Flu Season

I am under the weather a bit (summer flu!) so outta here early today.

Thanks for reading.

Enjoy the evening.

Be safe.

BY Doug Kass · Jul 22, 2024, 3:49 PM EDT

I am under the weather a bit (summer flu!) so outta here early today.

Thanks for reading.

Enjoy the evening.

Be safe.

BY Doug Kass · Jul 22, 2024, 3:49 PM EDT

From the Washington Post:

BY Doug Kass · Jul 22, 2024, 3:41 PM EDT

Occidental Petroleum OXY trades like a dog with fleas.

Thus far (with apologies to my dachshunds Ollie and Daisy), not re-engaging has been the right "call."

BY Doug Kass · Jul 22, 2024, 3:36 PM EDT

With S&P cash +59 handles I am back shorting Index calls (in the money, August expiration).

BY Doug Kass · Jul 22, 2024, 2:36 PM EDT

Our Trade of the Week from eleven days ago, TerrAscend (TSNDF) is +14% today to $1.45.

From early July:

TerrAscend (TSNDF) is among the most attractive cannabis equities.

Well managed and strategically located (geographies).

From my friend Shadd Dales and The Dales Report.

Position: Long TSNDF (S)

BY DOUG KASS JUL 11, 2024 10:45 AM EDT

BY Doug Kass · Jul 22, 2024, 2:04 PM EDT

Abie from Brooklyn responds to my AI/CrowdStrike column:

Dougie

my guess is that CRWD now introduces a premium service level where they guarantee an experienced coder actually checks the code before they blow your company up.and yes, the coding error was indeed SO basic as to practically guarantee that no human programmer checked it before it was put into service....it referred to a place in memory where the rule is "NEVER GO THERE" so it's basically a community college level entry course programming error....or sabotage

MIT tech magazine this issue has a BIG article on "WHAT IS AI?" which i read to say:1. AI is above all other things right now at least, just a HUGE correlation machine...so big, it doesn't seem possible for creators to actually see what correlations are being made2. Because it learns correlations and generates predictive rules from that, it is subject to too kinds of critical errors a. the "correctness" and "completeness" of the correlations are hugely dependent on the data bases from which it has acquired data and calculated correlations. Now that many data bases are restricting access to their site data, that will be come both more expensive and likely less complete in future AI "trainings" and b. will always be subject to the errors of all correlations when and if they are not actually completely causal in nature, there will those outcomes that do not fit the expected correlation and BOOM!! when they are important

I suppose AI training can try to brute force these problems:-- more data and even try to create algorithms that can recognize unrealistic responses but looks to me like we are creating a new generation of AI babysitters that review all the output of AI that matters enough to support the expense.

BY Doug Kass · Jul 22, 2024, 1:10 PM EDT

This was a prescient technical view of Disney DIS from Bobby Lang — back a few months ago.

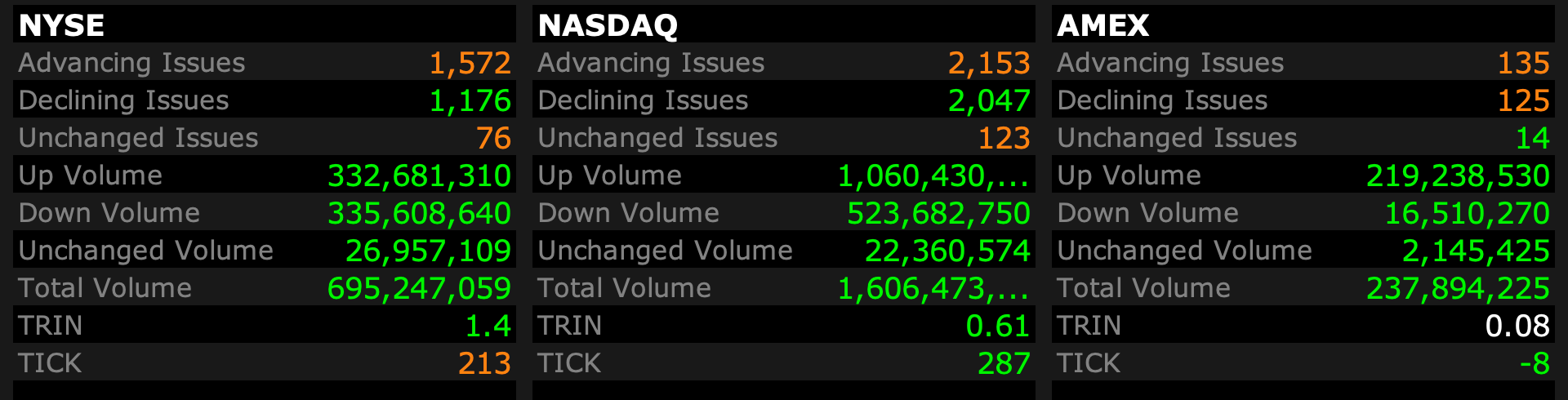

BY Doug Kass · Jul 22, 2024, 11:55 AM EDT

- NYSE volume 121M shares, 12% below its one-month average;

- NASDAQ volume 1.56B shares, 5% below its one-month average;

- VIX down 6.23% to 15.49

BY Doug Kass · Jul 22, 2024, 11:25 AM EDT

Dougie Kass

Today's Trades (my opener is in seque)

Covered my SBUX short at $76.52.

Buying MSOS with $7.55 limit.

Sold my GRBK long at $71.62.

Added to TOL $132.37 and DHI $175.54 shorts.

With S&P cash +54 I sold small (and adding on a scale) SPY and QQQ calls (in the money, monthly Augusts).

BY Doug Kass · Jul 22, 2024, 11:00 AM EDT

On the subject of what caused the Crowdstrike CRWD problem that caused a global internet glitch last week, there is a fair bit of speculation on the Web.

We have different hypotheses of what went wrong. But the stuff I have seen all suggests the coding error was quite simple and basic. I suspect this is one more thing we will never get a clear answer to, but I wouldn’t be surprised if the problem was that whoever made the mistake with the section of code in question used a generative AI tool to help write it. It could be just a coincidence, but it is interesting we had the biggest self-inflicted crash of all time when programmers have started to use generative AI to help write code.

It's just like when the chatbots first rolled out, and a lawyer naively tried to use one to help with a legal brief, only to learn he cited fake cases (and got in trouble with the judge). Is it possible the programmer got bad or hallucinated code? Granted, I am speculating, although I expect we will never know for certain exactly what happened. We might find the exact source of the error, but probably not why the error was made. It will be interesting if it is as simple and basic as some are suggesting.

Following is my prior diary entry on the issues with generative AI writing code from July 9:

The following blurb on AI writing code is interesting.

This is something I was under the impression that it was better at doing, in part because code is more strictly rules-based. But recently I had been hearing stories that it is not so great at writing code, either.

