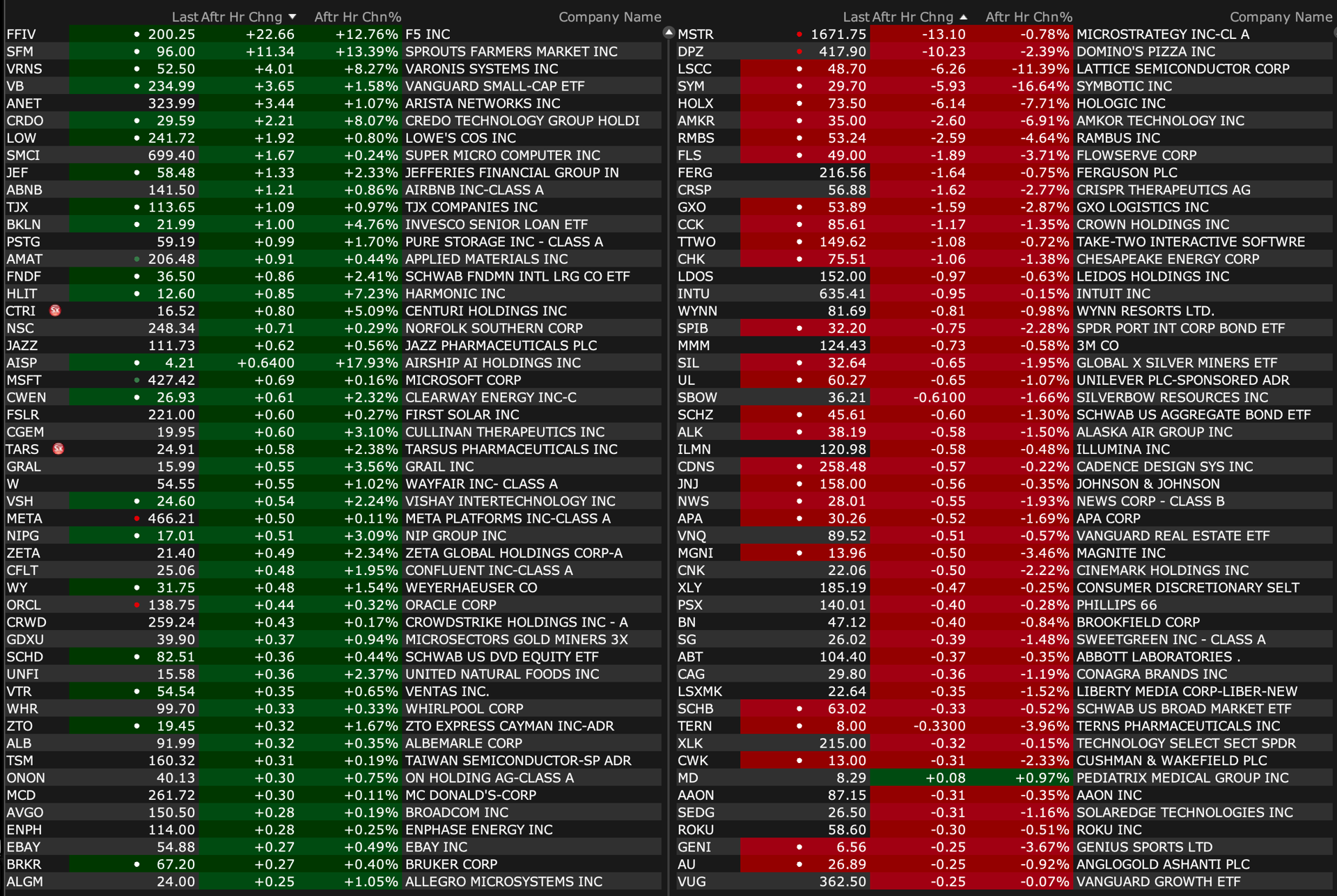

Stocks Moving in After-Hours Trading

BY Doug Kass · Jul 29, 2024, 5:00 PM EDT

BY Doug Kass · Jul 29, 2024, 5:00 PM EDT

Thanks for reading my Diary today.

Enjoy the evening.

Back to bed.

Be well.

BY Doug Kass · Jul 29, 2024, 4:45 PM EDT

Once again:

BY Doug Kass · Jul 29, 2024, 4:27 PM EDT

Because the AI works so well.

