Weekly Roundup

As we enter this seasonally challenging month, we'll keep eying for chances to add to Bank of America, McDonald's, Qualcomm, and Trinity Capital, while evaluating our inverse ETF holdings.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

August saw stocks give back gains won in June and July -- but the hardest hit of all last month were the small caps.

When all was said and done by Friday, the S&P 500 shed 1.8% and the Nasdaq Composite fell 2.2%. The Russell 2000 got whopped with a 5.2% drop.

Weighing on stocks during the month at first were prospects for above-trend gross domestic product growth in the current quarter that could extend the Fed's inflation fight, potentially leading to one more rate hike. That was the message Fed Chair Powell delivered at Jackson Hole, as well as reminding us the Fed's 2% inflation target is a fixed one, and the Fed is prepared to hold rates at elevated levels for some time to endure it goal is achieved.

We also had renewed concerns over the speed of China's economy, something that as we moved through August led to incremental stimulus efforts. Late this week, even as we received August PMI data for China that showed a return to growth for its manufacturing economy, reports suggested China's banks are preparing for fresh interest-rate cuts, while the government is expected to relax home-purchase restrictions amid a ballooning property-market crisis.

These shifting landscapes saw the dollar move higher in August with the same true for 10-year Treasury yields as well as shifting probabilities tracked by the CME FedWatch Tool. Late this week, however, as we started to get economic data for August, it became clearer the job market picture was slower than previously thought, wage pressure is abating, and the manufacturing economy in the U.S. continues to soften. That news "checked" many Fed boxes, which in turn lowered expectations for a potential rate hike later this year.

In our view the aggregated data builds the case for that, but we also recognize a few things. First, the updated Atlanta Fed GDPNow figure following all of this week's data still puts GDP for the current quarter at 5.6% as we embark for the Labor Day weekend. That is a far quicker pace than this week's revised 2Q 2023 GDP figure of 2.1%.

Second, we have several pieces of data ahead of us, including August Services PMI and the August consumer price index and producer price index reports, which will add another dimension to the speed of the economy, inflation pressures, and therefore potential Fed policy.

Third, Friday afternoon brought the first update to S&P 500 earnings expectations from FactSet since early August, a time when not all constituents of that basket had reported quarterly results. This update showed consensus EPS expectations for the S&P 500 rising 5.9% in the second half of 2023 vs. the first half of 2023 -- a tad less than the 6.1% figure from a few weeks ago. And while we some lift in consensus EPS expectations for 2023 to $222.45 from $220.17, the year over year growth expected in 2024 was also revised a smidge lower to 11.7% from 11.9%. Near-term we are far more concerned with the prospects for the second half of 2023 and that will have us focus our post Labor Day attention to the series of investor conferences at which management teams will offer up some fresh insights and data points about the back half of 2023. Odds are we will see some jockeying around of expectations for the current quarter.

In last week's Roundup, we shared our thoughts the market would be once again trading based on the data point it received last, and that was the case this week. Given what's ahead of us, we suspect that will be the way it is during next week's shortened trading week, as well. We'll remain on the disciplined path, looking to pick up stocks on our shopping list when and where it makes sense the most sense for the portfolio and for members.

And be sure to mark your calendar for Wednesday, Sept. 6, when we will hold our September Members-Only Call at noon ET. We look forward to seeing you there!

Catching Up on the AAP Portfolio This Week

As we noted above, this week closed out August and kicked off the final month of the current quarter. Over the last few weeks, we've seen strong moves in our shares of Axon Enterprises AXON , Deere & Co. DE , Universal Display OLED , Apple AAPL and United Rentals URI . As we said in our alert discussing the July Construction Spending report on Friday, given the resurgence in URI shares that has them approaching our price target, we are inclined to convert some of those better than 60% gains to realized profits for the portfolio and members.

Offsetting those pronounced gains, were declines in our shares of Elevance Health ELV , Bank of America BAC , and PepsiCo PEP as well as smaller cap holdings ChargePoint CHPT , and Clear Secure YOU . August was a challenging month for small-cap stocks amid renewed concern for one more Fed rate hike later this year. But as we entered September and digested the data it brought with it, that concern faded, giving some lift to not only the Russell 2000 but our shares of ChargePoint, as well. Bank of America shares were recently added to our shopping list, and we have some room to complete our ELV position as well. While the portfolio has a full position in PEP shares, we see the current share price as an excellent place for newer members to pick up the shares with the same being said of exiting members as well.

During August, we upgraded the shares of Apple and Amazon AMZN to "Two" ratings from "Three," and did the same more recently for the sharesof Marvell MRVL . Early in the month we added to our Axon position, and closed out the one we had in Cboe Global Markets CBOE locking in a more than 25% gain in the last of those shares. As we moved through the month, we started and built on positions in McDonald's MCD and Qualcomm QCOM , as well as added further to our holdings in Coty COTY , Clear Secure, and Trinity Capital TRIN .

