Pivot for T.J. Maxx Parent Could Clear Way for This Price Target

After reporting its latest numbers, TJX Companies is under some pressure.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Wednesday morning, amid the beatdown over at Target TGT and the euphoric pop over at Williams-Sonoma WSM, discount retailer TJX Companies TJX, a now long-time Sarge holding, also reported the firm's quarterly numbers. For the firm's fiscal third quarter, which ended November 2, TJX posted a GAAP EPS of $1.14 on revenue of $14.063 billion.

These top- and bottom-line numbers both beat Wall Street's expectations, while sales reflected year-over-year growth of 5.7%. Comp sales printed up 3%, which was at the high end of the previously given range. So, the stock is trading higher on Wednesday morning? Not exactly. Let's explore.

Sales by Division

- Marmaxx (U.S.) generated sales growth of 4% to $8.438 billion, as comp sales increased 2%.

- HomeGoods (U.S.) generated sales growth of 7% to $2.355 billion, as comp sales increased 3%.

- TJX Canada generated sales growth of 5% to $1.382 billion, as comp sales increased 2%.

- TJX International (Europe and Australia) generated sales growth of 16% to $1.888 billion, as comp sales increased 7%.

Note: Marmaxx includes TJ Maxx, Marshalls, and Sierra stores. HomeGoods includes HomeGoods and Homesense stores. TJX International includes TK Maxx and Homesense.

Operations

As net sales grew 5.7% to $14.063 billion, the cost of sales increased 5.3% to $9.622 billion, while operating expenses increased 6.6% to $2.748 billion. After accounting for interest, other income and taxes, GAAP net income attributable to shareholders printed at $1.927 billion, which was up 8.9% from the year-ago comp. This works out to $1.14 per fully diluted share, up from the year-ago comparison of $1.03.

The CEO

CEO and President Ernie Herrman commented in the press release: "Across the company, customer transactions drove our comp sales increases, which tells us that our values and treasure hunt shopping experience are appealing to a wide range of customers."

Herrman then added: "The fourth quarter is off to a strong start, and we are excited about our opportunities for the holiday selling season. In stores and online, we are offering consumers an ever-changing and inspiring shopping destination for gifts at excellent values and feel confident that there will be something for everyone when they shop us."

Guidance

For the current quarter, TJX continues to project comp store sales growth of 2% to 3%. Pre-tax profit margin is seen at 10.8% to 10.9%, producing a GAAP EPS of $1.12 to $1.14, which is up sharply from prior guidance of $0.88 to $0.90. The only problem for traders would be that Wall Street already knew the guidance had to come up and was looking for something around $1.18.

For the full year, TJX sees comp store sales growth of 3%, with a pre-tax profit margin of 11.3%. This should put full year GAAP EPS at $4.15 to $4.17. Again, this was up from prior guidance of $4.03 to $4.09, but at the midpoint missed the $41.7 that Wall Street had in mind by a penny.

Fundamentals

For the three-month period reported, the firm generated $1 billion worth of operating cash flow and returned $997 million to shareholders in the forms of dividend payouts and share buybacks. Nine months into the fiscal year, TJX has generated operating cash flow of $3.412 billion. Out of that came $1.404 billion in capex spending. This left a nine-month free cash flow of $2.008 billion. Out of this total (and beyond), TJX has repurchased $1.661 billion in common stock for its treasury and paid out $1.226 billion in cash dividends to shareholders.

Turning to the balance sheet, TJX ended the period with a cash position of $4.718 billion and merchandise inventories of $8.371 billion. This puts current assets at $14.352 billion. Current liabilities add up to $12.017 billion. There is no short-term debt on the books. That puts the firm's current ratio at 1.19, which is not bad in any industry, but really rocks among large retailers. We don't follow quick ratios very closely across this industry due to the inventory-focused nature of the business.

Total assets amount to $32.436 billion, including just $95 million worth of goodwill and no other intangible assets listed. Obviously, that is squeaky clean in my book. Total liabilities less equity comes to $24.263 billion. This does include long-term debt of $2.865 billion, which is something that the firm could take care of out of pocket if need be. This balance sheet is solid gold, especially when one considers that TJX is primarily a brick-and-mortar retailer.

