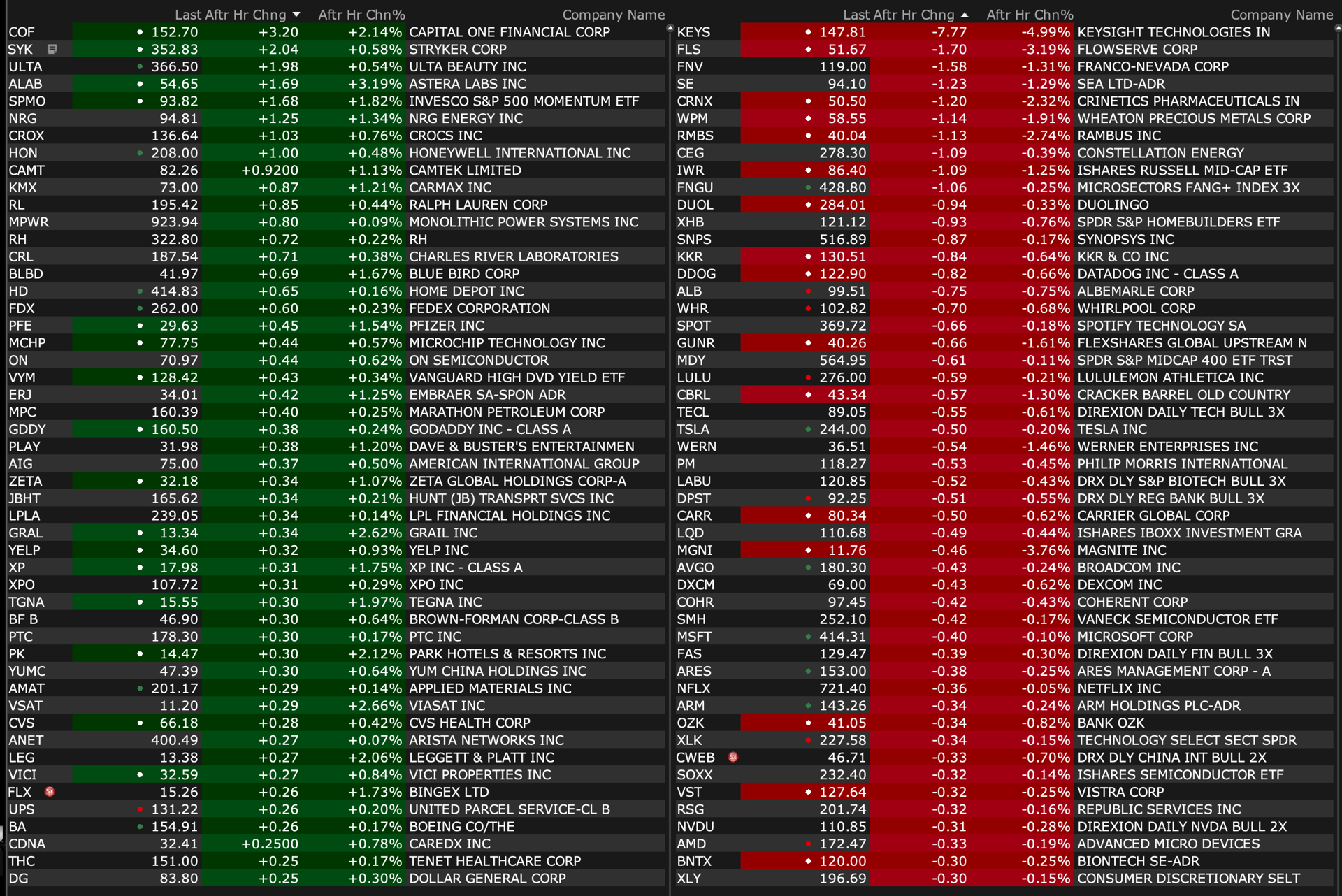

Tuesday's After-Hours Movers

As of 4:26 p.m.:

BY Doug Kass · Oct 8, 2024, 4:55 PM EDT

As of 4:26 p.m.:

BY Doug Kass · Oct 8, 2024, 4:55 PM EDT

BY Doug Kass · Oct 8, 2024, 4:39 PM EDT

From The Divine Ms M:

BY Doug Kass · Oct 8, 2024, 4:10 PM EDT

BY Doug Kass · Oct 8, 2024, 4:00 PM EDT

Equities rose "from flag pole to that's all." (That's an old horse racing term!)

There were no macro events that impacted the markets today.

Today's "things":

* Late last night —when SPOOS were flattish — I purchased SPY/QQQ common to offset my medium-sized short Index calls postion. Delta adjusted neutral going into today's trading day.

* Even though the equity market reversed yesterday's losses, the neutral Oscillator kept me from being aggressive on the short side. In looking at my trades, I made a lot of shorts, but sized very small today — especially with the rally not that broad (away from Mag 7).

* Shorted PEP (cost basis of $168.91) after lower organic growth. Currently the shares are +$2.80 to $170.

* Added to KO short at $69.37.

* Added to very small MCD short at $302.31.

* Added to an existing RBLX short at $40.01.

* Three tranches of small short Index calls: with S&P cash up 33 handles, 43 handles and 48 handles. (Currently +52 handles).

* Added small to all five homebuilder shorts: TOL at $152.06, GRBK at $79.21, DHI at $185.93, KBH at $80.58 and LEN at $182.32.

* I covered my entire ARES short (-$5) at $155-ish.

* New short TSLA at $243.37.

* Purchased more VRNOF at $3.28, GTBIF at $10.20 and MSOS at $6.90.

* Added to BABA at $109.97 short and PDD at $142.51 short.

* Added to AAPL short at $224.94.

BY Doug Kass · Oct 8, 2024, 3:30 PM EDT

I was disappointed for about 24 hours with my recent energy sales.

No more.

Oil vey.

A warning from five days ago:

Crude is +$1.91 but energy stocks are lower.

This is a warning signpost and makes me feel more comfortable about my recent energy sales.

By Doug Kass Oct 3, 2024 9:37 AM EDT

BY Doug Kass · Oct 8, 2024, 3:18 PM EDT

I added to all of my homebuilder shorts this afternoon.

BY Doug Kass · Oct 8, 2024, 1:57 PM EDT

I added to my Apple AAPL short at $224.93.

BY Doug Kass · Oct 8, 2024, 1:48 PM EDT

Run, don't walk to watch MRKT CALL with Guy and Carter now.

This is a place where there is true value-added information and Guy and Dan are among the only "talking heads" in the business media that are transparent and take ownership of their mistakes.

And its free!

Let's go to the videotape! Tech Stocks Lead Market Rebound (youtube.com)

BY Doug Kass · Oct 8, 2024, 1:26 PM EDT

I received this email from Tesla TSLA late yesterday:

Hello!

I hope you are doing well, I wanted to connect with you regarding your interest in Tesla. Please let me know if you have upcoming availability and I will give you a call back.

We are currently offering amazing incentives as well as price reductions on our vehicles!

Feel free to message me here or you can call me at 631-XXX-XXXX ext. XXXXXXX

Best,

Nick from Tesla Sent from my iPhone

BY Doug Kass · Oct 8, 2024, 12:22 PM EDT

With S&P cash +43 handles (I state this in my posts so you have a sense of my entry point levels), I am effecting my third tranche of Index shorts (via short calls) now.

BY Doug Kass · Oct 8, 2024, 12:13 PM EDT

At 11:15 a.m.

- NYSE volume 17% below its one-month average;

- NASDAQ volume 3% below its one-month average

BY Doug Kass · Oct 8, 2024, 11:40 AM EDT

Unfortunately I have a zoom funeral I want to attend over the next 60 minutes.

Radio silence.

BY Doug Kass · Oct 8, 2024, 11:20 AM EDT

With S&P cash +48 handles, I am entering my second tranche of short Index calls.

BY Doug Kass · Oct 8, 2024, 10:54 AM EDT

With S&P cash +33 handles I am adding to my SPY/QQQ November (in the money) call shorts. Now very slightly net short indexes (on delta adjusted basis).

