Recommended Viewing

If you are invested in cannabis, I highly recommend watching Shadd Dales' interview with a leading legal expert in the field.

BY Doug Kass · Jul 10, 2024, 4:51 PM EDT

If you are invested in cannabis, I highly recommend watching Shadd Dales' interview with a leading legal expert in the field.

BY Doug Kass · Jul 10, 2024, 4:51 PM EDT

BY Doug Kass · Jul 10, 2024, 3:45 PM EDT

Wolf Street howls about home affordability.

BY Doug Kass · Jul 10, 2024, 3:35 PM EDT

* But the data doesn't matta...

BY Doug Kass · Jul 10, 2024, 3:10 PM EDT

Investors continue to chase the same heavily weighted Index stocks.

With so many sectors weak (Pharma, Energy, Consumer, etc.) why buy what some view as "value stocks" such as Disney DIS, McDonald's MCD, Nike NKE, Starbucks SBUX, etc. when Amazon AMZN, Apple AAPL, Meta META, Alphabet GOOGL, Nvidia NVDA and Microsoft MSFT rise daily?

Adding to the performance chase (in a market characterized by unprecedentedly narrow leadership) are passive products and strategies that worship at the altar of price and have no understanding or interest in value or valuation.

This sort of sums it up!

BY Doug Kass · Jul 10, 2024, 2:54 PM EDT

From Peter Boockvar:

10 yr auction was good

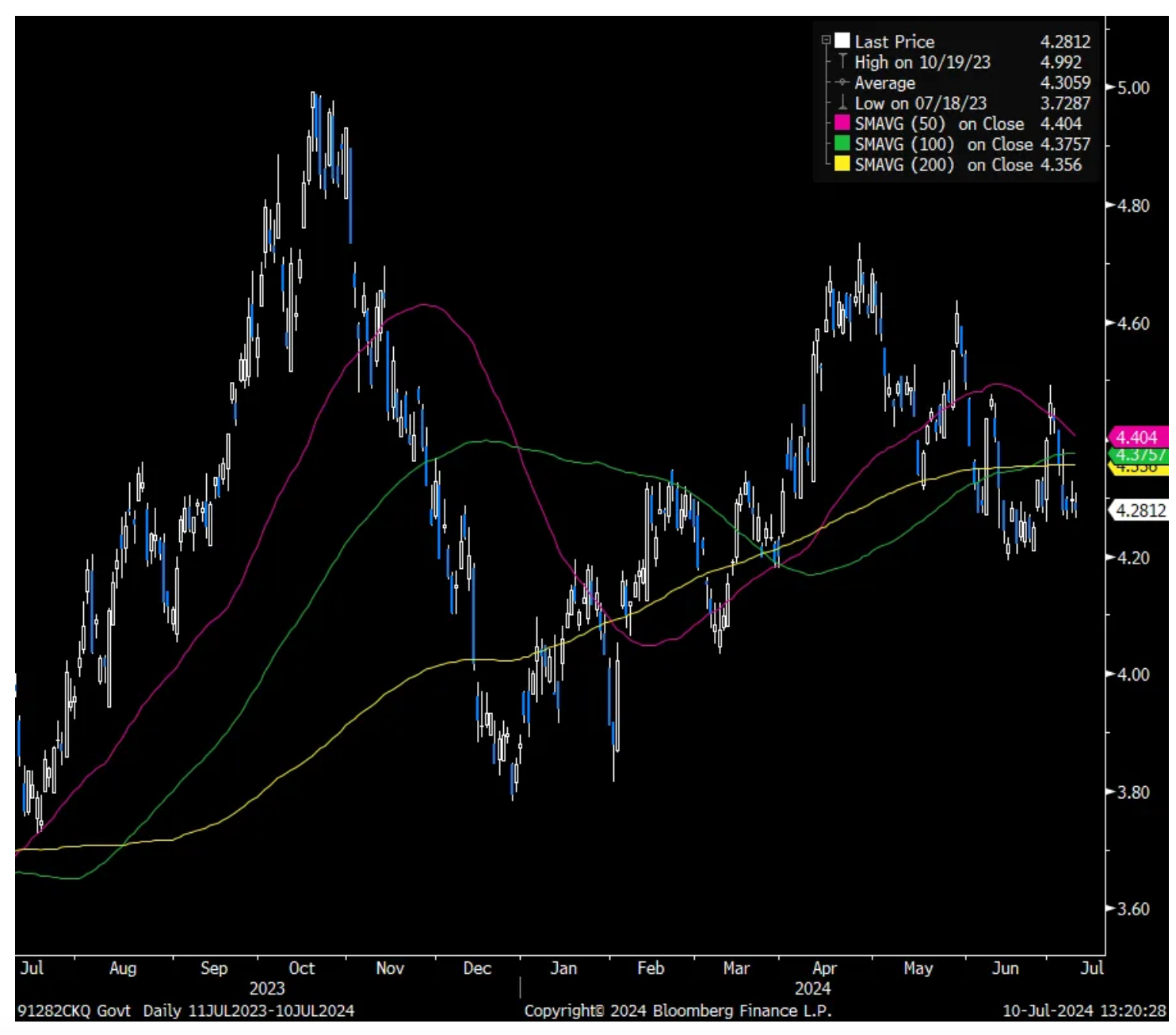

Ahead of CPI tomorrow and post Powell, the 10 yr note auction was pretty good. The yield of 4.276% was 1 bp below the when issued pricing. Also, the bid to cover of 2.58 was just above the one year average 2.52. Also, direct and indirect bidders took 88.5% of the auction which is similar to the June auction but the most since last August.