First of all, AI was only good for basic low-level code to begin with. Then I have been told its performance is degrading. Sure enough, I was just sent the blurb below with excerpts from an assistant professor at the University of Glasgow. AI's code work is getting worse and not better. In part that's because it cannot think and needs humans, and it's in part because the technology itself does not work well and is unstable. What we are seeing now is akin to the little boy putting his finger in the dike to stop a leak, but new leaks keep springing up. No matter how much money you spend, if the dike is faulty, you are not going to make it viable:

Overall, ChatGPT was fairly good at solving problems in the different coding languages—but especially when attempting to solve coding problems that existed on LeetCode before 2021. For instance, it was able to produce functional code for easy, medium, and hard problems with success rates of about 89, 71, and 40 percent, respectively.

“However, when it comes to the algorithm problems after 2021, ChatGPT’s ability to generate functionally correct code is affected. It sometimes fails to understand the meaning of questions, even for easy level problems,” Tang notes.

For example, ChatGPT’s ability to produce functional code for “easy” coding problems dropped from 89 percent to 52 percent after 2021. And its ability to generate functional code for “hard” problems dropped from 40 percent to 0.66 percent after this time as well.

“A reasonable hypothesis for why ChatGPT can do better with algorithm problems before 2021 is that these problems are frequently seen in the training dataset,” Tang says.

Essentially, as coding evolves, ChatGPT has not been exposed yet to new problems and solutions. It lacks the critical thinking skills of a human and can only address problems it has previously encountered. This could explain why it is so much better at addressing older coding problems than newer ones.

“ChatGPT may generate incorrect code because it does not understand the meaning of algorithm problems.” —Yutian Tang, University of Glasgow

“ChatGPT may generate incorrect code because it does not understand the meaning of algorithm problems, thus, this simple error feedback information is not enough,” Tang explains.

BY Doug Kass · Jul 22, 2024, 10:05 AM EDT

From Peter Boockvar:

Another drama filled weekend/I'm feeling big moves in next two weeks/Other good stuff

