Is Verizon Stock a Buy Amid $20 Billion Frontier Deal?

Making the investment case for and against the telecomm giant.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It's been a while since I have thought about even thinking about telecom. No joke. Stocks like Verizon VZ and AT&T T have been dead money, literally, for years. T-Mobile TMUS has to be left out of that statement, as that stock has performed, but I think you catch my drift.

This week that changed. Verizon was in the news, rumored to be interested in acquiring Frontier Communications FYBR. Verizon's stock was up 2.8% on Tuesday and down 3.4% on Wednesday. Frontier's stock was down 2.6% on Tuesday and up an astounding 38% on Wednesday. That was smoke.

Today, There's Fire

News broke early on Thursday morning. Hard news. Verizon Communications had announced an all-cash deal to acquire Frontier Communications for $38.50 per share, which amounts to roughly $20 billion or a 43.7% premium to FYBR's 90-day volume-weighted average share price on September 3, 2024. That was the final day of trade ahead of the first reports in the media speculating that such a deal might occur. Put more plainly: the deal price was a 37% premium to Tuesday's closing price. VZ is down 1% shortly after Thursday's opening bell, while FYBR is down around 9%, which kind of makes one wonder, given that this is a cash deal.

The deal, expected to close within 18 months, is expected to be accretive to Verizon's revenue and adjusted EBITDA growth rates while driving substantial cost synergies upon closing. Verizon states that the firm expects to realize $500 million or more in run-rate cost synergies by year three from the benefits of increased scale and distribution, as well as network integration. Frontier's fiber network encompasses 2.2 million subscribers across 25 U.S. states, and this will be integrated into Verizon's portfolio of fiber and wireless assets.

Separately, Verizon reaffirmed the firm's full year guidance for adjusted EPS of $4.50 to $4.70 and wireless service revenue growth of between 2% and 3.5%. Verizon also announced a quarterly dividend of $0.6775 per share, up from $0.665, which is a 1.9% increase. The next installment will be payable to shareholders of record on October 10, 2024, At $2.71 per year, based on Thursday morning's last sale, Verizon yields a beefy 6.62%.

Regulatory Issues?

CEO Hans Vestberg appeared on CNBC on Thursday morning and said, "We are very confident that this will go through, but we also expect that the process will be thorough, and we have dealt with these types of processes before."

Vestberg sees no issues with overlap as Frontier "was sort of a piece of Verizon before."

Back in 2020, Frontier purchased FIOS internet and TV infrastructure from Verizon in the Fort Wayne, Indiana, region as well as Verizon properties in 14 states at that time. Frontier also acquired the Bell System in West Virginia which was merged into the company's existing operations in that area. In short, these firms may very well complement each other.

Moving back to the present, on TV this morning, Vestberg summed things up with "It's going to take some time, so it's heads down and continue to execute on what we've done the last couple of quarters with good progress both on wireless and fixed wireless access and fiber."

Verizon's Balance Sheet

Verizon reported on July 22, 2024, and is set to report again on October 22, 2024. As of the end of that June quarter, the firm had a cash position of $2.487 billion and current assets of $38.056 billion. That included another $1.354 billion in "restricted" cash and inventories of $1.841 billion.

Current liabilities added up to $60.806 billion, including $7.163 billion in unearned revenue, but also $24.901 billion in debt due to mature within 12 months. On top of that, Verizon has another $127.496 billion in long-term debt on the books. Obviously, Verizon, even with no deal, was going to have to refinance its shorter-term debt-load at prevailing interest rates. Now, tack on more debt, unless I'm missing something, in order to get this deal done. These fundamentals are not pretty.

What about free cash flow? Any help from that direction? The firm is a cash flow beast. That much is true. Over the past 12 months, Verizon has generated $36.024 billion in operating cash flow, out of which came $16.768 billion in capex spending. That left free cash flow over a year of $19.256 billion. All good? Not really.

Out of that number, the firm paid out $11.136 billion in cash dividends (and just increased the dividend) That left $8.12 billion that going forward would have to be put towards both the deal itself and debt servicing. They'll get the deal done. I have no doubt about that. It would be much easier to do with a smaller dividend, but obviously that would hurt the stock and Vestberg is not going to go there.

My Thoughts

I do not see this deal as a reason to get long VZ shares. The math just doesn't excite me, and I don't know why or how this acquisition does more than perhaps increase cash flows. That might be huge, but that's a year and a half away.

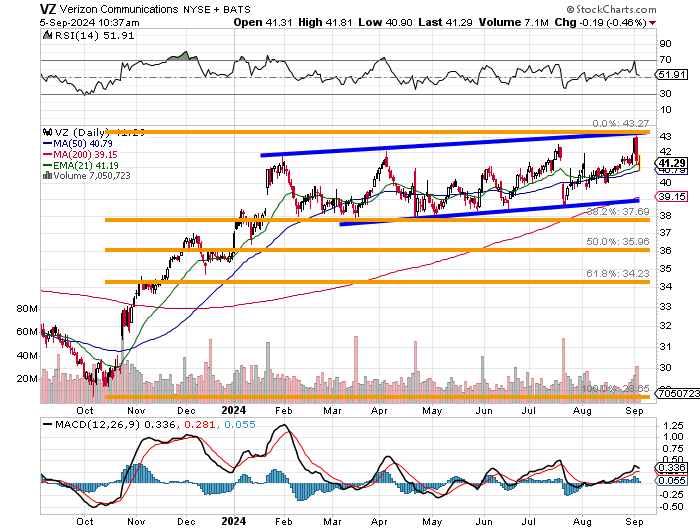

Readers will see that VZ has been mired in a narrow ascending price channel since January. Readers will also note that the 200-day SMA is currently running about $2 below the last sale and a 38.2% Fibonacci retracement level of the October 2023 to the present rally is about a buck and a half below that. What that means is that, while I don't see the stock taking off, I also see plenty of technical support. I do not expect the shares to sell off dramatically anytime soon.

The bottom line? While I do not love the deal and I do not love the balance sheet, I do love the operating and free cash flows and I do love, if I am a shareholder, the firm's commitment to the size of its dividend. No, don't buy VZ because of this Frontier deal. Don't buy Frontier because you're looking for growth. Buy VZ as a dividend stock to help line the defensive side of your portfolio. In fact, I think I'll call my Uncle Leo. He's always looking for dividend stocks to invest in.

At the time of publication, Guilfoyle had no positions in any securities mentioned.