An Encouraging GE Turnaround Continues

After GE Aerospace's latest report, we've got a new price target and guidance for this surging stock.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Tuesday morning, GE Aerospace GE released the firm's second quarter financial results. Just a reminder: GE Vernova GEV was spun-off on April 2, 2024, and will report that firm's own earnings tomorrow morning. For the three-month period ended June 30, 2024, GE Aerospace posted a (continuing) GAAP EPS of $1.20 on an adjusted revenue of $8.223B. Adjusted revenue? Yes. GE Aerospace did provide both adjusted and GAAP data, where both the adjusted and GAAP EPS printed at $1.20, but the route taken to get there differentiated.

Total GAAP revenue came to $9.094 billion, but that included insurance and non-operating benefits. The EPS print(s) easily beat the $0.98 that Wall Street was looking for, but the "adjusted" revenue print fell a couple hundred dollars short of consensus view. That number was, however, good for year-over-year growth of 4% when isolating the aerospace business for last year. Encouragingly, total orders increased 18% to $11.2 billion.

Comments From the Chairman and CEO

CEO Larry Culp commented in the press release, "The GE Aerospace team delivered another strong quarter marked by double-digit increases across orders, operating profit, and free cash flow. Given our performance year-to-date and momentum across our businesses we are raising our full-year profit and free cash flow guidance."

Culp then added: “We are accelerating our actions and leveraging FLIGHT DECK to unlock supply constraints and fully meet customer demand. I am confident that advancing our strategic priorities for today, tomorrow and the future, will enable us to meet the needs of our customers and create exceptional value for shareholders."

About That Guidance

For the full year, GE Aerospace now sees adjusted revenue growth in the high single digits (percentage-wise), down from April's vision of low double-digits plus. Other than that, it's all positive. Operating profit is seen at $6.5 billion to $6.8 billion, up from April's guidance of $6.2 billion to $6.6 billion, as adjusted EPS is now seen at $3.95 to $4.20. That's up from April's projection of $3.80 to $4.05. Free cash flow for the full year is seen at $5.3 billion to $5.6 billion, up from April's vague guidance of something greater than $5 billion.

Segment Performance

- Commercial Engines & Services generated revenue of $6.132 billion (+7%), on orders worth $9.152 billion (+38%), producing a segment profit of $1.679 billion (+21%) on a segment margin of 27.4% (+320 bps).

- Defense & Propulsion Technologies generated revenue of $2.401 billion (+1%), on orders worth $2.334 billion (-25%), producing a segment profit of $344 million (+71%) on a segment margin of 14.3% (+580 bps).

Fundamentals

GE generated operating cash flow of $957 million for the period reported. Tack on $407 million in cash separations and $29 million in restructuring expenditures, then carve out capex spending of $295 million, and the firm was left with free cash flow of $1.098 billion. For the first half of the year, GE Aerospace has generated free cash flow of $2.767 billion. Over that time frame, the firm has repurchased $2.623 billion worth of common stock for its treasury, while dishing out $394 million in cash dividend payments to shareholders. I like what the firm is doing here. I would prefer to see returns to shareholders brought down to 100% or less of operating cash flow.

Glancing at the balance sheet, GE ended the quarter with a cash position of $15.445 billion and inventories of $9.469 billion. That puts current assets at $37.352 billion. Current liabilities add up to $32.75 billion, including short-term debt of $1.7 billion. The firm now has a current ratio of 1.14 and a quick ratio of 0.85. These ratios more than just barely pass muster for a large industrial firm and are a testament to how far Culp has taken GE.

Total assets amount to $123.19 billion, including goodwill and other intangibles of $13.253 billion. At less than 11% of total assets, this is not a problem. Total liabilities less equity comes to $104.347 billion. This does include $17.973B billion in longer-term debt, which I would like to see whittled down a bit with that free cash rather than repurchase as many shares for the treasury as the firm has. I am naturally conservative. That does not mean that this is not a strong balance sheet, nor that Culp is doing it wrong. He most certainly is not.

My Thoughts

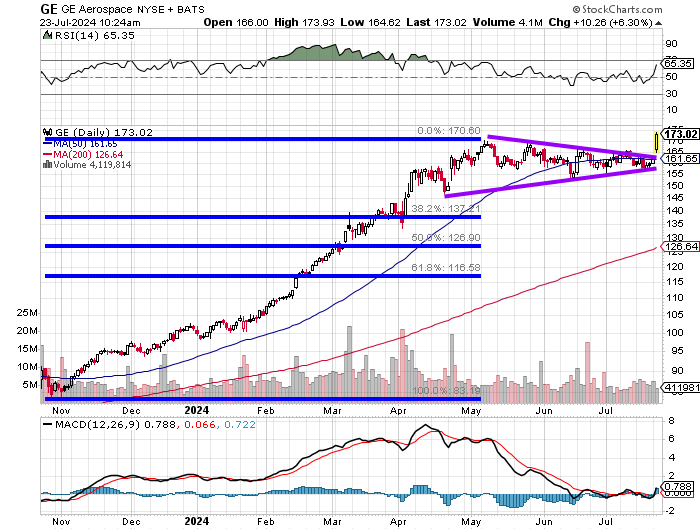

Culp continues to make something great out of something that was far from it a few years ago. The positive free cash flow and the expectation for a continuance of the ability to produce in that manner is a key weapon in the creation of this stock's future and sustainable success. Today, the stock is breaking out. Let's take a look.

The 103% rally from the lows of November 2023 to the highs of May 2024 are not a flagpole and the basing period of consolidation from May into July is not a bear flag. These patterns are too elongated for that, but we are seeing a similar response to positive news coming out of that kind of set-up. Replace "bull flag" with "pennant" and we have a ball game.

Relative strength that had been weakening is experiencing some reborn pop this morning. The daily MACD has just seen a bullish curl with the 12-day and 26-day EMA and the histogram of the nine-day EMA all in positive territory. Consider the 50-day SMA that had become a magnet for the last sale for this stock as pivot. From there, we try to map out this breakout.

GE Aerospace (GE)

- Target price: $193

- Pivot: $161 (50-day SMA)

- Add: Below 4170 down to pivot

- Panic: Loss of 50-day SMA or 8% loss

At the time of publication, Guilfoyle was long GE equity.