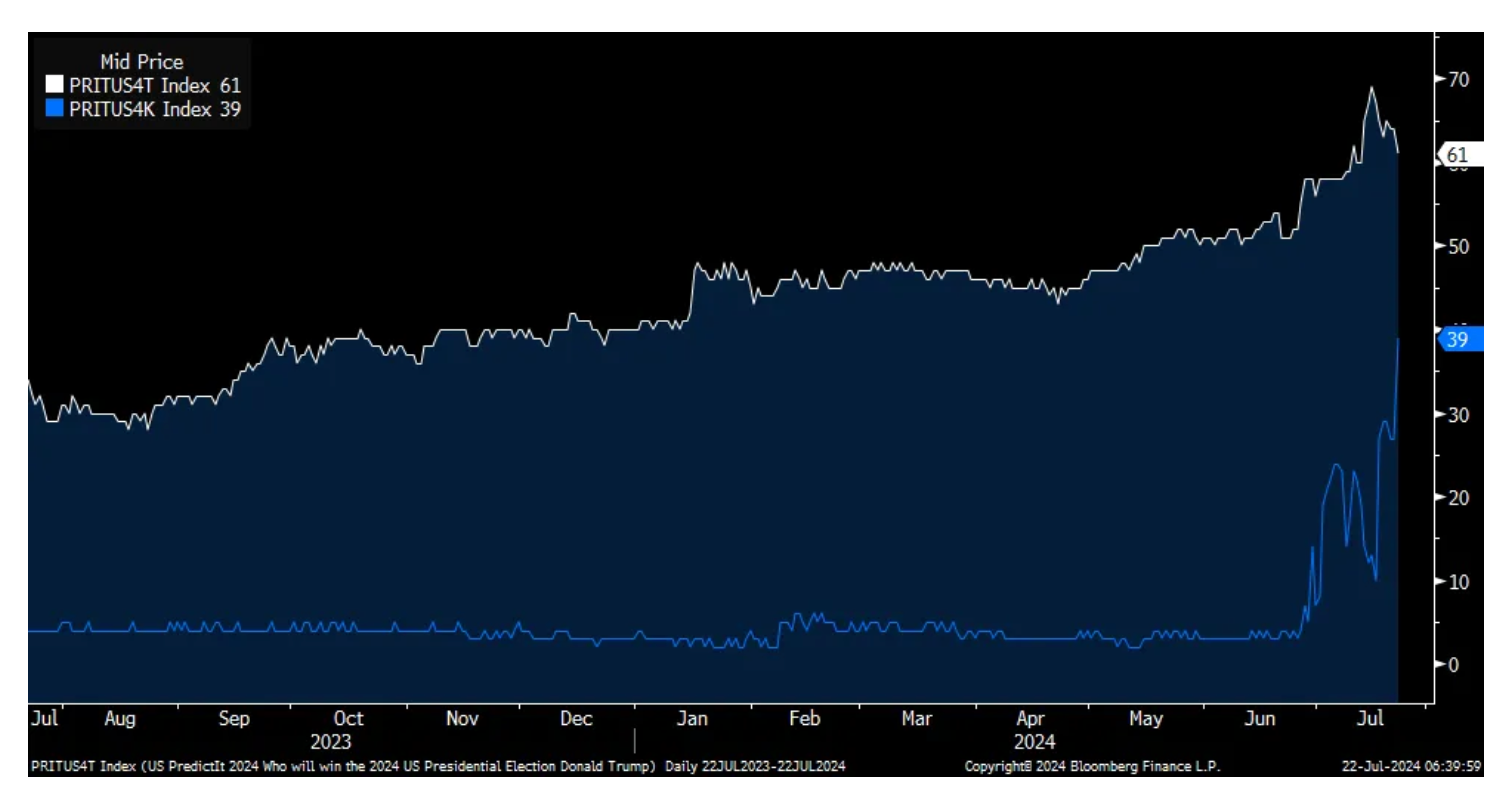

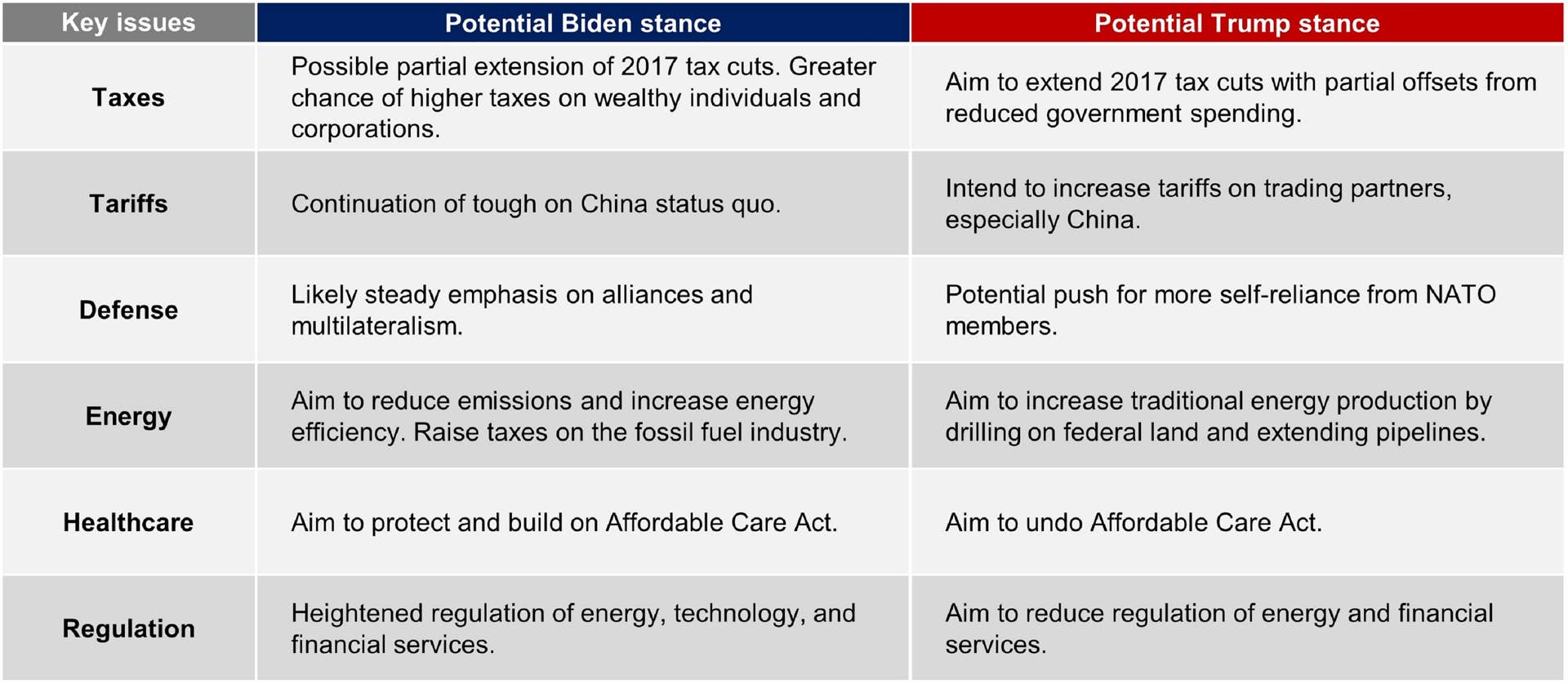

According to PredictIt, Trump's odds of winning have slipped by 3 pts from Saturday to 61%. Harris has jumped to 39%. With my back of the envelope economic analysis/guesses, and of course depending on how Congress shakes out in terms of control, I don't expect a change in the corporate tax rate regardless of who wins. Debts and deficits are going to continue to skyrocket regardless of who wins. If Trump wins, we'll get a full extension of the 2025 tax cuts but a possible slew of tariffs, more protectionism and likely a weaker dollar. If Harris wins (assuming she's the nominee), some of those Trump tax cuts will not be extended and we'll get only some tariffs but still a lot of protectionism and possibly a weaker dollar. With respect to the regulatory state, the Chevron Supreme Court overrule will send more authority over to Congressional lawmaking and judicial discretion and away from the Executive Branch, thus limiting the ability of either to act but Trump will do his best to ease the burden while Harris will do the opposite. Either way, I think up until the election markets are going to trade more so on the trajectory of inflation, earnings, the economy and what the Fed does.

Trump in white, Harris in blue

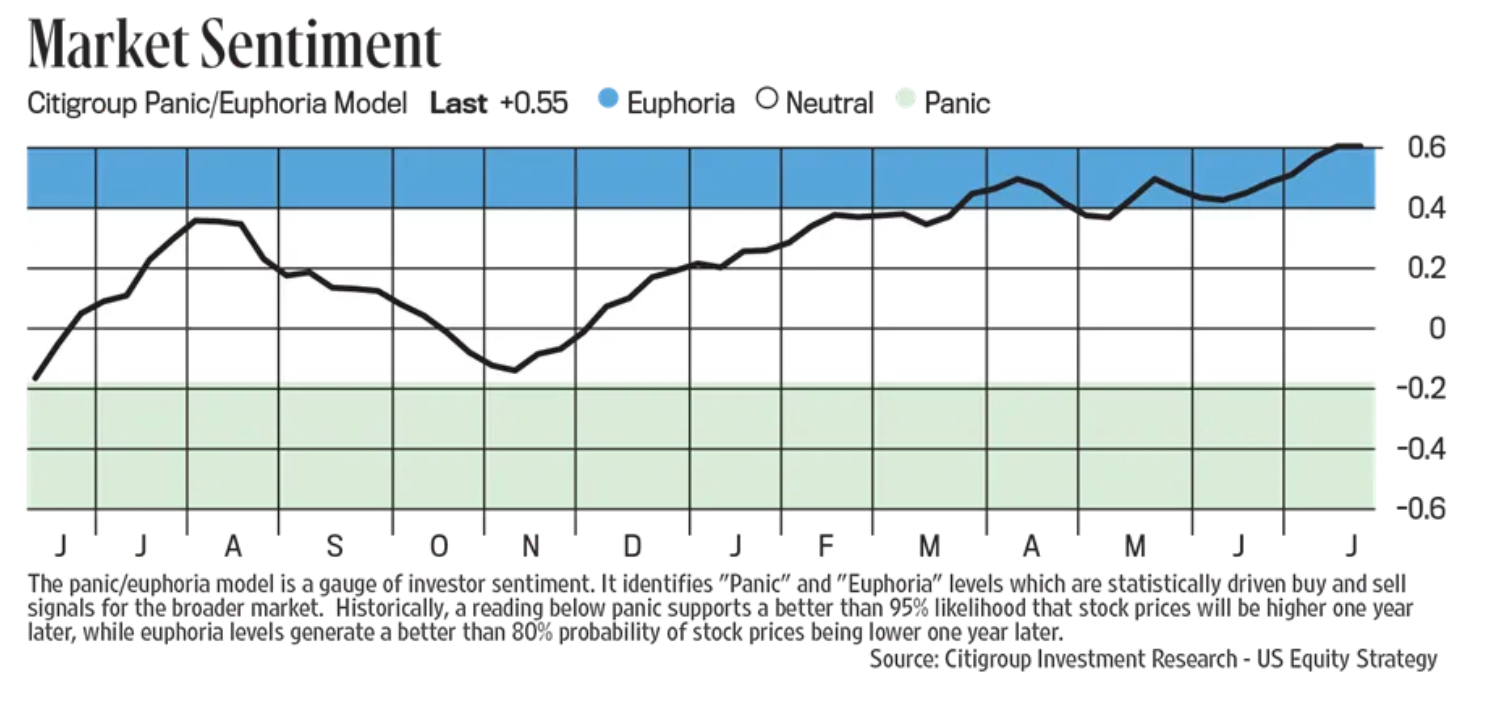

I feel like we're headed for some big market moves over the next two weeks as we digest a flood of earnings, and particular from the biggest cap names. I always like to say that valuations don't matter until they do and all of a sudden they have in both directions. The biggest names are finally being questioned in terms of whether all this AI spend will deliver suitable returns and whether they will be impacted by the broader economic worries at the same time the stocks have little valuation support if they disappoint and the small and mid cap names are finally being discovered for the bargains that many of them are. Also, notwithstanding some shaking of the tree in those big names, and a VIX on Friday that closed at the highest level since April, the level of bullishness is dangerously high (from a contrarian standpoint). The updated Citi Panic/Euphoria index, seen over the weekend, rose to a fresh multi year high at .56 from .52 in the week prior. The threshold for Euphoria is .41.