Bottom line, today’s good auction follows a good one yesterday and a few solid ones seen a few weeks ago. The focus I believe in terms of buyer attitudes is the shift in focus to the slowing economic data and growing belief that the Fed will cut rates in September with rate cut odds up to 80%. At least for now, debt and deficit worries are taking a back seat in terms of supply/demand concerns. The irony here is that if the economy continues to slow, tax receipts falter and assuming deficit spending continues on, the supply/demand imbalances get even worse.

10 yr Yield

BY Doug Kass · Jul 10, 2024, 1:45 PM EDT

Bond Market Update

* The data doesnt matta...

There is nothing in the fixed-income market to account for the continued rip higher in equities:

* The yield on the 2-year Treasury is flat.

* The yield on the 10-year Treasury is -1 basis point.

* The yield on the long bond is -2 basis points.

BY Doug Kass · Jul 10, 2024, 1:23 PM EDT

BY Doug Kass · Jul 10, 2024, 1:10 PM EDT

Viking Therapeutics VKTX is +$4 today and I have just eliminated my position at about $58/share.

I will revisit in a correction.

BY Doug Kass · Jul 10, 2024, 12:40 PM EDT

The unrelenting advance is a marvel to behold.

That advance to new highs is feeding upon itself.

BY Doug Kass · Jul 10, 2024, 12:30 PM EDT

From Peter Boockvar:

Finally a question on the size of the Fed's balance sheet

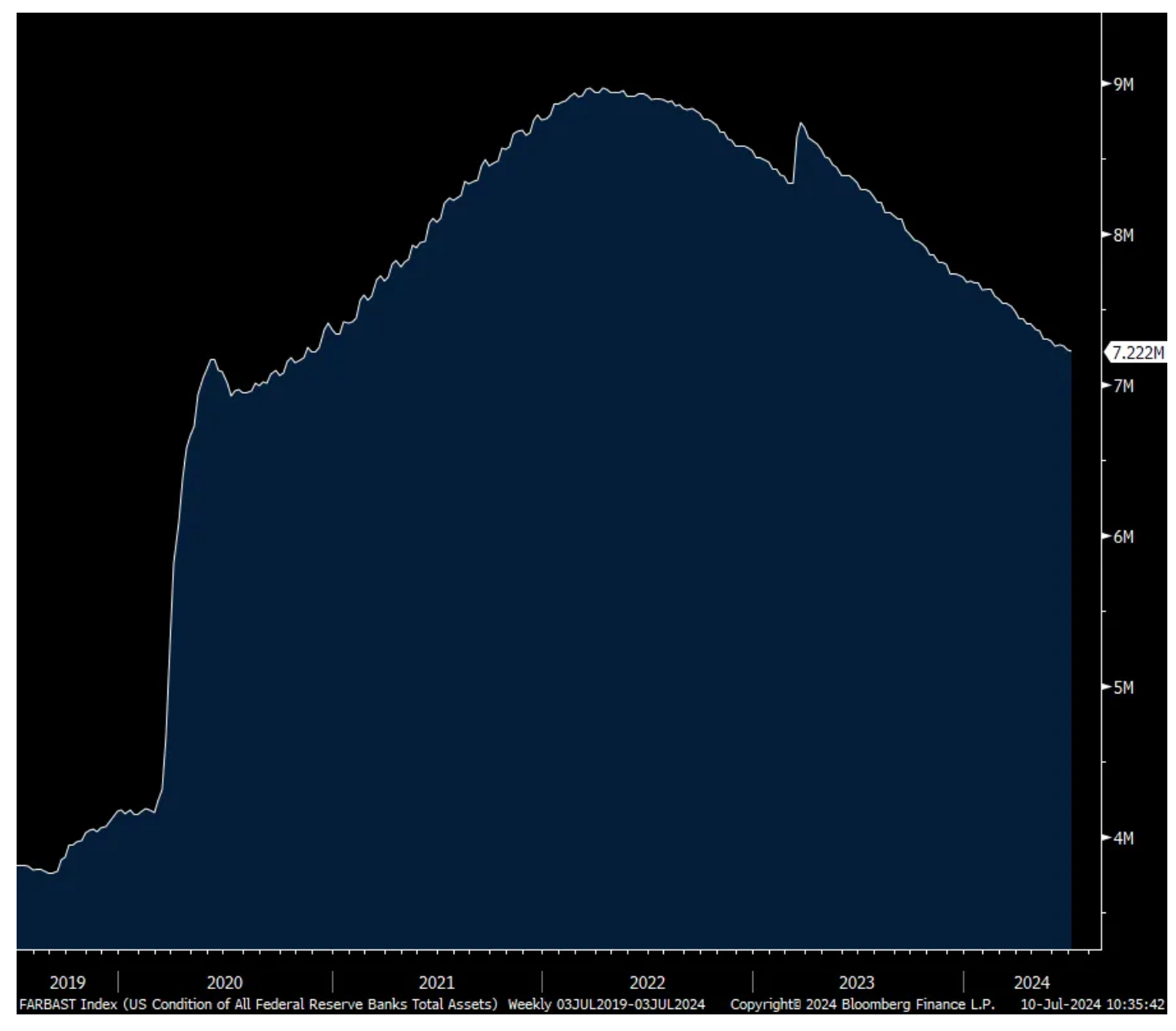

Early on today and unlike yesterday, Jay Powell was asked about the Fed’s balance sheet and he said they have a “good ways to go” in shrinking it “and going slower will allow us to go further.” The balance sheet currently stands at about $7.2 trillion, down from almost $9 trillion but still up from around $4 trillion before Covid. Where it eventually ends up at? He didn’t say today but as Powell has said before, they’ll know it when they see it.

