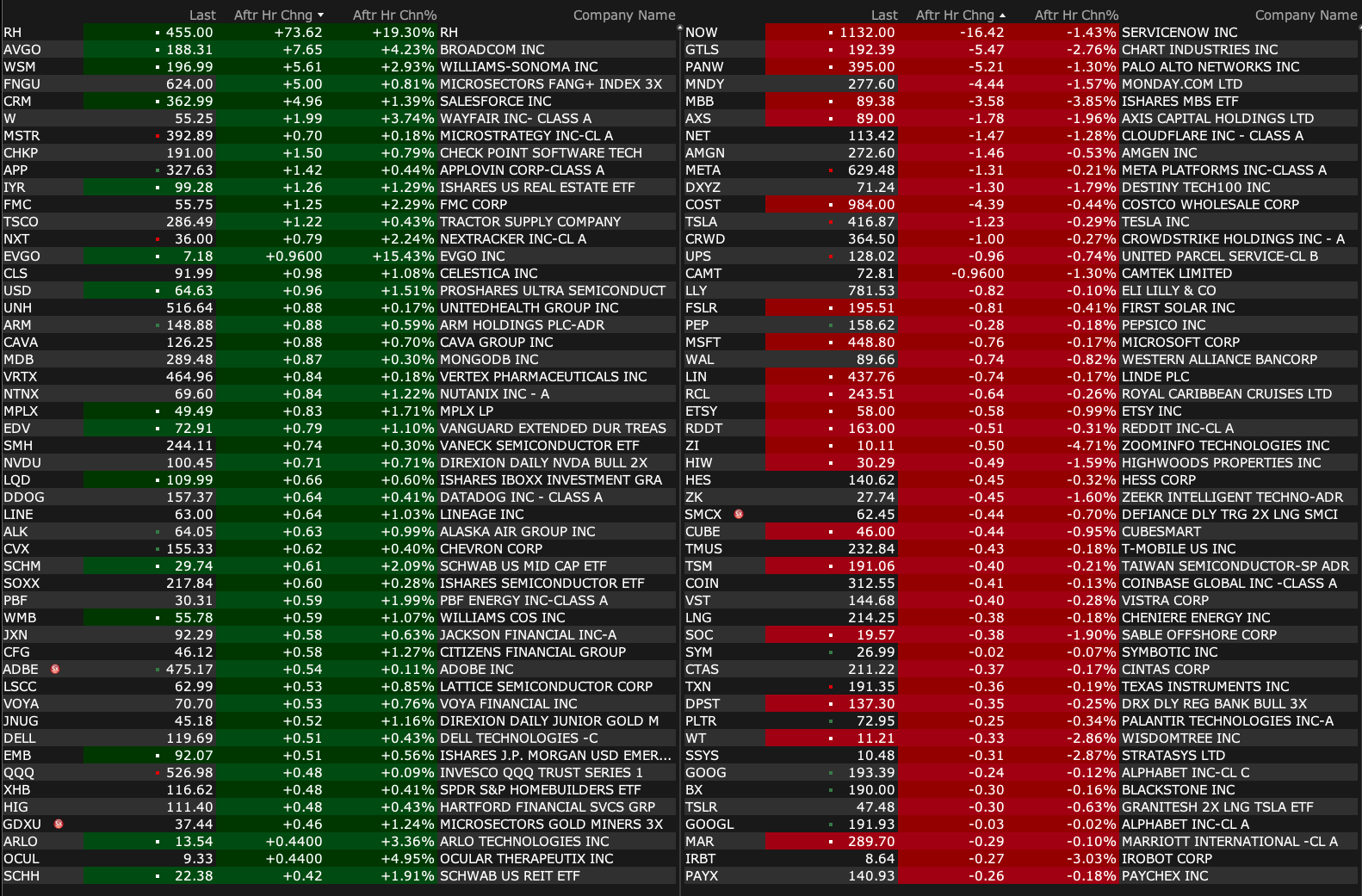

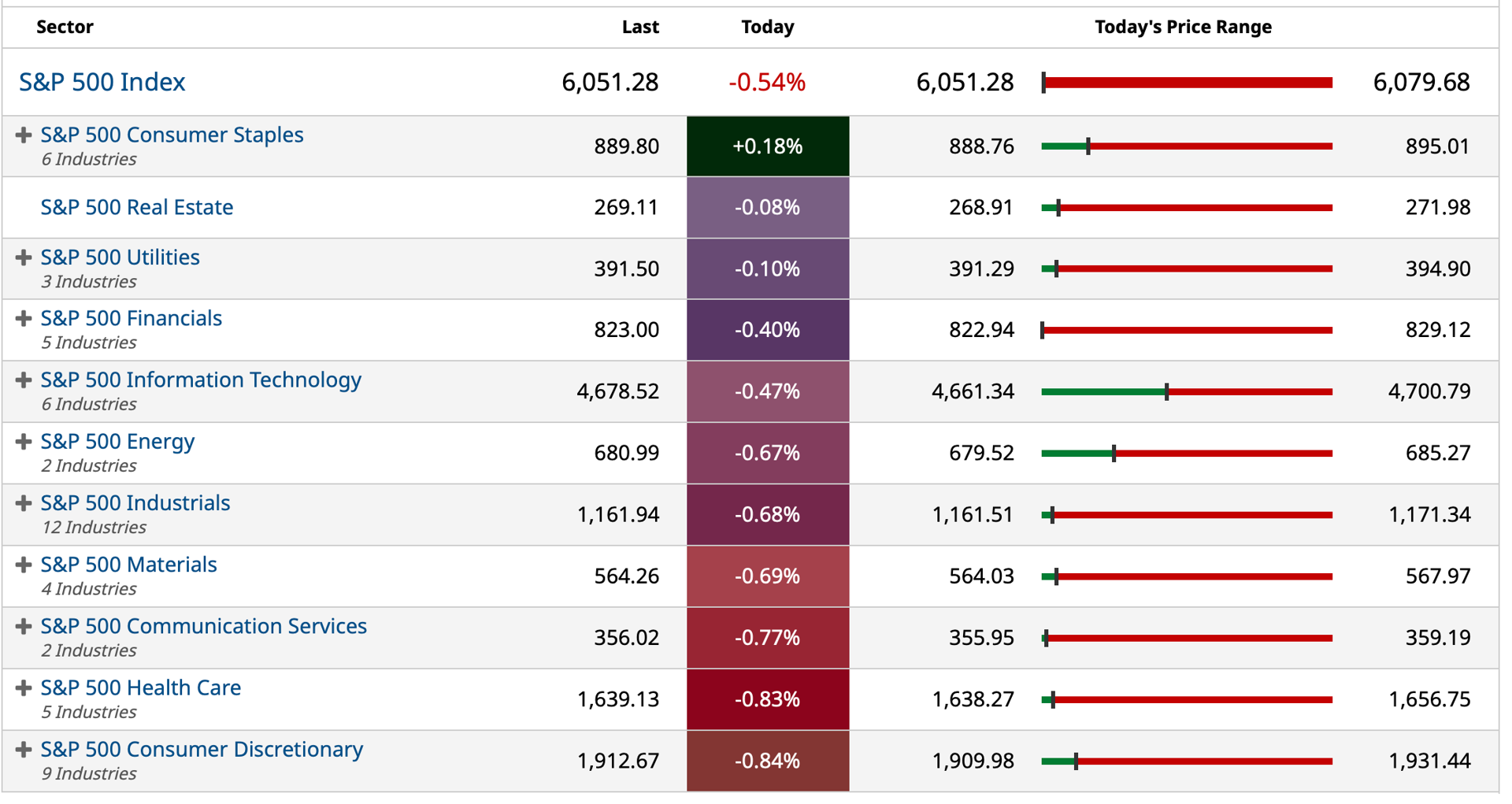

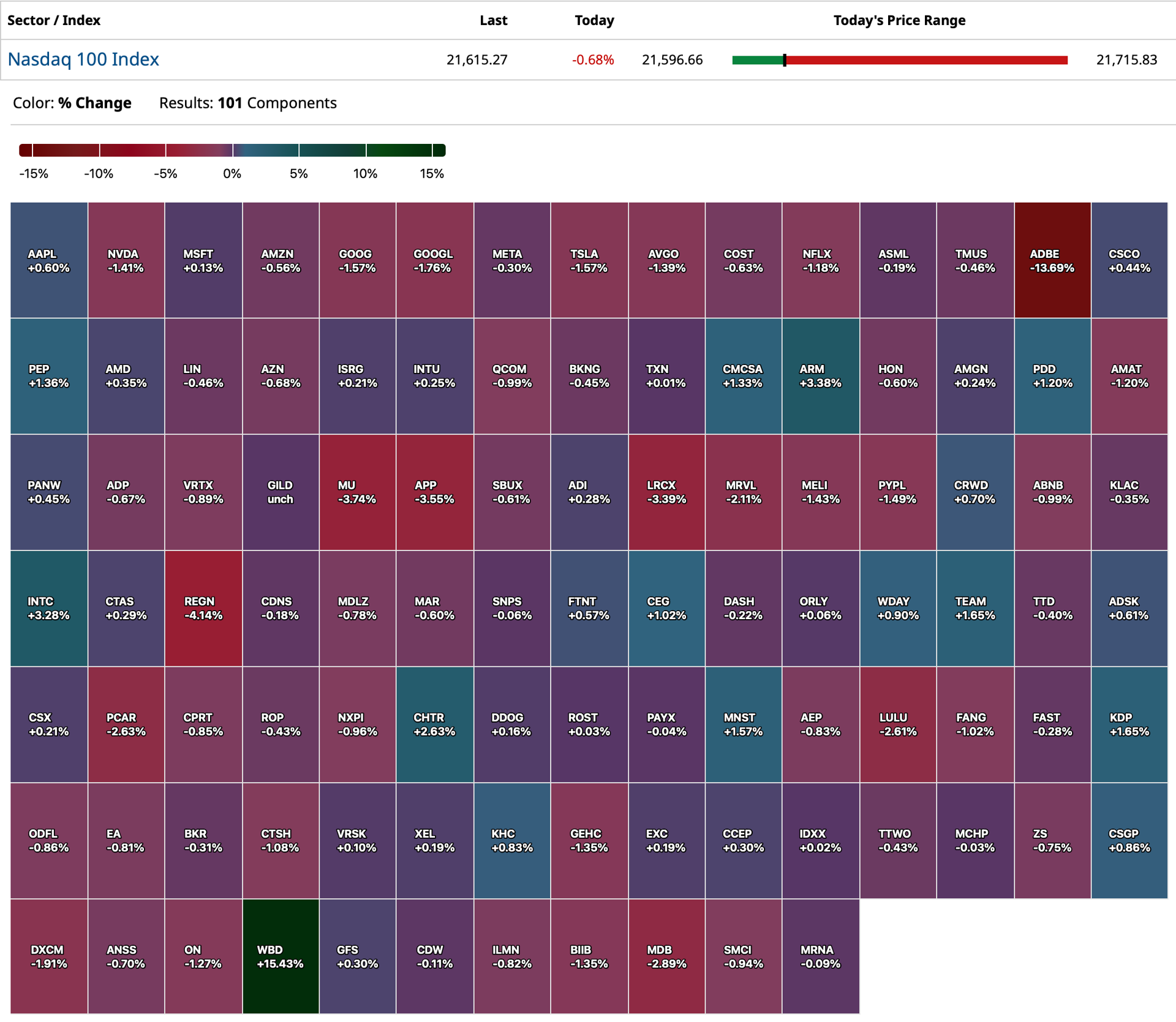

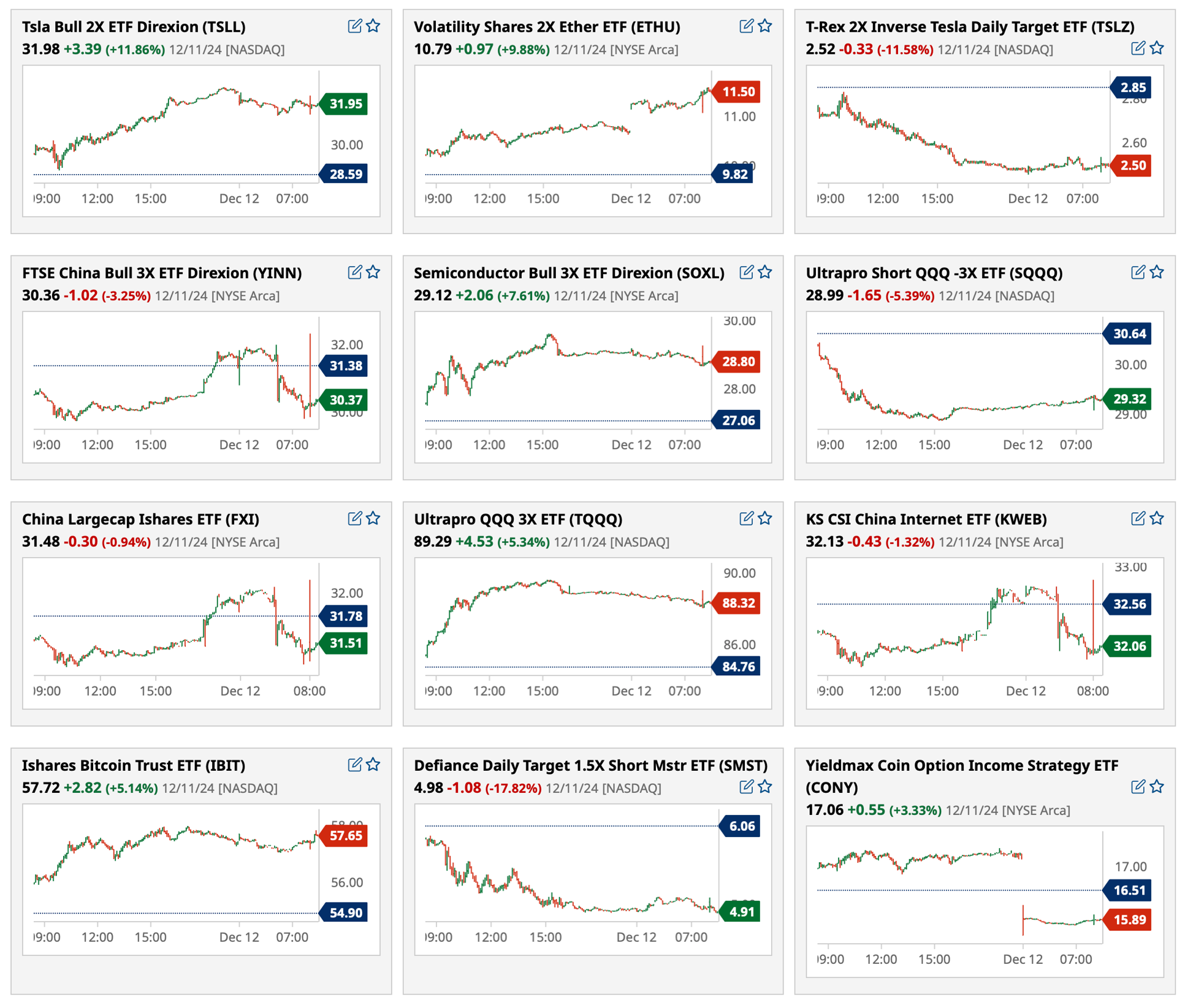

After-Hours Movers

As of 4:21 p.m.:

BY Doug Kass · Dec 12, 2024, 5:10 PM EST

As of 4:21 p.m.:

BY Doug Kass · Dec 12, 2024, 5:10 PM EST

BY Doug Kass · Dec 12, 2024, 4:59 PM EST

As mentioned today and yesterday, I will be out of the office for the next few hours.

BY Doug Kass · Dec 12, 2024, 1:56 PM EST

BY Doug Kass · Dec 12, 2024, 1:26 PM EST

% Movers as of 12:22 p.m.:

BY Doug Kass · Dec 12, 2024, 12:45 PM EST

douglas cassel

31 minutes ago

For those who do not read the divine Ms. M. She posted this note this morning

"If you are wondering why the breadth of the market is so poor, I have a theory. All the money that would typically be going into stocks to lift breadth, even if it is speculative money, looks like it is going into crypto garbage. Yes, it is still speculation, but it is not in stocks."

I have long wondered when the impact of crypto investment would start to be felt in other markets. I think options will be impacted even more strongly than stocks, as the volatility becomes what is important (thanks TN).