As we move deeper into September, a month that historically been a challenging one for equities, our plan will remain prudently picking up shares that are on our shopping list, including the aforementioned Bank of America, but also McDonald's, Qualcomm, and Trinity Capital. Given the recent surges in Applied Materials AMAT and Universal Display OLED shares, unless we see some share price weakness, we would need to first adjust our respective price targets higher to justify picking up additional shares.

Recognizing September tends to be a challenging month for stocks, we are inclined to hold onto our inverse exchange-traded funds. But if upcoming data confirms the prospects the Fed is likely to be finished hiking rates, then we may revisit the rationale for holding the ETFs. If signs suggest the economy is slowing far more than expected, risking downside revisions to S&P 500 earnings expectations for the second half of 2023 or 2024, that could be a factor in our decision.

This Week's AAP Videos and Podcasts

We cover a lot of ground during the week in our Daily Rundowns and the AAP Podcast. If you happened to miss one or more of them, here are some helpful links:

Monday, August 28: Here's How We View 3 Portfolio Stocks as the Summer Winds Down

Tuesday, August 29: Why We Still Believe in ChargePoint

Wednesday, August 30: How to Make the Most of Your Action Alerts PLUS Membership

Thursday, August 31: What the Latest Inflation Numbers Mean for the Portfolio

Thursday, August 31: Ahead of Friday's Econ Data, Let's Take Another Listen to Key Podcasts

Friday, September 1: Bob Lang on the Jobs Report, the Fed and September Stock Markets

