A Definitive Take on AT&T Stock As it Trades Higher After Earnings

Here's what investors should consider when looking at the telecommunications giant after it reported earnings in line with expectations.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The shares of AT&T T are trading higher after earnings, no kidding.

For the firm's second quarter, which ended June 30, 2024, AT&T posted an adjusted EPS of $0.57 (GAAP EPS: $0.49) on revenue of $29.797 billion. The adjusted earnings number landed precisely upon expectations, as the top-line print not only fell short of consensus but reflected a year-over-year contraction of 0.4%. The firm allows that the contraction in sales was largely due to lower business wireline service revenues and decreased mobility equipment revenue driven by lower volume. These negatives were offset for the most part, by higher mobility service, consumer wireline and Mexico revenue.

Operations

As revenue was contracting by 0.4%, the cost of equipment sales decreased 4.8% to $4.815 billion, and the cost of other (service) revenues decreased 2.1% to $6.627 billion. Administrative expenses increased 0.5%, asset impairments increased from zero to $480 million and depreciation/amortization increased 8.5% to $5.072 billion. All in all, total operating expenses increased 2.2% to $24.037 billion. This left an operating income of $5.76 billion (-10.1%).

After accounting for interest, other income/expenses and taxes as well as income due non-controlling interests and preferred shareholders, net income attributable to AT&T common shareholders decreased 20.1% to $3.546 billion. That takes earnings per diluted common share to $0.49. The adjusted EPS print landed at $0.57 due to adjustments made for restructuring costs of $0.05 and intangible amortization of $0.03 related to DIRECTV.

Segment Performance

Communications Segment

Mobility: Generated revenue of $20.48 billion (+0.8%), producing operating income of $6.716 billion (+1.6%). Operating income margin improved 20 bps to 32.8%. The firm added 419,000 monthly bill-paying prepaid wireless phone subscribers, compared with projections for about 284,000 additions. This is one reason why the stock is popping despite a weak tape.

Business Wireline: Generated revenue of $4.755 billion (-9.9%), producing operating income of $102 million (-74.2%). Operating income margin decreased 540 bps to 2.1%. Total monthly subscribers increased 3.2% to 115,474.

Consumer Wireline: Generated revenue of $3.347 billion (+3%), producing operating income of $184 million (+9.5%). Operating income margin improved 30 bps to 5.5%.

Total broadband connections were up 0.3% to 15,352.

Total retail consumer voice connections contracted 18% to 6,089.

Latin America Segment

Latin America: Generated revenue of $1.103 billion (+14.1%), producing operating income of $6 million (up from $-39 million). Operating income margin improved 450 bps to 0.5%. Total monthly subscribers increased 4.4% to 22,636.

Fundamentals

For the period reported, AT&T generated operating cash flow of $9.093 billion. Add to that number $392 million from distributions from DIRECTV, then subtract capex spending of $4.36 billion and $550 million in cash paid for vendor financing. That's how we get to free cash flow of $4.575 billion (+8.7%). Out of that number, the firm paid out cash dividends of $2.099 billion to shareholders.

Moving onto the balance sheet, the firm might have healthy cash flows, but only has a cash position of $3.093 billion, which is down more than half over six months. Inventories are down to $1.816 billion, which left current assets of $29.868 billion. Current liabilities add up to $42.429 billion that includes $5.249 in short-term debt and $3.981 billion in advanced billings and customer deposits. That last item is not really a financial obligation, but these ratios are going to be ugly.

The firm's current and quick ratios at this time, stand at 0.70 and 0.66. That certainly does not pass muster in my book. Even when adjusting for the advanced and deposited funds, these ratios rise only to 0.78 and 0.73. Not only are these ratios well below what I consider acceptable for investment consideration, I certainly do not like that the cash stash only amounts to 59% of the firm's debt maturing in less than 12 months. The firm also has more than $2 billion in dividends payable listed as a current liability. Obviously, the firm is going to either have to cut the dividend again or refinance the debt-load at current interest rates.

Total assets amount to $398.026 billion, including $73.131 billion in goodwill and other intangibles. At less than 20% of total assets, I do not see that as a problem. Total liabilities less equity comes to $108.918 billion. Fortunately, I do not see any long-term debt on the books, so if the short-term paper can be refinanced and pushed out in maturity, the dividend should be safe.

My Thoughts

There is some improvement in part of the business. The balance sheet overall really is not that bad. That said, the current state (short-term) of the balance sheet is a wreck and needs to be cleaned up. Given the robust cash flows that the firm has been generating, this is certainly do-able.

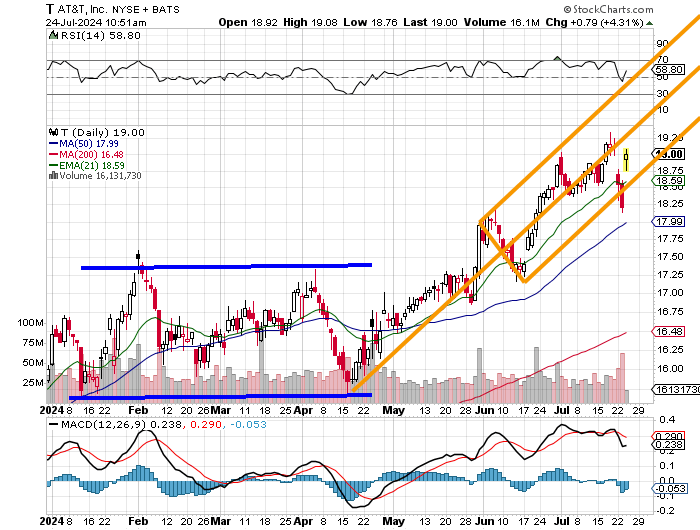

Readers will see that this morning's pop has pulled the shares out of a nosedive that had threatened the foundation of the pitchfork model that has contained the rally in the share price since mid-April. If one looks closely, this pop has interrupted a double-top bearish reversal that had developed going into earnings.

On top of that, relative strength is neutral to moderately strong, but the daily MACD is a mess. The 26-day EMA stands above the 12-day EMA despite the fact that both are in positive territory, while the histogram of the nine-day EMA stands in negative territory.

This was not a bad quarter, but it also is not a good quarter. The fundamentals are not horrible but do require some hands-on tinkering. The technicals tell me that right now, and I am not positive as I have no position, that I think his stock in this environment is a "sell." I would not buy this stock today. I think it comes in from here.

At the time of publication, Guilfoyle had no positions in any securities mentioned.