Fed’s Balance Sheet

BY Doug Kass · Jul 10, 2024, 11:52 AM EDT

BY Doug Kass · Jul 10, 2024, 11:32 AM EDT

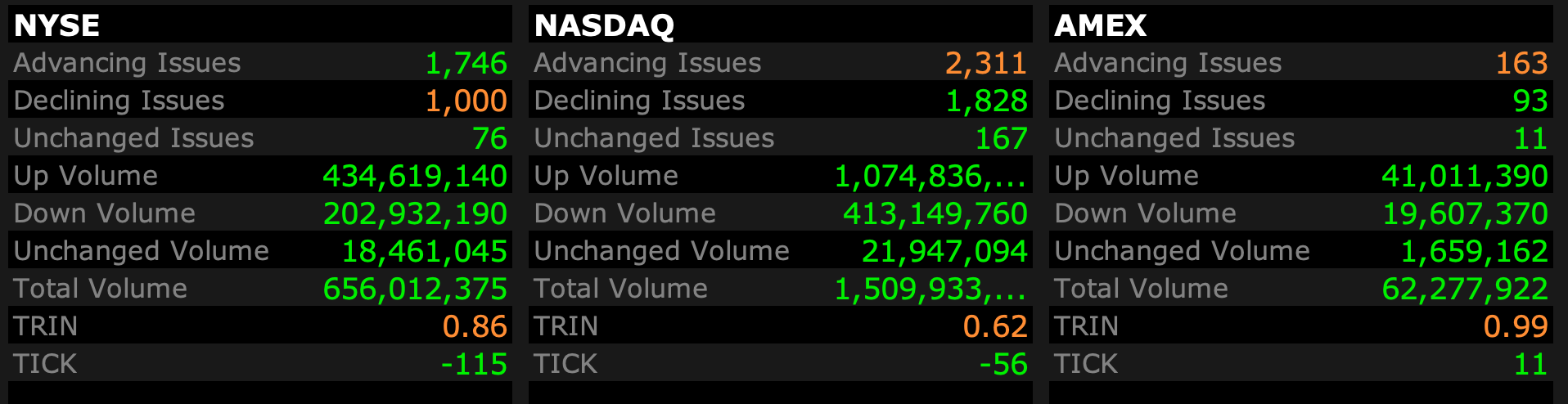

Breadth improved this morning:

BY Doug Kass · Jul 10, 2024, 11:18 AM EDT

Housekeeping items:

I am covering more CHGG and RILY.

BY Doug Kass · Jul 10, 2024, 10:33 AM EDT

With the rescheduling comments period ending in 12 days (and a likely rescheduling announcement in August) I am super sizing my MSOS position on the recent weakness.

BY Doug Kass · Jul 10, 2024, 10:13 AM EDT

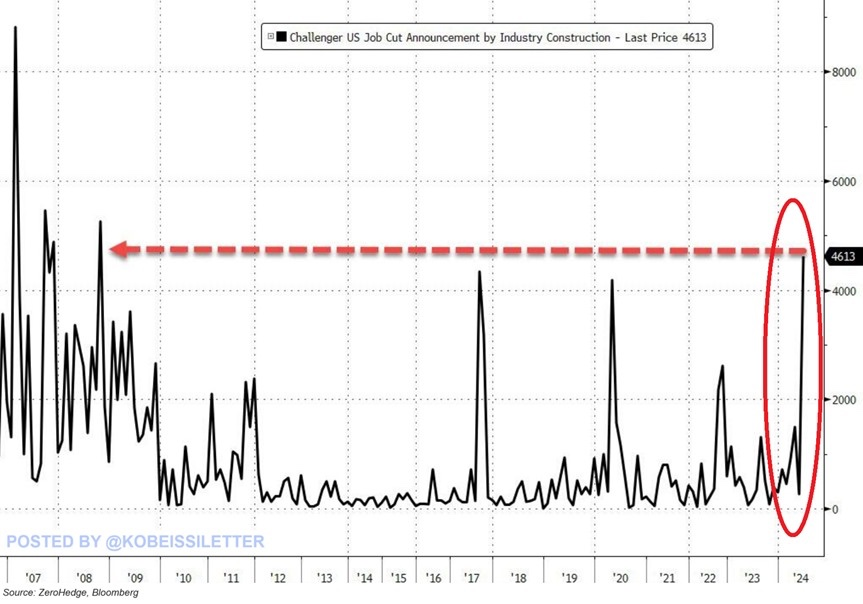

The construction industry had 4,613 layoffs last month - that the most since The Great Recession and higher than the layoffs during Covid:

BY Doug Kass · Jul 10, 2024, 10:00 AM EDT

From Peter Boockvar:

Another reminder of the stretched consumer/Other stuff

Jay Powell specifically said yesterday in response to a question from Louisiana Senator Kennedy that he is currently giving no guidance as to when they might cut. That likely takes any potential for new news today off the table when he presents to the House. One thing we didn't hear anything about yesterday was color on the Fed's balance sheet and where it might end up in size when QT ends.