And this guy is on the sell-side, which means if the car ran five people over and then crashed into a train, he would probably say it was working great:

Robotaxi jolt: Tesla autonomous driving test goes poorly for Truist Securities | Seeking Alpha

And per my point about sell-siders and running people over and crashing into trains being good things, there is this today. Party on:

Tesla Stock Roars Back As Some Analysts Buy Into Full Self-Driving Hype

BY Doug Kass · Jul 29, 2024, 3:45 PM EDT

Crude is (again) lower on the day — with a drop of -$1.33/barrel.

I have no investments in energy — an area that the "value crowd" admires.

And, though OXY has entered my buy zone (under $60), I am holding off for now given the growing evidence of a domestic economic slowdown.

BY Doug Kass · Jul 29, 2024, 3:18 PM EDT

BY Doug Kass · Jul 29, 2024, 2:55 PM EDT

The vicious rotation continues with small-cap, financials and energy in the crapper.

The moves are unpredictable — just look at the premarket strength in IWM (+1%) and compare to current price (-1.5%).

BY Doug Kass · Jul 29, 2024, 2:39 PM EDT

"There is a plane waiting for us to take us to Miami in an hour.

Don't make a big thing about it.

I know it was you Fredo...

- The Godfather I know it was you Fredo - YouTube

I knew it was pneumonia — you broke my heart!.

Getting my sea legs back.

BY Doug Kass · Jul 29, 2024, 2:11 PM EDT

I am going back to my doctor now.

I should be back by noon.

BY Doug Kass · Jul 29, 2024, 11:40 AM EDT

Banks, private equity and homebuilders are deeply overbought now.

Trade/invest accordingly.

BY Doug Kass · Jul 29, 2024, 11:28 AM EDT

GLASF, my latest cannabis buy... is getting jiggy today.

BY Doug Kass · Jul 29, 2024, 11:08 AM EDT

From Peter Boockvar:

'I want the best of both worlds and honey, I know what it's worth'

Having seen Sammy Hagar & Co in concert Saturday night playing a bunch of Van Halen songs (Loverboy opened up and I'm staying long Live Nation stock with the crowd 17,000 strong), the markets are certainly hoping that the Federal Reserve this week and through the rest of the year delivers the Best of Both Worlds. That being rate cuts along with the paradise of further inflation moderation and a stabilized economy around the current 2% growth level. So easy, right? With expectations already priced in for further cuts in 2025, what would upset that paradise would be if the economy slows further coincident with a continued rise in the unemployment rate as rate cuts may not be enough to stave that off. That's when bad news is bad news for stock and credit markets.

"I want the best of both worlds and honey, I know what it's worth. If we could have the best of both worlds we'd have heaven right here on earth."

"You don't have to die and go to heaven or hang around to be born again. Just tune in to what this place has got to offer 'cause' we may never be here again."

In case you missed these comments from the UoM in Friday's Succinct Summation, they highlight the importance of the stock market to consumer confidence for the part of the population that owns stocks. "The fact that sentiment has moved little over the past three months obscures substantial variation in attitudes across the population...Not surprisingly, consumers with large holdings (of stocks) tend to exhibit higher levels of sentiment than those with smaller (or no) holdings, due in part to the financial security and purchasing power afforded by more wealth," said UoM. I'll add, this interrelationship, this wealth effect, can be the dividing line between economic expansion and contraction as the higher income consumer is holding the US economy on its shoulders right now, along with all that government spending, though the multiplier effect on that government largess is usually less than zero.

We've seen the spike in container shipping rates and the flow thru to air cargo rates continues according to World ACD. They said Friday, "Air cargo spot rates from Asia Pacific continue to soar, despite a drop in demand from China to the USA in the last two full weeks, according to the latest weekly figures and analysis from WorldACD Market Data."

"Average global air cargo rates rose by a further 2% in the 3rd full week of July to US$2.56 a kilo, thanks to increases from Asia Pacific and Middle East & South Asia origins...That average worldwide of $2.56 a kilo is +14% above the equivalent week last year and remains significantly higher than the equivalent period prior to Covid (+47% compared to July 2019)."

