Weekly Roundup

We exited Chipotle, got into Morgan Stanley, and added to Marvell, PepsiCo and the Energy Select Sector SPDR Fund.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The big winner this week? The small-cap stocks.

The Russell 2000 continued to claw its way back, as the Dow Jones industrial average ended the week unchanged and the S&P 500 finished up slightly, continuing to flirt with overbought territory.

While that move this week was small, it put the S&P 500 to a new high for the year, which also means it is trading at almost 21-times expected 2023 earnings and nearly 19-times expected 2024 earnings per share. When looking at the Nasdaq, which benefited from renewed AI-related headlines this week, including those from our own Alphabet we see a similar technical picture.

During the week, we shared expectations for rate cuts have continued to swell in recent days. Some observers are calling for as many as four or five rate cuts by the Fed in 2024. Weaker-than-expected job openings and job creation data reported this week helped fuel as did the drop in oil prices. When we've seen the market priced to perfection in the past, especially after such a pronounced run and at a time when the Cboe Volatility Index is near its lowest levels of the year, it doesn't take much to upset the stock market apple cart. And yes, the CNN Business Fear and Greed Index is also in "Greed" territory.

As we see it, this has the market walking a data tightrope ahead of and most likely after the Fed's policy meeting next week. Economic data below expectations would support the Goldilocks narrative and a soft landing giving the Fed room to cut rates. But data that points to a resurgence in the economy could raise concerns as there is more fight left against inflation. And if the economic data implies the economy is about to fall out of bed, it means a more serious think about 2024 revenue and EPS expectations as well as the consensus view that S&P 500 EPS will grow 11.5% next year will be needed.

The market's response on Friday to the stronger-than-expected November employment report, which also showed wage growth picking back up was a little surprising, especially given the rebound in 10-year Treasury yields to 4.23% from the low of 4.12% on Wednesday. That said, the November jobs report showed more people working with more money going to their pockets and that's a good thing for the economy, no matter how you slice it.

We continue to think the market's back in a place we've seen it several times over the last two years -- trading day to day based on the latest day between today and Wednesday when the Fed not only shares its latest policy decision but its updated economic projections as well. In those projections, the Fed will tell us how many rate cuts it sees as of that date for 2024. If it's less than the four to five expected by the market, we could traders take some of the market's recent gains off the table. It doesn't take much when the market is priced to perfection and the S&P 500's price-to-earnings multiple is stretched.

Taking out some of the froth that has worked its way into the market would be a good thing in our view. It would allow us to put more capital to work at better stock prices and more favorable valuations. While our inverse exchange-traded finds worked against us in November, they were among the stronger performers in August, September, and October when the market was under pressure. With a stretched and overbought market navigating that tightrope in a complacent market, we'll continue to own them.

Catching Up on the AAP Portfolio This Week

Measured against the very modest increase in the S&P 500 this week, notable portfolio performers included Apple, Axon, Costco, Alphabet, Qualcomm, as well as newly added Morgan Stanley shares. With 14 trading days left for the year, more than half of the portfolio is ahead of the quarter-to-date move in the S&P 500 led by Qualcomm, Microsoft, and Axon shares.

During the week, we exited the portfolio's position in Chipotle shares, locking in a more than 40% gain on the last slug of those shares. With those proceeds, we called up the aforementioned Morgan Stanley shares from the Bullpen with a $90 target and a Two rating. We also added to our existing Marvell and PepsiCo holdings. Later in the week, we made a contrarian call by adding to our Energy Select Sector SPDR Fund shares in anticipation of expanded OPEC+ production cuts coming on stream in the first quarter of 2024.

While we made some moves with the portfolio this week, we continued to flesh out the Bullpen with the addition of Waste Management. We would continue to favor the market giving back some of its recent and quick gains, which would not only take some of the froth out of the market, it would also allow us to put more capital to work at better stock prices and more favorable valuations.

This Week's AAP Videos and Podcasts

We cover a lot of ground during the week in our Daily Rundowns and the AAP Podcast. If you happened to miss one or more of them, here are some helpful links:

Monday, December 4: Why Inverse ETFs Are an Important Part of Our Game Plan

Tuesday, December 5: How to Deal When S&P Forecasts Are 'All Over the Freakin' Map'

Wednesday, December 6: A Christmastime Gift Might Await Traders

Wednesday, December 6: This Isn't Crock-Pot Investing. Here's Our Portfolio Recipe

