Disasters Have a Way of Not Happening

* We are buying at the sound of cannons... "When it's time to sell you won't want to." - Doug Kass "When its time to buy you won't want to." - Wally Deemer The business media, investment strategists and money managers are herd-like. They think in consensus terms and operate, generally, with "first ...

You've reached your free article limit

You've read 0 of 1 free Pro articles.

* We are buying at the sound of cannons...

"When it's time to sell you won't want to."

- Doug Kass

"When its time to buy you won't want to."

- Wally Deemer

The business media, investment strategists and money managers are herd-like. They think in consensus terms and operate, generally, with "first level thinking." When the tide is rolling in and price momentum is favorable -- in a market that is dominated by passive strategies and products -- the herd typically wins. But, once the tide goes out and price momentum inflects, their lack of rigor, risk management and investment process are revealed. It is then that we realize:

"There is no there there."

- Gertrude Stein

Unfortunately, while market advances are a staircase higher, market declines are often elevators lower - as we have recently witnessed.

In the main and throughout the last 18 months few of those cohorts expressed economic, inflation, interest rate, geopolitical and valuation concerns. Indeed (and in the extreme), as I wrote several months ago, panelists on the "shows" literally could not find any adverse outcomes at all.

For this reason and others are why I wrote this column one week ago:

The Business Media Has Failed You

* Not providing two way discourse/debate (and relying on formulaic programming) has prepared investors poorly for when the halcyon days are over and the tides starts going out...

"So much for objective journalism. Don't bother to look for it here--not under any byline of mine; or anyone else I can think of. With the possible exception of things like box scores and race results, there is no such thing as objective journalism. The phrase itself is a pompous contradiction in terms.”

― Hunter S. Thompson, Fear and Loathing

My comments below should be a familiar refrain for those that follow me on Twitter and elsewhere...

Hubert Humphrey once said, "Freedom is hammered out on the anvil of discussion, dissent, and debate." The same applies to the generation and display of ideas -- in this case, market, economic and company views/outlooks. They are best presented and hammered out in disputation.

The business media, especially Fin TV, has once again failed to properly serve their most important stakeholder - their viewers and readers.

Journalists best serve their constituents by providing balanced and objective reporting. It is especially important for the media to always inject a degree of skepticism. This is even more important when the tide is coming in and the salad days of bullishness (come euphoria) are upon us. The media should do so to prepare for the inevitable downturn in fundamentals, stock prices and investors' sentiment.

It is also important for journalists to remain independent of view and to not have personal relationships (or the desire to have access) with company managements to influence their views. (Salesforce (CRM) , ServiceNow (NOW) and Nvidia (NVDA) come to mind!)

The business media has not provided this service. Instead, formulaic programming offers up the same (day after day) uber confident and non objective "talking heads" and their ever superficial "analysis" that is miles long but only inches deep (by practitioners who would never even qualify for interviews as analysts in any serious hedge fund and who never met a market they did not like) -- and, too often, are not supported by rigorous analysis or investment process.

"Praise by individual, criticize by category."

- Warren Buffett

My comments are not intended to be ad hominem, they are (like Meet The Press' Tim Russert was) fact based - taken from archived videos and interviews.

Without time stamps, guests and panelists in the business media are not held accountable. (Worse yet, they are too often filled with hubris). Case in point, a panelist on CNBC's Halftime, who, in the last three years, has endorsed only three specific stocks as his foundational, "forever" and largest holdings - Alibaba (BABA) , Moderna (MRNA) and UnitedHealth (UNH) :

* BABA missed last night and the shares are -$7 overnight - the shares have receded from $192 to $128 (he has recommended all the way down - as recently as two weeks ago Trade Tracker: Steve Weiss buys more Alibaba )

* MRNA dropped precipitously from $500 to a low of $22 (now $52)

* UNH declined from $595 to $282

(I should note that in the case of Alibaba, the panelist berated the other panelists who purchased BABA due to the ownership structure in which you are not a shareholder but own an interest in an offshore vehicle! Then he bought near the top of the chart.)

Contrary views (read: bearish) are underemphasized or not delivered at all in a backdrop of giddiness and FOMO ("fear of missing out").

