As Amazon Steers Through a Troubled Landscape, Trade It This Way

The robust online storefront for Amazon has become perhaps the greatest platform for advertisers in history.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Tuesday night, the New York Mets held "Dollar Dog Night" at Citi Field in Queens. Not only did the home team win the ballgame, but they also sold 44,269 hot dogs, which was a franchise record.

In other exciting news, both Advanced Micro Devices AMD and Amazon AMZN reported their quarterly financial results on Tuesday evening. I came into the event long but had reduced exposure in both cases as I did not know what to expect. Amazon has traded higher overnight as AMD has sold off.

I know that my followers expect me to cover both in depth. I can only follow one right now. The questions now would be... where we start to rebuild our core long position in AMD, and do we trust AMZN enough not to just take profits here. These questions are more easily asked than answered.

Oh, and followers, if they were not aware, probably would like to know that I offloaded about 25% of my Microsoft MSFT long on Tuesday morning. The stock does not look so good on the charts, and I simply took the step to reduce exposure. I did inform followers on both "X" (formerly Twitter) and in the comments section at Doug's Diary here at TheStreet PRO.

Amazon

Let's tackle Amazon this morning and leave AMD for a slower earnings day. For the firm's first quarter, which ended March 31st, Amazon posted a GAAP EPS of $0.98 on revenue of $143.313B. This compares quite well to the EPS of $0.31 posted for the year ago quarter, while reflecting year over year sales growth of 12.5%.

Readers are reminded that CEO Andy Jassy had made cost cutting a priority at the firm's e-commerce business, prioritizing profitability there, while spending in a big way on increasing the firm's generative AI capabilities at the cloud unit and other parts of the firm where it might better position the firm in its efforts to generate expanded margins on increased overall sales.

This quarter, I believe, shows substantial progress on those fronts. I remind readers that both Microsoft's Azure and Alphabet's Google Cloud put together very nice quarters.

Operations

As mentioned above, revenues generated for the quarter increased 12.5% to $127.358B. This came on $60.915B (+6.9%) in the sales of products and $82.398B (+17.1%) in sales of services. Total operating expenses, including the cost of sales, fulfillment, technology/content, marketing, and administrative costs came to $128.006B, up just 4.4%.

This left a GAAP operating income of $15.307B, which was up 221% (not a misprint), as operating margin improved from 3.75% to 10.68%. This crushed expectations for an operating margin of 7.9%. After accounting for interest, taxes and non-operating income/expenses, GAAP net income printed at $10.431B (+229%). This works out to earnings of $0.98 per share after dilution.

Segment Performance

- North America generated sales of $86.341B (+12%), producing operating income of $4.983B (+455%).

- International generated sales of $31.935B (+10%), producing operating income of $903M (+172%).

- AWS (Amazon Web Services) generated sales of $25.037B (+17%), producing operating income of $9.421B (+84%).

Business Unit Sales

- Online Stores generated sales of $54.67B (+7%).

- Third Party Seller Services generated sales of $34.596B (+16%).

- Amazon Web Services generated sales of $34.596B (+17%). See above.

- Advertising Services generated sales of $11.824B (+24%).

- Subscription Services generated sales of $10.722B (+11%).

- Physical Stores.generated sales of $5.202B (+6%).

- Other Businesses generated sales of $1.262B (+23%).

CEO Andy Jassy

- From the press release: "The combination of companies renewing their infrastructure modernization efforts and the appeal of AWS’s AI capabilities is reaccelerating AWS’s growth rate (now at a $100 billion annual revenue run rate); our Stores business continues to expand selection, provide everyday low prices, and accelerate delivery speed (setting another record on speed for Prime customers in Q1) while lowering our cost to serve; and, our Advertising efforts continue to benefit from the growth of our Stores and Prime Video businesses."

- During the call: "I think there are really unbelievable growth opportunities in front of us. And I think what people sometimes forget on the AWS side, it's a $100 billion revenue run rate business, that we're still 85-plus percent of the global IT spend is on premises. And if you believe that equation is going to flip, which we do, it means we have a lot of growth in front of us, and that's before the generative AI opportunity, which I don't know if any of us have seen a possibility like this in technology in a really long time, for sure, since the cloud, perhaps since the Internet."

Guidance

For the current quarter, Amazon is projecting net sales to land in between $144B and $149B, which implies growth of 7% to 11%. This was just a touch below the $150B that Wall Street was looking for, but this was largely due to a projected negative impact of 60 basis points worth of foreign exchange imbalances.

The firm did suggest that CapEx spending may have hit a low for the year during the quarter reported as there are no plans to slow or stall the firm's investment in the firm's cloud and AI capabilities. Even so, operating income from the current quarter is seen at $10B to $14B, and that would be up from $7.7B for Q2 2023.

