Boockvar on Home Prices, Consumer Confidence and More

From Peter Boockvar:

Home prices, let's draw the trendline/Consumer confidence mixed/Mfr'g recession continues on

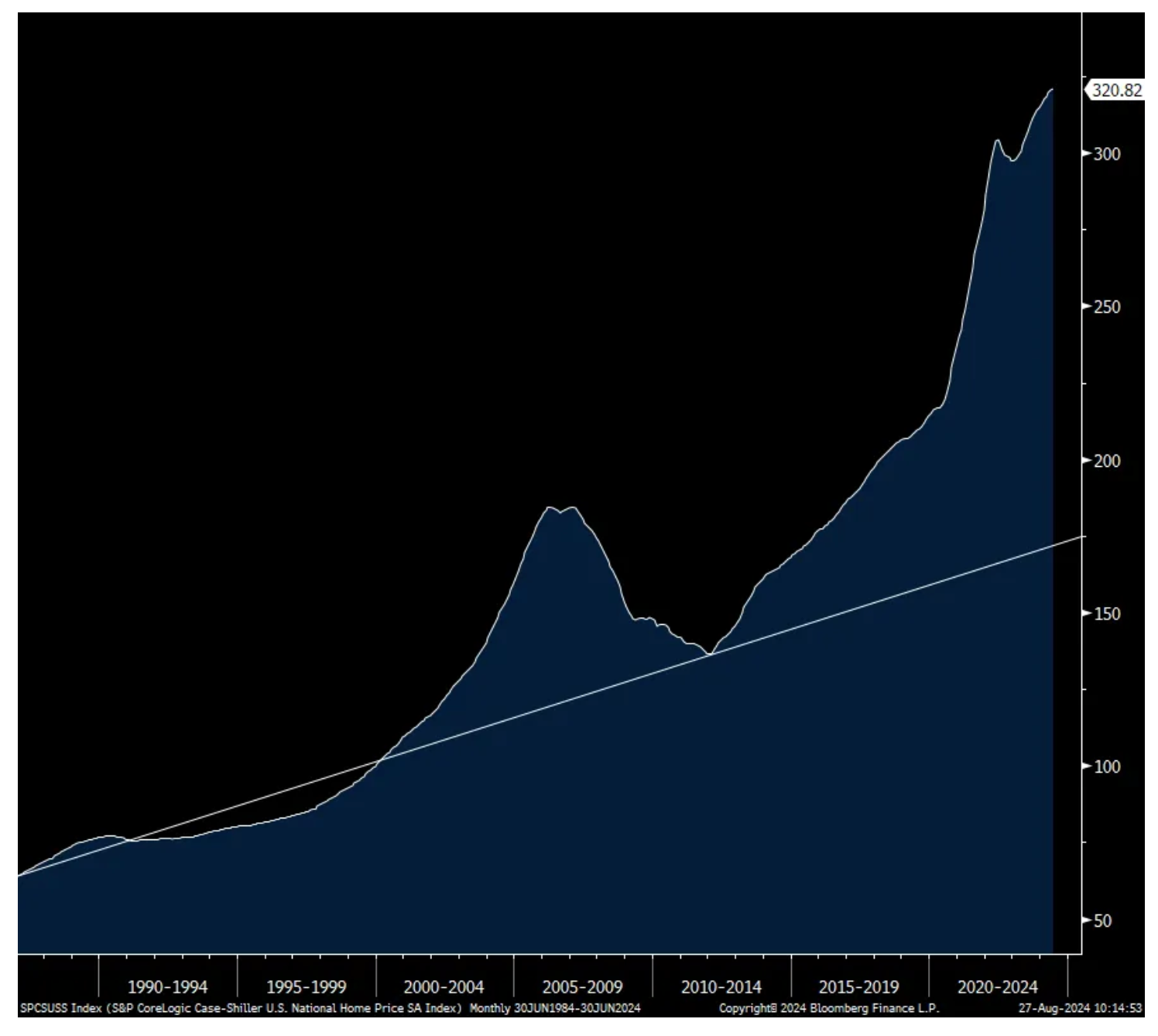

Continuing its march higher, home prices rose again in June, by .2% m/o/m and by 6.5% y/o/y according to S&P CoreLogic. It’s certainly great for existing homeowners but a tough financial situation for those first time buyers and mitigating any relief that lower mortgage rates provide.

Leading the home price gains is where the supply is very constrained, in San Diego, NY, Chicago and LA. Lagging was Portland, Denver, Minneapolis and Dallas.

Here is a chart of this index going back to 1987 that I have data on and I drew a trend line for perspective. While the market currently needs more supply, you can see the extent in which the Fed had peddle to the medal with the demand side, both back in the early 2000’s when Greenspan took the fed funds rate to 1% and via zero rate and QE policy (both Treasury and MBS) that followed in the housing crash aftermath, and then juiced again during Covid.

You want a culprit, with all good intentions, when it comes to the unaffordability of the US housing market, it’s not hard to find.

