Why I'm Buying Kohl's Before the Holiday Season

This small-cap retailer could be in line for a turnaround.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Here's a small-cap retailer that might just be ready to not stink anymore.

Kohl's Stores KSS was not always a small cap. At a market cap of less than $2.2 billion, though, it is now. Back in late August, the firm reported its second quarter financial results. The firm surprised Wall Street in terms of profitability, big time. A GAAP EPS of $0.59 ($0.15) better than consensus on revenue of $3.53 billion. The sales number fell a little short of what Wall Street was looking for. OK, that's not great, but the firm had learned to live within its means and run its business effectively.

The sales print was "good" for a year-over-year contraction of 4%, but the EPS print was a return to profitability after a rough Q1. Looking ahead to the full fiscal year at the time, the firm guided sales growth down to a decrease of 4% to 6%, from 2% to 4%.

That said, Kohls also saw an adjusted EPS of $1.75 to $2.25, up from prior guidance of $1.25 to $1.85 and above the then consensus of $1.50. Operating margins for the full year were seen improving to 3.4% to 3.8% from a previously issued outlook of 3% to 3.5%. On a down note, comp store sales were seen slowing to -3% to -5%.

Some Fundamentals

For that second quarter, the firm generated operating cash flow of $254 million. Out of that number came $113 million in capex spending, leaving $141 million in free cash flow. These cash flows had been negative for the quarter prior. The firm has not repurchased any common stock since 2022, but did pay shareholders $56 million in cash dividends. The firm has continued to pay that dividend of $2 per share per year, which, at these prices... yields 10.2%. With cash flows like this, just maybe that dividend can be sustained.

The balance sheet is a little beaten up but is vastly improved from where it was a couple of years ago. Getting the firm's debt-load under control while still paying the shareholders has obviously been a priority of management, whether announced or not. I, for one, have noticed.

Kohl's ended the August period with a cash position of just $231 million. That's not great. The firm also had inventories of $3.151 billion, making current assets of $3.713 billion. Current liabilities add up to $3.438 billion, including $763 million in shorter-term debt. The current ratio of 1.08 is acceptable, but certainly not a home run. The level debt coming due within 12 months will require Kohl's to roll over some debt at prevailing interest rates.

Total assets amount to $14.18 billion, most of which is property. There is no entry made for intangible assets, which we find commendable. Total liabilities less equity will come to $10.35 billion, including long-term debt of $1.173 billion. That's a lot, but it is down by more than $900 million over the past six months.

The Current Quarter

Kohl's will report on November 27. Wall Street is looking for a GAAP EPS of $0.32 on revenue of $3.75 billion. That will be down from $0.53 a year ago, with sales down 5% year over year, Thats said, the firm should start showing actual sales growth with the April 2025 quarter, or that's at least what Wall Street sees in consensus. One more thing: About three weeks ago, the most recent data I have, a rough 49% of the entire float was held in short positions.

I really think I am going to grab a few shares ahead of the holiday season. Because there is an obvious attempt being made to clean the firm's fundamentals, because the dividend may be able to hold its level, because there's always the possibility of a short squeeze. Oh, and because CEO Tom Kingsbury is not former CEO Michelle Gass who in my opinion, was awful. You did notice the sudden post-earnings train wreck at Levi Strauss LEVI last week, right? You know who their CEO is? That's right, Gass.

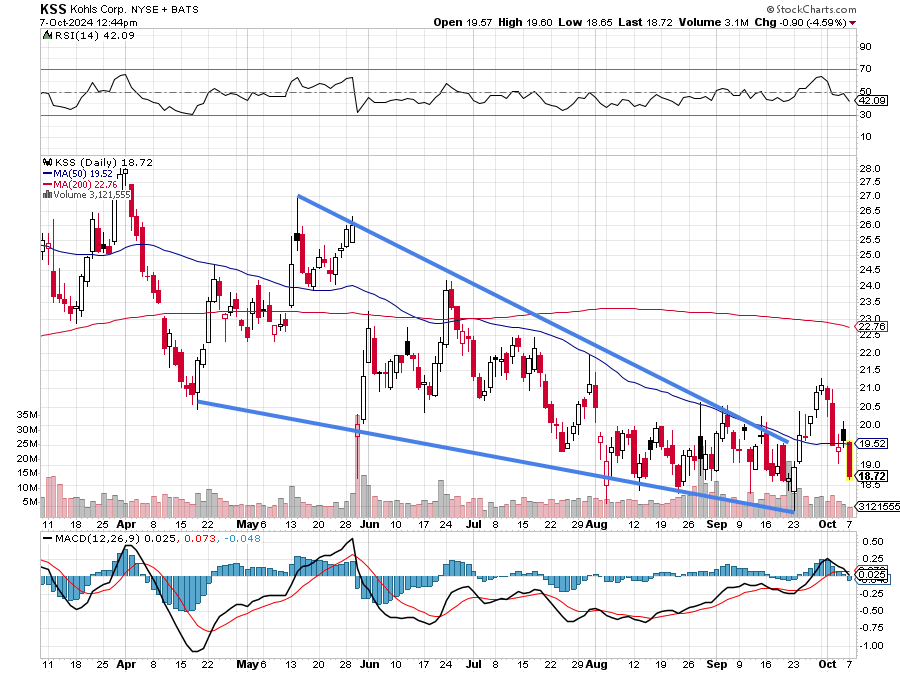

The Chart

Readers will note the falling-wedge pattern that stretches from last April into late September. This is a pattern of bullish reversal. Note the failed attempt at a breakout over the final week of September.

Now, having taken and failing to hold its 50-day SMA, and with a suddenly bearish looking daily MACD, we'll find out if KSS returned to its downward trend, or finds support before doing so. No promises, but that $2 per share and that short interest is calling my name. I think the risk/reward proposition for this name has improved from where it was six months or more ago. I will wait for this piece to reach publication before acting on my own behalf.

At the time of publication, Guilfoyle had no positions in any securities mentioned.