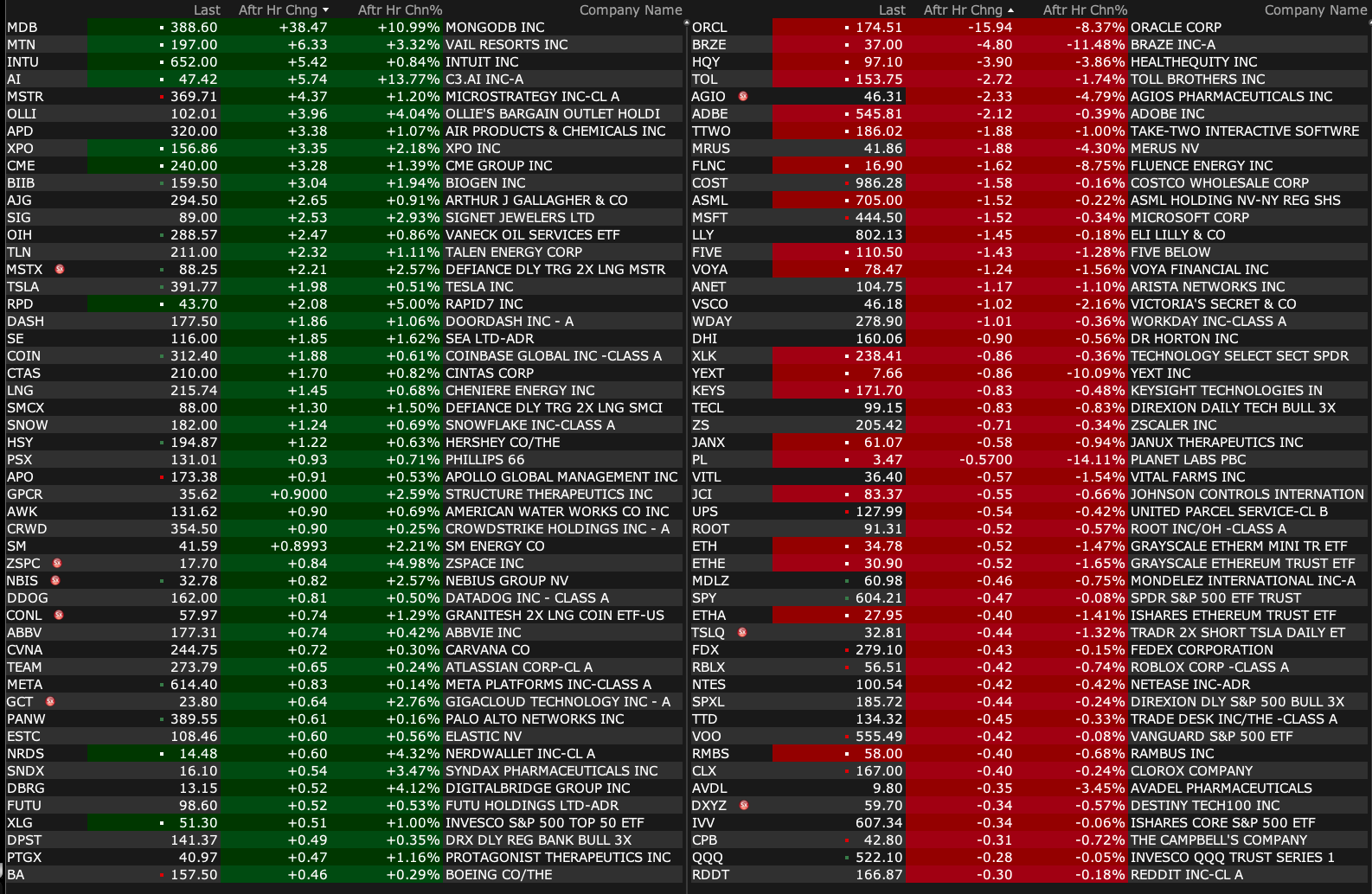

Monday's After-Hours Movers

As of 4:15 p.m.:

BY Doug Kass · Dec 9, 2024, 5:00 PM EST

As of 4:15 p.m.:

BY Doug Kass · Dec 9, 2024, 5:00 PM EST

BY Doug Kass · Dec 9, 2024, 4:40 PM EST

If you can get access to Rosie's latest piece (Rosie hasn't given me permission to reproduce his Lament of a Bear — The Sequel) it is really a good read.

Rosie makes some of the points — some of which we share (particularly the paper-thin equity risk premium).

I will have more on my general market view early tomorrow morning!