Thursday, December 7: The 'Goldilocks' Story Gets Its Stress Test

Friday, December 8: Futures Expert Carley Garner Sees S&P 500 at These 3 Numbers

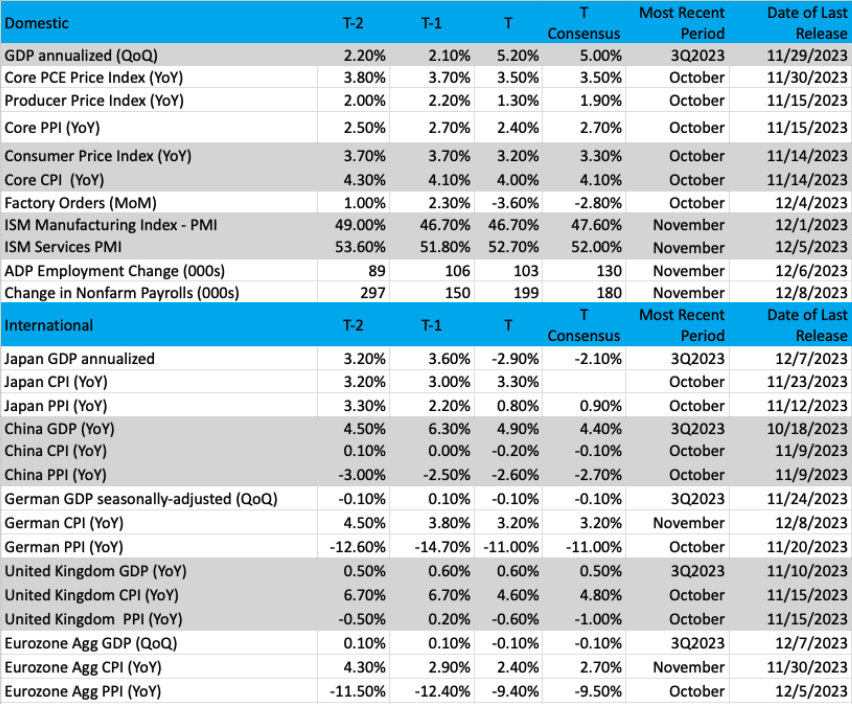

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

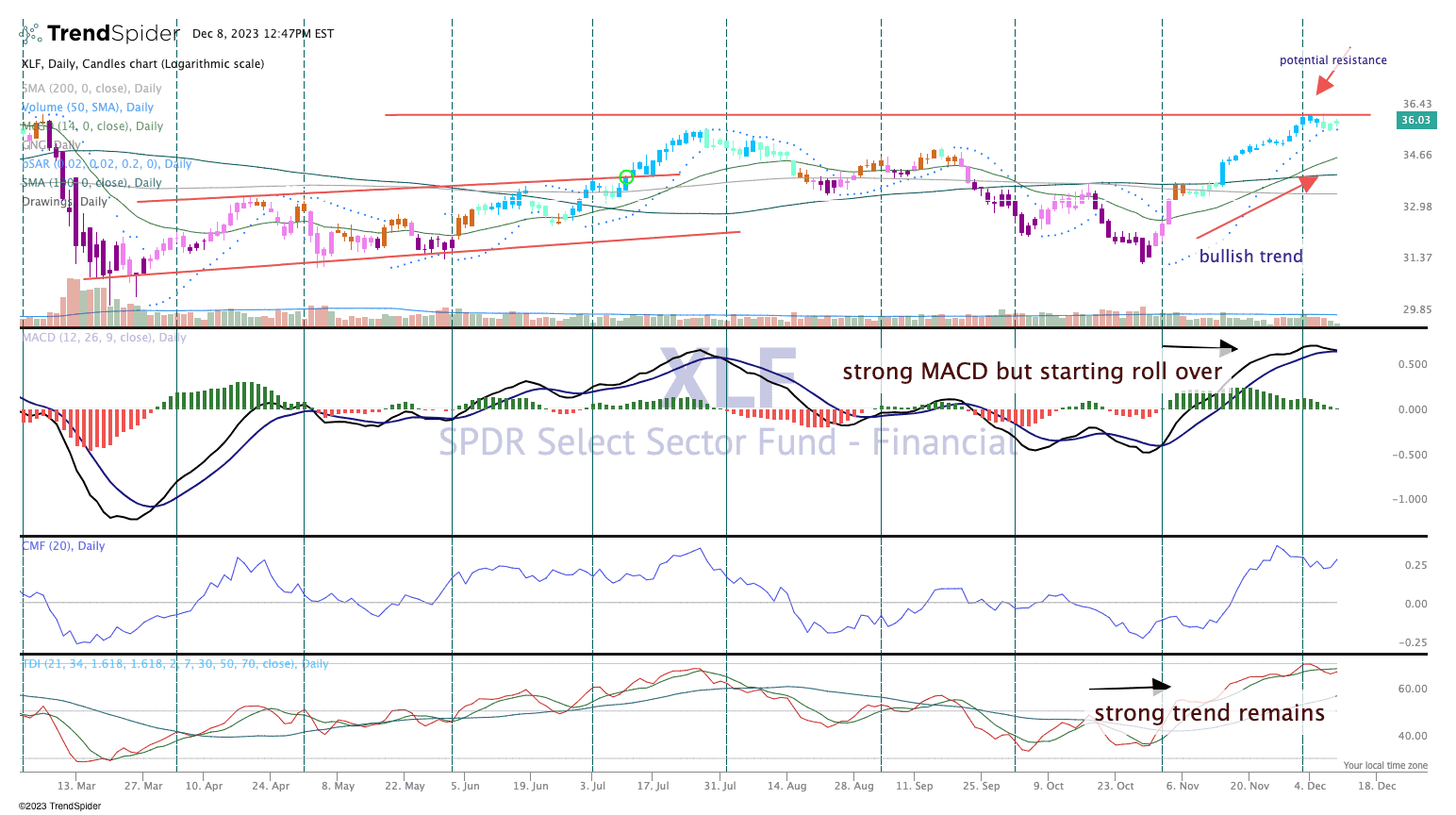

Chart of the Week: The Financial Select Sector SPDR Fund

For the most part, financials have been beaten up badly in 2023. We all remember the scare from the Spring when Silicon Valley Bank went belly up along with a few others and put all the banks on notice: Take less risk!

Of course, the big banks not only reduced their risk, but also downside exposure, as Treasury yields rose. The names that are mostly covered in the SPDR Select Sector Financial fund -- names like JP Morgan, Bank of America, Morgan Stanley, Wells Fargo, and others. These banks did a nice job of hedging risk whereas others did not do as well. However the collateral damage was far-reaching for all the financials, and we should mention a higher interest rate environment is not exactly the most fertile business ground for the banks. Some are saying banks will do much better in 2024, very strong if rates come down further.

The chart of the XLF is looking far better today with a series of higher highs, and higher lows. The bullish trend that started in late October sports a nice uptrend that ran this exchange-traded fund up by more than 15%. That's a big move for a short period, but the indicators we follow remain bullish.

One thing we learned long ago is don't fight a trend. The parabolic SAR system (stop and reverse) shows price action as bullish. This indicator tells us about the change in trajectory before it happens. The Moving Average Convergence Divergence (MACD) oscillator may be starting to roll over here and that might be a concern, but for now, we see any pullbacks in financials being bought, so the XLF is a good ETF to own.

For a more detailed look at the chart, clickhere.

Other charts we shared with you this week were:

Monday, December 4: S&P 500 - We Keep Pushing the Boulder Up the Hill

Monday, December 4: McDonald's (MCD) - McDonald's Is McSlumping No More

Tuesday, December 5: Clear Secure (YOU) - Running on Fumes and Into a Brick Wall

Wednesday, December 6: Waste Management (WM) - This Stock Isn't Waste-ing Time

Thursday, December 7: Morgan Stanley (MS) - Morgan Stanley Encounters Opposing Forces

Poll of the Week

Bitcoin is back in the headlines as it passed the $43,000 level, fueled in part by the liquidation of short positions and optimism building for a spot bitcoin ETF being approved in the US. That brings us to our AAP Poll of the Week. Even though we have no plans to wade the portfolio into bitcoin, we want to know about your appetite when it comes to crypto:

*Never used, not open to it

*Curious, would own it in an ETF

*Curious, would own Bitcoin directly

*I've adopted crypto, am a user

As you can see below, we continue to leverage X as a platform to capture your votes.

You can

The Coming Week

Next week starts slow on the economic data front but make no mistake it will be a big week for the data and potentially the market. Ahead of Wednesday's Fed policy decision and updated economic projections, Tuesday morning brings the next iteration of the Consumer Price Index report followed by the November Producer Price Index on Wednesday morning. The learnings in those two reports will signal if the Fed adopts a more dovish tone and whether rate cuts are finally entering the Fed's meeting conversations. While the expectation is the Fed will leave interest rates unchanged next week, its policy note, Fed Chair Powell's presser comments, and updated projections will tell us how rate cut expectations are. On Friday, the CME Fed Watch Tool showed the market sees 4-5 rate cuts in 2024 with the Fed Funds rate ending between 400-450 basis points vs. its current 525-500. If the Fed or next week's data throws cold water on that model's findings, it would be a reason for an overbought stock market to give back some of its recent gains.

Exiting the week, we have an earlier-than-usual reading for December Flash PMIs. We understand the timing of year-end holidays is why the Flash data is being released so early, but that means its predictive accuracy could be below par. Even so, we'll read through the data for what it can tell us about inflation pressures, the pace of the economy as we close out 2023, and what new order activity indicates for the start of 2024.

Next week also brings the December Members-Only Meeting, which will be held on December 13th at noon. You can watch the live stream on the AAP website. We hope to see you there!

Here's a closer look at the economic data coming at us next week:

U.S.

Tuesday, December 12

- NFIB Small Business Optimism Index - November (6:00 AM ET)

- Consumer Price Index - November (8:30 AM ET)

- Treasury Budget - November (2 PM ET)

Wednesday, December 13

- Weekly MBA Mortgage Applications (7:00 AM ET)

- Producer Price Index - November (8:30 AM ET)

- Weekly EIA Crude Oil Inventories (10:30 AM ET)

- FOMC Rate Decision, Economic Projections (2 PM ET)

Thursday, December 14

- Weekly Initial & Continuing Jobless Claims (8:30 AM ET)

- Import/Export Prices - November (8:30 AM ET)

- Retail Sales - November (8:30 AM ET)

- Business Inventories - October (10:00 AM ET)

- Weekly EIA Natural Gas Inventories (10:30 AM ET)

Friday, December 15

- Empire Manufacturing Index - December (8:30 AM ET)

- Industrial Production & Capacity Utilization - November (9:15 AM ET)

- S&P Global Flash Manufacturing and Services PMI - December (9:45 AM ET)

International

Monday, December 11

- Japan: Machine Tool Orders - November

Tuesday, December 12

- Japan: Producer Price Index - November

- UK: Unemployment Rate - October

- Eurozone: ZEW Economic Sentiment Index - December

Wednesday, December 13

- UK: GDP, Industrial Production, Manufacturing Production - October

- Eurozone: Industrial Production - October

Thursday, December 14

- UK: Bank of England Interest Rate Decision

- Eurozone: European Central Bank Interest Rate Decision

Friday, December 15

- Japan: Jibun Bank Flash Manufacturing and Services PMI - December

- China: Industrial Production, Retail Sales, Vehicle Sales, Foreign Direct Investment - November

- Eurozone: HCOB Flash Manufacturing and Services PMI - December

- UK: S&P Global/CIPS Flash Manufacturing and Services PMI - December

While we had no portfolio companies reporting this week, Costco (COST) will be on deck next week, on Thursday after the bell. We'll also be chewing through quarterly results from Darden (DRI), focusing on food cost inflation as well as confirmation consumers are trading down when dining out. We'll be gauging comments on both cloud and AI in quarterly results from Oracle (ORCL) and Adobe (ADBE). Following comments from RH (RH) this week that "With 82% of homeowners having mortgages below 5%, and 62% below 4%, we continue to expect the existing housing market to remain frozen until interest rates and/or home prices fall meaningfully", we'll be interested in delivery expectations from homebuilder Lennar (LEN).

