Fed Warning Signals, Hot Markets, Inflationary Pressures, Trading Apple

Perhaps most interesting yesterday was the Conference Board's Leading Indicators Index for February.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Oh, they seem to be loving equities now, don't they? The FOMC policy meeting has come and gone. The takeaway among portfolio managers seems to be that the central bank is suddenly more worried about a liquidity drain as its reverse repurchase agreement facility winds down, potentially along with excess bank reserves.

Wall Street has decided more or less that the Fed is so worried about a liquidity drain later this year that they may have decided to do more than just maintain an easy money policy. Heck, we all know current monetary conditions are not restrictive. Perhaps even, if need be, (not just, if need be, it's what the Fed is signaling) the FOMC may be willing to reduce short-term interest rates even as inflation reheats, and while simultaneously tapering the pace of its quantitative tightening program.

Unless we all got them wrong. Unless the Fed came off as more dovish than intended. I don't think so. I think the signaling was an honest attempt to warn about the potential for something that worries the Fed more than inflation, and to let us know that they were not asleep at the wheel.

For what it's worth, Fed Chair Jerome Powell has been added to today's docket of Fed speakers. Readers will notice three speakers below. Fed Gov. Michael Barr and Atlanta Fed Pres Raphael Bostic had scheduled Friday's appearances at least a week ago. Powell's 09:00 ET appearance at a "Fed Listens" event in DC was a late addition. Perhaps there is something he needs to get right or even reset in regard to the current narrative.

Marketplace

On Thursday, equity markets remained hot to the touch, maintaining the late Wednesday, post-FOMC rally, despite some weakness in Treasuries. Was it Powell? To a degree, but it was also about the macro, which we had seen as getting softer only a few days ago. The S&P 500 gained 0.32% on Thursday as the Nasdaq Composite gained 0.2%. New all-time closing high records to be sure.

However, it was the corners of the marketplace that are more reliant upon increased economic activity that have been the warmest. The Dow Transports popped for a gain of 1.14%, as did the small-cap Russell 2000. Yes, they both ran 1.14% for the session.

Beyond those two, the KBW Bank Index screamed 2.16% higher as the Philadelphia Semiconductor Index reclaimed its daily crown with a gain of 2.29% on Micron Technology's MU big day. That stock stormed to a 14.1% gain on Thursday, followed by Broadcom AVGO, which was up "just" 5.6%.

This is what's interesting, gang. Ten of the eleven S&P sector SPDR ETFs shaded into the green on Thursday, led by the five cyclicals. How interesting is that? Though not one of these funds even gained a full percentage point on the day, sectors reliant upon improved economics outperformed while defensives took four of the bottom six rungs on the daily tables.

Breadth was solid. Not spectacular, but solid. Winners beat losers by more than two to one at the NYSE and by a rough three to one at the Nasdaq. Advancing volume took a 62.5% share of composite NYSE-listed trade and a 55.6% share of Nasdaq-listed trade. However, aggregate trading volume was a little quirky. For the day, trading volume across NYSE-listings and the membership of the S&P 500 increased on a day over day basis, but all four of these sessions have experienced lower trading volume than the final three sessions of last week, which were all red candle sessions.

Trade across Nasdaq-listings and the membership of the Nasdaq Composite wasn't even up day over day on Thursday, despite the fact that so much of Wednesday's trade was packed into the final two hours of that regular trading day.

What does it all mean? It means, in my opinion, that a high percentage of professional money movers are trading trends but are not fully committed to investing at these levels at this time. Hey, you asked. Well, actually, I am writing in the dark in the middle of the night. I guess I just pretended you asked, but you wanted to. Right?

Solid Macro...

What manner of sorcery is this? Sarge doesn't pipe up too much when the macro is solid. Hey, stop it. I know that you're just in my head. I do acknowledge positive looking data, don't I? I mean I don't want to just be the written opposite of those ridiculous cheerleaders that we see on financial television every day. Half of these dingbats don't even realize that the Fed now fears something more than they do inflation. Otherwise, a dovish talk wouldn't make sense as one traverses a newly reinvigorated inflationary landscape.

You kids catch the Philly Fed on Thursday. Arguably the most important regional manufacturing survey in the US, Philly printed in positive territory for March, not just at the headline, but also for New Orders, Shipments and Unfilled Orders. An inflection point? Perhaps. That said, both Number of Employees and Average Workweek continued to contract in Philly, suggesting that more is being asked of fewer workers. Yes, that is often when worms do turn. Let's see this seed grow into a sapling.

Perhaps most interesting for the day, I thought, was not February Existing Home Sales, which printed well above consensus view, but the Conference Board's Leading Indicators Index for February. That data-point printed up just 0.1% month over month.

What's so big about that? February 2024 was the first month that this item, which is a diffusion index encompassing ten leading economic indicators, showed growth for the first time since February 2022. That's right, two years of persistent contraction finally came to an end. Go ahead and believe the GDP prints for Q3 and Q4 though. The simpletons on TV do, and don't worry about running out of Kool-Aid, we have more.

