come. And as we saw with the internet, the impact of AI will exert a powerful influence on our lives, both personally and professionally. But the stock market will be on a different plane as investors confront a landscape where multiples contract, as they always do once the cycle shifts to a new chapter, when there is no more good news to be priced in since it has already been fully incorporated (and at peaks, more than fully priced in).

As was the case with the internet in the mid to late 1990s, artificial intelligence has supercharged the stock market, and the capex surge is becoming increasingly evident with mega expansion spending into data centers and specialized microchips. JPMorgan estimates that capital spending and research by just the Magnificent Seven will be $500 billion in the next year, with a total corporate AI spend of more than $1 trillion in the U.S. — bigger than the defense budget. At issue, which we see time and again when the technology curve hits an inflection point, investors see the capex boom (R&D spending is definitely booming) and then anticipate fat returns from this capital deployment. The problem is when investors start to over-anticipate. That is the real question — where are we in this cycle? We know what happened when the gig was up in the winter of 2000, but is this 1996? 1997? 1998? 1999? The internet bull market that morphed into a mania and then into a huge bubble began in the summer of 1995, but the party went on for nearly five years.

To reiterate, an ERP at or near zero is a sign that investors in today’s world are willing to treat equities as a riskless asset. No different than T-bills. Except for the simple reality that T-bills carry no capital risk at all. Equities do. This is the extent to which the equity market has become a true believer in the phrase “it is different this time.” This also happened in the mid-to-late 1990s. A similar phenomenon exists today in the bond market, where investors are treating investment-grade corporate bonds as if they are Ginnie Mae mortgage bonds — except that one has a historic default rate of 1.5% and the other 0%.

In other words, the concept of risk has been totally turned on its head these past 18 months. We are living through a rare period in financial history. But these cycles don’t tend to end very well. More like in tears.

I am still not participating, but I do recognize that all exponentially rising markets go further than we think, and this one is no different than the others in the past. But because they do not correct by moving sideways, and I can’t possibly know when this mania will end (let’s call it a mania going forward, not a bubble, because only a fool would say this is not a mania), I am still largely (not at all totally) on the sidelines. As I said, when everyone ends up heading for the exits when this cycle ends and finds out there are few buyers on the other side, things will turn very ugly. My biggest concern is the undue 70% concentration of equities on household balance sheets (roughly 10% are in bonds). Retail investor flows into passive indexed equity funds are off the charts — this blind investing is now fast approaching 60% of the entire stock market capitalization. And institutional investors are sitting on record low liquidity ratios of barely more than 1% — think of what that means if client redemptions ever do resurface. And they always resurface because fear and greed are part and parcel of the cycle at extremes… these primal emotions never go away, and we have to add that the equity market is, after all, an asset class that is speculative by its very nature. I am still very much in low-risk/low-beta/low-cyclicality mode and interested primarily in the preservation of capital and cash flows. Nothing wrong from my end with a barbell of 4.5% yielding T-bills and 5.5% yielding government-guaranteed mortgage bonds. Municipal bonds with an effective after-tax yield of 6%-plus also deserve a look. And then throw in gold which remains in a full-fledged bull market whose tailwinds remain fully intact. Safe and sound.

BY Doug Kass · Dec 16, 2024, 3:10 PM EST

BY Doug Kass · Dec 16, 2024, 2:55 PM EST

At 4.41%, the yield on the 10-year U.S. note is at the day's high and six basis points above its morning low.

This is the sixth consecutive day that Treasury yields have climbed.

I remain astounded by the strength in the indices.

Meanwhile, RSP (the equal weighted S&P Index) is now down on the day.

BY Doug Kass · Dec 16, 2024, 2:40 PM EST

From "Meet'" Bret Jensen:

Hope things are better in the rest of the country dept.

Don't know about rest of the nation, but economic activity seems to be seeing a big downturn in Delray Beach recently. Passed by Brule Bistro early evening yesterday. Only one person at the 15-seat bar. This time last year, it was hard to find a single seat. Same story at Joseph's next door, whose business is down 40% to 50% compared to last year based on conversation with owner. Only other person there was a real estate broker lamenting how nothing is moving right now and some major supply in the pipeline. Rooms at The Ray can be had for the coming weekend for just over $250/night. Last year it was $450 to $500/night if you were lucky enough to reserve. Locals are hoping the snowbirds are just late in arriving this year as weather has been pretty good so far in the Northeast. I have my doubts.