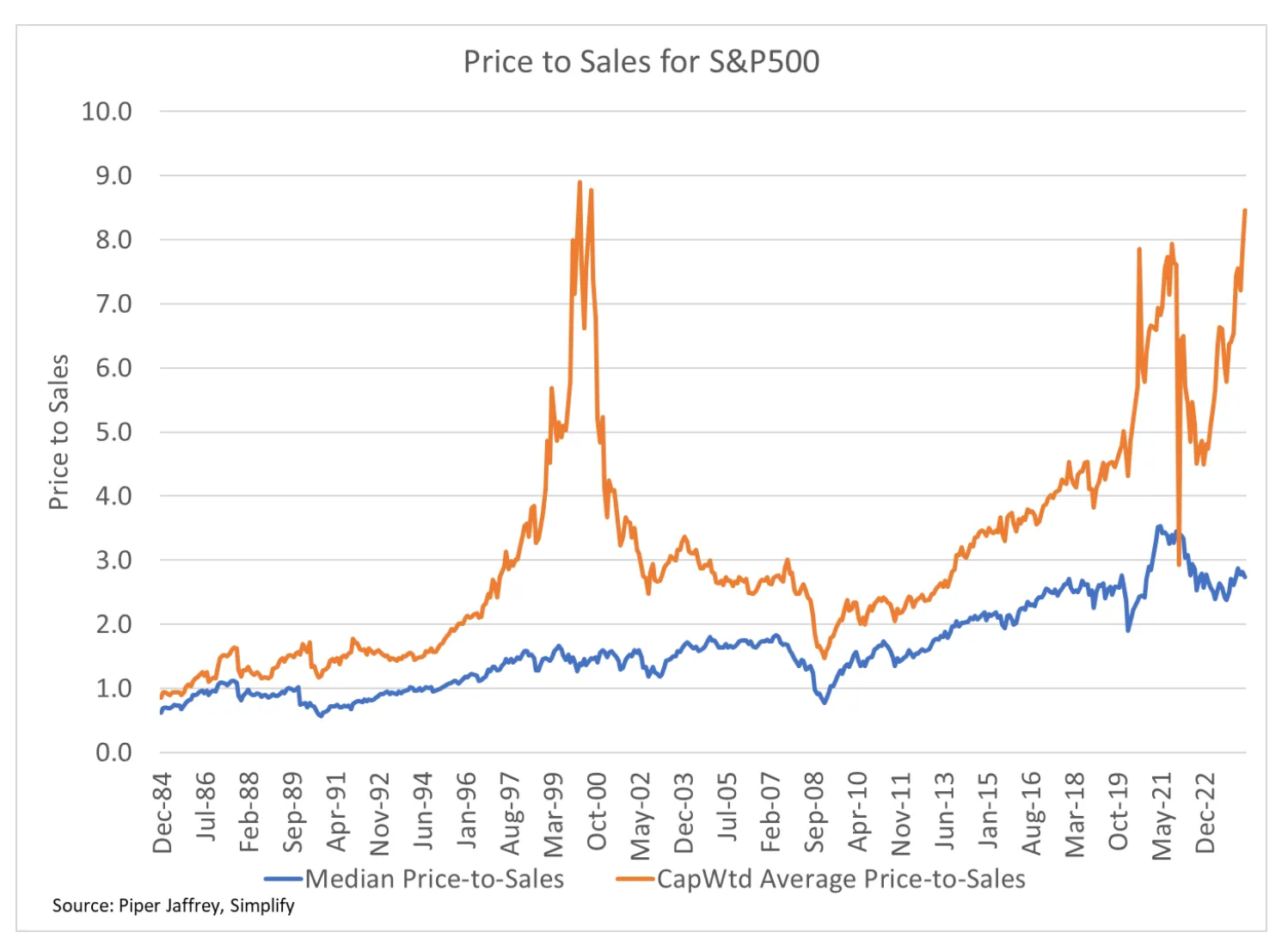

Thanks to my friend Michael Green who showed me this chart on Friday highlighting the valuation divergences in the broad large cap market relative to the biggest names.