BY Doug Kass · Oct 8, 2024, 10:41 AM EDT

From Peter Boockvar:

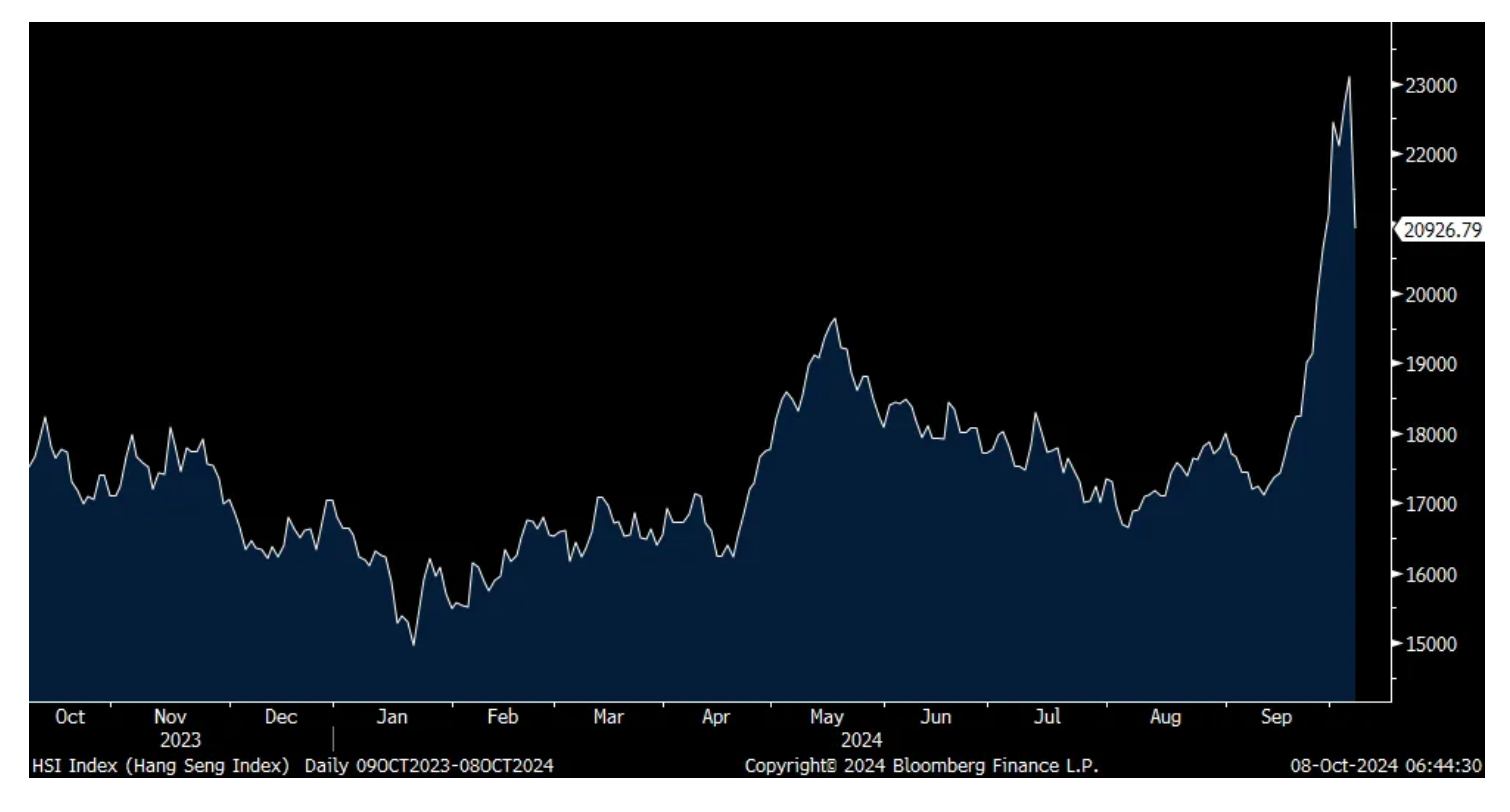

Chinese people are back from Golden Week vacation and the Chairman of the National Development and Reform Commission Zheng Shanjie held a press conference on the fiscal steps they are taking but the lack of firm detail was reason for the Hang Seng to take a break from its violent rally. It fell 9.4% overnight, though still up 23% year to date. Metals are pulling back too with copper down 2.6% and iron ore lower by 5.2%.

On the steps to boost interest in buying up some of the excess home inventory, I mentioned the Reuters story yesterday and today Bloomberg News is saying "Beijing city saw expressions of intent to buy new homes double in the first three days of October" CCTV reported. "In Shenzhen, sales of new homes jumped more than 10 times in the first six days of the month, while used home transactions more than tripled, Cailian reported, citing Shenzhen Centaline Property figures. Real estate agents in Shanghai rolled out a 'no closing hour' policy after visitors increased, while some buyers in Shenzhen even paid deposits for apartments without viewing them in person, according to the Securities Times." Hopefully there is follow through.

Hang Seng

The Dallas Fed released its October Banking Conditions Survey yesterday and said "Loan volume declined in October despite the drop in loan prices, which retreated for the first time since 2021. Overall, credit tightening continued and loan nonperformance rose but at slower pace for both. Bankers’ outlooks reversed sharply and turned optimistic. They expect a significant improvement in loan demand and business activity six months from now, although they foresee continued deterioration in loan performance in the next six months."

We assume expectations for a 'significant improvement in loan demand' is in response to the Fed rate cut and hopes for more but what if the Fed doesn't have enough wiggle room to sharply cut and it's more of a rate tweaking cycle? What if long rates go up while short rates go down as I think will happen?

While a non-voting member, it sounds like this Fed member wasn't on board with a 50 bps rate cut. Alberto Musalem, the relatively new St. Louis Fed president said yesterday "Given where the economy is today, I view the costs of easing too much too soon as greater than the costs of easing too little too late." These were prepared remarks and not an off the cuff response to a question. That said, he still said "I believe that further gradual reductions in the policy rate will likely be appropriate over time." Defining 'over time' will only come however in time.

If there is one thing that comes out when the Fed decides it's easing time is the dove or hawk true colors. Fed Governor Adriana Kugler is falling into the former camp. She said today in Europe, "While I believe the focus should remain on continuing to bring inflation to 2%, I support shifting attention to the maximum employment side of the FOMC's dual mandate as well." As to the strong payroll figure seen Friday, it was "very welcome" she said but "several metrics point toward labor market cooling" and the Fed is not just going to look at one payroll report above all else.

NY Fed president John Williams was talking to the FT and he covered all his bases and ended up saying nothing new. They reported, "If inflation fell even faster than expected, that 'would call for policy to normalize a little bit more quickly', he said. Conversely, if inflation stalled, 'that would call for interest rates to come down more slowly.' "

For perspective, the almost 40 bps rise in the 2 yr yield since the day before the Fed's September 50 bps rate cut was accompanied by a 30 bps rise in inflation expectations in the 2 yr TIP.