Monday, December 11

- Open: FuelCell Energy (FCEL)

- Close: Casey's General Store (CASY), Oracle (ORCL)

Wednesday, December 13

- Open: REV Group (REVG)

- Close: Adobe (ADBE), Nordson (NDSN)

Thursday, December 14

- Close: Costco (COST), Lennar (LEN)

Friday, December 15

- Open: Darden Restaurants (DRI)

ONEs

Alphabet GOOGL; $ 134.99; 850 shares; 3.06%; Sector: Communication Services

WEEKLY UPDATE: November global search engine market share from Statcounter showed Google held onto its dominant position with 91.5% of the market, unchanged compared to September and October. However, the big news this week that led our GOOGL shares higher was Wednesday's unveiling of the company's Gemini large language model that moved it further into the generative AI race. This included three version of Gemini - Ultra, Pro, and Nano - which should allow Gemini to be used across different use cases & hardware capabilities, from data centers to mobile devices. Gemini Pro will power Google's Gen AI chatbot, Bard, which competes with ChatGPT. Taking some steam out of the announcement, the Ultra flavor Gemini isn't expected to be available until "early" 2024. Nano is the large language model that can be used directly on devices, including smartphones, as edge AI computing becomes more prevalent. Also on Wednesday, Alphabet announced a new version of its tensor processing unit chip, the Cloud TPU v5p, used for AI and showed off its AI Hypercomputer from Google Cloud. In our view, these announcements confirm Alphabet isn't to be underestimated in the AI arms race.

1-Wk. Price Change: 2.4%; Yield: 0.00%

INVESTMENT THESIS: We believe that while search and digital ad dominance are what will carry shares in the near- to mid-term, longer-term it is the company's artificial intelligence "moat" that will provide for new avenues of growth. AI is what has made the company's search, video, and targeted ad capabilities best-in-class and is the driving force behind the company's success in voice (Google Home) and autonomous driving (Waymo). Furthermore, we believe it is this AI expertise that will also make the company more prevalent in other industries, including healthcare via its subsidiary Verily, as AI and machine learning continue to disrupt operations across industries. Lastly, compounding our positive view of the company's future opportunities, we believe that Alphabet's free cash flow generation and solid balance sheet set it apart and are what will allow the company to continue taking chances on far-out ground-breaking and potentially world-changing projects.

Target Price: Reiterate $155; Rating: One

Panic Point: $115

RISKS: Regulatory risk (data privacy), competition, and macroeconomic slowdown impacting consumers and therefore ad buyer activity.

ACTIONS, ANALYSIS & MORE: FY2Q21 Earnings Analysis (7/27/21), Why GOOGL Has Shrugged Off Antitrust Headlines in Early Trading Tuesday (10/20/20)

Amazon AMZN; $147.42; 835 shares; 3.28%; Sector: Consumer Discretionary

WEEKLY UPDATE: Amazon shares were little changed this week, and we look forward to next week's November Retail Sales report that should confirm consumers pivoting to digital shopping even more so this holiday season. During the week, it was reported Amazon plans to offer Prime members an option to pay $9.99 per month to get unlimited grocery delivery from Whole Foods and Amazon Fresh on orders of more than $35. Subscribers will also have access to 30-minute pickup on orders of any size. That's a big improvement compared to its current offering and tells us Amazon is serious about making inroads in grocery. We also have another data point that says Amazon is focusing on margins and maximizing its opportunities. The company's streaming unit Twitch said that it will shut down its business in South Korea on Feb. 27 due to high operating cost and network fees. Bank of America published its annual holiday pricing survey, finding that, by a wide margin, Amazon had the fastest average shipping speeds on common items. We see that a competitive weapon, especially during the holiday shopping season. And several months ago, during one of our monthly Members Only calls, we shared Amazon was our top pick for the balance of 2023, and it's up more than 15% quarter to date, easily more than double the S&P 500. Now Oppenheimer named the stock its top large cap pick for 2024 with a $200 price target. As we move past the holiday shopping season, we'll be focused on margin improvement as well as wins at AWS and the company's advertising business when we look for upside relative to our $170 target.

1-Wk. Price Change: 0.3%; Yield: 0.0%

INVESTMENT THESIS: We believe upside will result from Amazon's continued eCommerce dominance, AWS' continued leadership in the public cloud space, and ongoing growth of the company's advertising revenue stream, which feeds off Amazon's eCommerce business. Additionally, we believe profitability will continue to improve as AWS and advertising account for a larger portion of total sales as both these segments sport higher margins than the eCommerce operation. And while we believe the increasing share of revenue from these higher margin businesses will be key to driving profitability longer-term, we believe margins on eCommerce stand to improve as the company's infrastructure is further built out and economies of scale further kick in. The embedded call option is that management is always looking to enter a new space and generate new revenue streams.

Target Price: Reiterate $170; Rating: One

Panic Point: $108

RISKS: High valuation exposes the stock to volatile swings, eCommerce has exposure to slower consumer spending and competition, management is not afraid to invest heavily, potential headwinds resulting from new eCommerce regulation in India, and management is not scared to invest aggressively for growth, which can at times cause volatile reactions as near-term concerns arise relating to the impact on margins.

ACTIONS, ANALYSIS & MORE: FY2Q21 Earnings Analysis (7/29/21), 2020 Letter to Shareholders (4/15/21), Initiation (2/2/18), Investor Relations

Applied Materials Inc. AMAT; $147.72; 275 shares; 1.08%; Sector: Semiconductor Manufacturing

WEEKLY UPDATE: Applied Materials continued to pull back towards strong support in the $145-$148 area on milder turnover. When a stock corrects or pulls back, we want to see it happen on lower volume, this tells us the sellers do not have much conviction. The stock has been volatile recently and we would welcome a slowdown and some sideways action before the stock is ready for its next move. This week the company unveiled a joint lab with CEA-LETI for rapidly growing specialty chip markets. The recent news about an investigation into their potentially illegal sales to China (violating export restrictions) is going to be a drag on the stock, but hopefully over time this will be proven to be a non-event.

1-Wk. Price Change: -2.6% Yield: 0.9%

INVESTMENT THESIS: Applied provides manufacturing equipment, services, and software to the semiconductor, display, and related industries. With its diverse technology capabilities, Applied delivers products and services that improve device performance, power, yield, and cost. Applied's customers include manufacturers of semiconductor chips, liquid crystal, and organic light-emitting diode displays, and other electronic devices. Applied operates in three reportable segments: Semiconductor Systems (73% of 2022 revenue, 78% of 2022 operating income), Applied Global Services (22%, 19%), and Display and Adjacent Markets (5%, 2%). Key customers include Samsung (12% of 2022 sales), Taiwan Semiconductor (20%), and Intel (10%). The company has a rising dividend bias with the current annualized dividend reaching $1.28 per share vs. the 2017 dividend of $0.43 per share and 2018's $0.64 per share.

Target Price: Reiterate $165; Rating: One

Panic Point: $120

RISKS: Manufacturing and Supply Chain, Competitive Factors, Government Regulation, Technology Change.

ACTIONS, ANALYSIS & MORE: We're Pulling This Name Up From the Bullpen, Investor Relations.

Axon Enterprise Inc.AXON; $236.38; 620 shares; 3.91%; Sector: Aerospace & Defense

WEEKLY UPDATE: Axon shares continued to be a strong performer quarter to date, rising more than 18%. That move leaves around 10% to our $260 price target, which is ahead of the Wall Street consensus near $245. As the shares move closer to our target, we'll revisit our price target, but the result may still see us downgrade AXON shares to a Two rating.

1-Wk. Price Change: 2.1% Yield: 0.00%

INVESTMENT THESIS: Axon Enterprise Inc develops, manufactures, and sells conducted energy devices and cloud-based digital evidence management software designed for use by law enforcement, corrections, military forces, private security personnel, and private individuals for personal defense. The company operates in two segments: Taser and Software & Sensors. Taser develops and sells CEDs used for protecting users and virtual reality training. Software & Sensors manufactures fully integrated hardware and cloud-based software solutions such as body cameras, automated license plate reading, and digital evidence management systems. Axon delivers its products worldwide and gets most of its revenue from the United States. President Biden's fiscal year 2023 budget requests a fully paid-for new investment of approximately $35 billion to support law enforcement and crime prevention -- in addition to the President's $2 billion discretionary request for these same programs. According to Mordor Intelligence, the wearable, and body-worn cameras market on its own was valued at $1.62 billion in 2020 and is expected to reach $424.63 billion by 2026.

Target Price: Reiterate $260; Rating: One

Panic Point: $195

RISKS: Manufacturing and supply chain, competitive factors, government regulation, technology change.

ACTIONS, ANALYSIS & MORE: Strong Demand Bodes Well for This Conducted Energy Devices Firm, Initiating a New Position in a Public Safety Technology Name, Investor Relations.