Discipline and assessment of downside risk relative to upside reward are nearly always abandoned as an extreme level of complacency is urged at just the time markets mature and overvalued equity prices peak (in a valuation promise of a new never ending bullish cycle and paradigm).

Geopolitical risks, extreme valuations and private equity/credit concerns - were risks that some of us ursine types have been warning about for twelve months. Yet these factors were given little discussion or weight in the media. It is only "after the horse left the barn" (when the problems have surfaced), that a proper discussion is permitted.

Memo to the business media:

There are some situations one simply cannot be neutral about, because when you are neutral you are an accomplice. Objectivity doesn't mean treating all sides equally. It means giving each side a hearing.

By Doug Kass Mar 19, 2026 7:40 AM EDT

Looking Forward

As mentioned above, disasters have a way of not happening. (h/t Byron Wien)

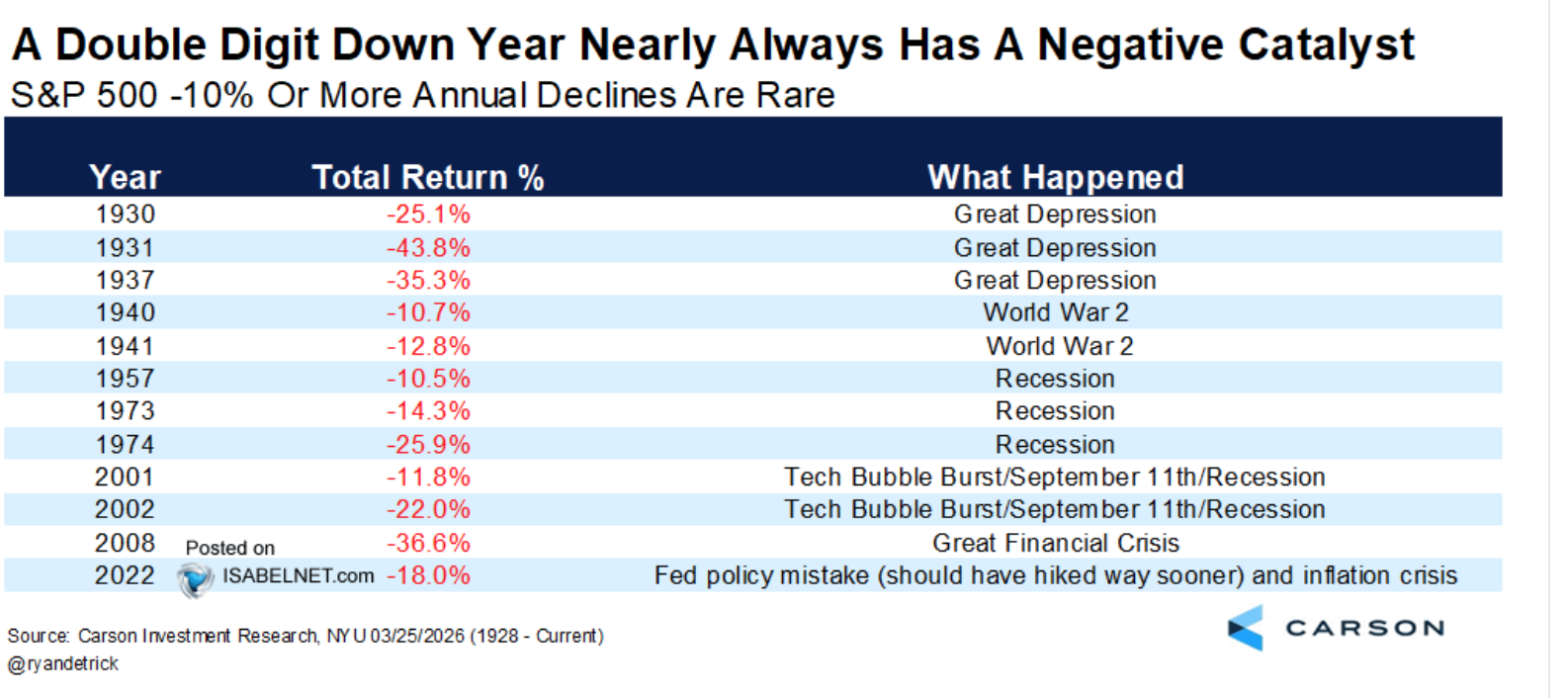

There have been only 12 data points in which the S&P Index fell by 10% or more:

For the reasons mentioned in "Growing Less Bearish" I have begun to accumulate equities - after being net short for some time.

