Bezos Rings the Register

BY Doug Kass · Jul 3, 2024, 11:35 AM EDT

BY Doug Kass · Jul 3, 2024, 11:35 AM EDT

I am covering some more B. Riley RILY at $16.66.

BY Doug Kass · Jul 3, 2024, 11:25 AM EDT

* My opener highlighted my diminished expectations for U.S. economic growth...

In support. From Bramo:

BY Doug Kass · Jul 3, 2024, 11:10 AM EDT

As you all are aware I have been bearish on Disney DIS for almost five years.

I initiated a Disney long under $98 this morning.

I don't think my entry point will prove ideal but I plan to be a scale buyer on weakness.

More early next week.

BY Doug Kass · Jul 3, 2024, 10:56 AM EDT

I will be leaving about an hour before the close (1 p.m.) to do some family stuff.

BY Doug Kass · Jul 3, 2024, 10:35 AM EDT

BY Doug Kass · Jul 3, 2024, 10:25 AM EDT

Adding to MSOS calls (in the money for July).

BY Doug Kass · Jul 3, 2024, 10:10 AM EDT

From "Meet" Bret Jensen:

Bret Jensen/STAFF

37 minutes ago

The biggest thing for me as investor has little to do with politics, because there is no one in either party that will do what needs to be done to get the country on a fiscally sustainable path.

The market trades at 22 times forward earnings on the S&P when the yield on short term treasuries is north of 5.3%. Deficit spending is at 6.7% of GDP based on latest CBO projection and GDP growth is looking to be around 1.5% in the first half of 2024. We could probably get much better GDP growth by just dropping money out of helicopters. Market breadth is in the same territory or worse than before the 1974 and 2000 crashes. CRE continues to deteriorate, the consumer is beyond tapped, Ukraine is not 'winning', and it is likely tensions in the Middle East rise further. This isn't going to end well. The only question is whether the market recognizes this at some point in 2024 or whether the curtain comes down in 2025. JMTC

BY Doug Kass · Jul 3, 2024, 9:59 AM EDT

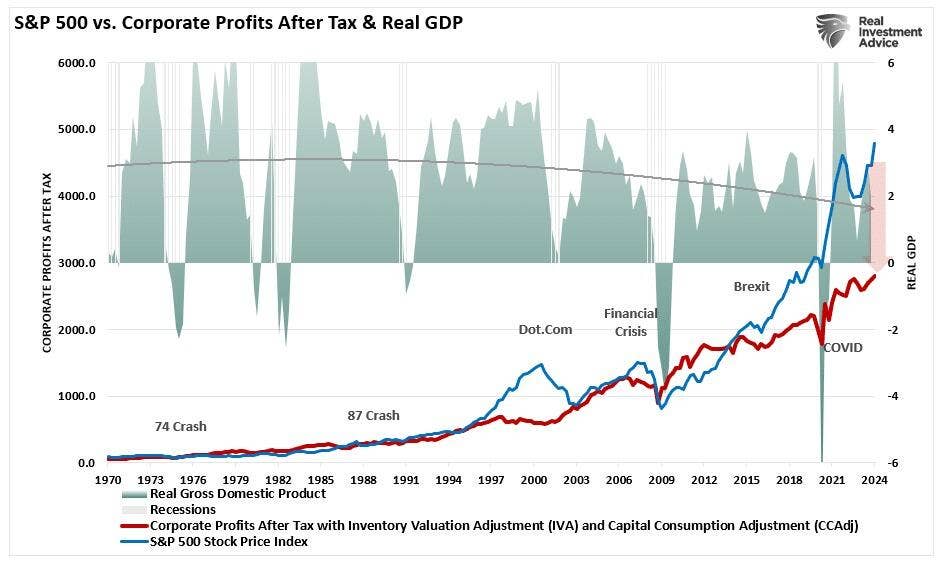

* Optimism surrounding corporate profit growth in 2024-2025 form the foundation of many bullish stock market forecasts.