BY Doug Kass · Dec 9, 2024, 4:32 PM EST

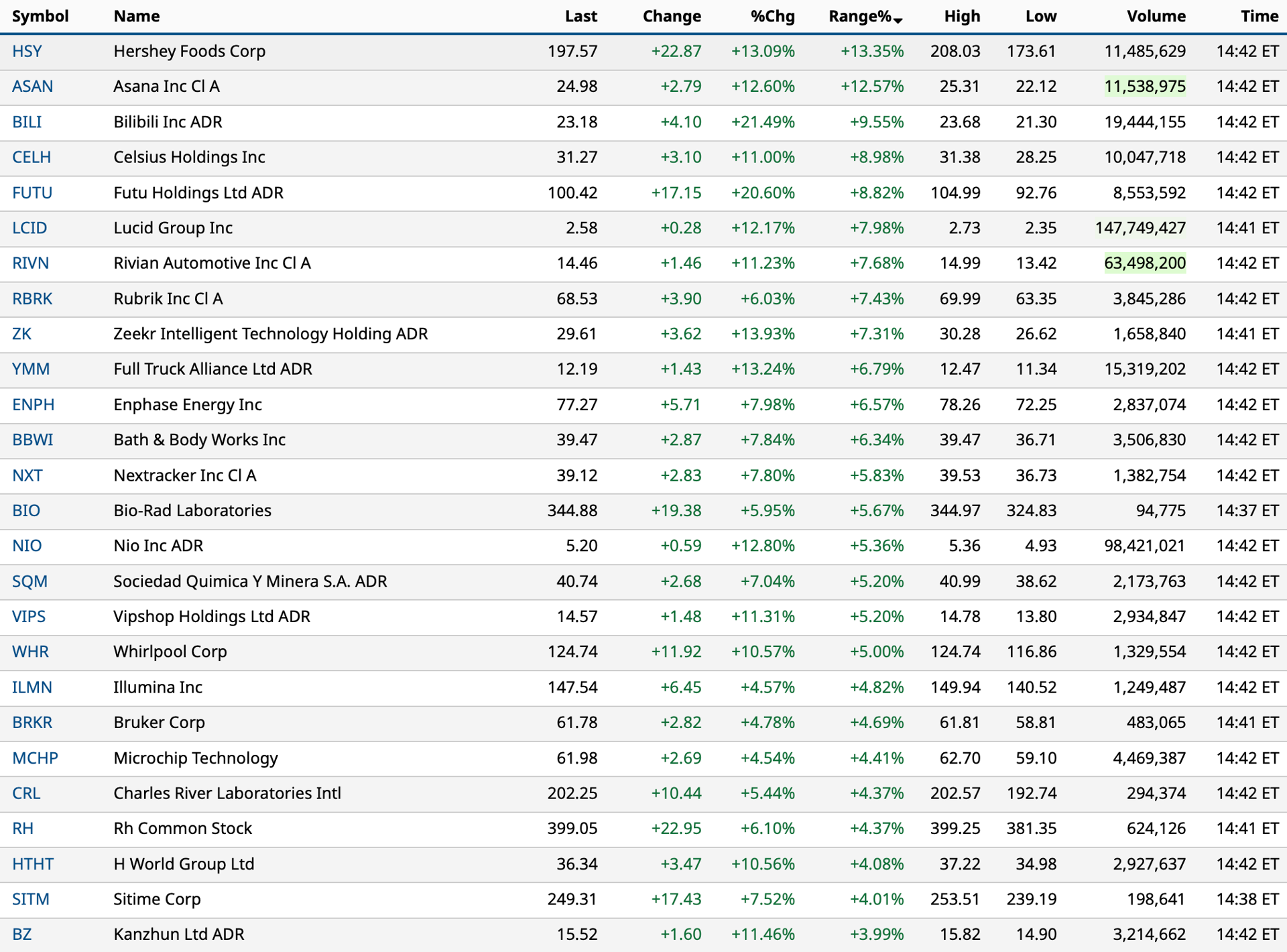

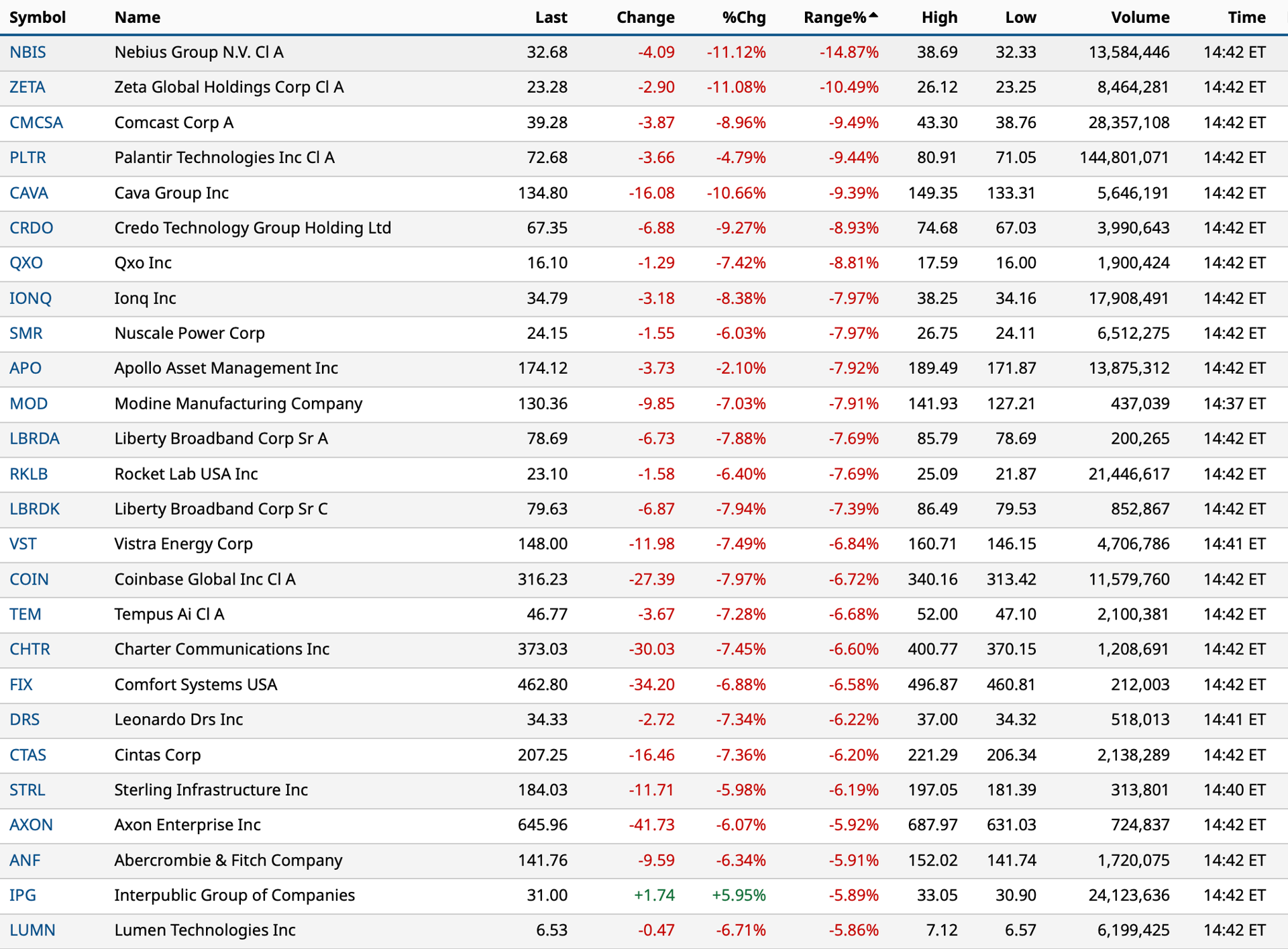

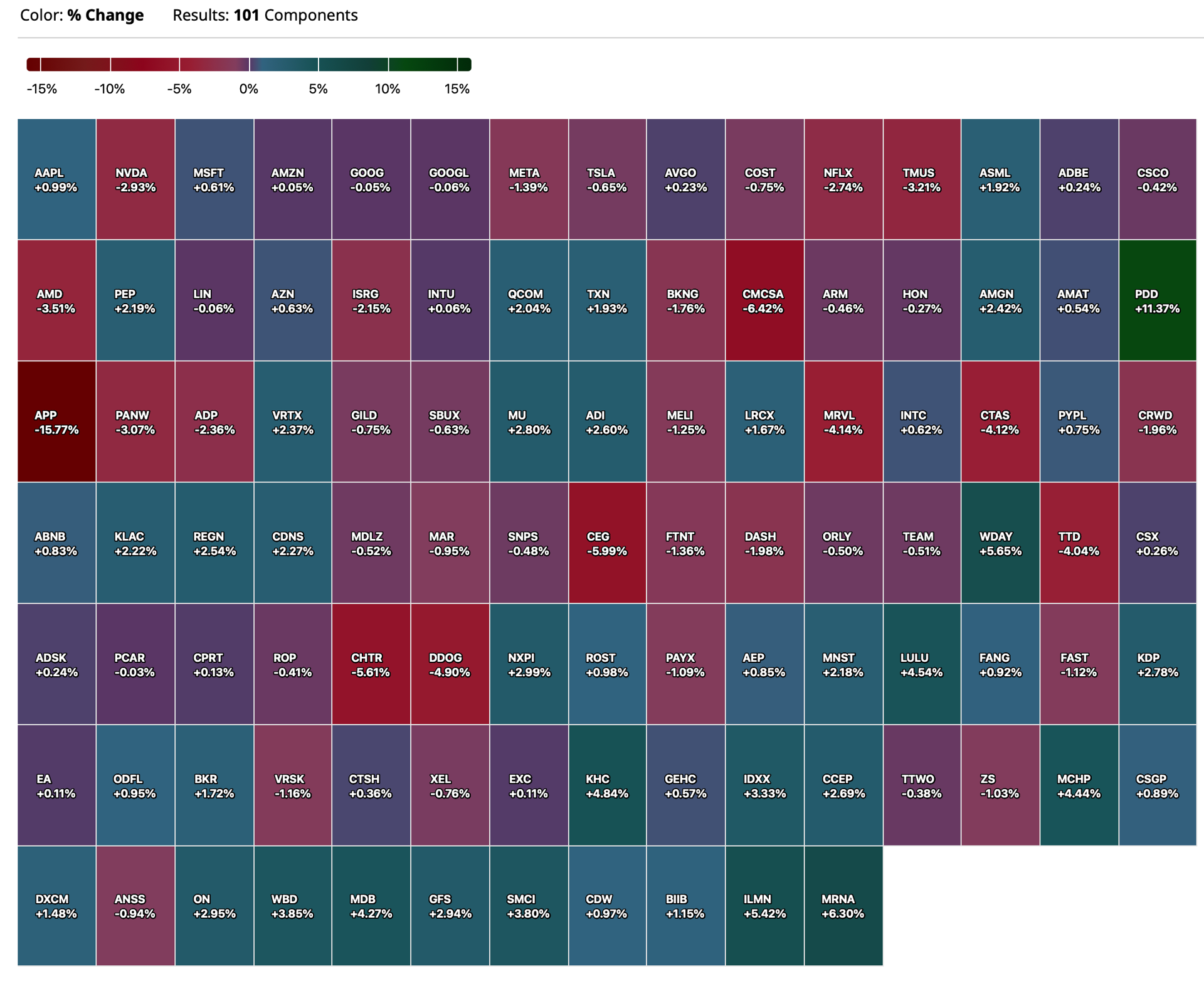

Large-cap stocks with widest % range on the day:

BY Doug Kass · Dec 9, 2024, 3:19 PM EST

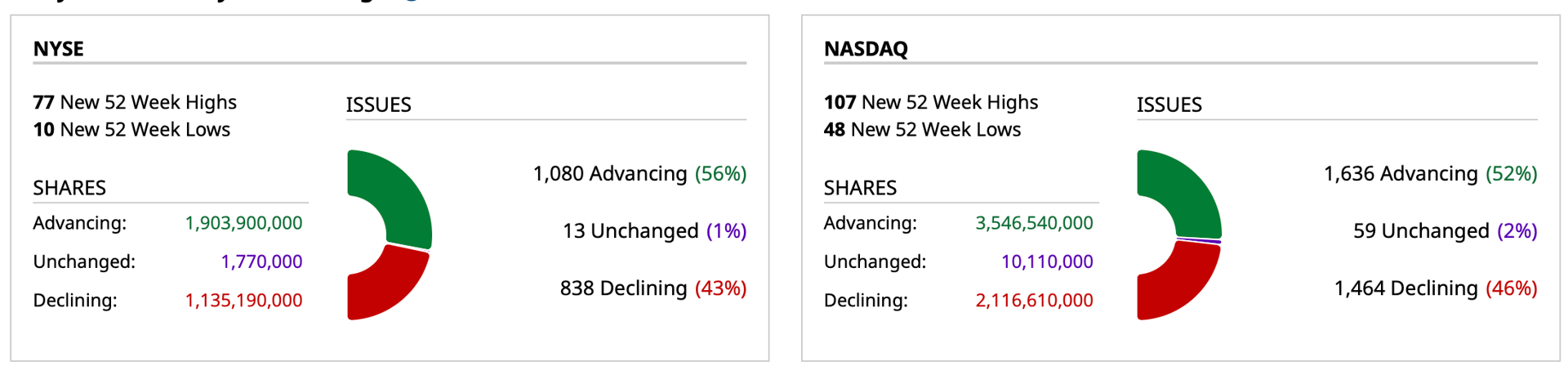

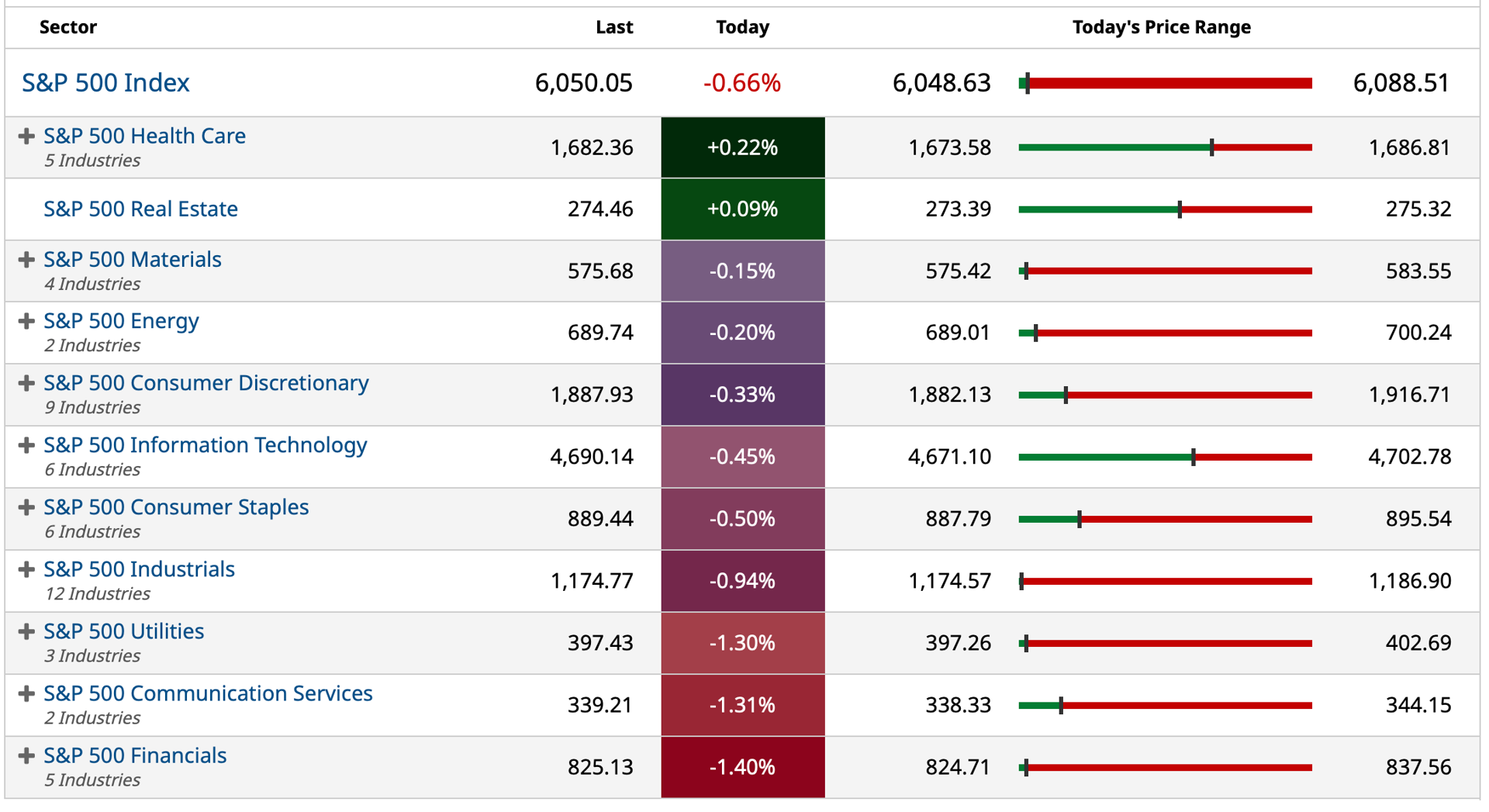

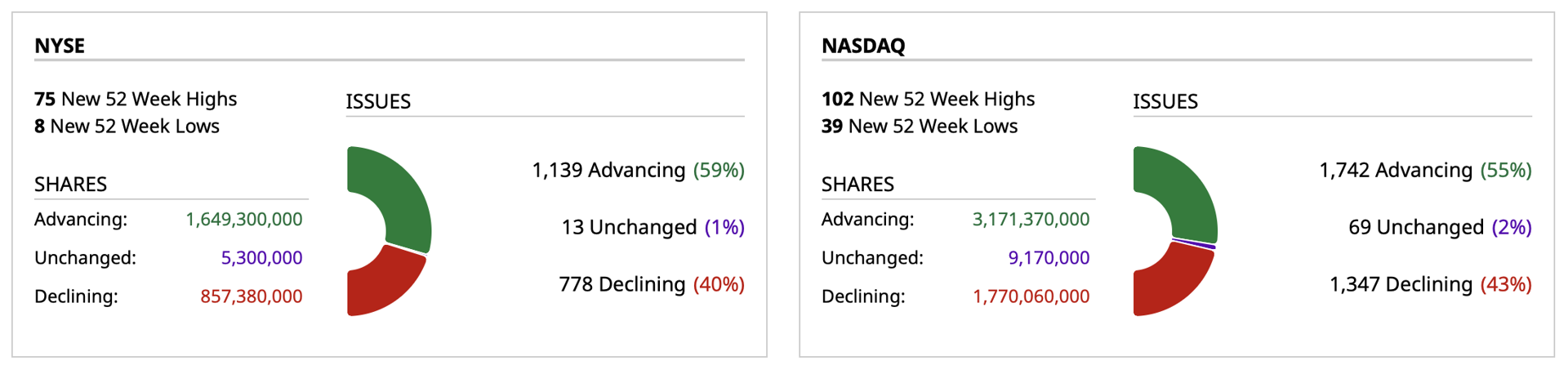

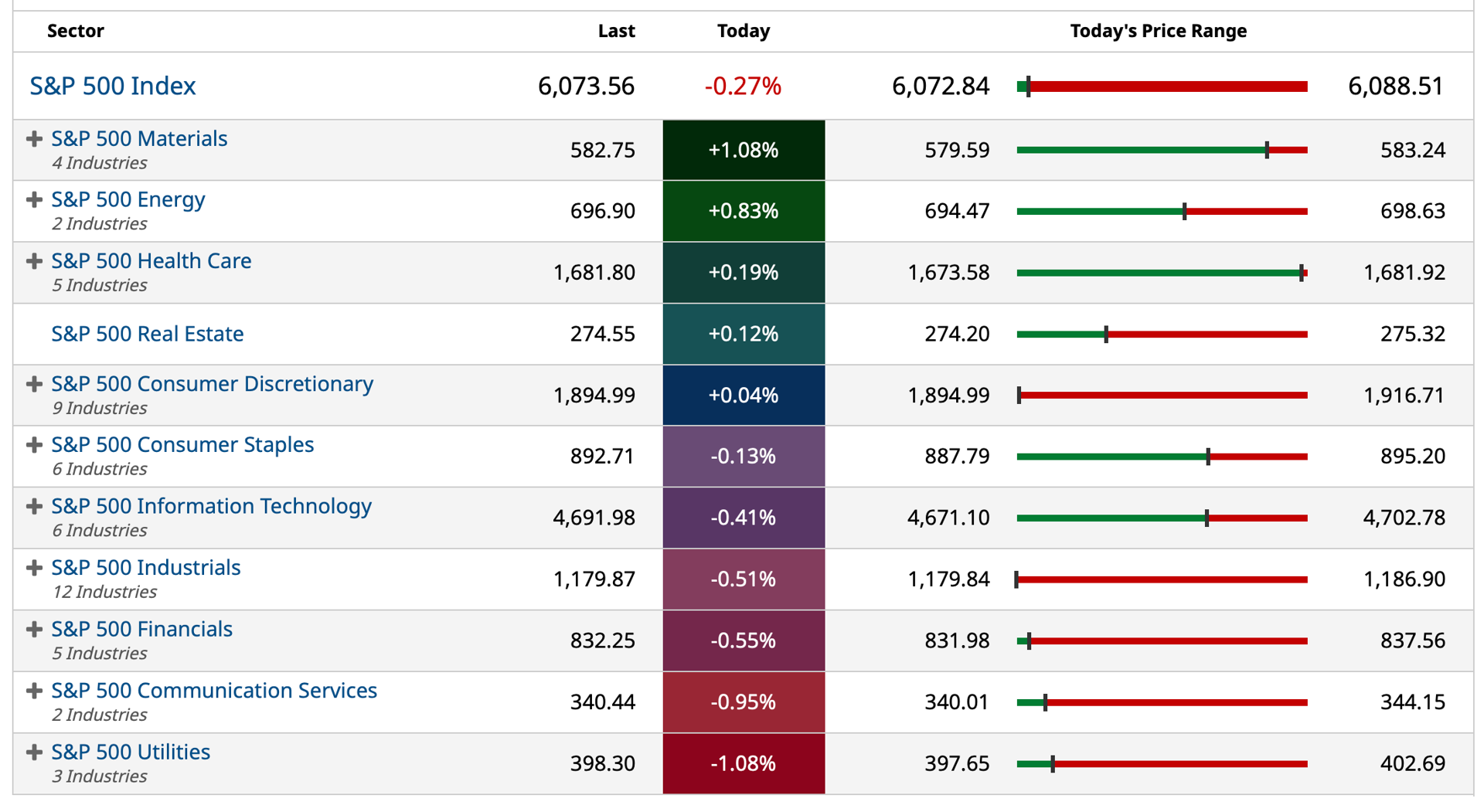

* Thus far, a clear change in market complexion from anytime since the November election.

* There were quite a few reversals of fortune — most noteworthy in private equity stocks that exploded to the upside in the early going and reversed hard (check out AINV, which was added to the S&P).

* Breadth was not terrible — thought the averages were terrible.

At 2:45 p.m. S&P cash was -34 handles.

Here are today's "Things:"

* Shorted PLTR in premarket at $80.95 and covered an hour or so later at $72.45.

* Shorted JPM at $227.51 (I lost my entire long position at expiration on Friday).

* Shorted more TSLA at $399.78.

* Shorted more AAPL at $245.47.

* Added to WMT short at $96.09.

* Added to HOOD short at $41.59.

* Added to AXP short at $304.01.

* Sold some BA long at about $161 (its up $20 in the last few weeks).

BY Doug Kass · Dec 9, 2024, 3:10 PM EST

I have two research calls at noon and 12:45 p.m. today.

BY Doug Kass · Dec 9, 2024, 12:50 PM EST

I just covered Palantir PLTR at $72.45 for a large gain (+$8.45/share) from the premarket.