Here are some more reasons I have begun to buy:

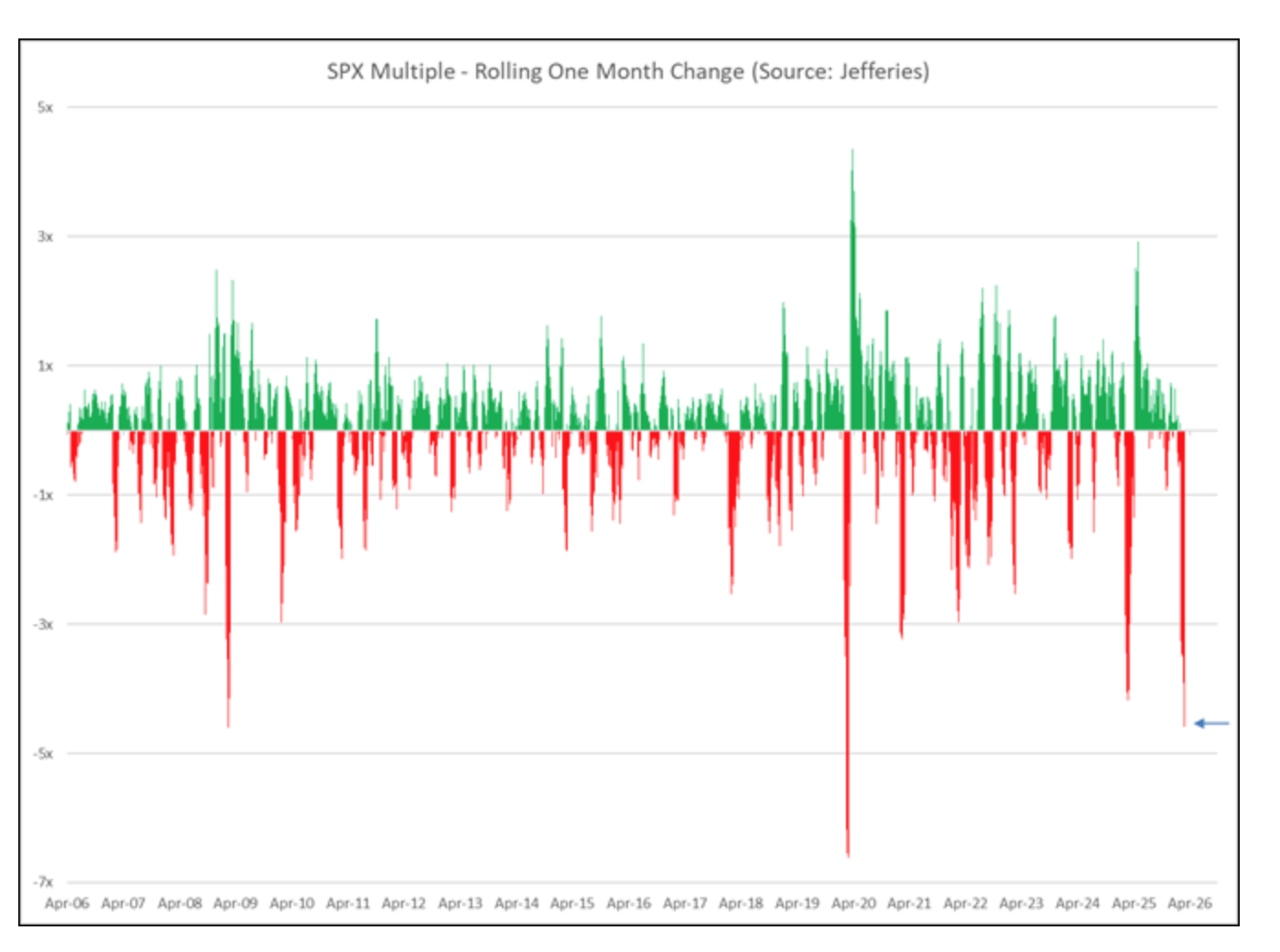

* The compression in valuations has been multiple driven and the swiftness of the drop in price earnings multiples was last seen five years ago during Covid:

* The price earnings ratio of the S&P Index is now one turn under the five year average:

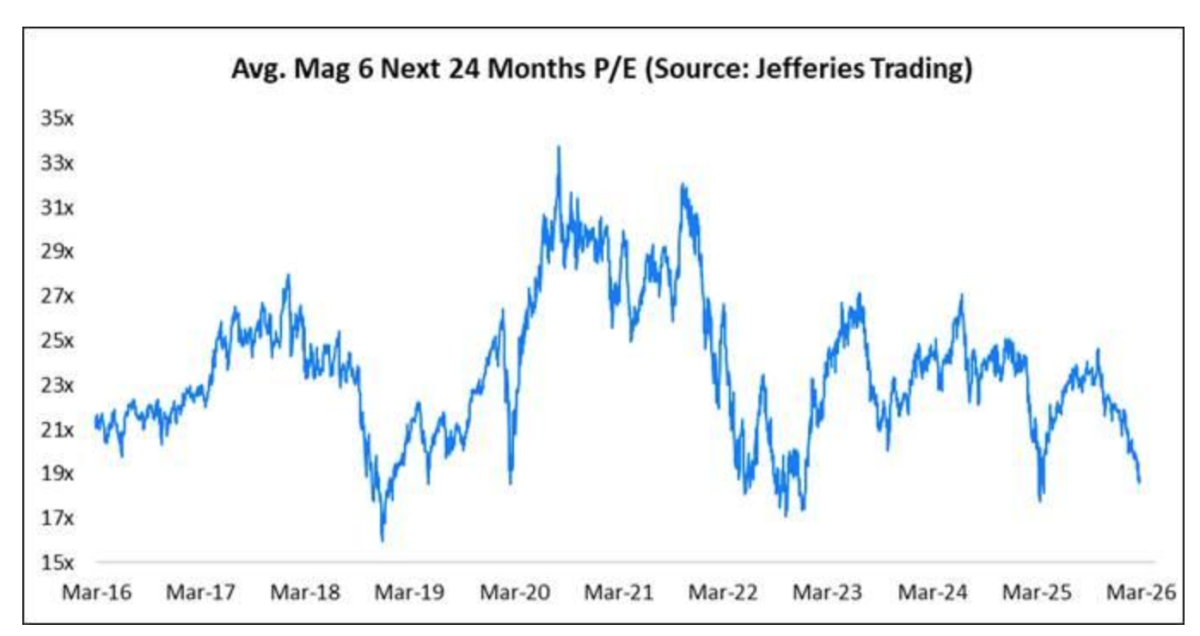

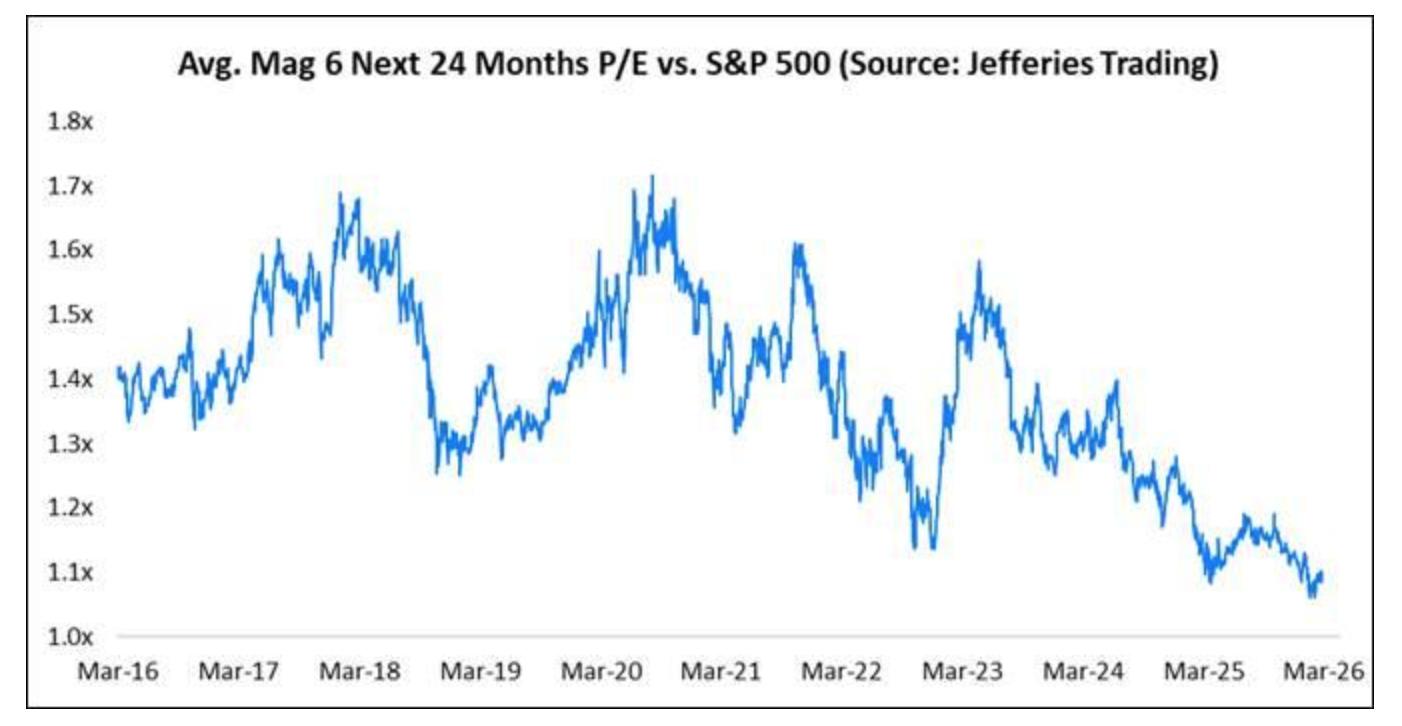

* MAG 7 valuations (excluding Tesla) is down to 19-times vs. 