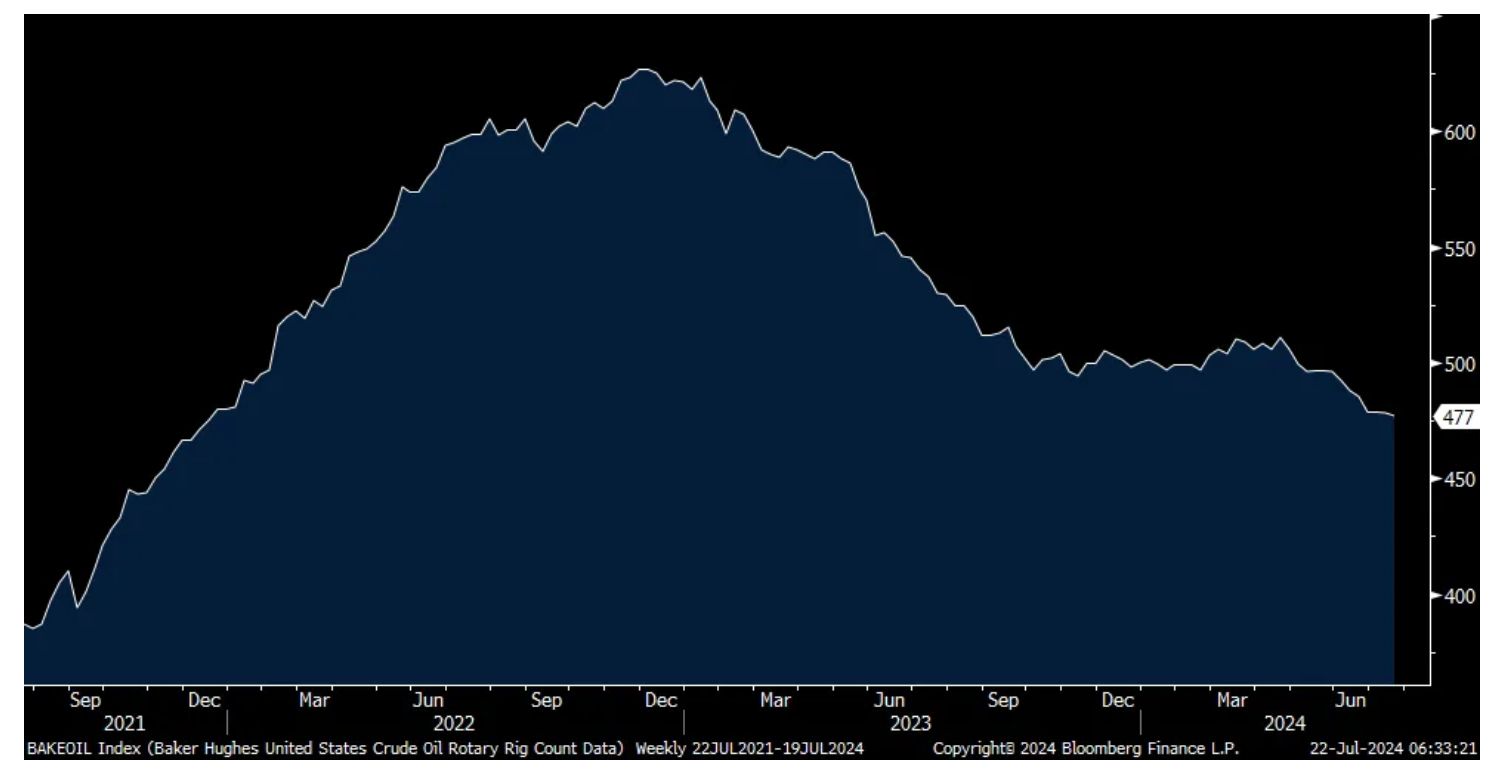

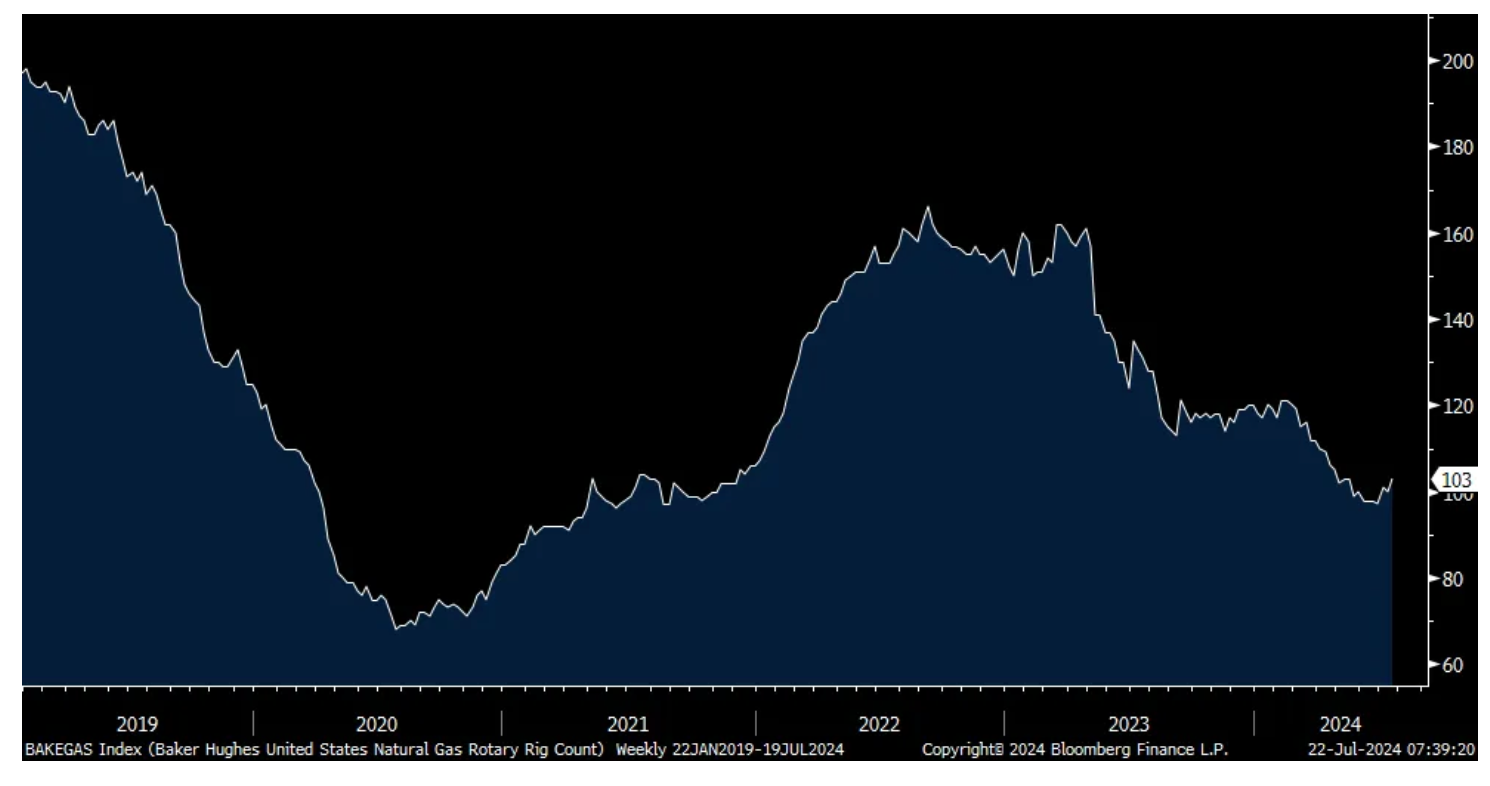

I'll reiterate our positive and long stance on oil and gas stocks as the crude oil rig count keeps on dropping. Though down just 1 rig w/o/w, at 477 it is the least since December 2021. The natural gas rig count has rebounded this month by 6 rigs but at 103 it's down from 160 early last year.

Oil Rig Count

Natural Gas Rig Count

China surprised markets with a 10 bp rate cut for its 7 day repo rate, which impacts short term rates and the 1 yr and 5 yr loan prime rate that influences bank lending rates. The new rates are 1.7%, 3.85% and 3.35% respectively. While 10 bps are really meaningless, China is trying to quicken the trip through the residential real estate downturn. I think the best policy rolled out so far in terms of absorbing the excess supply is turning many of the unused buildings into rentals. Time though is what is most needed for the housing market but there is little doubt that the dropping home prices is negatively impacting the wealth psychology of the Chinese, many of which have most of their net worth in property.

The market response was mixed as the Shanghai comp fell .6% but the H share index in Hong Kong rallied as did the Hang Seng. The yuan is a touch lower for a 3rd day vs the US dollar.

Shifting to earnings, Ryanair is trading down by 14% in Dublin after they disappointed. The CFO said this on their earnings call, "Consumers are just a little bit more frugal. People want to get out there, but they're just a bit more cautious in how they're spending their money." They also expect lower ticket prices this summer but based on what we've heard from other airlines, capacity is coming out of the industry quickly.

From American Express:

Said Friday but similar to the Ryanair comments, "We did see some slower growth in certain T&E categories vs the prior quarter, such as in airline and lodging."

But also this, "At the same time, growth in our largest T&E category, restaurants, remained strong and goods and services strengthened a bit vs the prior quarter when excluding the impact of the Leap year."

"Obviously, organic spending, we'd like to see a little bit higher, but it is a slower growth economic environment."

On the corporate side, "Spending growth from our US small and medium enterprise customers increased a bit sequentially vs last quarter but remained modest." They are seeing faster business spend from their international customers.

Overall, "while we are not in a high growth spend environment, particularly in the US, our spending volumes are tracking in-line with our expectations and support our revenue expectations for the year."

Fifth Third Bancorp told us where their loan growth was the best:

"In our industry verticals, production was strongest where federal government spending has had an outsized benefit, including in aerospace, and defense contractors and with manufacturing and infrastructure construction firms." Total average portfolio loans and leases were flat q/o/q.

"As we look ahead to the rest of the year, we remain cautious due to the wide range of potential economic and geopolitical scenarios that could unfold. As a result, we will remain disciplined and will not chase loan growth at the expense of our return targets."