BY Doug Kass · Dec 16, 2024, 2:25 PM EST

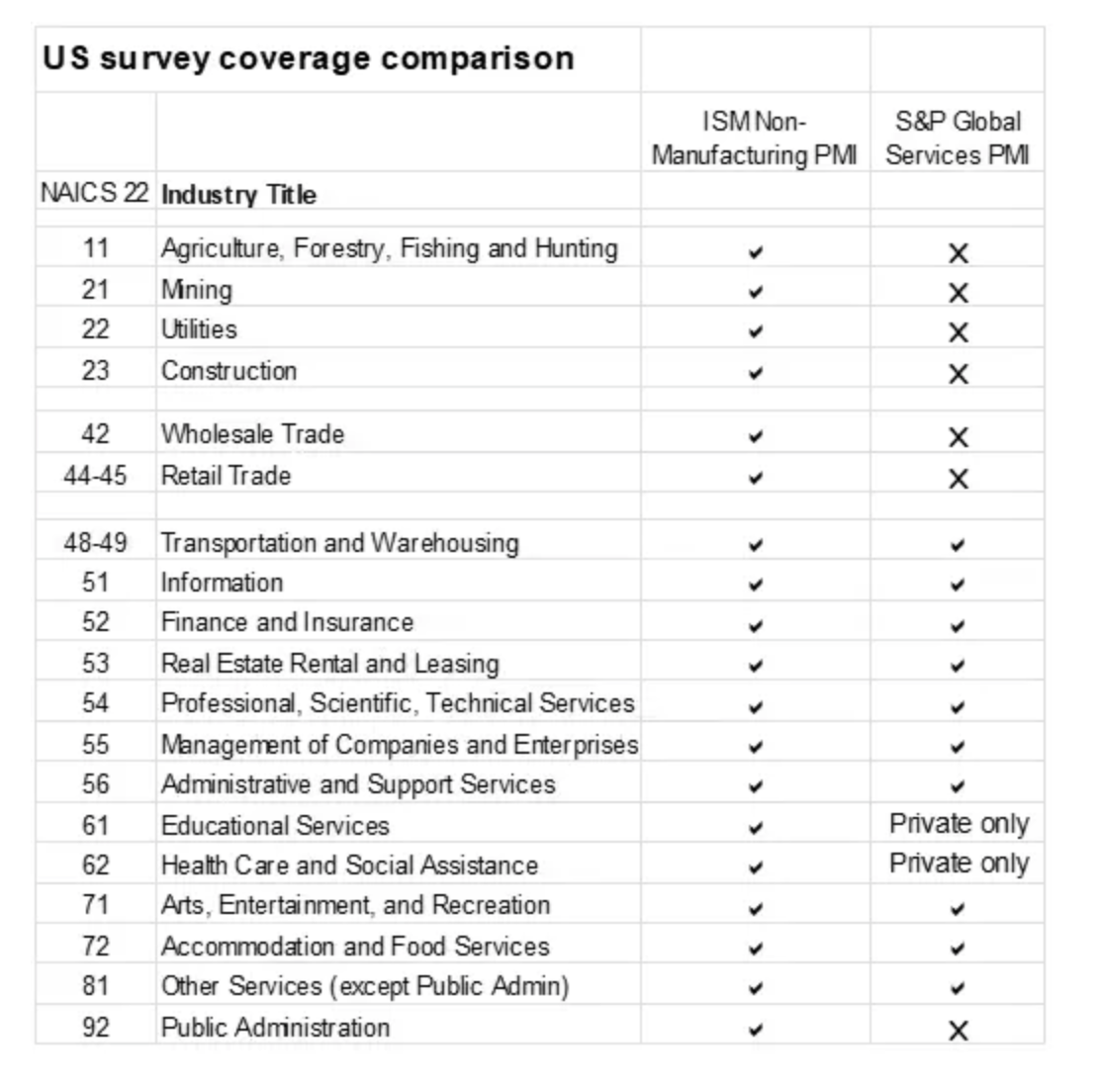

I forgot to remind readers in my last note (h/t DDM and thanks for reminder) something I’ve pointed out many times before: That the S&P Global services PMI does not include retail and construction (along with wholesale trade and mining). We know those two sectors have been much more mixed depending on one’s customer and what is being constructed (data center or multi-family building or EV battery plant). The ISM services index does include these sectors and I’m not sure why S&P Global does not.

BY Doug Kass · Dec 16, 2024, 2:15 PM EST

From Peter Boockvar:

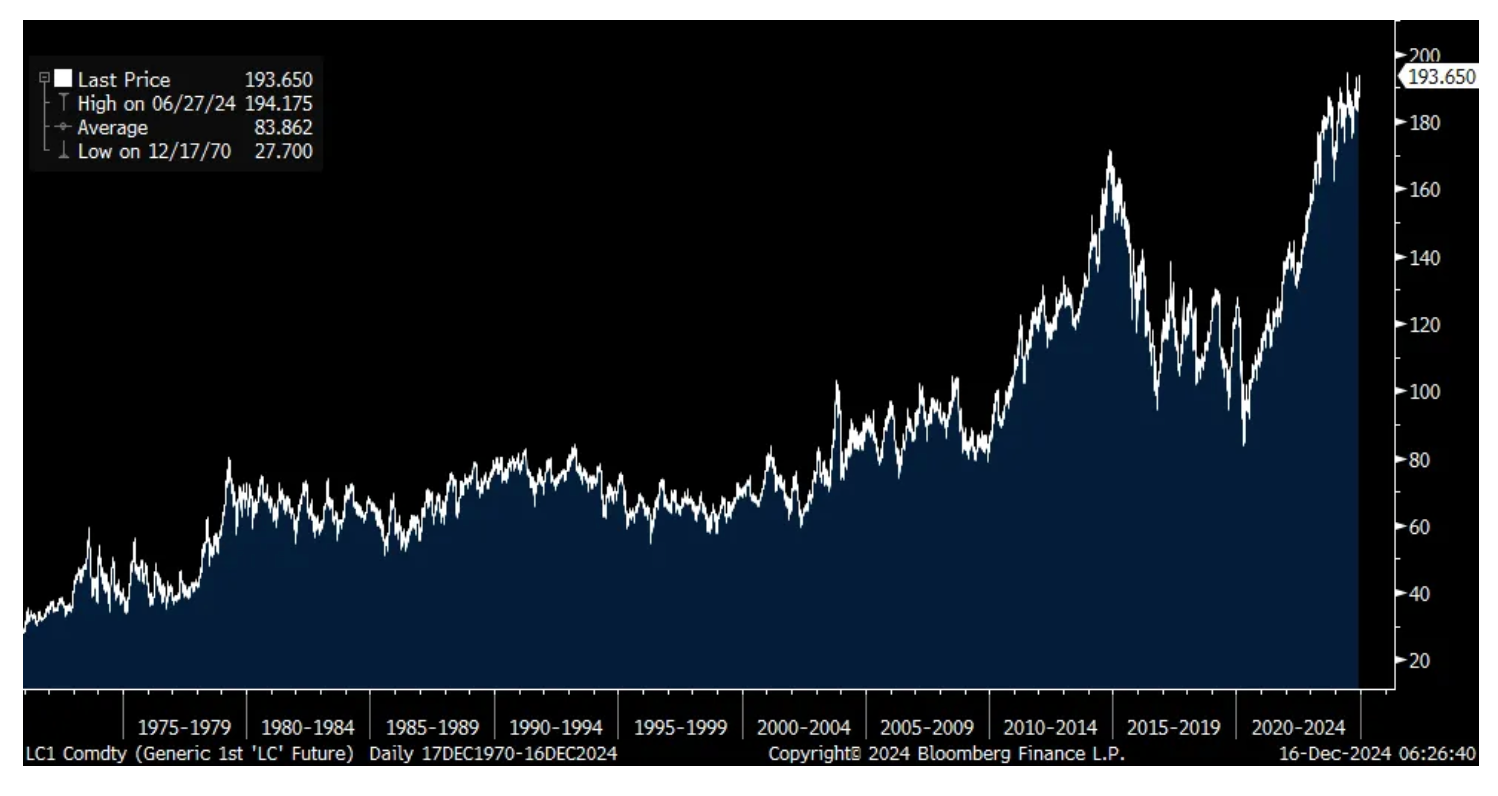

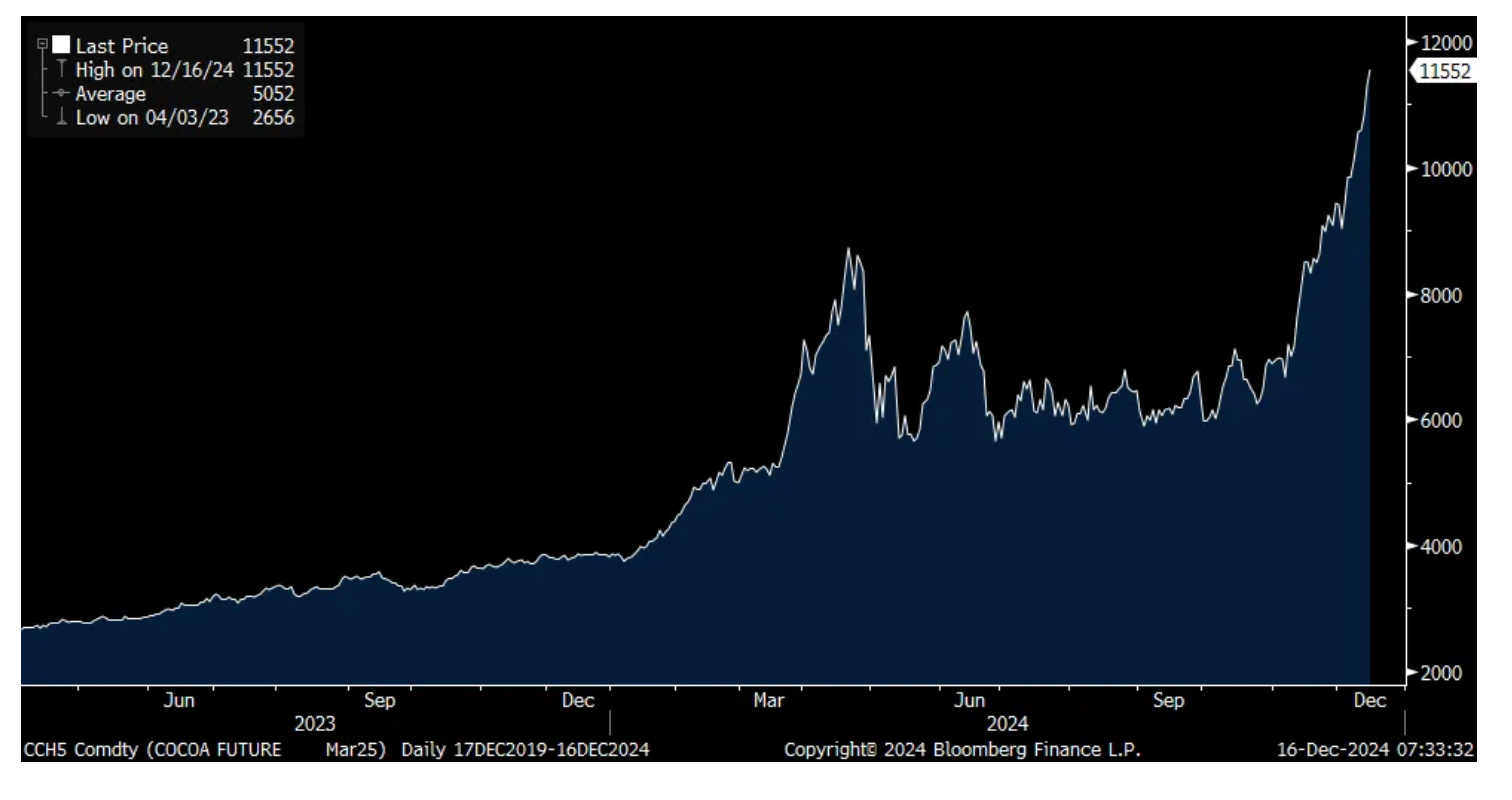

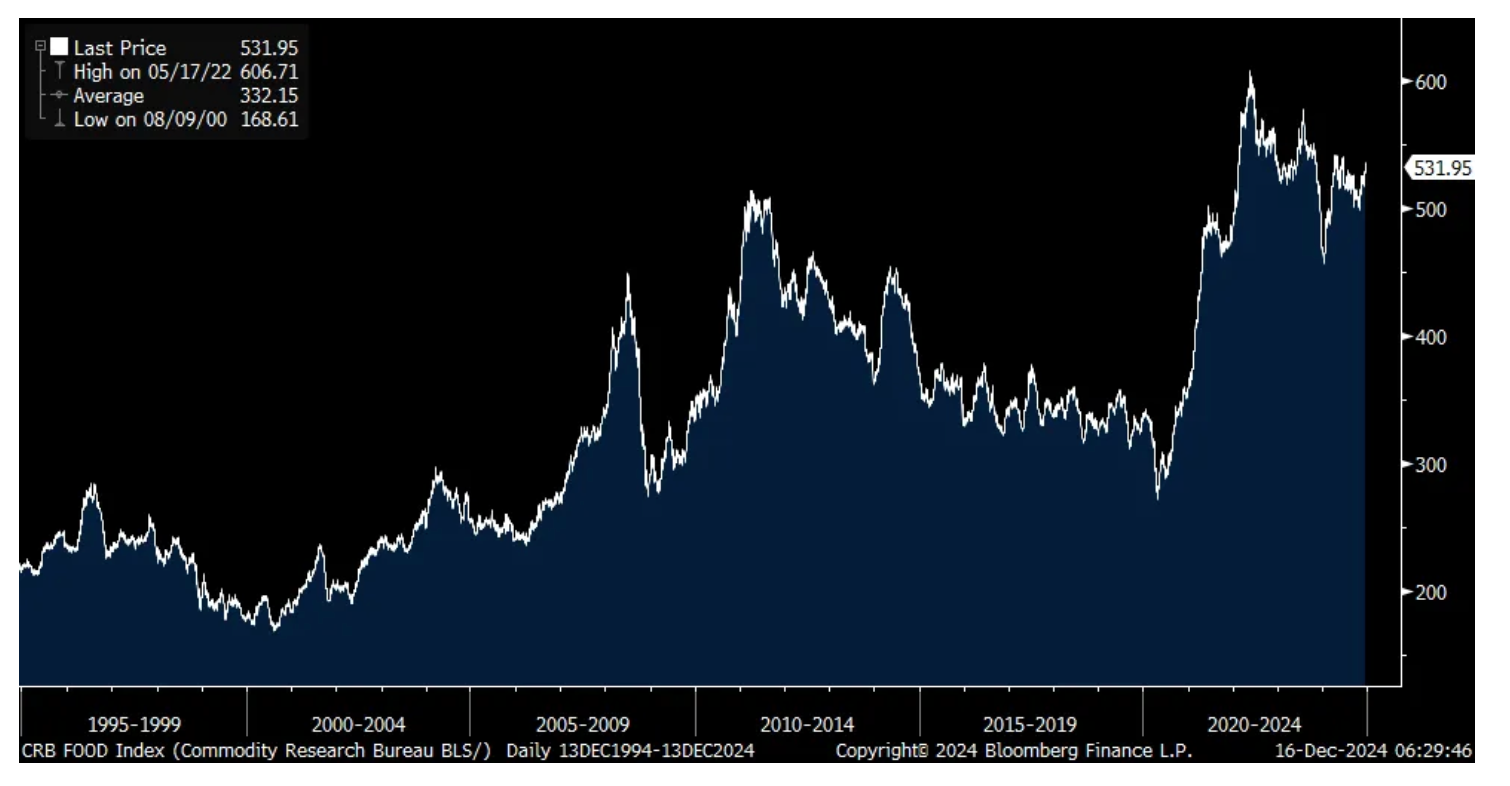

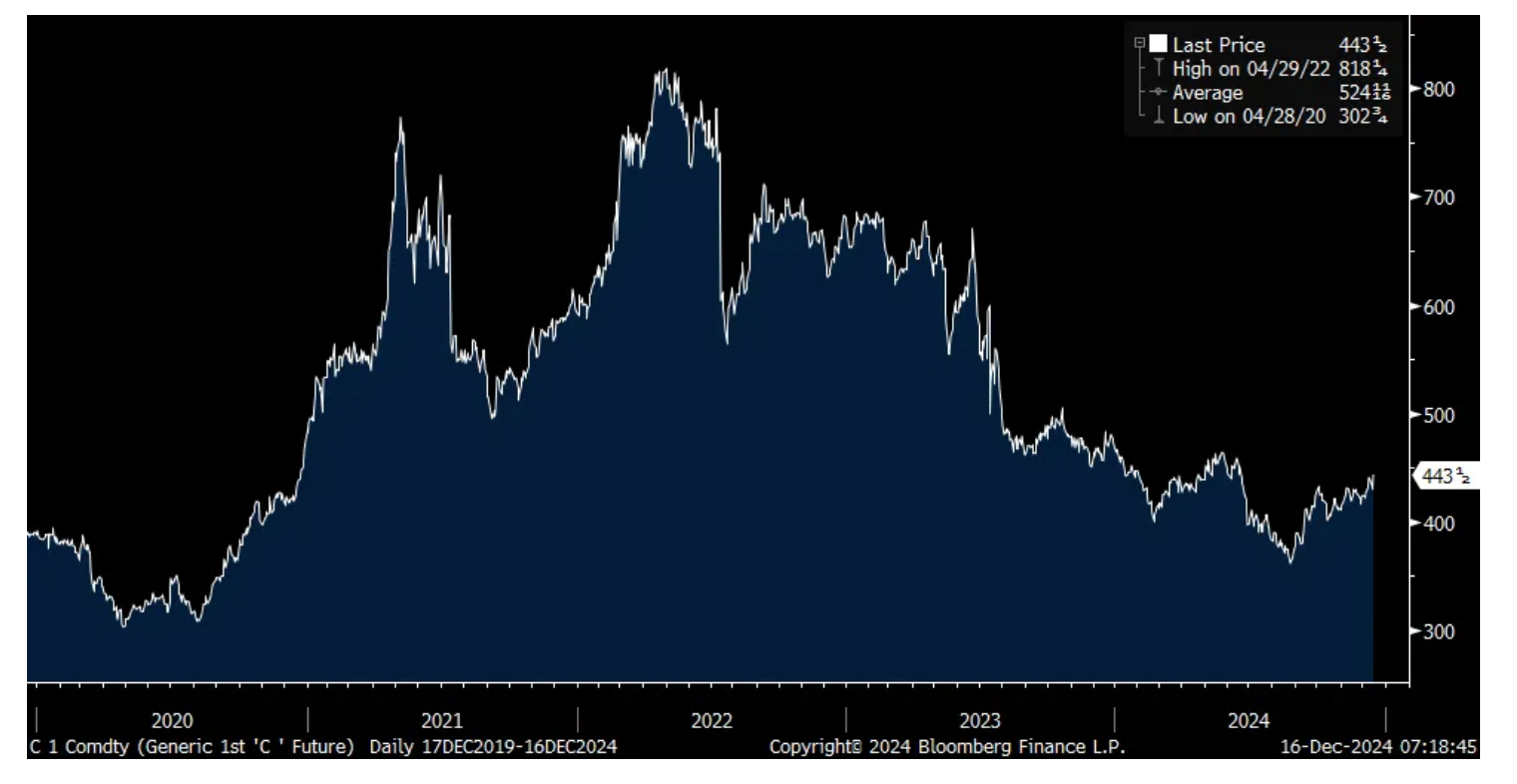

Last week coffee prices, this week cattle and cocoa/Sentiment/PMI's and China