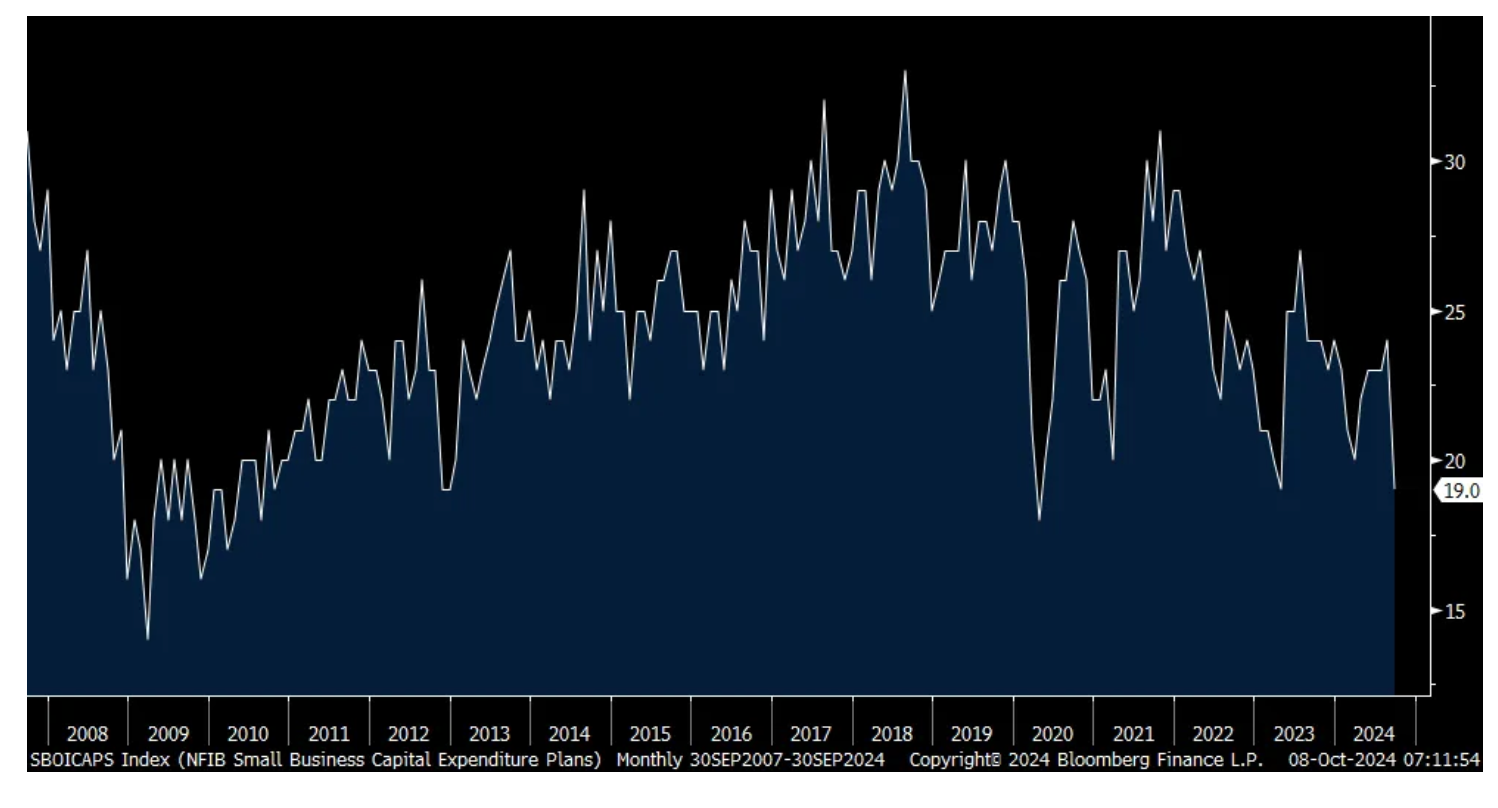

The September NFIB Small Business Optimism index rose a touch m/o/m to 91.5 from 91.2, though remaining soft. The 3 month average is now 92.1 and the 6 month average is 91.3 and continues to bounce along the bottom.

After falling 2 pts in August, Plan to Hire rose 2 pts in September. Of note, Job Openings Hard to Fill fell by 6 pts to the least since January 2021, pointing to the loosening of the labor market we've heard elsewhere. Compensation was little changed, down 1 pt but Compensation Plans rose 3 pts to the highest since January. What also stands out was the 5 pt drop in capital spending plans to 19% which also came with a 2 pt drop in Plan to Increase Inventory. That 19% figure matches the lowest since the Covid shutdowns and 2010 prior to that.

Those that Expect a Better Economy rose 1 pt but still deeply negative at -12%. Those that Expect Higher Sales fell 9 pts in August and rose 9 pts in September. There was no change to those that said it's a Good time to Expand. As for the earnings outlook, it dropped by 7 pts in August and rose 3 pts in September. Higher Selling Prices rose 2 pts after falling by a like amount in the month before.

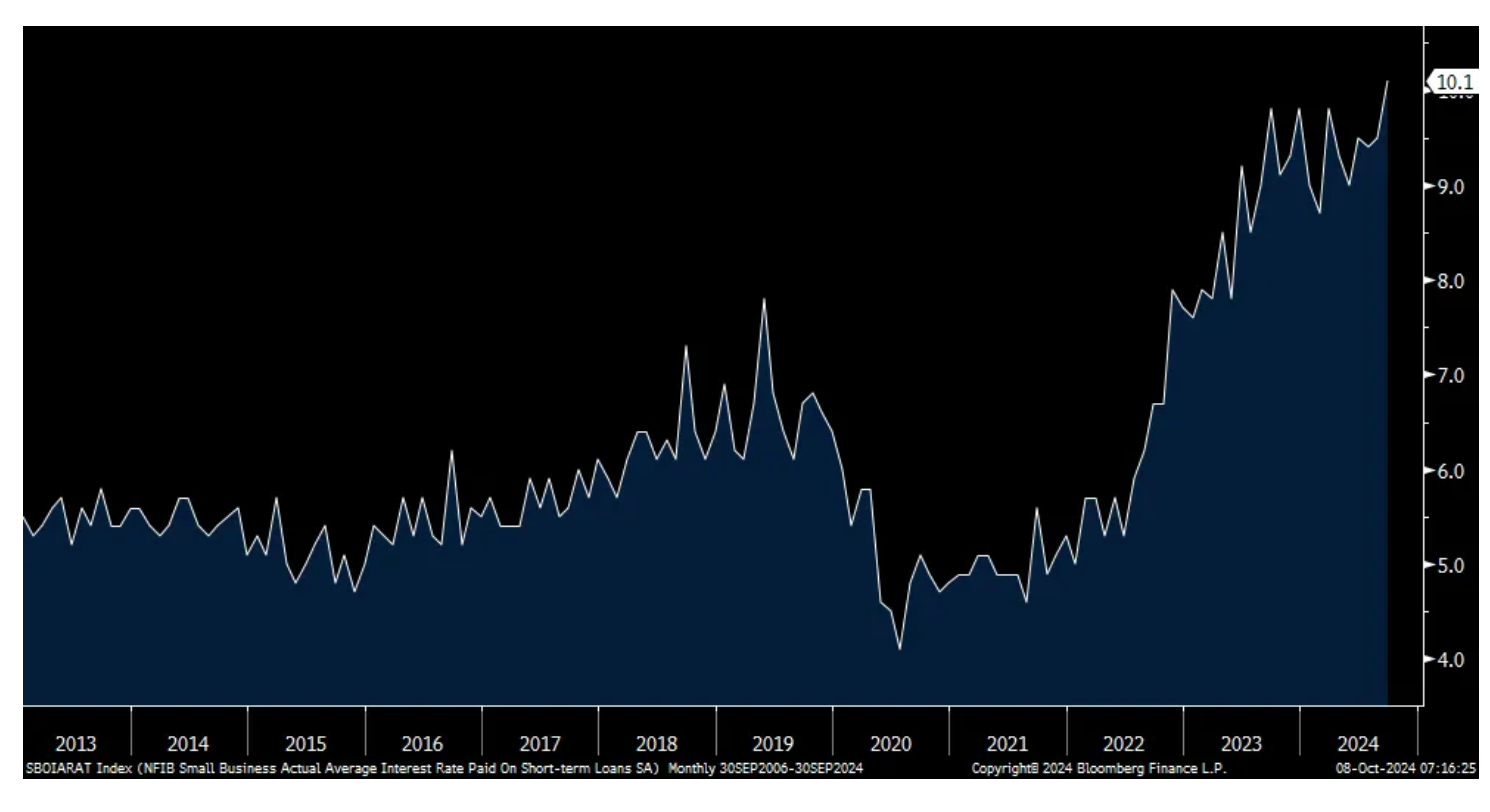

There was no easing of credit conditions but the average rate now paid on a loan rose to 10.1% from 9.5%. That is the highest cost of capital since the NFIB started tracking this in 2013.

