We would expect Amazon’s shares to have a positive reaction to the initial read of its operating results. AMZN’s Q1’24 earnings report produced a beat across the board compared to GS/Street (FactSet) estimates as the momentum of its global eCommerce business, an outsized performance in terms of Operating Income, re-accelerating AWS revenues and strength in Advertising Services collectively framed the company’s operating performance in a positive light. The standouts would be consolidated Operating Income outperformance with $15.3bn (beating our estimate by ~30%) and AWS revenue growth of +17% YoY with 38% segment EBIT margins (exceeding prior period levels even when adjusted for accounting changes). In terms of forward commentary, Amazon’s Q2 guided revenue range roughly bracketed the GS/Street estimates at the high end and the Q2 Operating Income forecast of $14bn at the high-end was solidly above our pre-earnings estimate of $12.75bn. Looking forward to the earnings call, we would expect investors to focus on a few key areas – the state of the Amazon consumer globally (especially with Online Stores performance being more inline), any forward key investments across the eCommerce markets (grocery, same day), the framework for forward growth and margin dynamics within AWS and the positioning of AWS against the broader AI theme, any update on consolidated forward capex trends and any discussion of future period capital return (a rising focus among global technology investors).

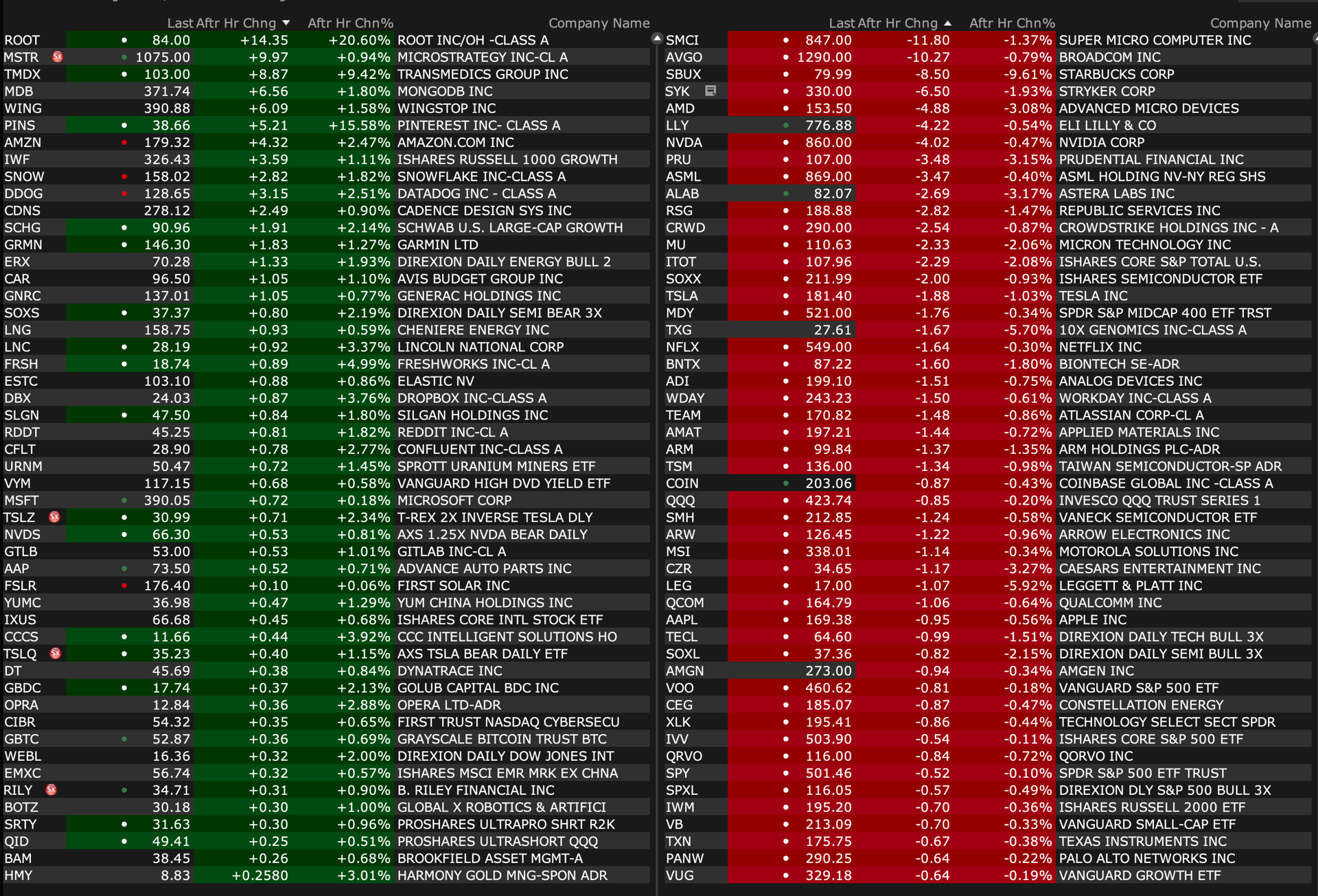

Starbucks misses by $0.12, misses on revs; US comps -3%; global comps -4%; will guide on conference call at 17:00 ET (88.49 +0.16)