From earlier:

I shorted - trading rental - Palantir (PLTR) (right before the opening at $80.95) only based on overbought and my proprietary stochastic guide.

Again I am being transparent and most should not short (especially a rocket ship called Palantir!)

This will be a quick trade - whether a win or a loss....

Position: Short PLTR

By Doug Kass Dec 9, 2024 9:44 AM EST

BY Doug Kass · Dec 9, 2024, 11:20 AM EST

- New York Stock Exchange volume is 30% above its one-month average;

- Nasdaq volume is 25% above its one-month average;

- Volatility Index: up 7.52% to 13.73

BY Doug Kass · Dec 9, 2024, 11:09 AM EST

* Shorted more AXP $304.41 and AAPL $244.07.

BY Doug Kass · Dec 9, 2024, 10:03 AM EST

From Peter Boockvar:

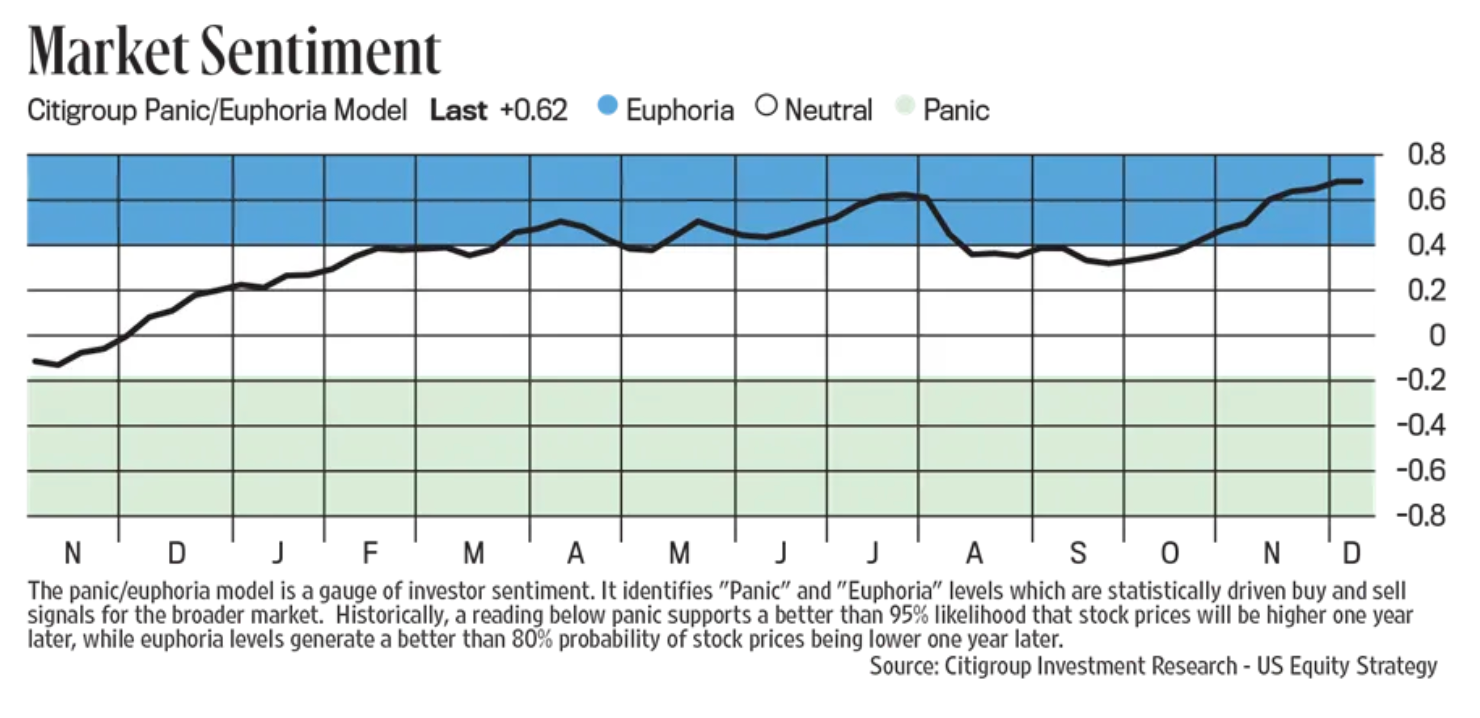

It doesn't matter until it does but something we should continue to acknowledge and be aware from a short term trading and contrarian perspective. That is the ever rising bullish sentiment that continues to get more extreme. The updated Citi Panic/Euphoria index rose to .62 w/o/w from .58 in the week before. It's now about 50% above the Euphoria threshold and above the previous July peak. Again, Citi claims that above .41 is statistically significant in terms of the one year performance from here.