From PPG Industries, the coatings company:

"our aggregate volumes in the quarter were flat y/o/y, falling shy of our initial expectations as overall demand in Europe and global auto OEM production were below what we assumed in our 2nd quarter guidance."

On costs, "we experienced mid single digit percentage raw material deflation that we expect will normalize into flat to low single digit deflation for the 3rd quarter as we anniversary prior year impacts. This benefit was partially offset in our results by general inflation, including higher y/o/y wages and employee benefits."

On pricing pass through, "We anticipate overall company selling prices to be flat in the third quarter."

With respect to the overseas data of note, Taiwan disappointed with a June export orders figure up 3.1% y/o/y vs the estimate of up 12.3%. There was a slowdown in exports to Japan (maybe weaker yen having an influence) and to China. Taiwan's economy ministry said "The growth of the global economy will continue to be affected by high interest rates, and risks from US-China trade and geopolitical issues remain, which may inhibit the momentum of global trade growth." The TAIEX continued with its selloff, lower by 2.7% and down by 3.4% month to date.

BY Doug Kass · Jul 22, 2024, 9:35 AM EDT

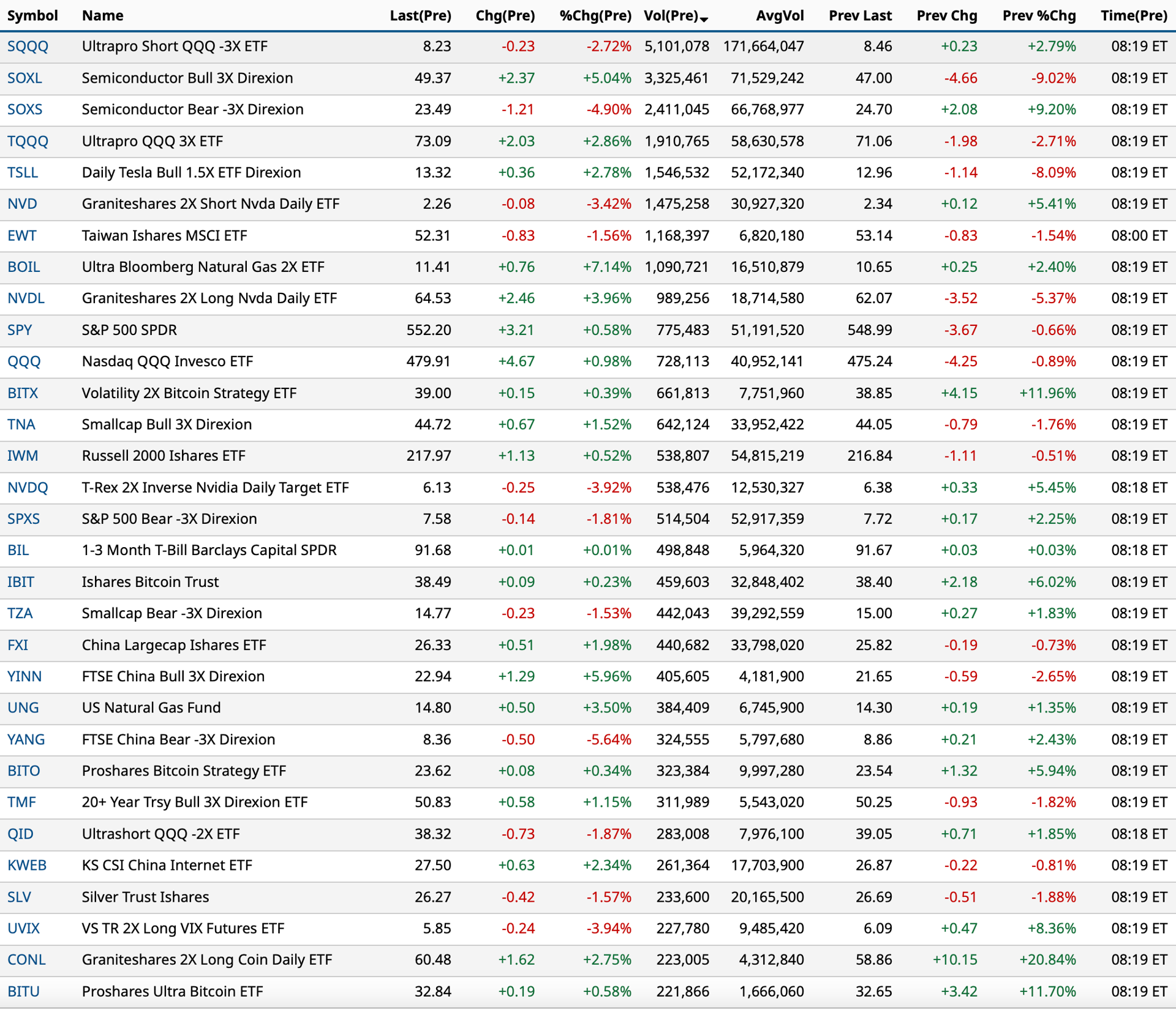

As of 8:40 a.m.:

BY Doug Kass · Jul 22, 2024, 9:12 AM EDT

As of 8:19 a.m.:

BY Doug Kass · Jul 22, 2024, 9:00 AM EDT

Upside:

-TELL +65% (Woodside Energy Group to acquire Tellurian in cash deal with EV of $1.2B)

-HEPA +19% (Pharma Two B plans to go public via merger with Hepion and concurrent $11.5M private placement)

-CLW +12% (enters into Definitive Agreement to sell tissue business to Sofidel America Corporation for $1.06B)

-DQ +7.2% (Board authorizes $100M share repurchase program)

-MEIP +6.3% (to consider strategic alternatives including potential transactions and out-licensing opportunities for existing programs and merger and acquisitions)

-S +5.4% (continued strength following CRWD disruption)

-TXG +4.4% (Jefferies Raised TXG to Buy from Hold, price target: $24)

-EMBC +4.3% (reportedly hired advisor amid sale consideration)

-VSTO +3.9% (CGS increases purchase price offer for Kinetic Group from $2.0B to $2.15B and increased cash consideration of $24.00/shr; affirms FY25 guidance)

-STIM +3.8% (Aetna expands TMS availability for adolescents with depression, effective immediately)

-ON +3.1% (selected to power Volkswagen Group’s next-gen EVs)

-IONS +2.5% (announces positive detailed results from HALOS Study of ION582 in people with Angelman syndrome)

-IQV +2.5% (earnings, guidance)

-SAVA +2.3% (anticipates successful Simufilam Phase 3 trials, with read out by December 2024, in Alzheimer’s disease as 24-month open-label Phase 2 clinical safety trial demonstrate stable cognition for two full years in Alzheimer’s disease patients with mild dementia)

-TLRY +2.2% (receives first new cannabis cultivation license in Germany under new regulations)

-NVDA +2.1% (said to working on new version of 'flagship AI chips' for China market compatible with US export controls)

Downside:

-RYAAY -14% (earnings, guidance)

-CRWD -4.4% (continued weakness following software update that caused widespread crashes)

-VZ -3.3% (earnings, guidance)

-IMMP -3.1% (holds meeting with FDA on Phase III Design in Non-Small Cell Lung Cancer)

-IPG -2.0% (Morgan Stanley Cuts IPG to Underweight from Equal Weight, price target: $28)

BY Doug Kass · Jul 22, 2024, 8:49 AM EDT

* The toxic interaction of monetary and fiscal policy has now led to a nation of entitlements with a bloated balance sheet and an unsustainable budget.