Compared to last year, the Asia Pacific to US route is up 67% even though tonnage is down and I'll say again that I have with container prices, someone will have to eat this, either the consumer or profit margins. https://www.worldacd.com/trend-reports/weekly/worldacd-weekly-air-cargo-trends-week-29/

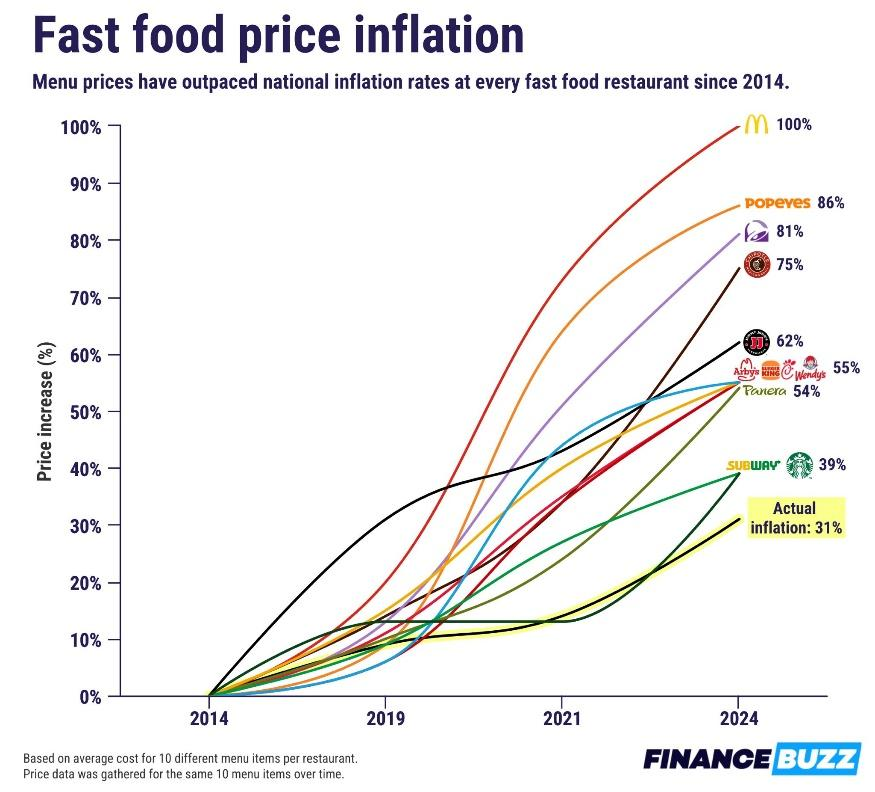

From McDonald's who missed top and bottom line estimates and comp estimates:

From their press released, in the US: "Comparable sales results were driven by negative comparable guest counts, partly offset by average check growth due to strategic menu price increases. Successful restaurant level execution and continued digital and delivery growth positively contributed to results."

Outside of the US, "Segment performance was impacted by negative comparable sales across a number of markets, driven by France...The continued impact of the war in the Middle East and negative comparable sales in China more than offset positive comparable sales in Latin America and Japan."

From MMM Friday, whose stock spiked on improved execution as organic sales grew 1.2% or 2.4% "excluding geographic prioritization and product portfolio initiatives":

"These results reflect the trends that we have previously discussed, including strong growth in electronics, mixed industrial end markets and continued softness in consumer retail discretionary spending."

Specifically with electronics, "we continued to gain spec in wins on consumer electronic devices and in semiconductor manufacturing."

On the consumer side, "We continue to expect that consumer retail discretionary spending on hardline goods to remain muted in the balance of the year."

From Colgate-Palmolive, the maker of toothpaste, toothbrushes, soap, deodorants, pet food, etc...:

To a question about the state of the global consumer, "I think overall, quite constructive around the world, and that's obviously reflected in the strong volume growth, and likewise, the penetration and market share growth." That said, "We've seen a little bit more price-value shopping in North America, but nothing too unusual right now. But we'll have to watch that carefully as we move through the back half of the year."

Also, "we've seen a little bit more volume on deal coming through in North America, but nothing that's not in line with historical numbers, quite frankly. So overall, U.S. watchful, Europe seems to be okay. Latin America, you've seen a really strong volume growth over the last 3 or 4 quarters, despite significant pricing, and so, we're seeing a good consumer environment there. Africa, Asia, Eurasia, strong, again, good volume growth. And pleasingly starting to see some good volume growth coming back out of Asia and India specifically, which is encouraging."

From Eastman Chemical:

"The issue we face that I think everyone in the industry faces right now is that it's a really tough economic environment. We have some version of stagflation, right? You have inflation still impacting consumers and demand being quite weak in many sort of discretionary markets...And it's duration, it's not just demand is weak, it's been weak for over two years now. And so, that weighs on companies and their economics...They're all so focused on managing their cost structure like everyone is right now. And so, the rate at which they're ramping up volume on some of the programs that we've won with these customers is going a bit slower than we thought."