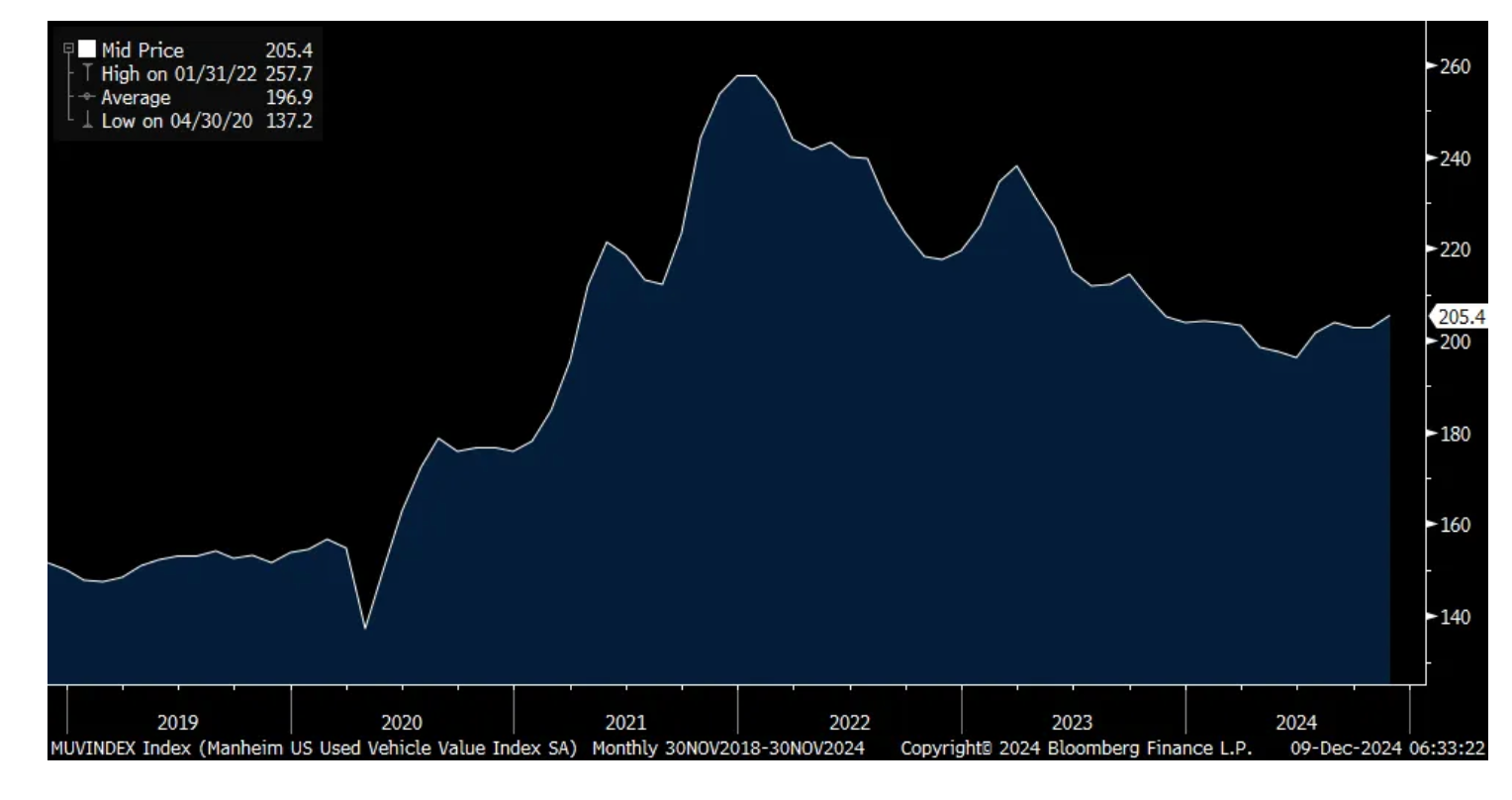

Ahead of the inflation stats this week, on Friday the Manheim used vehicle index measuring wholesale prices for November rose to the highest level since October 2023, up by 2.6% sequentially but flattish y/o/y. Manheim said "Wholesale values gave back a little bit of the strength we saw earlier in the month but depreciated less than what we normally see in November ... tight supply in wholesale and retail markets will support healthy dealer demand through the final month of the year."

Something to watch after the disinflation in goods prices we've seen. You've heard me say many times that with still below pre Covid trends in the sale of new cars means less used cars eventually in terms of supply.

Manheim Used Car Index

As we get closer to the holidays, air cargo rates continue higher. World ACD on Friday said "Worldwide air cargo rates rose to a 2024 high in November of US$ 2.76 per kilo, despite a slight (-2%) drop in flown tonnages compared with October." Average worldwide rates rose 6% m/o/m and are up 11% y/o/y. That combines both spot and contracted rates. As for spot rates, they are up 21% y/o/y and contract rates are higher by 10% y/o/y.

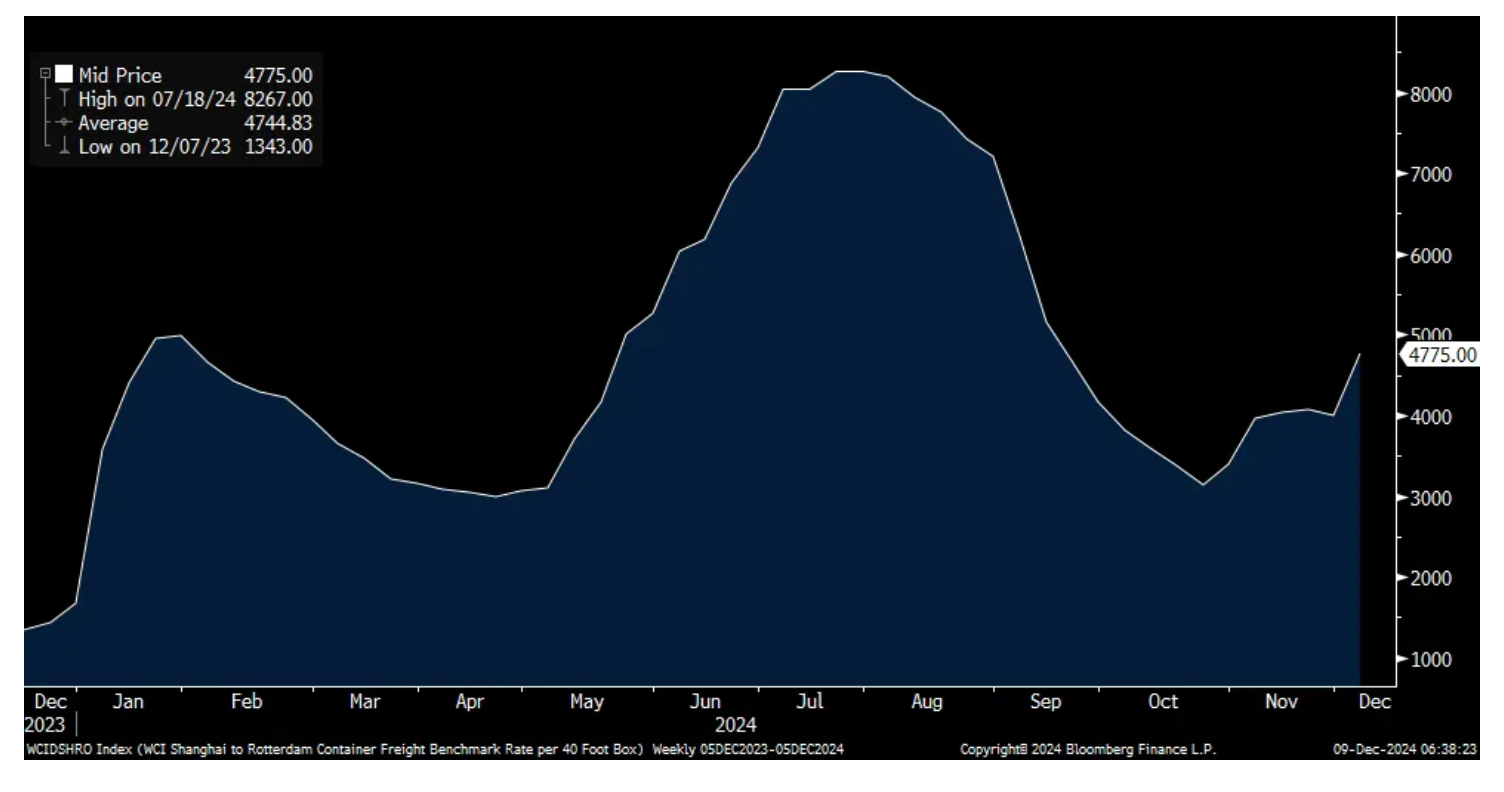

An update too on container shipping costs, the Shanghai to Rotterdam route saw a 20% w/o/w jump as of 12/5 to $4,775. While that is well off its summer high, it is up from $1,667 to start the year. In contrast, the Shanghai to LA route saw prices fell for a 5th straight week to $3,719 but compares with $2,100 at the beginning of the year.

I'll finish on transportation costs by looking at the updated Dry Van per mile rate as of yesterday and that stands just below the highest level since July at $1.67. That is up 3.7% y/o/y.

Bottom line, the path to a sustainable, and I emphasize 'sustainable', path to 2% inflation will not be easy. Yes, slower rents should keep a lid on services inflation in 2025 but on the other hand the CPI/PCE calculations never fully captured the spike in rents. We then watch, in part due to the things mentioned above, whether goods prices are bottoming.