As if we needed any new reminder on the stretched condition of many US consumers, we heard from Helen of Troy yesterday whose business is about 50% 'home and outdoor' with brands like Hydro Flask, Osprey and Oxo and the other half 'health and wellness' making products under the brands Braun, Curlsmith, drybar, Vicks and Revlon. Their products of hair dryers, curling irons, shavers, brushes, combs, mirrors, etc... are sold in all the major retailers, warehouse clubs, grocery, dollar and drug stores.

Its stock fell 28% yesterday in response to earnings and they said this:

"As has been widely reported, the macro environment and the health of consumers and retailers has worsened. Consumers are even more financially stretched and are even further prioritizing essentials over discretionary items. Specific to our business, we have seen some areas become more challenged over the last three months. For example, an unexpected slowdown in the global outdoor category impacted sales of our packs and accessories. There was also more pressure in the specialty beauty channel and mass beauty overall, especially in beauty tools under $100. Also, more discretionary household items like dry food storage continue to trend down."

Also, "We've heard broadly from mass retail that traffic overall is slower throughout the country and promotional pressure is increasing. In reaction to these dynamics, retailers are managing inventories more closely to account for the slowdown, and some are implementing new systems to allow for just in time inventory management. All of this exposes us to more volatility and less visibility into order volumes and timing."

I'm sorry but this is nothing but consumer recessionary type language. Again, I believe the Fed will be cutting rates in September. That said, the days of zero rates are over and the Fed's ability to respond to economic downturns is much more limited this time around because of the inflationary possibilities again if they do too much.

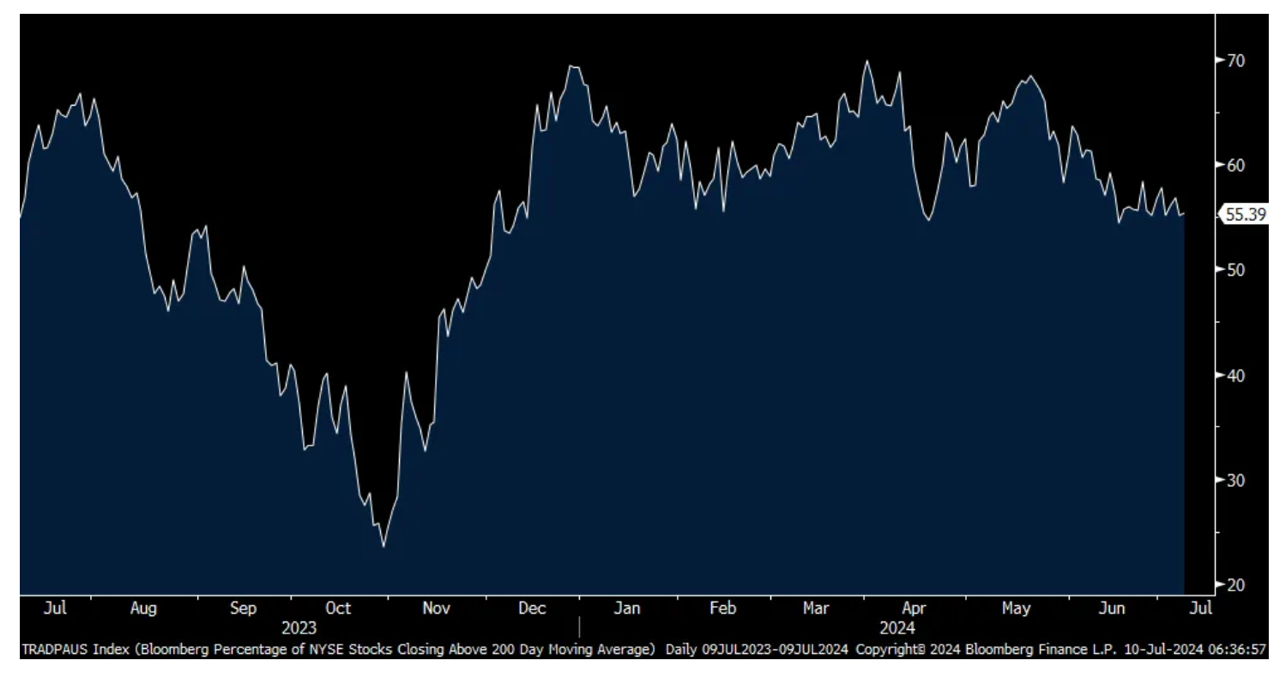

I'm showing a chart again of the S&P 500 percentage increase over its 200 day moving average of 14.2% at the same time the number of stocks on the NYSE that are trading above its 200 day moving average is a whisper from the least amount since December 2023.

% of NYSE Stocks Closing Above its 200 Day Moving Average

Manheim yesterday said its June wholesale used car index fell .6% m/o/m and are down 9% y/o/y. It's tough to say how much of the CDK software issue impacted this.

Manheim said "Wholesale value declines have been stronger than we normally see for much of the last two months. However, even though much of the industry was feeling the retail sales disruptions caused by the CDK outages in the latter part of the month, Manheim started to see wholesale price declines decelerate, ending the month at a seasonally normal pace. Sales conversion is currently running several points above the previous three years, including 2021, indicating that buyer demand is relatively strong despite all the uncertainty in the market." We wonder though how much of the used car sales lift was because of the software trouble negatively impacting the sale of new cars.

The Reserve Bank of New Zealand kept its benchmark rate unchanged at 5.5% as expected but the language in their statement reflects an easing bias, though not anytime soon. "The Committee agreed that monetary policy will need to remain restrictive. The extent of this restraint will be tempered over time consistent with the expected decline in inflation pressures."

