Fed Analysis, Dot, Dot, Goose, Reaction, Inflation Progress? S&P Shooting Star

The optimism expressed both in Fed Funds Futures pricing and across the Treasury yield curve was seen in stocks as well, regardless of what the Fed and Powell tried to tell us.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Well ahead of the release of the FOMC policy statement on Wednesday afternoon, the Bureau of Labor Statistics released their data on May consumer prices on Wednesday morning. May CPI hit the tape flat from April at the headline, which was a tick below expectations for monthly growth of 0.1%. The core print crossed the tape at month-over-month growth of 0.2%, which was also just a tick better than consensus view.

On a year-over-year basis, which is almost always more focused upon than the monthly data, headline May CPI printed at growth of 3.3%, while core CPI showed growth of 3.4%. Both of these prints beat expectations by one-tenth of a percentage point, and both were down from the pace experienced in April.

Something of a victory over inflation? Some certainly seem to feel that way. This was a second consecutive month of slowing year-over-year CPI. Then again, CPI is still running hotter on a year over year basis than it was as recently as February, and we have seen fits and starts in slowing inflation a couple of times over the past year.

Much of this latest deceleration in consumer prices came courtesy of outright deflation across energy prices, but it wasn't just energy. New autos, apparel, and transportation services all printed at least on a month-over-month basis with minus signs in front of their number. Interestingly, inflation for medical care commodities actually heated up, and shelter remained an issue.

Demand for Treasury debt securities after these prints crossed expressed an investor view, or should I say an investor "hope" for a reduced interest-rate regime going forward. The U.S. 10-Year and 2-Year Notes each rallied, as their respective yields dropped seven basis points apiece to 4.33% and 4.77%. As it turned out, the Fed, after having been fooled once or twice on inflation, was to show more caution than anything else a few hours later.

The Fed Steps to the Plate

First came the statement as it always does. This time the FOMC's quarterly economic projections came along for the ride. The Fed was not to be as easily led by a moderately softer-than-expected inflation print for May as was Wall Street. Wall Street was on "risk-on" mode for most of the rest of the day, though there was a late reversal that might be cause for short-term concern. I'll show you that chart in a few minutes.

The FOMC Policy Statement for June 12 was simply another "cut and paste" job, and this time, there was even less original content than usual. There was a minor change in the first paragraph where a "lack" of progress towards the Fed 2% inflation objective was replaced by "modest" progress. Guess that was their response to the May CPI report. I thought it somewhat important that the sentence "The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent" was left unchanged.

That alone informs the reader that the Fed is not feeling exceptionally dovish at this time and could be a warning that barring an economic calamity, this might just be the ballgame until after the national election in early November.

Dot, Dot, Goose!

There were no jaw-dropping surprises to be found in the Fed's economic projections. 2024 GDP was left at growth of 2.1%, which is where the Fed saw this data-point back in March. The committee also left its unemployment rate for 2024 where it was in March, at 4%. Then there are some minor tweaks. Headline PCE inflation for 2024 was moved up to growth of 2.6% from growth of 2.4%. while Core PCE for 2024 was moved up to growth of 2.8% from growth of 2.6%.

As one might expect, with the Fed expected to experience less success in 2024 as far as returning inflation to their objective, the FOMC also expects to be less aggressive in the implementation of easier monetary policy this year. Their median projection for year's end 2024 Fed Funds Rate is now 5.1%, up from 4.6%. With the current target for the FFR at 5.25% to 5.5%, this equated to a reduction of 25 basis points this year, down from a projection for a reduction of 75 basis points this year made three months ago.

The FOMC projects much more success over 2025 and 2026 in getting their target range for the Fed Funds Rate lower, but in all honesty, they always see greater success in the future and any projections made beyond the short-to medium-term future should be taken with a grain of salt. The Fed also sees 2% GDP growth, exactly 2% GDP growth for both 2025 and 2026, while unemployment remains in the low 4%'s and inflation continues to moderate towards 2%.

I hope they are correct. I doubt it will be that easy. The fiscal situation this country now finds itself in, makes me wonder why anyone would want to win the election in November. It's practically written in stone that the next president will be saddled with an abundance of blame for what Congress did fiscally both during and after the pandemic era.

Fed Funds Futures

Probabilities for rate cuts at future 2024 FOMC policy meetings ran wild throughout the day on Wednesday, at times showing expectations for easier policy (after the CPI was released) and at other times, after the FOMC statement was released, showing less "optimism." As I work my way through the zero-dark hours on Thursday morning, the probability for a 25-basis point rate cut on July 31 stands at just 8%, but the likelihood for a 25-basis point rate cut by September 18 now stands at 61%.

That's interesting, given that the decision made that day will be less than seven weeks ahead of the presidential election and the Fed would face serious questions about both its credibility and independence from the Biden administration if such action was to be taken that close to Election Day without an overt, significant threat to the economy also being present. These futures markets are pricing in a 57% probability for a Fed Funds Rate reduction of 50 basis points by year's end.

Equities

The optimism expressed both in Fed Funds Futures pricing and across the Treasury yield curve was seen in equities as well, regardless of what the Fed and Chair Powell tried to tell us. Algorithms just saw that 0.0% monthly print for May headline CPI and traders rejoiced.