Bank of America Corp. BAC; $30.96 ; 3,615 shares; 2.98%; Sector: Financial Services

WEEKLY UPDATE: BofA's CEO Brian Moynihan joined other bank CEOs in Washington this week to warn lawmakers that the "Basel III endgame" proposal will hurt the economy and hamper lending. None of the bank CEOs indicated that their companies couldn't meet the higher capital levels in proposed rules. The impact would be far greater on smaller banks, which in our view would allow for additional share gains by the likes of Bank of America. The decline in Treasury yields this week and the move lower in mortgage rates bode well for lending activity at BofA, while the continued increase in IPO filing should eventually drive activity at its investment banking business. Appearing at the Goldman Sachs 2023 US Financial Services Conference this week, Moynihan shared his view the US economy has entered a soft landing, reiterated the company's net interest income (NII) guidance for the current quarter of $14 billion and shared its investment banking fee should be ~$ 1 billion this quarter. Moynihan went on to share that as interest rates come down, it should have a positive impact on the company's NII in 2024. BAC shares have made a nice double-digit move quarter to date, but ample upside to our $35 target remains.

1-Wk. Price Change: 0.1% Yield: 3.10%

INVESTMENT THESIS: Bank of America is one of the world's leading financial institutions, serving individual consumers, small and middle-market businesses, and large corporations with a full range of banking, investing, asset management, and other financial and risk management products and services. The company provides unmatched convenience in the United States, serving approximately 67 million consumer and small business clients with approximately 3,900 retail financial centers, approximately 16,000 ATMs, and award-winning digital banking with approximately 56 million verified digital users. Bank of America is a global leader in wealth management, corporate and investment banking, and trading across a broad range of asset classes, serving corporations, governments, institutions, and individuals around the world. Bank of America offers industry-leading support to approximately 3 million small business households through a suite of innovative, easy-to-use online products and services. The company serves clients through operations across the United States, its territories, and approximately 35 countries. From a reporting basis, the company's business breaks down as follows: Net Interest Income breakdown: Consumer Banking 57%, Global Banking 23%, Global Wealth & Investment Management 14%, and Global Markets 6%; Income Before Tax breakdown: Consumer Banking 42%, Global Banking 27%, Global Wealth & Investment Management 16%, and Global Markets 15%. Bank of America pays a quarterly dividend of $0.22 per share.

Target Price: $35; Rating: One

Panic Point: $24

RISKS: Financial markets, fiscal, monetary, and regulatory policies, economic conditions, and credit ratings.

ACTIONS, ANALYSIS & MORE: We're Upgrading and Building Upon a Position, We're Initiating a Bank Position, Investor Relations

Coty Inc. COTY; $11.62; 12,850 shares; 3.98%; Sector: Consumer Discretionary

WEEKLY UPDATE: Coty shares continued to move higher this week following an upbeat presentation at the Morgan Stanley Global Consumer & Retail Conference. Those gains added to the impressive mover over the last month, which have led COTY shares to become the portfolio's largest holding. During the conference presentation, the company shared it continues to make progress on lowering the cost of goods sold for its consumer beauty business. It also reiterated its goal to deliver several percentage points of margin improvement over the next few years even as it continues to invest in advertising and promotional activity. We are in the seasonally strongest time of the year for Coty's business, one that extends through the holiday shopping season to mid-February. The company's Board recently bumped up its share repurchase program to $1 billion, and Coty is expected to repurchase 27 million shares in its March 2024 quarter, 23 million shares in fiscal 2025, and 25 million shares in fiscal 2026. This offers another layer of support for COTY stock and is another reason to think consensus calendar 2024 EPS expectations are conservative. While the AAP portfolio has a full position in the shares, we continue to rate COTY shares a "One" at current levels.

1-Wk. Price Change: 0.3%; Yield: 0%

INVESTMENT THESIS: Founded in Paris in 1904, Coty is one of the world's largest beauty companies with a portfolio of iconic brands across fragrance, color cosmetics, and skin and body care. Coty serves consumers around the world, selling luxury and mass-market products in more than 130 countries and territories. The company derives almost 45% of its revenue from the Americas, 44% from Europe, the Middle East and Africa, and the balance from Asia Pacific. By revenue category, Prestige drives 62% of Coty's revenue but more than 80% of its operating income with the balance derived from its Consumer Beauty segment. Management intends to further grow the Prestige business, expanding its prestige fragrance brands, through the ongoing expansion into prestige cosmetics, and the building of a comprehensive skincare portfolio leveraging existing brands. Management is also targeting margin improvement at its Consumer Beauty brands as well as expanding its presence in China across both of its reporting segments. China's beauty and personal care market is expected to grow at a quicker pace of 5.4% per annum through 2027, putting it at $70 billion-$75 billion by 2027.

Target Price: $15; Rating: One

Panic Point: $9

RISKS: Industry competition and consolidation, product efficacy and safety, currency, and brand licensing.

ACTIONS, ANALYSIS & MORE: We're Making Our Portfolio a Little More Beautiful Today, We're Adding a Name to the Bullpen, Investor Relations.

Elevance Health Inc. ELV; $477.97; 275 shares; 3.50%; Sector: Health Care

WEEKLY UPDATE: Elevance pulled back this week from a very strong overbought condition. The stock made new relative highs (not all-time highs) recently and with the indicators and the rest of the market strong it was time for a breather. The stock remains in a solid uptrend of higher highs, higher lows. That is the textbook definition of an uptrend. However, a bit more downside is likely with the 20-day moving average coming into view, circa $470.50. A pullback to that level might trigger some buying before the end of the year.

1-Wk. Price Change: -1%; Yield: 1.2%

INVESTMENT THESIS: Elevance, formerly Anthem/Blue Cross Health, is a premier healthcare brand that appears to be in the sweet spot for HMO companies. Mostly domestic, this company has a wide reach and coverage across the U.S., serving more than 118 million people via medical, pharmacy, clinical, and care solutions. Founded in 1944, Elevance offers a terrific business model that works in boom or bust economic times. The opportunity to find a company with reliable and dependable revenue and cash flows is right here with Elevance. Revenue growth for this company has surged in recent years, with better than double-digit growth since 2018 as the company thrived during the pandemic.

Target Price: Reiterate $550; Rating: One

Panic Point: $410

RISKS: With any insurance business the risk is high for changes in regulation and government programs. Since the onset of Obamacare more than 10 years ago, companies like Elevance have changed their model to be more in line with a better cost/benefit analysis, reducing waste and squeezing out excesses (as was outlined and suggested in Obamacare). Separately, as the population increases and ages, there is more opportunity for Elevance to grow, but with those changes, there is a risk. Lastly, competition is brisk with some very strong opponents who keep their costs low (Humana, Cigna, UNH, CVS/Healthnet).

ACTIONS, ANALYSIS & MORE: We're Trimming One Stock to Add to Another,2021 Annual Report, 2Q 2022 Earnings Report, Investor Relations.

PepsiCo Inc.PEP; $165.68 ; 800 shares; 3.53%; Sector: Consumer Defensive

WEEKLY UPDATE: With panic over weight loss drugs having subsided and fresh data that pointed to consumers re-embracing eating at home to save money and control their budget, we added to our PEP position this week. During the week Barron's published a piece on PepsiCo noting its consistent business, prospects for margin improvement in the coming quarters and its status as a Dividend Aristocrat, all of which make it a stock to own. We certainly agree.

1-Wk. Price Change: -1.8%; Yield: 3.1%

INVESTMENT THESIS: PepsiCo is one of the largest food-and-beverage companies globally. It makes, markets, and sells a slew of brands across the beverage and snack categories, including Pepsi, Mountain Dew, Gatorade, Doritos, Lays, and Ruffles. The firm uses a largely integrated go-to-market model, though it does leverage third-party bottlers, contract manufacturers, and distributors in certain markets. In addition to company-owned trademarks, Pepsi manufactures and distributes other brands through partnerships and joint ventures with companies such as Starbucks. The combination of the consumable nature of those products along with PepsiCo's ability to realize price increases has led to consistent revenue, EPS, and dividend growth during both the Great Recession and the Covid pandemic.

Target Price: Reiterate $210; Rating: One

Panic Point: $140

RISKS: Economic conditions, supply chain constraints, raw material costs.

ACTIONS, ANALYSIS & MORE: Adding to 2 Positions on Market Weakness, We're Initiating 1 Name While Adding to Another, This Stock Should Have 'Pep,' Even in a Recession, Investor Relations

Vulcan Materials Company VMC; $216.03; 613 shares; 3.53%; Sector: Building Materials

WEEKLY UPDATE: While there was no company specific news, we noted the consensus 2024 EPS forecast for the company has inched up over the last week or so to $8.06 from $7.99 and the expected $6.90 for 2023. Not a massive boost, but one that reflects a full year of infrastructure spending and prospects for an incrementally better housing market given the recent backing off in mortgage rates. With the impact of the CHIPs Act and EV charging station infrastructure dollars yet to be felt, we could see a few more rounds of upward adjustments for 2024 EPS.

