Adobe Is Red Hot, Here's How I'm Trading

The cloud king seems to have gotten its act in gear, beating Wall Street expectations.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The cloud king that had flopped as an AI firm up to this point released its second quarter financial results on Thursday evening. We speak of Adobe ADBE, the firm that Jim Cramer had once named one of his "cloud kings" that had been mired in a nearly four-month downturn that had only been exacerbated in response to the firm's first quarter earnings release back in mid-March. Adobe, my friends, apparently looks to have gotten its act in gear.

For the three-month period ended May 31, 2024, Adobe posted an adjusted EPS of $4.48 (GAAP EPS: $3.49) on revenue of $5.309 billion. The adjustment was made primarily for stock-based and deferred-compensation expenses. These top- and bottom-line results both beat Wall Street, while the sales print was good for year-over-year growth of 10.2%. Remaining performance obligation (RPO) exited the quarter at $17.86 billion (+1.6% in three months).

Operations

As Adobe was generating 10.2% revenue growth to $5.309 billion (mostly driven by subscription sales), the cost of that revenue printed at $598 million (+4.7%), leaving a GAAP gross profit of $4.711 billion (+11%) on a gross margin of 88.7%, up from 88.1%. Operating expenses increased 7.9% to $2.826 billion, leaving GAAP operating income of $1.885 billion (+16.1%). This came on a GAAP operating margin of 35.5% up from 33.7%. On an adjusted basis, operating income printed at $2.441 billion on an operating margin of 46%.

After accounting for interest, taxes and other income/losses, GAAP net income hit the tape at $1.573 billion (+21.5%), which works out to $3.49 a diluted share, up from $2.82 for the comparable year-prior period. Adjusted, net income landed at $2.023 billion, or $4.48 per diluted share.

Segment Sales Performance

- Digital media generated revenue of $3.91 billion (+11%)

- Creative generated revenue of $3.13 billion (+10%)

- Document cloud generated revenue of $782 million (+19%)

- Digital media drove net new annualized recurring revenue (ARR) of $487 million, exiting the quarter with segment ARR at $3.15 billion

- Creative ARR grew to $13.11 billion

- Document cloud grew to $3.15 billion

- Digital experience generated revenue of $1.33 billion (+9%)

- Digital experience subscription-based revenue grew 135 to $1.2 billion

Guidance

For the current quarter, Adobe sees total revenue at $5.33 billion to $5.38 billion, which was slightly below the $5.4 billion that Wall Street had in mind. Digital media is seen generating revenue of $3.95 billion to $3.98 billion, while digital experience drives $1.325 billion to $1.345 billion. Digital media should produce a rough $460 million in net-new ARR, while digital experience drives subscription-based revenue of $1.2 billion to $1.22 billion. The firm sees GAAP EPS of $3.40 to $3.45 and adjusted EPS of $4.50 to $4.55, which is above the $4.48 consensus view.

For the full year, the firm sees total revenue of $21.4 billion to $21.5 billion, which pulls the mid-point of the range just below the $21.46 billion that Wall Street was looking for. Digital media is seen driving revenue of $15.8 billion to $15.85 billion, while digital experience produces sales of $5.325 billion to $5.375 billion. Digital media is expected to add net-new ARR of about $1.95 billion, while digital experience brings subscription-based revenue up to $4.775 billion to $4.825 billion. Adjusted EPS is seen at $18.00 to $18.20, bringing the midpoint well above the $18.03 consensus view.

Fundamentals

For the period reported, Adobe generated operating cash flow of $1.94 billion. Out of that came capex spending of just $41 million, leaving free cash flow of $1.899 billion. The firm repurchased about 4.6 million shares of common stock for about $2.5 billion for the firm's treasury, which is a little much in my book, relative to free cash flow.

Glancing at the balance sheet, Adobe ended the quarter with a cash position of $8.065 billion and current assets of $11.023 billion. Current liabilities add up to $9.474 billion that includes no short-term debt, but an impressive $5.558 billion in deferred revenue. Remember, deferred revenue is an obligation of goods or services owed, but not a true financial obligation. This puts the firm's current ratio at a passable 1.16, but once adjusted for deferred revenue, rises to a quite robust 2.81.

Total assets amount to $30.007 billion, including $13.736 billion in goodwill and other intangibles. At 45.8% of total assets, I think this is a bit much. Not quite as awful as Oracle's ORCL percentage was yesterday, but on the edge of being more than I am comfortable with. Total liabilities less equity comes to $15.164 billion, including longer-term debt of $4.127 billion, which is something that Adobe could easily handle out of pocket.

