As European Bonds Get Spooked, Treasuries Could Get a Boost

French elections shake up confidence in the region, and breadth is sorely lacking. Let’s dig into both.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

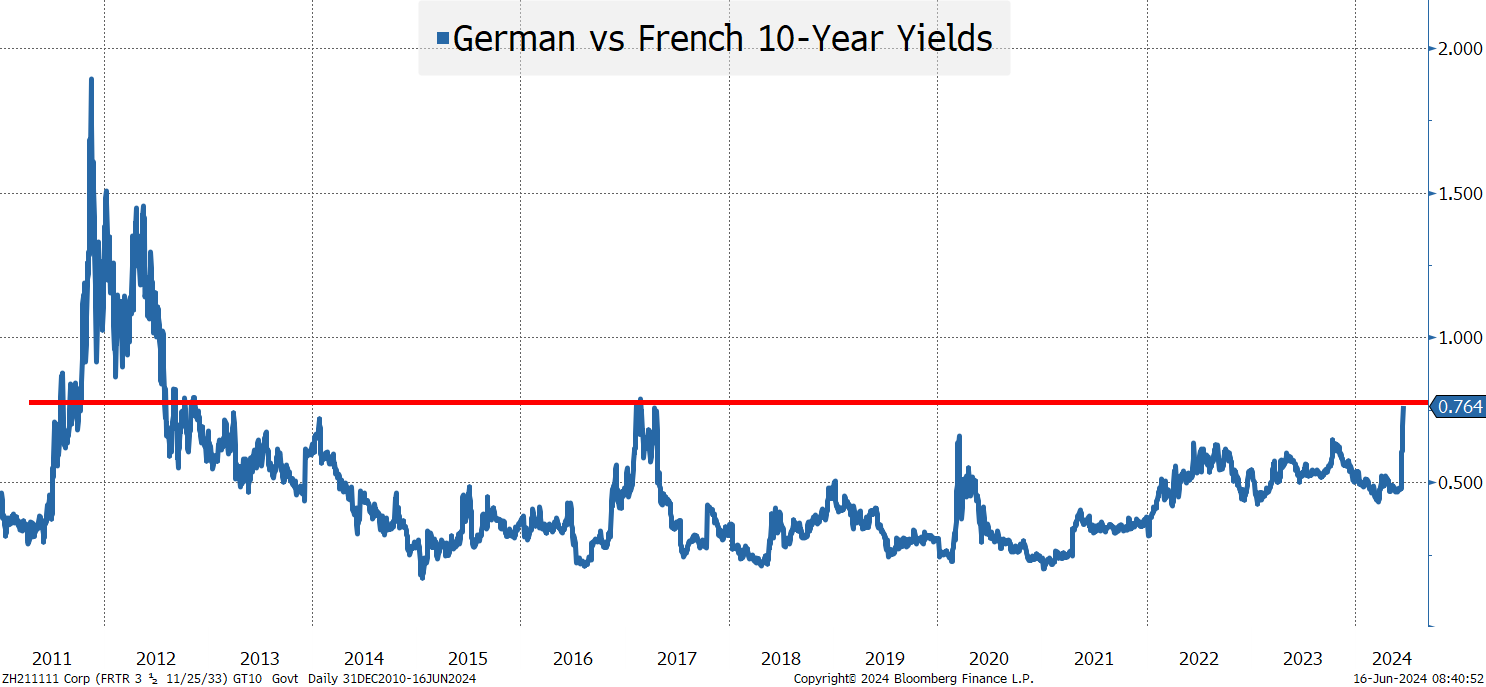

Elections in France seem to have finally spooked European bonds. This jolt appears to go beyond Marine Le Pen’s party having some recent success. The concern is the risk that both the extreme left and extreme right parties take away power from a more “centrist” Pres. Emmanuel Macron.

The spread between French bond yields and German bund yields (which are viewed as the risk-free rate in Europe) are now trading at one of the widest spreads since the European debt crisis. It isn’t just France that is a concern on the political front in Europe. Other countries are experiencing a rise in popularity for “extreme” candidates. Is the European Union at risk? Not yet, but it makes Europe even more difficult to invest in than it was. The European Central Bank had the most hawkish cut I can remember. It cut rates but raised inflation expectations.

Expect money to flow out of Europe and into the U.S., as investors digest the political landscape in Europe. If so, this move might help treasuries. There has been a mixed reaction to higher European bond yields. Some days we seem to get a “flight to safety” trade, while on others we moved higher in sympathy. I think the 10-year fits nicely into a 4.3%-4.5% range and am selling fixed income products at or below 4.3% while adding at 4.5% and above (for now).