1-Wk. Price Change: 0.2% Yield: 0.8%

INVESTMENT THESIS: Vulcan Materials operates primarily in the U.S. and is the nation's largest supplier of construction aggregates (primarily crushed stone, sand, and gravel), a major producer of asphalt mix and ready-mixed concrete, and a supplier of construction paving services. Its products are the indispensable materials used in building homes, offices, places of worship, schools, hospitals, and factories, as well as vital infrastructure including highways, bridges, roads, ports and harbors, water systems, campuses, dams, airports, and rail networks. Ramping spending associated with the Biden Infrastructure Law should drive demand for Vulcan's products over the coming years. Vulcan has historically complemented its organic growth prospects by acquiring businesses to expand its geographic reach and product scope. Since 2014, the company has acquired more than two dozen companies, including the 2021 acquisition of U.S. Concrete. That combination has allowed the company to deliver steady top and bottom-line growth over the last decade, with only a modest decline when the pandemic hit in 2020.

Target Price: Reiterate $245; Rating: One

Panic Point: $175

RISKS: General economic and business conditions; dependence on the construction industry; timing of federal, state, and local funding for infrastructure; changes in the level of spending for private residential and private nonresidential construction.

ACTIONS, ANALYSIS & MORE: Initiation Post, Investor Relations

TWOs

Apple AAPL; $195.71; 700 shares; 3.65%; Sector: Technology

WEEKLY UPDATE: Apple got a nice pop this week on strong turnover. The stock made a run Monday to the 20-day moving average and powered right up. Tuesday was a bold move for the stock as its major iPhone manufacturer Foxconn raised their guidance. Reports out on Friday indicated Apple and its suppliers aim to build more than 50 million iPhones in India annually within the next two to three years, with additional tens of millions of units planned after that. No doubt the company is using in-country efforts to sweeten its relationship with India to tap its demographically friendly population for its products and services. Today, Apple has a relatively small share of the India smartphone market, well behind Samsung, Xiaomi, Vivo, and others. The opportunity, however, remains large as India is expected to exit 2023 with ~130 million 5G users compared to its ~1.4 billion population. Also on Friday, Morgan Stanley upped Apple's price target to $220 from $210 and kept an Overweight rating. Finally, it appears Apple remain on track to update its line of iPads and other devices in 1H 2024. Apple also plans to release its Vision Pro headset early next year. For later in 2024, it's working on an updated Apple Watch and revamped low-end and mid-tier AirPods that add a USB-C port.

1-Wk. Price Change: 2.3% Yield: 0.5%

INVESTMENT THESIS: While we acknowledge that near-to-midterm performance remains heavily influenced by iPhone sales, the dynamic is shifting as investors finally place greater emphasis on Services growth. We are bullish on the 5G upgrade cycle and believe longer-term upside will continue to come as Services revenue grows its share of overall sales. Services provide for a recurring revenue stream at higher margins, a factor that serves to reduce earnings volatility while allowing for a higher percentage of sales to fall to the bottom line; as a result, we believe that Services growth and the installed base, are much more important than how many devices the company can sell in each 90-day period. In addition to improved profitability, we also believe the transparent nature of this revenue stream will demand an expanded price-to-earnings multiple as segment sales grow. Furthermore, we believe that Apple's desire to push deeper into the healthcare arena will help make its devices invaluable as more life-changing features are added and the company works to democratize health records. Lastly, also see upside resulting from increased adoption of wearables (think the Apple Watch) and potential new product announcements such as an AR/VR headset or an update on Project Titan, the company's secretive autonomous driving program.

Target Price: Reiterate $195; Rating: Two

Panic Point: Reiterate $160

RISKS: Slowdown in consumer spending, competition, lack of new product innovation, elongated replacement cycles, failure to execute on Services growth initiative.

ACTIONS, ANALYSIS & MORE:FY3Q21 Earnings Analysis (7/27/21), Apple Product Launch Event Takeaways (4/20/21), Takeaways from WWDC (6/22/20), Initiation (1/4/10), Investor Relations

Costco Wholesale COST; $610.78; 240 shares; 3.91%; Sector: Consumer Staples

WEEKLY UPDATE: Costco will report its quarterly results on Thursday, December 14 after the market close. Consensus expectations have the company delivering EPS of $3.41 on revenue of $57.7 billion and guide its February quarter to EPS of $3.62 on revenue of $58.85 billion. During the earnings call, we'll be interested in the company's comments on holiday shopping but also inflation and where it may be seeing deflation. We will again be listening for comments about the much-expected membership price increase, something we think is only a matter of time. Hand in hand with that, we will be looking for an update on Costco's warehouse expansion plan, a harbinger for its high margin membership fee revenue stream. As we digest all that, we will be contemplating our price target, which currently sits at $625.

1-Wk. Price Change: 2.4% Yield: 0.7%

INVESTMENT THESIS: We like Costco's long-term prospects, driven by a club-based operating model that focuses on volumes, not margins, and therefore offers its customers a value proposition of everyday low prices. The strength of this model has created an incredibly loyal customer base with low churn and continued share gains in both bricks-and-mortar and e-commerce. And this is a global concept, evidenced by the strength of sales both in the U.S. and abroad, which includes an emerging China opportunity. We see the company's membership model as a key differentiator vs. other retailers and its plans to open additional warehouse locations in the coming quarters should drive retail volumes and the higher-margin membership fee income as well. We also appreciate management's approach to capital returns and their willingness to return cash when it is in excess on the balance sheet.

Target Price: Reiterate $625. Rating: Two

Panic Point: $525

RISKS: Inability to pass through higher costs, fuel prices, weaker consumer, and membership churn.

ACTIONS, ANALYSIS & MORE: FY4Q21 Earnings Analysis (9/23/21), FY2Q21 Earnings Analysis (3/4/21), Upgrading Costco to a One (2/25/21), $10 Per Share Special Dividend (11/16/20), Recent Buy Alert (2/28/20), Initiation (1/27/20), Investor Relations

Deere & Co. DE; $363.67; 357 shares; 3.46%; Sector: Farm Machinery & Equipment

WEEKLY UPDATE: During the week we shared that, as expected, consensus calendar 2024 EPS for DE has moved lower. We continue to see DE shares as a "show me" margin story for the next few quarters. Friday's December World Agricultural Supply and Demand Estimates (WASDE) report showed an unchanged outlook for 2023/24 U.S. wheat with higher exports and reduced ending stocks with the same for corn and soybeans. This suggests modest changes to those key commodity types and should support farmer income and the ag equipment upgrade cycle. Also on Friday, Deer's board hiked its quarterly cash dividend by 9% to $1.47 per share. The new quarterly dividend brings the company's annualized dividend rate to $5.88 per share. This first of this new dividend will be paid out on Feb 8 to shareholders of record as of Dec 29, 2023.

1-Wk. Price Change: -1.4% Yield: 1.6%

INVESTMENT THESIS: The global agriculture equipment market size is expected to reach $166.5 billion in 2027, growing at a 6% CAGR over the 2020-2027 period. The favorable outlook for equipment purchases in the coming quarters reflects rising farmer income that historically drives new equipment purchases. At the same time, Deere continues to lean into the sustainability movement with its precision ag offering. That technology is helping farmers drive crop yields higher while also realizing cost savings, which makes the new technology a productivity upgrade compared to older equipment. In February, Deere announced a 4.2% in its quarterly dividend per share to $1.25 from $1.20.

Price Target: Reiterate $435; Rating: Two.

Panic Point: $315

RISKS: Geopolitical uncertainty, economic conditions, raw material, and other input prices, prices for key agricultural commodities.

ACTIONS, ANALYSIS & MORE: Initiation (10/25/21), Investor Relations

First Trust Nasdaq Cybersecurity ETF CIBR; $51.04 ; 2,900 shares; 3.94%; Sector: Cybersecurity

WEEKLY UPDATE: CIBR shares continued to inch ahead this week, pushing their quarter to date gain firmly into double-digits and well ahead of the major market averages. During the week Amazon CEO Andy Jassy reminded us of the dark side about AI that is data security and privacy as AI will be used to scale phishing, information operations and other campaigns. We see that as another growth vector in addition to IoT and ransomware as a service for cybersecurity spending. We continue to see cybersecurity as a core investor holding but with CIBR shares in overbought territory, we would recommend new subscribers and one's underweight CIBR shares wait for a pullback in the shares near the $46 level. However, given the moves in CIBR shares we will lift our panic point to $42 from $38.50,

1-Wk. Price Change: 1.4% Yield: 0%

INVESTMENT THESIS: The First Trust Nasdaq Cybersecurity ETF seeks investment results that correspond generally to the price and yield (before the fund's fees and expenses) of an equity index called the Nasdaq CTA Cybersecurity Index. The Nasdaq CTA Cybersecurity Index is designed to track the performance of companies engaged in the cybersecurity segment of the technology and industrial sectors. It includes companies primarily involved in the building, implementation, and management of security protocols applied to private and public networks, computers, and mobile devices to protect the integrity of data and network operations. To be included in the index, a security must be listed on an index-eligible global stock exchange and classified as a cybersecurity company as determined by the Consumer Technology Association. Each security must have a worldwide market capitalization of $250 million, have a minimum three-month average daily dollar trading volume of $1 million, and have a minimum free float of 20%.