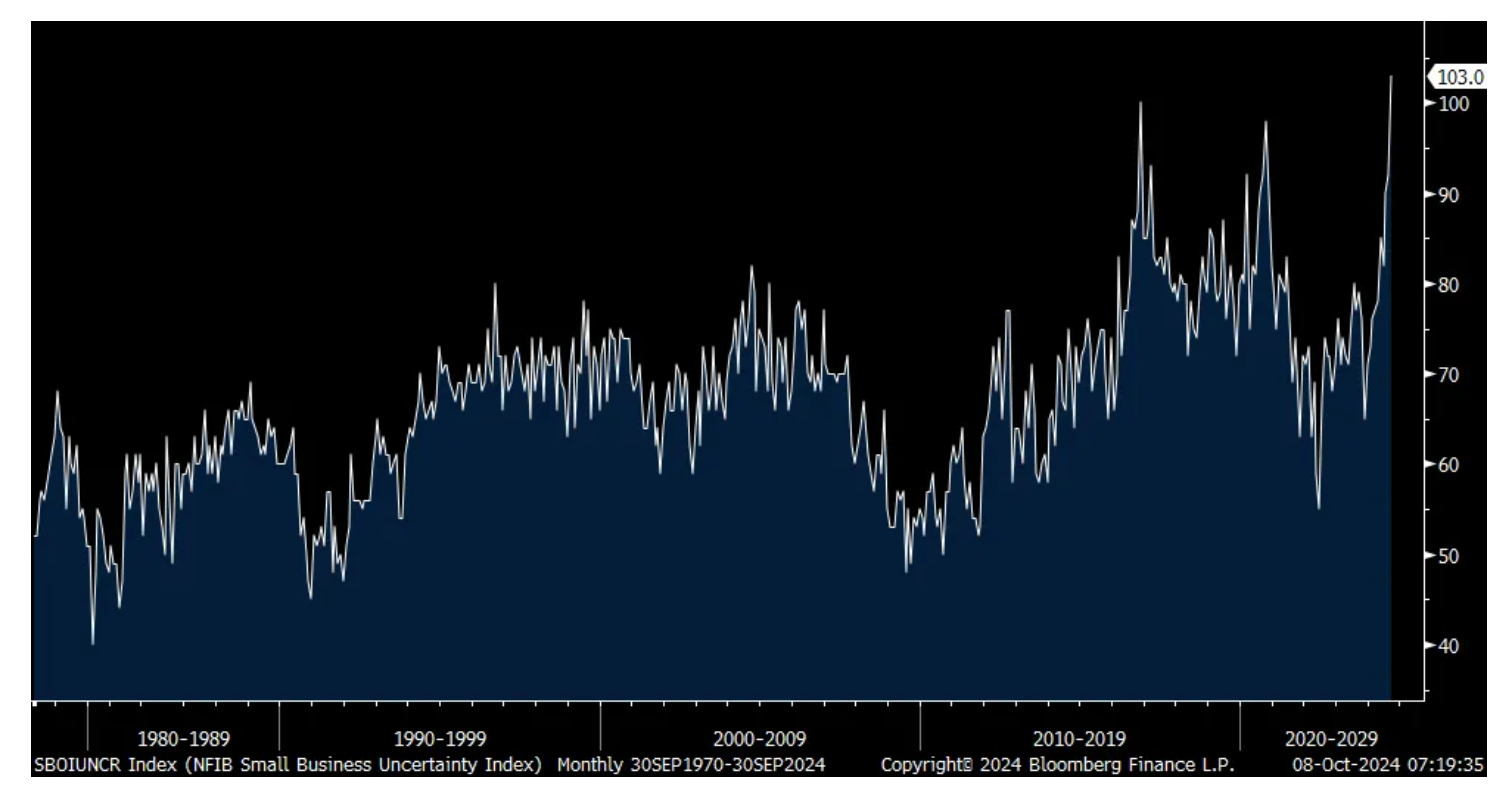

Finally, going back to 1975, the NFIB Uncertainty Index rose to a record high. I guess this makes sense in this upside-down, post inflationary spike and higher cost of money world and one month before a very consequential election, as every one seems to be.

The bottom line from the NFIB, "Small business owners are feeling more uncertain than ever. Uncertainty makes owners hesitant to invest in capital spending and inventory, especially as inflation and financing costs continue to put pressure on their bottom lines. Although some hope lies ahead in the holiday sales season, many Main Street owners are left questioning whether future business conditions will improve."

I'll add, there is no doubt that small to medium sized businesses have been less able to handle the current challenging economic environment relative to its big company peers. You can go by what the GDP figure says but if I had a dollar for every time I heard 'challenging macro economic environment' this year in hundreds of earnings conference calls...

NFIB

Job Openings Hard to Fill

Capital Spending Plans

Average Interest Rate Paid on a Loan

Uncertainty Index

Pepsi said this in their earnings release today:

"Our businesses remained resilient in the 3rd quarter, despite subdued category performance trends in North America, the continued impacts related to certain recalls at Quaker Foods North America and business disruptions due to rising geopolitical tensions in certain international markets."

A few things to note from overseas.

Taiwan said its September exports rose 4.5% y/o/y which was less than half the estimate of up 10.9%. Tech shipments remained solid, up by 50% y/o/y but was offset by weaker exports in industrial related products like chemicals and plastics with most of the world in a manufacturing recession.

