Nu Skin in the Game?

The stock of this small-cap hasn't aged well so far, but I can see a strong foundation and how it could shape up.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Let's take a look at Utah-based Nu Skin Enterprises NUS, a publicly traded small-cap corporation whose stock traded under $10 ... so, right up our alley. The company has sold off since mid-2021 — back when it was worth about six-times more.

But maybe it's not as bad as it looks. Let me explain why this is one to keep on your radar.

Nu Skin Enterprises develops and distributes a broad portfolio of beauty and wellness products across roughly 50 global markets, including China, South Korea, Japan, Hong Kong, Taiwan, Europe and the Middle East and Africa.

Nu Skin has three brand names: The Nu Skin brand focuses on beauty, while the Pharmanex brand focuses on wellness, and the ageLOC brand focuses on slowing down the negative impacts of aging. Nu also runs a strategic investment business, Rhyz, that runs two segments of its own Manufacturing and Rhyz Other.

Earnings Ugliness

In early August, Nu Skin posted second quarter earnings, revealing an adjusted earnings per share of $0.21 (unadjusted loss per share of $2.38) to the tape on revenue of $439.081 million. That compares to an unadjusted EPS of $0.54 for the year-ago period on revenue of $500.257 million (note: Nu did not need to adjust a year ago and only gave GAAP EPS). Sounds awful.

What amounted to a year-over-year revenue contraction of 12.2% led to a sizable reduction in profitability, even on an adjusted basis. The adjustment mentioned was made for the purposes of restructuring costs and impairment charges. Still sounds awful. I hear ya.

Guidance: Hard to Look At

In early August, as Nu Skin released those earnings, it gave guidance for the current quarter, with revenue at $430 million to $465 million (contraction of 14% to 7%) leading to unadjusted EPS of $0.08 to $0.18 or an adjusted EPS of $0.15 to $0.25. Wall Street, at the time, had been looking for revenue of about $460 million, and adjusted EPS of roughly $0.42. So, third-quarter guidance was light.

For the full year, Nu projected revenue of $1.73 billion to $1.81 billion (contraction of 12% to 8%), leading to an unadjusted loss of $2.01 to a loss of $1.81 or adjusted EPS of $0.75 to $0.95. Consensus view on Wall Street had been for revenue of $1.77 billion and adjusted EPS of $1.10. So, full-year revenue guidance was actually in line with Wall Street, but adjusted profitability for the full year as well as for the third quarter, was not up to the standard set.

Upcoming Earnings

Third-quarter earnings ending in late September, will not be reported until early November. Right now, after adjusting to Nu's own guidance, Wall Street (which amounts to three analysts) is looking for a print for adjusted EPS of $0.20 on revenue of $440 million. That would be a top-line contraction of 15%, below guidance.

From the CEO ...

Nu Skin President and CEO Ryan Napierski said, "As our core Nu Skin business continues to navigate the macro-economic environment, we were encouraged by sequential gains in several of our markets including the U.S. and most of Southeast Asia/Pacific. Additionally, our Rhyz business grew 32 percent versus the prior-year quarter led by strong performances in our Mavely affiliate platform and manufacturing companies."

Napierski added, “We are enhancing our developing market strategy including a revised business model, targeted product offering and streamlined operating infrastructure beginning with Latin America and parts of Southeast Asia in the second half. In addition, we are intensifying our plans to enter India with a proprietary business model that will be a catalyst for expansion into other emerging markets. We are also exploring integrated brand building initiatives, including digital marketing and third-party marketplaces, as we strive to be wherever our customers seek to find us.”

Fundamentals

Over the trailing 12 months as of the end of June, Nu Skin generated operating cash flow of $159.7 million. Out of that number came capital spending spending of $52.7 million, leaving free cash flow of $107 million. Out of that, it paid out $44.7 million in cash dividends to shareholders and paid down $53.2 million in debt.

Looking at the balance sheet, Nu Skin ended June sitting on a cash position of $242.4 million and inventories of $244 million. That put current assets at $654.4 million. Current liabilities added up to $308.6 million including just a small amount of shorter-term debt ($30 million) and unearned revenue ($11.8 million). This left Nu Skin with a current ratio of 2.12 and a quick ratio of 1.33. Those are both very strong ratios, especially for a smaller company going through a restructuring period.

