Market's Muscle Mirage

Let's look at the big-picture economy, including futures, global policy uncertainty and price creep ... and see something building: GE's charts.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Equity index futures are trading lower overnight, after seemingly trading higher on Monday. I say "seemingly," because things are not always as they appear. Sure, the Nasdaq Composite had a nice day, gaining 0.83%, as its sibling the Nasdaq 100 tacked on 0.66%. Sure, the S&P 500 managed to wring out a very pedestrian looking gain of 0.27% for the regular trading session on Monday. That's more or less where the fun stopped. The S&P Midcap 400 give up 1.01%, and the Russell 2000 gave up 0.86%. The Dow Transports, meanwhile, surrendered 0.76%, and the equal-weighted S&P actually lost 0.79% on Monday.

Remember, the first trading day of the second half is usually a "plus" day.

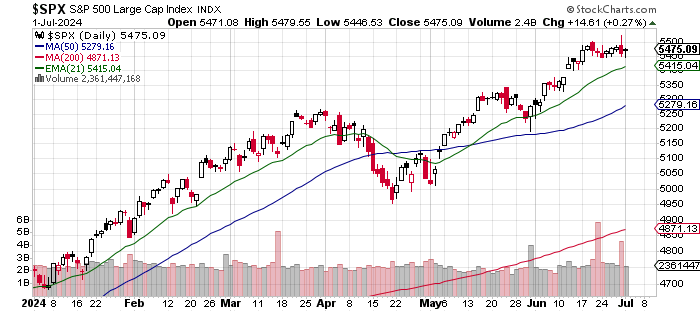

I mean, I guess if all one does is look at the headline indexes as they are presented on the local 6 p.m. news, then Monday was indeed an "up" day. But do any digging at all, and well ... not so much. Remove all comments and notations from a six-month chart of the S&P 500, and you see an index that appears to maybe be consolidating for a couple of weeks. No real cause for concern just yet.

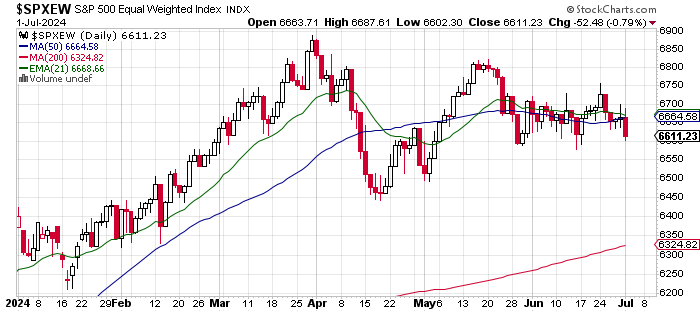

Then we move on to the equal-weighted S&P 500, and the image changes significantly...

Remove the market cap weighting that overvalues a handful of stocks, and place as much focus on the other 494 or so stocks in the index, as we do the leaders, and what looked like some minor consolidation at the top and right of the chart, looks a lot more like a symmetrical triangle coming to a close that has not produced a record high since very late March. Oh, and you know what closing triangles often foretell? Heightened volatility, that's what. Helmets, flak jackets, and two sources of water from here on. You never know. Gas masks on the hip.

Global Monetary Policy 'Uncertainty'

The U.S. Ten Year Note got slapped around a little bit on Monday, yielding 4.47% (up 7 basis points) by day's end, while the yield for the U.S. Two Year Note stayed close to where it was, moving up just one basis point to 4.75%. The steepening of the slope of the Treasury yield curve continued despite the Monday resurgence of the U.S. Dollar Index. The U.S. Dollar continued to gain against the Japanese yen, which as we explained yesterday, is part of the story here.

I saw some foolish talk in the media last night (at a supposedly respected financial news website) trying to explain that debt markets were trying to price in a Trump victory in the November election. Understand this, if you saw that story: That was a desperate attempt by a "journalist" to explain something in financial markets that they did not understand. The bond market is not trying to price in something still five months away where the outcome remains extremely uncertain. The market is trying to price in uncertainty in the trajectory for global monetary policy.