Longer term, I see this as a real drag on the stock and bond markets in general. Why invest in a slowly growing company or low paying bond when you can write calls against against a BTC etf? Such programs become very attractive for those of us lucky enough to be sitting on large gains.

Lost in the cacophony of Michael Saylor's statements was a remarkably prescient one, that has been largely ignored. Every company slows down or loses its edge over time. The fast growing companies of the past, GE,IBM, DEC, Xerox etc have faded as a natural process of capitalism. Apple, NVDA and PLTR will be the same. BTC however, if anything about it is true, does not have the same decay curve, and should even undergo wider adoption with time.

If any of the hype about cypto is correct, the choice is pretty clear.

BY Doug Kass · Dec 12, 2024, 12:30 PM EST

BY Doug Kass · Dec 12, 2024, 12:27 PM EST

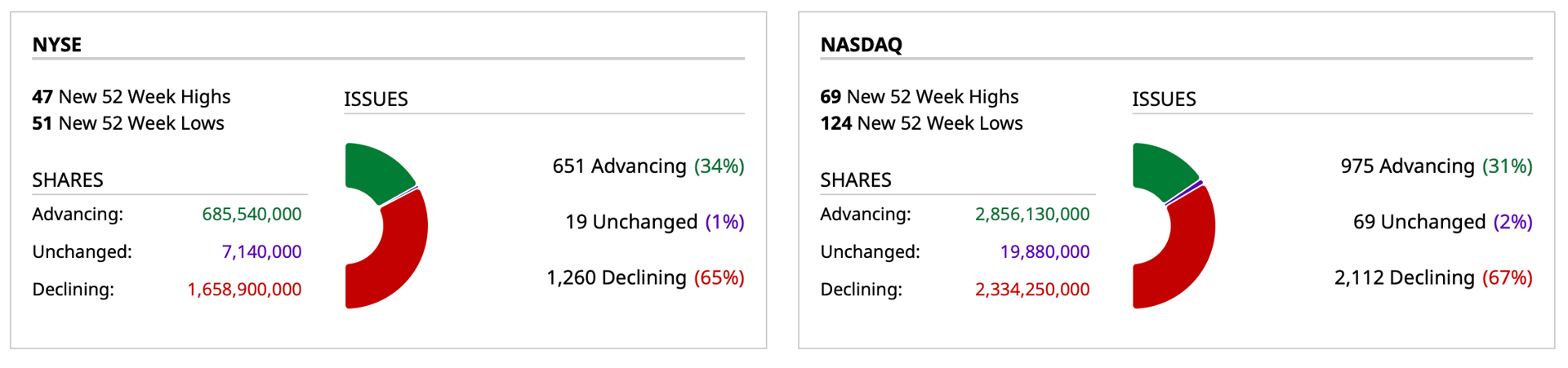

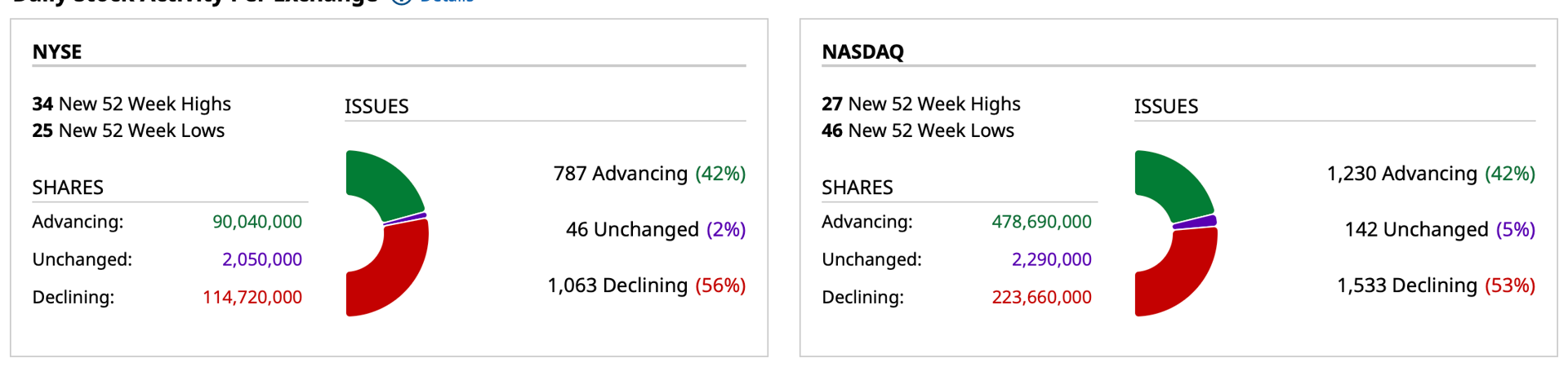

- NYSE volume is 14% below its one-month average;

- Nasdaq volume is 12% below its one-month average

BY Doug Kass · Dec 12, 2024, 11:06 AM EST

Intraday as of 10:08 a.m.:

BY Doug Kass · Dec 12, 2024, 10:45 AM EST

I remain short Nvidia NVDA and, the shares too, appear to be rolling over.