S&P CoreLogic Home Price Index

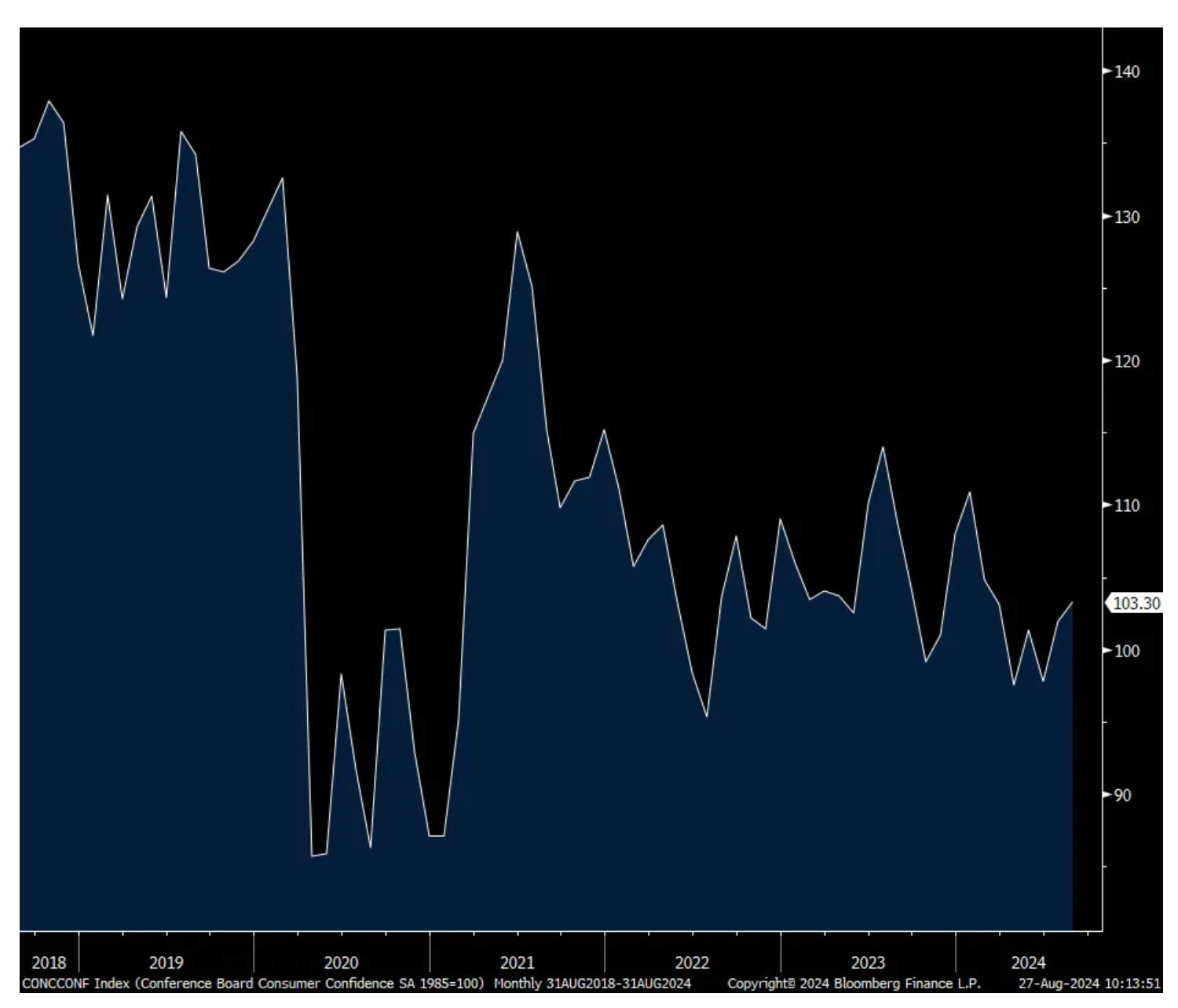

The August Conference Board Consumer Confidence index rose to 103.3 from 101.9 and that was 2.6 pts above the estimate. That’s also the best since February but still well below the February 2020 print of 132.6. The Present Situation was higher by 1.3 pts m/o/m and the Expectations component by a like amount.

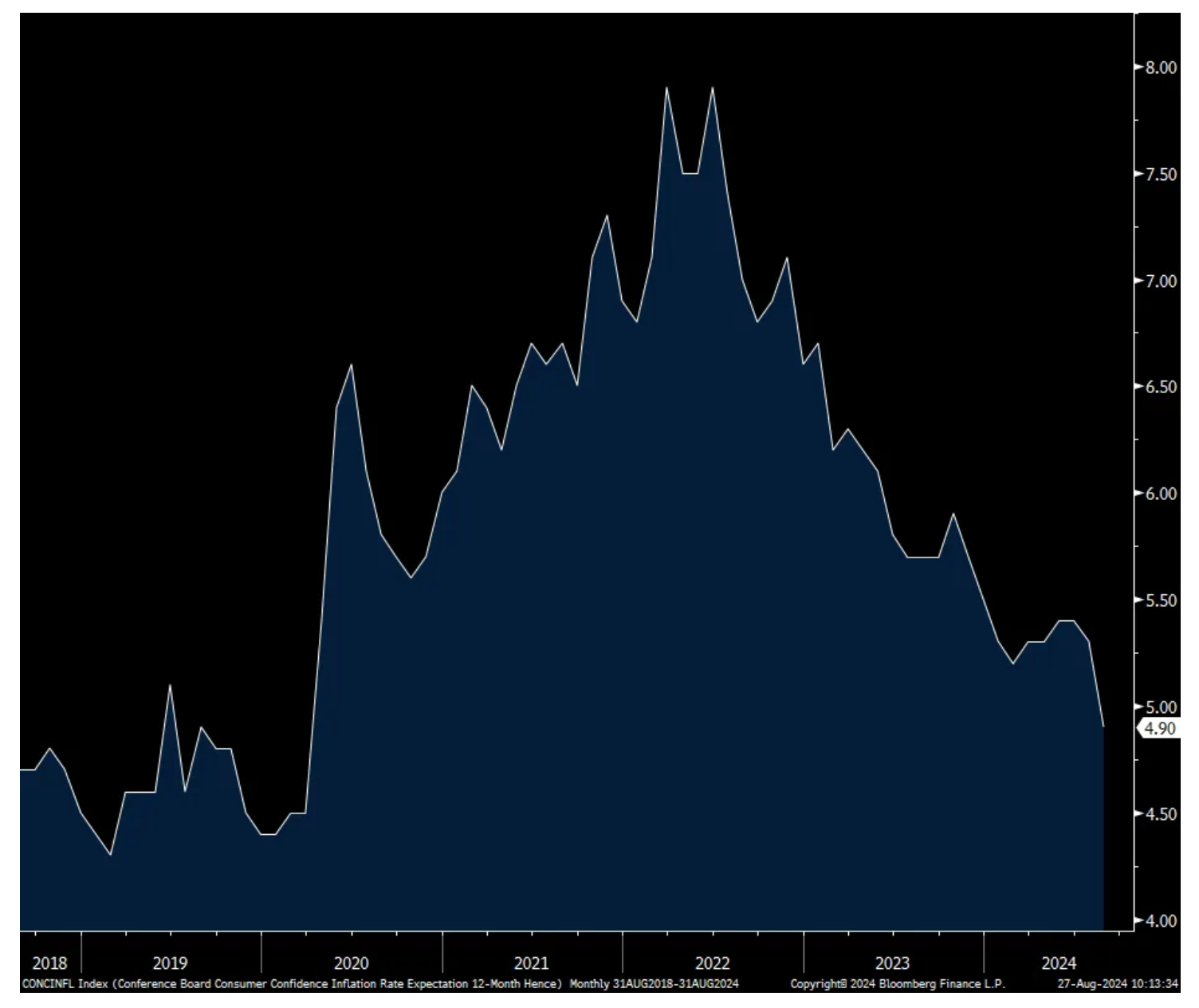

Of note, one yr inflation expectations fell to 4.9% from 5.3% and that is the lowest since March 2020.