In China, its CPI in June rose .2% y/o/y which was below the estimate of up .4% but ex food and energy remained stable, rising by .6% y/o/y for the 3rd month in the past 4. Lower food prices continue to keep a lid on overall consumer prices. As the Chinese consumer is more selective, low inflation for them is a good thing. Nothing market moving here.

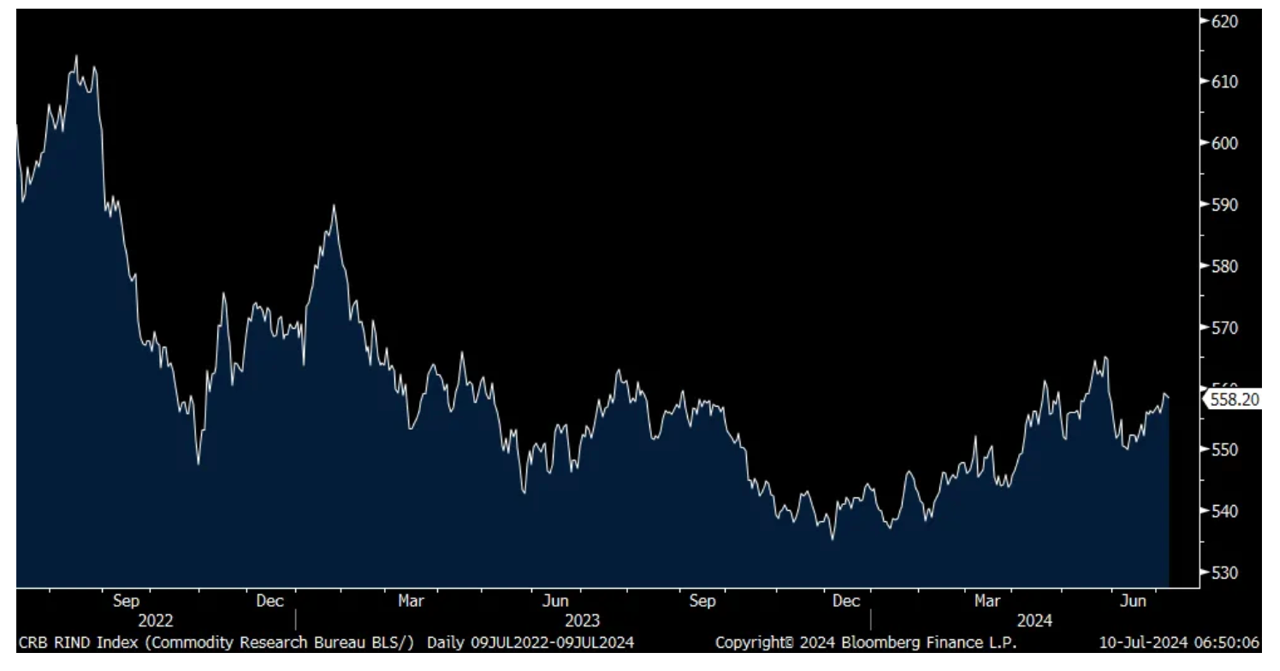

PPI fell .8% m/o/m as forecasted and a slower pace of decline from the 1.4% drop in May. It's also the least negative since December 2022 with easy comps being a big reason as PPI fell 5.4% in June 2023. The CRB raw industrials index remains well off its highs of a few years ago but is still only 7 pts from the highest since February 2023.

CRB Raw Industrials Index

BY Doug Kass · Jul 10, 2024, 9:50 AM EDT

A notable downgrade:

Visa downgraded to Neutral at BofA on limited valuation upside

BofA analyst Jason Kupferberg downgraded Visa (V) to Neutral from Buy with a price target of $297, down from $305. While the firm maintains a favorable view on Visa and MasterCard's (MA) "premier" business model and competitive moat, it is making a non-consensus call and downgrading both as it sees limited upside potential to the valuation multiple and estimates, while also noting that investor positioning remains crowded. While the firm said the rating change "is not a call on the quarter," as it sees calendar Q2 estimates as achievable amid generally stable overall consumer spending, it notes that both continue to have second half acceleration embedded in guidance and the firm struggles to see material upside to near-term estimates.