* But over the last quarter, this year's consensus S&P EPS for the full year of 2024 has fallen by $5/share - for next year profit projections have recently dropped by $9/share.

I seriously question the optimistic U.S. corporate profits projections that many strategists now use to rationalize today's elevated stock prices.

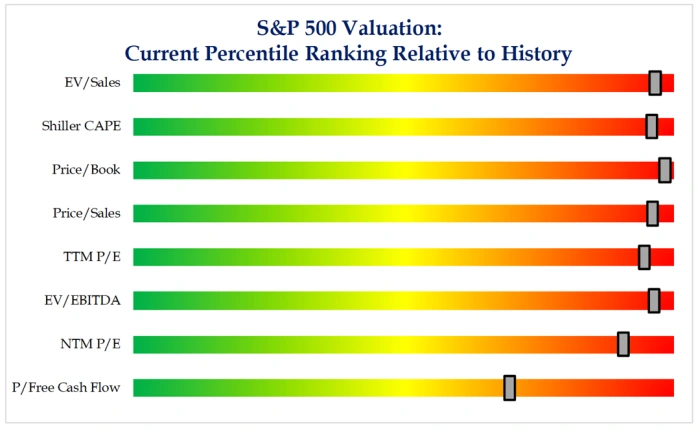

Importantly (and as noted in yesterday's Diary), a too optimistic/misguided profits outlook comes at a time in which most traditional valuation metrics are in the 90%+ tile:

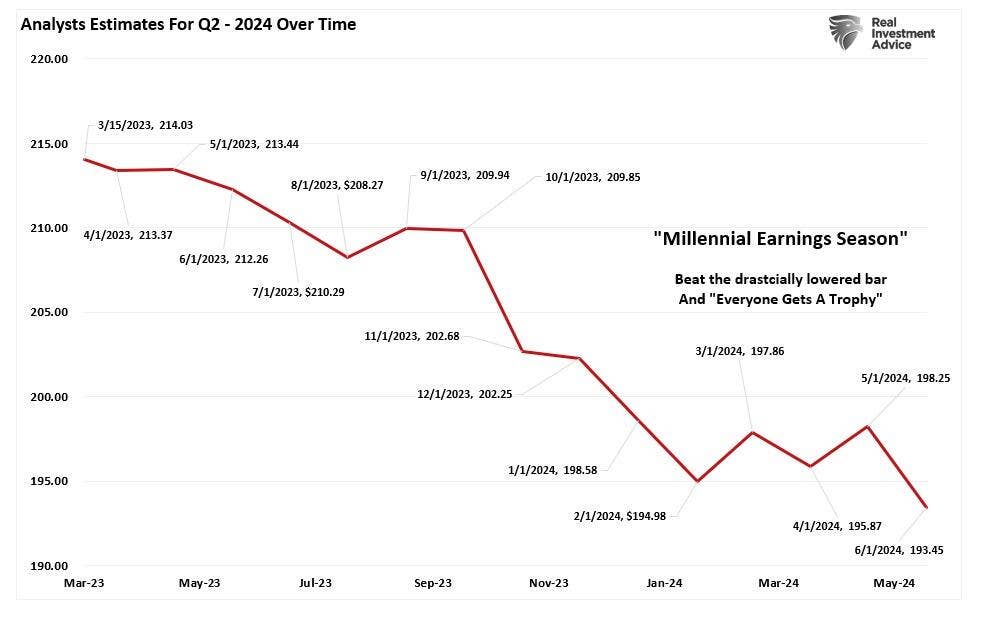

To begin with, the second-quarter 2024 forecasts have been consistently lowered over the last three months. During the last month second quarter 2024 S&P 500 profits forecasts have been reduced by about $5/share :