BY Doug Kass · Dec 12, 2024, 10:33 AM EST

Multi week low for JPMorgan Chase JPM. Seems like the money center bank and selected financials may finally be rolling over.

BY Doug Kass · Dec 12, 2024, 10:27 AM EST

From Peter Boockvar:

The ECB cut to 3%, by 25 bps as expected and Lagarde is speaking right now. She's still acknowledging sticky service inflation in part due to higher wages but believes policy is still restrictive. She said they "are not pre-commmitting to a particular rate path." The euro is flat and bond yields, are up only slightly and off their earlier morning highs of the day.

Headline PPI in November rose .4% m/o/m, twice the estimate but ex food and energy it was higher by .2% as forecasted. The y/o/y headline gain accelerated, up 3% vs 2.6% in the month before. The core rate was up by 3.4% y/o/y, unchanged with October. A spike in food prices accounted for the headline beat as they rose 3.1% m/o/m and up 5.1% y/o/y. There was a 55% rise in chicken eggs which accounted for 25% of the PPI increase. Also, according to the BLS, "Prices for fresh and dry vegetables, fresh fruits and melons, processed poultry, non-electronic cigarettes, and residential electric power also increased."

Core goods prices rose by .2% m/o/m for the 5th straight month and up by 2.2% y/o/y. Thus, persistent around this trend.

Service prices rose .2% m/o/m and 3.9% y/o/y. The BLS said "Over 1/3 of the advance in prices for final demand services can be traced to margins for machinery and vehicle wholesaling, which increased 1.8%." Prices rose too for securities brokerage, dealing, and investment advice and we know because of the rise in markets. Also gains were seen in auto fuels, food wholesaling, and apparel/footwear/accessories retailing. They fell for 'airline passenger services.'

Bottom line, as seen, food prices accounted for all of the upside surprise but not out of nowhere as the CRB food price index is nearing the highest level since October 2023. Coffee in particular is trading at levels never before seen, cocoa too. That said, core PPI is still up 3.4% y/o/y, matching the highest level since February 2023.

Core PPI y/o/y

The initial jobless claims data was quite a surprise with a 242k print, well more than the estimate of 220k, up from 225k in the week before and a 2 month high. This brought the 4 week average to 224k from 219k, a 5 week high. Delayed by a week, continuing claims rose to 1.886mm from 1.871mm and still hovering around 3 yr highs.

Bottom line, a one week anomaly in the claims jump or something more? We'll obviously have to wait to see but enough to get the Fed to cut next week irrespective of the stickier inflation stats seen yesterday and today and why rate cut odds are at 98%. That said, they will most likely signal a January pause.

Inflation breakevens are unchanged but Treasury yields are off their morning highs in response to the jump in claims.

BY Doug Kass · Dec 12, 2024, 9:41 AM EST

-LAES +49% (bringing quantum technology to professional drones and UAVs via partnerships with Parrot and AgEagle)

-TRVI +46% (Independent Data Monitoring Statistician reaffirmed CORAL trial sample size remains at N=160 with Haduvio (oral nalbuphine ER) Trial reaching 75% enrollment)

-CDT +27% (to revolutionize drug development through agreement to use AI and Cybernetics)

-ZENA +25% (launches Quantum Computing Project for Traffic Optimization and Weather Forecasting Using Drones)

-SHOT +15% (Q4 revenue guidance)

-IVAC +13% (guidance, announces dividend)

-CIEN +12% (earnings, guidance)

-CSBR +11% (earnings)

-CTHR +11% (receives interim award in Wolfspeed arbitration; Wolfspeed claim for $22.8M in damages rejected)

-MDCX +11% (announces Minor Use (MUMS) Designation from US FDA for Doxorubicin-Containing Microneedle Array (D-MNA) Patch)

-SGRP +11% (affirms intent to close Highwire merger at $2.50/shr)

-TRNR +11% (signs Exclusive Letter of Intent to Acquire Scaled and Profitable, Connected-Fitness Equipment Business)

-TELO +10% (raises $1M at $7/shr in a no-warrant, restricted common stock deal, representing a 20% premium to closing price)

-DBVT +9.8% (confirms alignment with U.S. FDA on Accelerated Approval Pathway for Viaskin Peanut Patch in Toddlers 1 - 3 Years-Old)

-GAMB +9.4% (enters into Definitive Agreement to acquire Odds Holdings, parent of OddsJam in accretive transaction)

-WBD +6.8% (Board of Directors authorizes implementation of a new corporate structure designed to enhance its strategic flexibility and create potential opportunities to unlock additional shareholder value)

-PHX +6.5% (initiates strategic alternatives review, including potential merger or sale)

-UAMY +5.3% (Director purchases $102K in common shares)

-QSI +5.2% (expands international distribution network to 15 partners)

-PYCR +3.6% (BMO Capital Markets Raised PYCR to Outperform from Market Perform, price target: $24)

-CELH +3.3% (JPMorgan Chase and Co Initiates CELH with Overweight, price target: $37)

-NNE +3.3% (LIS Technologies and NANO Nuclear Energy are One of Six Awarded U.S. Department of Energy Contracts as Part of Low-Enriched Uranium Acquisition Program with An Aggregate Appropriation of $3.4B Over 10 years)

-UBER +3.1% (CFO comments from Barclays conference)

-CNC +2.8% (guidance ahead of Investor Day)

-LGTY +2.8% (issued a statement in response to recent market rumors and media reports)

-KROS -73% (voluntarily halted dosing in 3.0 mg/kg and 4.5 mg/kg treatment arms in ongoing TROPOS trial, a Phase 2 clinical trial of cibotercept (KER-012) in combination with background therapy in patients with pulmonary arterial hypertension (“PAH”), based on a safety review)

-LOVE -22% (earnings, guidance)

-ADBE -11% (earnings, guidance)

-SCLX -10% (announces $17M registered direct offering)

-NDSN -6.2% (earnings, guidance)

-ACHR -5.2% (announces Strategic Partnership with Anduril to Develop Hybrid VTOL Military Aircraft; raises An Additional $430M)

-OXM -3.5% (earnings, guidance)

-CHWY -2.9% (prices 15.9M shares; to buy back $50M in stock from the selling stockholder)

-FISI -2.7% (prices 4M shares at $25/share)

-GD -2.5% (multiple broker downgrades)

-KGS -2.2% (files to sell 5.5M shares of common stock by selling stockholder)

BY Doug Kass · Dec 12, 2024, 9:26 AM EST

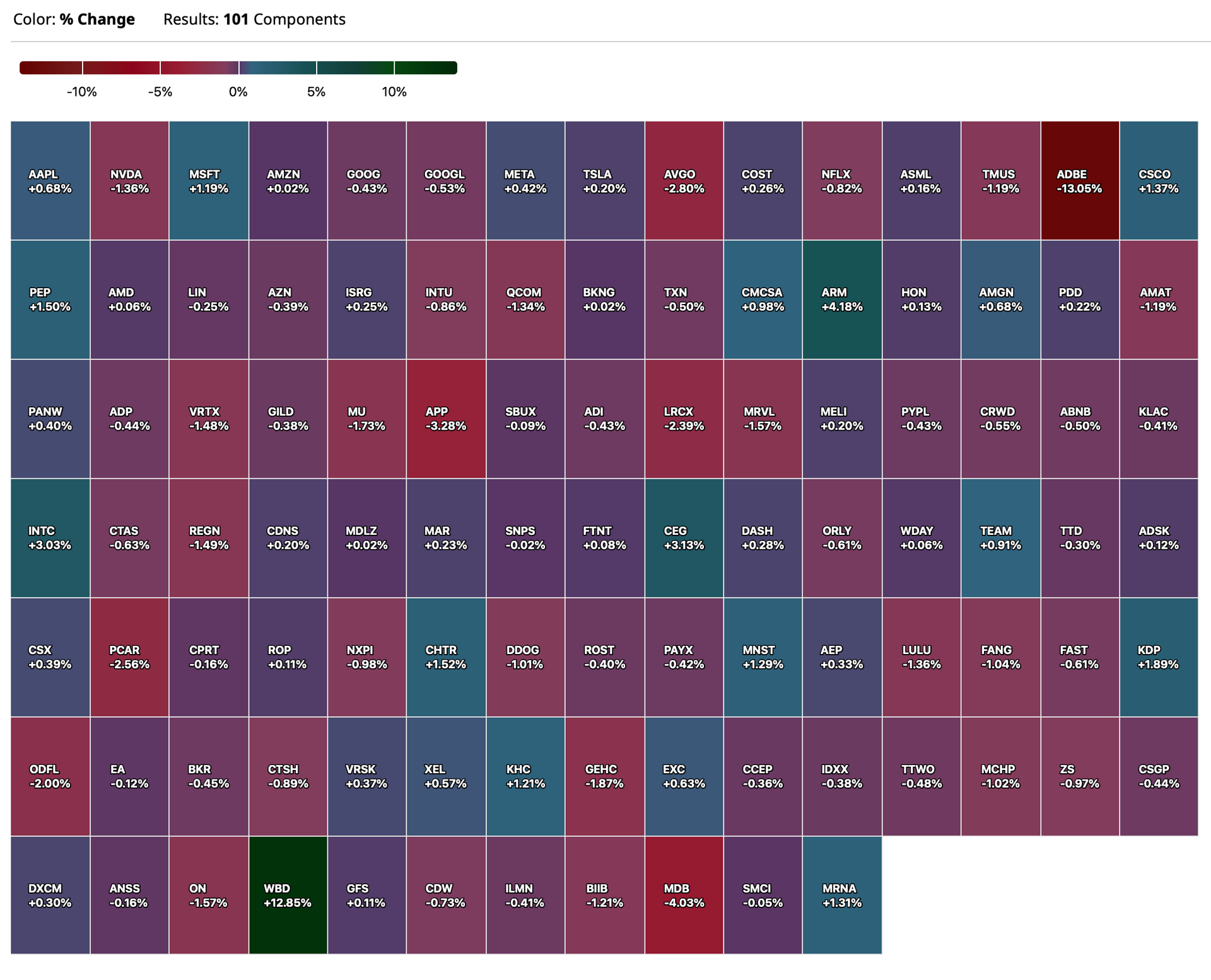

Charts from 8:24 a.m. ET:

BY Doug Kass · Dec 12, 2024, 9:09 AM EST

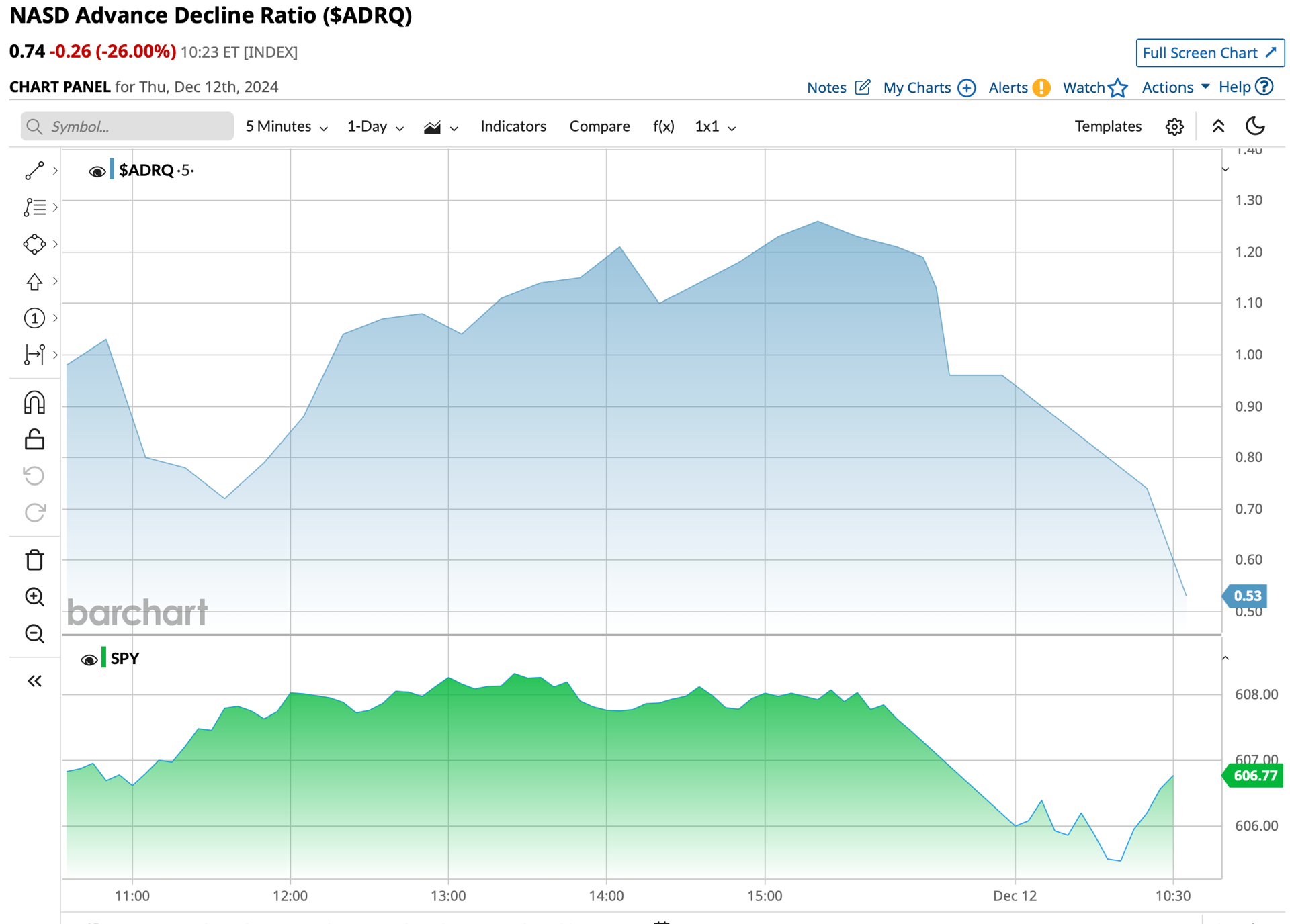

Chart from 8:42 a.m. ET:

BY Doug Kass · Dec 12, 2024, 8:54 AM EST

From Peter Boockvar:

Ahead of the expected 25 bps cut from the ECB today at 8:15am est, a bunch of central bank actions have taken place and rather than wait until there is evidence that inflation will stay down on a sustainable basis, a few are trying to catch that falling inflation knife. But not all. I say 'not all' because the Brazilian central bank hiked rates by 100 bps last night and said expect another 200 bps to come.

From the Bank of Canada yesterday giving reason for their 50 bps rate cut to 3.25%, "With inflation around 2%, the economy is in excess supply, and recent indicators tilted towards softer growth than projected." Going forward its next move won't be as obvious as "we will be evaluating the need for further reductions in the policy rate one decision at a time. Our decisions will be guided by incoming information and our assessment of the implications for the inflation outlook." The BoC also laid out the big risk out there, tariffs. Risk of course if they happen but even risk if there are just threats of them. "No one knows how this will play out in the months ahead - whether tariffs will be imposed, whether exemptions get agreed, or whether retaliatory measures will be put in place. This is a major new uncertainty."

As the policy rate calibration from here is a bit cloudier than what's been seen in Canada, the Canadian$ is up for a 2nd day, though very slightly. The 2 yr yield was up by 5 bps yesterday but still well off its levels of a few weeks ago.

The Swiss National Bank is giving themselves absolutely no room for maneuver if there are any economic surprises to the downside as they surprisingly cut its benchmark rate by 50 bps to .50%. As I hope I NEVER see negative interest rates again, it's bizarre to me that the SNB is playing this game again around zero rates. To the possibility of NIRP, Governor Schlegel said he doesn't like NIRP but would not exclude the possibility of them again. He said "With our easing of monetary policy today we are countering the lower inflationary pressure." He also threatened the use of FX intervention in order to stem further Swiss Franc gains of substance.

The Swiss Franc is lower in response but not by much. Versus the dollar, its exchange rate is pretty much in the middle of its one year range but is at record high vs the euro and what the SNB is seemingly trying to push back against, to no avail so far.

Euro/Swiss Franc cross rate (how many Swiss Francs one Euro can buy)

On the dovish flip side is the hawkish Brazilian central bank which hiked its Selic rate by 100 bps yesterday to 12.25%. They said "In light of a more adverse scenario for inflation convergence, the Committee anticipates further adjustments of the same magnitude in the next two meetings, if the scenario evolves as expected." For perspective, their inflation goal is 3% and no higher than 4.5% and it is currently running at 4.87% in November. When it comes to fighting inflation, they don't mess around. They said the Selic rate could get to 14.25% by March.

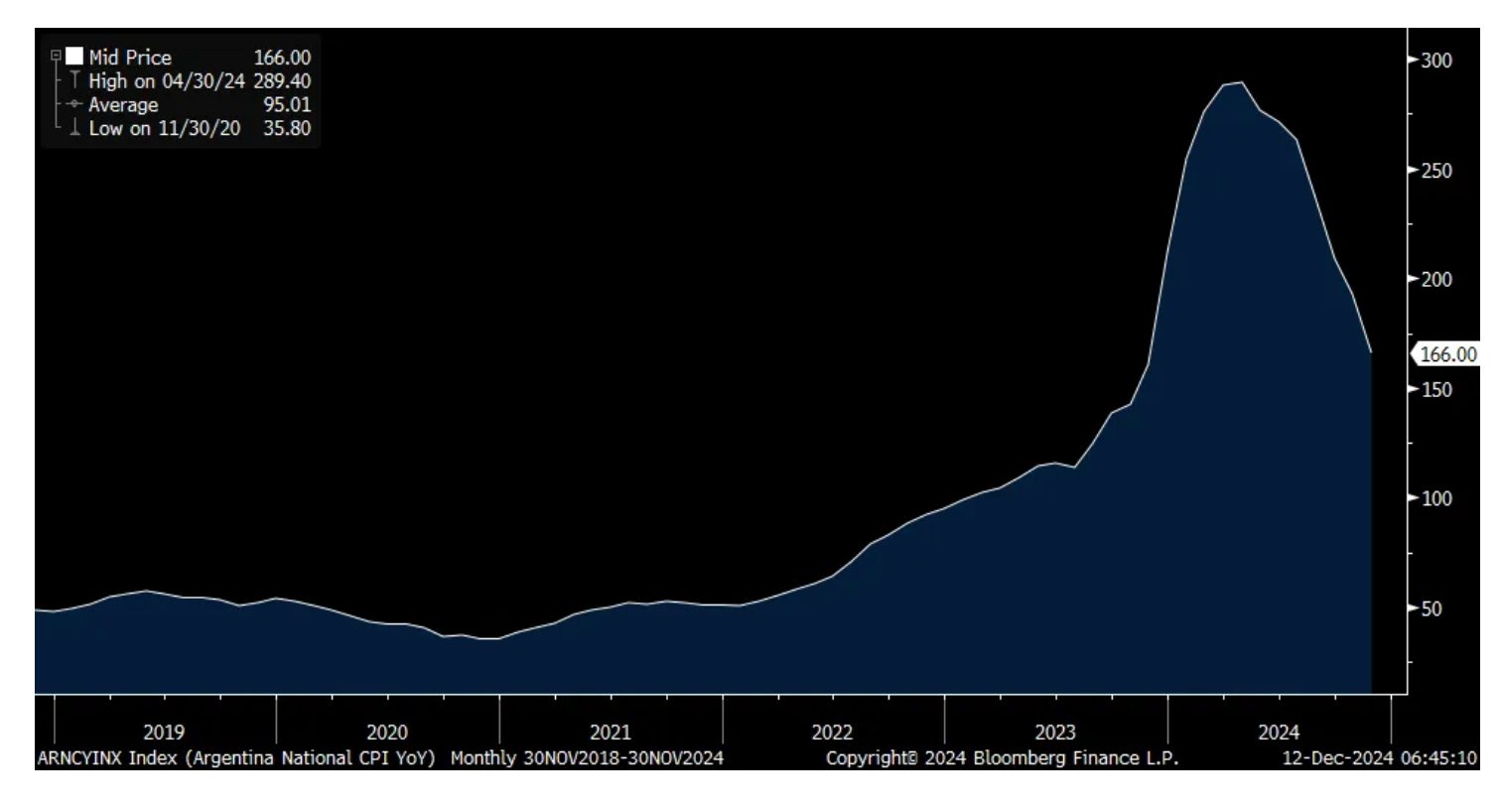

With respect to inflation in the other key South American country, Argentinian president Javier Milei has worked wonders so far via massive spending cuts. Argentina said yesterday that its November CPI, while running still red hot, continues to decelerate, rising by 2.4% m/o/m, its slowest monthly gain since July 2020. This is still a hyperinflationary situation at 166% y/o/y but that is down from 289% in April. I continue to cheer on Javier Milei for his grand moves to get Argentina out of its socialist morass.