Interesting article from David Stockman:

Fed’s Fake Victory Over Inflation - LewRockwell

The section below reminded me of something. The Fed (and U.S. government) seem to make up the rules as they go along.

Remember the notion introduced out of thin air a few years ago that if inflation runs below targeted rates for a period of time, it should be allowed to run above targeted rates for a period of time, to make up the difference? That one didn’t turn out too well.

At any rate, shouldn’t the same logic hold in reverse? They would probably try to argue otherwise and claim deflation is more dangerous than inflation. It is beyond me how you can make that distinction, history tells you both can be dangerous, although I do think there have been more inflationary disasters than deflationary disasters.

Further, I am not sure the risk of deflation exists to the degree everyone seems to fear (nor could it exist if we didn’t have the inflationary bubbles in the first place that put excess into the system). Lack of inflation, especially when driven by productivity, is not a bad thing, and ought to have been left alone in the past. Recently, it seems that the risk of deflation has only come from inflationary bubbles popping — which is interesting.

We have a doom loop now. Recessions used to be considered an inevitable and ultimately positive (although uncomfortable while they are happening) part of a capitalistic economy. I guess we now have a planned economy — it is hard to argue otherwise when looking at the bulk of the evidence. As discussed in the article, the Fed really does seem to make it up as they go along. They also use data they know are bad to guide decisions, because the data are designed to lean loose, which is what the mono-thinkers prefer.

The toxic interaction of monetary and fiscal policy, has now led to a nation of entitlements with a bloated balance sheet and an unsustainable budget, along with a population that expects to be coddled and not work. We also have come to a place where belief in the system is starting to collapse. Without belief, it does not work. Belief is an odd notion, and not quantifiable, but very important.

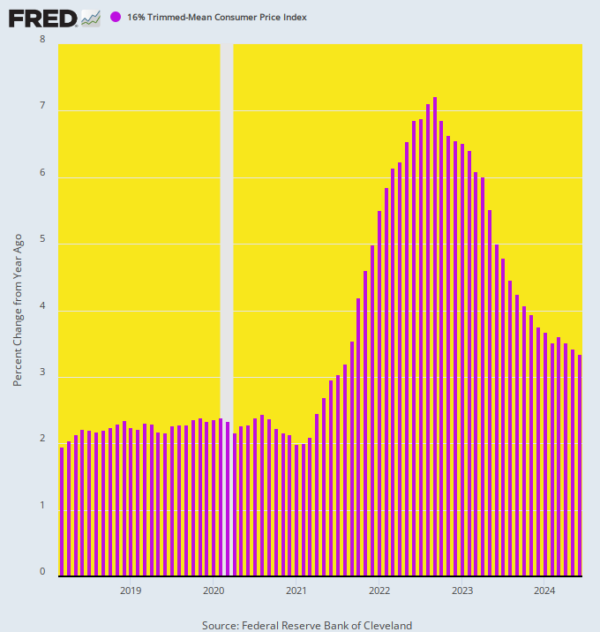

The chart below, which depicts the trend of Y/Y change in the 16% trimmed mean CPI, tells you all you need to know about the true inflation story at present. For the last 75 months running, the most stable measure of inflation available has posted Y/Y inflation well above 2.00%. On a cumulative basis, in fact, the gains have averaged 3.7% per annum.

To be sure, the 2.00% annual inflation “goal” itself is nonsense. Yet when you overshoot even that arbitrary pro-inflation target by nearly 100%, why in the world is the Fed claiming that victory over inflation is at hand, and that the next round of rate-cutting and monetary stimulus is fixing to commence?

If nothing else, you’d think that the paint-by-the-numbers monetary central planners at the Fed would at least deign to give America’s battered savers and wage earners an extended breather from inflation risk for several more quarters or even years. That is, by keeping its foot on the monetary brakes the Fed could preclude another burst of inflation—even as the most recent outbreak was being absorbed by savers, wage earners and entrepreneurs.

Y/Y Change In 16% Trimmed Mean CPI, March 2018 to June 2024

BY Doug Kass · Jul 22, 2024, 8:40 AM EDT

DraftKings DKNG price target lowered to $50 from $54 at BofA BofA lowered the firm's price target on DraftKings to $50 from $54 and keeps a Buy rating on the shares. Ahead of the company reporting earnings after market close on August 1, the firm is lowering its Q2 EBITDA estimate to $130M, compared to DraftKings' Q2 guidance of $150M, to reflect unfavorable hold outcomes and higher customer acquisition, but adds that it thinks investors are expecting a Q2 miss. The firm is also lowering its 2024 EBITDA estimate to $440M, compared to current guidance of $460M-$540M, but adds that it is encouraged by DraftKings' 36% year-to-date handle growth and calls the digital gaming space "a rare high-growth subsector in consumer."

Warner Bros. Discovery WBD could be worth $11 in break-up, says Citi Citi believes that with the shares down 25% year-to-date, Warner Bros. Discovery management may consider strategic alternatives. Press reports suggest one option the company may consider is breaking up into two entities, the analyst tells investors in a research note. Under this scenario, Citi's sum-of-the-parts suggest the equity could be worth $11 per share. It keeps a Buy rating on the shares.

BY Doug Kass · Jul 22, 2024, 8:03 AM EDT

BY Doug Kass · Jul 22, 2024, 7:50 AM EDT

Berkshire Hathaway BRK.B has sold over 33 million shares of Bank of America BAC.

BY Doug Kass · Jul 22, 2024, 7:40 AM EDT

US: Futs are higher led by Tech with RTY positive but lagging; pre-mkt Mag7 and Semis are leading. Bond yields are mixed as the yield curve twists flatter and USD is weaker. Cmdtys are mixed with Ags higher and Energy/Metals lower. The biggest news is Biden dropping out of the Presidential race and VP Harris is now the presumptive nominee, though others may enter the race. We had seen some unwinds of the Trump Trade, it is possible that unwinds further as the market looks to Trump with a split Congress. It is a light macro day as we enter the second busiest week of earnings season with ~20% of the SPX reporting.

and...

EQUITY AND MACRO NARRATIVE: Last week, the SPX lost 2.0% its biggest loss since the April sell-off. The losses last week were driven by a rapid rotation catalyzed by the dovish July 11 CPI print that seemingly cemented September as the launch for the next easing cycle. At one point during the week, RTY registered its largest 5-day outperformance relative to SPX in history. This rotation occurred as the yield curve bear flattened; the 10Y yield added 5.6bps closing the week at 4.24%. Sector outperformance was a mix of Cyclicals (Energy, Financials, and Industrials) and Defensives (Real Estate, Staples); this occurred as Tech was sold. Mag7 lost 5.3% its worst performance since late April when it lost 7.8% in a week.