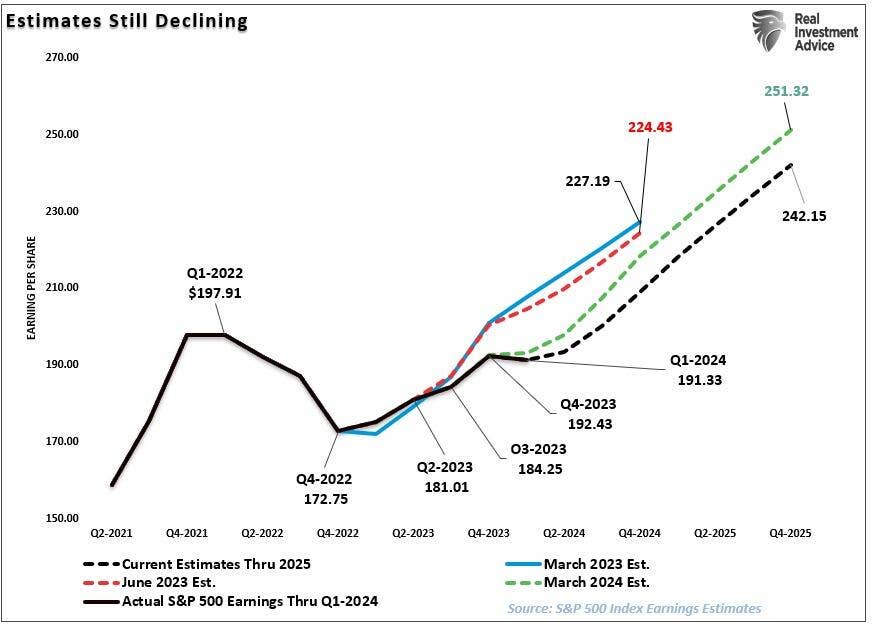

Meanwhile full-year 2025 S&P EPS forecasts have been lowered by $9/share:

Why Are Strategists So Optimistic Given the Backdrop of Interest Rates and Inflation?

Equity prices generally (and over long period of time) tend to track economic growth and earnings. Over the last 7-8 decades the economy has expanded by a 6.4% growth rate, EPS have compounded by 7.7% annually and stock prices have risen by 9.3%/year.

Most strategists are expecting about a 10% rise in S&P profits in 2024 and near 15% again next year.

How is this possible given the following backdrop?

* The economic bounce back from Covid is over. GDP Now is forecasting a moderating growth in GDP - reducing 2Q Real GDP to 1.7%(e) vs. the prior forecast of +2.2%(e). GDPNow - Federal Reserve Bank of Atlanta (atlantafed.org)

* Inflation remains prickly. Expectations of six rate cuts (as recently as five months ago) has been reduced to one to two cuts.

* Inflation has dropped dramatically to around 2.5%-3.0%. With economic growth decelerating and inventories no longer scarce, companies have likely far less pricing power today than at any point in the last two to three years.

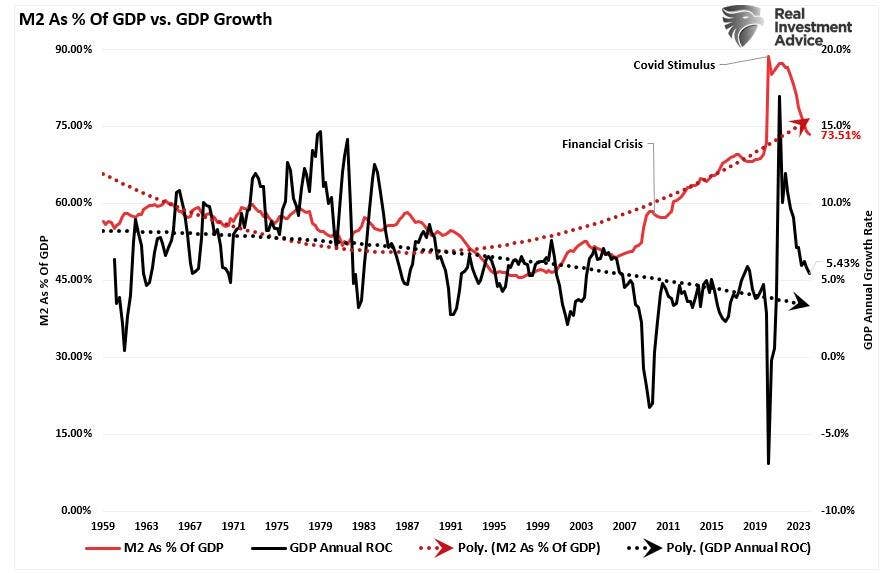

* The surge in liquidity/money supply is over:

From ZeroHedge:

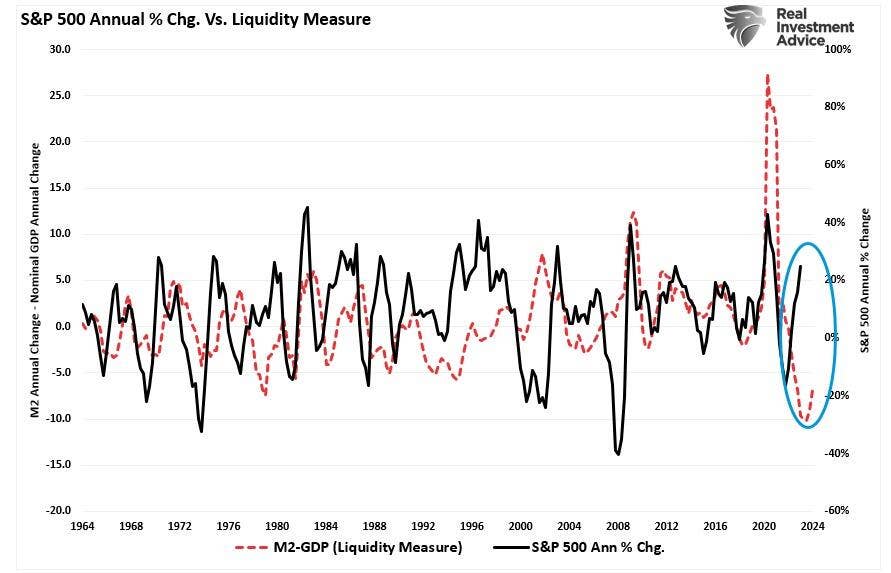

While the media often states that “stocks are not the economy,” as noted, economic activity creates corporate revenues and earnings. As such, stocks can not grow faster than the economy over long periods. A decent correlation exists between the expansion and contraction of M2 less GDP growth (a measure of liquidity excess) and the annual rate of change in the S&P 500 index. Currently, the deviation seems unsustainable. More notably, the current percentage annual change in the S&P 500 is approaching levels that have preceded a reversal of that growth rate.

So, either the annualized rate of return from the S&P 500 will decline due to repricing the market for lower-than-expected earnings growth rates, or the liquidity measure is about to turn sharply higher.

* Not only won't monetary policy stimulate much growth, but (out of hand) fiscal policy will not be as stimulative over the next 18 months as in the past several years.

* Though currently ignored by authorities and investors, the U.S. deficit and debt load is out of hand and must be addressed. Former President Trump's tax cuts expire next year. More tax cuts will be inflationary, lowering growth. Should the incumbent prevail, tax increases are likely - this will also dampen economic growth.

* Following the pandemic, consumption has been pulled forward. The consumer has reduced/eliminated excess savings and has taken on loads of debt - the consumer is now spent up not pent up.