Wall Street

Since these earnings were released, I have come across nine highly-rated (four-plus stars at TipRanks) who have opined on ADBE. You would be surprised how many poorly-rated analysts had something to say, and I had to weed that crowd out. (Just an aside: For those who do not know, it is shocking how many analysts are featured on CNBC and other financial media outlets who rate poorly and do not qualify for inclusion in my articles at TheStreet Pro. We have a much higher standard here than you'll get on the tube.)

Among these nine analysts, there are seven "buy" or buy-equivalent ratings, one "hold" rating and one outright "sell" rating. After allowing for changes, the average target price across the nine is $601.67 with a high of $685 (Gil Luria of DA Davidson) and a low of $450 (Jackson Ader of KeyBanc). Once omitting these two as potential outliers, the average target across the other seven rises to $611.43.

My Thoughts

The stock was red hot on Friday morning, up about 15%. The quarter was strong. Cash flows are strong. Guidance was a little light on the sales side, but stronger on the margin side. The balance sheet is squared away. There is too much value placed on intangibles in my opinion but squared away nonetheless.

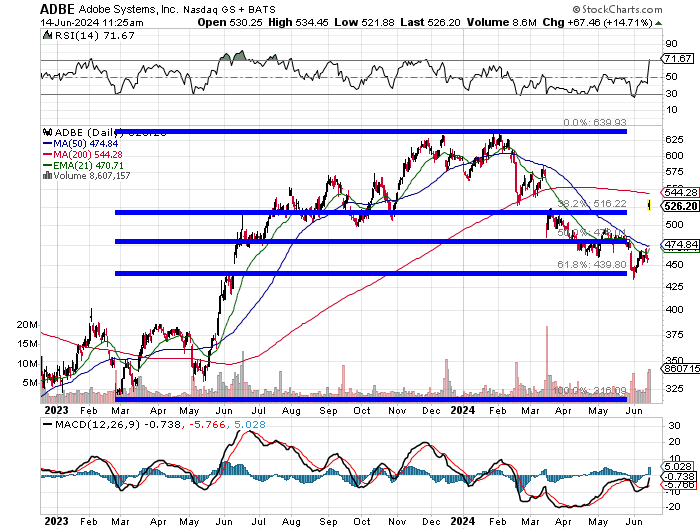

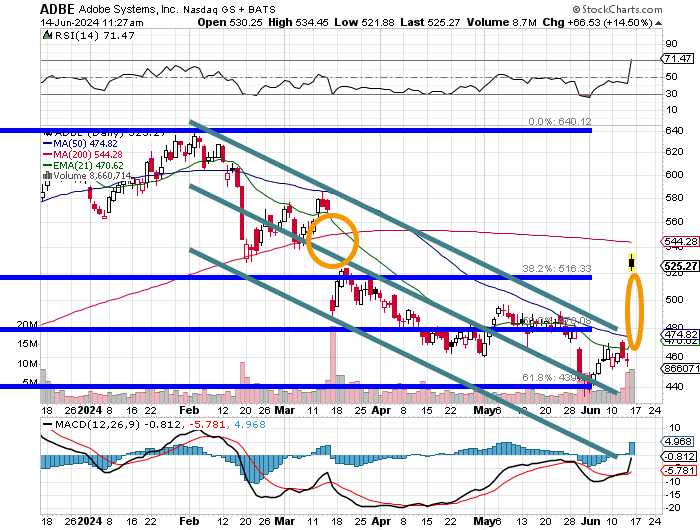

This chart could serve as a billboard advertisement for using Fibonacci retracement levels as well as respecting the danger apparent in double-top reversals. Let's zoom in.

Readers will see that ADBE has gapped significantly higher this morning and even started working to refill that gap created back in March. The stock will have to trade at least as high as $580 to accomplish that task. Relative strength and the daily MACD are suddenly in better shape. The stock has retaken its 50-day SMA, currently at $474 this morning and is still trading well short of that 200-day SMA up at $544.

My feeling is that the stock is less likely in the short-term to test the 200-day line than it is the 50-day line, which means that, although this rally is meaningful, the short- to medium-term risk is probably at the downside after this run. If I am a trader in this name, I am probably taking profits going into the weekend. If I am an investor, I am probably thinking about getting long a June 28, 2024, $525/$515 bear put spread for a net debit of roughly $4.25. In other words, I am not so bold as to short the equity but might risk $4.25 to try to win back $10.

At the time of publication, Guilfoyle had no positions in any securities mentioned.