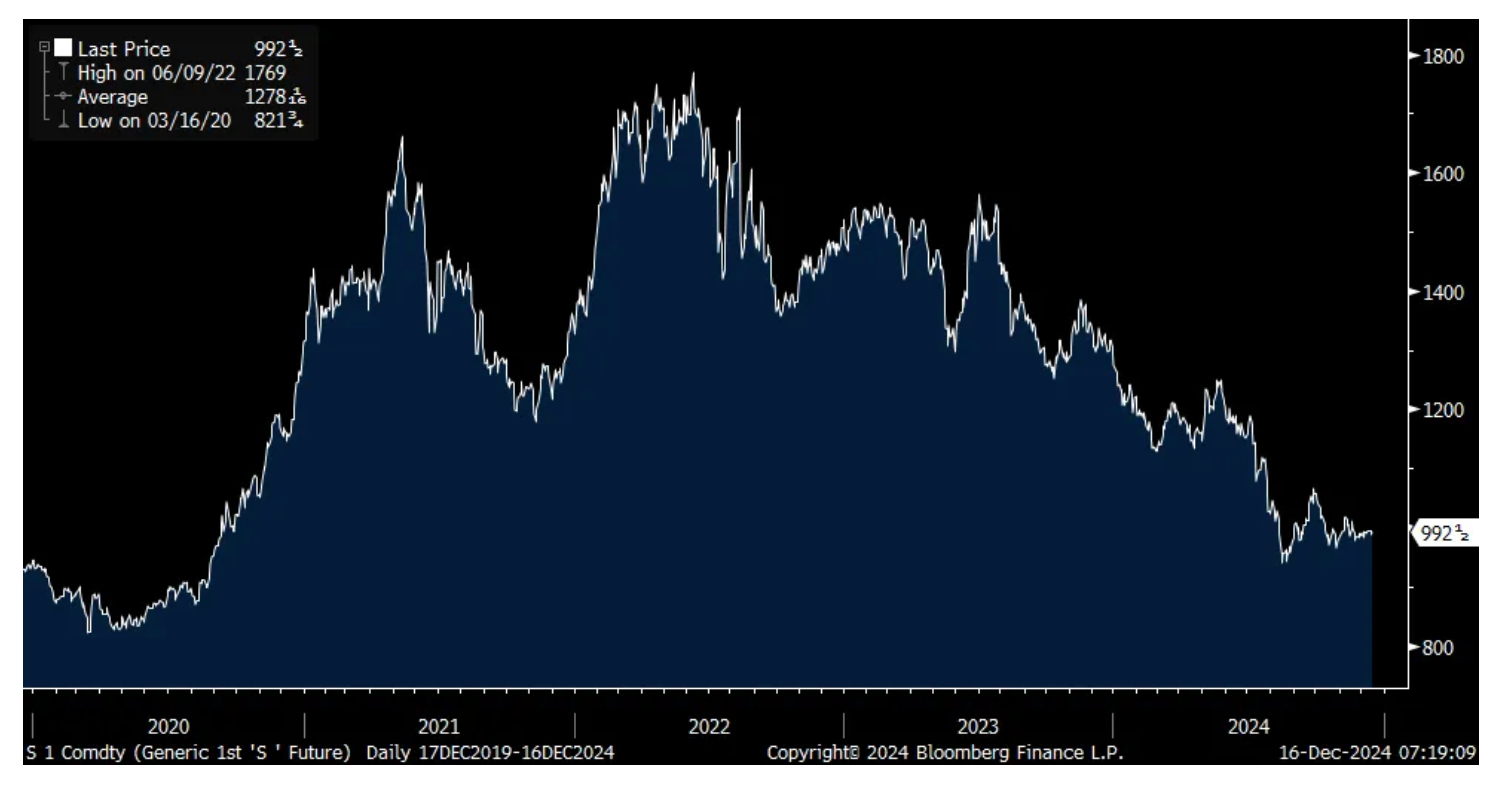

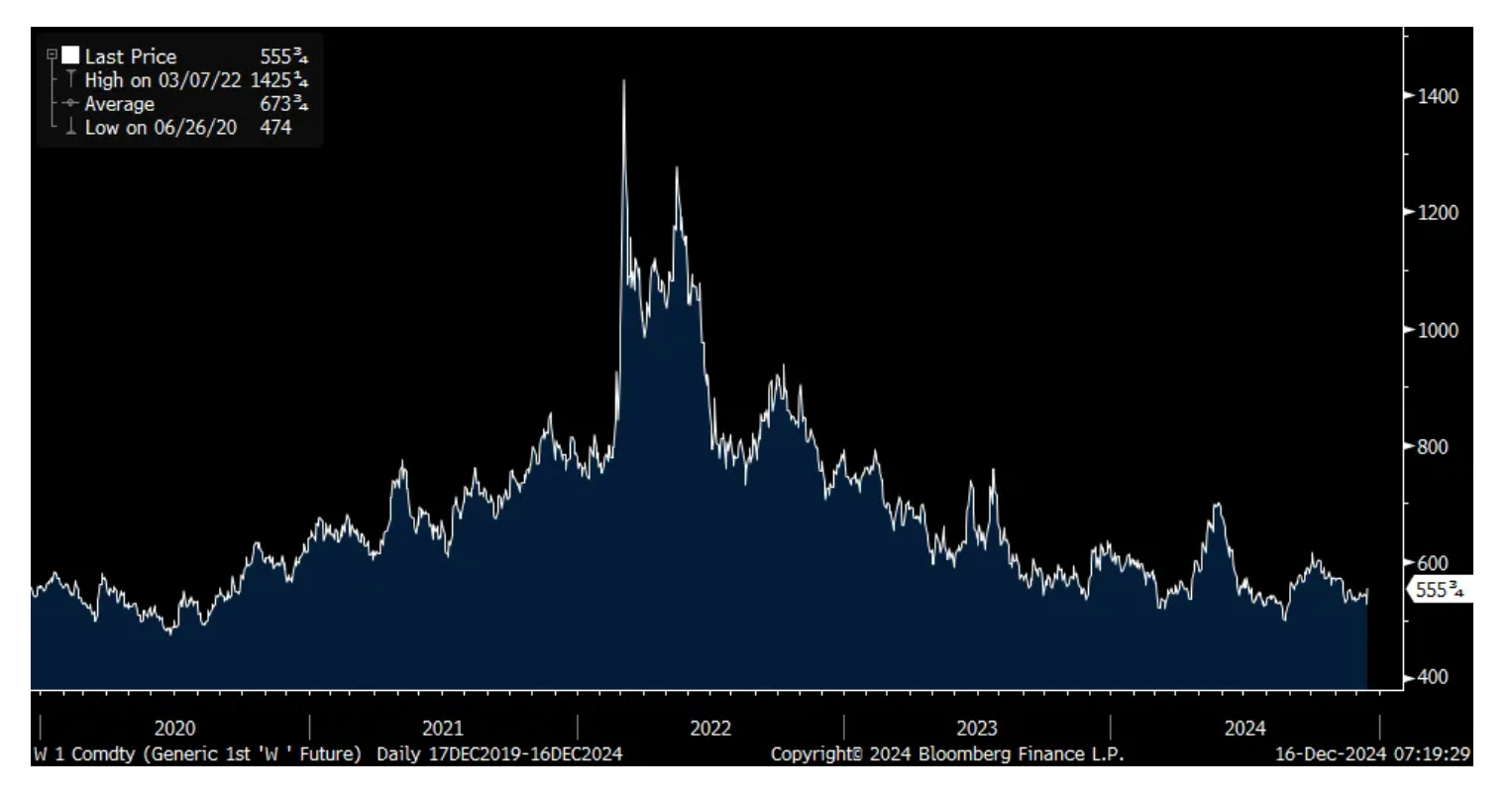

We saw last week coffee prices go to a record high and today cattle prices are as well at almost $194 per pound. So are cocoa prices. Food inflation has not gone away and that steak is only getting more expensive but corn, soybeans and wheat prices remain well off their highs and why the CRB Food index is not at its highs. We remain bullish on ag, particularly the fertilizer stocks, in part expecting a move higher in those particular row crops off depressed levels.