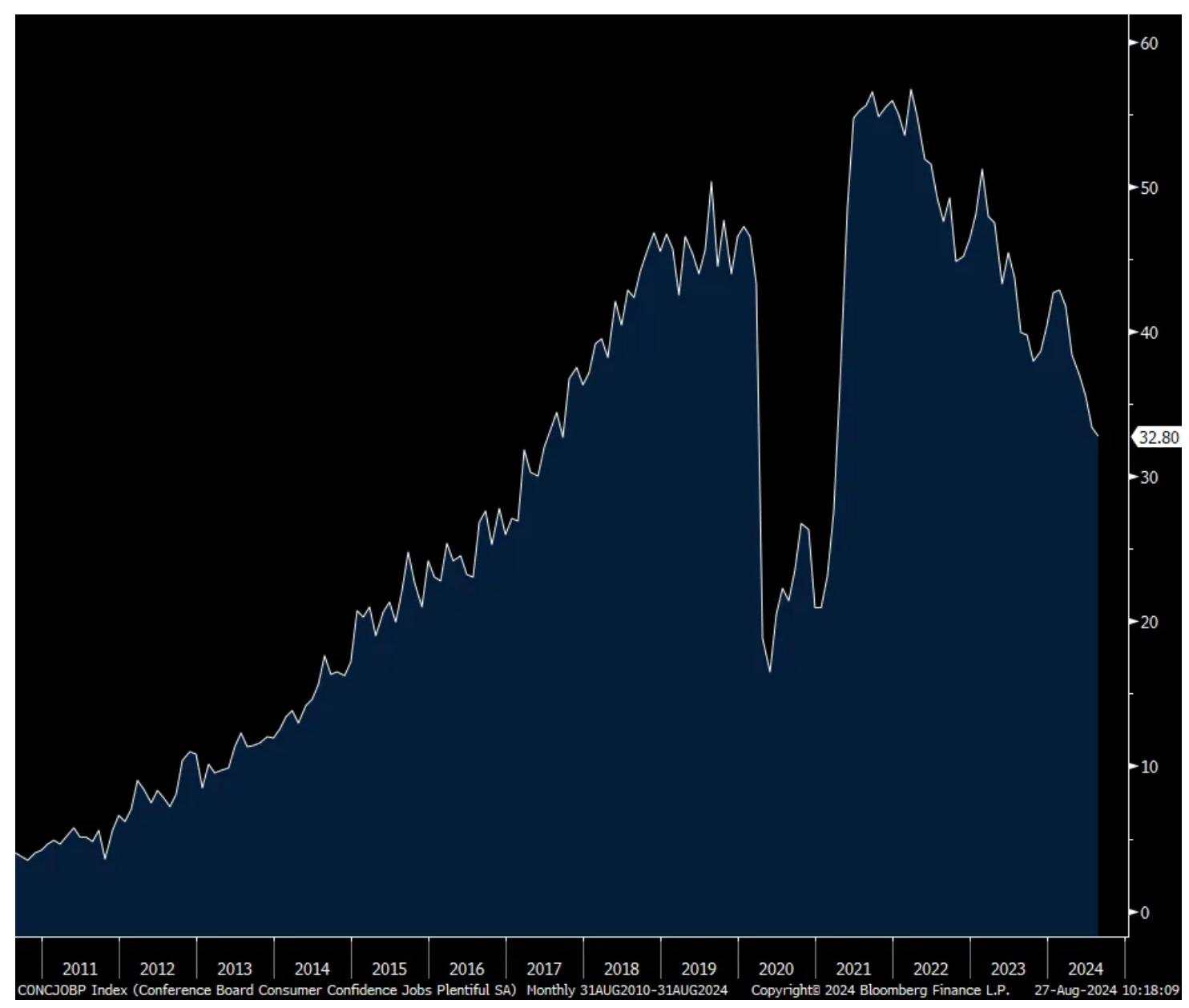

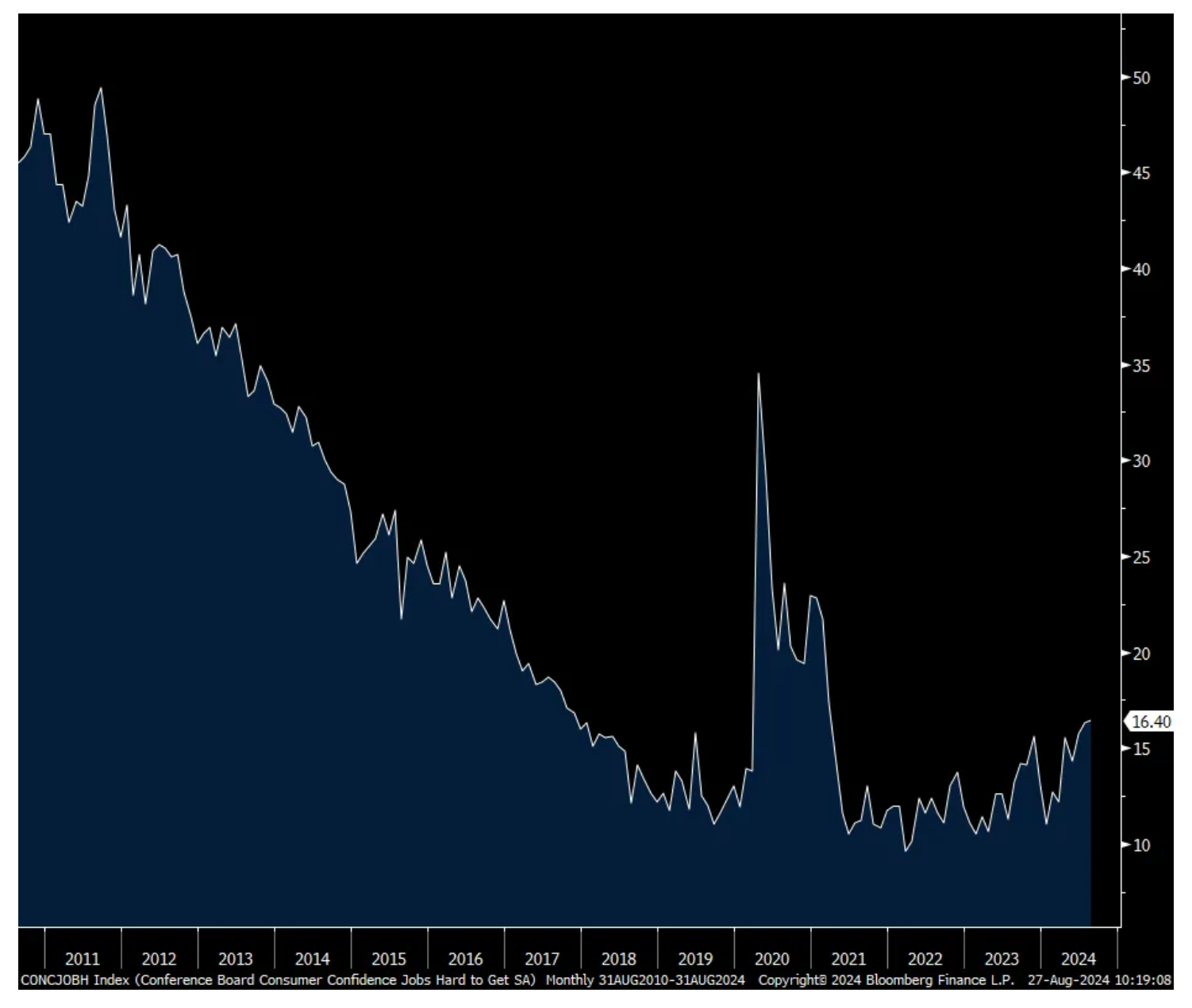

Notwithstanding the lift in headline confidence, it got no help from the current situation with the labor market. Those that said jobs were Plentiful fell to the least since March 2021 and to September 2017 not including Covid. ‘Jobs Hard to Get’ rose just .1 pt but to the most since March 2021 and 2017 previously.

There is optimism though that things get better from here as the 6 month outlook for ‘more jobs’ rose by .9 pts m/o/m to the highest since December 2023. After rising 1 pt in July, those expecting a rise in income fell .3 pts.

