These Sectors Are Driving 2026 Consensus S&P 500 EPS Prospects

Changing overall earnings and sector-level expectations from mid‑December to late January reveal several notable trends.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

As we move into February and get ready for another big week of earnings, let’s take a snapshot of consensus EPS expectations for the S&P 500 and how they’ve changed since mid-December.

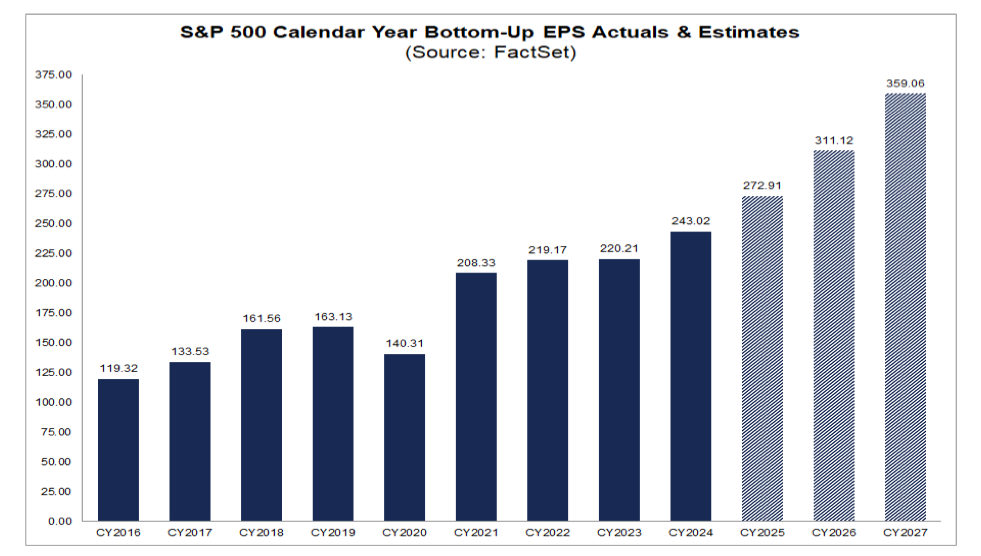

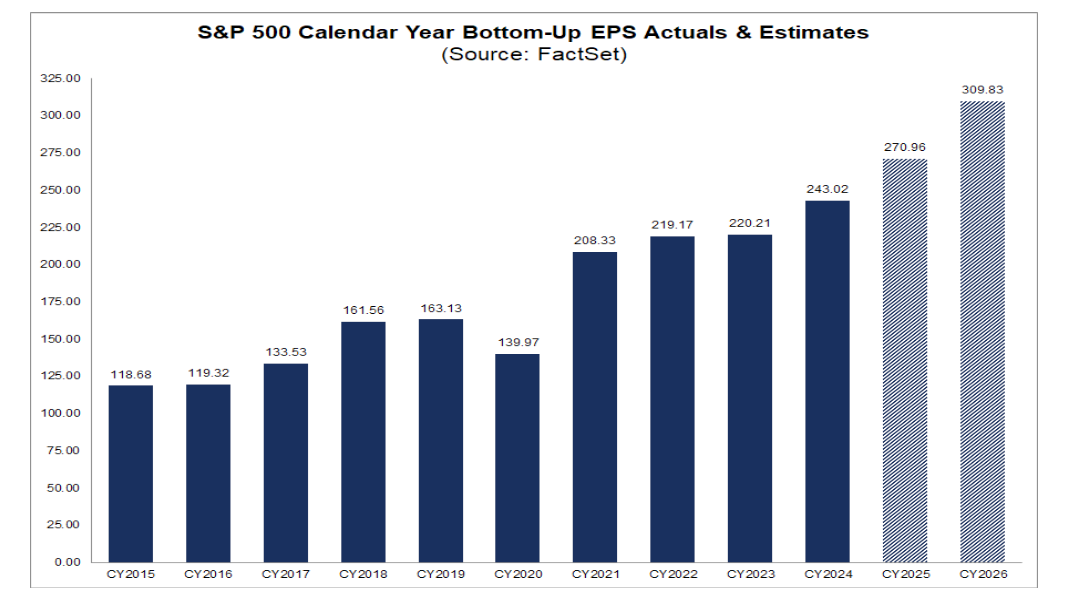

In looking at the two charts of annual EPS expectations, we see the markets expects stronger December-quarter performance, hence the bump up to the current $272.91 from $270.96 in late December. More importantly, given that the market is a forward-looking animal, is that 2026 consensus EPS for the basket has been lifted to $311.12 from $309.83 in mid-December.

