More Than a Meme? Don't Bury GameStop Just Yet

For a company without a healthy business, GameStop is spectacularly well-managed. Even while burning cash, it was profitable this past quarter and broke even the quarter prior to that.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

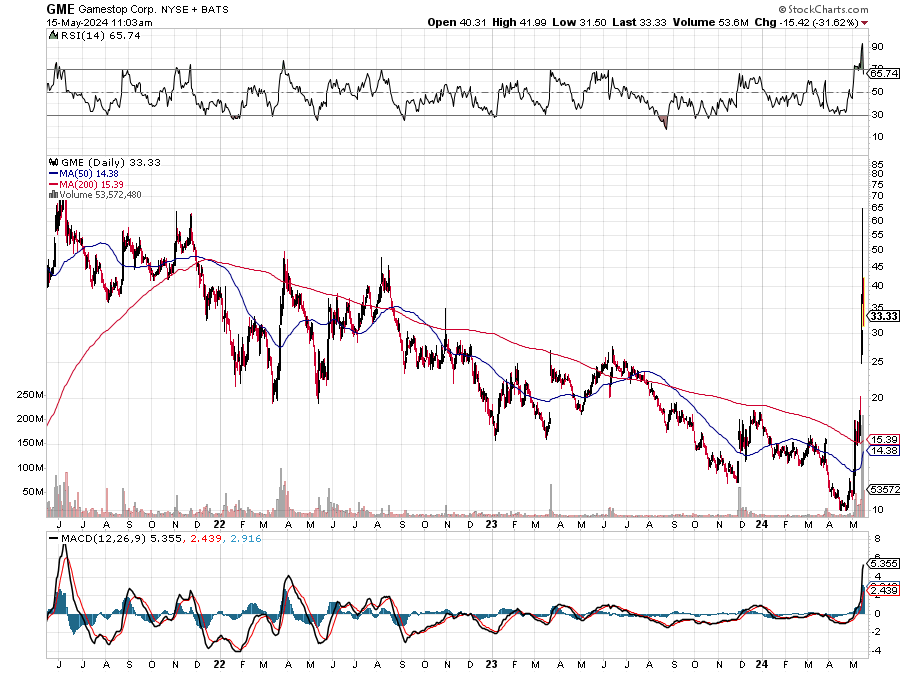

You knew it had to happen. The weasel went pop. GameStop GME was down about 30% at last glance on an "up" tape. Is it over? Has it been GameStopped?

I was playing this game on the AMC Entertainment AMC side. Already took profits on half of my position. The rest is nicely hedged. I won't get rich on this one, but I won't lose money either.

What about GameStop though? Fundamentally speaking, AMC is a hot mess. In addition to the hot mess, every time the stock pokes its head up, the company issues more shares, thus further diluting the equity and forsaking its beloved apes who have been so loyal. GameStop has been quiet though.

The stock pops. We don't hear from the company. CEO Ryan Cohen of Chewy CHWY fame is famous for avoiding the media and even avoids holding earnings calls after the release of its quarterly numbers.

The GameStop business is a mess. Sure. The company historically sells video games and video-game paraphernalia. Well, kids don't go to physical stores to buy physical video games anymore.

The company has tried to evolve into something else. Collectibles. NFTs. Nothing has really taken. Still, GameStop is probably much sounder fundamentally than most folks think. The books, in the case of GameStop, are as clean as a whistle.

Can GameStop return to prominence? Not as what they were, no. That said, I would not start digging out a spot in the graveyard just yet.

Earnings Coming

GameStop is expected to report its first-quarter earnings during the first week of June. Expectations are currently for an adjusted loss per share of $0.09 on revenue of $1.05B. That would be "good" for a year-over-year contraction in revenue generation of another 11.5%. From what we've heard, the company is in cost-cutting mode, including reductions in headcount.

Going back to March 26, GameStop reported adjusted EPS of $0.22 (GAAP EPS: $0.21), which missed expectations quite badly, on revenue of $1.79B. The revenue print also fell short of consensus, while reflecting a year-over-year contraction of $19.7%.

Looking ahead, analysts are projecting that revenue contraction drops to roughly 5% by this coming October quarter and almost incredibly... consensus is for adjusted profitability by the January 2025 quarter. That's not really that far off.

Operations

For the most recent quarter, as revenue contracted 19.7%, the cost of sales contracted 20.4% to $1.374B. That left a gross profit of $419.2M (-16.1%), as gross margin widened from 22.5% to 23.4%. General and administrative expenses dropped 20.8% to $359.2M. This left operating income of $55.2M (+19.5%) as operating margin improved from 2.1% to 3.1%.

After accounting for interest, and taxes, net income landed at $63.1M, up 30.9% from the year-earlier comparison. This works out to a GAAP EPS of $0.21 versus last year's $0.16.

Fundamentals

Obviously the most recent fundamental financial information that we have for GameStop is for the February 2024 quarter. For the trailing 12 months at that time, GameStop generated operating cash flow of -$203.7M. Tack on capex spending of $34.9M, and that makes for a free cash flow of -$238.6M. Not so hot. As far as 12-month periods go, this was not quite as good as January 2023, but far better than January 2022.

Looking at the balance sheet, as of February, GameStop has a cash position of $1.199B and inventories of $632.5M. This put current assets at $1.974B, Current liabilities added up to $934.5M, including short-term debt of just $10.8M, but unearned revenue of $283.6M. That puts the headline current ratio at 1.28 and a quick ratio of 0.61.

Remember, we don't hold retailers to the same standards when figuring quick ratios as we do other industries due to the inventory-reliant nature of that business. I show it here because I truly do not know what GameStop's inventories are worth. Are some inventories outdated video games? I don't know.

That said, there is a healthy enough entry for unearned revenue, which as we know, is not a true financial obligation. Adjusted for unearned revenues, the company's current and quick ratios rise to 1.84 and 0.87, respectively. These ratios are likely far stronger than most financial news consumers likely realize.

Total assets amount to $2.709B. GameStop claims no value for intangible assets, which we appreciate. Total liabilities less equity comes to $1.37B, including just $17.7M in long-term debt. The largest liability, by far, is for capital leases. Should the business evolve from physical retail into something online more effectively than they have to date, these liabilities will start to disappear.

That said, you read that right. GameStop has a cash position of $1.199B, runs with a debt-load of just $28.5M and burnt $238.6M in cash over the past 12 months. GameStop can't do that forever, but the goose is nowhere near cooked.

My Thoughts

Of course, GameStop is a tough sell. The stock trades at a ridiculous multiple. However, even while burning cash on an annual basis, the company was profitable this past quarter and broke even the quarter prior to that.

Given that there is close to no debt on the books and a beefy cash position, the cash burn, even if chronic, can go on for two to three more years before this business would have to rely on a credit facility of some kind or sell notes in order to fund itself. For a company without a healthy business to lean on, GameStop is a spectacularly well-managed corporation.

Nice chart. Would you invest in GME here? I don't think so. Would you pay the last sale ($33) for 100 shares, if you could sell one $35 call expiring this Friday for $5 and sell or write one $23 put expiring this Friday for another $1? You might.

It's still gambling, but a net basis of $26 is a whole lot better than a net basis of $33. Then again, a more timid trader could write one June 21 $15 puts for close to $2. That's a whole lot safer.

At the time of publication, Stephen Guilfoyle was long AMC equity, long AMC puts, short AMC calls.