This Market Seems Ready to Roll Over

A gauge of the market shows too much focus on a single stock and raises some concerns.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

As someone who likes to be a “contrarian,” I need to understand market sentiment. Right now, I’m having trouble figuring that out.

My gut is that we are set to roll over, that many things I normally watch have been overwhelmed by the AI trend and that trend has peaked, for now.

Breadth, along with the role that options are playing in the market, and a whirlwind of geopolitical risks, were discussed on Bloomberg TV on Tuesday (my segment starts at the 50-minute mark).

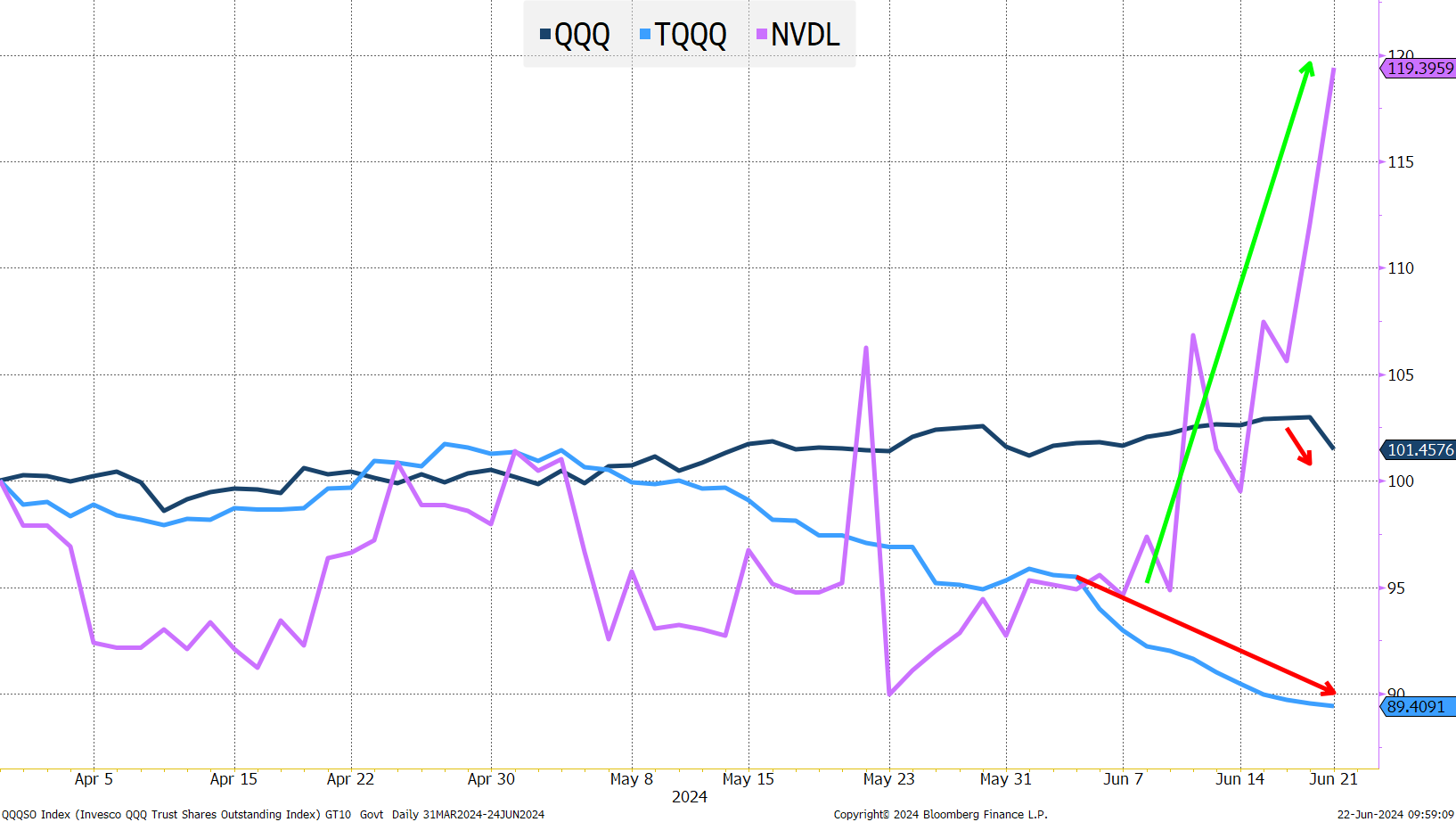

The 'One-Stock' Stock Market at a Glance

We start with three ETFs:

- TQQQ, a 3x leveraged ETF on the Nasdaq 100 (with a $24 billion market cap), has been experiencing outflows for several weeks. While we didn’t include it here, SQQQ, a 3x inverse ETF on the Nasdaq 100, has been garnering some serious inflows (though only $3 billion). I own some SQQQ and am considering adding significantly to that position. One way to interpret this data, is that “faster” money has been taking profits in the Nasdaq 100 and, while still outright bullish (based on relative market caps), it shows signs that the market is tired.