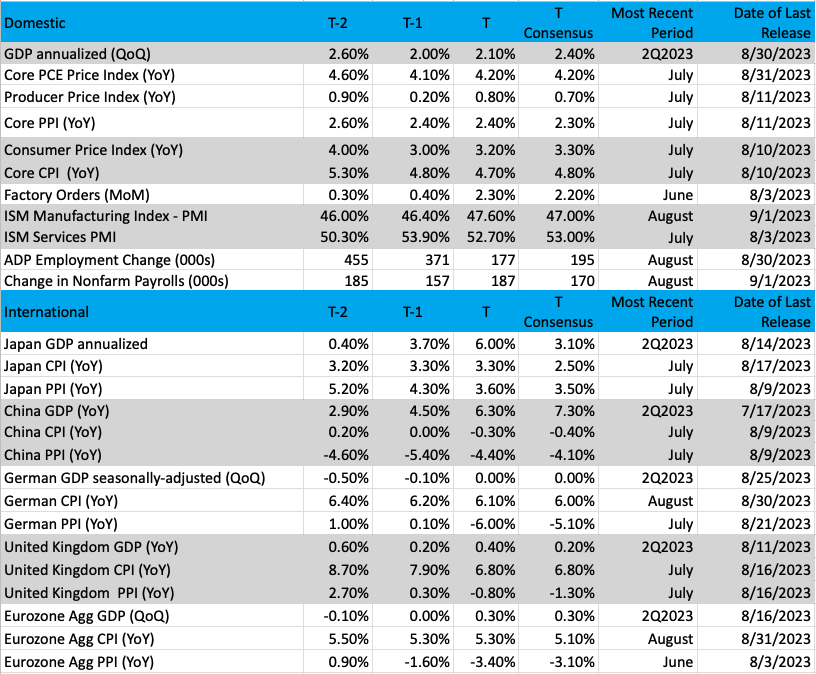

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

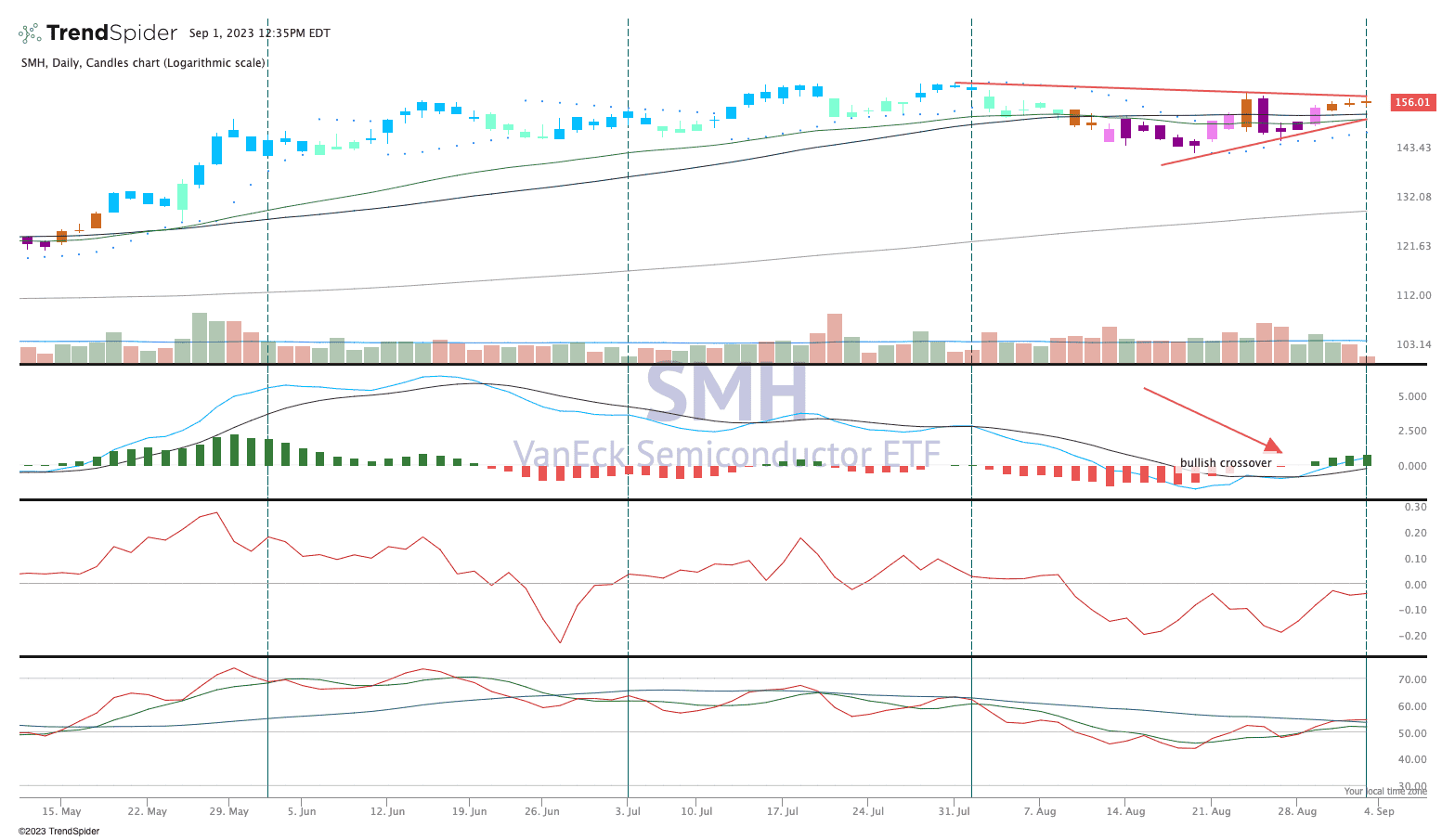

Chart of the Week: Semiconductors Start to Shine

The chart of the VanEck Semiconductor ETF SMH is starting to look much better of late. The series of higher-highs, higher-lows is a sharp contrast from what we witnessed at the start of August. The decline, though, took the stock through a good support level at $143 or so, and with recently strong volume and earnings out of the way for most names in this ETF there is a nice potential for a breakout move.

The indicators on this chart are looking bullish or nearly confirmed. The parabolic SAR (stop and reverse) is pointing higher and the Moving Average Convergence Divergence (MACD) oscillator is now on a confirmed "buy" signal. Money flow is nearly on a buy, too. Resistance is at the $160 level and could be tough, but this next move could be the one for this ETF to move higher.

Recently, we upgraded Marvell in the portfolio and today we added more Qualcomm. This was by design, these are two quality names that will shine with the advent of AI and a resurgence in technology in our economy. Keep a close eye on this group, they tend to lead the technology sector.

For a closer look at the chart above, click here.

Other charts we shared with you this week were:

Monday, August 28: Russell 2000 - Small-Caps May Lead the Way Lower

Monday, August 28: Mastercard - What Will This Portfolio Name Do for an Encore?

Tuesday, August 29: Trinity Capital - Sideways Action With Hints of Bullishness

Wednesday, August 30: First Trust Nasdaq Cybersecurity ETF - Cybersecurity Remains the Name of the Game

Thursday, August 31: Amazon Is About to Break Out

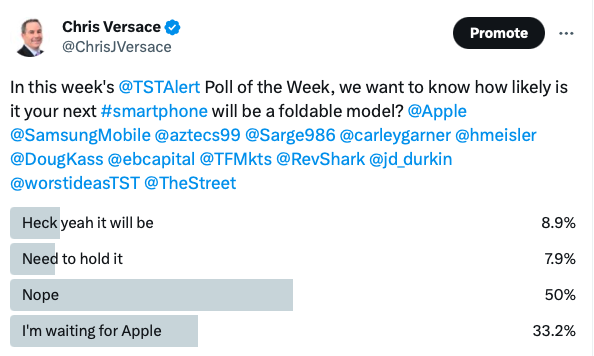

Poll of the Week

Samsung, Google GOOGL, Oppo and others are leaning into foldable smartphones, which can offer either an even smaller form factor or one that potentially replaces the need for a small tablet. Adoption of that form factor is one of the drivers behind our owning Universal Display OLED shares in the portfolio.