Argentina m/o/m CPI

Argentina y/o/y CPI

From Macy's, and while they are challenged by the book keeping antics of a particularly employee and internal accounting control issues, they said this on their underlying business:

"Let me talk about the high end, first of all, in terms of the sales guide. When we think about what we've seen quarter to date, we're seeing sequential improvement across many dimensions of our business. We're seeing sequential improvement in digital, we're seeing sequential improvement in stores, we're seeing sequential improvement in Macy's nameplate, we're seeing sequential improvement in luxury, both Bloomingdale's and Bluemercury. We're seeing sequential improvement in F50. We're seeing sequential improvement in the other go-forward stores that have not received the investments yet."

From Oxford Industries, the apparel company:

"We are excited to be in the midst of a holiday season where the consumer appears to be regaining confidence and is more willing to make discretionary purchases." That said, the stock is trading down pre market and they said "But before jumping into the results of the 3rd quarter, I want to acknowledge the multiple headwinds faced by our brands in the 3rd quarter, including the conclusion of the most intense election cycle in recent memory and the impact of the two major hurricanes that devasted parts of the Southeastern Unites States."

"We should also point out that we own a portfolio of premium brands that sell primarily at full price with very limited exposure to the off-price outlet channels. These value-oriented channels have been thriving as cautious consumers seek special offers and clearance pricing. We believe our full price premium strategy has been and will be a long-term competitive strength, but in the current environment, it is a headwind to our top-line while acting as a tailwind for others in our space."

I will leave the competitive positioning of Adobe to others and the big down move in the stock but did want to highlight this one comment from the call on the impact of FX and the US dollar rally. "We expect an approximate $200 million headwind to FY '25 revenue as a result of the effect of foreign exchange and a smaller impact of the continued move to subscriptions from perpetual offerings." Expect more of that when we see Q4 earnings early next year.

If you do a lot of business in Europe specifically, earnings season to be seen in January/February will be pretty interesting both from what was experienced there in light of the sluggish activity in Germany and France in particular and the strength of the US dollar vs the Euro.

Overseas, we're seeing a rally in the Aussie$ and a selloff in Australian bonds after they reported a better than expected November jobs figure with a drop in its unemployment rate to 3.9% from 4.1% and where an expected rise to 4.2% was the consensus. The ASX was down by .3%.

BY Doug Kass · Dec 12, 2024, 8:35 AM EST

* Among multiple factors, markets (especially of a Nasdaq-kind) remain immune to negative data points (of prickly inflation, rising interest rates), geopolitical instability, the rising likelihood of less Fed interest rate cuts and extended valuations...

* In this morning's opening missive I highlight stubborn inflation and some similar (general) thoughts on the markets that both Rosie and I possess.

When I perused the inflation release at 8:30 a.m. on Wednesday morning I thought that, with inflation clearly a continuing, stubborn and disturbing factor, the high inflation print would be interpreted as a market-unfriendly data point during the regular trading session.

I was clearly wrong as stocks continued to soar — extending the post-election rally.

What bothered me about the release? Multiple factors that suggest inflation will not be contained:

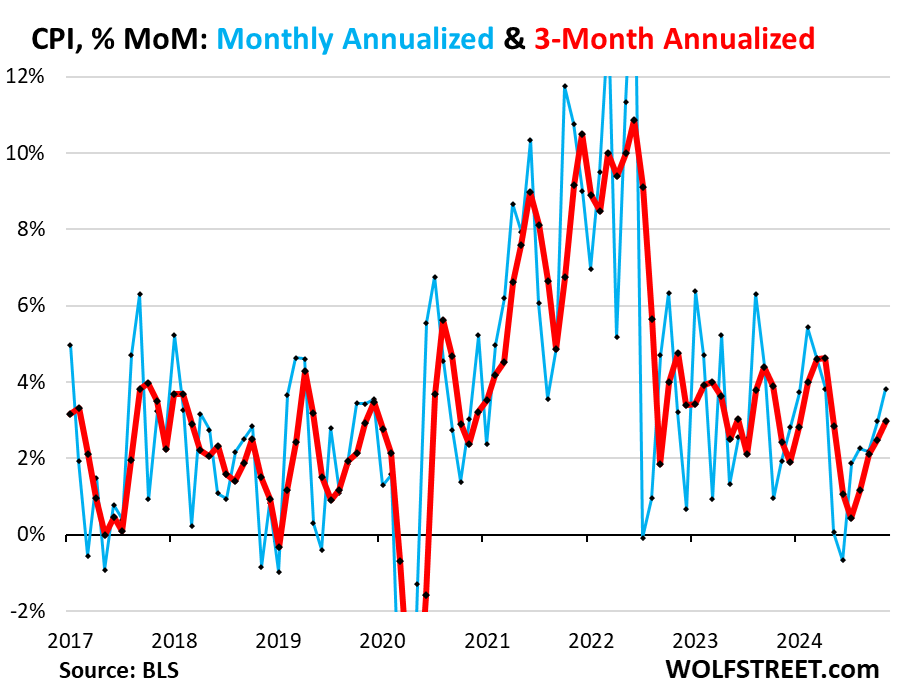

* The overall Consumer Price Index rose by 0.31% (+3.8% annualized) in November from October, the sharpest increase since April. It has been accelerating since June (blue).

The three-month average jumped by 3.0% annualized, also the sharpest increase since April, and the fourth month-to-month acceleration in a row:

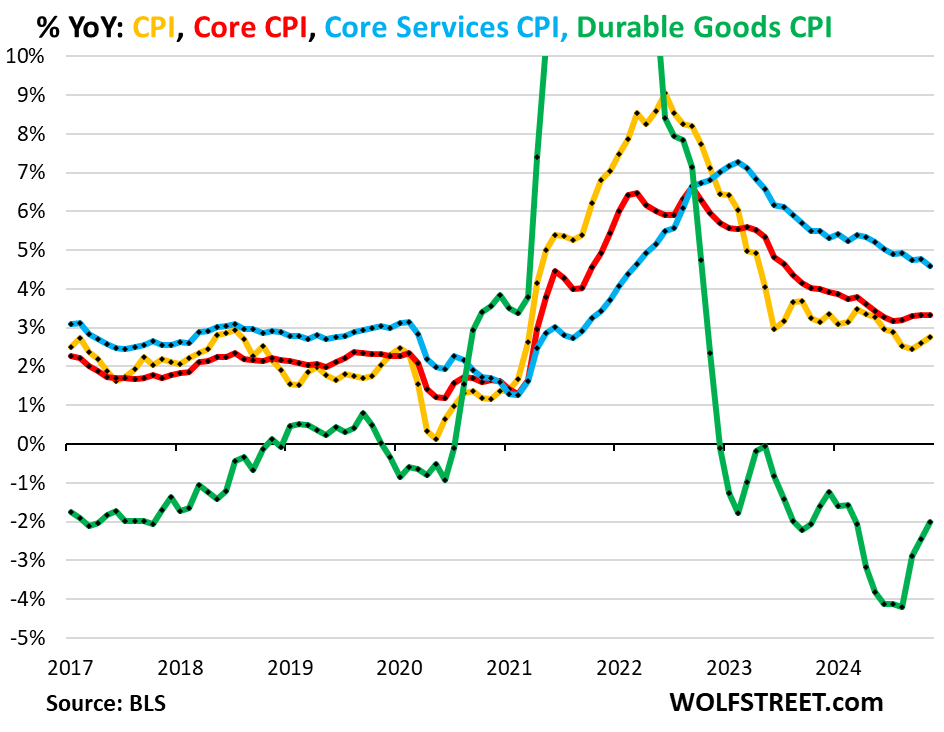

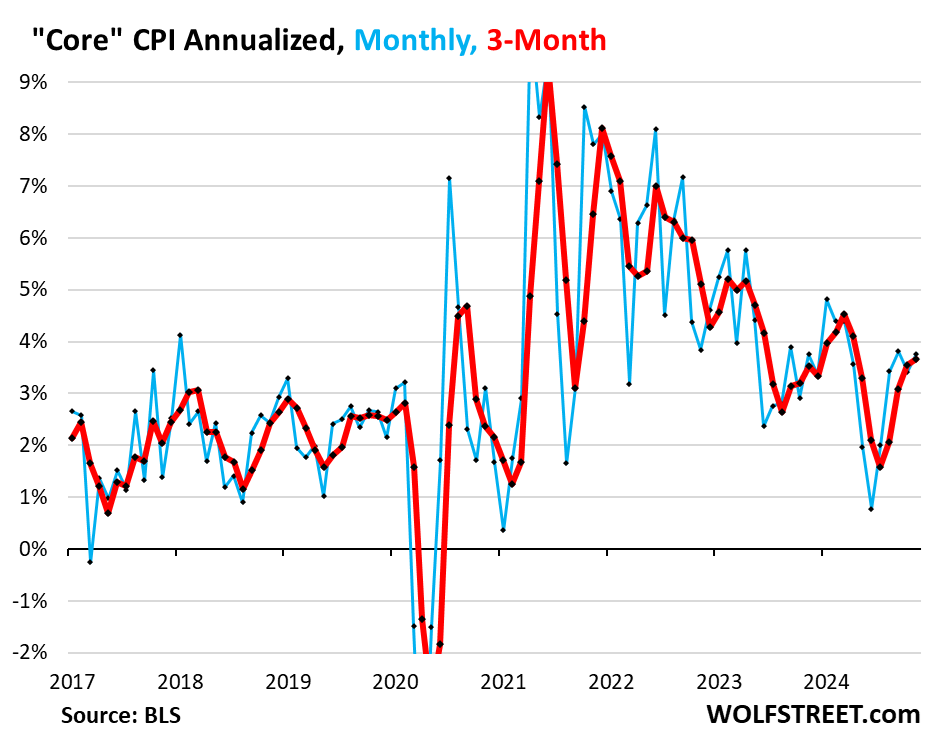

* The Core CPI, which excludes food and energy components to track underlying inflation, rose by 3.32% year-over-year. It has been in this range for six months in a row, and above where it had been in June.