Cattle

Cocoa front month contract

CRB Food Index

Corn

Soybeans

Wheat

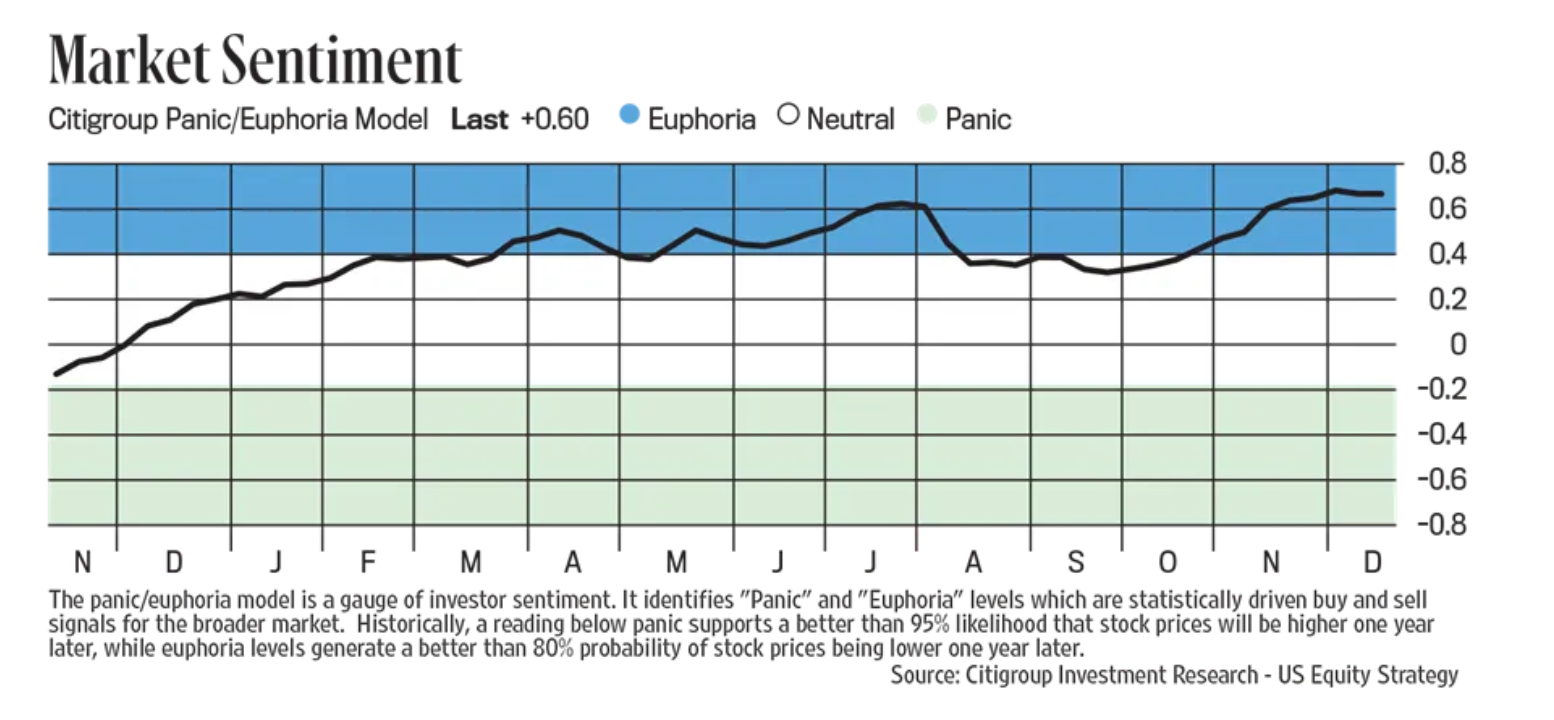

An update on stock market sentiment, the bullishness remains giddy but a hair less so. The Citi Panic/Euphoria index remains well in Euphoria territory at .60 but down a touch from .62 last week. Above .41 is statistically significant according to Citi. Investors Intelligence last week said Bulls fell by .6 pts w/o/w to a still very high 62.3. Bears are at just 16.4 vs. 16.1 in the week before. The 45.9 pt spread is well above the 40 level that would be consider extreme. The NAAIM (Nat'l Assoc of Active Investment Mgrs) Exposure Index is at 99.24, the highest since early July. Above 100 is considered all in from an exposure perspective.

