Extreme Currency Valuations Have a Shelf Life

Today’s yen weakness feels as unsustainable as the 2011 yen strength was.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The Japanese currency has been in a freefall against the U.S. dollar for weeks, leaving the yen at its lowest valuation since the 1990s. While the Bank of Japan is known for intervening in the currency markets, the central bank has been noticeably quiet.

Coming into this week, analysts and pundits seemed to believe both the BOJ and market participants had accepted the weakness in the yen. Accordingly, the masses were expecting the yen to remain lower for longer. Yet, interventions are best performed when the markets least expect it, and speculators are holding historically aggressive short positions in the yen. That seems to be precisely what could be transpiring.

Monday’s snapback rally from overnight lows has been a one-day-wonder thus far, but there are a few red flags on the monthly chart that suggest we might have turned the corner. We talked about this on Ausbiz TV recently; click here to view the clip.

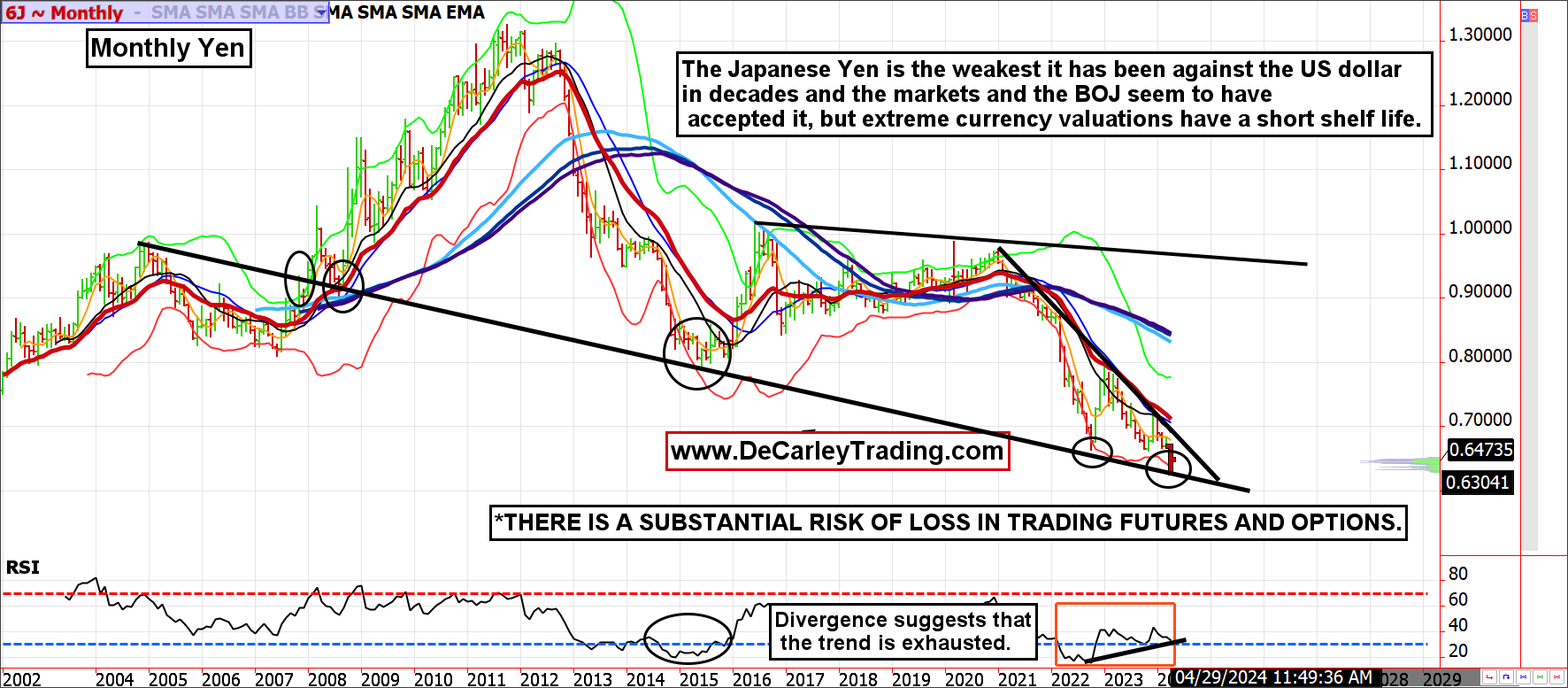

Monthly Japanese Yen Chart

A pivot line on a monthly chart dates back to the pre-Financial Crisis era that is currently in play and should act as support in the coming weeks. This pivot line began in the early 2000s as resistance but became supportive as the yen rallied during the financial crisis.

The downtrend in the yen has been intact for over a decade and has been successfully tested on three separate occasions — each concluded with a large rally. Further, the RSI (Relative Strength Index) is making higher lows while the underlying yen futures contract is making lower lows. This is a sign of dysfunction and an exhausted trend.

If support holds, as expected, a sharp short-covering rally could dominate trade to increase prices substantially. A break above 0.700 (70 cents in U.S. currency for every 100 yen) leaves the door open for the mid-0.800s or even the mid-0.900s if the yen benefits from flight-to-safety buying.

Today’s yen weakness feels as unsustainable as the 2011 yen strength was. For clarity, yen futures traded on the CME Group are quoted in terms of the dollar. It is the inverse of the standard FX pair JPY/USD.