The major components, year-over-year:

* Month-to-month “Core” CPI rose by 0.31% (+3.8% annualized) in November from October. Over the past four months, core CPI has risen in this range of +3.4% to +3.8% annualized, the biggest increases since March (blue in the chart below).

The 3-month average “core” CPI accelerated to +3.7% annualized, the fourth month of acceleration in a row, and the highest since April (red).

The sharp price increase of used vehicles in November, the third month in a row of price increases, was a big factor in the stubbornly high and accelerating core CPI rate, having U-turned from a historic plunge that until mid-2024 had been one of the big factors in the cooling of core inflation.

Used vehicles, on a month-to-month basis, are now fueling inflation, and we have seen that for months beneath the surface in rising used-vehicle wholesale prices, very tight inventories and strong demand (stimulated by the plunge in prices from early 2022 till mid-2024).

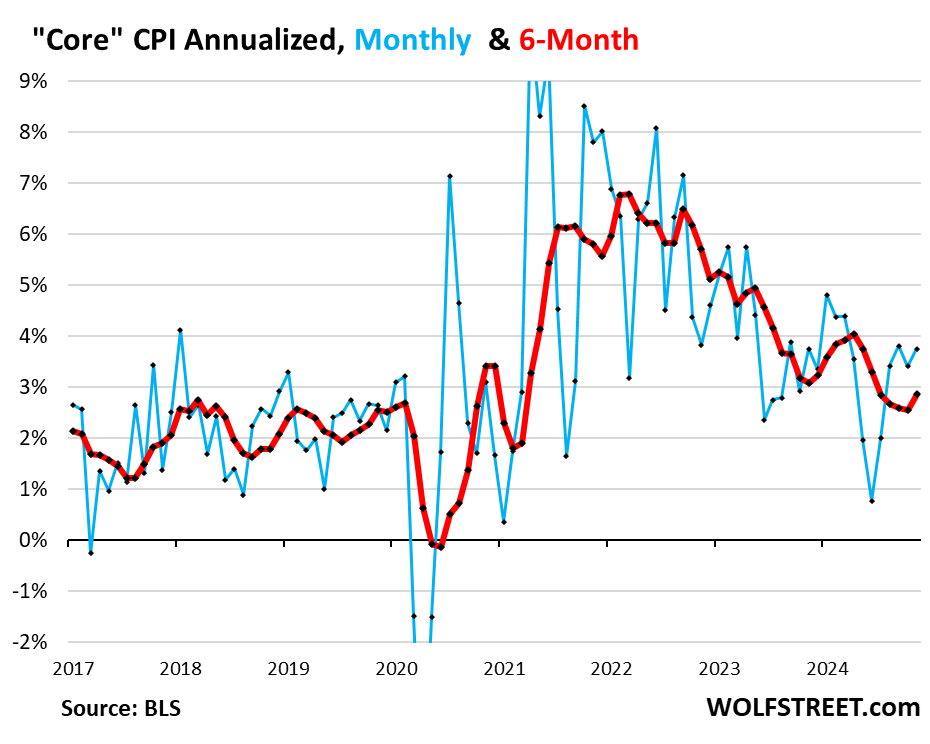

* The 6-month average “core” CPI – which irons out most of the month-to-month squiggles but lags further behind – accelerated to +2.9% (red):