WCI Shanghai to Rotterdam

Dry Van per mile

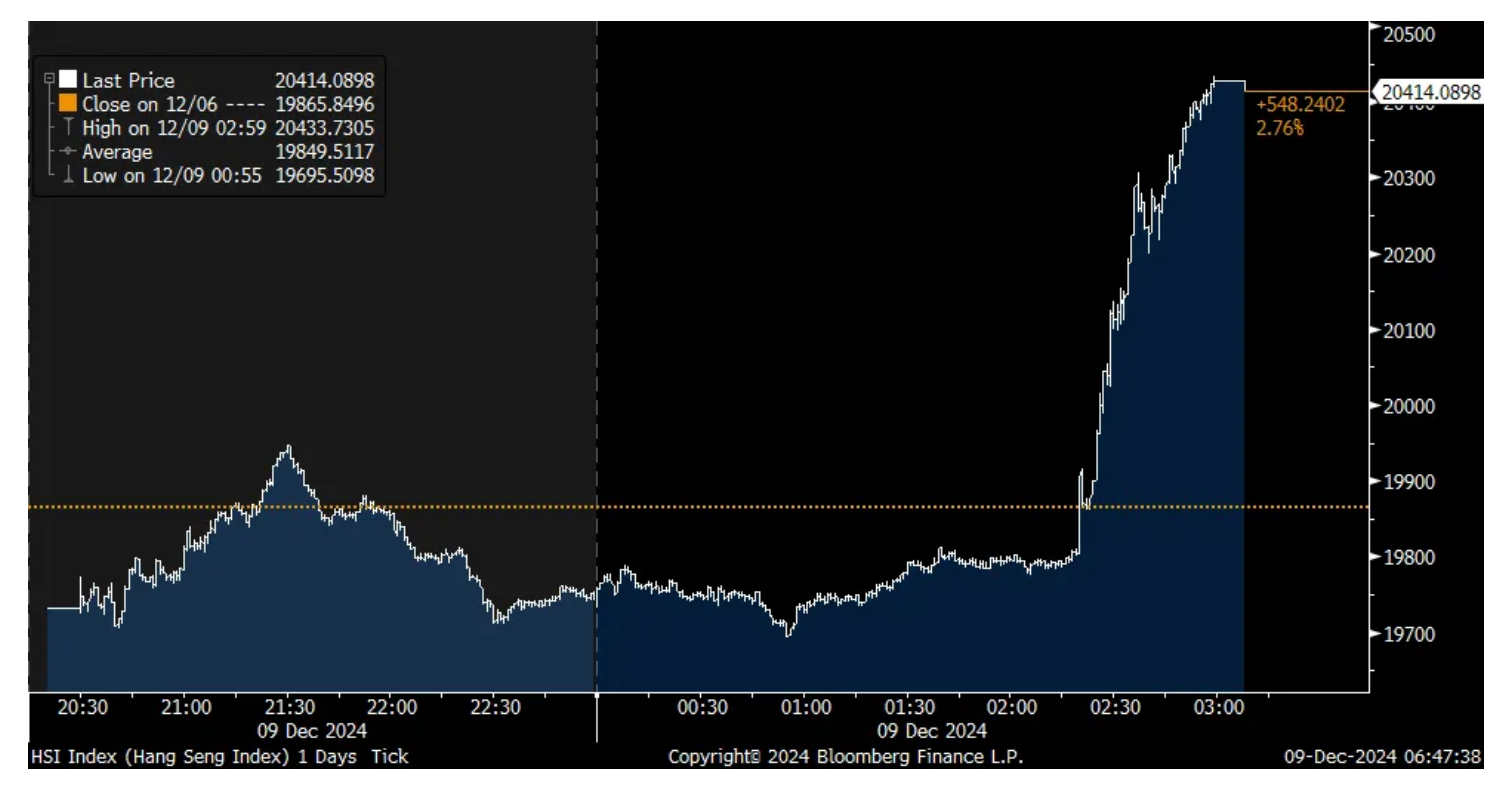

China stocks saw a late day rally after the printout of the Politburo meeting today came out and this was said on monetary policy, "A more proactive fiscal policy and an appropriately loose monetary policy should be implemented, enhancing the refining the policy toolkit, strengthening the extraordinary counter-cyclical adjustments." 'Appropriately loose' is what the markets are hanging their hat on as that is a change in tone as usually they say they will pursue 'prudent' monetary policy instead.

Hang Seng intraday

China also reported its inflation stats. Price stability for consumer prices is what they continue to see with prices up .2% y/o/y. Taking out both energy and food saw prices up .3%. While some cry 'deflation' as a problem here, stable prices is good for a still hesitant Chinese consumer. If you polled the US consumer and asked them whether they would choose a .2% rise y/o/y in their cost of living or 2%, the Fed's target, I'd bet 100% would say .2%.

PPI, more reflecting commodity prices and industrial pricing, saw prices drop by 2.5% y/o/y but which is less negative than expectations of 2.8% and vs -2.9% in October.

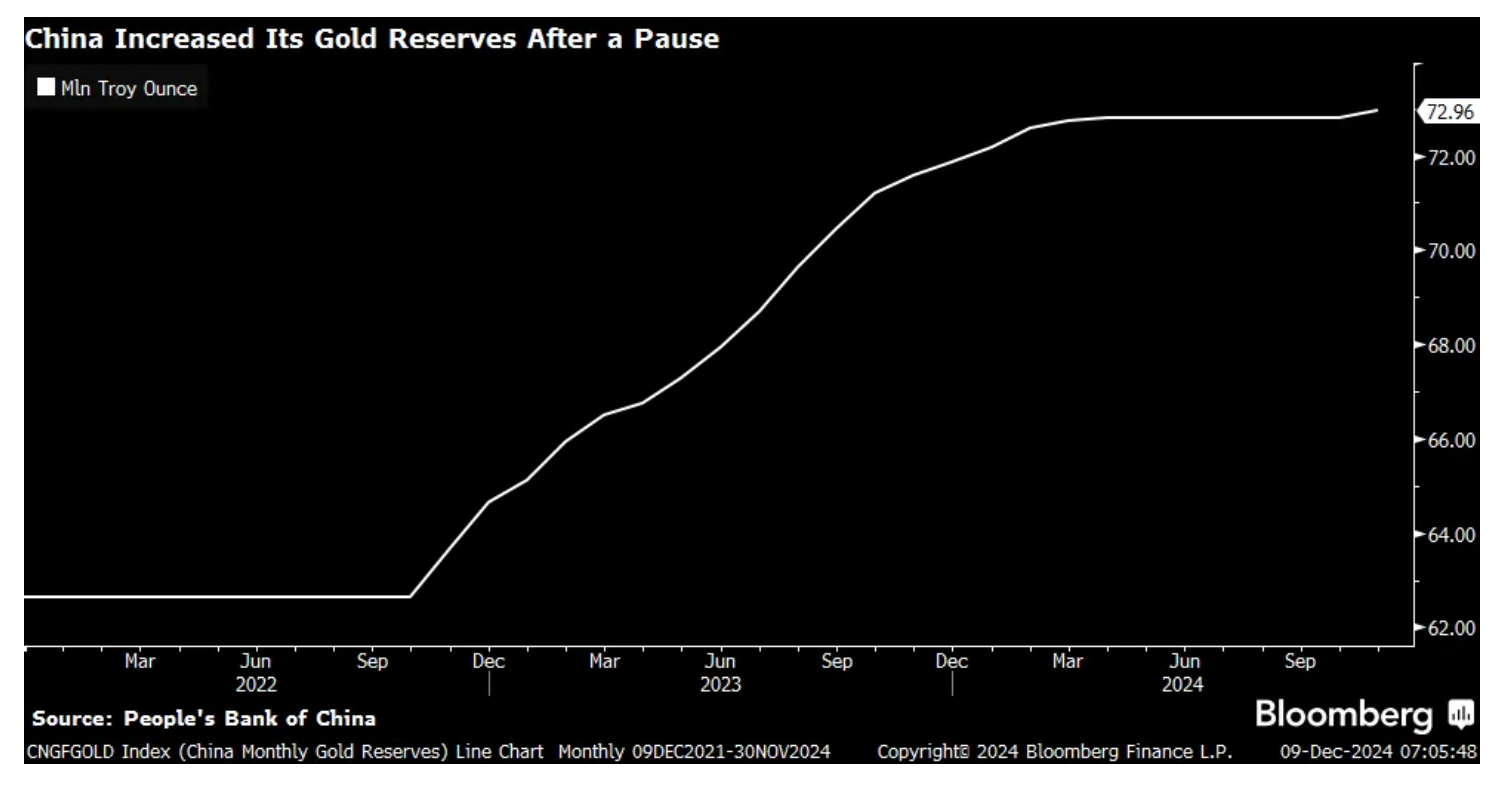

China too said they were back in the market in November buying gold, the first time since April according to the PBOC. Understand that the buying of gold has risen just as China's holdings of US Treasuries have fallen. Gold is higher by $18 in response to the news.