- QQQ is a Nasdaq 100 ETF. It is a whopping $284 billion, and I view it as a bellwether of flows from buy and hold “mom and pop” accounts, to hedge funds, to large asset managers adjusting their asset allocations. It has trickled higher in terms of flows since the start of the second quarter, but had some meaningful outflows in the past few days. Again, more “trimming” than exiting risk, but an interesting development.

- Which brings us to NVDL, an ETF that provides a 2x leveraged return on NVDA. It is $4.3 billion in size, so not big, but big enough for us to pay attention to. While investors were shedding risk in the Nasdaq 100, this ETF was getting large inflows! I still cannot understand why the regulators approve single stock ETFs of any sort (especially leveraged). There seem to be enough ways to invest in single stocks without needing an ETF. Let alone an ETF that is path dependent. The leveraged ETFs (unless a stock moves in one direction day after day) will always underperform the leveraged return of the stock from the initial investment date (it is a function of the rebalancing mechanism). Why this ETF exists, I don’t know, but it seems to give us a glimpse into the “one-stock” nature of this market.

I didn’t include XLK (a $71 billion ETF focused on the tech sector) in the chart, but asides from two flows related to rebalancing the top-two holdings, it showed a similar, greedy, but less greedy pattern.

My understanding of the rebalancing is that the rules that this ETF follows only allow for two stocks to be weighted above 5% (at the time of the reweighting). Currently, those two stocks are MSFT and AAPL (both a little over 20%). NVDA (at 5.8%) is expected to “flip flop” with AAPL as one of the two most weighted stocks. That seems to be setting up traders. Could this rebalancing be affecting signals?

While we are not here to hammer on “passive,” it seems important to remember that every $100 that currently flows in or out of QQQ (for example) creates $45 of buying or selling for seven companies (eight stocks but seven companies, as both GOOGL and GOOG are in the top eight).

Equal-weight ETFs are not getting big inflows, further adding to my view that the “catch up” trade is unlikely to occur.

I’m stuck seeing too much focus on a single stock and am concerned by the nature of passive funds impacting a variety of stocks. I cannot get behind the “catch up” rally, because unlike last fall, where you could bet that the data was improving and the average stock had not responded, we’ve had the “good” data and haven’t been able to get a strong response from much of the market.

Investor Sentiment

The first two things I look to when thinking about investor sentiment are:

- The CNN Fear & Greed Index. It currently registers as “fear.” With the VIX at 13, that didn’t jump out as being an obvious place for this index to register. A month ago, the index was in “greed” mode, and I’m not really sure how it is coming up with “fear,” but I have to respect it (maybe it is picking up on some of the fund flows we’ve been seeing, which have shown reductions in risk taking). So, we have one measure saying “fear.”

- The next stop is the AAII Investor Sentiment Survey. Lo and behold, 44.4% are bullish. Higher than a month ago. Only 22.5% are bearish, far lower than a month ago. This measure is telling me “greed.”

While these two measures don’t always agree (and are generally good contrarian signals at the extremes), one is saying fear (though not at a “signal” strength), and the other is saying greed (at close to “signal” strength).

“Clear as mud” is one possible explanation. One picks up surveys where investors can’t help thinking about the broad market and the economy overall, and the other picks up “hard data” where much of that hard data is influenced by all the changes in the options markets. We didn’t even talk about the option selling based ETFs or even the heavily skewed weightings in indices. Something to explore at the very least.

Given those mixed signals, we can go back to my favorite fallback indicator: RSI. RSI (or relative strength indicator) for the Nasdaq 100 is in overbought territory but has been coming down. At least this indicator makes some sense to me. Greedy, but less greedy than a few weeks ago.

Rates

The 10-year is still sitting below 4.3% (I continue to believe that 4.3% to 4.5% is the “right” range for now).

- Inflation data is likely to continue softening, supporting Fed cut projections and helping yields across the curve.

- European politics will add volatility. Last week, political news out of Europe seemed to help the bond market, but I’m not expecting that to be the norm.

- Our deficits. The CBO raised their estimates for this year’s deficit to just under $2 trillion (more than a 25% increase from earlier projections). They see no end in sight, and I believe that the debate will put the deficit in the headlights (and not in a good way) as the reality of most policies seems to be destined to increase the deficit (just doing it in different ways).

The short end of the curve should benefit from data, while the longer end of the yield curve is likely to be impacted by re-focusing on the deficit, and the debate seems like an ideal catalyst for that.

Bottom Line

Maybe we get the “catch up” but only because leadership is fading and that will drag markets lower.

Look for yields to rise, especially as the debate could be a catalyst for people to refocus on the deficit.

Credit, I like, though given my view on rates, I’d be adding to floating rate products (like the CLO ETFs JAAA and JBBB) or maybe some BDCs and holding off on fixed-rate products (like closed-end muni funds, and IG bonds) and looking for better entry points.

At the time of publication, Tchir was long SQQQ and short QQQ.