My Thoughts

OK. Maybe I'm a little biased. The quarter was solid. The guidance was strong, even if Wall Street was looking for slightly more. Cash flows are strong. These flows may have to be better allocated in the future but that is not today's issue. The balance sheet is a work of art for a large retailer.

TJX is possibly the best at what it does. The firm purchases overstocked items or last year's styles from the higher-end retailers at bulk and sells apparel, home goods and other items to budget-conscious consumers at what are discounted prices. Companies like TJX do well during tough times for consumers as this is one of the chain retailers that these consumers will flock to.

Times haven't been that tough, you say. That's true, if most of the people in your circle provide to their households upper-middle- to upper-class incomes. Inflation over the past three years has absolutely crushed the middle-, lower-middle- and lower-income classes and they still need clothing, and they still have to dress their children. That's where TJX comes in.

TJX is slightly expensive at 25-times forward-looking earnings relative to the S&P 500, which is close to 22-times. That said, Walmart WMT trades at 32-times and Burlington Stores BURL trades at 28-times. These are not apples-to-apples peers of TJX, but they are firms that specialize in catering to the budget conscious.

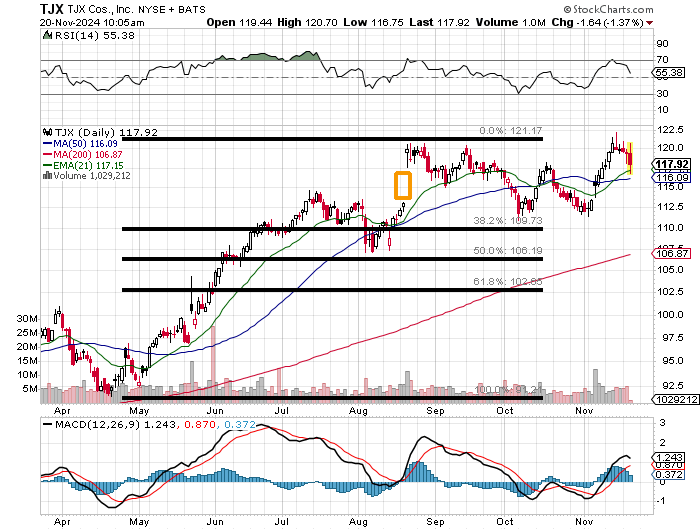

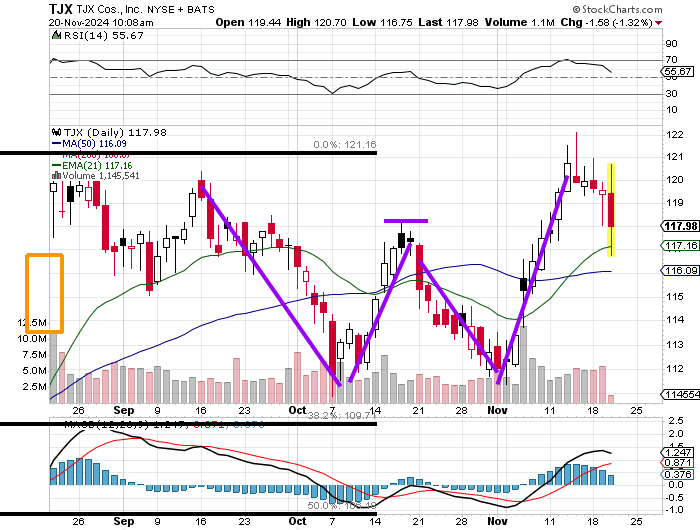

Readers will see that TJX rallied from late April into mid-August. The resistance formed at that spot has developed into the top end of the range for a period of basing consolidation. Support for that range developed at the 38.2% Fibonacci retracement level of that move. Let's zoom in a bit:

A double bottom has formed within this basin period with a $118 pivot. This pivot is currently under some pressure this morning. Should the stock fail to hold that line or at least close above it, that would be a technical negative. Relative strength is falling but still above average. The daily MACD is also easing a bit, but still bullishly postured. The $118 level is key.

What Am I Going to Do?

Should the stock fail at $118, I'll give it until it cracks its 50-day SMA (just like every other portfolio manager) and peel off a few shares. Should the stock bottom this week above that 50-day SMA, this is a buying opportunity. There is nothing in this report on Wednesday that discouraged me as an investor. The $118 pivot, if it stands, allows for a $141 target price.

At the time of publication, Guilfoyle was long TJX and WMT equity.