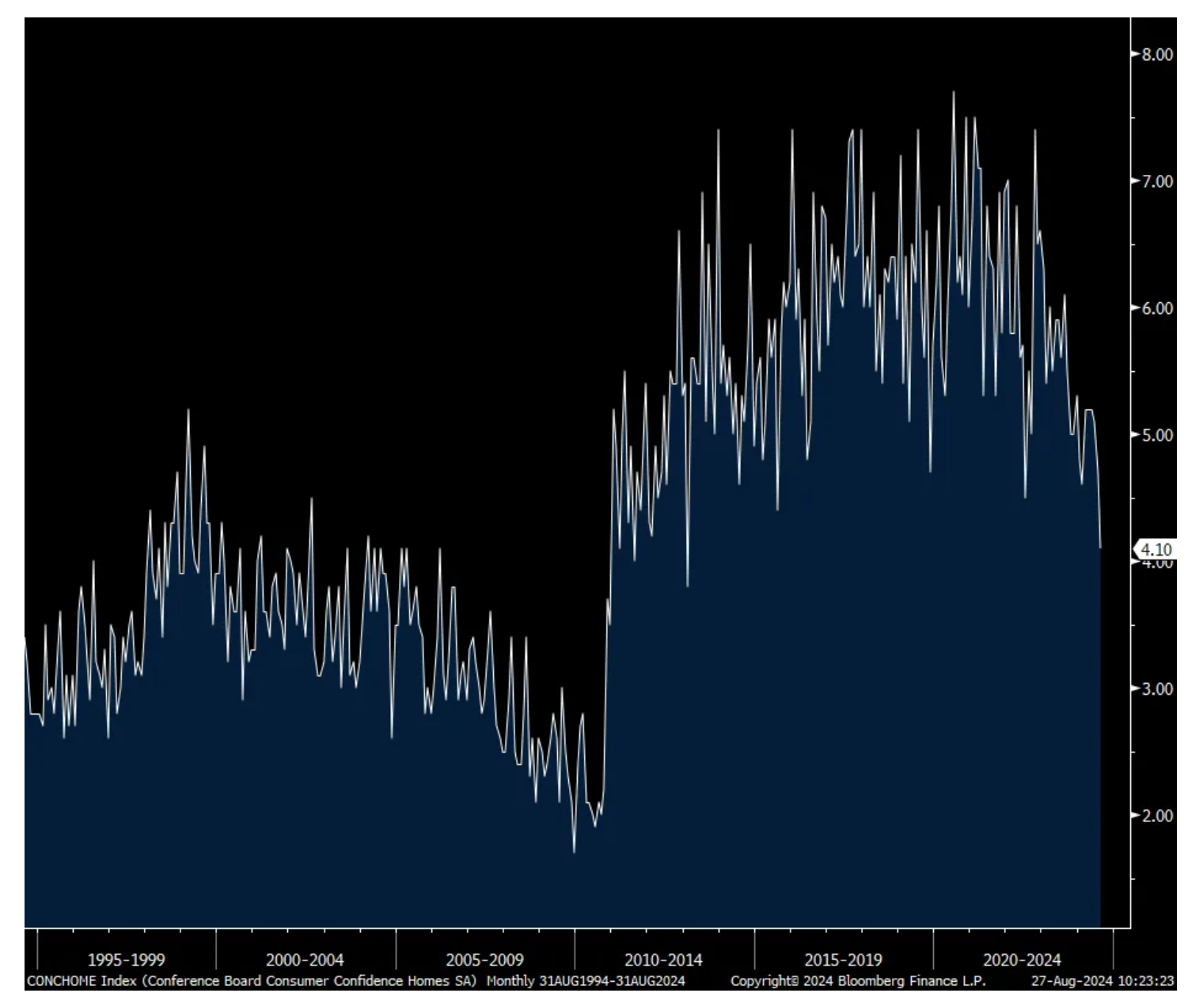

Spending intentions continue to weaken. Plans to buy a vehicle fell to the lowest since February. Plans to buy a home, even with the recent drift lower in mortgage rates, fell to the least since February 2013. For a major appliance, it fell to a 4 month low.

The bottom line from the Conference Board, “Overall consumer confidence rose in August but remained within the narrow range that has prevailed over the past two years. Consumers continued to express mixed feelings in August.” That was clearly seen with the stats above.

Similar to what we heard from the UoM, “Consumers were likely rattled by the financial market turmoil in early August…August’s write-in responses also included more mentions of stock prices and unemployment as affecting consumer’s views of the US economy.”

You want to have a recession/no recession debate, and if the former, to what extent, you must have an opinion, as difficult as it is, on the direction of the S&P 500 from here as the upper income consumer is helping to hold the US economy on its shoulders.

Consumer Confidence

One yr Inflation Expectations

Jobs Plentiful

Jobs Hard to Get

Plans to Buy a Home

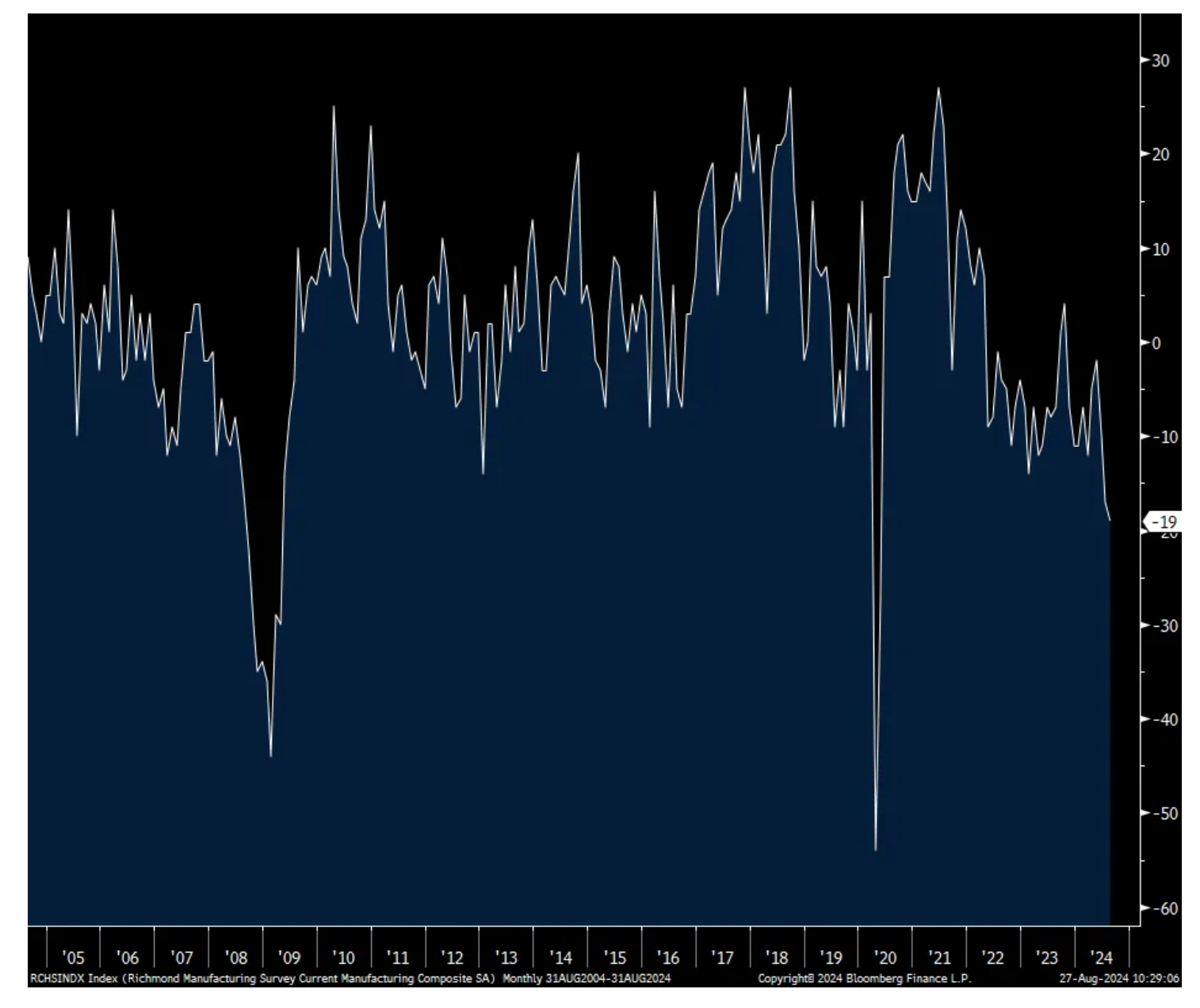

Joining all its regional peers still in contraction, the August manufacturing index from the Richmond area fell to -19 from -17. That’s the worst print since April 2009 not including Covid. The recession here in August continues.