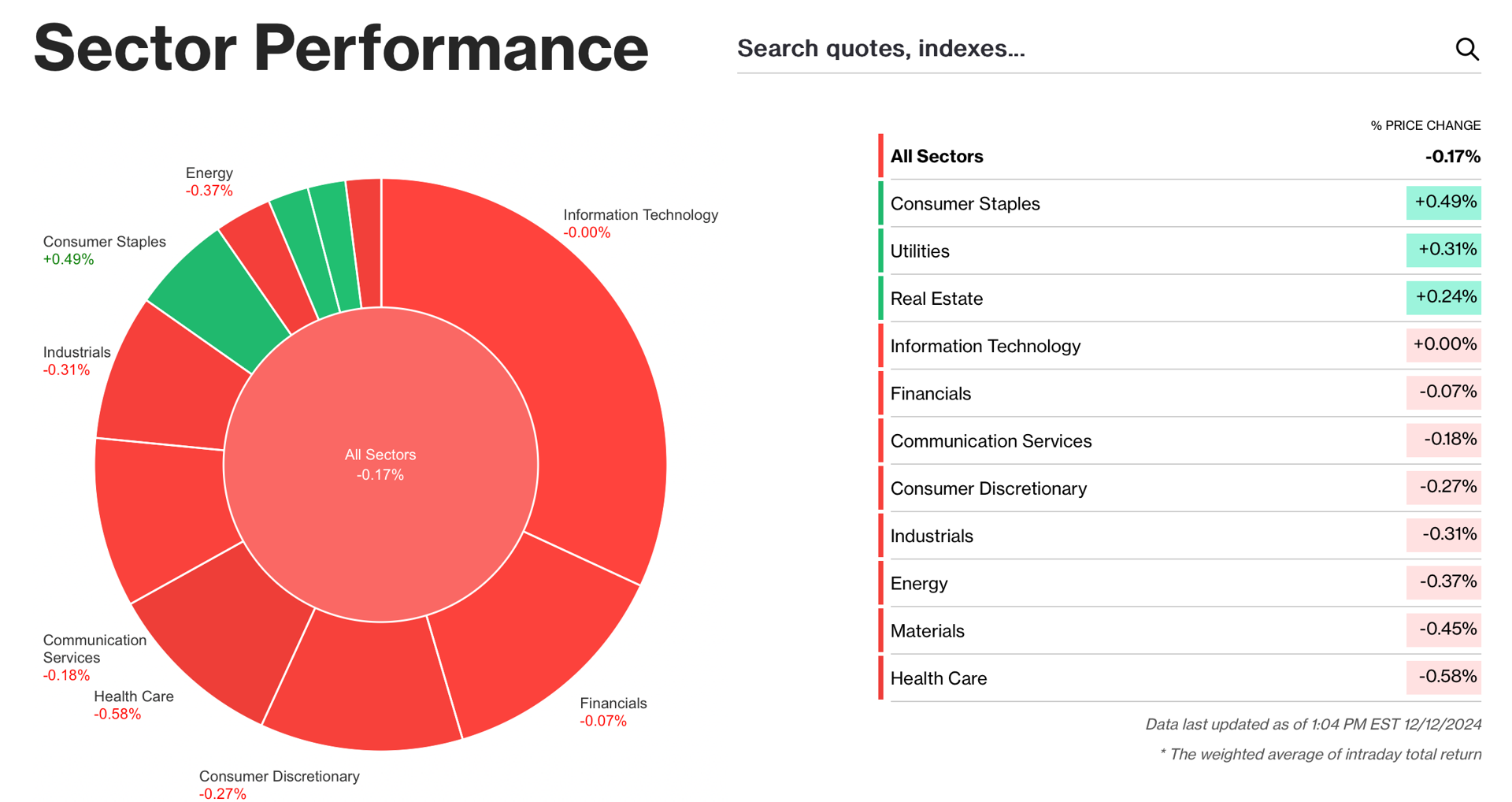

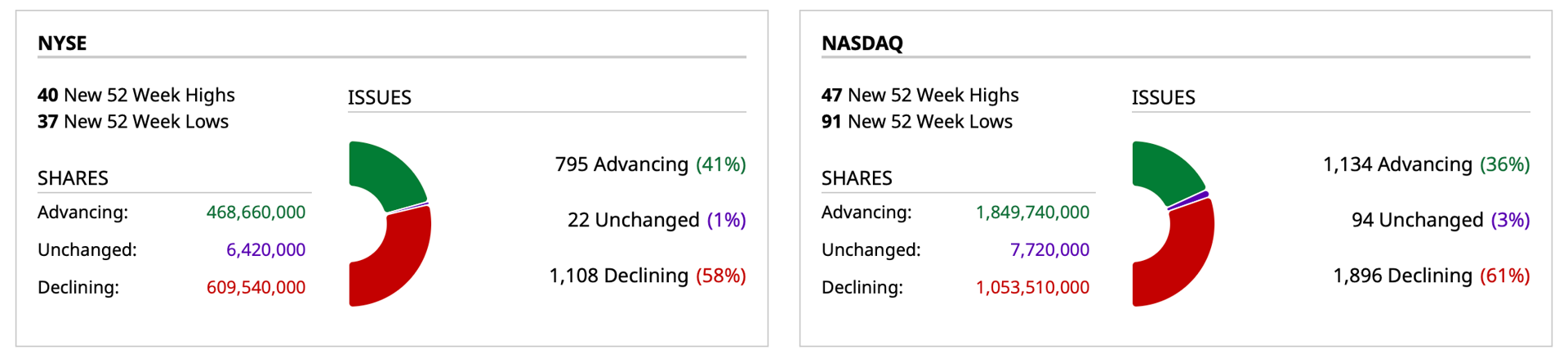

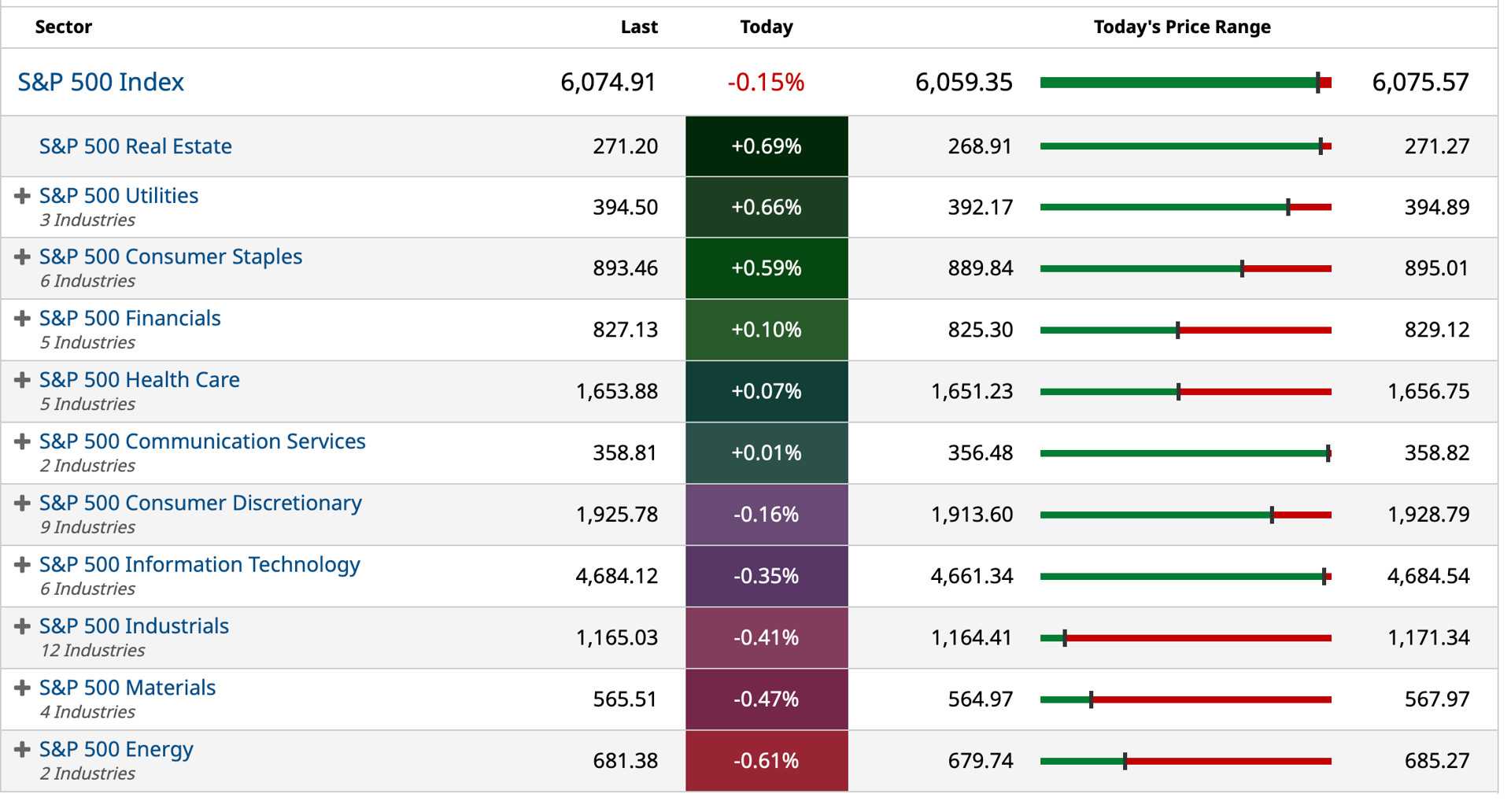

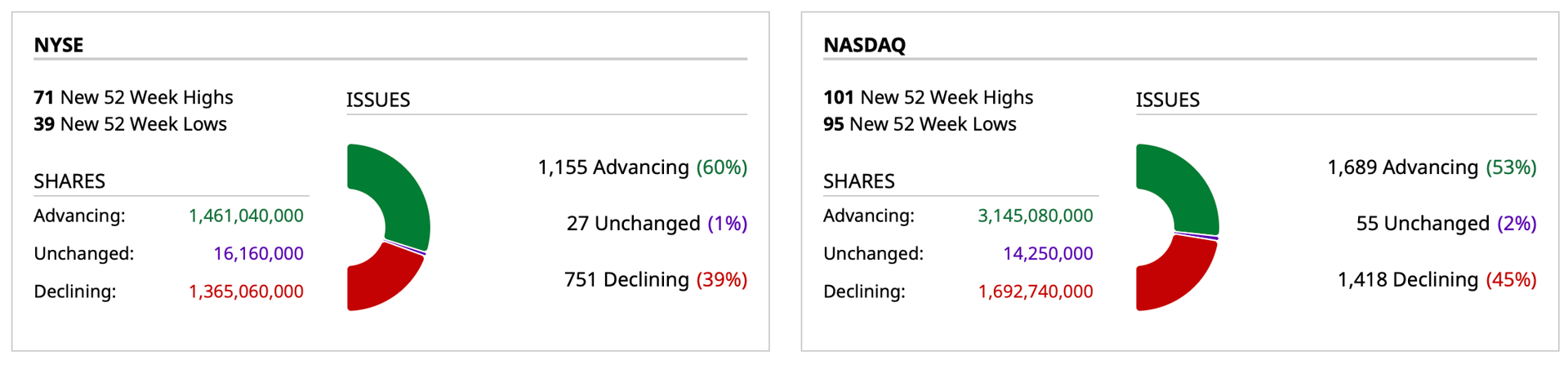

Meanwhile, despite averages flying ever higher, market breadth was lackluster and not representative of the size of the climb in the S&P and (especially the) Nasdaq Indices:

Wednesday's Index Returns

* S&P +0.64%

* Nasdaq +1.60%

* Russell +0.41%

* RSP (equal weighted S&P) +0.21%

Here were yesterday's unimpressive breadth figures (achieved on lower volumes):

-- New York Stock Exchange volume was 3% below its one-month average

-- Nasdaq volume was 4% below its one-month average

Yesterday I highlighted my pal/buddy/friend Rosie's Lament of the Bear (Original and Sequel).

We share similar concerns — specifically regarding historical valuation metrics (being in the 96%- tile), stubborn inflation, a thin equity risk premium and skepticism regarding corporate profit growth (and AI's contribution to productivity).

Rosie's words, in The Sequel succinctly explain the gravity defying market and the market's impervious reaction to any negative data point:

Extended Valuations: Second, as part of this evaluation, I laid out the possibility, even the plausibility, that investors have lengthened their time horizons, as they have done in the past amidst a shift in the technology and productivity curve. This means classic short-term valuation metrics may not work — and the reality is that they haven’t worked (as in scaring anyone off) over the past year-and-change.

AI Overhyped: Fourth, I highlighted what will likely bring this bull market to an end: renewed inflation that causes the Fed to reverse course, concrete recession signs coming to the fore, a global tariff and trade war, and anything that shows a deviation in the AI boom from current expectations, which is what brought the Tech boom to an end in the winter of 2000.

As to my particular concern regarding the paper thin equity risk premium, Rosie writes:

A Slim Equity Risk Premium: Seventh, with the equity risk premium (ERP) close to zero, investors have no compulsion to part with their stocks, ever. This may be why I am reluctant to jump into the market even after acknowledging the reasons why I missed the amazing rally these past two years and why, as per the first part of Bob Farrell’s Rule #4, we could still be in the phase of the extraordinarily rising market going further than we think. You may ask: “why not start participating more actively after my revelation?” That is because I was raised by Depression-era parents who were not gamblers but were hard workers and believed in thrift. And even if the first half of Bob Farrell’s Rule #4 may still apply now and in the near/intermediate term, let’s not forget the second half of the Rule, which is that these sorts of bull markets don’t correct by going sideways.

Eighth and final point — I came back to #7 right above. What is the razor-thin ERP telling us? Investors willingly investing in the market in this environment, to repeat, can only rationally be doing so if they are in it for the long run; never to sell under any circumstances. If that is your belief, then go right ahead. This is your sort of market. But if you believe that the ERP should be positive or anywhere close to the long-run mean of 300 or 400 basis points, then arithmetically, only three things can happen: (i) interest rates have to come down, (ii) the equity market will have to come down, or (iii) some combination thereof. I know there are folks out there who believe +20% average annual profits growth is easily doable and who believe that the ERP is appropriate — again, to believe that is to believe there will never be any sellers. That is what equity portfolio managers also believe, because they are running their funds with barely more than 1% cash ratios — unheard of in the annals of financial history.

Rosie Summarizes:

Because I believe that earnings growth estimates are too lofty, even with the AI craze and how it will change the world, and because I believe that the ERP should be above zero (as risky assets should command a risk premium against riskless assets), I am still largely on the sidelines. I also believe that by the time the top is turned in, there will be a mad scramble to get out because the two extreme primal emotions of investing, fear and greed, never go out of style. Greed has been working, and may continue to work in 2025, but nothing lasts forever.

The problem is that because there is so much overexposure to equities on household balance sheets, everyone is going to be trying to bail out together with precious few buyers on the other side, because there aren’t exactly a whole lot of folks out there with a cash position like mine (oh, save for Warren Buffett… the two of us will be there, rest assured, to provide liquidity when the time comes). I don’t know when that time will be, but I do know it will come.

Like the lynx-eyed Rosie, I have no idea how long the ascent continues but I am highly confident, with each leap, the reward vs. risk deteriorates ever further and "the margin of safety" is narrowing.

For those that are "playing" the upside momentum, bravo.

I am not and I have no interest in the near future in succumbing to animal spirits and "the fear of missing out" (FOMO).

I am fact-based and not emotionally based in my investing. I worship at the altar of fundamentals and valuations... not at the altar of price momentum.

And over multiple market cycles this discipline has worked out for me.