The European Central Bank makes its next policy decision on July 18. The ECB held its "Forum on Central Banking" on Monday, which will spill over into this morning. Markets had more or less started to price in a second short-term interest rate cut at that meeting and then a third in September. On Monday, the ECB's Mario Centeno spoke of being prudent with further rate cuts, while the ECB's Pierre Wunsch, added "I would say there is room for a second cut." Then, Wunsch, who hails from Belgium, warned, "To continue with cuts, I would need to have some more comfort that we really are going down from 2.5% inflation to something which is closer to 2%."

Finally, early this morning, European Central Bank Vice Pres. Luis de Guindos stated on policy: "It's quite clear we don't have a predetermined path; we have confidence inflation will converge to our definition of price stability" ... "We have to be very prudent." When asked how many cuts he sees the ECB making in 2024, de Guindos stated flatly, "We don't know."

European equity markets, sovereign debt markets, and U.S. equity index futures markets, all showed displeasure at the uncertainty expressed overnight at the ECB Forum on Central Banking.

But Wait, There's More...

The ECB central banking clambake is not quite done. There is a "policy panel" discussion set for 9:30 a.m. ET Tuesday morning. Both Fed Chair Jerome Powell and ECB Pres. Christine Lagarde are scheduled to participate.

Just Another Manic Monday

As mentioned above, once we moved past mega-cap and elite large-cap performance on Monday, U.S. equities were quite sloppy. Losers beat winners by greater than a two to one margin at the New York Stock Exchange, and by more than five to three at the Nasdaq. Advancing volume took a 35.5% share of composite NYSE-listed trade, but a 56.2% share of composite Nasdaq-listed activity.

Seven of the 11 S&P sector SPDR ETFs closed out the Monday session in the red, led lower by the Materials XLB and Industrials XLY that were both off by more than 1% for the day. Technology XLK led to the upside at 0.76%, but it was not the semiconductors that supported tech on Monday. The Dow Jones U.S. Software Index posted a gain of 1.49%. Big data names Snowflake SNOW and MongoDB MDB were the leaders, gaining 5.69% and 5.42% respectively.

As expected, with a holiday looming and coming off of last Friday's extreme volume- producing event, there was a tremendous downshift in activity. Aggregate trading volume across NYSE-listings was down 51.5% day over day, while aggregate trade across Nasdaq-listings was down 42.1% day over day. Even more telling of how many folks might be out this week, trade on Monday was down 5.6% and 5.7% on a week over week basis for NYSE and Nasdaq-listings respectively.

Readers will recall that last Monday, markets were coming off of a triple-witching expiration, so there are some similarities in trading patterns. Does this make whatever happened on Monday less than meaningful? The short answer is, "yes." Does this make the rest of the week less meaningful? With June Jobs Day on Friday, that's hard to say.

The Big Picture: Weak Manufacturing

The ISM Manufacturing Index for June hit the tape in a surprisingly weak state. The headline print of 48.5, landed below the 49.2 that Wall Street was looking for and printed in a state of contraction for a disturbing 19th month in the past 20. The rate of decay in New Orders slowed, but the slowdown in Backlog of Orders somehow re-accelerated, printing in the hole for a 17th consecutive month. Industrial recession much? Oh, Prices still expanded. That was the only component of the ten that actually showed any growth at all.

In addition, Construction Spending for May hit the tape at -0.1% month-over-month , which was well below the consensus view for +0.3%. This was the fourth month in five that construction spending failed to show any growth at all.

After these two disappointing data-points crossed the tape, the Atlanta Fed had to revise its GDPNow model for the second quarter down to growth of 1.7% from 2.2% as Atlanta tries desperately to get back in line with the New York, St. Louis and Cleveland Feds, who have all been well below Atlanta on second-quarter gross domestic product for weeks.

Did I Mention ... Prices?