Reports Q2 (Mar) earnings of $0.68 per share, excluding non-recurring items, $0.12 worse than the FactSet Consensus of $0.80; revenues fell 1.8% year/year to $8.56 bln vs the $9.12 bln FactSet Consensus.

Global comparable store sales declined 4%, driven by a 6% decline in comparable transactions, partially offset by a 2% increase in average ticket. North America and U.S. comparable store sales declined 3%, driven by a 7% decline in comparable transactions, partially offset by a 4% increase in average ticket. International comparable store sales declined 6%, driven by a 3% decline in both comparable transactions and average ticket; China comparable store sales declined 11%, driven by an 8% decline in average ticket and a 4% decline in comparable transactions. The company opened 364 net new stores in Q2, ending the period with 38,951 stores: 52% company-operated and 48% licensed. At the end of Q2, stores in the U.S. and China comprised 61% of the company's global portfolio, with 16,600 and 7,093 stores in the U.S. and China, respectively.

GAAP operating margin contracted 240 basis points year-over-year to 12.8%, primarily driven by deleverage, incremental investments in store partner wages and benefits, increased promotional activities, lapping the gain on the sale of Seattle's Best Coffee brand, as well as higher general and administrative costs primarily in support of Reinvention. This decline was partially offset by pricing and in-store operational efficiencies.

"While it was a difficult quarter, we learned from our own underperformance and sharpened our focus with a comprehensive roadmap of well thought out actions making the path forward clear," commented Rachel Ruggeri, chief financial officer. "On this path, we remain committed to our disciplined approach to capital allocation as we navigate this complex and dynamic environment," Ruggeri added.

Company typically guides on conference call at 17:00 ET.

I respect the trading sardine concept, but truly believe the future is extremely bright for weed stk...The 280 IRS rule will be history, greatly increasing the cash flow to these companies. The only question, of course, is how much of this is fully discounted already. I think not entirely. And the prospect of institutional buying lurks.

Dougie Kass

You might be correct.

But the total addressable market for cannabis is materially less than consensus.

State silos create diseconomies of scale.

State dispensary limitations in popular/large states preempts (the BurgerKing/McDonalds-like) market penetration opportunities.

Accounting standards for sector are weak.

Managements are not ready for prime time players.

Accumulated debt and non payment of taxes represent a heavy load for companies not delivering returns anywhere near their cost of capital.

As noted previously, the notice/review/lawsuits issues during six month plus comment period will get nasty.

The cannabis industry now faces a lengthy notice, comment, review and hearing period of at least six months - with regard to the rescheduling process.

It will not likely be a smooth period for the industry.

Stocks are likely headed higher, in the fullness of time, but not without a lot of volatility and, perhaps, some backing and filling after today's gaps.

I mentioned the now 2 yr contraction in the Dallas manufacturing index, which followed continued softness from NY and a rebound in Philly and today the Chicago April manufacturing index just posted at 37.9 print, well below 50 and vs the estimate of 45. I don't have the internals yet as the release is delayed to non-subscribers. Reconciling all of this, the ISM manufacturing index is expected to come in at exactly 50.