BY Doug Kass · Dec 12, 2024, 7:30 AM EST

Chart of the Day:

BY Doug Kass · Dec 12, 2024, 7:00 AM EST

BY Doug Kass · Dec 12, 2024, 6:50 AM EST

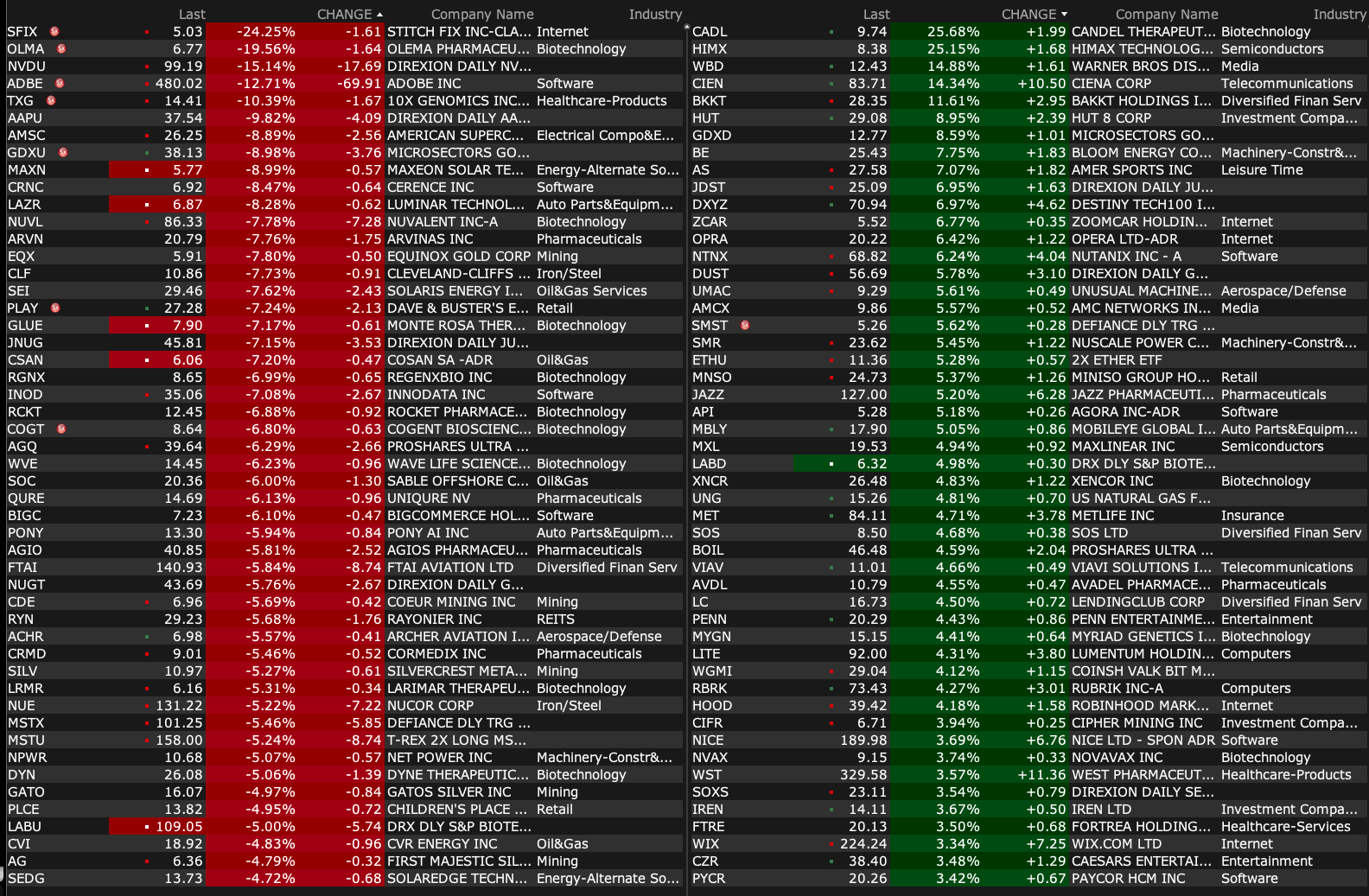

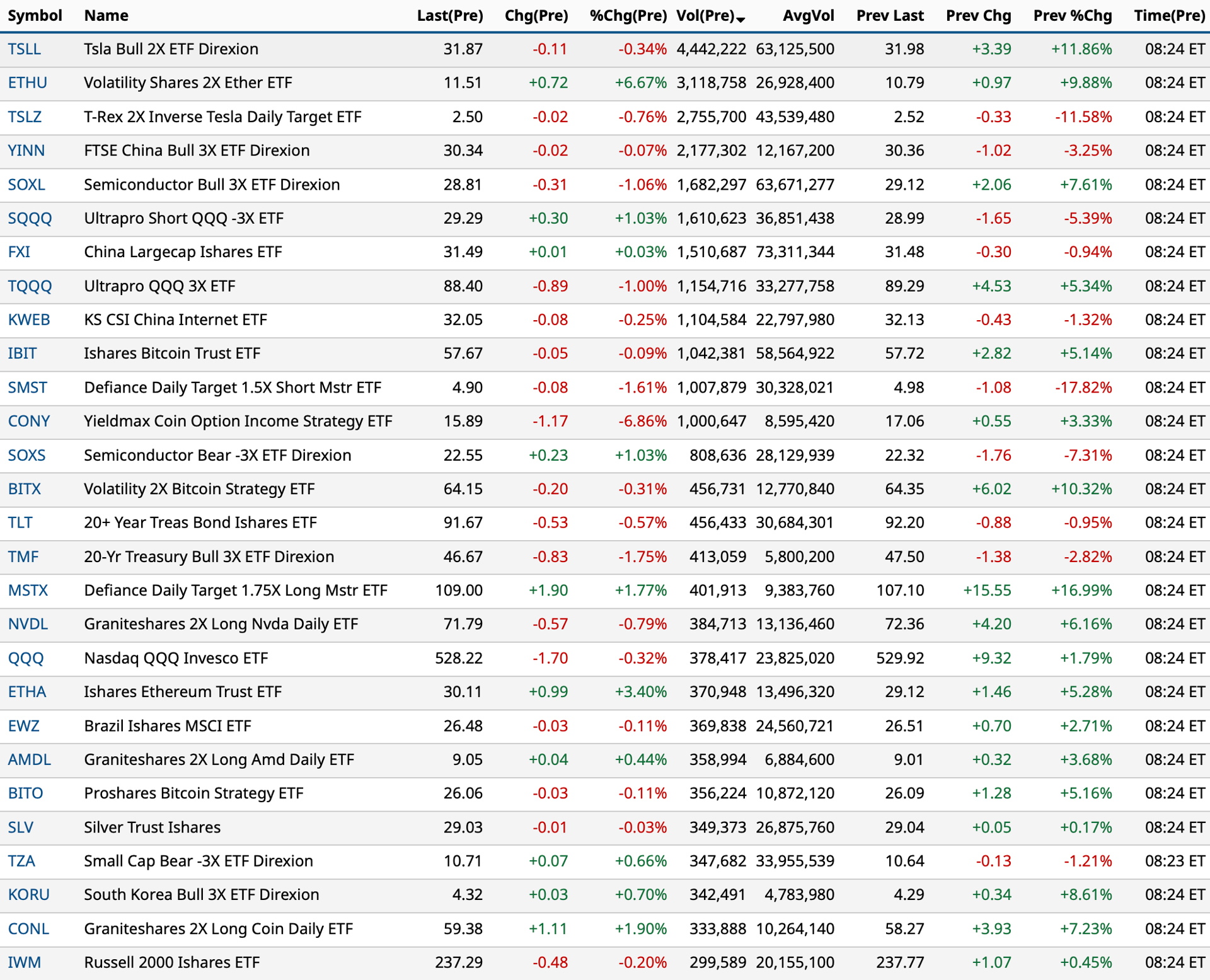

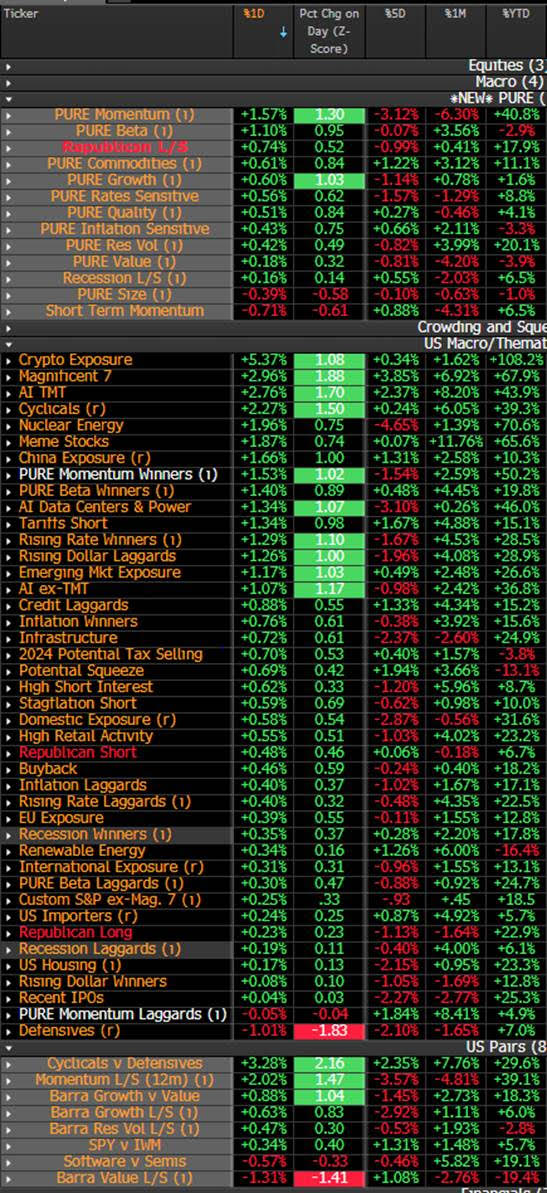

This is a valuable table for momentum-based short-term traders:

BY Doug Kass · Dec 12, 2024, 6:40 AM EST

From JPMorgan:

US: Futs are lower as bond yields rise 2-3bps across the curve; USD is weaker and cmdtys are mostly bid led by energy, Ags, and base metals. Pre-mkt, Mag7 names are mostly higher led by GOOG/TSLA, but Tech is lagging after NDX set an ATH yesterday. Banks are weaker despite positive reports at an industry conference. Today’s macro focus is on PPI and Jobless Claims.

and...

EQUITY AND MACRO NARRATIVE: Yesterday’s CPI print solidified the market’s expectation for a 25bps cut next week. While the first two days of the week were market by a cautious tone, the bullish narrative returned with Mag7, Semis, Cyclicals leading. For today and Friday, PPI is the main macro data point in the US with the ECB decision later this morning and more G7 Industrial Production/CPI releases still to come. On the earnings side, Broadcom and Costco are the major releases left this week and then FDX next week. The balance of the note includes (i) Roadmap to year-end); (ii) positioning update; (iii) quick thoughts on Jan 2025; (iii) 24Q4 earnings preview; (iv) macro calendar; and (v) a reposting of our Bull v. Bear debate.

BY Doug Kass · Dec 12, 2024, 6:30 AM EST

Bonus — Here are some great links:

S&P 6100 Target Has Been Achieved

BY Doug Kass · Dec 12, 2024, 6:10 AM EST

The S&P Short Range Oscillator is now in neutral — at 0.22% vs. -0.80%.

BY Doug Kass · Dec 12, 2024, 5:45 AM EST