Boockvar Is Watching the Dollar (But Not the One You Think)

From Peter Boockvar:

I'm watching the Singapore dollar, are you?

Whenever the US dollar starts to weaken I always wonder if this is it. 'It' being that ever exploding US debts and deficits actually matter in the eyes of the holders of dollars. Rather that than the dollar, along with all other fiat currencies, just being an interest rate differential play as it was beginning in June 2021 (Jay Powell said he's thinking about trimming QE) through its peak in October 2022 (around the time the Fed finished its last 75 bps rate hike) when it rallied notably. I bring this up because just maybe, and I emphasize 'maybe', it will be the FX market that reflects the ever worsening US government financial situation initially instead of the US Treasury market.

The currency that I'm focused on is the Singapore dollar because US yields remain about 100 bps above those seen in Singapore but the Singapore dollar is at a 10 yr high vs the US dollar. The Singapore budget deficit is less than .5% of GDP which compares to the US at around 6%. Yes, Singapore is a tiny nation state of just 6mm people, the size of a US major city and an amazing city it is, but fiscal responsibility in this case apparently matters for its currency. I've mentioned it a few times over the years but we remain bullish and long some Singapore stocks, and by extension the SGD. The Straits trades cheaply at 11x '24 eps and with a 5.4% dividend yield.

As for the euro/yen heavy DXY, it's at its lowest level since July 2023 where it traded then for a few days below 100. That is the key level as if it breaks there convincingly, go back to April 2022 the last time it did. Outside of gold which is at a record high, in part because of the US dollar weakness, some commodities have recently bounced with the CRB raw industrials index at a 5 week high, but they remain well below their highs. Their performance from here will be key to watch as will import prices with the weaker dollar. We remain bullish and long energy, uranium, copper, precious metals and fertilizer stocks.

Singapore Dollar/US Dollar Cross (lower on the chart equals higher SGD)

As we digest last week's Jackson Hole coffee talk, I heard again Jay Powell defer some blame on believing in transitory by saying inflation was a global thing. And while it was, a lot of it flowed out of the US. My friend Barry Knapp, who runs Ironsides Macro, hit this well in his weekend piece by saying "the seemingly politically motivated characterization of inflation as a global phenomenon, now by Chair Powell, underestimates the role of US consumption in global economic activity. The US runs a massive current account deficit, other major economies run surpluses due to having export dependent economic models. Increased US goods demand following massive fiscal stimulus drove the global supply demand goods imbalance." https://substack.com/@ironsidesmacro

Ahead of the August Richmond manufacturing survey at 10am est, yesterday's Dallas survey was less bad at -9.7 vs -17.5 in July, though still less than zero for a 28th straight month. As the internals are always so volatile each month, I'll just post here some respondent comments.

Chemical Mfr'g:

"Difficulties in ship travel to the Red Sea area have made it difficult to secure ships for bimonthly/quarterly shipments."

"Turbulence in the market, increased global instability and further concerns over US political instability in the current administration have all fueled weakening in the market."

Textile Product Mills:

"Uncertainty is high, and we are very unsure how the next quarter will go."

Paper Mfr'g:

"Things are soft but steady."

Food Mfr'g:

"We are preparing for the recession."

"Suppliers are demanding longer lead times. Some commodity prices have declined, but value-added items (packaging items) are seeing price increases. We'll have an annual wage increase in October in the range of 3 to 8%. Wages for positions requiring physical work are increasing more than desk jobs."

Plastics & Rubber Products Mfr'g:

"Heading into the holiday season with an election in the near future, our customers are beefing up supplies from China for the near term but hitting pause beyond that."

Machinery Mfr'g:

"The slowdown is settling in with business activity at a very low level."

"Things are just plain bad all over. There is no skilled labor available."

"Our business usually has seasonal decreased in the summer months, but the decrease this summer is more significant than usual. We are now not so sure about the future."

Computer & Electronic Product Mfr'g:

"It appears the industry is approaching a cyclical bottom; we see signs of several markets beginning to correct. Regionally, China was strong, U.S. was OK, Europe was weak, and Japan was very weak."

"We are getting more resistance to higher prices from our customers. We are also seeing orders reduced or delayed from a few of the more price-sensitive ones. The biggest uncertainty is about the election; a lot of our customers are taking a "wait and see" approach. All small business owners that I talk to are very concerned about the high-tax, anti-growth and anti-small business policies that [we think] are certain to come from a [Kamala] Harris presidency."

Furniture & Related Product Mfr'g:

"We are experiencing slower pay on accounts receivable. There is a continued shortage of skilled carpenters and saw operators. Project size has increased from general contractors. Inexperienced architects and construction project managers cause significant construction timeline delays."

Overseas, Hong Kong reported better than expected trade data for July.

German consumer confidence softened to -22 from -18.6. The estimate was for a slight improvement to -18.2. "Apparently, the euphoria of German consumers triggered by the European football championship was only a brief flare up and faded after the end of the tournament" said the survey. And, "Slightly rising unemployment figures, an increase in company insolvencies and staff reduction plans at various companies in Germany are causing a number of employees to worry about their jobs."

Notwithstanding no growth in the region's largest economy, the euro is hovering around a one year high against the US dollar. The Eurozone has a trade surplus with the US. Bond yields are up too today as are stocks modestly. The DAX in particular is up 11.4% year to date.