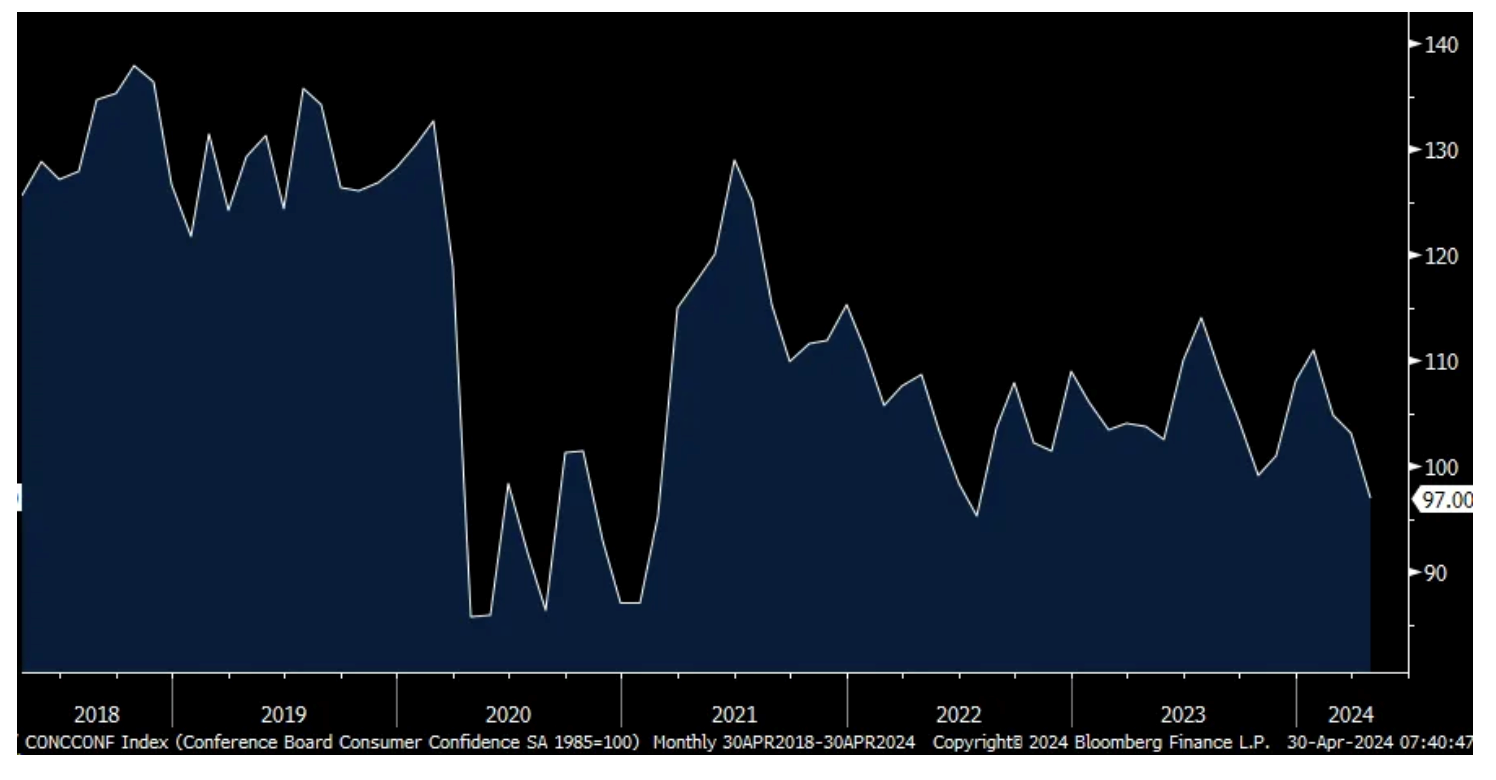

The April Conference Board Consumer confidence index fell to 97 from 103.1, 7 pts below expectations and that is the weakest print since July 2022. The Present Situation fell by 4 pts while the Expectations component was down by almost 8 pts. One yr inflation expectations held at 5.3% for the 3rd month in the past 4.