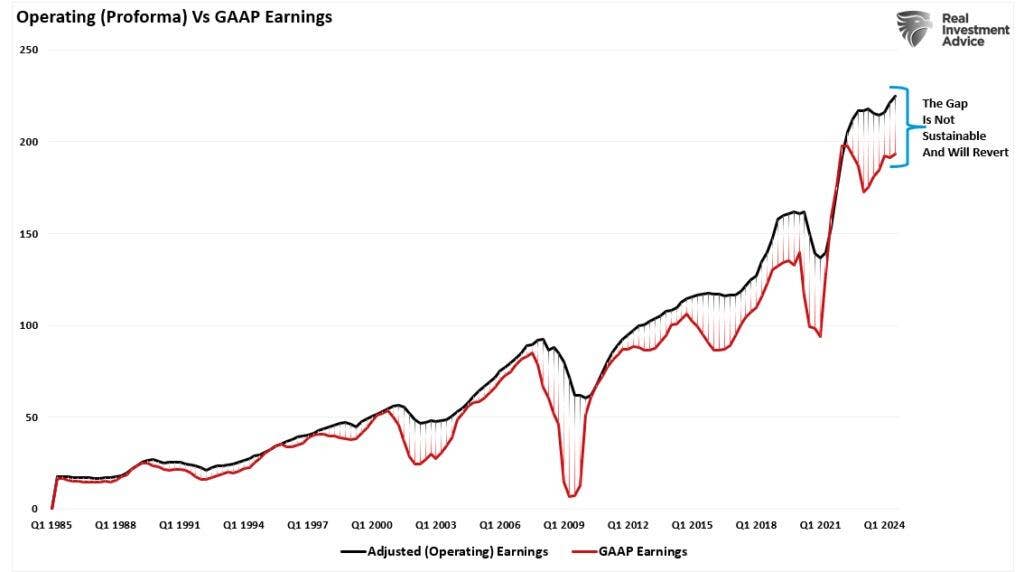

* The quality of earnings remains suspect. Again from ZeroHedge:

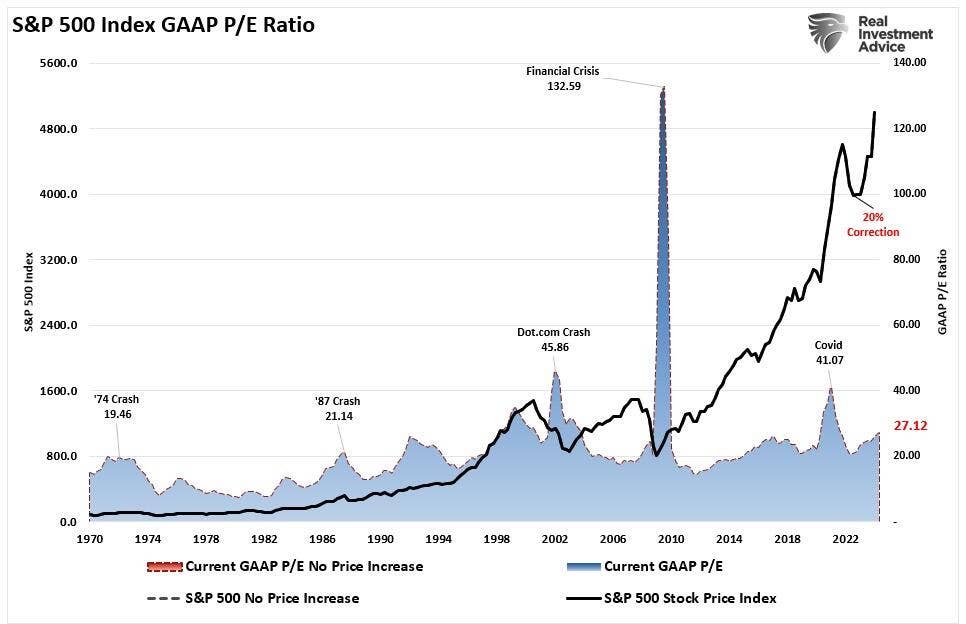

Most companies report “operating” earnings, which obfuscate profitability by excluding all the “bad stuff.” A significant divergence exists between operating (or adjusted) and GAAP earnings. When such a wide gap exists, you must question the “quality” of those earnings.