This next part is going to be fun to write. The S&P Global US Flash PMIs for March hit the tape on Thursday in expansionary territory. Remember, these are meaningful only until the ISM (Institute for Supply Management) prints their surveys. Then everyone forgets about the S&P Global surveys. That said, the Flash Manufacturing PMI for March landed at 52.5, which was not only above expectations, but also a 21-month high. The Flash Services PMI for March crossed the tape at 51.7, a tad below expectations, but still growing. All good, right?

Not So Fast, My Friend

I won't claim credit for this myself as I had not seen it yet. I was on the phone with our pal Chris Versace, and he pointed it out to me at the time, but you kids are going to love the following quotes, though Jerome Powell probably did not.

From the S&P Global Flash PMI release....

"Inflationary pressures picked up in March. The rate of input cost inflation quickened to a six-month high amid faster increases across both monitored sectors. Service providers indicated that higher operating expenses generally reflected increased wages, while rising oil and gasoline costs were often mentioned by manufacturers."

"In turn, companies in the US raised their own selling prices at a faster pace. In fact, the rate of inflation was the sharpest in just under a year and stronger than the series average. Respective rates of output price inflation accelerated sharply across both manufacturing and services, quickening to 13- and eight-month highs as companies passed through higher input costs to their customers."

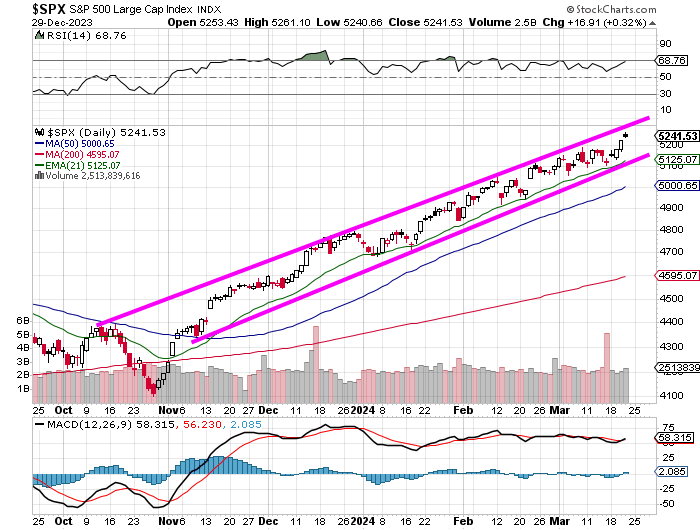

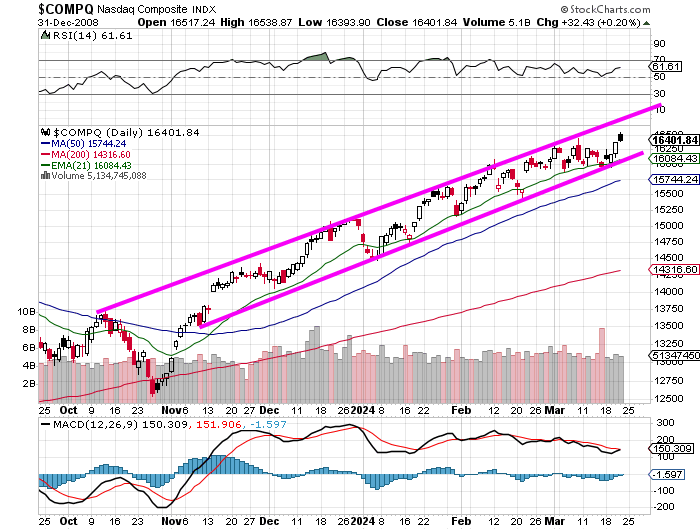

Proof of Alien (I Mean Algorithmic) Life

Our own Helene Meisler has been talking and writing about trend and price channels of late for the S&P 500. If you have not seen her material you have to see this, and it applies to the Nasdaq Composite as well.

You think humans could do that? I mean, I guess anything is possible, but talk about the trend as your friend... gee whiz!

Trading

I am guessing that most readers saw the news on Apple AAPL on Thursday. The US Department of Justice and sixteen state and district attorneys launched an antitrust attack on the firm's iPhone and iOS ecosystem. In addition, there is talk that both Apple and Alphabet (GOOGL) are about to face an EU investigation into the firms' compliance with new laws in Europe meant to rein in the power of large tech.

I used the 4% selloff in Apple yesterday to finish covering my short in that name. Not that I don't think AAPL cannot go lower, but Thursday's dip reestablished my 11% gain on the position, and I also see the risk of at least short-term upside in that name as the Vision Pro headset and Nvidia's NVDA collaboration may or may not reignite enthusiasm for the stock but that is a risk, if you're a short seller sitting on a nice win.

Economics (All Times Eastern)

13:00 - Baker Hughes Total Rig Count (Weekly): Last 629.

13:00 - Baker Hughes Oil Rig Count (Weekly): Last 510.

The Fed (All Times Eastern)

09:00 - Speaker: Federal Reserve Chair Jerome Powell.

13:00 - Speaker: Reserve Board Gov. Michael Barr.

16:00 - Speaker: Atlanta Fed Pres. Raphael Bostic.

Today's Earnings Highlights (Consensus EPS Expectations)

No significant quarterly earnings scheduled.

At the time of publication, Stephen Guilfoyle was long NVDA equity.