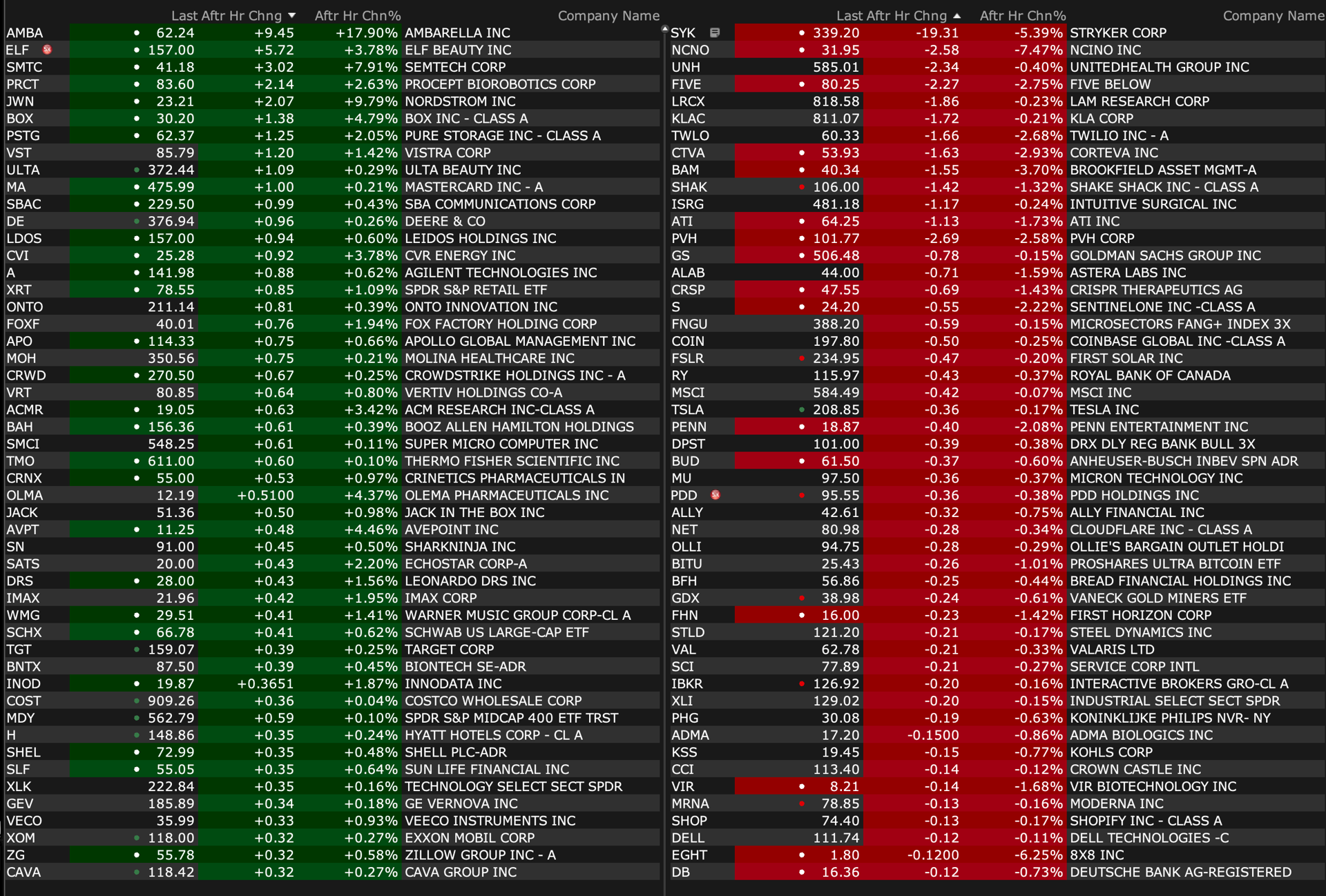

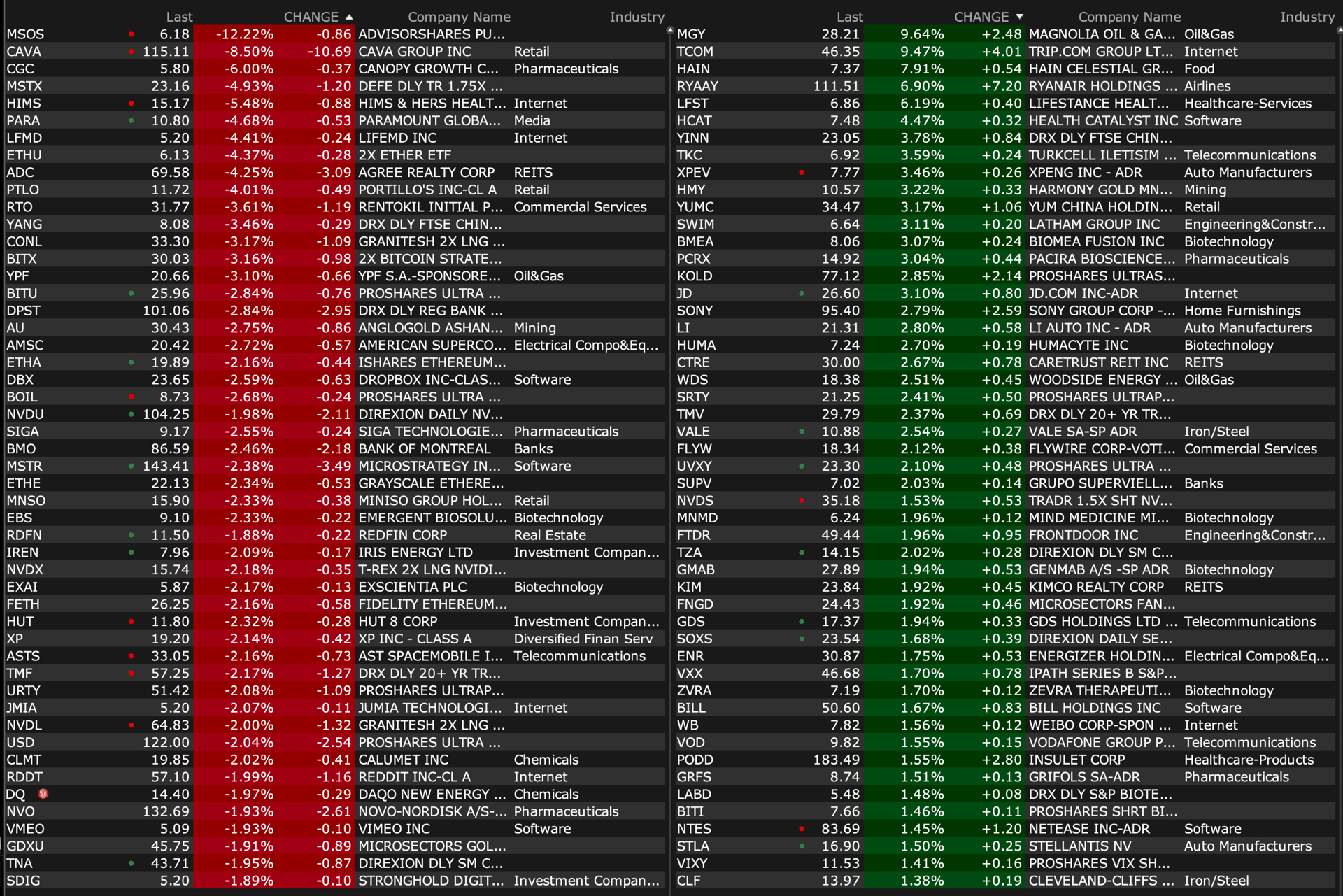

-TRIB +52% (announces increased orders for TrinScreen HIV and raises 2024 sales guidance)

-TUYA +15% (CFO Yao Liu resigns, effective Sept 16th; to be succeeded by Director and Co-Founder Yi Yang)

-TCOM +10% (earnings)

-HAIN +5.4% (earnings, guidance)

-JD +3.6% (announces new $5.0B share buyback)

-VALE +3.2% (Gustavo Pimenta reportedly to be the next CEO)

-CNTA +2.6% (announces Late-Breaking Poster Presentation of Non-Human Primate Data for ORX142, a Novel Orexin Receptor 2 (OX2R) Agonist, at the 27th Congress of the European Sleep Research Society)

-CLF +2.5% (Seaport Global Securities Raised CLF to Buy from Neutral, price target: $16.50)

-ENR +2.1% (Truist Raised ENR to Buy from Hold, price target: $40 from $30)

Downside:

-AAMC -45% (announces intention to voluntarily delist and deregister its common stock, effective Sept 6th)

-CSCI -44% (hormone deficiency drug fails to meet main goal in late-stage study)

-AMWD -13% (earnings, guidance)

-CAVA -9.0% (insiders file to potentially sell shares)

-CTRN -8.1% (earnings, guidance)

-GOTU -7.1% (earnings, guidance)

-SCSC -6.0% (earnings, guidance)

-CTRN -5.3% (earnings, guidance)

-HIMS -4.8% (weakness following LLY discount Zepbound single-dose vial announcement)

-PARA -4.7% (confirmed that it has been informed by Edgar Bronfman, Jr. that the acquisition proposal from his consortium of investors has been withdrawn)

-PRTG -4.2% (earnings)

-BMO -2.5% (earnings)

-MSTR -2.5% (BTC weakness)

-HSY -1.8% (CitiGroup Cuts HSY to Sell from Neutral, price target: $182 from $195)

Whether a groundbreaking or grand opening, the ceremonial ribbon cutting ceremony symbolizes a new beginning. The ritual originated in London at an ancient service to open the Cloth Fair at Bartholomew the Great. Beginning in 1133, the Lord Mayor of London opened the fair by cutting a piece of cloth. Ribbon-cutting is also based in romance; it’s a traditional rite of wedding celebrations across Europe. In Italy, the bride’s father, or the bride herself, cuts a ribbon that’s placed over the door of the family home, symbolizing the departure from her family of birth and newfound freedom in that of her betrothed. In France, brides cut ribbons while being escorted to the church by their grooms, embodying their commitment to overcoming obstacles hand-in-hand. The U.S. rituals recognized today began in the late 1800s. The first documented cutting opened a Louisiana railroad line. Since then, the ceremonies have become ubiquitous fixtures at everything from charitable ventures to hospital groundbreakings, all of which feature those iconic giant scissors.