Target Price: Reiterate $62; Rating: Two

Panic Point: Increase to $42 from $38.50

RISKS: Cybersecurity spending, technology, and product development, the timing of product sales cycle, new products, and services in response to rapid technological changes and market developments as well as evolving security threats.

ACTIONS, ANALYSIS & MORE: We're Swapping One Cybersecurity Stock for Another, ETF Product Summary

Lockheed Martin Corp. LMT; $448.02; 295 shares; 3.52%; Sector: Aerospace & Defense

WEEKLY UPDATE: Lockheed Martin continues to rack up more contract wins with the US government. However, the stock continues to dance around the 200-day moving average on lower turnover. This tells us the area could be an inflection point, meaning LMT is ready to make a move in one direction or the other. Technical indicators are flat, the MACD is not showing us much while the relative strength hovers neutral. Flat is the new 'Up' for LMT. On Friday it appeared House and Senate lawmakers cleared the way for passage of the nearly $900 billion defense and national security policy bill clearing the way by the end of the year. That gave some lift to defense contractors, including our shares of Lockheed Martin as that overhang looks to be removed. The proposal calls for roughly $170 billion to buy helicopters, combat vehicles, Navy submarines, and weapons such as bombs and rockets. It also includes a $1.9 billion, 684-foot-long ship to transport Marines, anchor overseas security operations, and provide humanitarian aid to struggling regions. Rounding out the bill is $145 billion for research and technology development and $300 million for security assistance to help fortify Ukraine's military. All in all, we see it adding to Lockheed's multi-year backlog, but we still want to see progress on margins as well as F-35 deliveries.

1-Wk. Price Change: -0.3% Yield: 2.8%

INVESTMENT THESIS: Lockheed Martin is the largest defense contractor globally and has dominated the Western market for high-end fighter aircraft since the F-35 program was awarded in 2001. Lockheed's largest segment is aeronautics, which is dominated by the massive F-35 program. Lockheed's remaining segments are rotary and mission systems, which is mainly the Sikorsky helicopter business; missiles and fire control, which creates missiles and missile defense systems; and space systems, which produces satellites and receives equity income from the United Launch Alliance joint venture. Historically, the stability of defense spending has been a haven during periods of economic uncertainty, and we see that repeating once again even as geopolitical conflicts are likely to lead to incremental demand for Lockheed's products. The company has increased its dividend consistently over the last 19 years and is widely expected to boost it again in the coming days. In October 2022, Lockheed announced its board authorized the purchase of up to an additional $14.0 billion of LMT stock under its share-repurchase program.

Target Price: $520; Rating: Two

Panic Point: $360

RISKS: Contracts and budget risk with the U.S. government and the Department of Defense, F-35 program funding and renewal, competition, and subcontractor issues.

Marvell Technology Inc.MRVL; $52.88; 2,340 shares; 3.3%; Sector: Technology

WEEKLY UPDATE: In last week's Roundup, we shared a pullback to the $50-$52 would be an area at which we would look to add to our MRVL position. That's what we did this week when the shares were just below $51. During the week AMD (AMD) updated its outlook of the AI chip industry, forecasting it could climb to more than $400 billion in the next four years, more than twice as high as the company's projection this past August. Later in the week, Broadcom (AVGO) confirmed the strong demand for data center and AI chips as well as networking related equipment and chips. The next catalyst we are watching for its November revenue from Taiwan Semiconductor.

1-Wk. Price Change: 0.2%; Yield: 0.5%

INVESTMENT THESIS: Marvell is a fabless supplier of high-performance standard and semi-custom infrastructure semiconductor solutions. These solutions power the data economy, enabling the data center, carrier infrastructure, enterprise networking, consumer, and automotive/industrial end markets. With roughly 75%-80% of Marvell's revenue stream tied to digital infrastructure, we see it continuing to benefit from rising content consumption and creation. Pointing to that rising demand that necessitates network densification and the build of digital infrastructure, Ericsson sees global monthly average usage per smartphone reach 46 gigabytes (GB) by the end of 2028 vs. 19 GB in 2023 and 15 GB in 2022.

Target Price: Reiterate $62; Rating: Two

Panic Point: $45

RISKS: Technology risk, customer risk, competition risk, reliance on manufacturing partners, and supply chain constraints.

ACTIONS, ANALYSIS & MORE: We're Watching These Three Names Set to Report Thursday, Why We Added This Chip Stock to the Bullpen, Investor Relations.

Mastercard MA; $412.16; 275 shares; 3.02%; Sector: Info. Tech

WEEKLY UPDATE: Mastercard boosted its quarterly cash dividend by 16% to $0.66 per share from $0.57 and announced its board approved a new $11 billion share repurchase program. The cash dividend will be paid Feb. 9, 2024, to holders of record as of Jan. 9, 2024. The new repurchase program will kick in once Mastercard utilizes the remaining $3.5 billion authorized under its existing $9 billion repurchase program. No expiration date for the new buyback program was announced, which suggests it will span more than just a few quarters. Even so, it helps support the earnings-per-share growth of 17% that Wall Street expects Mastercard to deliver in 2024. In mid-November, we lifted our MA price target to $425 from $410, and the combination of these two new announcements led us to increase it once again to $440. Late in the week, BMO Capital initiated coverage on MA shares with an Outperform rating and a $475 target, calling the shares a "core holding in US Financials."

1-Wk. Price Change: -0.5% Yield: 0.6%

INVESTMENT THESIS: Mastercard is a card network company that benefits from the secular shift away from cash transactions and toward card-based and electronic payments. On Covid-19 dynamics, we view MA as a "reopening" play and an economic recovery play within technology because its cross-border volumes fell sharply during the pandemic but will rebound as mobility increases and travel restrictions ease. Mastercard has more international exposure relative to Visa, making its growth outlook more susceptible to new travel restrictions. However, we view MA as the better long-term play as we are betting on that inevitable recovery.

Target Price: Reiterate $440 Rating: Two

Panic Point: $350

RISKS: The recovery in cross-border transactions, regulation in the payments market, competition from other fintechs, pricing pressures.

McDonald's Corp. MCD; $285.53; 410 shares; 3.12%

WEEKLY UPDATE: At its Investor Day this week, management shared McDonald's will lean into its strength in burgers and chicken with new menu offerings in the coming quarters. Management also plans to increase its active loyalty user base to 250 million 90-day active users and deliver $45 billion in annual systemwide sales to loyalty members by 2027. The company also shared plans to accelerate the pace of restaurant openings, targeting expansion to 50,000 restaurants by the end of 2027, up from 40,275 entering 2023. Those targets put McDonald's back in growth mode, but more importantly management guided the company's 2024 operating margin to be in the mid-to-high 40% range, which suggest it should be able to stomach these initiatives without missing a beat. As part of that effort, McDonald's announced a strategic partnership with Google Cloud during its investor event that will include the roll out of generative AI across its digital platforms at its restaurants, kiosks, and the company's mobile app. Finally, the company intends to roll out 10 new locations for its new, small store format, CosMC's, that will feature customizable specialty beverages to challenge Starbucks (SBUX) and Dunkin' Donuts. It will also serve snacks - including a few of its classic menu items. All the above keeps us bullish on MCD shares and led JP Morgan to lift its MCD price target to $300 from $285, while Cowen upped its target to $325, matching ours.

1-Wk. Price Change: -0.2%; Yield: 2.3%

INVESTMENT THESIS: The company franchises and operates McDonald's restaurants, which serve a locally relevant menu of quality food and beverages in communities across more than 100 countries. Of the 40,275 McDonald's restaurants at year-end 2022, approximately 95% were franchised. The US market accounts for ~40% of total revenue, International 50%, and International Developmental Licenses Markets & Corporate ~10%. With consumers facing continued inflation pressures, we see McDonald's winning consumer wallet share as it benefits from pricing action put in place in recent quarters and improving input costs.