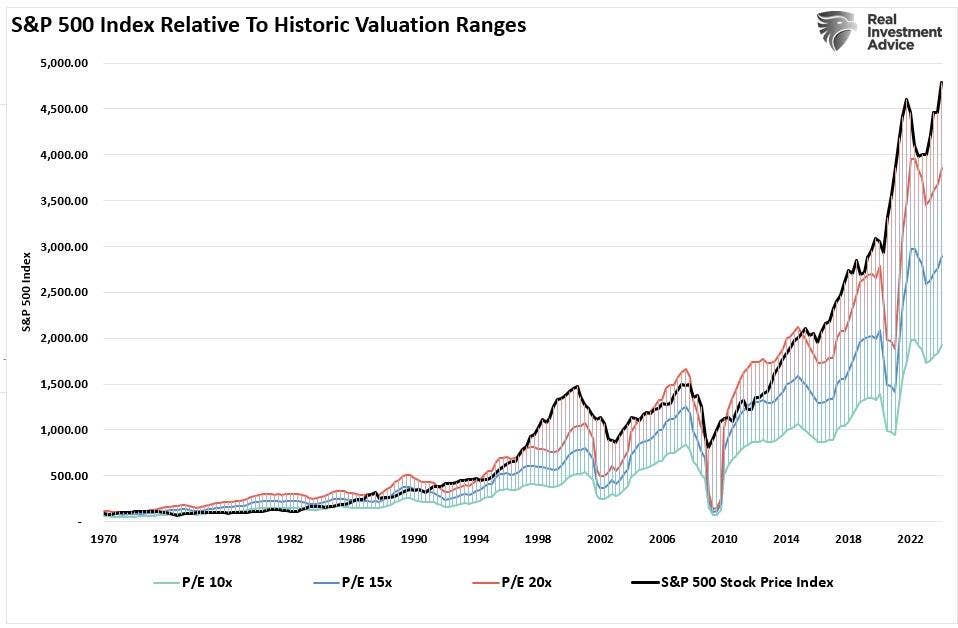

The chart below uses GAAP earnings. If we assume current earnings are correct, then such leaves the market trading above 27-times earnings. (That valuation level remains near previous bull market peak valuations.)

I could go on!

BY Doug Kass · Jul 3, 2024, 9:29 AM EDT

And they (the bearish strategists) are all gone:

BY Doug Kass · Jul 3, 2024, 8:59 AM EDT

And my Tweet on the same subject:

BY Doug Kass · Jul 3, 2024, 8:56 AM EDT

Walgreens Boots Alliance WBA price target lowered to $12 from $17 at UBS 05:33 UBS analyst Kevin Caliendo lowered the firm's price target on Walgreens Boots Alliance to $12 from $17 and keeps a Neutral rating on the shares. The fiscal Q3 results underscored that pharmacy and front end gross margin pressures remain constant for Walgreens, and that there is little visibility into when core pharmacy fundamentals will stabilize, the analyst tells investors in a research note. The firm says it has enough concern over the long-term viability of the business that it considers near-term adjusted earnings and adjusted EBITDA less relevant. UBS believes Walgreens' valuation multiples only explain the current price, but do not suggest whether the stock is "cheap" or "expensive" versus historical ranges.

BY Doug Kass · Jul 3, 2024, 8:52 AM EDT

This chart is as of 8:11 a.m. ET:

BY Doug Kass · Jul 3, 2024, 8:23 AM EDT

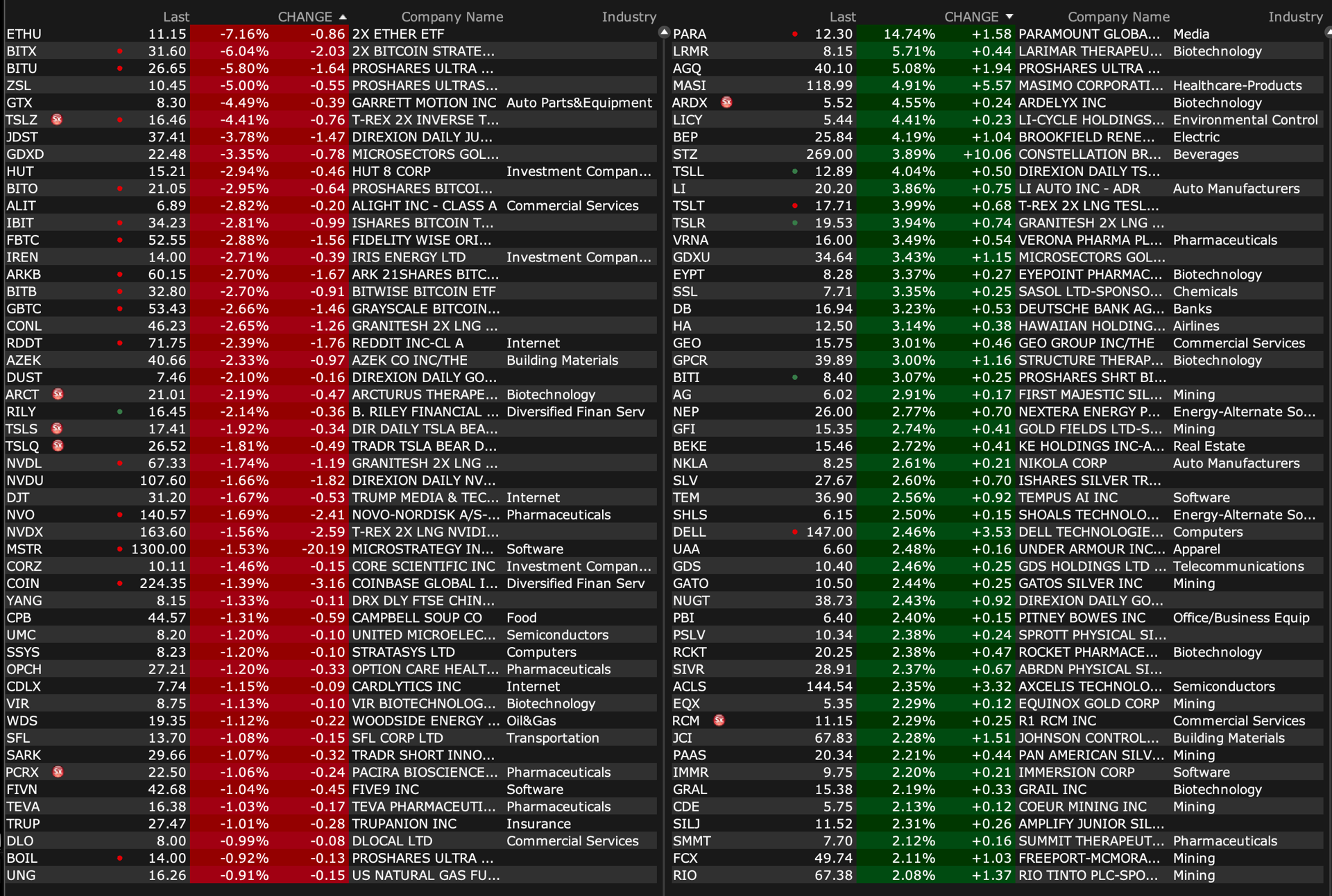

Here are some U.S. select premarket movers as of 7:42 a.m. ET:

-CDMO +5% earnings

-PARA +12% Skydance acquires ~50% of Paramount's controlling shares at $15/shr

-DM Nano Dimension to Acquire Desktop Metal for $5.50/shr in cash at total consideration $183M

-DOYU +25% special dividend announcement

-RPAY -11% convertible notes offering

-SLP -8% earnings, discontinues dividend

-FFWM raised capital $4.10

BY Doug Kass · Jul 3, 2024, 8:17 AM EDT

From JPMorgan:

· US: Futs are flattish with both Tech and small-caps poised to outperform as the market received a bullish boost from Powell but now the question is whether the macro data (and earnings) can deliver with ISM-Srvcs today and NFP on Friday; our scenario analysis is below. Pre-mkt, TSLA is leading Mag7 +2.8% with NVDA weaker but broader Semis are up small. Bond yields are flat to +1bps as the curve is flattening; USD is lower and cmdtys are higher led by metals where silver is the standout. Today’s macro data focus is on ISM-Srvcs, ADP/Jobless Claims, Factory Orders, and Fed Minutes (released after the Equity close).

and...