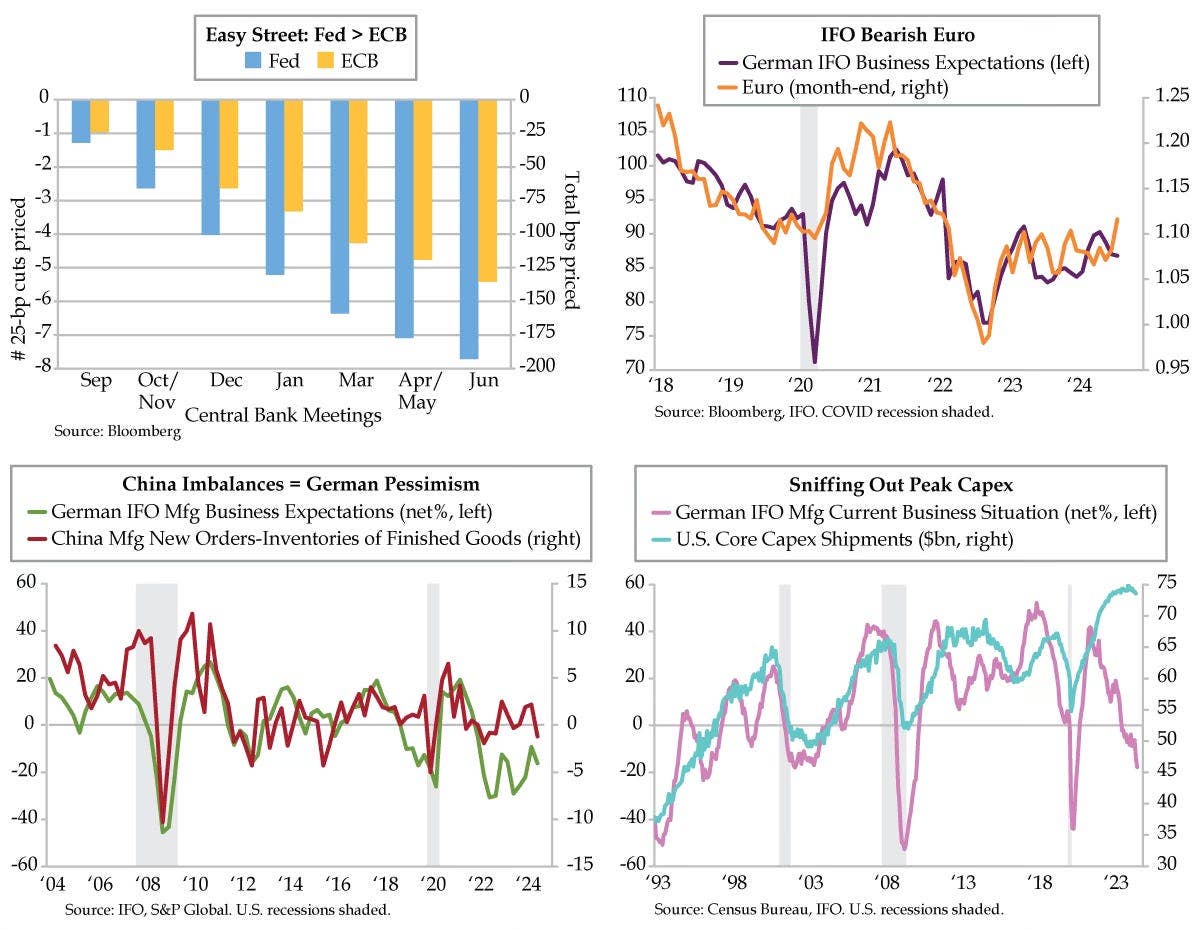

Scissors are not the tool of choice for central bankers’ rate-cutting exercises. Like local officials and business owners, however, microphones are similarly summoned. In the age of transparency and telegraphy, monetary policy communications have become the accepted means to anchor market expectations. As we’ve been informed by Federal Reserve Chair Jerome Powell, the September 18th rate cut has been guided by the convergence of high inflation and low unemployment.

Focusing solely on the labor side, the 0.7 percentage point year-over-year (YoY) gain in the U.S. unemployment rate saw this latter side of the Fed’s mandate move up faster than policymakers’ forecast by mid-year. To wit, the current 4.3% level stands nine-tenths above the April 2023 3.4% cycle low. Unlike the Fed, the European Central Bank (ECB) is not beholden to a dual price/labor mandate. And yet, the ECB began its rate-cutting cycle months ahead of the Fed, despite the Euro Area unemployment rate through June being unchanged YoY at 6.5%, just off its April and May 2024 cycle low of 6.4%. Call it rigidity – the factor that differentiates the Euro Area vis-à-vis its U.S. counterpart, in which labor markets are more dynamic, a polite way to say it’s easier to fire workers.

Given the differences in the unemployment trends, it follows that the Fed should have more rate cuts priced than the ECB. Through the end of 2024, futures markets call for four cuts totaling 100 basis points (bps) in the U.S., slightly higher than the two and three reductions totaling 50-75 bps in the Euro Area. By the middle of next year, the Fed and ECB are expected to have cut by nearly 200 bps and 125 bps, respectively (blue and yellow bars). Dollar bears have jumped on this differential, catalyzing a crowded momentum trade that’s yet to find a bottom for the greenback. While the euro has benefitted, there are signs that the long euro camp should start to depopulate.

The key litmus test month in and month out to set risk appetite is Germany’s IFO business survey. Investors breathed a sigh of relief Monday with news that the August IFO Expectations of 86.8 whisked past the consensus expectation of 85.8. That said, the six-month low mark (purple line) is still running counter to the euro’s path (orange line), suggesting the U.S. side of the exchange rate (read: Fed expectations) should outweigh the Euro Area side regarding short-run influences.

The most cyclical aspects of the IFO survey provided the most color. The commentary distinguished the factory sector from services, trade and construction (bolding ours): “In manufacturing, the index fell considerably. Companies were significantly less satisfied with the current business situation. Expectations fell to the lowest level since February. Companies once again reported declining order backlogs. The situation for investment goods manufacturers, in particular, is difficult.”

Persistent weakness in order backlogs flags an acceleration in Germany’s layoff cycle. Little wonder, forward-looking unemployment expectations rose to 10-month high in the Euro Area, half the 20-month high in Germany. Calling out investment goods manufacturers nods to the capex cycle, which trends with labor over time and echoes deterioration in the U.S. industrial heartland as seen in the Chicago and Kansas City Fed Districts. Much further east, Germany’s export exposure to China also factors in. Thus far this quarter, IFO Manufacturing Business Expectations have backslid from -17.8 in August from July’s -14.5 July. The quarter-to-date average of -16.2 begins a triple dip (green line). No coincidence, China moved to excess supply conditions at the start of the quarter as its July manufacturing New Orders-Finished Goods inventories spread fell to -1.2, a two-year low.