China Gold Holdings

China US Treasury Holdings in dollars ($772b currently)

Also from Asia, Taiwanese November exports rose 9.7% y/o/y, above the estimate of 8.4% with tech again the main focus and driver. Exports to the US rose 10.6% y/o/y and to China by 9.5%. Semi exports in particular jumped by 16% y/o/y. The TAIEX was up .3% and up by 30% year to date, just above the S&P 500.

Another reminder of the sclerotic economic situation in Europe, outside of some bright spots like Spain and Greece, the Sentix Investor Confidence index fell to -17.5 from -12.8 with both the current situation and expectation components lower. That is the lowest print in one year and, "There is also serious disappointment to report in the German data: Following the announcement of new elections to the German Bundestag, there is no mood of optimism." We know all about Germany's economic challenges.

Sentix

BY Doug Kass · Dec 9, 2024, 9:58 AM EST

I shorted - trading rental - Palantir PLTR (right before the opening at $80.95) only based on overbought and my proprietary stochastic guide.

Again I am being transparent and most should not short (especially a rocket ship called Palantir!)

This will be a quick trade - whether a win or a loss....

BY Doug Kass · Dec 9, 2024, 9:44 AM EST

* American Express AXP price target raised to $301 from $286 at JPMorgan JPMorgan raised the firm's price target on American Express to $301 from $286 and keeps a Neutral rating on the shares. The firm says market outcomes for consumer and specialty finance in 2025 will likely be determined by how far the Trump administration can go in implementing its policy objectives. The stocks already appear to be incorporating many of the more likely outcomes into valuations, with the sector factoring significant regulatory relief, less restrictive capital requirements, and higher capital returns, the analyst tells investors in a research note. JPMorgan believes this limits upside with risk/rewards "skewing unfavorably as premium valuations may constrain returns and downside scenarios could be exacerbated should events fail to unfold as expected."

* Bank of America BAC downgraded to Equal Weight from Overweight at Morgan Stanley Morgan Stanley downgraded Bank of America (BAC) to Equal Weight from Overweight with a price target of $55, up from $48. The firm now sees a more balanced risk reward and prefers money centers with a higher skew to capital markets, the analyst tells investors. In 2026, the firm estimates investment banking and trading will reflect 27% of revenues at BofA, 32% at Citi (C) and 68% at Goldman (GS), adding that in a bear case, BofA is more credit exposed versus capital markets pure plays.

* Wells Fargo WFC price target raised to $85 from $69 at UBS 08:26 UBS raised the firm's price target on Wells Fargo to $85 from $69 and keeps a Buy rating on the shares. The Fed's mid-December meeting "could be the final catalyst of the year for the banks," but this week's popular end-of-year peer conference will be the last time hearing from the companies, notes the analyst. The firm generally expects the updates on Q4 to be positive, but expects "scant '25 updates," the analyst added.

* Elanco ELAN initiated with a Buy at UBS UBS initiated coverage of Elanco with a Buy rating and $18 price target. The shares are down 19% year-to-date and 7% last week alone on Zenrelia concerns, the analyst tells investors in a research note. The firm believes the market is assuming a "bleak" Zenrelia outlook and nominal value to Elanco's other pipeline assets. However, the firm can "reasonably bridge" to accelerating EBITDA growth in 2026 from a 2025 trough. It believes the strong potential for EBITDA recovery against low downside risk "present a compelling 3:1 skew, highlighting an attractive long opportunity at depressed levels."

* Occidental Petroleum OXY price target lowered to $51 from $58 at UBS UBS lowered the firm's price target on Occidental Petroleum to $51 from $58 and keeps a Neutral rating on the shares. The firm sees "a mixed outlook for Energy in 2025," noting on the positive side that it sees natural gas momentum building, but adding that crude oil prices face downward pressure and "attractive valuations may not be enough to bring in new investors."

BY Doug Kass · Dec 9, 2024, 9:25 AM EST

-LDTC +448% (announces collaboration with Texas Instruments for Advanced Driver Assistance Systems and Autonomous Driving Solutions; enters into amendments to Credit Facility and Bridge Financing Offer)

-IPG +15% (Omnicom confirms to acquire Interpublic in all stock transaction; Interpublic shareholders will receive 0.344 Omnicom shares for each share of Interpublic common stock)

-MCRB +13% (FDA grants Breakthrough Therapy Designation to SER-155 for Reduction of Bloodstream Infections in Adults Undergoing Allogeneic Hematopoietic Stem Cell Transplant (allo-HSCT))

-QBTS +13% (enters into common stock sales agreement for $75M with Needham, Roth Capital, B. Riley, Craig-Hallum)

-SMCI +9.1% (announces Receipt of Extension from Nasdaq Stock Market; currently expects to file all the required reports by February 25th deadline)

-PLTR +7.3% (awarded one-year, $36.8M expansion of its contract with the U.S. Special Operations Command (USSOCOM) to deliver technology solutions in support of enterprise capabilities)

-STXS +5.9% (confirms JV Unit Magbot Robotic Magnetic Navigation Ablation Catheter Approved by China’s NMPA)

-ENTA +4.5% (announces positive topline results from First-in-Pediatrics Phase 2 Study Evaluating Zelicapavir for the Treatment of Respiratory Syncytial Virus (RSV))

-DOW +4.0% (announces partnership with Macquarie Asset Management to launch Diamond Infrastructure Solutions)

-ANGO +3.6% (receives FDA Clearance for The NanoKnife System for Prostate Tissue Ablation)

-KOD +3.6% (hearing Jefferies Raised KOD to Buy from Hold, price target: $20)

-SNDX +3.5% (announces additional positive data for Revuforj (revumenib) from AUGMENT-101 Trial in Relapsed or Refractory mNPM1 AML and BEAT AML Frontline Combination Trial)

-M +3.2% (Activist Barington Capital reportedly built stake in Macy's, seeking board representation and plans to push Macy's to make changes to boost its stock, including the creation of a separate real-estate unit )

-PRCH +2.5% (affirms Q4 adj EBITDA target)

-RIOT -5.4% (files to sell $500M of convertible senior notes due 2030)

-WOLF -3.6% (files mixed shelf of indeterminate amount; files to sell $200M in stock through equity distribution agreement)

-OMC -2.5% (Omnicom confirms to acquire Interpublic in all stock transaction; Interpublic shareholders will receive 0.344 Omnicom shares for each share of Interpublic common stock)

-NVDA -2.3% (China market regulator opens probe, suspecting NVIDIA of violating anti-monopoly laws in China related to Mellanox acquisition in 2020)

-NKLA -1.9% (files to sell 34.1M of common stock for holders)