Total assets amount to $1.586 billion, including goodwill and other intangibles of just $188.4 million. At less than 12% of total assets, this is no issue whatsoever. Total liabilities less equity comes to $899.8 million, including long-term debt of $428.3 million.

My Take

The stock has relentlessly sold off since mid-2021. We're talking about a $60 stock if we go back that far. The business is clearly in decline. Nu Skin seems to understand this and is trying to evolve where it is and grow where it is not.

Cash flows are still positive and the balance sheet, at least the current situation is much stronger than one probably suspects when looking at this stock. Long-term debt is a bit much, but not out of control and the company has demonstrated over the past year a commitment to paying it down.

Lastly, Nu Skin still pays a quarterly dividend of $0.06 per share, which is down from 2023, but not nothing. This works out to an annual yield of 3.3%.

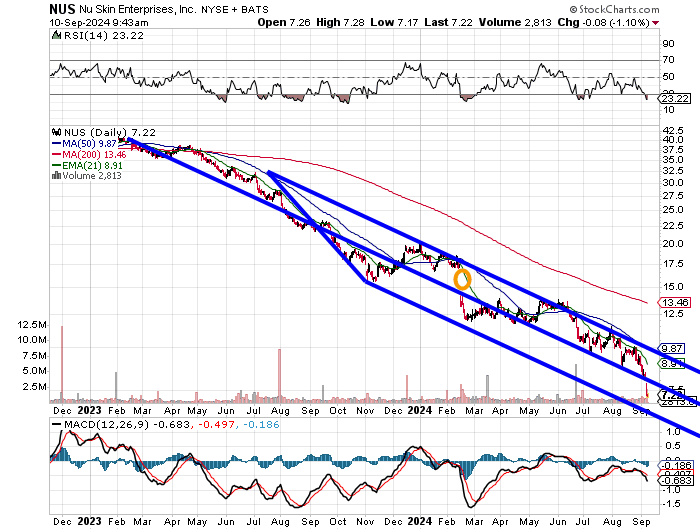

Not much we can do with this chart. The Andrews Pitchfork model I drew up for you goes back to the start of 2023. The stock has not broken out of the model one way or the other. There remains an unfilled gap between $15 and $17 from early 2024.

The daily Moving Average Convergence Divergence indicator is still bearish. The reading for Relative Strength looks technically oversold. Typically, the stock gets a minor pop when that happens for the traders.

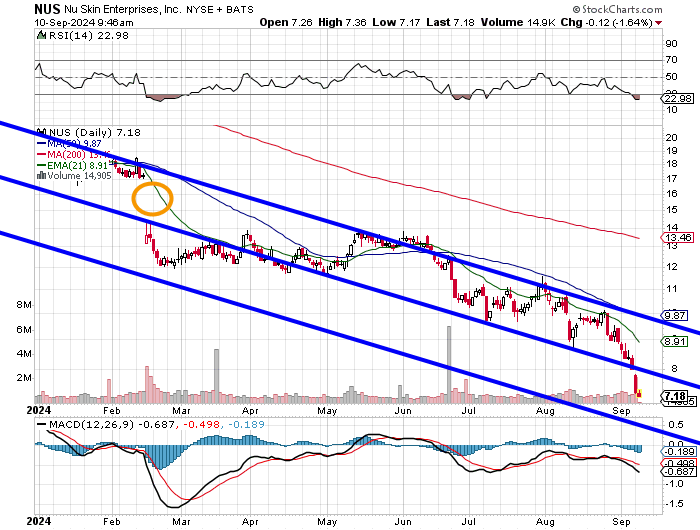

Let's zoom in:

The stock now trades at 9-times forward looking adjusted earnings with a solid balance sheet and positive cash flows. That's cheap. For the investors ... I don't know when and where. This chart still has secrets, but I don't think this one is going out of business.

There are fundamental reasons to invest in this name. For me, I have not decided yet whether I want that to be ahead of, or after earnings. This is definitely one, in my opinion, to put on your radar, or in the parlance of the "Stocks Under $10" portfolio, in the bullpen.

At the time of publication, Guilfoyle had no position in any security mentioned.