My Largest Holding Is Cooking With Gas and I've Got a New Plan

CrowdStrike is my "best in class" for this sector and I've got a new plan for this holding after a strong earnings report.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

If you follow me, then you know that CrowdStrike CRWD is a personal favorite and you know that I refer to CrowdStrike as the "best in class" cybersecurity business, a moniker that I had once used to describe Palo Alto Networks PANW.

If you follow me, then you know that I added on weakness last week. You also know that I got more aggressive in CrowdStrike once Zscaler ZS reported positive earnings and CRWD continued to sell off. I was so confident going into last night's earnings that, as of this writing, CRWD is my largest holding by a wide margin. If you know me, it has been years since Microsoft MSFT did not hold the top spot. Yes, I will take some profits in CRWD this morning and return that name's weighting upon my book to something more reasonable, but this name will remain a top holding of mine for the foreseeable future.

That said, the shares are selling off of the early morning highs rather quickly since the open. I may not have to take that haircut.

CrowdStrike Saw an Overnight Surge

On Tuesday afternoon, CrowdStrike reported the firm's fiscal first quarter financial results. For the three-month period ended April 30, the firm posted an adjusted EPS of $0.93 (GAAP EPS: $0.17) on revenue of $921.036 million. These top- and bottom-line results both beat Wall Street's expectations, while the sales print was good for year-over-year growth of 33%. Of the $0.75 per share adjustment, $0.73 were for the purpose of share-based compensation expense.

At the period's end, annual recurring revenue (ARR) grew 33% to $3.65 billion, while net-new ARR grew 22% to $212 million. These two numbers as much as the headline beats are what is driving the stock's overnight surge in its share price. For the period, CrowdStrike set new firm records for both operating and free cash flows, which we will get to down below.

Reviewing CrowdStrike's Operations

As seen above, revenue generation grew 33% for the period. Within that number, subscription-based revenue increased 33.9% to $872.172 million as revenue generated by professional services grew 18% to $48.864 million. The cost of this revenue grew 33% as well to $225.003. This left a gross profit of $696.033 million on a gross margin of 79.8%. Subscription-based gross margin came to 78% or, once adjusted, 80%.

Operating expenses increased by 27% to $697.097 million, leaving a GAAP operating income of $6.936 million, up from $-19.456 million. On an adjusted basis, operating income increased from $115.879 million a year ago to $198.74 million. After accounting for interest, taxes and other income, GAAP net income increased from the year ago comp of just $491,000 to $42.82 million of $0.17 per diluted share. On an adjusted basis, net income increased from the year ago comp of $136.36 million to $231.666 million, or $0.93 per diluted share.

CrowdStrike Is Beating Wall Street Expectations

For the current quarter, CrowdStrike sees revenue generation of $958.3 million to $961.2 million. This took the low end of the range above the consensus view for about $955 million and would also keep sales growth above 30%. Adjusted operating income is seen at $208.3 million to $210.5 million, adjusted net income is seen at $245.7 million to $247.8 million. That would put the adjusted EPS at $0.98 to $0.99.

For the full year, CrowdStrike sees total revenue at $3,967.3 billion to $4,010.7 billion versus consensus for about $3.97 billion. That too would keep growth above 30%. The firm sees full-year adjusted operating income of $890.1 million to $916.5 million and full-year adjusted net income at $985.6 million to $1.012 billion. This would produce a full-year adjusted EPS of $3.92 to $4.03. Wall Street was looking for $3.91.

Reviewing CrowdStrike Fundamentals

For the period reported, CrowdStrike generated operating cash flow of $383.228 million (+27.4%). Out of that number came capex spending of $49.683 million and capitalized internal use software development costs of $10.479 million, leaving free cash flow of $323.066 million (+42.1%). The firm does not return capital to shareholders.

Turning to the balance sheet, CrowdStrike ended the period with a cash position of $3.702 billion and current assets of $4.842 billion. Current liabilities add up to $2.684 billion, including no short-term debt, but an incredible $2.309 billion in deferred revenue which is not a true financial obligation. The firm's current ratio stands at a healthy 1.8, but once the ratio is adjusted for those deferred revenues, rises to an absurdly robust 12.9.

Total assets amount to $6.842 billion, including goodwill and intangibles of $843.997 million. At 12.3% of total assets, this is not an issue. Total liabilities ex-equity comes to $4.273 billion. This does include long-term debt of $742.866 million and another $760.05 million in deferred revenue. One, the firm could pay off that debt-load roughly five times over out of cash, and two, that's almost $1 billion worth of deferred revenue. This business is cooking with gas, and this is one heck of a strong balance sheet.