Overseas, Vietnam, the growing manufacturing plant destination, saw its exports in July rise 19.1% y/o/y which was much better than the estimate of up 13.5%. Helping is Samsung in particular which makes up alone about 30% of Vietnam's exports with 4 factories and about 200,000 employees.

BY Doug Kass · Jul 29, 2024, 10:49 AM EDT

"It is clear that our value leadership gap has shrunk recently..."

- McDonald's MCD CEO (Post EPS comments)

* QSR sector meaningfully slowed in majority of markets, industry traffic declined in US, Australia, Canada, Germany

* Remain on track to have 'Best Burger' deployed in nearly all markets by end of 2026

* Seeing falling demand among low income diners

* Seeing falling demand for families in Europe

* CONSUMER SENTIMENT IN CHINA IS WEAK

BY Doug Kass · Jul 29, 2024, 10:00 AM EDT

I have no Index positions on currently.

BY Doug Kass · Jul 29, 2024, 9:35 AM EDT

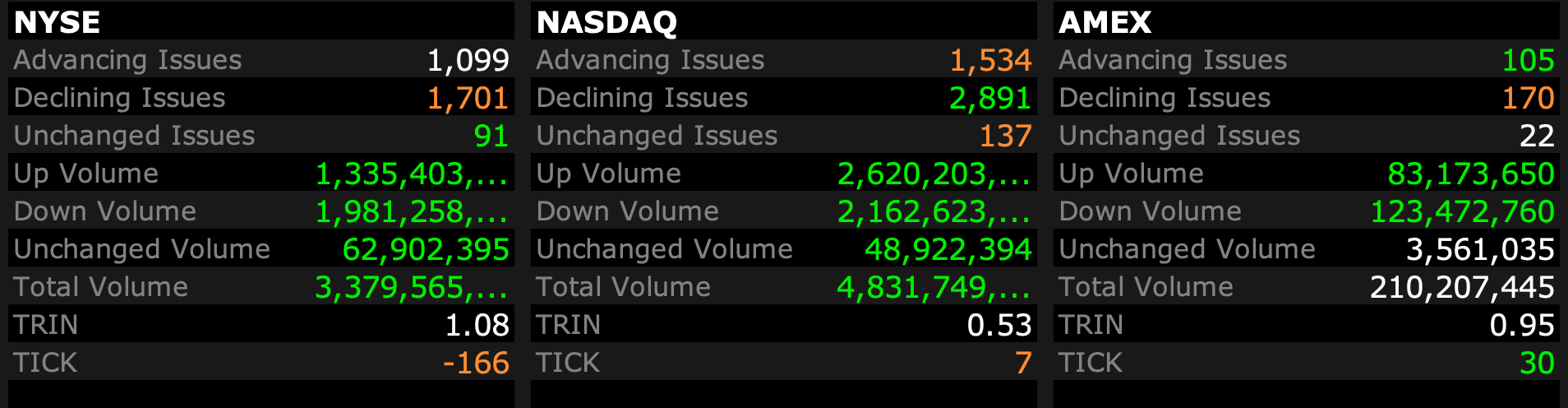

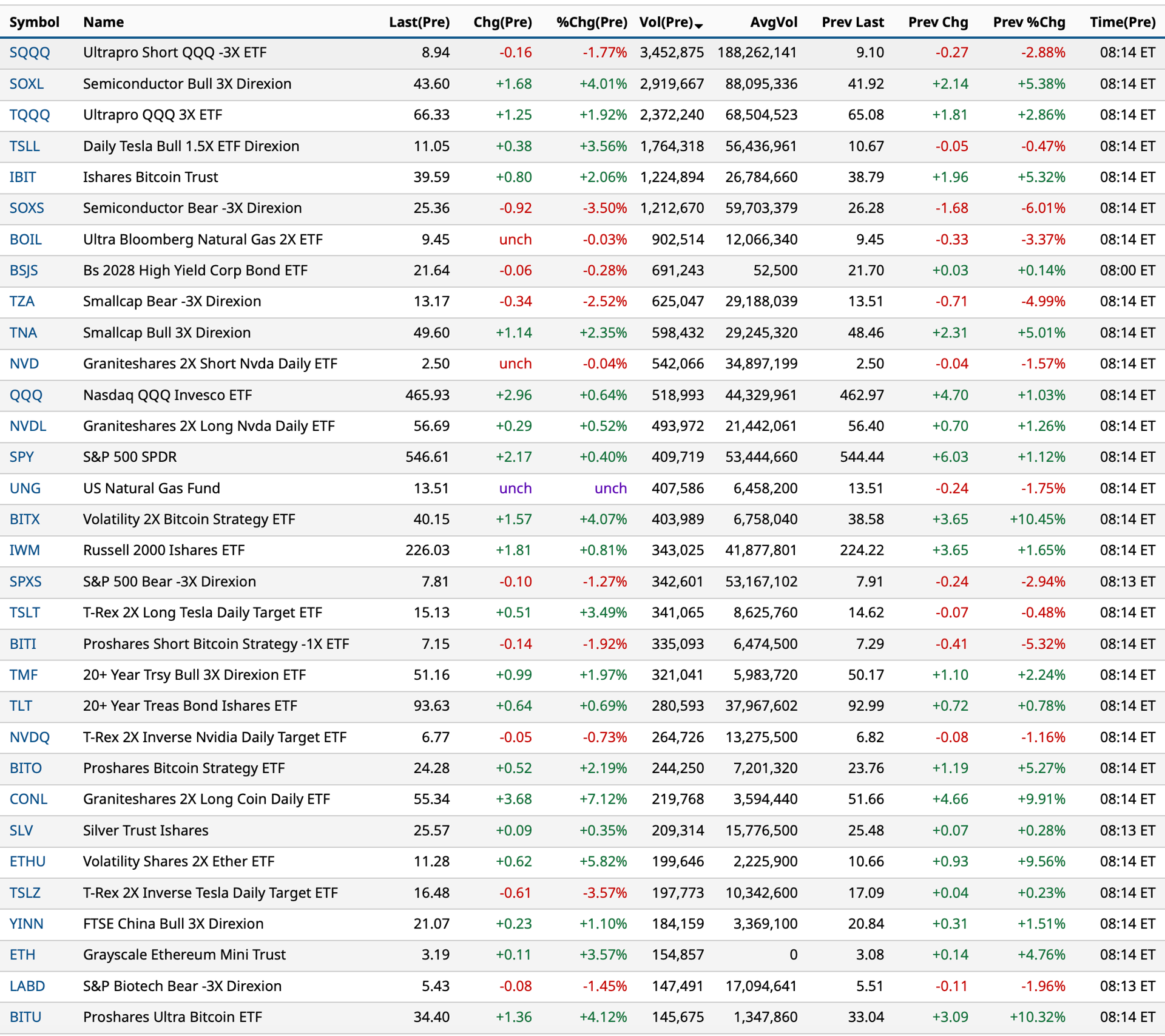

Exchange-traded fund moves as of 8:14 a.m. ET

BY Doug Kass · Jul 29, 2024, 9:20 AM EDT

Big movers, percentage-wise, as of 8:32 a.m. ET:

BY Doug Kass · Jul 29, 2024, 9:10 AM EDT

Here are the U.S. select premarket movers as of 8:23 a.m. ET:

-GH +12% (Shield Blood Test approved by FDA as a Primary Screening Option, Clearing Path for Medicare Reimbursement and a New Era of Colorectal Cancer Screening)

