The Oil Market Was a Victim of Its Own Success

Although traders were caught on the wrong foot weeks ago, here's why the path of least resistance is likely higher from here.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

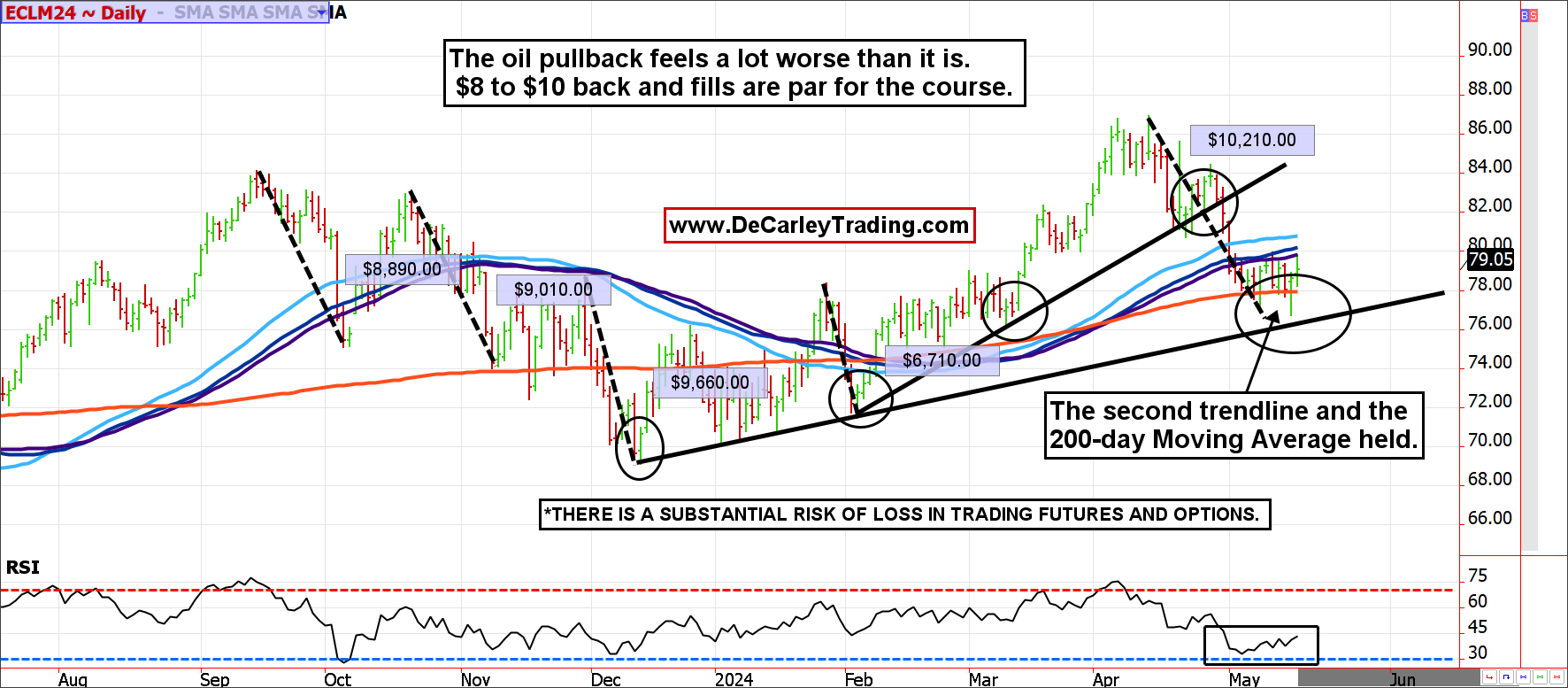

The oil market was a victim of its own success. The rallies triggered by Middle East violence last month lured aggressive speculative buying that had to be unwound as traders discovered the anticipated supply disruptions didn't materialize. In other words, a buy-the-rumor, sell-the-fact scenario completely removed the war premium from pricing.

However, the underlying fundamentals haven't changed. The same supply constraints exist today that were there prior to political flare-ups. Although traders were caught on the wrong foot weeks ago, the path of least resistance is likely higher from here.

In recent years, most digestive pullbacks in crude oil have spanned about $9 to $10 or $9,000 to $10,000 per futures contract, so this selloff is par for the course. It wasn't that long ago that we saw $10.00 to $15.00 moves in hours, not days. Oil is a volatile market and always will be; $10.00 moves don't necessarily change the trend. In fact, a move in that increment can be considered noise even though such moves seem outsized in percentage terms.

OPEC has worked too hard and given up too much market share to U.S. producers to let the market flood now. Further, the U.S. Strategic Petroleum Reserve is historically low after the U.S. government released oil from reserves to thwart higher prices in 2022.

The action was successful but not without delayed consequences. Since then, the refill process has mostly been non-existent. The government is targeting refill barrels at $79.00 or lower, so we are getting back into the desired price range. Yet, the Biden administration has announced they will not be actively refilling the SPR any time soon.

The SPR was originally developed as a tool to deter overseas crude oil producers from using energy as a weapon. Unfortunately, the SPR's low reserves keep OPEC incentivized to do just that. The longer the cartel can keep prices elevated, the more vulnerable the U.S. becomes.

Some argue that the risk of energy being weaponized in the same manner it did during the 1970s oil embargo has dissipated now that the U.S. is the largest oil producer in the world. However, this might be a naïve take because although other global players are smaller, most of them are conspiring together to manipulate prices. In other words, we remain vulnerable to energy warfare until the U.S. produces more than all OPEC countries combined.

Further, due to improved technology, U.S. oil production is at an all-time high. Still, investment in infrastructure and political opposition suggest that output of roughly 13 million barrels per day could be plateauing at best and heading toward decline at worst. A year ago, about 760 oil rigs were in operation; today, there are only about 600. Technology might not be able to continue doing the heavy lifting.

We've all been focused on inflation, but we could easily be talking about deflation by next year. Recessions cure inflation; oil was $150 per barrel before the financial crisis, and natural gas was $13.00 per MMBtu.

Until now, the wealth effect has worked in favor of consumers, but that isn't guaranteed going forward. There are good arguments that rallies in risk assets such as stocks and Bitcoin have pulled forward prosperity from the future that will need to be paid back at some point. Eventually, demand will wane, but we expect that to be later in the year and from higher prices.