EQUITY AND MACRO NARRATIVE: After a slow start to the quarter, yesterday added a bit more confidence that the market realizes positive seasonality with both stocks and bonds rallying. SPX closed above 5,500 for the first time with the 10Y bond finding support near 4.5%. The 10Y yield had increased ~17bps after the Presidential Debate, so it is possible that we could see that response resume. The Hill reports that in the first batch of post-debate polls Trump has a 0.7% lead vs. 1.0% at the beginning of June; though some polls have Trump leading by as much as 3%. It may be the case that Trump needs to grow his lead to see a sustained move in bond yields, as well as closer proximity to the election. Focusing on today, ISM-Srvcs is an important print to shape the market’s view on growth with ISM-Mfg failing to provide confidence. With ISM-Srvcs, Feroli sees a 53.0 print which is above the Street’s 52.6 survey and below last month’s 53.8 print. His full comments are below followed by our scenario analysis for Friday’s NFP print.

BY Doug Kass · Jul 3, 2024, 8:09 AM EDT

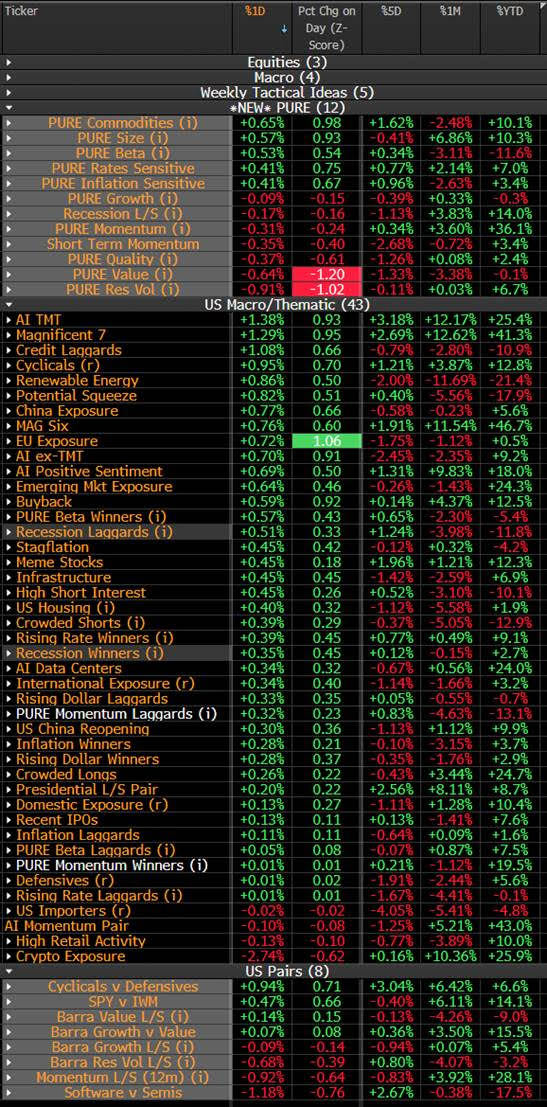

This table of themes and sectors is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Jul 3, 2024, 8:00 AM EDT

“When people are looking for performance, they sharpen their pencils and find reasons to buy.”

- Michael Price

Bonus — Here are some great links:

BY Doug Kass · Jul 3, 2024, 6:35 AM EDT

BY Doug Kass · Jul 3, 2024, 6:20 AM EDT

BY Doug Kass · Jul 3, 2024, 6:10 AM EDT

The S&P Short Range Oscillator is unchanged at 1.6% (and remains overbought).

BY Doug Kass · Jul 3, 2024, 5:58 AM EDT

BY Doug Kass · Jul 3, 2024, 5:45 AM EDT