GE Crushes It Thanks to CEO Larry Culp: Is It Time to Buy?

General Electric appears well positioned to launch GE Aerospace and GE Vernova as independent companies in the beginning of the second quarter.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

General Electric reports... Or should I say, the new "GE" reports.

On Tuesday morning, General Electric GE released the firm's third quarter financial results. For the three month period ended September 30th, GE posted an adjusted EPS of $0.82 (GAAP EPS: $0.23, continuing EPS: $0.08) on revenue of $17.346B. Both the adjusted earnings print and sales number absolutely crushed expectations with those revenues being good enough for year over year growth.

Within the firm, across all segments, the sale of equipment increased 21% to $6.939B as the cost of those equipment sales increased 8.9% to $7.065B, leaving an equipment driven gross profit/loss of $-126M. The sale of services increased 18.2% to $9.565B as the cost of selling those services increased 15.7% to $5.839B. That left a services driven gross profit/loss of $3.726B.

After figuring for more items than you can shake a stick at such as operating expenses, separation costs, insurance losses, earnings from discontinued operations interest and taxes, net earnings attributable to shareholders came to $258M, or $84M from continuing operations and $173M from discontinued operations.

Segment Performance

GE Aerospace orders increased 34% to $9.793B, producing revenue of $8.409B (+25%), which resulted in a segment profit/loss of $1.712B (+33%) on segment margin that improved from 19.1% to 20.4%.

Renewable Energy orders increased 5% to $3.918B, producing revenue of $4.151B (+15%), which resulted in a segment profit/loss of $-317M (up from $-934M) on segment margin that improved from -26 to -7.6%.

Power orders increased 2% to $4.257B, producing revenue of $3.974B (+13%), which resulted in a segment profit/loss of $238M (+69%) on segment margin that improved from 4% to 6%.

Note: Upon separation, GE Aerospace will stand alone, while retaining the GE legacy and ticker symbol. Renewable Energy and Power will be combined to form GE Vernova and upon separation will trade under the ticker symbol GEV. Readers will recall that back in January, GE HealthCare was separated from GE and has traded under the ticker symbol GEHC ever since.

Guidance

With three quarters in the books, GE has adjusted full year 2023 guidance taking organic revenue growth to the "low teens" from "low-double-digit." The firm took full year adjusted EPS to $2.55-$2.65 from prior guidance of $2.10-$2.30 and well above the Wall Street consensus of $2.35. Free cash flow for the year is now seen at $4.7B to $5.1B, up from prior guidance of $4.1B to $4.6B.

As if separated, GE Aerospace is seen growing organic revenue in the low 20%'s up from "high teens to $20%" three months ago, with operating profit at roughly $6B, up from prior guidance of $5.6B to $5.9B. Free cash flow is seen trending "even better" up from prior guidance of "up y/y".

Also, as if separated, GE Vernova (Power & Renewable Energy) is seen growing organic revenue in the high-single-digits, up from the middle-single-digits, producing an operating profit/loss of $-0.3B to $0.1B, which is up from prior guidance of $-0.4B to $0.1B. Free cash flow here is still expected to be flat to slightly improved as it has been seen all year long.

Fundamentals

For the quarter reported GE generated operating cash flow of $1.888B. Out of that came CapEx of $402M, and insurance costs, separation cash expenditures, restructuring cash expenditures and taxes related to business sales of $279M, leaving free cash flow of $1.672B. For the first nine months year to date, free cash flow amounts to $2.189B. Out of that came the repurchase of $945M worth of common stock for the firm's treasury and $501M in cash dividend payments to shareholders.

Taking a look at the balance sheet, GE ended the quarter with a cash position of $20.181B and inventories of $17.02B. This puts current assets at $56.434B. Current liabilities add up to $48.164B, including short-term debt of just $1.33B. That leaves the firm with a current ratio of 1.17 and a quick ratio of 0.82. These ratios are acceptable given the nature of the business. The cash position is understated as well, which I will explain.

Total assets amount to $156.662B, including goodwill and other intangibles of $18.967B. At 12% of total assets this is fine. Also included in total assets are another $35.528B in investment securities not labeled as current, so they don't count as cash. Clearly, these assets are saleable if the firm needed the dough and that would take both the firm's cash position and current assets up to $55.709B and $91.962B, respectively. Now that's the stuff of a fortress-like balance sheet. Total liabilities less equity comes to $126.83B, including $19.488B in longer-term debt and insurance liabilities of $35.832B.