17-times low over the last decade:

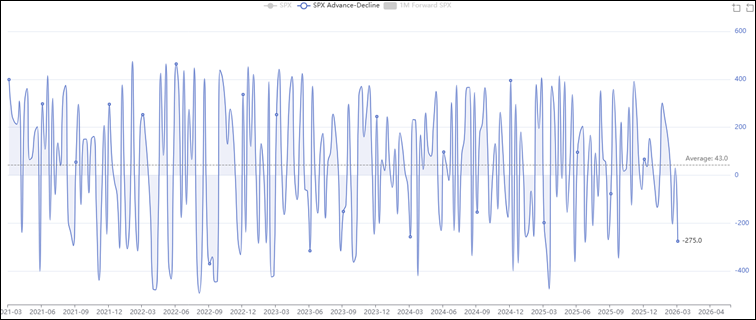

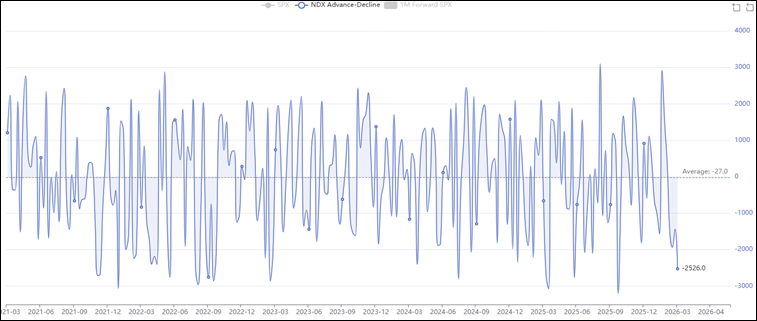

* Sentiment has deteriorated. S&P and Nasdaq advance/decline lines are near five year lows:

Position: Long UNH (S)