Investor Sentiment Turns on the Red Light

Some clouds may be gathering over the market.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It's the start of another busy week in the markets between Apple AAPL WWDC event, key inflation reports and of course, an all-important Fed meeting.

We still see the near-term trends for the major equity indexes mixed from bearish to bullish. Cumulative market breadth saw some deterioration Friday.

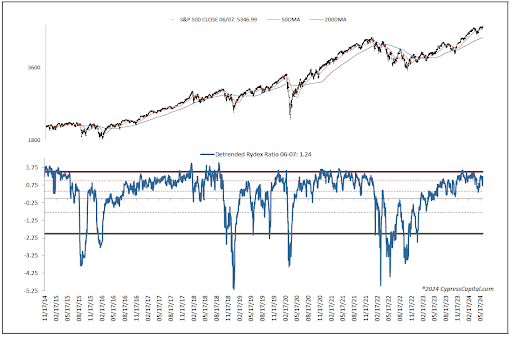

Regarding the data, it suggests some clouds may be gathering. Friday saw an increase in insider selling while the detrended Rydex Ratio (contrarian indicator) reversed back to bearish implications as the leveraged ETF traders are back to being leveraged long. Finally, based on earnings estimates for the S&P 500, current valuation continues to appear rich.

Cumulative Market Breath Weakens

On the charts, all the major equity indexes closed lower on Friday with negative breath and up/down volume.

All closed near their session lows as the near-term trends stayed bullish on the S&P 500, Nasdaq Composite and Nasdaq 100 (see below).

The DJIA and Dow Jones Transports are neutral with the MidCap 400 and Russell 2000 bearish.

Cumulative market breadth weakened with the All-Exchange advance/decline line turning bearish as is the Nasdaq’s. The NYSE’s A/D/ is neutral.

No stochastic signals of import were generated.

Investor Sentiment Back on Red Light

The data have turned a bit more mixed..

The 1-Day McClellan Overbought/Oversold Oscillator are still neutral on the All Exchange and Nasdaq with the NYSE’s slightly oversold (All Exchange: -47.490 NYSE: -50.15 Nasdaq: -46.81).

The percentage of S&P 500 issues trading above their 50-day moving averages (contrarian indicator) slipped to 48%, staying neutral.

However, the detrended Rydex Ratio (contrarian indicator) has shifted back to bearish with the leveraged ETF traders leverage long at 1.24.

Last week’s AAII Bear/Bull Ratio (contrarian indicator) dropped to 0.6 and neutral.

However, the Investors Intelligence Bear/Bull Ratio (contrary indicator) is bearish at 17.9/58.2 as bulls increased and outweigh bears.

The Open Insider Buy/Sell Ratio saw some increase in insider selling, dropping to 30.9 from 39.5.

Leveraged ETF sentiment is -7.8, remaining neutral.

Valuation Remains Extended

The 12-month consensus earnings estimate for the S&P 500 from Bloomberg rose to $253.00 per share. Its forward P/E multiple at 21.1x remains well above the “rule of 20” ballpark fair value of 15.6x. It remains an important concern for us as a 500-basis point premium is significant.

The S&P's earnings yield is 4.73%.

The 10-Year Treasury yield jumped to 4.43% from 4.28% and above resistance. Support is now 4.32% with new resistance at 4.47%. Its intermediate-term trend is still negative.

The U.S. dollar, via the UUP ETF, closed higher as well at $28.77 and also above resistance. It is neutral with support at $28.59 and resistance at $28.90.

Bottom Line

Breadth is questionable while risk is high on individual names that are trading at premiums to their projected one-year growth rates and seeing significant declines if they disappoint. It is a stock picker's market and should be approached as such. Honor sell signals and be very careful on the buy side.