-CGTX +11% (Phase 2 SHINE trial demonstrates consistent improvement in cognitive outcomes with once-daily oral CT1812 in mild-to-moderate Alzheimer’s patients)

-INSP +11% (reports prelim Q2 revenue, raises FY guidance)

-ON +6.2% (earnings, guidance)

-L +5.5% (earnings; appoints new CEO)

-OIS +5.5% (earnings)

-RVTY +4.2% (earnings, guidance)

-MSTR +4.1% (BTC strength)

-COIN +3.7% (BTC strength)

-BABA +2.8% (said to start charging a basic software service fee of 0.6% on confirmed transactions for vendors on both the Tmall and Taobao platforms, starting from Sept 1st)

-CNK +2.3% (opening weekend of Deadpool & Wolverine was its highest-ever domestic opening box office for a film premiering during the summer moviegoing season)

-AKAM +2.2% (Guggenheim Securities Raised AKAM to Buy from Neutral, price target: $128)

-VTVT -45% (Cadisegliatin program for Type 1 Diabetes placed on Clinical Hold based on discovery of a chromatographic signal in a recent human absorption)

-NAMS -36% (Pivotal Phase 3 BROOKLYN Clinical Trial Evaluating Obicetrapib in Patients with Heterozygous Familial Hypercholesterolemia reported)

-IART -19% (earnings, guidance)

-SNDX -14% (US FDA extends Revumenib NDA PDUFA action date 3 months to December 26, 2024 for Relapsed or Refractory KMT2Ar Acute Leukemia)