The Baltic Dry Index is now back at nearly two-month highs. The average daily rate for cape-size vessels was up almost $2,900 to $31,438,000 on Monday, as rates appear to be rising more quickly for Atlantic passages than they are in the pacific. Yes, this is inflationary. Highly inflationary.

Pay Day

Readers likely noticed the strong performance across the banking sector on Monday. Late Friday, JP Morgan JPM, Morgan Stanley MS, Bank of America BAC, Goldman Sachs GS, and Wells Fargo WFC all announced increased returns to shareholders in the forms of cash dividends or share repurchase programs or both after passing the Fed's stress tests earlier in the week. All of those names traded nicely higher on Monday.

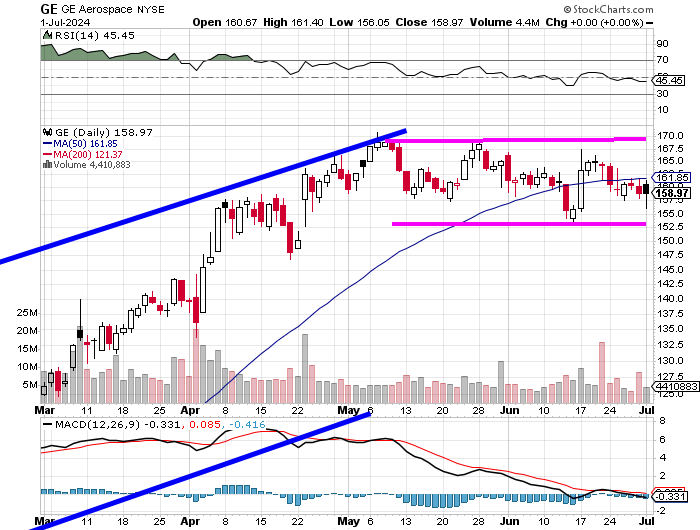

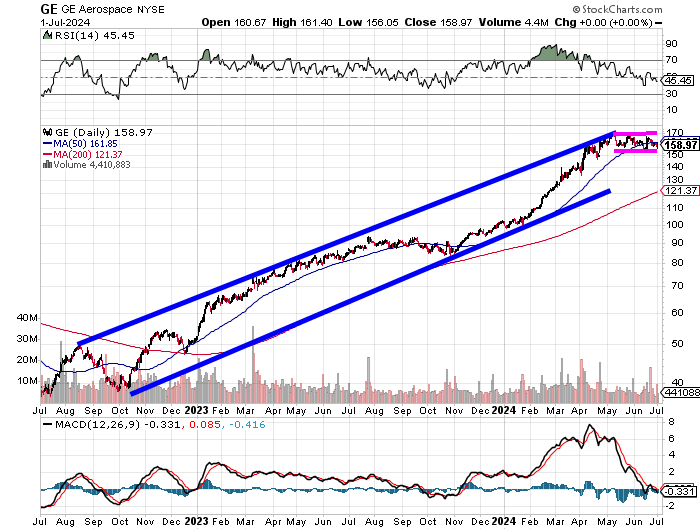

MVP: GE Aerospace Ascending Price Channel

On Monday, the board of directors for GE Aerospace GE approved an employment agreement for chair and CEO Larry Culp that pushed out his employment with the company from August 2024 to December 31st, 2027.

Consolidation? Yes.

Still in a two-year ascending price channel? Also, yes. Easily.

Pivot: $162.

Target: $186.

Economics (All Times Eastern)

08:55 - Redbook (Weekly): Last 5.3% y/y.

10:00 - JOLTs Job Openings (May): Last 8.059M.

10:00 - JOLTs Job Quits (May): Last 3.507M.

16:30 - API Oil Inventories (Weekly): Last +914K.

The Fed (All Times Eastern)

09:30 - Speaker: Federal Reserve Chair Jerome Powell.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: MSM (1.33)

At the time of publication, Guilfoyle was long WFC and GE equity.