Despite the violent moves in Equities, my colleague Calvin Chan tells us that IG Credit closed the week 1bps wider at 105bps; while this outperformed Equities it underperformed HY. Calvin points to Credit index composition differentials as a reason IG likely outperforms Equities should this rotation persist. That said, IG Credit is trading with a bearish tilt given negative seasonals, a heavy primary calendar, weaker liquidity, and a broader macro rotation illustrated by the move in VIX from 12 to 16. Similarly, Ben Schaefer points to the rotation benefitting HY Credit as the asset class is thought to be a beneficiary of a Trump Presidency. Separately, Ben flags that BBs are very rich relative to BBBs. A trade that our Credit Strategists like is buying Protection on CDS Indices (Saul Doctor’s full note is here).

BY Doug Kass · Jul 22, 2024, 7:30 AM EDT

From Rev Shark:

BY Doug Kass · Jul 22, 2024, 7:15 AM EDT

BY Doug Kass · Jul 22, 2024, 7:05 AM EDT

This is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Jul 22, 2024, 6:50 AM EDT

"Successful investing is about having people agree with you... later."

- James Grant

Bonus — Here are some great links:

BY Doug Kass · Jul 22, 2024, 6:35 AM EDT

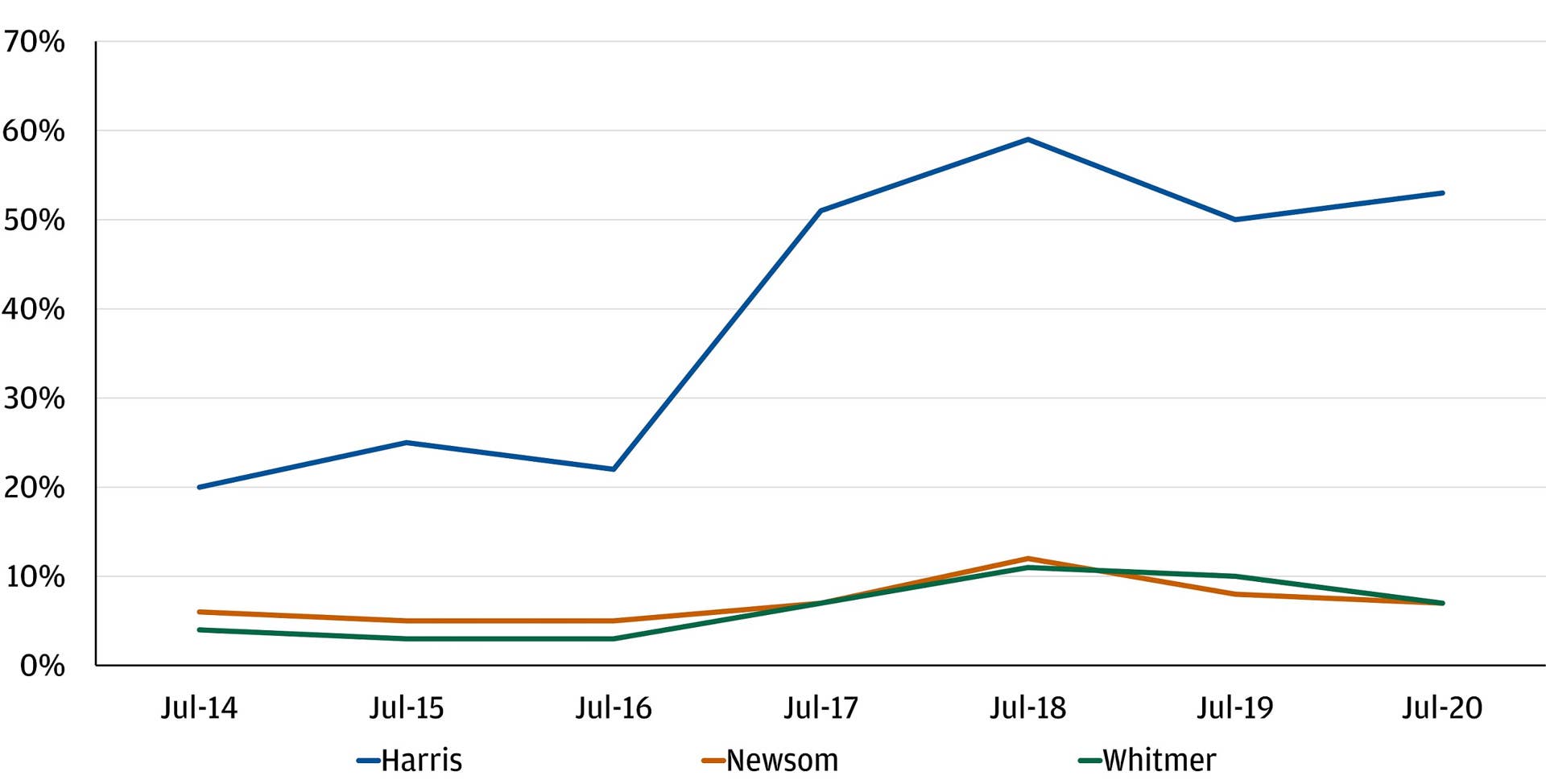

JPMorgan's take on Kamala Harris:

After weeks of growing calls from Democrats to step aside, President Biden has officially dropped out of the 2024 election. A tip of the hat to our own Michael Cembalest for introducing this possibility in our client dialogues much earlier: See his November 2023 Eye on the Market and the "Top Ten Surprises" section of his 2024 Outlook.

So, now what? While there are still a few unknowns, the possible path forward is that the Democratic National Convention to be held from August 19 to 22 will be an “open” one, meaning delegates would be legally free to vote for whomever they want. Still, prediction markets and most commentary, including President Biden’s endorsement, suggest Vice President Kamala Harris is the presumptive Democratic presidential nominee.

Implied odds to win the Democratic nomination

From a campaign and policy perspective, we don’t expect Harris’s platform to differ much from Biden’s (see the below overview). However, we do think it could make the election more competitive once again.

What does this mean for investors?

• Markets don't like uncertainty, and some of the strength in risk assets through the summer was likely due to the increased likelihood of a Republican sweep. We wouldn't be surprised to see more turbulence as the presidential race evolves.

• Focus on what stays the same. Spending on security is likely to continue no matter the outcome of the elections, which is why the resulting infrastructure build is one of our highest conviction ideas. Likewise, the national debt and deficit will likely remain on a challenging trajectory under either party, which emphasizes the need to focus on tax efficiency in portfolios.

BY Doug Kass · Jul 22, 2024, 6:25 AM EDT

Doomberg on "In Search of the Next Shale."

BY Doug Kass · Jul 22, 2024, 6:15 AM EDT

* We have no trading short rentals or Index shorts on now...

I have covered all my trading short rentals.

Position: None

BY DOUG KASS JUL 19, 2024 1:45 PM EDT

BY Doug Kass · Jul 22, 2024, 6:05 AM EDT

Wolf Street howls about "The Rotation."

BY Doug Kass · Jul 22, 2024, 5:55 AM EDT

BY Doug Kass · Jul 22, 2024, 5:45 AM EDT