-SILC -9.3% (earnings, guidance)

-ESGR -6.1% (to be acquired by Sixth Street for $330.00/shr in cash)

-ABT -5.3% (Missouri state jury finds Abbott's specialized formula for premature infants caused girl to develop dangerous bowel disease; Ordered to pay $95M in compensatory damages and $400M in punitive damages)

-PRKS -4.7% (prelim earnings)

-EXAS -4.6% (weakness from GH Shield Blood Test FDA approval)

-ALMS -3.2% (initiates ONWARD Phase 3 Clinical Program Evaluating ESK-001, an Oral TYK2 Inhibitor, in Moderate-to-Severe Plaque Psoriasis)

-ARLP -3.1% (earnings, guidance)

-ARM -1.9% (HSBC Cuts ARM to Reduce from Hold, price target: $105)

BY Doug Kass · Jul 29, 2024, 9:00 AM EDT

I am giving a presentation on the market outlook to a group of investors after the close.

Here is my power point of 27 charts and tables:

BY Doug Kass · Jul 29, 2024, 8:21 AM EDT

BY Doug Kass · Jul 29, 2024, 8:12 AM EDT

BY Doug Kass · Jul 29, 2024, 7:57 AM EDT

A core investment short McDonald's MCD spits the bit on earnings per share and announces weaker-than-expected organic sales.

Here is the company's press release. McDONALD'S REPORTS SECOND QUARTER 2024 RESULTS (prnewswire.com)

I have long been of the view that the cumulative or "stacked" inflation since 2020 bodes poorly for personal consumption expenditures.

Whether it is the cost of admission for theme parks (at Disney DIS or Comcast CMCSA) or the price of a latte - demand elasticity is hitting hard now.

A consumer-led economic slowdown likely lies directly ahead.

We are short 13 consumer related equities.

BY Doug Kass · Jul 29, 2024, 7:19 AM EDT

* I continue to expect cannabis rescheduling...

Not surprising, Republican legislators push back on rescheduling of cannabis:

BY Doug Kass · Jul 29, 2024, 7:05 AM EDT

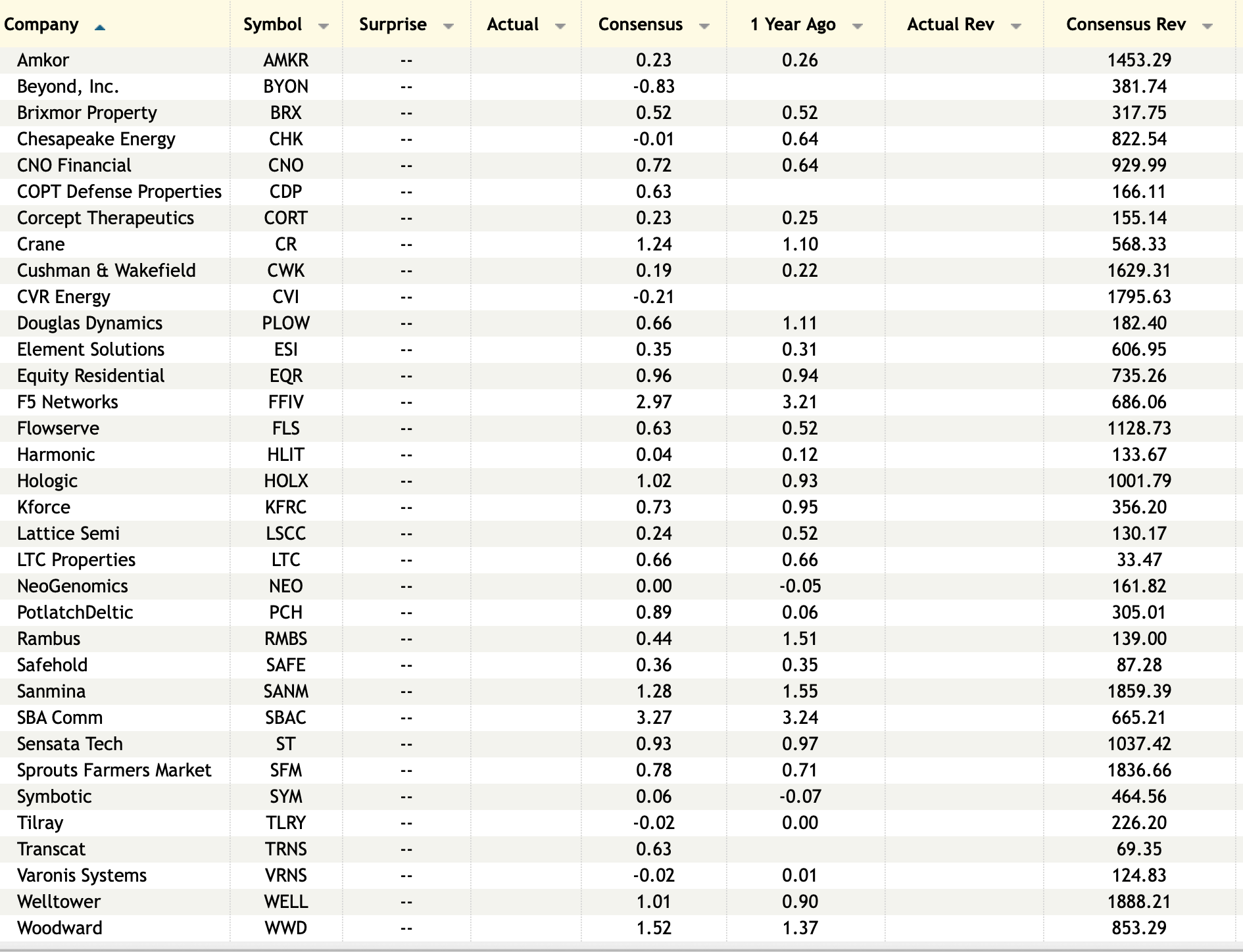

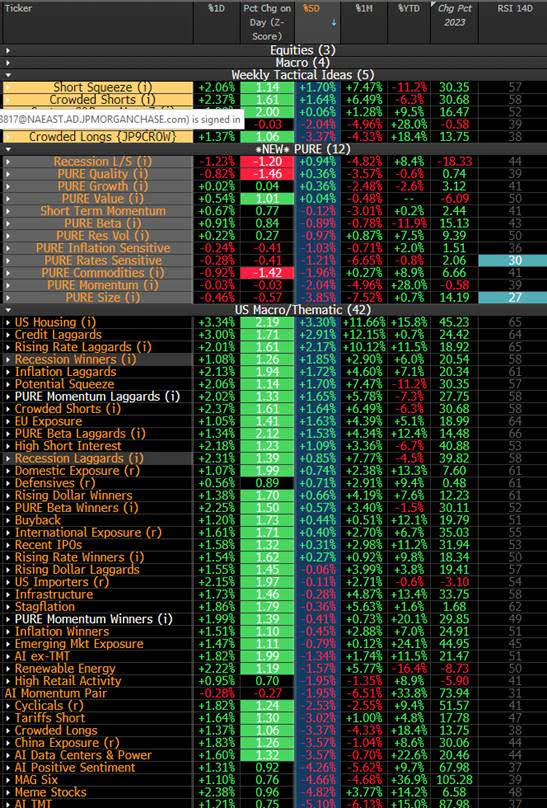

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Jul 29, 2024, 6:50 AM EDT

From JPMorgan:

US: Futs are higher with Tech rebounding from last week’s losses. Pre-mkt, MegaCap Tech are outperforming: GOOG/L +81bp, META +71bp, NVDA +57bp. Bond yields are 1-3bp lower and USD is higher. Commodities are mixed: oil lower and precious metals/ags are higher. We will enter one of the busiest weeks in Q1: we will hear from 3x Central Banks (Fed, BOJ and BOE), as well as a slew of labor market data (JOLTS, ADP, EXI, NFP) and ISM-Mfg. On earnings, we will hear from 40% of SPX companies, including MegaCap Tech (JUL 30: MSFT, JUL 31: META, AUG 1: AAPL, AMZN).

and...

EQUITY AND MACRO NARRATIVE: Last week, the SPX lost 83bp while RTY gained 3.5%. Since July 11, the NDX/RTY spread has declined -16.6% (NDX lost -8.0% vs. RTY +10.2%). In addition, Mag 7 (JP1BMAG7) and Semis (SOXX) have a -12.4% and -13.6% correction, respectively.

Despite relatively benign PMIs and PCE releases, last week’s losses were mainly driven by some notable earnings disappointments. Particularly, GOOG/L and TSLA kicked off a weak start of the MegaCap Tech earnings amid high expectations. Despite the fact that GOOG/L reported solid numbers across the broad, the YouTube ads revenues miss was enough to create a -8% decline in the following three trading days. Higher expectations are not limited to MegaCap Tech: FactSet data suggests that comparing to average levels, the market is rewarding positive EPS surprises less and punishing negative EPS surprises more.

