Who the Heck Is indie Semiconductor?

This small-cap name recently reported its latest financial results and there's not much to like.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Ever heard of indie Semiconductor INDI? Me neither, so let's explore. (By the way, the name of the firm is spelled with a lowercase "i," so that's not a misprint. And my light case of OCD is being triggered by not being able to capitalize that letter.)

Who the Heck Is indie Semiconductor?

indie Semiconductor is an Aliso Viejo, California based — wait for it — semiconductor designer. The firm offers automotive chips and software solutions for advanced driver assistance systems, driver automation, in-cabin user experience and electrification.

This company focuses on edge sensors, light detection and ranging radar, ultrasound and computer sight. The firm is an approved vendor to tier one automotive suppliers and indie platforms can be found in vehicles produced by well-known automobile manufacturers globally.

Here in the U.S., indie Semiconductors has design centers in Austin, Boston, Detroit, San Francisco and San Jose. The firm is also in Argentina, Hungary, Germany, Scotland, Switzerland, Morocco, Israel, Canada, South Korea, Japan and China.

Earnings

Last week, indie reported the firm's second quarter financial results. For the three months ended June 30, 2024, indie posted an adjusted EPS of $-0.09 (GAAP EPS: $-0.11) on revenue of $52.355 million. The earnings print landed precisely upon consensus. The revenue print, however, fell just short of the mark, while reflecting year-over-year "growth" of -0.5%.

Operations

As revenue was contracting one half of 1% to $52.355 million, costs and expenses decreased 4.1% to $88.989 million. This left an operating income/loss of $-36.634 million, up from the year ago comp of $-40.725 million. After accounting for interest, taxes, other income/losses and a gain in fair value of contingent considerations and acquisition related holdbacks, the firm's net income/loss dropped from $-13.127 million to $-19.16 million. That works out to a GAAP EPS of $-0.11 down from the year ago comparison of $-0.09.

Fundamentals

For the quarter reported, indie generated operating cash flow of $-19.7 million. Tack on capex spending of $3.7 million, and the firm's free cash flow at $-23.4 million. The firm is obviously in no position to return capital to shareholders.

Turning to the balance sheet, indie ended the quarter with a cash position of $112.3 million, inventories of $42.5 million and current assets of $247.6 million. Current liabilities add up to $93.1 million including short-term debt of $12.6 million and $3.2 million in unearned revenue. This brings the firm's current and quick ratios to 1.21 and 0.75. These ratios kind of, almost pass muster. I would definitely like to see a stronger quick ratio.

Total assets amount to $797.3 million, but that includes $494.7 million in goodwill and other intangibles. At 62% of total assets, I would see this as something of a red flag. Total liabilities less equity comes to $294.7 million, including $157.3 million in long-term debt. This balance sheet does not excite me in the least.

My Thoughts

This name came to me by virtue of subscriber request. I have to say that there is not a lot to like here. The firm is losing money, burning cash, bloats the asset side of its balance sheet with intangibles and owes more than half of the total value of the firm's tangible assets. The tangible book value of this firm works out to $-0.14 per share. I would not buy this stock with my money and if the SU $10 Portfolio were still in existence, it would not find a slot either in the portfolio itself nor in the bullpen.

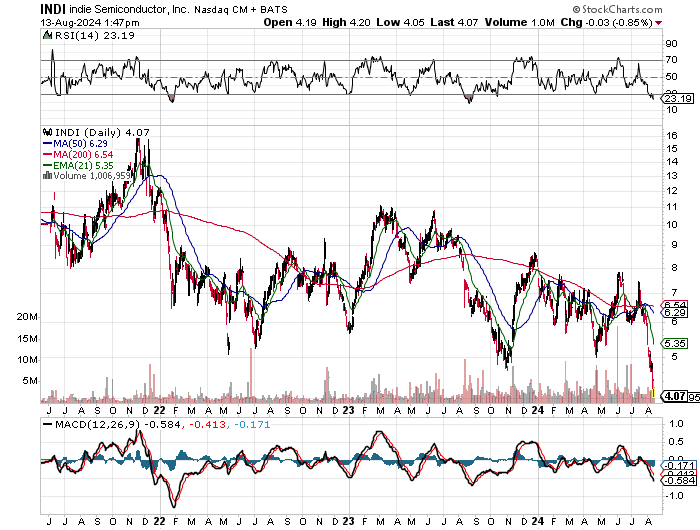

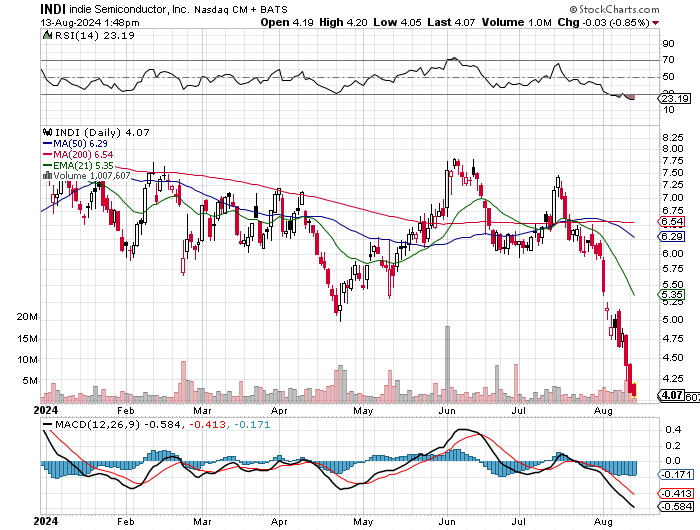

Here's a three-year chart of INDI, just so readers can visualize what we're looking at.

On the year-to-date chart, readers can see that the daily MACD, RSI and share price have all gone into free-fall together. The last sale now stands 35% below its 50-day SMA and 24% below its 21-day exponential moving average. Not even with your money. Even if I hated your guts. Even if you dumped my sister in high school.

At the time of publication, Guilfoyle had no positions in any securities mentioned.