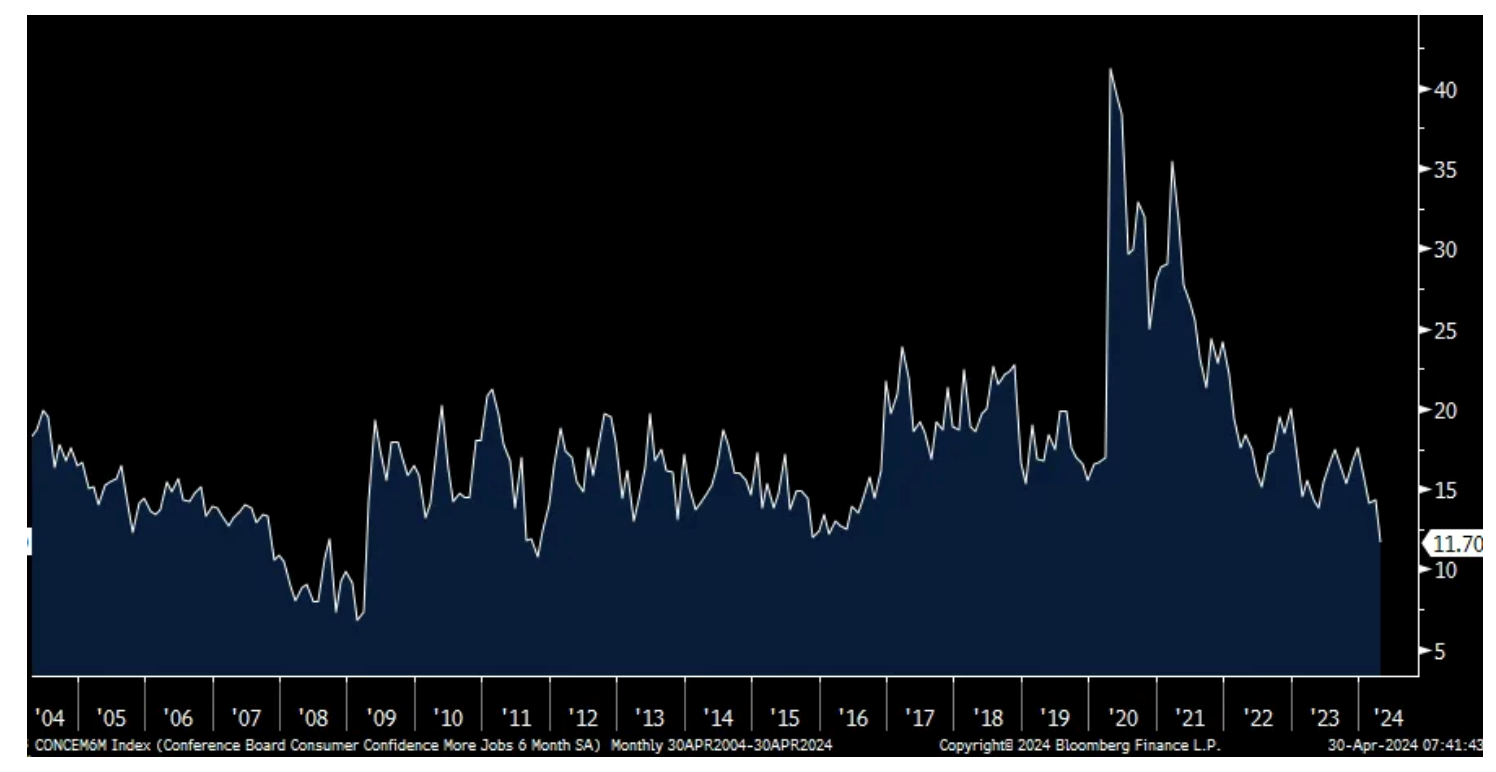

The key culprit in the confidence drop was the softer answers to the labor market questions. Those that said jobs were Plentiful fell by 1.5 pts to the lowest level since November. Those that said they are Hard to Get rose by 2.7 pts, the most since November. Also of note, there was a 2.6 pt drop in those expecting 'more jobs' in the coming 6 months, the least since October 2011 and that includes Covid. Income expectations fell too, by 1.9 pts m/o/m for those expecting an increase.

Spending intentions also fell across the board for autos, homes and major appliances.

The cumulative impact of multiple years of higher inflation has clearly taken its toll. The Conference Board said "According to April's write-in responses, elevated price levels, especially for food and gas, dominated consumer's concerns, with politics and global conflicts as distant runner-ups."

Bottom line, worries about the labor market were the biggest factor in the confidence drop, while inflation stresses remain. While just another labor market anecdote, here is more evidence that the labor market is on shakier ground than what the BLS has reported.

Consumer Confidence

Those Expecting 'More Jobs'

In February, and thus somewhat dated, S&P CoreLogic said its national home price index rose 6.4% y/o/y, giving first time buyers no relief when combined with a mortgage rate around 7%.

If the economy is so good, believed by some, why are federal tax receipts coming in less than anticipated? Fair question I believe and gets to my continued point that I think the US economy is very uneven with more pros mixed with cons than I've seen in all my years researching, analyzing, and investing in markets/macro and individual companies.

I say this because this is what the US Treasury said yesterday in the announcement that they needed to borrow more than expected in Q2, "The borrowing estimate is $41 billion higher than announced in January 2024, largely due to lower cash receipts, partially offset by a higher beginning of quarter cash balance." The bold is mine as with an unemployment rate still below 4% and the economy supposedly 'strong', why are tax receipts coming in less than expected?

Just maybe, the massive government spending/tax and grant incentives is distorting the economic stats to such an extent that it really muddies the economic situation in terms of impact and trying to figure out what's real and what's artificially induced is that much more difficult as a result. After all, when the government spends $2 trillion more than what they take in, that excess flows everywhere into the private sector either directly or indirectly.

There was something else that was interesting out of the Treasury yesterday, it was a statement on the economy from Eric Van Nostrand, 'performing duties of Assistant Secretary for Economic Policy for the Treasury Borrowing Advisory Committee.' There is this empirical assumption that the US economy, because of labor force growth forecasts, only needs to hire about 100,000 on a net basis to keep the unemployment rate for rising over a sustainable period.