BY Doug Kass · Jul 10, 2024, 9:30 AM EDT

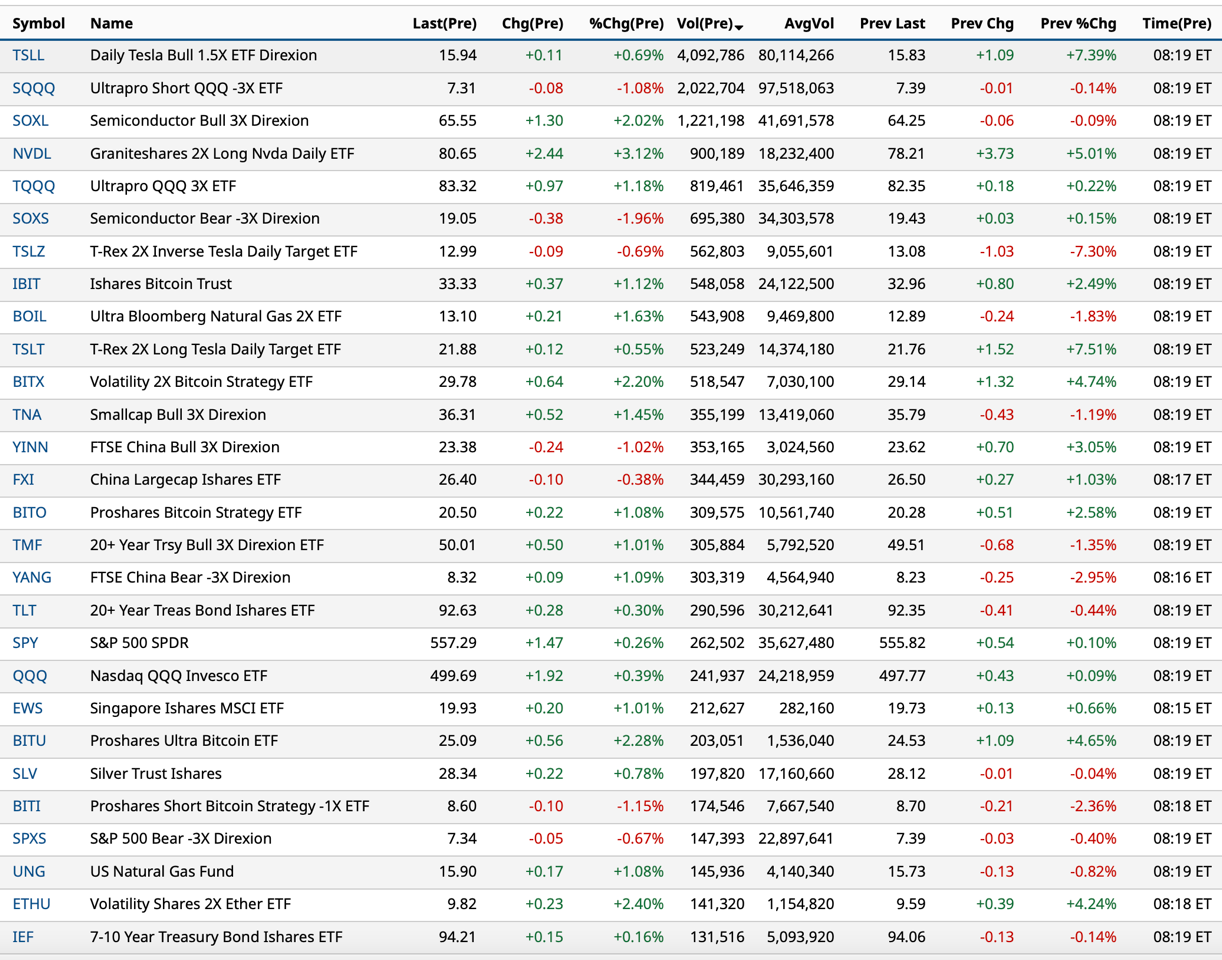

Most active pre-market exchange-traded funds as of 8:19 a.m.