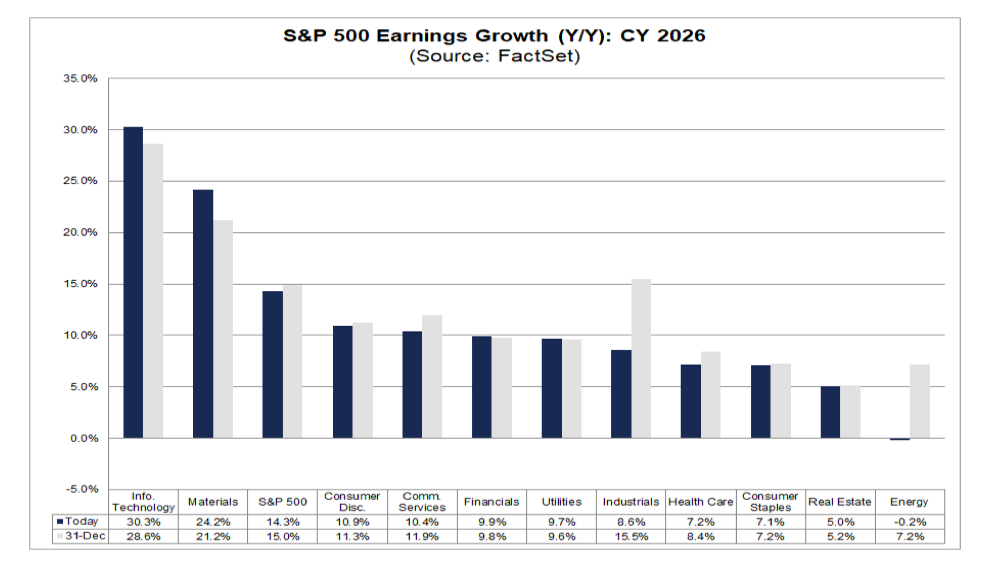

As we collect upcoming reports from our holdings and those from others, we’ll want to keep in mind where the market expects quicker earnings growth than the S&P 500. As of Friday, here is what the market expects per data from FactSet

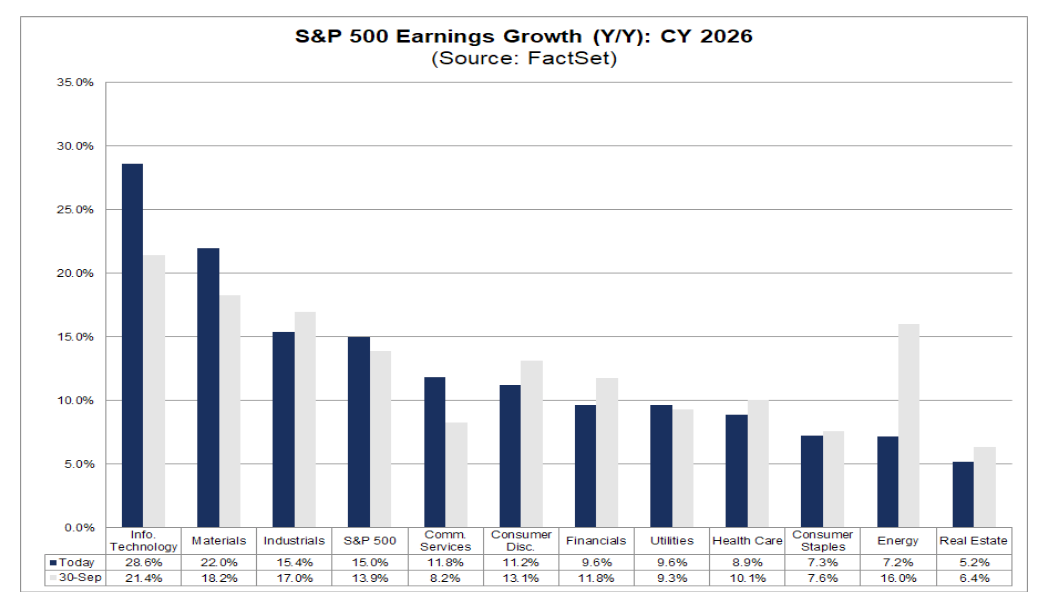

And let’s compare that to what was expected in mid-December

What do we see between the two charts?

EPS growth expectations for the Information Technology sector, which includes software, hardware, semiconductors, IT services, and related technology infrastructure companies, have risen meaningfully since the end of September. By comparison, EPS growth expectations for Energy have collapsed, Industrials’ have been cut in half, and those for Consumer Discretionary have been trimmed.

Here’s the thing, though. We’ve had a few weeks filled with earnings reports, but including today, we still have 67% of the S&P 500 yet to report. This week brings another 127 or another 25% of that basket, including S&P 500 heavyweights Amazon (AMZN) and Alphabet (GOOGL) . That means that by this time next week, we’ll have a better feel for 2026 EPS prospects, but still not a complete one. We won’t get that for at least another few weeks, until the likes of Walmart (WMT) and other retailers report mid-month.

What we’ve seen so far and the fuller picture we’ll get will be helpful to us, but a central part of our long-term strategy to identify and invest in companies for the medium to longer-term is to focus on those with superior EPS growth and multi-year structural tailwinds. With the latter in mind, we’ve already collected a bunch of signals for our next collection that we’ll share with you on Saturday.

With that in mind, on February 9, once about half of our holdings have reported their December quarters, we’ll update our Portfolio table of consensus EPS expectations, RSI levels, and other data. We won’t stop there, of course, as we’ll continue to update that table as we get past 75% of the S&P 500 that has reported, and again when we cross the 90% level.

More Pro Portfolio:

- We’re Trimming This Holding Before Earnings and Following a Big Run

- Stocks & Markets Podcast: Silver, Gold, Oil, King Dollar, and Small-Caps

- January Monthly Roundup: Stocks Slide Into February as Volatility Spikes

At the time of publication, TheStreet Pro Portfolio was long AMZN and GOOGL.