This week, we will enter one of the busiest weeks in Q3: On macro, we will hear from 3x Central Banks (Fed, BOJ and BOE), as well as a slew of labor market data (JOLTS, ADP, EXI, NFP) and ISM-Mfg. On earnings, we will hear from 40% of SPX companies, including MegaCap Tech (JUL 30: MSFT, JUL 31: META, AUG 1: AAPL, AMZN). We discussed the tactical scenarios in July 22’s Morning Briefing (Macro Stronger/Weaker + Earnings Stronger/Weaker). After last week’s development, the market seems to be leaning towards the “stronger macro + weaker earnings” scenario. However, we are still relatively early on earnings calendar. This week’s earnings results will be critical to assess whether we can reenter the “stronger macro + stronger/resilient earnings” camp.

ROTATION – In July 22’s Morning Briefing, we wrote the following: “Returning to Equities and the April sell-off which saw the index lose ~5.5% over 3 weeks before retracing ~45% of those losses in the final week of April, clients are asking ‘Are we setting up for a repeat of that sell-off?’ I do not think so. That pullback in April saw 10 of 11 sectors and was characterized by surging bond yields in response to hotter than expected 24Q1 inflation; in the first 3 weeks of April the 10Y yield increased from 4.20% to 4.62% and VIX moved from 13.0 to 18.7. Energy was the only positive sector as oil made a 52-week high on Apr 5 ($84.24) before ending the period flat to where it started at $80.88. The current rotation is more driven by extended positioning, potential rate cuts, exhaustion of the AI trade, and the hopes for a broader catch-up (SPX493) based upon improving earnings.” We still hold the same view and see this week’s earnings to be the most critical catalysts to assess this current rotation.

o Our Positioning Intelligence team tells us that “there has not been very clear or outsized capitulation in equities” and sees uncertainty around current rotation.

o On the other hand, Our Delta-One desk (Manish Sinha) tells us that we saw the outperformance in Growth and quality factors, which typically indicates that the rotation is nearing its end.

· EARNINGS UPDATES – FactSet data says that with 41% of the SPX reporting, the aggregated earnings and revenue surprise are 4.4% and 1.1%, respectively. That said, if we assume the market consensus for the rest of the companies holds, that will give us a 9.8% and 5.0% YoY growth in earnings and revenue. On sector basis, Tech and Financials are leading the earnings growth. Interestingly, comparing to the previous seasons, markets have been rewarding less on positive surprise and punishing more on negative surprise, partially driven by the fact that equities reached their all-time highs into the earnings season. Margins are holding well: the blended 24Q2 net profit margin for SPX is 12.1%, higher than 11.6% in 23Q2 and 11.8% in 24Q1. Financials and Tech reported the highest YoY increase in net profit margin.

· CENTRAL BANKS - This week, we will hear from 3x central banks (Fed, BOJ and BOE). Feroli expects no policy changes at the meeting and points that the main focus will be any tweaks to the post-meeting statement and Powell’s press conference. He expects Powell to express greater confidence but avid giving any calendar guidance. On BoJ, JPM Economist Ayako Fujita has an out-of-consensus view that BoJ will raise policy rate by 15bp to 0.25% (consensus sees no change to policy rate). If this comes to fruition, Jay Barry tells us that we will likely see a bearishly flatter JGB curve, which is marginally bearish for US yields.

BY Doug Kass · Jul 29, 2024, 6:35 AM EDT

* Confident technicians embrace small-cap...

* Ten cuidado!

"I think the best rule for me personally, is that if I feel a little unsafe where I'm going, then I'm going in the right direction. If I'm feeling comfortable with what I'm doing, something's wrong."

- David Bowie

Technicians follow price, by definition. So there is a lot of technical observations in today's column about how cheap the Russell Index is relative to the S&P Index. The rotation into small-cap is the rotation du jour. But, just as technicians confidentally embraced the Mag 7 (recently and near the top, before a sharp correction), they are equally confident that small is now better:

Bonus: Here are some great links:

Stock Market Analysis (AlphaTrends)

BY Doug Kass · Jul 29, 2024, 6:20 AM EDT

Funny:

Ludacris Forecast: Beer companies (who are losing market share to weed cultivators/dispensaries are the first to acquire cannabis companies after rescheduling is announced.

BY Doug Kass · Jul 29, 2024, 5:46 AM EDT