Stanley Black & Decker Is Investable, But Not on Days Like Today

A new CEO is making clear progress with the tools and hardware leader.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Tool maker Stanley Black & Decker SWK posted the firm's second quarter financial results on Tuesday morning. For the three-month period, the firm posted an adjusted EPS of $1.09 (GAAP EPS: $-0.13) on revenue of $4.02 billion. The adjusted bottom line result beat expectations quite handily, while the top-line number reflected a year-over-year contraction of 3.4%, while meeting expectations. Gross margin improved to 28.4% from the year-ago comp of 22.4%. Adjusted, that improvement ran from 23.6% to 29.2%. Adjustments totaling $1.22 per share were made primarily for supply chain transformation costs, and other costs related to acquisition and integration. For those who do not know, but care: Stanley Black & Decker is the home to the Stanley Black & Decker, DeWalt, Craftsman and Cub Cadet brand names.

Segment Performance

- Tools & Outdoor: Generated sales of $3.529 billion (-0.03%), producing a segment profit of $316.1 million (+209.9%) on a segment margin of 9%, up from 2.9%.

- Industrial: Generated sales of $495.7 million (-19.6%), producing a segment profit of $382.9 million (+120.6%) on a segment margin of 13.5%, up from 11.6%.

Note: The firm credits its supply chain transformation and lower inventory destocking costs with the dramatic margin expansion.

Guidance

The firm is now cutting its full-year guidance for GAAP EPS to $1.60 to $2.00 from $1.60 to $2.85 due to Q2 environmental reserve adjustments. On an adjusted basis, full year EPS is now seen at $3.70 to $4.50, up from $3.50 to $4.50. Projected free cash flow got a bump up too, from $600 million to $800 million to $650 million to $850 million.

The CEO

CEO Donald Allen commented in the press release: "We extended our trajectory of solid execution on our operational priorities, which drove gross margin improvement versus the prior year and strong cash generation in the second quarter. Strength in DEWALT, outdoor and aerospace fasteners combined to yield organic growth amidst a weak consumer backdrop."

Focus

The press release also stresses that the firm's primary areas of its multi-year strategy remain advancing innovation, simplifying the organization, returning adjusted gross margin to 35%-plus and the prioritization of cash flow generation and inventory optimization.

Fundamentals

For the period reported, SWK generated $573 million in operating cash flow. Out of that came $87.2 million in capex and software spending. That left free cash flow of $485.8 million. Out of that number came $121.8 million in cash dividends paid to shareholders.

Turning to the balance sheet, SWK ended the period with a cash position of $318.5 million and inventories of $4.562 billion. That made for current assets of $6.785 billion. Current liabilities add up to $5.343 billion including $992.5 million in short-term debt and long-term debt with current maturities. While the firm's current ratio stands at an acceptable 1.27, the quick ratio stands at a wobblier 0.42.

The fact that the debt-load that will mature within 12 months outweighs the cash balance by more than three to one means that even with a redirection of that positive cash flow, the firm will have to refinance a chunk of that debt at today's interest rates.

Total assets amount to $22.454 billion, including goodwill and other intangibles of $11.802 billion. At 53% of total assets, I find that to be a bit much. Total liabilities less equity comes to $13.732 billion including another $5.604 billion in longer-term debt. Needless to say, this balance sheet is challenged. I think the firm understands this. Hence, the layered plan to improve performance across brands.

My Thoughts

Allen has been in this job since 2022. He is still kind of new, and the improvements are already visible. The balance sheet is a black eye, but cash flows were in a bad spot. Allen fixed that, and that is where remediation starts. The firm pays out a $3.28 annual dividend that yields 3.4%. I know that the firm does not want to go "there" as in "cut the dividend" to help improve the balance sheet. Reducing the debt-load through free cash flow usage is mentioned in the press release.

That said, the firm trades at 23 times forward-looking earnings and is a bit on the expensive side for a firm that has not yet corrected all that needs correcting. I think this stock is investable, but not on days like today, where there is some algorithmic buying probably with some shorts in tow due to the improved guidance.

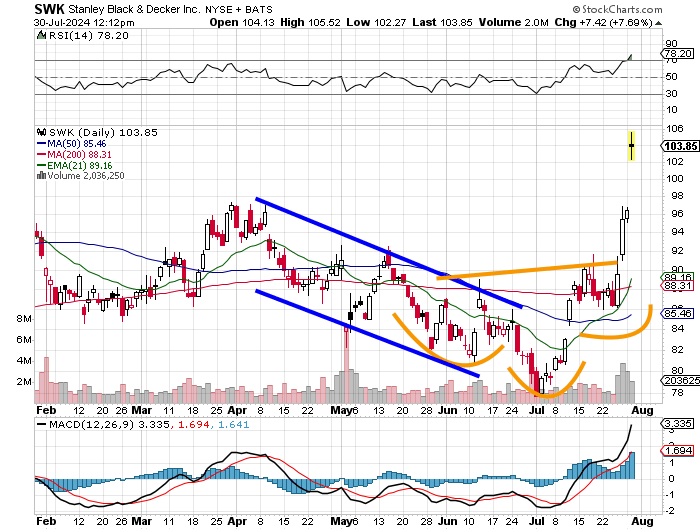

Readers will see a two-month descending price channel that morphed into an inverse head and shoulders pattern, which is a pattern of bullish reversal. Relative strength is now in technically overbought territory, The daily MACD is clearly extended. The pivot for the breakout would be a rough $91. That's already a 13.2% move past pivot. What are you going for? 15%, maybe 20%. I think long-term investors wait to see if the gap created this morning fills. For now, this may be a short-term opportunity to short a few shares. The target would be the gap fill down to the neckline of the pattern. As always, we are not willing to lose more than 8% on any position.

At the time of publication, Guilfoyle had no positions in any securities mentioned.