Target Price: $325; Rating Two

Panic Point: $240

RISKS: Consumer spending, competition, supply chain interruption, franchise business model, employment challenges.

ACTIONS, ANALYSIS & MORE: We're Moving This Bullpen Name Up to the Portfolio, Here's Why We're Adding This Name to the Bullpen, McDonald's Investor Relations.

Microsoft Corp. MSFT; $374.51; 325 shares; 3.24%; Sector: Technology

WEEKLY UPDATE: Microsoft has had a volatile couple of weeks. Just after Thanksgiving the stock nailed an all-time high of $384 but subsequently corrected before recovering some of that move lower this week. MSFT shares remain below the 20-day moving average but with some push above we could see another new all-time high potentially before year-end or in early 2024. The technical are strong, MACD recently rolled over but that is not unexpected after a sharp move higher in November. Relative strength has even turned up here, and money flows are still strong. In news, The UK's Competition and Markets Authority is seeking views from interested parties to address whether Microsoft's $10 billion investment in OpenAI has led to a "relevant merger situation," where two or more businesses have ceased or will cease to be distinct because of a transaction. While this ask is likely to attract comments from some competitors, it looks more like another round of sour grapes for the UK because it lacks a serious contender in the AI race. We're not going to outright dismiss this because it could lead to some headline risk, but in our view, this is more noise than anything else.

1-Wk. Price Change: -0.1% Yield: 0.8%

INVESTMENT THESIS: We believe the cloud to be a secular growth trend and that upside to shares will result from Microsoft's hybrid cloud leadership as the company grabs market share in this expanding industry. While companies may look to build out multi-cloud environments, Microsoft's Azure offering will be a prime choice thanks to the company's decision to provide the same "stack" used in the public cloud, to companies for their on-premises data centers. Additionally, we would note that hybrid environments are currently the preference for most companies because they allow them to maintain critical data in-house while taking advantage of the agility and scalability provided by public clouds. Outside of the cloud opportunity, we maintain a positive view on the company's growing gaming business, which we believe is becoming an increasingly prominent factor in the Microsoft growth story as gaming becomes more mainstream, management works to convert its gaming revenue from one-time license purchase to a recurring subscription model and as technologies like augmented/virtual reality evolve. Finally, as it relates to LinkedIn and other subscription-based services such as O365 and various Dynamics products, we continue to value them highly for their recurring revenue streams, which we remind members, to provide for greater transparency of future earnings. Quarter to date, MSFT shares are up nearly 18%.

Target Price: $390; Rating: Two

Panic Point: Reiterate $300

RISKS: Slowdown in IT spending, competition, cannibalization of on-premises business by the cloud.

ACTIONS, ANALYSIS & MORE: FY4Q21 Earnings Analysis (7/27/21), Ignite 2021, Microsoft Acquires ZeniMax (9/22/20), CEO Satya Nadella on CNBC (3/25/20), CEO Satya Nadella speaks at the World Economic Forum (1/23/20)

Morgan Stanley MS; $82.28 ; 460 shares; 1.01%

WEEKLY UPDATE: We called up MS shares from the Bullpen this week to the active portfolio with a $90 price target. With a "Two" rating for MS shares, it means we would look to pick up additional shares at lower levels. We previously discussed the $72-$74 level, and from a fundamental perspective, we would be more aggressive in picking up MS shares at such levels. From a technical one, they have support at their 20-day moving average ($78.47) and 50-day moving average ($76.71), and if successfully tested could give us some opportunities to nibble.

1-Wk. Price Change: 2.7%; Yield: 4.1%

INVESTMENT THESIS: Morgan Stanley reports in three business segment: Institutional Securities (42% of trailing 12-month revenue, 38% of trailing 12-month Income Before Tax), Wealth Management (48%, 55%) and Investment Management (10%, 6%). While the IPO window has yet to reopen, the potential IPO class for 2024 continues to build with recent additions including Panera Bread, Reddit, Fanatics, and Skims, which is backed by Kim Kardashian. This along with the Fed increasingly likely to start cutting rates in 1H 2024, suggests we are far closer to the IPO window opening on a sustained basis than we have been in some time. That would be a boon to private equity firms and others that have been nursing IPO candidates during the dark period and a positive for Morgan's investment banking business. Marginally lower rates could also generate a pick-up in M&A activity as the cost of capital with rates improving. As the Fed continues its cutting cycle to get rates back to normalized levels, that effort would also reduce rates for stock market alternatives, ones that quashed the "there is no alternative" trade earlier this year. That along with folks continuing to be behind in retirement savings bodes well for Morgan's wealth management business in the coming quarters.

Target Price: $90; Rating Two

Panic Point: $68

RISKS: Market and interest rate risk, credit risk, country risk, and operational risk, including cybersecurity.

ACTIONS, ANALYSIS & MORE: We're Exiting Chipotle, Initiating Morgan Stanley, and Adding to 2 Names, We're Closely Eyeing Morgan Stanley as an IPO Boost Looks Likely, Investor Relations.

ProShares Short QQQ ETF PSQ; $10.07; 4,070 shares; 1.09%

WEEKLY UPDATE: With the market in overbought territory, the Cboe Volatility Index (VIX) signaling investor complacency and investors still in Greed mode exiting the week, we will continue to own this Nasdaq inverse ETF ahead of the Fed's policy meeting next week. Friday's stronger than expected November Employment Report pushed back on the number of rate hikes the market expects in 2024. With the market "priced to perfection", it would not take much for it to give back some of the strong gains put in during November. When the Fed shifts its tone to being more dovish from neutral, subject to the market's technical set up at the time, will revisit owning PSQ shares in the portfolio.

1-Wk. Price Change:-0.4%; Yield: 0.0%

INVESTMENT THESIS: ProShares Short QQQ seeks daily investment results, before fees and expenses, that correspond to the inverse (-1x) of the daily performance of the Nasdaq 100 Index. The Nasdaq 100 Index includes 100 of the largest domestic and international non-financial companies listed on The Nasdaq Stock Market based on market capitalization.

Target Price: N/A; Rating Two

RISKS: Because PSQ shares track the inverse of the Nasdaq 100 Index, PSQ shares will move lower when the Nasdaq 100 Index moves higher.

ACTIONS, ANALYSIS & MORE: Selling Shares in 1 Position, Closing Another, Adding to 1, and Initiating 1

ProShares Short S&P 500 ETF SH; $13.64; 3,310 shares; 1.2%

WEEKLY UPDATE: With the market in overbought territory, the Cboe Volatility Index (VIX) signaling investor complacency and investors still in Greed mode exiting the week, we will continue to own this S&P 500 inverse ETF ahead of the Fed's policy meeting next week. Friday's stronger than expected November Employment Report pushed back on the number of rate hikes the market expects in 2024. With the market "priced to perfection", it would not take much for it to give back some of the strong gains put in during November. When the Fed shifts its tone to being more dovish from neutral, subject to the market's technical set up at the time, will revisit owning SH shares in the portfolio.

1-Wk. Price Change: -0.1%; Yield: 0.0%

INVESTMENT THESIS: The Pro Shares Short S&P 500 ETF seeks daily investment results, before fees and expenses, that correspond to the inverse (-1x) of the daily performance of the S&P 500. We are using SH shares to blunt market volatility and hedge the portfolio's performance against its benchmark, the S&P 500. Given the tactical nature of this position, we do not expect to hold SH shares for the same length of time as we do the portfolio's long positions.

Target Price: N/A; Rating Two

RISKS: Because SH shares track the inverse of the S&P 500, SH shares will move lower when the S&P 500 moves higher.

ACTIONS, ANALYSIS & MORE: Selling Shares in 1 Position, Closing Another, Adding to 1, and Initiating 1.

Qualcomm Inc. QCOM; $132.97 ; 1,005 shares; 3.56%

WEEKLY UPDATE: Broadcom (AVGO)'s wireless revenue rose 23% sequentially during its October quarter, benefitting from the rebound in the smartphone market. During the week, Morgan Stanley shared its findings the smartphone industry is poised for a recovery that is not "priced into the shares" of Qualcomm. That view is based on the adoption of Edge AI or artificial intelligence running on user devices, including smartphones. That plays into Qualcomm's chipset strengths as well as its AI related efforts for the IoT market. The next catalyst we are watching for its November revenue from Taiwan Semiconductor.