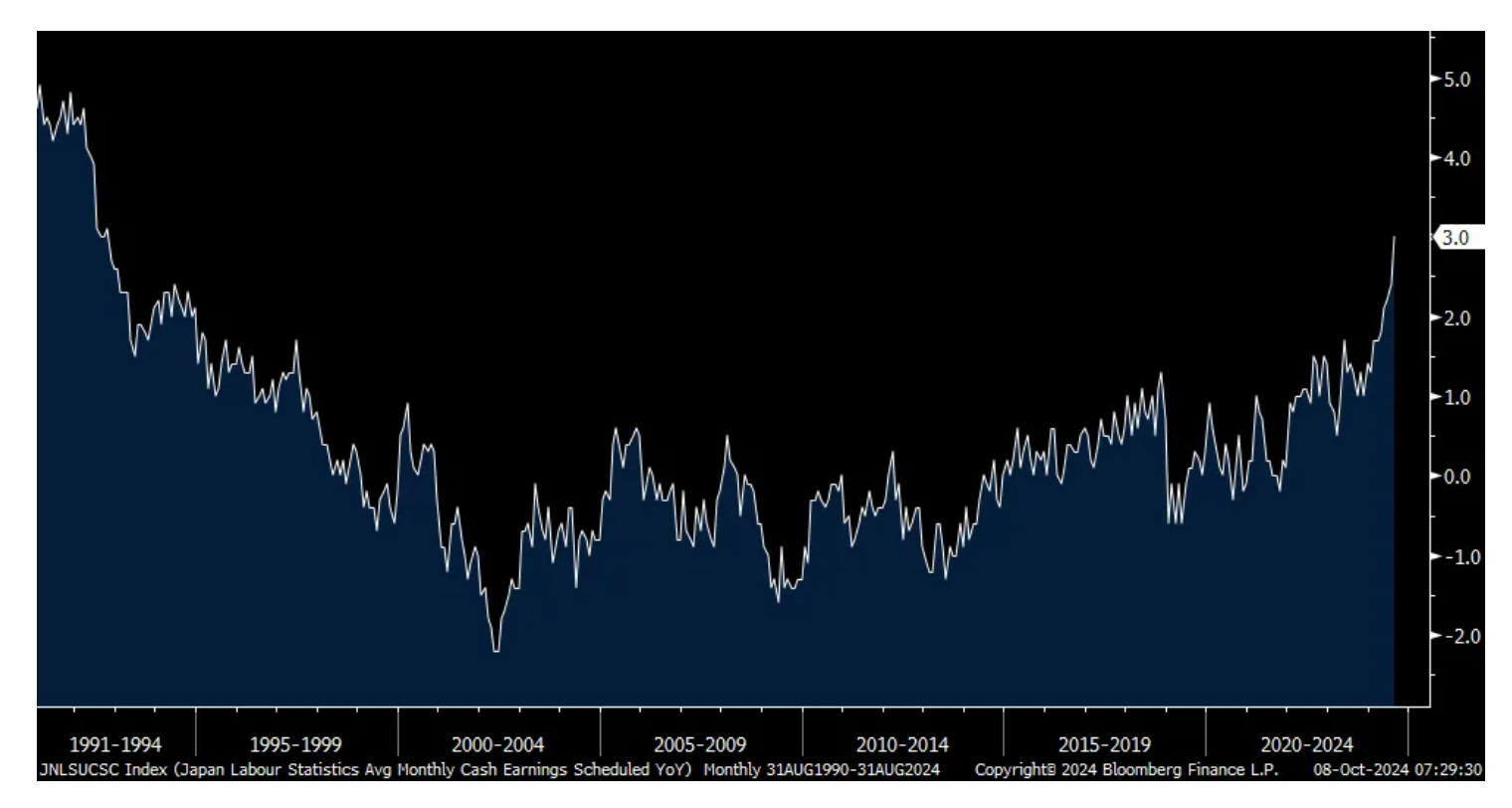

While the BoJ continues to hem and haw over when to raise interest rates again from .25%, base pay in Japan in August rose 3% y/o/y, up from 2.4% in July and it is the biggest increase since 1992. There wasn't much of a market move in response though as while the yen is up, it's up only slightly and JGB yields were little changed.

Base Pay Growth in Japan y/o/y

BY Doug Kass · Oct 8, 2024, 10:20 AM EDT

From one of my fave contributors, Peter Tchir:

STAFF

6 minutes ago

From Pro Contributor Peter Tchir:

I urged people to sell/reduce china exposure Monday on strength ahead of the reopening. I’m now deciding if this morning's selloff will be time to buy or still more downside. Entirely out of KWEB, have small FXI. Not sure which I’d buy back first or when.

BY Doug Kass · Oct 8, 2024, 9:50 AM EDT

Buying more GTBIF $10.20 and MSOS under $6.90 ("Trade of the Week").

As telegraphed, I am out of ARES short.

BY Doug Kass · Oct 8, 2024, 9:48 AM EDT

I am short TSLA at $243.

I am a scale seller on strength.

BY Doug Kass · Oct 8, 2024, 9:46 AM EDT

I moved to medium-sized short PEP at $168.67.

BY Doug Kass · Oct 8, 2024, 9:43 AM EDT

Ares ARES is making an acquisition of GCP International (Ares Management Corporation to Acquire GCP International) and the company is launching a convertible offering as the shares are -$5/share in premarket trading (Ares Management Announces Launch of Offering of Series B Mandatory Convertible Preferred Stock (yahoo.com)) .

The shares are trading -$5/share in premarket and I am starting to take in my short. (My entry point on this short was sub-optimal).

I plan to reshort on any strength.

BY Doug Kass · Oct 8, 2024, 9:35 AM EDT

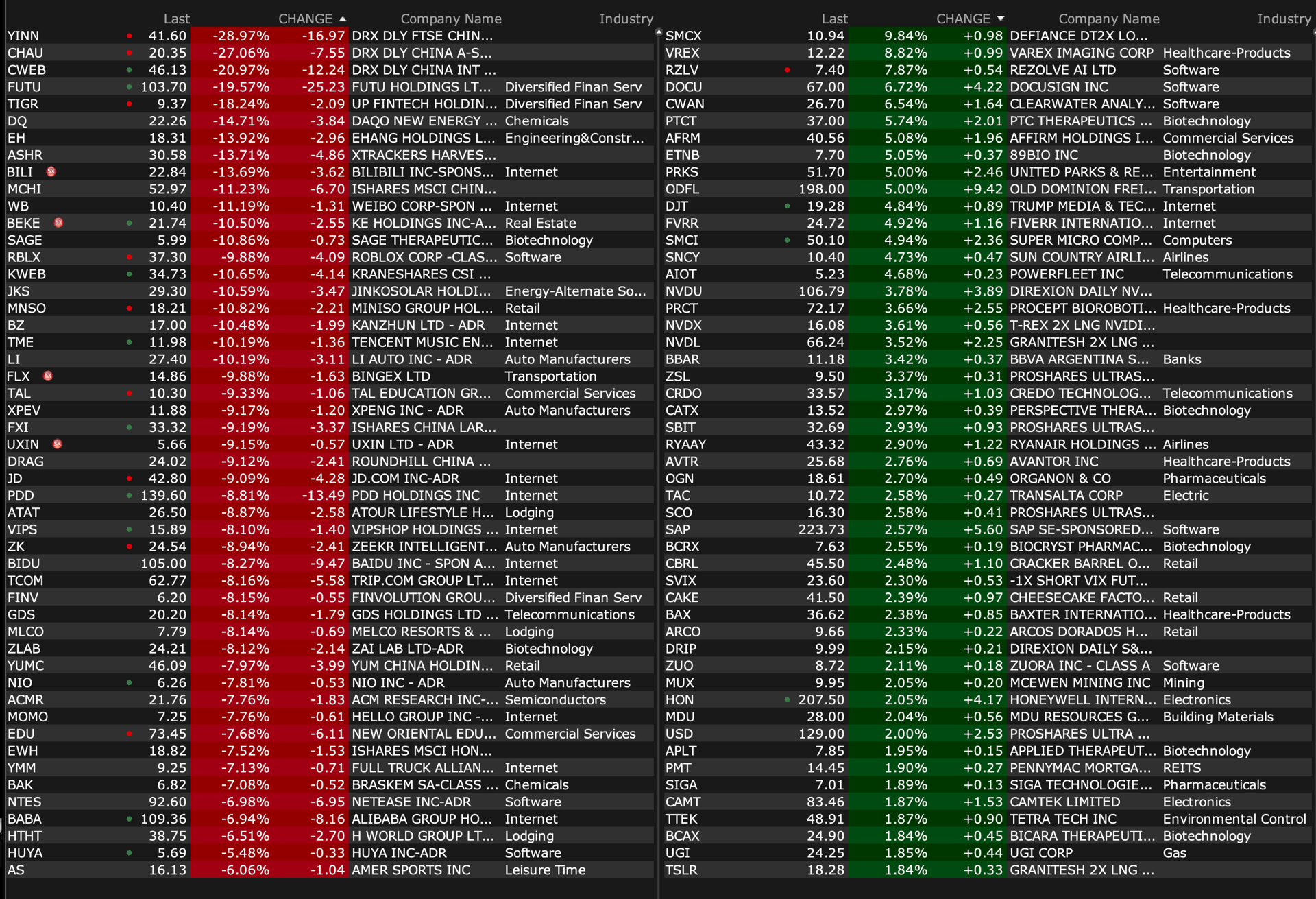

-AZUL +9.7% (reaches deal with lessors and manufacturers with 92% notes to eliminate obligations)

-SLNO +9.5% (FDA Review Division determined there does not appear to be a need for AdCom meeting at this time for NDA for DCCR (diazoxide choline) extended-release tablets for treatment of Prader-Willi syndrome (PWS))

-GNLN +9.1% (announces Non-Binding Letter of Intent to Distribute the CURB Lifestyle, Inc. Breakthrough Inhalation Device Technology for Nicotine, Cannabinoids and Other Wellness Compounds)

-DOCU +5.8% (to be added to S&P400 index)

-OCX +5.0% (DetermaIO Immuno-Oncology Assay Predicts Response to Atezolizumab in Phase 2 Clinical Trial)

-SMCI +4.7% (momentum driven by strong AI demand)

-AISP +3.7% (announces $1.2M Contract Award with Fortune 100 Transportation & E-Commerce Company for Acropolis Enterprise Video and Data Management Platform)

-MDU +2.0% (entering S&P Smallcap 600 Index)

-HON +1.8% (confirms plan to spin off advanced materials business to shareowners)