Well, Eric said this, "Recent analysis suggests that above-trend immigration - which was postponed during the pandemic - has increased the breakeven pace of job growth needed to sustainably maintain a stable unemployment rate with population growth. Current estimates are above 200,000 jobs, roughly double the estimated breakeven pace before the pandemic." Interesting and we'll see.

I've opined before that many conflate the real meaning of the Philips Curve. They think that a tight labor market leads to higher inflation as many have sold the theory that way. That wasn't what Philips said. He actually said a tight labor market leads to higher wages, simple supply and demand. Obviously though the rest of us can take that one step further and say that higher wages leads to higher prices but only sometimes. When it doesn't is when productivity gains offset higher labor costs and thus there is no need to raise prices. However, when productivity increasing options are limited, price is an easy lever to pull.

There is no better example than seeing what is going on with California fast food joints in response to the new $20 per hour mandated minimum wage law. I mentioned last week what Chipotle said in that they are raising prices in the state by 6-7%. Here was the WSJ article that touched on this whole issue yesterday, titled, "California Fast-Food Chains are Now Serving Sticker Shock". So yes, here is a perfect example of when higher labor costs lead to higher retail prices.

Let's get to some interesting earnings comments and then shift overseas.

From Domino's Pizza:

"And our growth in the US came through positive order counts across all income cohorts in both our carryout and delivery segments. We saw the largest growth in our lower income cohorts that are undoubtedly benefiting from the renowned value that we're offering."

"National promotions are another way we're driving renowned value...Clearly, customers want value and we are driving it profitably for our franchisees. Now as it relates to our promotional cadence in 2024, you can expect it to be consistent with what we did in 2019. As part of that, you can expect around six boost weeks (select promotions)... Customer responses to deals are stronger than to everyday low prices." Their rewards program also helped to drive traffic.

As for their California business and response to the new wage law, "Our price increase is probably in the high single-digits...overall, we're solving for profit dollar growth. That's what we are always solving for. And we are looking to protect that franchisee profitability in California and throughout the system."

From McDonald's earnings release and just reported:

The comp gain of 2.5% was just about all price increase driven. "As consumers are more discriminating with every dollar that they spend, we will continue to earn their visits by delivering leading, reliable, everyday value and outstanding execution in our restaurants."

From Sofi:

With regards to their lending business, "As we shared last quarter, we've taken a more conservative approach toward originations, given our concerns around rate uncertainty and the broader macro climate. For Q1, adjusted net revenue of $325 million was flat y/o/y. Personal loan origination growth slowed to 11% y/o/y to $3.3 billion, in line with our more conservative approach. In fact, the balance of personal loans on our balance sheet declined 2% q/o/q."

On the credit quality side, "We anticipate ongoing normalization in credit performance toward pre-pandemic levels of 7% to 8% life of loan losses." Their personal loan charge off rate is currently 3.45% from 4.02% in Q4 but includes "the impact of asset sales, new originations and the delinquency sale in the quarter."

While the commercial real estate industry is very challenging for those who have debt coming due this year and/or own non Class A type office buildings, the business of leasing space seems to be still going well according to Cushman and Wakefield.

They said, "During the quarter, we saw continued solid growth in leasing across our global platform, with revenues up 5% for the 2nd quarter in a row...The growth in Q1 was again global in nature, with Americas leasing up 1%, EMEA leasing up 30% and APAC leasing up 10%. In the Americas, we saw particular strength in midsize office and industrial leasing."

Here was the lay of the housing land from the carpet and flooring company Mohawk Industries speaking Friday:

"Across our regions, market conditions remain similar to the prior quarter with significant pricing and mix pressures due to industry competition for volume. Though slowing, the commercial channel continues to outperform residential. Residential remodeling remains soft due to the low housing sales and the impact of inflation on discretionary spending. Retailers have reported that consumers are reluctant to initiate higher-ticket projects with flooring facing greater pressure since most replacements can be readily deferred."

NXP, the chip maker that has more of an industrial customer base said this in their earnings release:

"Our first quarter results, guidance for the 2nd quarter, and our early views in the 2nd half of the year underpin a cautious optimism that NXP is successfully navigating through this industry-wide cyclical downturn." And they referred to the "challenging demand environment." Not everyone can sell AI chips I say.

On Semiconductor echoed the same thing on their call, another semi name with industrial customers:

"Inventory digestion persisted across the automotive and industrial markets with stabilization in the traditional part of our industrial business. We remain cautious about the 2nd half outlook, but we expect customer inventory levels to normalize and the market to stabilize."