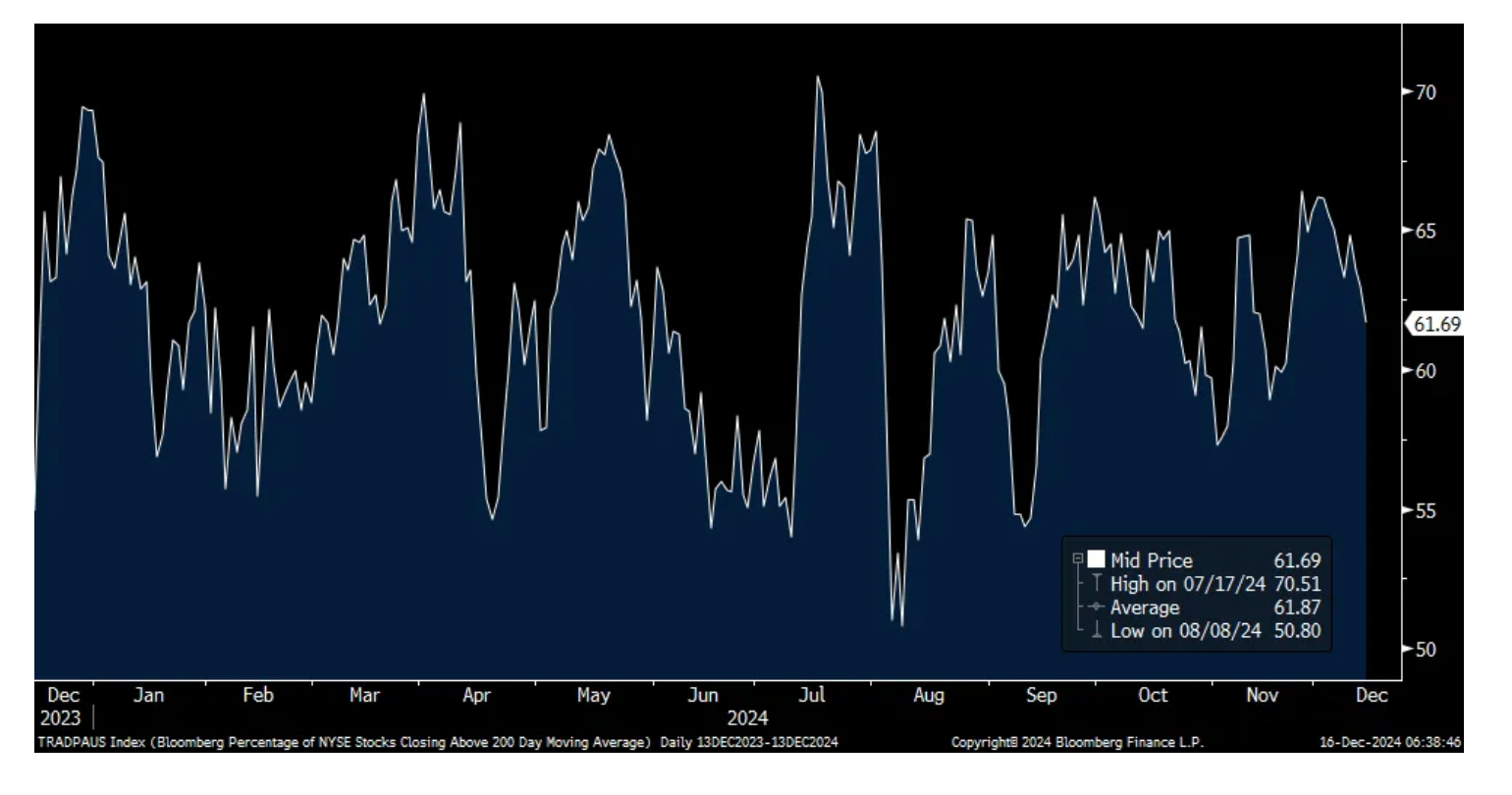

This comes as the market has gotten much more selective again as there have been more stocks down than up over the past two weeks. On the NYSE, just 62% of stocks are above their 200 day moving average which is exactly at the average over the past year but off the July highs at 70.5% and down 8 out of the last 9 days. Either the big names catch up to the rest of the market on the downside or we get a broadening out again to the upside. Or, maybe this either or market just continues on frustratingly.

Percent of NYSE stocks trading above its 200 day Moving Avg

The December PMIs started to roll out today and they remain mixed. Japan's composite index rose to 50.8 from 50.1 with services still leading the growth with this component at 51.4 from 50.5 vs manufacturing at 49.5 vs 49. Ahead of the BoJ meeting this week, S&P Global said "Stubborn inflation held back a stronger expansion of the Japanese private sector in December. Average input prices rose markedly again, and at the steepest rate for four months, with anecdotal evidence placing particular emphasis on the impact of the weakness of the yen in relation to inputs sourced from abroad. As such, the pace of selling price inflation also quickened on the month and was the fastest since May." JGB yields rose to near their recent highs but the yen is down a touch while the Nikkei was flat. The BoJ should absolutely be raising rates this week but no surprise if they drag their feet again.

Australia's index slipped a touch below 50 at 49.9 from 50.2 with services at 50.4 vs 50.5 and manufacturing at 48.2 from 49.4.

India remains the standout with its composite index at 60.7 vs 58.6 in November with services at 60.8 and manufacturing at 57.4, both higher m/o/m.

In the Eurozone, services rebounded to back above 50 at 51.4 from 49.5 and above the estimate of no change. Manufacturing remained though in the doldrums at 45.2, unchanged with November. While the ECB keeps cutting rates mostly over their worry about economic growth, S&P Global said this on inflation, "input costs rose at a faster pace for the third month in a row, and selling prices followed suit. Higher wage agreements are partly to blame, as businesses pass these costs on to customers."

The UK December PMI held steady at 50.5 with also services well outperforming manufacturing. The services component was 51.4 vs 50.8, offsetting manufacturing at 47.3 vs 48. S&P Global sounded downbeat on the UK economy, even though it is outperforming Germany and France. "Businesses are reporting a triple whammy of gloomy news as 2024 comes to a close, with economic growth stalled, employment slumping and inflation back on the rise. Economic growth momentum has been lost since the robust expansion seen earlier in the year, as businesses and households have responded negatively to the new Labor government's downbeat rhetoric and policies. Business confidence has sunk to a two year low as companies weigh up a tougher outlook for sales alongside rising costs, notably for staff as a result of changes announced in the Budget. The survey's price gauges are indicating that inflation is turning higher again."

Also of note, "Firms are responding to the increase in National Insurance contributions and new regulations around staffing with a marked pull-back in hiring, causing employment to fall in December at the fastest rate since the global financial crisis in 2009 if the pandemic is excluded."

You can't tax and regulate yourself to prosperity.

Bond yields are down slightly in Europe while the euro is down a bit too while the pound is up. The BoE meets this week and is not expected to cut rates again. Stocks in the regions are mostly red.

French yields in particular are down about 1-2 bps across its curve as they now have a new Prime Minister in Francois Bayrou, a supposedly seasoned politician that should last.

Back to Asia, China reported its November data and most importantly in my opinion, the decline in home prices has slowed. For new homes, prices fell .20% m/o/m, the smallest amount since June 2023. For existing homes, prices fell .35% m/o/m, the least since May 2023. Stabilizing the residential housing sector and seeing a stop to the fall in property prices has been the government's goal and hopefully we're another step to getting there. If so, that would help to stabilize consumer confidence too and who have a massive pool of savings.

Also out, retail sales in November were softer than expected, up 3% y/o/y instead of rising 5% as expected and after a 4.8% rise in October but Singles Day this year was in October vs the usual November time period so that likely pulled forward some sales. Industrial production grew by 5.4% y/o/y as forecasted and vs 5.3% in the month before. Not surprisingly, property investment remained soft, down 10.4% ytd y/o/y.

With still skepticism with the Chinese economy, stocks were lower as were bond yields. The 10 yr yield in fact is down to 1.72% and has fallen precipitously in 2024. Investors want instantaneous satisfaction with policy initiatives, but I do believe China is taking the right policy steps on housing and local government debt, however long it takes to play out. That said, Xi must embrace the private sector and let it do its entrepreneurial thing if the country is going to have healthy growth.