BY Doug Kass · Dec 9, 2024, 9:15 AM EST

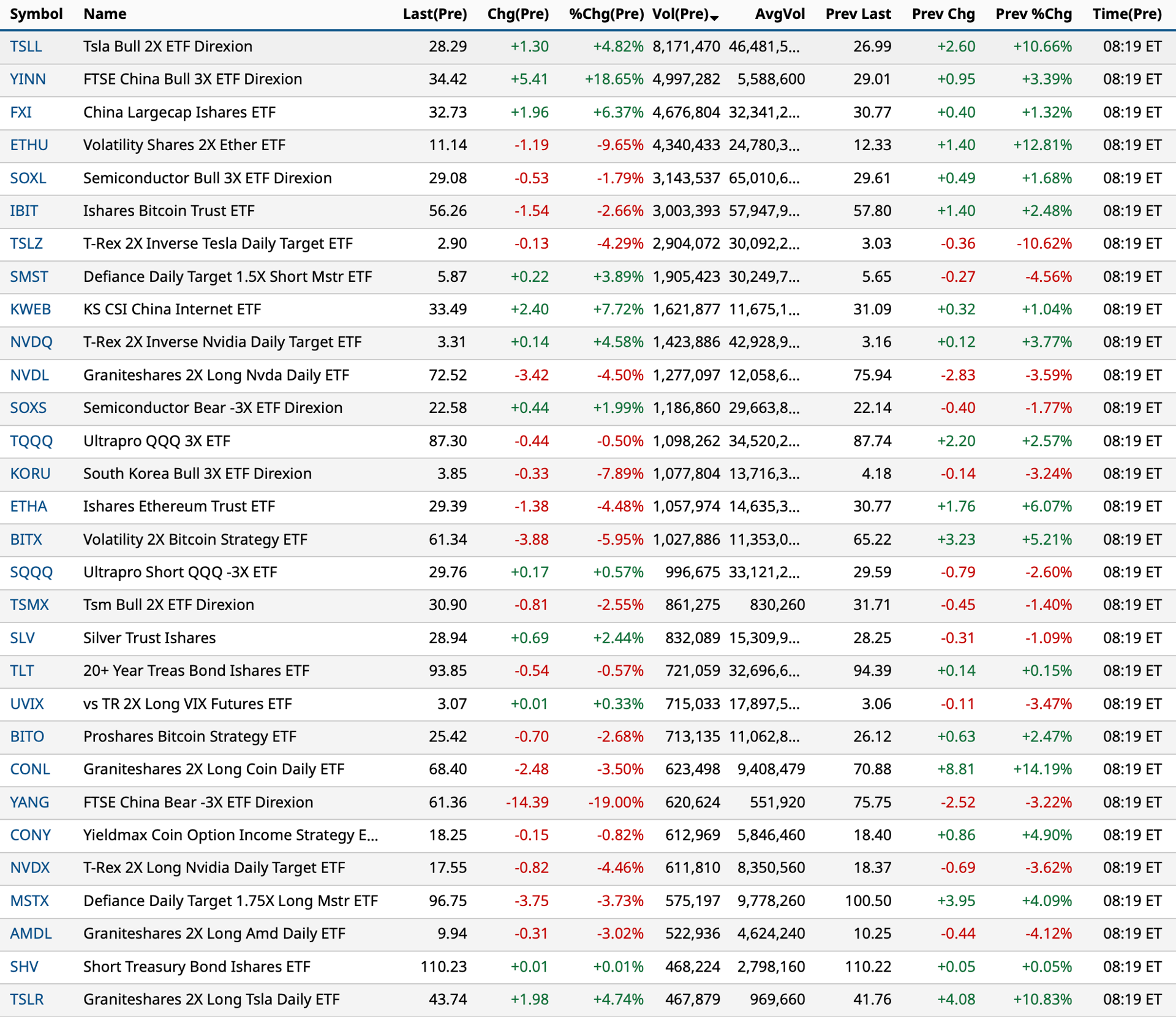

Charts from 8:19 a.m. ET:

BY Doug Kass · Dec 9, 2024, 9:00 AM EST

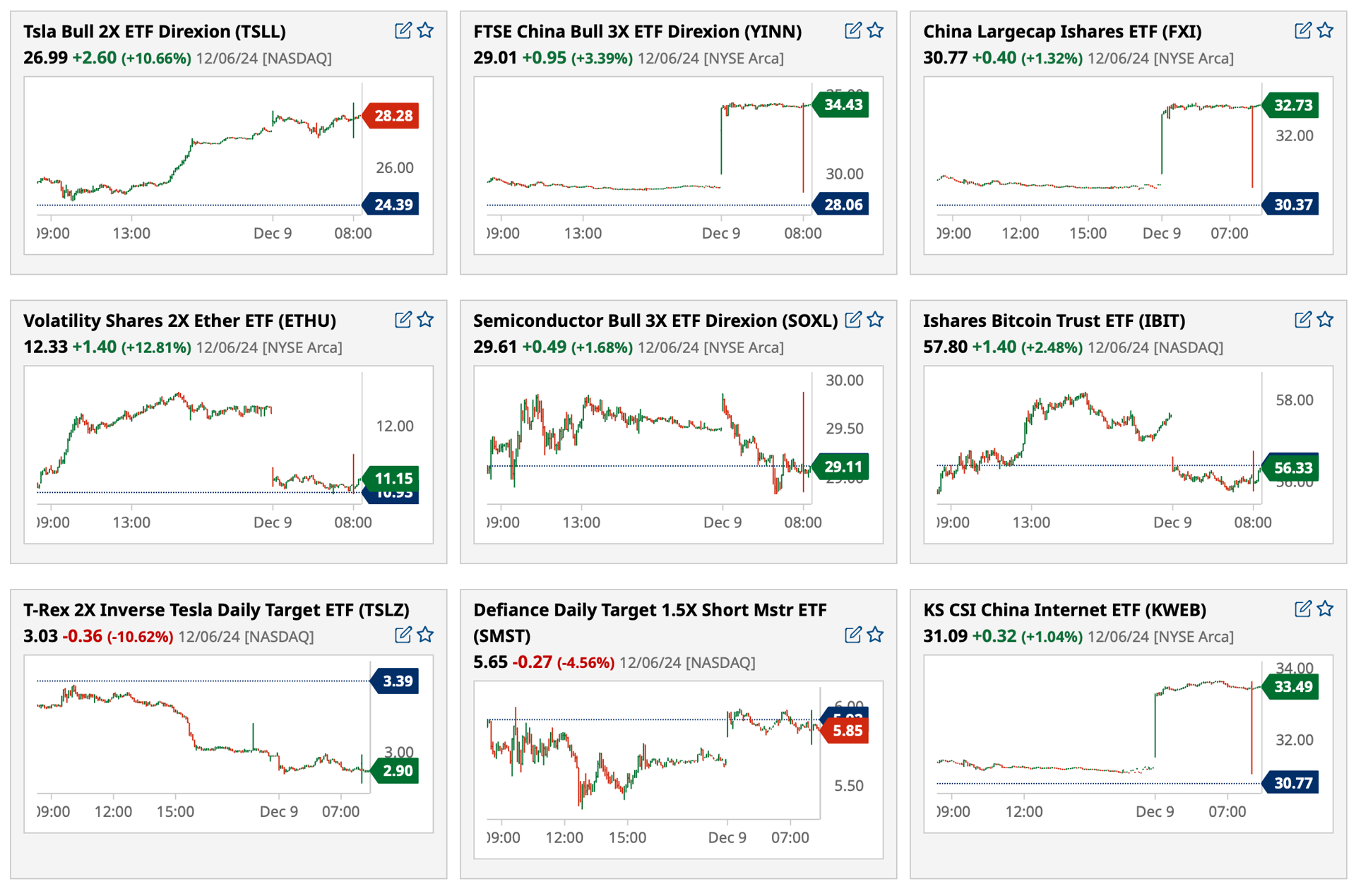

Chart from 8:37 a.m. ET:

BY Doug Kass · Dec 9, 2024, 8:46 AM EST

BY Doug Kass · Dec 9, 2024, 7:20 AM EST

This is a valuable chart for momentum-based short-term traders:

BY Doug Kass · Dec 9, 2024, 7:10 AM EST

From JPMorgan:

US: Futs are flat after SPX/NDX closed at record highs on Friday; Small-caps are outperforming. Pre-mkt, Mag7 is mixed while bond yields are flat to up 2bps. USD is being offered. Cmdtys are stronger, led by energy and base metals, as moves are being driven by the positive stimulus news from China. As the Fed enters its blackout window, the key macro data points are CPI/PPI, though it would take a tail-risk type of print to move the Fed away from cutting next.

and...

EQUITY AND MACRO NARRATIVE: Last week, SPX closed higher in 4 out of 5 trading days, with a WoW gain of +96bps; NDX added +3.3% WoW, while RTY declined -1.2%. The rally came with a narrow breadth: only 3 out of 11 sectors closed higher. Tech and Consumer were the standouts for the week, driven by encouraging earnings (CRM, MRVL, better-than-feared dollar stores earnings) and positive comments from MA/V on consumer spending. Macro data were mixed: we started the week with an upside surprise in ISM-Mfg and PMI-Mfg revisions, but the large miss in ISM-Srvcs pointed to some slowness in growth. Friday’s labor market data was marginally dovish: the U-3 rate was near cycle peak and in supportive of a December cut. The 10Y yield was flat and 2s/10s steepened 3.8bps. the DXY added +25bp. Commodities (BCOM) fell -67bp for the week as WTI declined -1.3%.

This week, CPI will be the main focus, along with control bank announcements (RBA, BoC, SNB and ECB). China will host its Central Economic Work Conference on Wed. On earnings, Tech (ORCL, ADBE, AVGO) and Consumer (COST) will remain the focus. The balance of this note includes sections on (i) Fedspeak; (ii) a macro data debrief; (iii) policy update post-US election; (iv) revisiting the bull v bear case; (v) macro data roadmap to year-end; (vi) tactical bull case on SX5E from Int’l Mkt Intel; (vii) previews for central banks activity; and (viii) an update from Positioning Intel.

BY Doug Kass · Dec 9, 2024, 6:55 AM EST

BY Doug Kass · Dec 9, 2024, 6:40 AM EST

I shorted more Tesla TSLA at around 8 p.m. Sunday night at $399.47.

Monday premarket trades:

* More shorts early this morning — Walmart WMT at $96.09 and American Express AXP at $303.53.

BY Doug Kass · Dec 9, 2024, 6:32 AM EST

BY Doug Kass · Dec 9, 2024, 6:20 AM EST

BY Doug Kass · Dec 9, 2024, 6:08 AM EST

BY Doug Kass · Dec 9, 2024, 5:55 AM EST

* Valuation excesses multiply...

The markets are overvalued by almost every historical metric:

BY Doug Kass · Dec 9, 2024, 5:45 AM EST