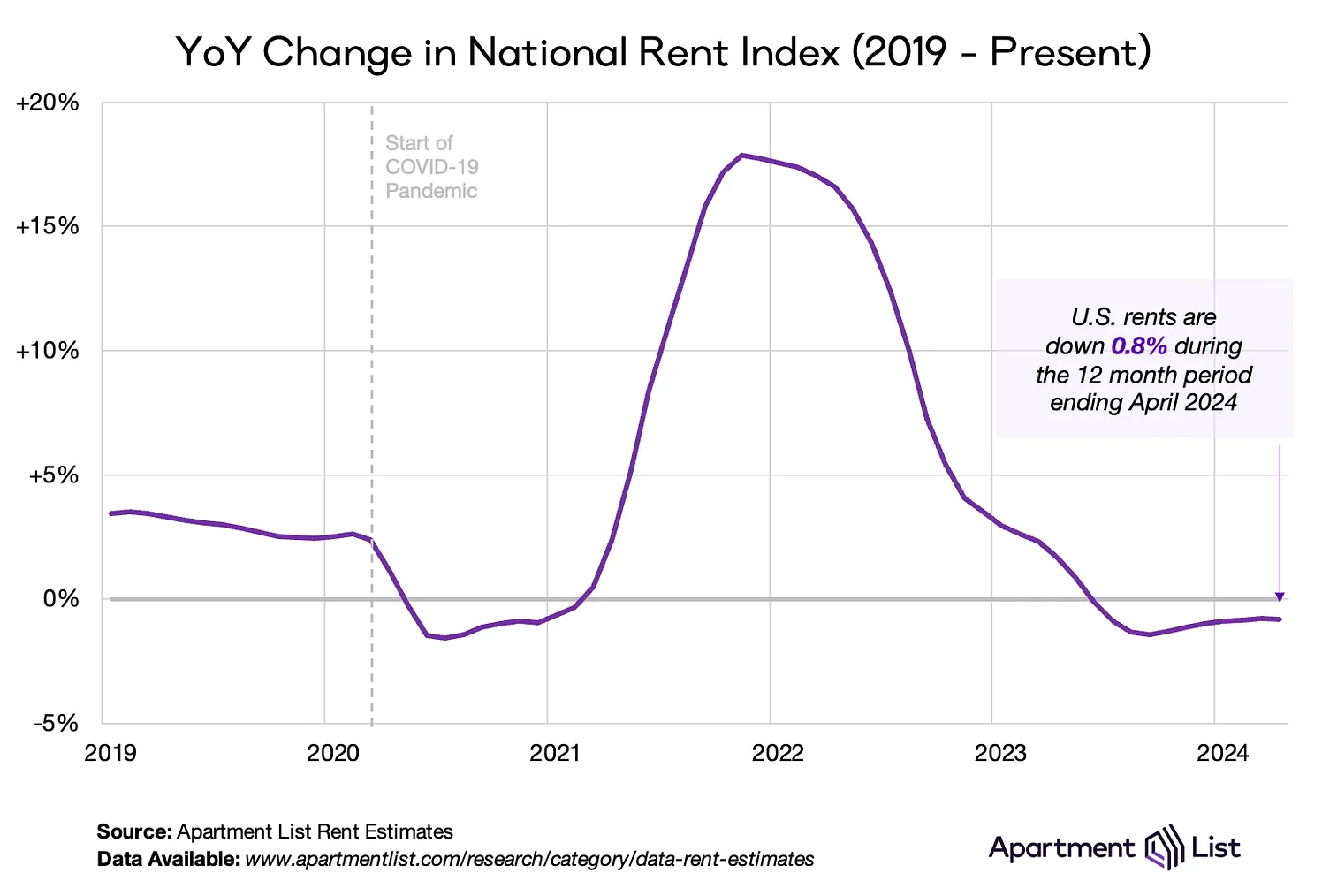

The new Apartment List National Rent Report is out and for April showed a .5% m/o/m increase in new lease growth but seasonally rises in the spring as this is the 3rd month of gains. Versus April 2023, new rents are still down .8%. Due to more supply, mostly in the sunbelt, the national vacancy rate is at 6.7% and should go up further as the year progresses because of all the new supply. Rents were up in 83 of 100 cities in April m/o/m, though 43 are up y/o/y. The sunbelt states of Austin, Raleigh and Orlando saw the biggest rental declines y/o/y.

Bottom line, rental growth should continue to slow y/o/y as we absorb all the new supply and the CPI will at some point capture this. Assume renewal rents are up about 2-4%. That said, rental growth is still up 22% from the beginning of 2021 while home prices are up about 40% so if the latter was included in CPI, it headline/core inflation would thus be much higher.