1-Wk. Price Change: 2.5%; Yield: 2.4%

INVESTMENT THESIS: Qualcomm focuses on foundational technologies for the wireless industry, including 3G (third generation), 4G (fourth generation), and 5G (fifth generation) wireless technologies and processor technologies including high-performance, low-power computing, and on-device artificial intelligence technologies. As a connected processor company, its technology roadmap aims to enable the connected intelligent edge (the next generation of smart devices) across industries and applications beyond handsets, including automotive and the Internet of Things (IoT). Qualcomm has three reportable segments: QCT (Qualcomm CDMA Technologies) semiconductor business, which develops and supplies integrated circuits and system software based on 3G/4G/5G and other technologies for use in mobile devices; automotive systems for connectivity, digital cockpit, and ADAS/AD; and IoT including consumer electronic devices; industrial devices; and edge networking products. QCT accounts for 80%-85% of revenue. QTL (Qualcomm Technology Licensing) licensing business grants licenses or otherwise provides rights to use portions of the company's intellectual property portfolio, which includes certain patent rights essential to and/or useful in the manufacture and sale of certain wireless products. QTL accounts for ~15% of Qualcomm's revenue but contributes a greater portion of the company's operating income. The company has been paying a quarterly dividend since 2003, and its next quarterly dividend of $0.80 per share will be paid on September 21 to shareholders of record on August 31.

Target Price: $150; Rating Two

Panic Point: $108

RISKS: Customer risk, technology advancement, competition risk, third-party supplier, and manufacturing partner risk.

ACTIONS, ANALYSIS & MORE: We're Making Another Call to the Portfolio's Bullpen, Here's When We'd Consider Taking a Position in Qualcomm, Qualcomm Investor Relations

SPDR Gold Shares ETF GLD; $185.66 ; 312 shares; 1.54%; Sector: Commodities

WEEKLY UPDATE: It was hard to argue with that surge in gold last week being anything but bullish. The ETF closed the week at an all-time high level and traded off some this week, which we chalk up to short-term profit taking given that GLD has surged more than 15% over the past two months. Recent developments in Japan (tighter monetary policy) with a stronger yen should also help give gold a boost as yen sellers move money to the metal. Gold is up a solid 10% in 2023 after a flat 2022. We see gold making a run towards $2,500 over time. Gold is a great asset class which offers diversification and a hedge for safety in times of war, conflict, and inflation.

1-Wk. Price Change: -3.3% Yield: 0.0%

INVESTMENT THESIS: The GLD ETF is a proxy for gold. This "trust" buys and sells gold futures each day to mimic the daily moves in the underlying asset, in this case, gold. We see gold as an ideal hedge against a weaker dollar, strong inflation (which tends to weaken the dollar) alternative, and in uncertain times (worry over war and battles). For the past 15 years, gold has been a strong asset class held by fund managers, countries, and banks. The metal is not correlated with markets and will move based on the demand/supply dynamic in the marketplace. Other precious metals such as silver and platinum are good proxies for the criteria stated earlier, however, gold is far more liquid and offers better upside opportunities.

Target Price: Reiterate $200; Rating: Two

Panic Point: $165

RISKS: Weak inflation data, interest rate risk, dollar strength relative to other currencies, geographic risk.

The Energy Select Sector SPDR Fund XLE; $82.23 ; 1,140 shares; 2.5%; Sector: Energy

WEEKLY UPDATE: We added to our XLE shares late this week, recognizing we are nearing the end of the seasonally weak period for oil and additional OPEC+ production cuts will begin in the coming weeks. That combination suggests a potential rebound in oil prices, especially if upcoming economic data doesn't fall out of bed. What's more, continued "Goldilocks" data for the U.S. and economic data out of China that isn't as bad as feared would support higher oil prices. We recognize that we may be a tad early with this move, but we also have room to scale out the position a bit further. Data that bolster the soft-landing, Goldilocks narrative, would support such a move. Alongside this trade, we upgraded XLE shares to a Two from Three rating, trimmed our price target to $90 from $98, and lowered our panic point to $75 from $82.50.

1-Wk. Price Change: -3.3%; Yield: 4%

INVESTMENT THESIS: The Energy Select Sector SPDR Fund is an exchange-traded fund that tracks the performance of the Energy Select Sector Index. The ETF holds large-cap U.S. energy stocks. It invests in companies that develop & produce crude oil & natural gas and provide drilling and other energy-related services. The holdings are weighted by market capitalization.

Target Price: Reiterate $90; Rating: Two

Panic Point: $75

RISKS: Interest rates, weakness in the broad economy, energy prices.

ACTIONS, ANALYSIS & MORE: Adding to 2 Positions on Market Weakness, We're Initiating a Position in the Energy Sector, State Street Global Advisors SPDR Fact Sheet for XLE.

Trinity Capital Inc. TRIN; $14.83 ; 4,610 shares; 1.82%

WEEKLY UPDATE: Trinity announced the commitment of $45 million in growth capital to Neurolens, a company commercializing innovative solutions to optimize vision. This is the latest investment that should drive the company's investment income higher in the coming quarters. Exiting the September quarter that investment portfolio had an aggregate fair value of approximately $1.1 billion and was comprised of $840.7 million in secured loans, $223.2 million in equipment financings, and $52.7 million in equity and warrants across 121 portfolio companies. We would look to add to our TRIN holding near $14.

1-Wk. Price Change: 0.3%; Yield: 14.6%

INVESTMENT THESIS: Trinity Capital is a Business Development Company that provides debt, including loans and equipment financing to growth-stage companies, including venture-backed companies and companies with institutional equity investors. Trinity aims to generate current income and, to a lesser extent, capital appreciation through its investments. It does this by making investments consisting primarily of term loans and equipment financings and, to a lesser extent, working capital loans, equity, and equity-related investments. Because Trinity is a BDC, it must pay out at least 90% of its net income to shareholders in the form of dividends. Trinity is positioned to fill the gap left by recent bank failures and shareholders should benefit as that lifts the company's investment portfolio and income stream, and its dividend payout to shareholders.

Target Price: $16; Rating Two

Panic Point: $12

RISKS: Global economic, political, and market conditions; regulations governing our operations as a BDC; credit facility provisions

ACTIONS, ANALYSIS & MORE: Let's Dig Into the Thesis Behind Our Newest Position, As Banks Start Tightening Up on Loans, Let's Check This Bullpen Stock, Listen as We Make a Bullpen Pick -- and Talk Business Development Cos.; Investor Relations.

United Rentals URI; $495.06; 300 shares; 3.96%; Sector: Industrials

WEEKLY UPDATE: Following our recent trim of URI shares and the downgrade to a Two rating, this week the shares were downgraded to Sector Weight at KeyBank while UBS cuts the shares to a Neutral rating. As we noted with our comments for Vulcan Materials, 2024 brings a full year of infrastructure spending but we should also see the start of the CHIPs Act and EV charging station infrastructure dollars. As interest rates fall, that could stimulate housing demand as well as other construction projects. All in all, we could see a few more rounds of upward EPS adjustments for United Rentals next year.

1-Wk. Price Change: -1.3% Yield: 1.2%

INVESTMENT THESIS: United Rentals, the largest equipment rental company in the world, operates throughout the United States and Canada, and has a limited presence in Europe, Australia, and New Zealand. It serves industrial and other non-construction; commercial (or private non-residential) construction; and residential construction. Industrial and other non-construction rentals represented approximately 50% of rental revenue, primarily reflecting rentals to manufacturers, energy companies, chemical companies, paper mills, railroads, shipbuilders, utilities, retailers, and infrastructure entities; commercial construction rentals represented approximately 46% of rental revenue, primarily reflecting rentals related to the construction and remodeling of facilities for office space, lodging, healthcare, entertainment, and other commercial purposes; and residential rentals around 4% of revenue. We see the company benefiting on three fronts -- the seasonal uptick in construction spending; the release of funds and projects associated with the five-year Biden Infrastructure Bill; and the company's nip-and-tuck acquisition strategy that should further enhance its geographic footprint. In January, the company announced a fresh $1 billion buyback authorization following the completion of $4 billion in share repurchases over the 2012-2021 period.

Target Price: Reiterate $470; Rating: Two

Panic Point: $410

RISKS: Industry and economic risk, competition and competitive pressures, and acquisition risk.

ACTIONS, ANALYSIS & MORE: Initiating a Position in This Equipment Rental Company, We're Adding This Equipment Rental Company to the Bullpen, Investor Relations

* The AAP Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

Action Alerts PLUS is long BAC, AXON, COTY, LMT, ELV, GLD, SH, PSQ, XLE, PEP, MA, CIBR, AMZN, AMAT, URI, MSFT, MRVL, GOOGL, DE, COST, MS, AAPL, VMC, TRIN, MCD, QCOM.