The firm can easily take care of the short-term debt without having to refinance and with the level of cash/investment securities held, as the longer-term paper matures, those decisions can be made when necessary. This is a rock solid balance sheet. Yes, I am talking about GE. CEO Larry Culp has done the job of a titan with this firm. I can not say enough, how competent his leadership has been after the clown show that preceded his tenure. No, that is not a shot at John Flannery who was simply in over his head. Yes, that is a shot at Flannery's predecessor.

The CEO

GE Chairman and CEO and GE Aerospace CEO Larry Culp commented in this morning's press release:

"GE delivered another quarter of very strong results with double-digit growth in revenue, profit, and cash. At GE Aerospace, we continue to experience rapid growth driven by robust demand and solid execution, largely in Commercial Engines and Services. At GE Vernova, our Grid and now Onshore Wind businesses were both profitable this quarter and we expect their performance to continue to improve. With our two largest Renewable Energy businesses delivering and Power's continued strength, we remain highly confident in GE Vernova's spin-off next year."

On separating the firm going forward.... "Based on our year-to-date results and continued momentum in the fourth quarter, GE is raising full-year 2023 guidance.

We're well-positioned to launch GE Aerospace and GE Vernova as independent companies in the beginning of the second quarter. I'm more excited than ever about our path ahead."

My Thoughts

I just noticed that in response to these earnings, Andrew Tobin, who is a five star rated analyst at Bank of America has reiterated his "buy" rating and $135 target price for GE. I like GE. No, I don't own it. Let me correct what I meant to say. I like GE Aerospace a lot. After the break-up, that's where Culp will be and that is obviously the one segment of this firm where there is growing demand for what they provide.

GE Vernov might be a tough sell. You could have another Kenvue KVUE on your hands there. Kenvue ticked at just below $28 per share back in May after spinning off from Johnson & Johnson JNJ and now trades with a $19 handle. That said, JNJ has gone from trading with a $175 handle in August to trading close to $151 this morning. Maybe not such a great comparison.

Still, it's obvious that GE Aerospace is the crown jewel of all of the components and former components that once made up a very sloppy conglomerate. May have to initiate ahead of the split next year in order to get the shop that Culp is going to run and hope the other half of the split at least holds its own.

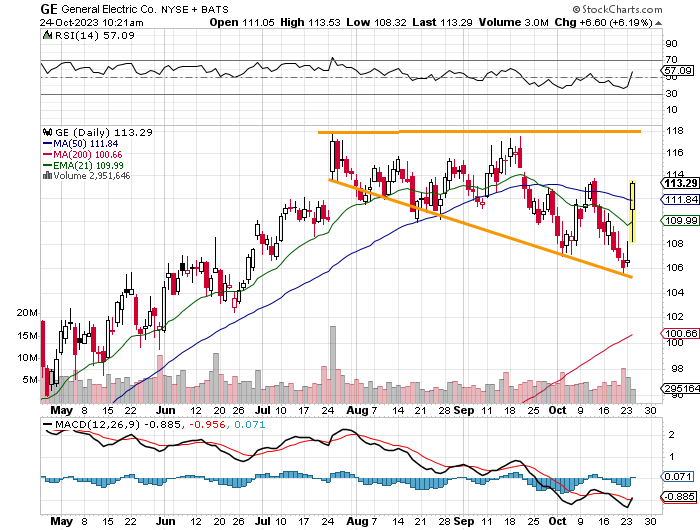

What you have here is a right angled broadening descending pattern. As the stock has popped, relative strength has improved and the daily MACD (moving average convergence divergence) at least looks less bad, is it time to get long GE?

The old adage says that one buys on the third touch of the descending line as this pattern is thought of as a pattern of reversal. Friday's low may have been the third touch, but it really looks like the fourth to me, which could mean that this rally is overdue. Could also mean that I am misreading the pattern.

I'll tell you what. IF GE holds the 50 day SMA (simple moving average) for more than just today, it probably is time to get involved. I'll initiate small and pay attention going into year's end. Should the 50 day line fail? Well then I head back to the downward trending line of support and wait for another shot. One can still get paid about $2.50 for one January $105 put if one wants to get paid to wait.

At the time of publication, Stephen Guilfoyle had no position in the securities mentioned.