Yesterday, the April Dallas manufacturing index remained deeply negative at -14.5 vs -14.4 in March. It has now been a full two years of contraction in this region. The optimism though for a bottoming is there as the 6 month outlook rose to 7.9 from 1.3 and that is the highest since February 2022. An inventory rebuild is what is hoped for as expectations for new orders rose to the best since March 2022.

Here were some of the notable comments from respondents in differing industries:

Furniture & Related Product Mfr'g:

"Consumer confidence for consumer goods has noticeably weakened."

Transportation Equipment Mfr'g:

"The business and political environment is terrible."

Computer & Electronic Product Mfr'g:

"We are close to an inflection point of a cyclical bottom. Customers have been reducing inventory over the last several quarters, which looks to be coming to an end in most markets."

"Industrial manufacturing is showing signs of positivity due to the possibility of an interest rate decrease. Please do it. Manufacturing is really hurting."

"Customer orders have dropped. The indication is the economy is hurting spending in our area specifically. Customer uncertainty is worsening."

"Business is generally good, but we're starting to see more customer resistance to prices. Our costs have increased dramatically over the last two years, and we have customers asking to hold prices to last year's level, which we just can't do. We continue to make capital investments to improve productivity and reduce unit labor cost."

Machinery Manufacturing:

"Business is in a state of flux. The elections I believe are affecting business decisions, and we expect this to continue for the foreseeable future."

"Business is extremely slow, and we see no signs of improvement."

"I keep thinking we'll hit bottom and either level out or turn up, but we keep pushing those hopes out a month, and another month, and another. Forecasting and predicting have become rather challenging. We've got a few small jobs here and there, but nothing significant and nothing sustainable. It could wind up being a long, hot, slow summer for our operation."

Nonmetallic Mineral Product Manufacturing:

"Inflationary pressures on raw materials and construction costs are driving up the cost of public projects. This is causing states to delay or scramble for funding for projects that have long lead times.

Paper Manufacturing:

"There has been a decrease in new orders for three weeks now. Currently, we think this will come around, but we get more concerned as time goes on."

Food Manufacturing:

"We're coming out of a seasonal low, and there seems to be a slight uptick in demand, despite prices for raw materials (and finished goods) increasing."

Overseas, China's state sector focused April manufacturing PMI fell slightly to just above 50 at 50.4 from 50.8 in March. The estimate was 50.3. Non-manufacturing is doing better but that component weakened to 51.2 from 53 and below the estimate of 52.3.

The Caixin manufacturing PMI was a bit better than above as they printed 51.4 from 51.1 in the month before. While some China watchers in the US think China is solely reliant on us, China does massive manufacturing business in the emerging market world and a trade surplus with them, along with the rest of the world, and means that they have no incentive to weaken the yuan as some think they should. I don't see it happening. Stocks in China were mixed and quietly the Hang Seng is now up 4.2% year to date.

Caixin said "Underpinning the latest acceleration in manufacturing sector growth was better demand conditions...Additionally, new orders from abroad expanded at the fastest pace for nearly 3 1/2 years. Global market demand improved at the start of the 2nd quarter, according to panelists."

In Europe, headline CPI in April rose 2.4% y/o/y as expected and the same pace seen in March. The core rate was higher by 2.7% vs 2.9% last month but one tenth above the estimate. Services inflation in particular was higher by 3.7% y/o/y vs 4% in the 5 months prior. Non-energy industrial goods prices were up by .9% y/o/y vs 1.1% in March and continues to slow and as seen in the US. Nothing here will change the expected June rate cut from the ECB. Bond yields are slightly higher in the region while the euro is a touch lower.

Germany's unemployment rate held at 5.9% in April but the number of unemployed did rise by 10k which was above the estimate of 8k and March was revised up by 2k to 6k. They also reported March retail sales that were about as expected when including the revisions. The DAX is down about 1/3 of a percent but still up almost 8% ytd.

Bottom line, Germany's economy was particularly hurt by the global manufacturing slowdown and the moderation in demand from China. Their services sector certainly carried the economic weight. Expect at best slight growth from the European region this year, even with rate cuts.

GDP growth in the Eurozone in Q1 did rise .3% q/o/q, 2 tenths above the estimate but Q4 was revised down by one tenth to a very slight contraction of .1%. Growth y/o/y was .4%.

Yields are moving higher, S&P futures lower after the Q1 Employment Cost Index rose 1.2% q/o/q, above the estimate of up 1%. That is the most since Q1 2023. The y/o/y gain of 4.2% was the same pace seen in Q4 with wages/salaries higher by 4.4% and benefits up by 3.7%.