With that in mind, our AAP Poll of the Week wants to know how likely is your next smartphone to be a foldable model?

Be sure to

The Coming Week

With U.S. equity markets closed to observe the Labor Day holiday, we once again have a shortened trading week for the first full week of September, the last month in the current quarter. We will see some shifting around for the usual weekly data, but economic items we will be focused on next week are the Service PMI data for August, the latest iteration of the Fed's Beige Book and the July Consumer Credit report. In those reports, we'll be looking to see if the Services economy continues to keep the domestic economy growing, if inflation in the Service sector has abated, and if consumer leaned further into credit card debt to make ends meet.

Here's a closer look at the economic data coming at us next week:

U.S.

Tuesday, September 5

- Factory Orders - July (10:00 AM ET)

Wednesday, September 6

- Weekly MBA Mortgage Applications (7:00 AM ET)

- S&P Global Final Services PMI - August (9:45 AM ET)

- ISM Non-Manufacturing Index - August (10:00 AM ET)

- Fed Beige Book (2 PM ET)

Thursday, September 7

- Weekly Initial & Continuing Jobless Claims (8:30 AM ET)

- Productivity and Unit Labor Cost - 2Q 2023 (8:30 AM ET)

- Weekly EIA Natural Gas Inventories (10:30 AM ET)

- Weekly EIA Crude Oil Inventories (11:00 AM ET)

Friday, September 8

- Consumer Credit - July (3 PM ET)

International

Tuesday, September 5

- Japan: Household Spending - July

- Japan: Jibun Bank Services PMI - August

- China : Caixan Services PMI - August

- Eurozone : HCOB Services PMI - August

- UK : S&P Global/CIPS Services PMI - August

- UK: New Car Sales - August

- Eurozone: Producer Price Index - July

Wednesday, September 6

- Germany: Factory Orders - July

Thursday, September 7

- China: Imports/Exports - August

- Japan: Leading Economic Index (Preliminary) - July

- Germany: Industrial Production - July

- Eurozone: 3Q 2023 GDP - Third Estimate

Friday, September 8

- Japan: 2Q 2023 GDP (Final)

- Germany: Inflation Rate, Consumer Price Index - August

- China: Inflation Rate, Producer Price Index - August

While we have a very light earnings report calendar next week, portfolio holding ChargePoint CHPT will be among that relatively short list. In that report and guidance, we'll be focused on the company's growth in active charge points, how it sees the inclusion of Tesla's charging standard, timing on stimulus funds for public EV charging stations, and an update on its cash position. We would also like to hear more on wins in the private sector as commercial fleets continue to adopt EV solutions both in the US and in Europe. We will also be interested on supply chain comments as well as how the company could benefit from better foreign currency dynamics.

In addition to that report, we will be interested in Kroger's, including what it says about food inflation, traffic and other relevant metrics given our position in PepsiCo PEP . The renewed pressure on those shares has them back in the buy zone for newer members or those who missed out when we recently added to the portfolio's position.

We also have the return of investor conferences next week, including Barclays Global Consumer Staples Conference, the Citi Global Technology and GEMs Conference, and the Goldman Sachs Communacopia Technology Conference to name but a few. These conferences will be filled with management presentations, ones we will be parsing and comparing to June-ending quarter guidance issues between several weeks ago and almost two months ago. We will also be collecting end market commentary as well as those about the global economy, inflation pressures and other data points as we sharpen our focus for the final four months of 2023 and the start of 2024.

Here's a closer look at the earnings reports coming at us next week:

Tuesday, September 5

- Close: AeroVironment (AVAV), Zscaler (ZS).

Wednesday, September 6

- Close: American Eagle (AEO), ChargePoint (CHPT), Dave & Buster's (PLAY), GameStop (GME), Sportsman's Warehouse (SPWH),

Thursday, September 7

- Open: Science Applications (SAIC)

- Close: DocuSign (DOCU)

Friday, September 8

- Open: Kroger (KR)

Action Alerts PLUS is long BAC, AXON, COTY, LMT, ELV, GLD, SH, PSQ, XLE, PEP, MA, CIBR, AWK, AMZN, AMAT, URI, MSFT, MRVL, GOOGL, DE, COST, CMG, CHPT, AAPL, VMC, TRIN, OLED, MCD, QCOM and YOU.