BY Doug Kass · Jul 10, 2024, 9:22 AM EDT

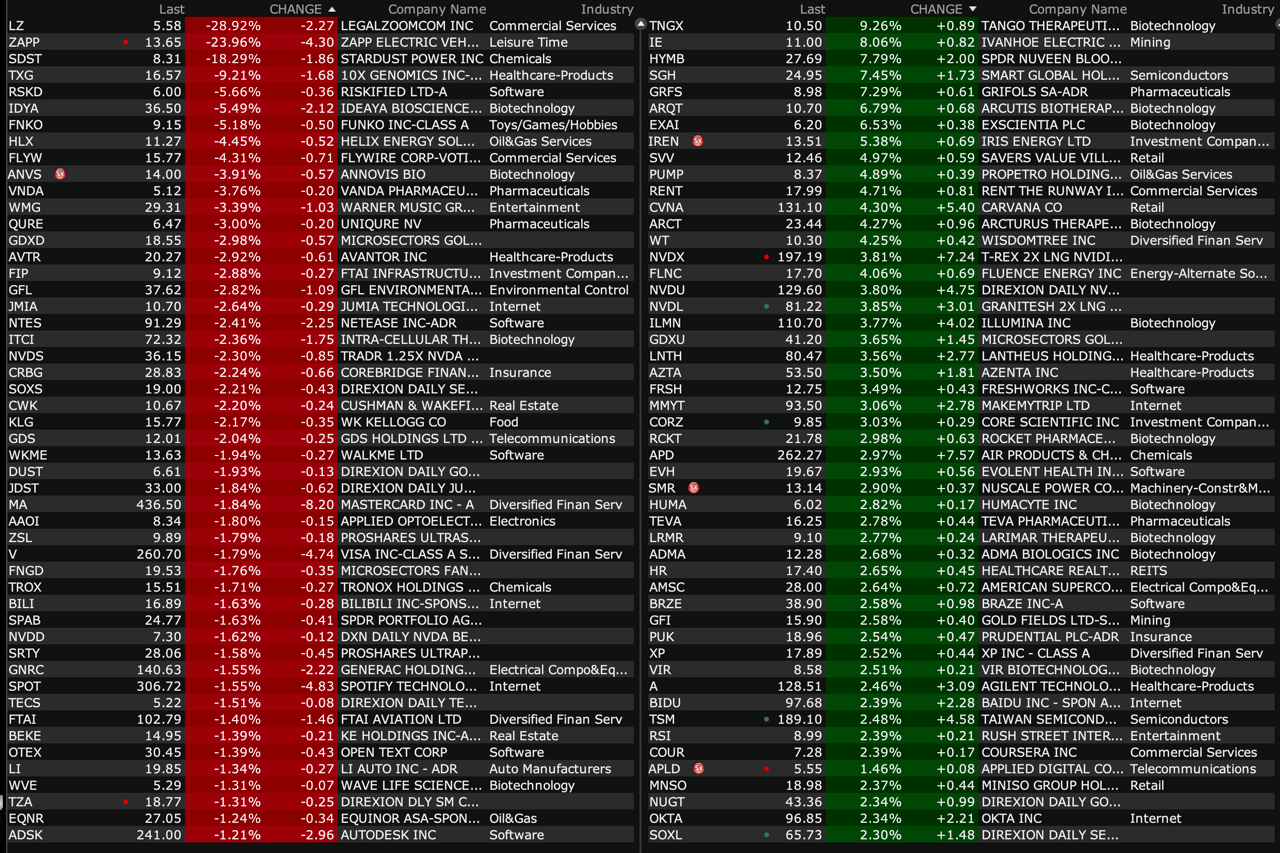

Here is a chart of the big movers, by percentage:

BY Doug Kass · Jul 10, 2024, 9:16 AM EDT

Here are U.S. select premarket movers as of 8:26 a.m. ET:

-VRPX +37% (continue to target end of year Probudur IND filing; announces results for a Swine Model pilot study for Probudur, long-acting liposomal bupivacaine formulation, injected at a wound site to provide both immediate and extended pain relief)

-LGVN +22% (US FDA Grants Lomecel-B Regenerative Medicine Advanced Therapy (RMAT) Designation for the Treatment of Mild Alzheimer’s Disease)

-AEHR +17% (earnings, guidance)

-PRZO +13% (received ASTM F3322-22 Standard Approval According to FAA New Regulations Allowing Flight Operation Over People)

-FRSX +11% (enters into Agreement with BuilderX Robotics to Enhance Autonomous Heavy Machinery Operations)

-ICCC +8.9% (reports prelim Q2 revenue)

-AMLX +8.5% (announces acquisition of Phase 3-ready GLP-1 Receptor Antagonist (Avexitide) with FDA Breakthrough Therapy Designation)

-SGH +7.6% (earnings, guidance)

-IREN +5.9% (Bernstein Initiates IREN with Outperform, price target: $26)

-OGEN +4.7% (improves ONP-002, intranasal drug formulation, for treating concussed patients)

-CORZ +4.4% (Bernstein Initiates CORZ with Outperform, price target: $17)

-GAME +4.4% (earnings, guidance)

-FLNC +4.0% (Truist Initiates FLNC with Buy, price target: $25)

-CVNA +3.8% (launches Streamlined Shopping and Checkout Experience for Used EV Buyers)

-HZO +3.8% (Island Capital Group LLC Issues Open Letter to Shareholders of MarineMax, Inc.)

-ILMN +3.7% (acquires developer of an emerging and highly differentiated single-cell technology Fluent BioSciences)

-ARQT +3.3% (US FDA approves ZORYVE (roflumilast) Cream 0.15% for treatment of Atopic Dermatitis in Adults and Children Down to 6 Years of Age)

-BIDU +3.2% (recent notable strength in Hong Kong being attributed to alleged signs of growing popularity for its Apollo Go robotaxi in China)

-SAR +3.1% (earnings)

-APD +3.0% (Honeywell confirms to acquire Air Products' LNG process technology and equipment business for $1.81B all-cash)

-A +2.5% (CitiGroup Raised A to Buy from Neutral, price target: $150)

-TSM +2.4% (earnings)

-BHF +1.9% (Jefferies Raised BHF to Buy from Hold, price target: $54 from $49)

-LZ -29% (current Board Chair Jeffrey Stibel named new CEO, effective immediately; cuts FY24 guidance)

-TXG -11% (ILMN acquires developer of an emerging and highly differentiated single-cell technology Fluent BioSciences)

-RSKD -5.7% (Goldman Sachs Cuts RSKD to Sell from Neutral, price target: $6)

-HPP -4.3% (Morgan Stanley Cuts HPP to Underweight from Equal Weight, price target: $4.25)

-KRUS -4.0% (earnings, guidance)

-IDYA -3.9% (prices 7.2M shares at $35/share)

-PET -3.2% (earnings, guidance)

-AVTR -2.6% (CitiGroup Cuts AVTR to Neutral from Buy, price target: $23)

BY Doug Kass · Jul 10, 2024, 9:07 AM EDT

10 a.m.: Fed Chair Jerome Powell delivers semi-annual monetary policy testimony before the House Financial Services Committee;

2:30 p.m.: Fed Bank of Chicago President Austan Dean Goolsbee (Non-Voter) and Federal Reserve Board Governor Michelle Bowman (Voter) gives opening remarks before virtual event, "FedListens: Exploring Challenges Facing the Childcare Industry, Working Parents, and Employers," Chicago, IL (Livestream available. No embargoed text);

7:30 p.m.: Fed Board Governor Lisa Cook (Voter) speaks on "Global Inflation and Monetary Policy Challenges" before the 2024 Australian Conference of Economists, Adelaide, South Australia 9Text available. Q&A from moderator. Webcast at https://www.youtube.com/@ACE_2024_Adelaide)

BY Doug Kass · Jul 10, 2024, 8:50 AM EDT

From my pal Peter Boockvar:

As if we needed any new reminder on the stretched condition of many US consumers, we heard from Helen of Troy yesterday whose business is about 50% 'home and outdoor' with brands like Hydro Flask, Osprey and Oxo and the other half 'health and wellness' making products under the brands Braun, Curlsmith, drybar, Vicks and Revlon. Their products of hair dryers, curling irons, shavers, brushes, combs, mirrors, etc... are sold in all the major retailers, warehouse clubs, grocery, dollar and drug stores.