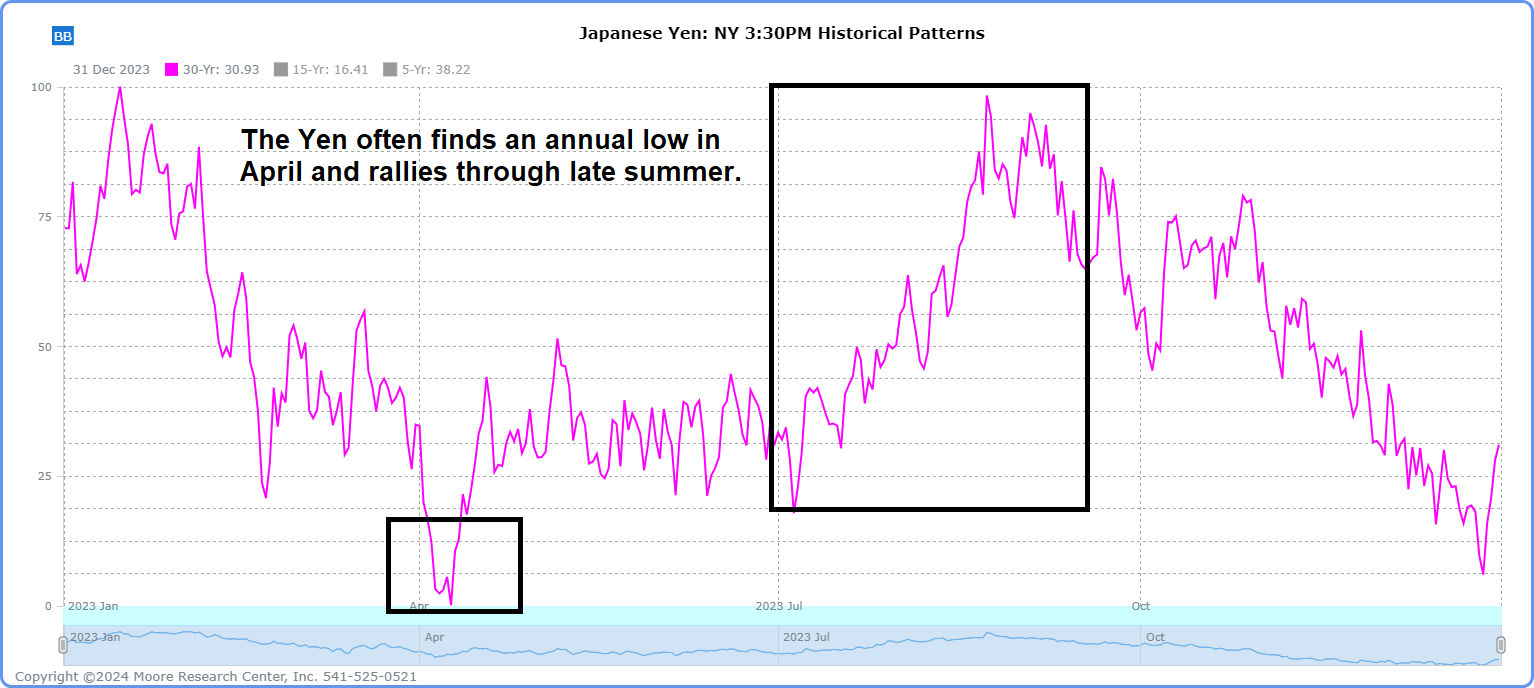

Yen Seasonality

Perhaps yen seasonality will act as a tailwind for the Japanese currency. Data spanning the last 30 years suggests the annual low is most often made in the month of April. That seasonal strength frequently continues through the late summer months.

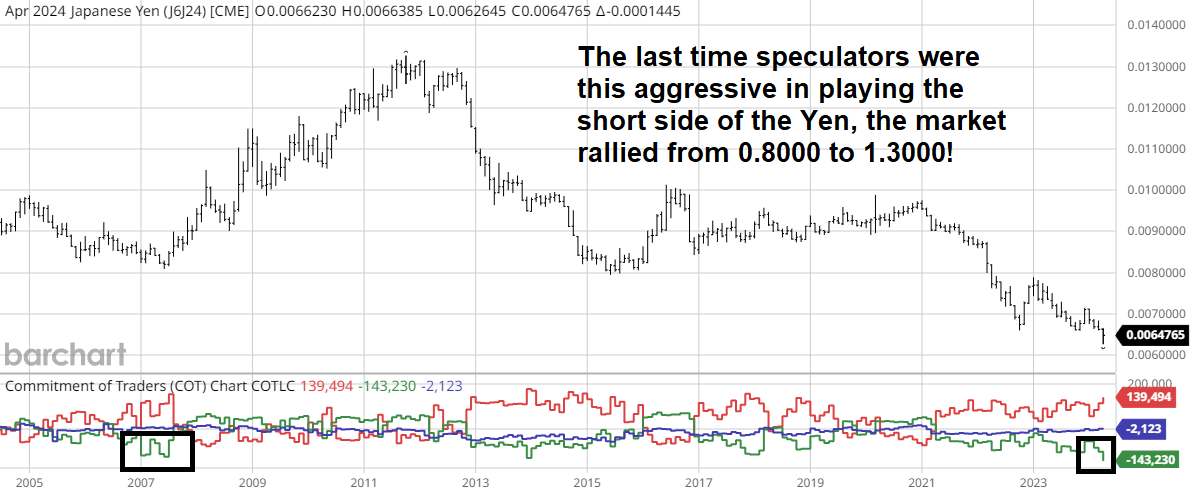

Commitments of Traders Report

The world is short the yen. For years, savvy investors have been participating in a carry trade in which they borrow yen at low-interest rates and invest at higher interest rates elsewhere. Further, hedge funds and speculators are known to be holding the largest net short position in history, or at least in the vicinity of such.

With support looming and seasonality favorable, the odds of a short squeeze are significant. The last time speculators were this short yen futures was just before the financial crisis. The market rallied from 0.8000 to 1.3000 as the carry trade was unwound.

Bottom Line

The yen did spend some time in the .3000s and .4000s in the 1970s and 1980s, but that was before the industrialization of Japan. Also, currency markets, like commodities, are self-correcting.

When currencies become attractively priced, the related country’s exports become more attractive to outside buyers. Further, the lower the yen gets, the more dangerous the carry trade becomes.

Congratulations if you have been short the yen in any capacity, but it is probably time to focus on risk management. Risk comes fast and complacency kills.