-SAGE -11% (Phase 2 LIGHTWAVE Study of Dalzanemdor (SAGE-718) in Treatment of Mild Cognitive Impairment and Mild Dementia in Alzheimer’s Disease did not demonstrate a statistically significant difference from baseline)

-KWEB -10% (weakness off less than hoped for stimulus)

-FXI -8.6% (weakness off less than hoped for stimulus)

-BIDU -7.8% (names Junjie He as interim CFO, effective immediately)

-BABA -6.4% (Cetera Investment Advisers sells shares)

-BDTX -3.0% (announces Restructuring Plan to Focus Resources on BDTX-1535 and Extend Cash Runway into 2Q25; CFO to depart)

-SCLX -2.8% (files to sell up to 11M shares, 5.5M warrants and up to 71.5M shares on behalf of holders)

-SRRK -2.7% (announces $275M Proposed Public Offering of Common Stock and Pre-Funded Warrants)

-ARES -1.8% (confirms to Acquire GLP's international business GCP International for $3.7B; launches 27.0M share offering of series B mandatory convertible preferred stock)

BY Doug Kass · Oct 8, 2024, 9:19 AM EDT

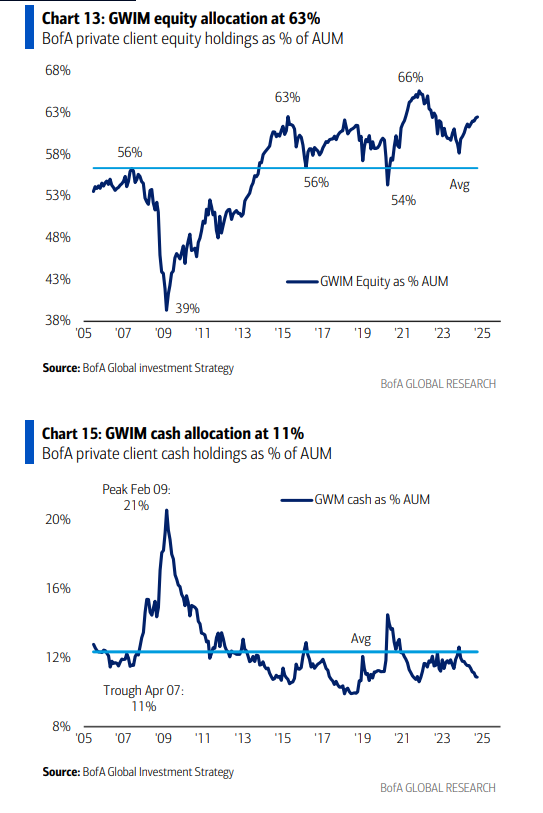

Great feedback from the lynx-eyed and my old friend Rich Bernstein in response to yesterday's "I Call BS on The Cash On The Sidelines Argument":

Dougie - To your point, Merrill data shows their private client accounts are well above average allocation to equities and below average cash allocation.

BY Doug Kass · Oct 8, 2024, 9:15 AM EDT

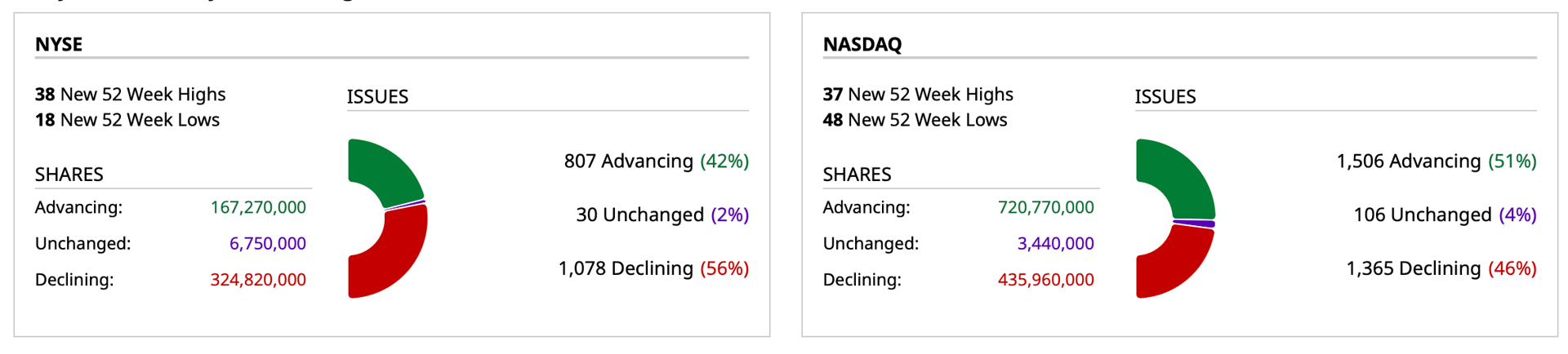

Charts from 8:24 a.m. ET:

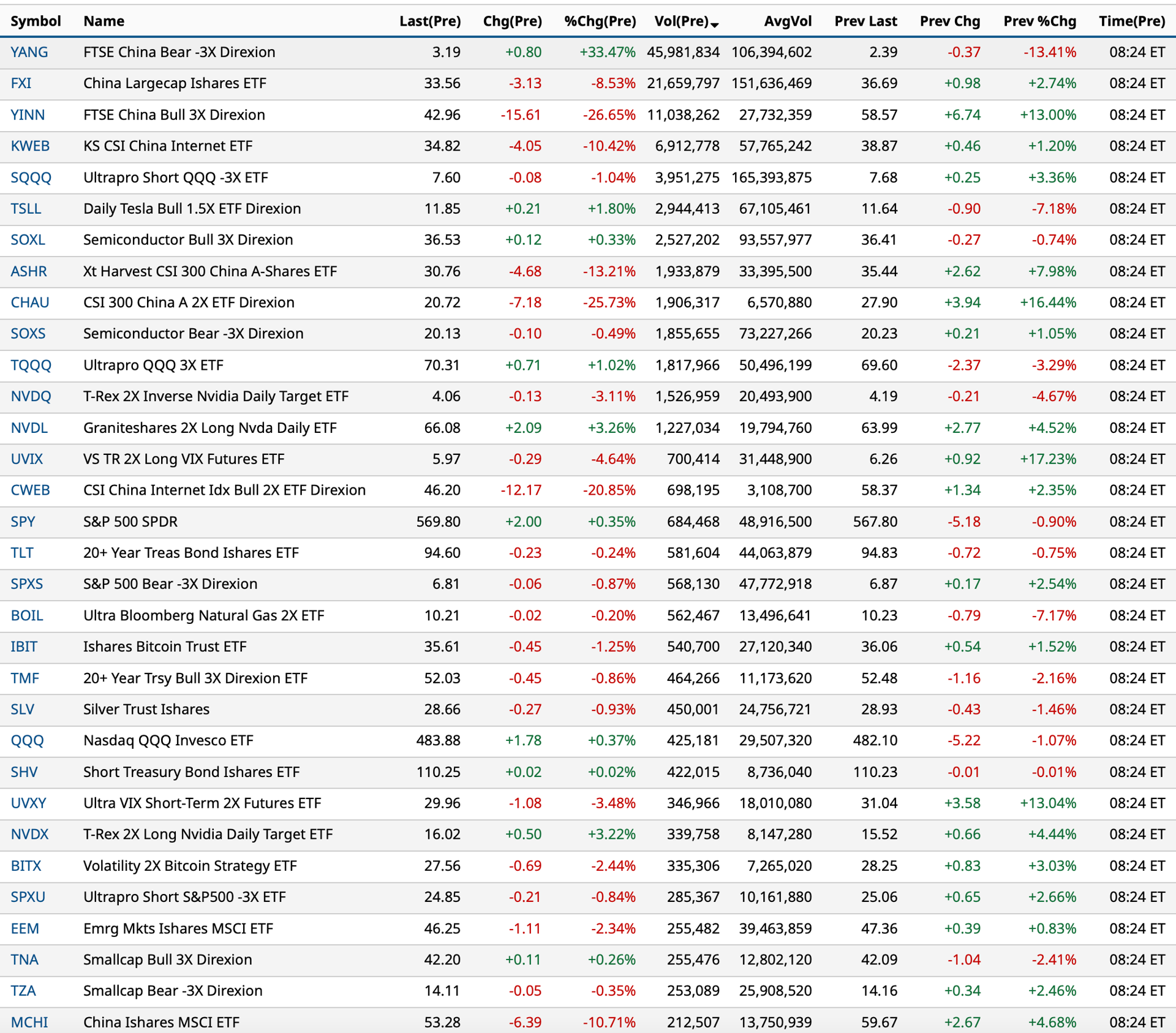

BY Doug Kass · Oct 8, 2024, 9:09 AM EDT

I have been short Roblox RBLX for a while.