Its stock fell 28% yesterday in response to earnings and they said this:

"As has been widely reported, the macro environment and the health of consumers and retailers has worsened. Consumers are even more financially stretched and are even further prioritizing essentials over discretionary items. Specific to our business, we have seen some areas become more challenged over the last three months. For example, an unexpected slowdown in the global outdoor category impacted sales of our packs and accessories. There was also more pressure in the specialty beauty channel and mass beauty overall, especially in beauty tools under $100. Also, more discretionary household items like dry food storage continue to trend down."

Also, "We've heard broadly from mass retail that traffic overall is slower throughout the country and promotional pressure is increasing. In reaction to these dynamics, retailers are managing inventories more closely to account for the slowdown, and some are implementing new systems to allow for just in time inventory management. All of this exposes us to more volatility and less visibility into order volumes and timing."

BY Doug Kass · Jul 10, 2024, 8:40 AM EDT

* The advance decline line has not made a high since Mid-May

* Only 32/500 S&P stocks made a high in yesterday's session

Equities continued their multi-day advance on Tuesday.

Despite some midday weakness, this occurred despite (again!) weak breadth, higher interest rates and more narrowing of leadership TheStreet Pro :

Technology (same old, same old!) came out victorious as bank stocks (perhaps the only value sector working) was stellar.

Little discussed was transports (which, unlike tech, are GDP correlated). Though the price of oil has declined, transports got schmeissed - down by -1.1% on the trading session (after falling by -0.8%) on Monday. Transports are now down by over 10% from the cycle high.

Confusing at best.

BY Doug Kass · Jul 10, 2024, 8:15 AM EDT

This is a valuable chart for momentum-based short term traders:

BY Doug Kass · Jul 10, 2024, 8:00 AM EDT

From JPMorgan:

US: Futs are up small with both Tech and small-caps outperforming following another ATH fueled by dovish Powell comments. Pre-mkt, Semis are higher as TSMC sales beat expectations, +40% vs. +35.5% consensus. All of the Mag7 are higher, and several Large-Cap Banks are higher, too. Bond yields are flat to -1bp and USD starts the day flat. Cmdtys are weaker but there is some relief in the Energy complex with both crude/natgas higher. Yesterday’s 3Y auction showed surprising strength, keep an eye on today’s 10Y auction, amid 4x Fedspeakers, where Jay Barry sees a concession as necessary for digestion. We may see another low volume session ahead of tmrw’s CPI release; the market is pricing Sep and Dec rate cuts so an inline print keeps that on track.

and...

EQUITY AND MACRO NARRATIVE: Tomorrow kicks off both earnings season and potentially the last meaningful CPI print of this cycle. The former should give some insight into the growth outlook and the potential for a broadening of the rally and the latter on the start, and potentially magnitude, of the beginning of the monetary easing cycle. Below is an earnings preview, Feroli’s thoughts on Powell, Trading Desk comments, and a re-post of the CPI scenario analysis.

BY Doug Kass · Jul 10, 2024, 7:45 AM EDT

The S&P Short Range Oscillator has moved from a less overbought - to 0.6% from 2.16%.

BY Doug Kass · Jul 10, 2024, 7:35 AM EDT

BY Doug Kass · Jul 10, 2024, 7:25 AM EDT

BY Doug Kass · Jul 10, 2024, 7:11 AM EDT

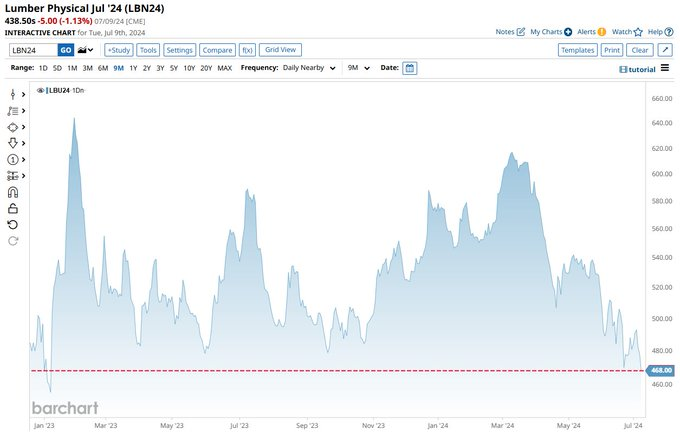

Lumber prices:

BY Doug Kass · Jul 10, 2024, 6:58 AM EDT

BY Doug Kass · Jul 10, 2024, 6:45 AM EDT

"Fortunes are made every year by those who take the time to learn to interpret charts properly."

- William J. O'Neil

Bonus — Here are some great links:

BY Doug Kass · Jul 10, 2024, 6:35 AM EDT

JPMorgan lowers the price targets on two consumer stocks — McDonald's MCD and Starbucks SBUX.

BY Doug Kass · Jul 10, 2024, 6:25 AM EDT

BY Doug Kass · Jul 10, 2024, 6:17 AM EDT

BY Doug Kass · Jul 10, 2024, 6:09 AM EDT

Wolf Street howls about residential real estate.

BY Doug Kass · Jul 10, 2024, 5:55 AM EDT

BY Doug Kass · Jul 10, 2024, 5:45 AM EDT