All of our major and mid-major equity indexes closed in the green on Wednesday, with the exception of the Dow Industrials, which is probably the least closely followed index of them all in 2024. That was largely due to beat-downs at Nike NKE and Salesforce CRM that offset another run for the roses by Apple AAPL.

The S&P 500 popped 0.85%, while the Nasdaq Composite soared 1.53%. Both of those majors closed at new records. Again. The Philly Semiconductors roared ahead by 2.9%. as the small-to mid-caps gained, the Transports gained and even the banks gained. Interestingly, only five of the 11 S&P sector SPDR ETFs shaded green for the session, led by a 2.21% run by Technology XLK. Defensive sectors took three of the bottom four slots on the daily performance tables, led lower by the Staples XLP.

Winners beat losers by almost 5 to 2 at the NYSE and by about 7 to 4 at the Nasdaq. Advancing volume took just a 51.4% share of composite NYSE-listed trade, but a cool 70.4% share of composite Nasdaq-listed trade thanks to the strength in tech and small caps. Aggregate trade did increase on a day-over-day basis across both exchanges as well as across the memberships of the S&P 500 and the Nasdaq Composite. That does make Wednesday's price discovery meaningful.

However...

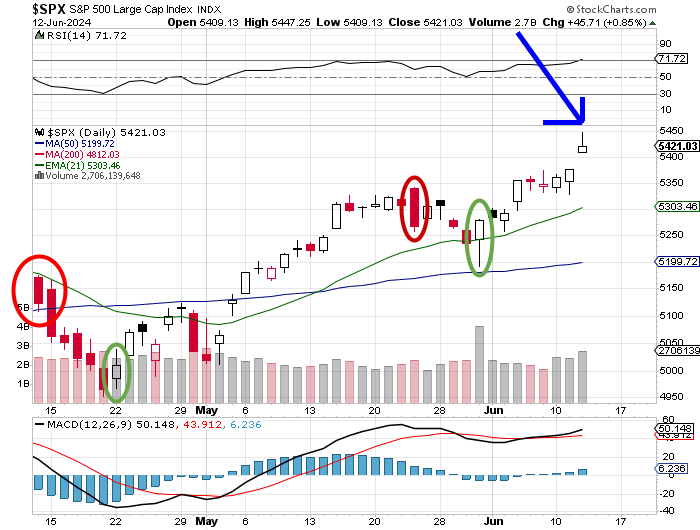

I did see something that I was not sure that I liked very much. Check out the daily chart of the S&P 500. Yes, we have an uptrend that extended on Wednesday, but look at Wednesday's candlestick.

That looks a lot like a "shooting star" one-day pattern versus an "inverted hammer." Though in isolation both patterns look the same, a shooting star occurs at the top of the chart and reflects a midday bearish reversal that can last into following sessions. We have that here.

What we do not have is that Wednesday was still an "up" day for the index. That does make the carryover for the reversal less certain. I still would walk patrol with my head on a swivel today if I were you, or if I were me.

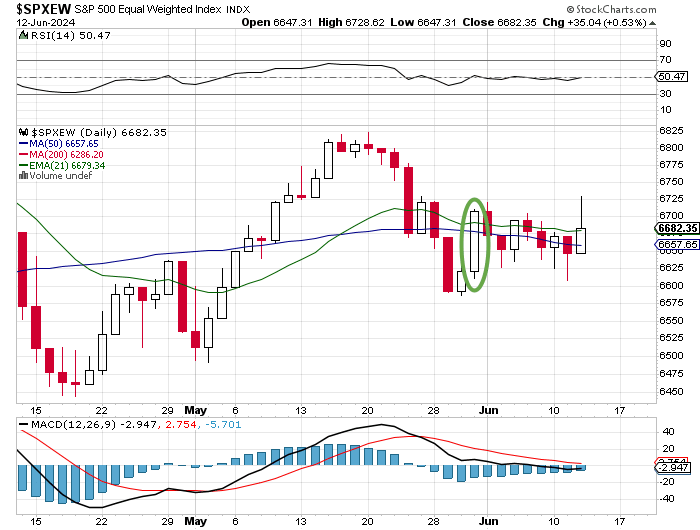

We see in the same chart, but of the equal-weight S&P 500, really no follow-through from the "Day One" change in trend two weeks ago, but we do see the failure of the broader market for large-caps to break away from its moving averages.

That's all for this morning. Carry on.

Economics (All Times Eastern)

08:30 - Initial Jobless Claims (Weekly): Expecting 225K, Last 229K.

08:30 - Continuing Claims (Weekly): Last 1.792M.

08:30 - PPI (May): Expecting 0.1% m/m, Last 0.5% m/m.

08:30 - Core PPI (May): Expecting 0.3% m/m, Last 0.5% m/m.

08:30 - PPI (May): Expecting 2.5% y/y, Last 2.2% y/y.

08:30 - Core PPI (May): Expecting 2.4% y/y, Last 2.4% y/y.

10:30 - Natural Gas Inventories (Weekly): Last +09B cf.

13:00 - Thirty Year Bond Auction: $22B.

The Fed (All Times Eastern)

12:00 - Speaker: New York Fed Pres. John Williams.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: KFY (1.12), SIG (0.98)

After the Close: ADBE (4.39), RH (-0.09)

At the time of publication, Guilfoyle was long AAPL equity.