This morning, 97 years after the airship accident (!), Hindenburg Research issued a sell/short analysis: "Roblox: Inflated Key Metrics For Wall Street And A Pedophile Hellscape For Kids – Hindenburg Research"

BY Doug Kass · Oct 8, 2024, 9:01 AM EDT

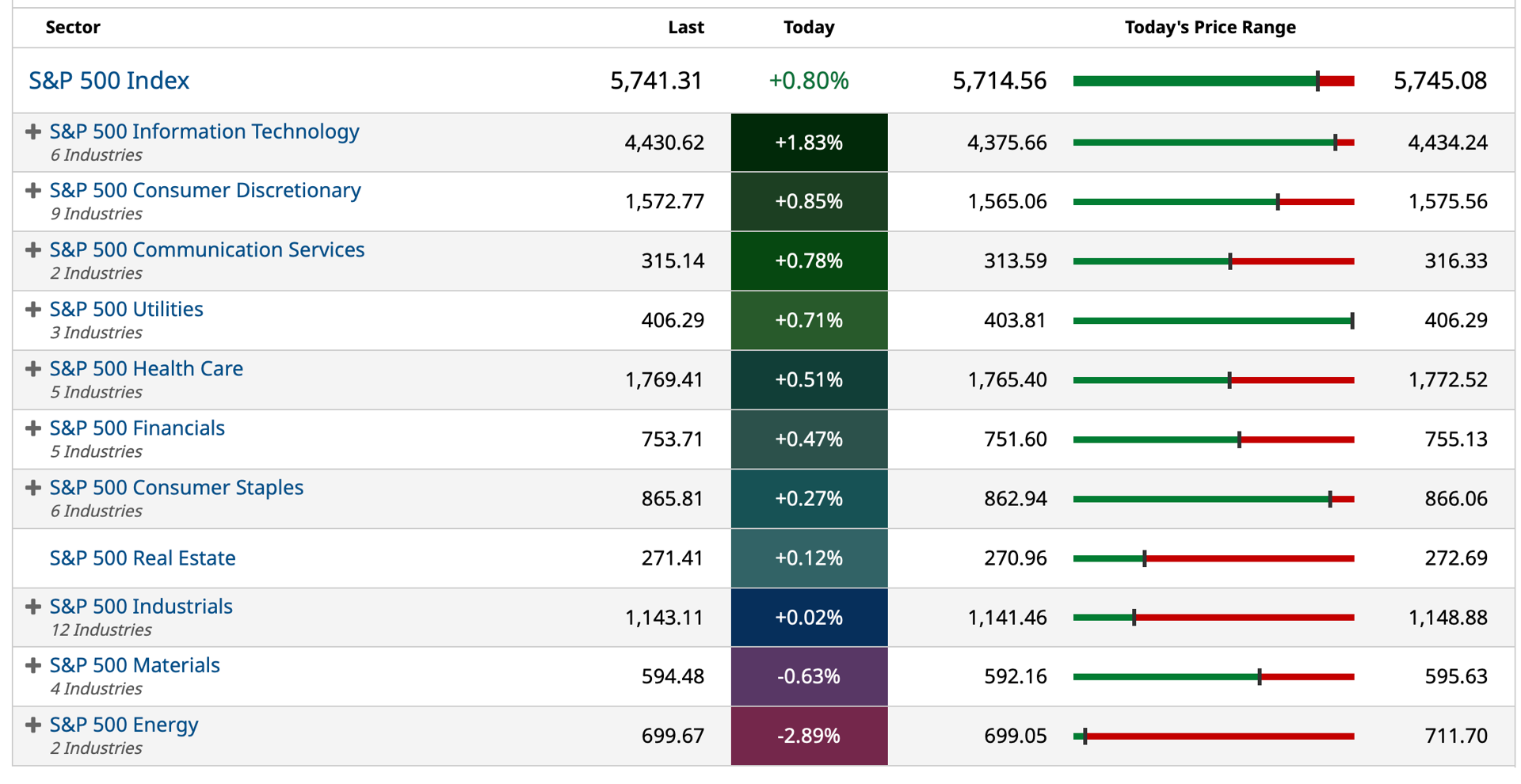

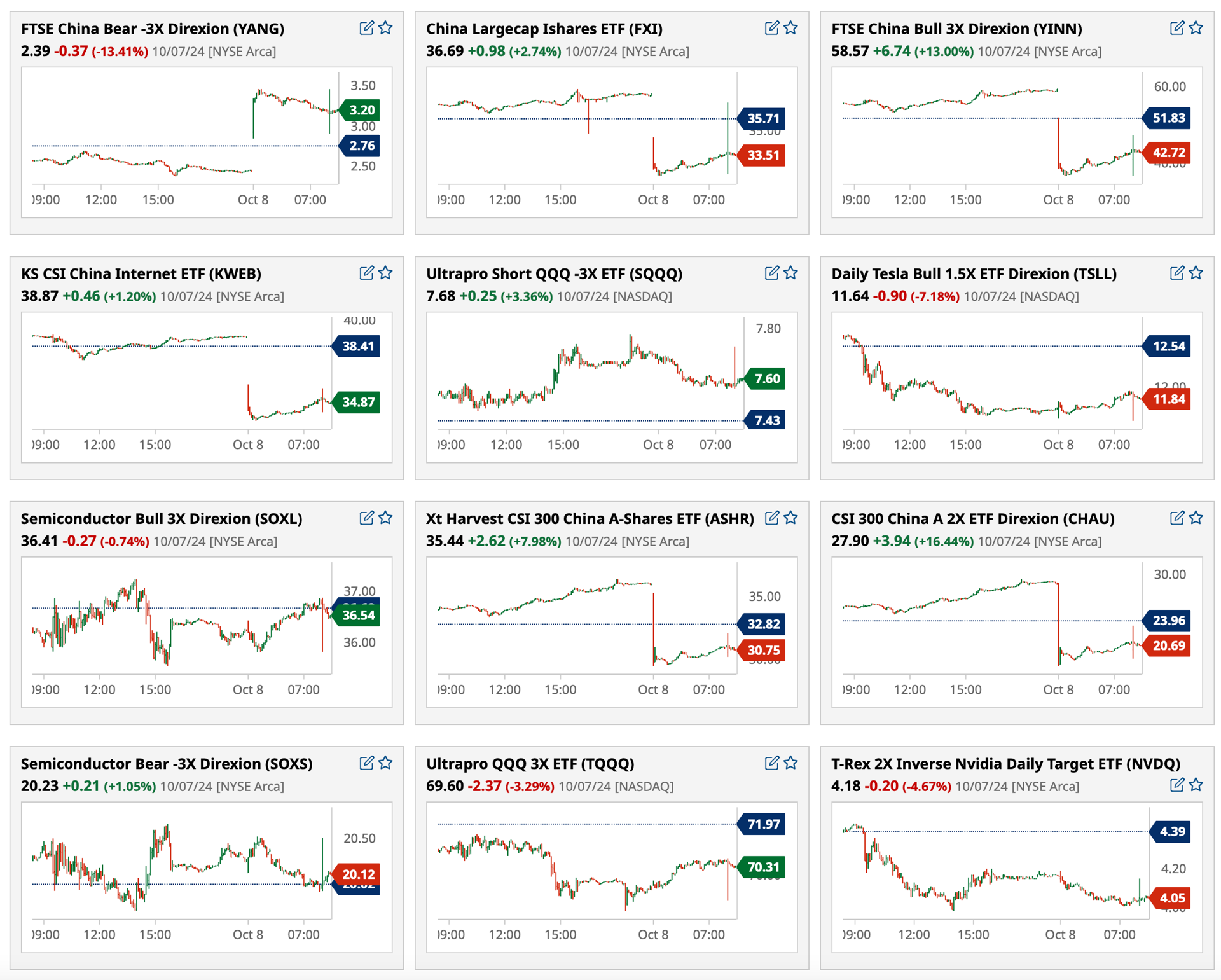

Chart from 8:43 a.m. ET:

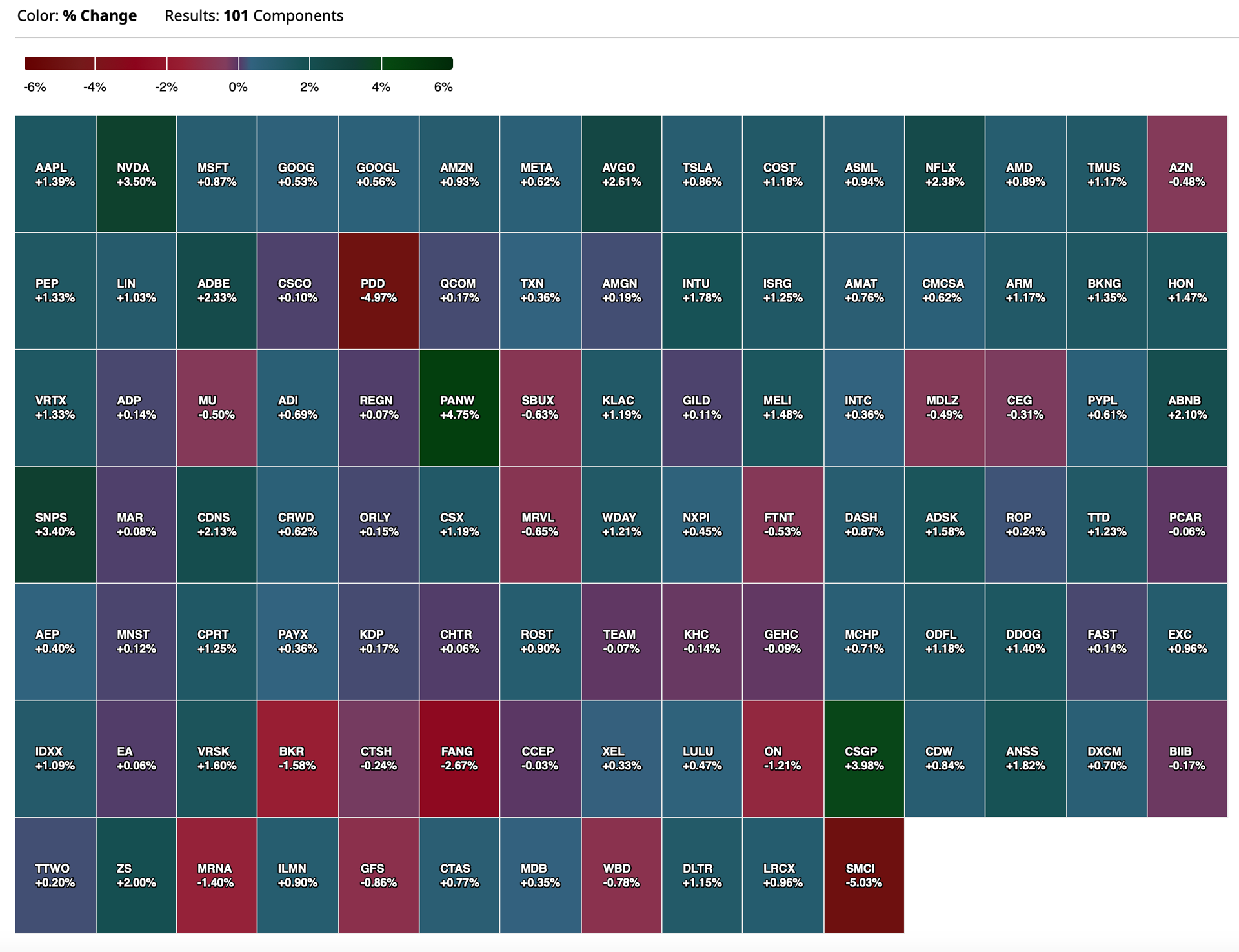

BY Doug Kass · Oct 8, 2024, 8:51 AM EDT

BY Doug Kass · Oct 8, 2024, 7:50 AM EDT

Masterhedge

Dealers are back in negative gamma, implying that higher volatility should be expected. As we noted yesterday, there was a lack of support to the downside, which allowed for a quick shift back to the 5700 strike.

While dealers are broadly short gamma, our GVT index implies only a moderate impact on the equity market at the current level. However, any further weakness should come with a convex response, which makes the 5700 strike a key level to watch this week.

There was some notable activity in the volatility space yesterday, which pushed our Hedging Stress index back above the 80%ile, marking the second-highest level since early 2022.

We find it no coincidence that there was a sharp drop in skew and overall less demand for tail risk after the introduction of daily expirations. However, now that a combination of longer-term risks is building in the market, including both the US elections and the rising geopolitical tensions in the Middle East, we're not surprised to see longer-term options come back into play.

It's also worth highlighting the recent decline in market breadth, as just 48% of SPX stocks are still trending higher than their respective 20-day moving averages, down from over 70% just one week ago.

If we continue to see the broader market decline, then SPX will become even more sensitive to downside moves from the mega caps, as there will be less underlying support from the broader index to balance out the weakness.

Tier 1 Alpha.

BY Doug Kass · Oct 8, 2024, 7:40 AM EDT

BY Doug Kass · Oct 8, 2024, 7:30 AM EDT

* MSOS is my Trade of the Week...

BY Doug Kass · Oct 8, 2024, 7:20 AM EDT

BY Doug Kass · Oct 8, 2024, 7:10 AM EDT

Bonus — Here are some great links:

How to Trade TSLA and AMD Events

BY Doug Kass · Oct 8, 2024, 6:55 AM EDT

Over the last two days (in the business media) the typically "late to the party" group of momentum-based investors (praise by individual, criticize by category) have confidentally gone long energy and China-based equities.

I wish them luck. (I have sold out nearly all of my energy holdings and, like Druck, will not buy China stocks until the country's leadership changes).

I think they will need luck.

I am short very small Chinese stocks but I would seriously discourage anyone in following me as I could be out at any point in time and the stocks are ridiculously volatile!

BY Doug Kass · Oct 8, 2024, 6:45 AM EDT

The S&P Short Range Oscillator stands at neutral now — at -0.08%.

That is down from an overbought 1.46%.

BY Doug Kass · Oct 8, 2024, 6:30 AM EDT

Break in!

PepsiCo PEP lowers guidance (for organic growth). I have shorted (very small).

PEP short joins Coca-Cola KO short.

BY Doug Kass · Oct 8, 2024, 6:20 AM EDT

The decline in used car prices has been as assist with the disinflation of the last six months.

Wolf Street howls that the end of those declines are near.

Combine this with the resumption in the meaningful commodities price increases over the last two months and the heady union wage agreements means the best part of the favorable patter on disinflation is likely behind us.

Watch the 10-year yield. I remain short bonds.

BY Doug Kass · Oct 8, 2024, 6:10 AM EDT

Wolf Street howls about the housing markets.

BY Doug Kass · Oct 8, 2024, 5:58 AM EDT

With S&P futures trading flat to slightly lower last night, I (tactically) purchased Spoos to offset my medium-sized short Index calls — to move into a delta adjusted neutral position in the Indices. (The position has now effectively become a buy/write).

If I hold until November expiration I will be taking in the premium that has expanded with a higher VIX (of nearly 23).

I plan to sell off the long side of the trade on a rally — as I have done repeatedly in the last several weeks.

Trading sardines.

BY Doug Kass · Oct 8, 2024, 5:51 AM EDT