The private sector internals saw wages and salaries up by 4.3% y/o/y, the same seen in Q4 and total comp was higher by 4.1% y/o/y. I want to put that 4.1% gain in perspective as while it is down from a peak of 5.5% in June 2022, the 20 yr pre Covid trend was just 2.7%.

It seems that in government work is where the upside surprise took place as wages and salaries increased to a 5% y/o/y gain from 4.7% in Q4. Total comp growth was 4.8% y/o/y and that compares with an average of 2.9%. That’s also just below the highest growth in at least 25 years.

Bottom line, as stated, higher comp for government employees drove the upside relative to expectations. Also, on one hand we want to see strong wage growth in order to help consumers grow their standard of living via REAL wage growth. On the other, the Federal Reserve worries that faster wage growth will translate into higher prices that they are trying to fight against. As stated this morning, sometimes it does, like in California franchisee restaurants, and sometimes it doesn't when productivity gains are strong.

They are: Nvidia NVDA, Tesla TSLA, Lilly LLY, and Novo Nordisk NVO.

* The perception of near open-ended market opportunities invokes speculation/animal spirits that typically produce much higher stock prices.

* "Game changers" are different than "core compounders" — the former, at a moment in time, are seen to having the sky as the limit whereas the latter have durable, deep and long-lasting competitive moats.

Nvidia (in AI (artificial intelligence)), Tesla (electric vehicles) and Novo Nordisk/Eli Lilly (in GLP-1 drugs) are recent examples of equities that are perceived to be facing "open ended" end-market opportunities — and outsized sales/profits growth — for the foreseeable future.

These stocks are seen to face such promising relative and absolute profit growth that determining terminal price earnings multiples are difficult. And, more often than not, the exceptional growth prospects are accorded a high valuation that, arguably and inevitably, results in so much speculation that historic stock prices and multiples are thrown out the window and animal spirits propel the stocks to almost geometric expansion.

By means of background, I tend to be a value investor. But, at the same time, I realize how one can generate excess returns ("alpha") by committing a portion of my portfolio to more speculative issues with an "open ended" flavor.

Some of my recent buys in biotech, cannabis and on-line gaming have similar characteristics to some of the past winners and game changers named above — in that the upside has that "open ended" character and feeling to them:

* Biotech - Long runway for GLP-1 drugs (Viking Therapeutics VKTX)

* Cannabis - New states lead to rising market demand (Florida), rescheduling means elimination of 280-e taxation/, SAFR means uplifting/resolution of custody issues/institutional buying (MSO, Curaleaf CURLF, Terrascend (TSNDF), Green Thumb GTBIF and Trulieve TCNNF)

This daily Futures feature is like inside baseball. I try to show you and write about what I believe thoughtful hedge fund managers are looking at when they awake -- let's call it our normal routine -- setting the stage for their strategy for the day. The market is a complicated mosaic and the more info you have, the better trader and investor you will be!

The market (and money) never sleeps -- and neither do I, it appears! I have previously described the importance that overnight futures trading hold for me here. It is a guidepost to my strategy in the regular trading session. Moreover, the overnight/early morning futures hold opportunities as they are (1) inefficient, though liquid and (2) it seems fear and greed are often exaggerated outside the regular trading session. I frequently try to capture those efficiencies by trading actively both in the pre- and after-market sessions.

Here are brief observations I wanted to highlight and provide a summary of overnight price movements in various asset classes:

* Stock futures were modestly lower overnight within a narrow range. S&P futures peaked at +2 and bottomed at -12. Nasdaq futures peaked at +18 and bottomed at -39. At 5:56 a.m. ET, S&P futures were -9 and Nasdaq futures were -35.

* Commodities are broadly lower. Brent crude was +$0.14 to $88.54.

* The S&P Short-Range Oscillator has moved back into an overbought last night at 2.83% v. 0.04%

* The VIX is at 14.85 (+0.18). We have been successfully putting on straddles on VIX strength and taking off on VIX weakness.

* The US dollar is very strong against the yen but unchanged from the euro and pound.

* Interest rates are higher by about 1-2 bps across the board. The yield on the two-year Treasury is 4.983% (+1 basis point). The yield on the 10-year Treasury is +2 basis points at 4.63%. The long bond yield is also +2 basis points at 4.748%.

* Overnight, the inversion of the 2s/10s Treasuries curve is down to -31 basis points.

Here is a synopsis of some of my columns I believe were important, or in the event you were out for the day and/or did not read my Diary. The principal intent is to review the logic of my market moves and other factors:

“Buy when everyone else is selling and hold when everyone else is buying. This is not merely a catchy slogan. It is the very essence of successful investments.”