As for the here and now, Germany’s current Manufacturing Business Conditions slumped to -17.7 in August, the pandemic aside, a level last recorded in the Great Recession (lilac line). The -11.4-point plunge from June to August was one of the largest two-month drops on record and scaled to a -1.6 z-score. Evisceration in German current factory conditions has historically closely tracked the U.S. core capex cycle. Ergo, it was no surprise that yesterday’s Nondefense Capital Goods Ex-Aircraft Shipments missed expectations in July and were revised down in June, further solidifying January as the cycle peak (aqua line). Further capex downgrades pose a clear risk that inevitably takes down other geographies in a domino effect. The whiplash rally in the greenback is the last thing fast money traders would see coming.

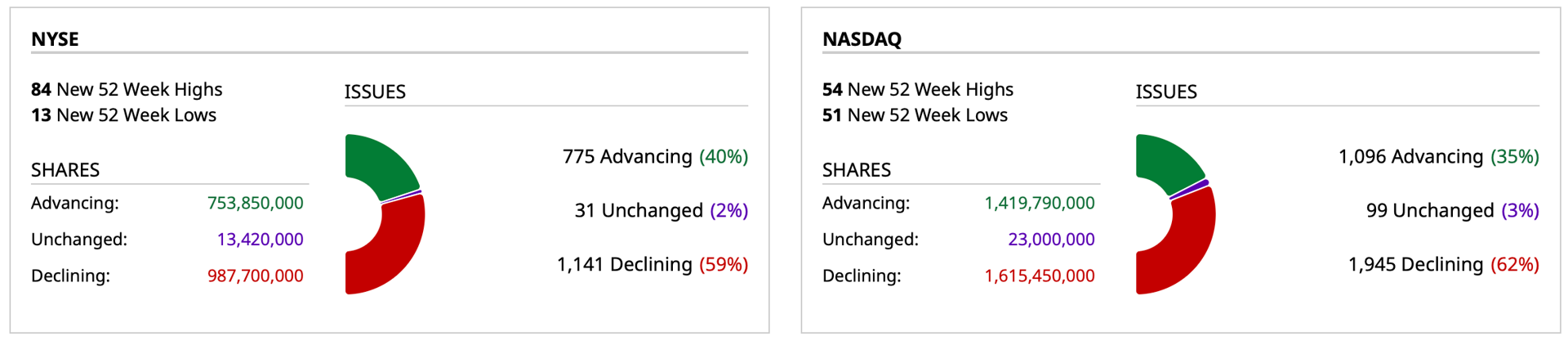

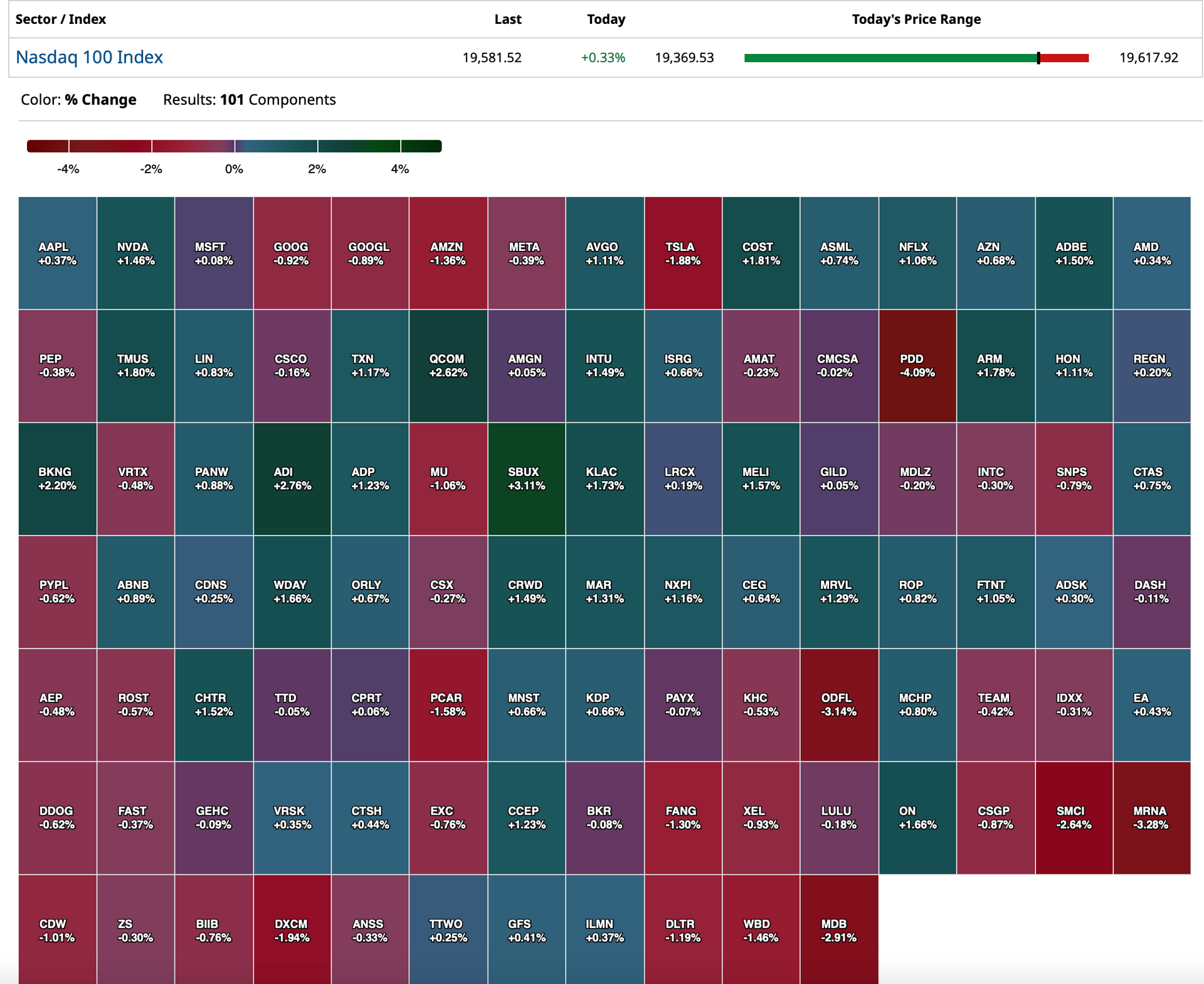

US: Futs are higher with Tech leading with NVDA/TSLA moving higher after lagging Mag7 yesterday. Mag7 and Semis are higher pre-mkt with bond yields higher amid a steeper curve. USD is weaker and cmdtys are lower ex-base metals and natgas. Today’s macro data focus is on Consumer Confidence, Housing Price updates, and regional activity indicators. There is a 2Y bond auction.

and...

EQUITY AND MACRO NARRATIVE: The follow-through from Jackson Hole dissipated as Tech came for sale, dragged by Semis, as investors square positioning into NVDA’s earnings on Wednesday. From a macro perspective, there was a rebound in Durable Goods and oil prices were bid up as Libyan supply comes offline. Keep an eye on Fedspeak, which can be impactful in driving the bond market when there is policy uncertainty, as there is now, as well as bond auctions this week. Ultimately, it is a quiet week with no catalysts capable of changing the market narrative ahead of NVDA earnings, so today and tomorrow may be quiet. That said, a detailed of review of positioning may be useful as investors square up into NVDA and the holiday weekend.