Chinese 10 yr bond yield

BY Doug Kass · Dec 16, 2024, 2:04 PM EST

Adding to ELAN under $12.10.

BY Doug Kass · Dec 16, 2024, 1:36 PM EST

Michael Saylor on CNBC:

BY Doug Kass · Dec 16, 2024, 12:40 PM EST

Energy is dreadful (I have zero involvement in oil), financials are weak (JPM and SCHW leading to the downside), market breadth is uninspiring (RSP, the equal-weighted S&P index, is flat) but the overall averages and technology (save Nvidia NVDA) are the "world's fair."

BY Doug Kass · Dec 16, 2024, 12:05 PM EST

From Douglas Cassel:

No one is better than Doug K in pointing out the problems with the U.S. economy and stock market. Hence when the markets continue to go up in spite of the many real issues, I cast about trying to justify why. I cannot just write it off to animal spirits and madness of crowds, as things have been going on too long for that.

Instead, I think it has more to do with the old joke about they guy changing his shoes when he and a friend encounter a bear. "I don't have to outrun the bear, I just have to outrun you." The real propulsion of the USA markets may be because as bad as things might be here, they are far worse elsewhere. Germany and France, which are the heart of the EU, are undergoing existential economic problems. The bargain struck with the German people, economic success in exchange for high taxes and constrained standard of living, is falling apart. The French and the rest of the EU are undergoing similar problems.

China is seeing the collapse of their export driven, mercantilistic system as the rest of the world has decided enough is enough. The attempts at stimulating domestic consumption are the equivalent of pushing on a string, as it will require a fundamental rewiring of the entire economy.

The developing world remains just that, too diverse to classify quickly, but with India stagnating and no other emerging economy actually emerging, no great place to invest.

The universal solution of printing money, now pretty much adopted by everyone results in huge amounts of liquidity searching for a place to go.

As bad as things might be, the USA is the best house in a bad neighborhood. Perhaps analysis of US markets should concentrate more on how badly everyone else is doing in addition to our problems.

Is this analysis true? Will things continue? I don't know, but the protestations of the bears needs scrutiny too. This is one explanation.

BY Doug Kass · Dec 16, 2024, 11:51 AM EST

I am back from a board meeting.

Getting my sea legs back!

BY Doug Kass · Dec 16, 2024, 11:25 AM EST

Again, on Bloomberg, another guest is endorsing the notion that inflation will be contained.

I see it differently:

BY Doug Kass · Dec 16, 2024, 8:00 AM EST

I am short AEG $6.13) - the subject of a short report this morning by Spruce Point Capital Aegon Ltd. - Spruce Point Capital Management LLC

BY Doug Kass · Dec 16, 2024, 7:44 AM EST

* NVDA's share decline is growing more conspicuous both absolutely and to its tech brethren...

This short little blurb from Microsoft's MSFT CEO Satya Nadella is interesting.

It describes what happened with the whole AI boom perfectly, something I have referenced before. It is only 90 seconds long, so have a listen:

Apparently, they all got caught off guard in the beginning; nobody wanted to be left behind; they had the money and piled in with zero caution with no regard to how much they spent, and what they spent it on. These were also big projects, that are now largely completed. Therefore, they are no longer chip-constrained, which are his words. In fact, I suspect many have ordered chips well ahead and beyond what they needed for these projects. And from what he is saying, it also sounds like they can’t find the power to run all of this stuff, either. And it is not going to be cheap if they do find it (nor is the content they need to keep training on now that they will need to start paying).

The funny thing is he is basically slamming a lot of the stuff MSFT invested in at massive valuations, too. Does he even know? Sometimes I wonder, these companies are so big now they are like the U.S. government, does anyone know where the money goes? Like at the Pentagon, where they just failed their 7th audit in a row.

The key thing is demand for what these projects are selling has not followed. For example, Copilot is a mess: https://www.businessinsider.com/microsoft-ai-artificial-intelligence-bet-doubts-marc-benioff-satya-nadella-2024-11.

Even if there were significant end demand for what these projects were selling, chip demand would have to taper just due to the math of getting the lump sum of projects first and then just followed by what underlying demand allows for. Without booming end demand for the final product, I am not sure how the supply chain can keep growing to the moon. Especially from the levels it is at.

Coincidentally regarding what I just sent, on the costs of power and the costs (and scarcity) of incremental data to train on: https://energynow.com/2024/12/ai-wants-more-data-more-chips-more-real-estate-more-power-more-water-more-everything/

Side note: BRCM shares advanced by 20% on Friday, which is about $200 billion of market cap. All on a quarter where the slightly missed revenue and slightly beat EPS. But the CEO says the word “AI” a bunch of times on the conference call, retail and the algos love it and there you go, I guess.

BY Doug Kass · Dec 16, 2024, 7:30 AM EST

Dougie Kass

The four core bullish factors for the last half of 2024 cited by Tom Lee have been that (1) interest rates would decline, (2) breadth would broaden out and improve (and that IWM would rally dramatically), (3) Nvidia would lead the markets and (4) consensus S&P earnings are too low.

The opposite is occurring in all four variables... as equities climb.

BY Doug Kass · Dec 16, 2024, 7:15 AM EST

Apparently rising interest rates and eroding breadth are no longer market influences.

I am watching a Bloomberg guest early this morning who is dismissing both factors...

* The RSP (equal weighted S and P Index) is down by -3.5% from its high:

* The RSP (equal weighted S&P Index) is down by -3.5% from its high:

* Breadth stinks:

* Less than 50% of the S&P Index stocks remain above their 50-day moving average:

Perhaps the Bloomberg guest might consider paying more attention to Bob Farrell and his 10 Lessons on Investing.

BY Doug Kass · Dec 16, 2024, 7:00 AM EST

BY Doug Kass · Dec 16, 2024, 6:45 AM EST

Wolf Street howls about rising yields and inversion of the yield curve.

BY Doug Kass · Dec 16, 2024, 6:35 AM EST

I sold SPY at $605.52 and QQQ at $532.16 longs in the premarket.

BY Doug Kass · Dec 16, 2024, 6:25 AM EST

The S&P Short Range Oscillator is oversold at -4.1% (vs. -2.1%).

BY Doug Kass · Dec 16, 2024, 6:15 AM EST

BY Doug Kass · Dec 16, 2024, 6:05 AM EST

BY Doug Kass · Dec 16, 2024, 5:55 AM EST

Doomberg: "Is the Chip War Already Lost?"

BY Doug Kass · Dec 16, 2024, 5:45 AM EST