Highly-Rated Analysts Rate CrowdStrike a 'Buy'

Since these earnings were released last night, I have come across 17 highly-rated (4+ stars at TipRanks) sell-side analysts that have opined on CRWD. All 17 of these analysts rate the stock as a "buy" or buy-equivalent. Across the 17, the average target price is $401.29 with a high of $435 (Andrew Nowinski of Wells Fargo) and a low of $350 (Shrenik Kothari of Robert W. Baird). Once removing these two as potential outliers, the average target across the remaining 15 rises to $402.47.

After This Sale, CrowdStrike Remains a Top-Five Holding

Once again, CrowdStrike has posted an excellent quarter, with beats for sales, earnings and annual recurring revenue. The firm also exceeded expectations in its forward guidance. Is there any doubt that CrowdStrike is cybersecurity's "best in class"?

You did see those cash flows and that balance sheet. Maybe Zscaler rises as a near peer, but in my opinion, nobody is on CrowdStrike's level. I will remain long this name, as well as SentinelOne S as far as this space is concerned.

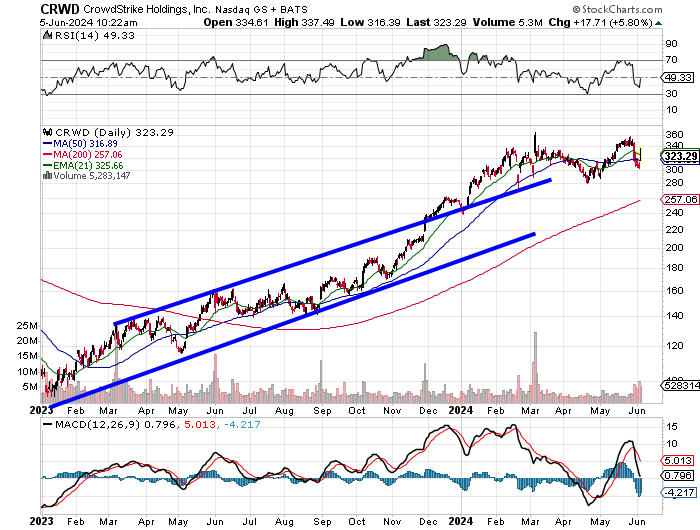

Readers will see the price channel that remained mostly intact and took CRWD higher for basically all of 2023. Then something funny happened. Let's zoom in:

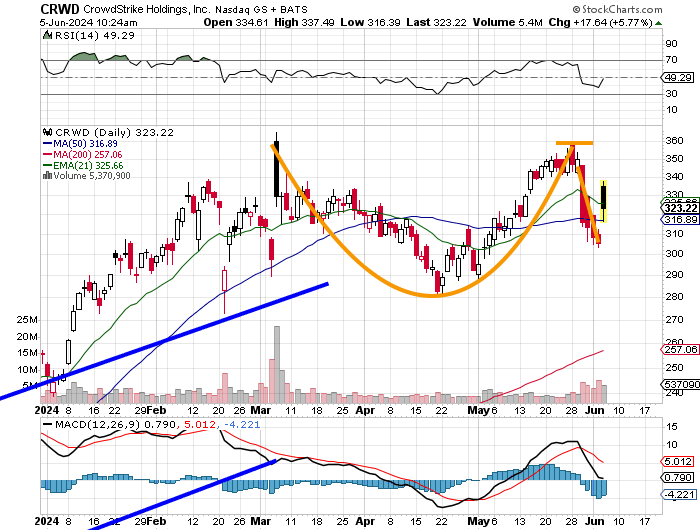

CRWD has developed a cup-with-handle pattern beginning with the highs of early March. The apex of the right side of the cup is our pivot ($359). Readers will also see an indecisive-looking reading for RSI and a bearishly postured daily MACD. For those reasons, I will take off some of what I purchased on weakness last week and early this week, but I do believe. After this sale, I will leave CRWD in my book as a top-five holding.

My Plan for CrowdStrike

Sell a portion today as an exercise in risk management.

Target Price: $431

Pivot: $359

Panic: On break of the 200-day SMA ($257)

At the time of publication, Guilfoyle was long CRWD, MSFT and S equity.