Bank of America Is Trading Higher and Investors Should Take a Look

Did Bank of America really have an up-5% quarter, as the latest shares run would suggest?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The shares of Bank of America BAC are trading higher. Let's take a look.

Bank of America, one of the few large, money-center banks that had yet to report this season, did so on Tuesday morning. For the firm's second quarter, Bank of America posted a GAAP EPS of $0.83 on revenue (net of interest expense) of $25.4 billion. These top and bottom-line results both beat Wall Street's expectations, while the revenue print was good enough for year-over-year growth of 0.8%. The firm-wide provision for credit losses amounted to $1.5 billion, an increase from $1.1 billion for Q2 2023 as non-interest expense increased 2% to $16.3 billion.

After taxes, net income printed at $6.9 billion, which was down 7% from the year ago comp, which works out to the above mentioned $0.83 per diluted share. These numbers were down from $0.83 on $7.4 billion for the year-ago period. As for the ratios, the return on average common shareholders' equity (ROE) dropped from 11.2% a year ago to 10%. The return on average tangible common shareholders' equity (ROTCE) dropped from 15.5% a year ago to 13.6%. The bank's efficiency ratio printed at 64% as it had a year ago, but down from 67% sequentially. The firm's standardized CET1 ratio did improve from 11.6% a year ago to 11.9%.

Net Interest Income

Net interest income (NII) printed at $13.7 billion or $13.86 billion on a FTE basis. This printed down from both Q1 2024 and Q2 2023 but did beat consensus for $13.81 billion by a hair. The firm projected net interest income of $14.5 billion for Q4 2024 (never mind Q3), which was above projections for $14.33 billion.

Returns To Shareholders

For the quarter, Bank of America paid out $1.9 billion in common dividends, while repurchasing $3.5 billion worth of common stock both for the firm's treasury and to offset shares awarded under equity-based compensation plans. That comes to returns of $5.4 billion in total to shareholders. The firm has also announced an 8% increase in the quarterly dividend effective this current quarter.

Segment Performance

- Consumer Banking: Generated revenue, net of interest expense of $10.206 billion (-3%), producing net income of $2.595 billion (-9%). Provision for credit losses moved up small to $1.218 billion, while non-interest expense increased small to $5.3464 billion.

- Global Wealth & Investment Banking: Generated revenue, net of interest expense of $.574 billion (+6%), producing net income of $1.026 billion (-4%). Provision for credit losses moved up small to $7 million, while non-interest expense increased 6% to $4.199 billion.

- Global Banking: Generated revenue, net of interest of $6.053 billion (-6%), producing net income of $2.116 billion (-20%). Provision for credit losses moved up small to $235 million, while non-interest expense increased small to $2.899 billion.

- Global Markets: Generated revenue, net of interest of $5.459 billion (+12%), producing net income of $1.41 billion (+18%). Sales and Trading revenue on the whole increased 9%. Within that performance, FICC-driven revenue was down 0.1%, while equities driven revenue was up 19%. Provision for credit losses moved down small to $-13 million, while non-interest expense increased small to $3.486 billion.

My Thoughts

This was not a bad quarter by any stretch. Was it an up-5% quarter as we are seeing the shares run on Tuesday morning? After being up six of the past seven trading days? Really, until this morning, BAC was only moving with the sector. Even Citigroup C, andJP Morgan JPM have gotten back on track after stumbling on earnings late last week.

Trading has been solid. Across the industry, investment banking has improved. Net interest income has not been stellar. That said, nearly every Fed watcher I know now expects to see the FOMC take the short end of the yield curve lower. This could end up steepening the yield curve, though that might seem counterintuitive. All that would take would be for the free market to remain in control of the long end of the curve.

That's quite possible with the federal government's fiscal imbalance and debt-situation the way it is, provided that the economy stays out of recession. Sounds good, but that's a big "if" as, once the economy contracts, the Fed will be once again pressured into purchasing treasuries across the maturity spectrum and free market results will be skewed by artificial intervention.

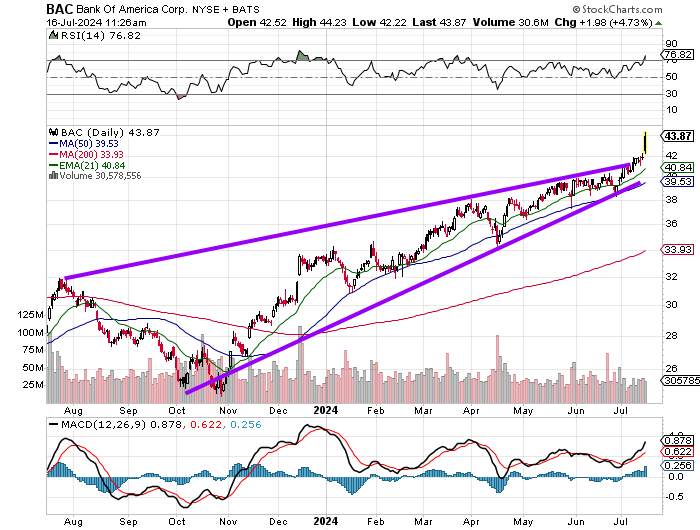

What we have here is a rising wedge, which is usually a pattern of bearish reversal, but is breaking out to the upside. Relative strength might be a little too strong. The daily MACD seems extended. I am not saying you are wrong if long on this name. I would be ecstatic if I were. That said, I would see this chart as cautionary. I am long some financials — Wells Fargo, which is underperforming; Bank of America; SoFi Technologies (SOFI), which is also breaking out but with a supportive chart pattern; and KeyCorp (KEY), which will report Thursday morning, but is also trying to break out right now. An industry thing? Probably.

Long this name, I would take something off. Flat this name, I would not short it as something is going on across the financials, but I would wait for a better day for entry.

At the time of publication, Guilfoyle was long WFC, SFI and KEY equity.