Fundamentals

For the trailing twelve months, Amazon generated operating cash flow of $99.147B (+82.5%). Out of this came CapEx spending of $48.988 (-15%), leaving free cash flow of $50.149B (up from $-3.319B). The firm did not return any capital in any way to shareholders over the past twelve months.

Glancing at the balance sheet, Amazon ended the period with a cash position of $85.074B and inventories of $31.147B. This puts current assets at $163.989B. Current liabilities add up to $152.965B. This includes no short-term debt, bit $15.927B worth of unearned revenue which is not a financial obligation.

At the headline that leaves the firm with a current ratio of 1.07 and a quick ratio of 0.87. These ratios pass muster even before adjusting for unearned revenue. Remember, that we are not as strict with retailers on quick ratios due to the inventory-heavy nature of that business. Once adjusted for unearned revenues, the firm's ratios rise to 1.20 and 0.97, respectively.

Total assets amount to $530.969B, including just $22.77B worth of goodwill, which is inconsequential. Total liabilities less equity comes to $314.308B. This does include long-term debt of $57.634B, which is something that Amazon could handle out of pocket if need be. This balance sheet is in good shape.

Wall Street

Talk about a unanimous consensus. Since these earnings were released on Tuesday evening, I have found 25 highly rated (4+ stars at TipRanks) sell-side analysts that have opined on AMZN. After allowing for changes, all 25 rate Amazon at a "buy" or their firm's "buy-equivalent" rating.

The average target price across the 25 is $220.80 with a high of $245 (Ronald Josey of Citigroup) and a low of $200 (Aaron Kessler of Seaport Global). Once these two are omitted as potential outliers, the average target across the remaining 23 analysts drops fractionally to $220.65.

My Thoughts

I own the stock for its cloud and advertising businesses. Increased AI-related up-spends are forcing corporate America to rely on AWS, Azure and Google Cloud more and more. AWS is still the leader in that group even if Azure is gaining share.

The robust online storefront for Amazon has become perhaps the greatest platform for advertisers in history. Jassy seems to have steered the firm through a troubled landscape and appears quite capable in staying the course.

The quarter was undeniably strong. Cash flows are robust. Margins are expanding. No single business unit seems to be struggling. Guidance was not spectacular, but at least it was explainable. There is a very good chance that this guidance, according to a number of pundits, turns out to be conservative. Perhaps intentionally so.

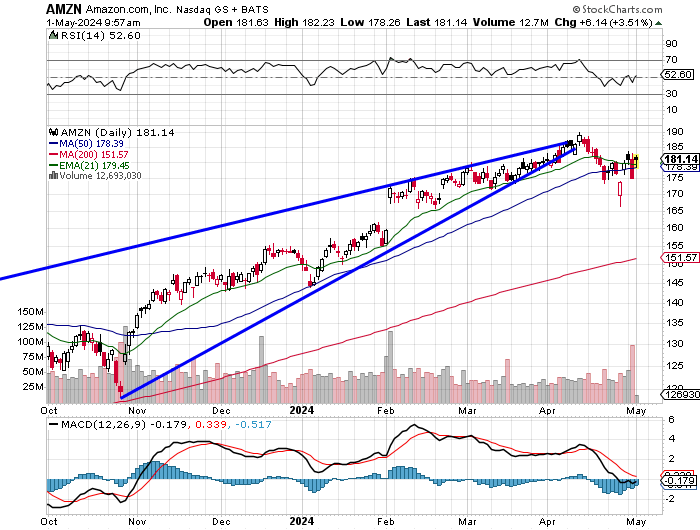

Readers will see that AMZN sold off from early April into last week as the ascending, narrowing wedge came to a close. After losing both the 21-day EMA (exponential moving average) and 50-day SMA (simple moving average), the stock has now regained both lines.

Relative strength is neutral as it has been for weeks. However, the daily MACD (moving average convergence divergence) has been bearish and now appears to be closing in on a bullish crossover of the 26-day EMA by the 12-day EMA as the histogram of the 9-day EMA closes in on the zero bund.

For those without the patience to look all that stuff up, the technicals are improving. The 50-day SMA (simple moving average) at $178 serves for me at this time (as we do not have a current pattern serving as a set-up) as pivot.

I will not yet be taking further profits on this name and would likely add should the 50-day SMA be tested. That would be during a normal week. This is not a normal week. I will not act ahead of the Fed this afternoon, but anything is possible for later today and later this week.

Amazon (my plan)

- Target Price: $214

- Pivot: $178

- Add: in between the April low ($166) and the 200-day SMA $151)

- Panic: On a loss of the 200-day SMA

At the time of publication, Stephen Guilfoyle was long AMZN, AMD, MSFT equity.