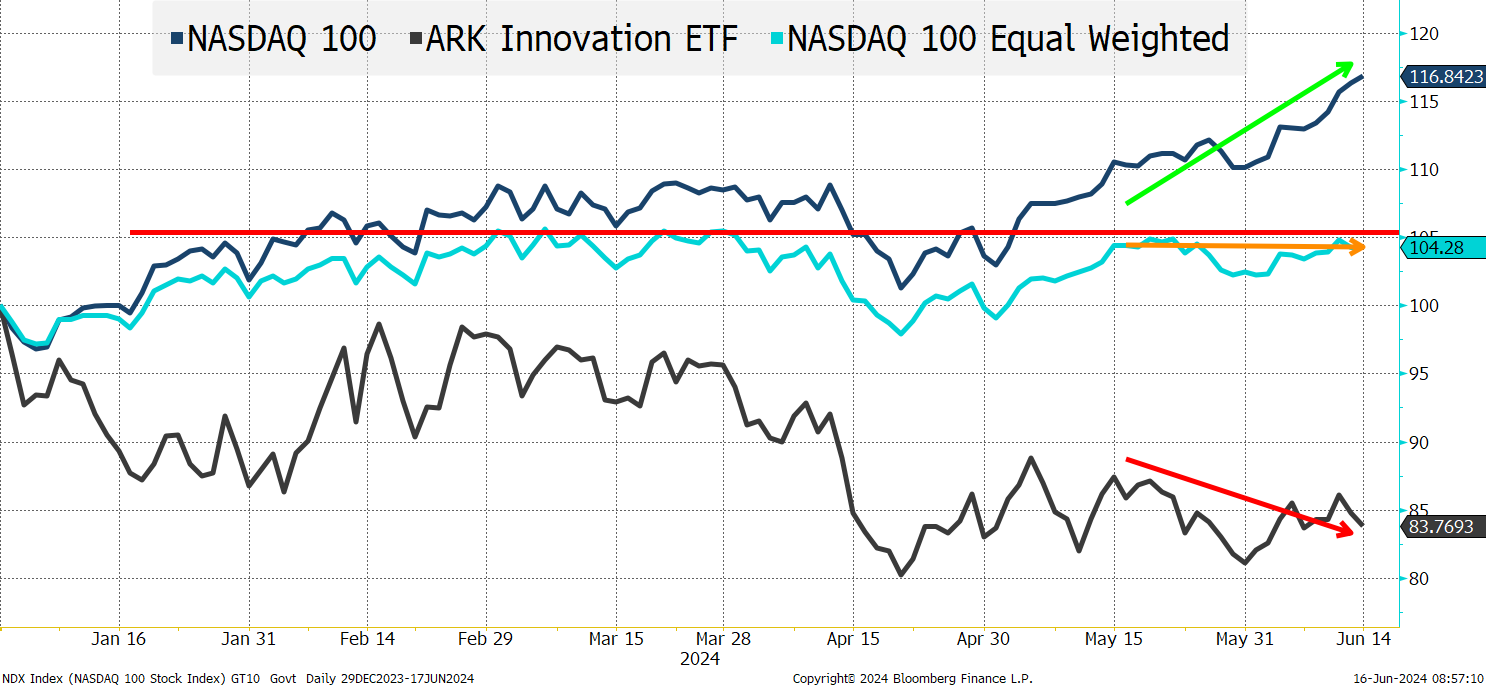

But don’t forget bout breadth.

My inbox is inundated with all sorts of pieces on the lack of breadth, how few stocks are at 52-week highs, record percentages for the top stocks in various indexes and so on.

This chart shows the Nasdaq 100, the Nasdaq 100 equal weight index and Ark Innovation Fund ARKK (the S&P 500 chart wouldn’t look dissimilar).

You can see that the equal-weight index isn’t at its highs and has barely budged in the past few weeks. In that same time-frame, the market-cap weighted index has been strong, confirming just how narrow this rally has been. It has been extremely artificial intelligence driven and continues to be AI driven. That is the main reason I included ARKK. It is my proxy for “innovation” and it continues to meander, while the Nasdaq 100 soars. So much of the return is now generated by a handful of large companies with great stories. But that leaves me wondering how long this bifurcated market can last? I am not sure, and the answer to that question might be, longer than we think.

If investors start pulling money out of Europe and into the U.S. I expect it will go into index funds, creating more demand for the most heavily weighted stocks.

If you remember, late October and early November of last year, I was pounding the table for the laggards to catch up and was rewarded as that trade worked out great. Right now, I cannot see that trade working. The “catch-up” scenario would make a lot of sense if the economy was firing on all cylinders, but that isn’t my outlook for the coming months.

We have inflows into indexes, getting invested heavily in the winners (because of their size) and while many are questioning valuations (I’m there), we are starting to see some “bubble” concerns that are believable.

Maybe it is the perfect time for a rotation, but I see that working so much better in a down market, rather than an up market. I am starting to rebuild a position in China (primarily through iShares China Large-Cap exchange-traded fund FXI) and I’m looking at starting a position in India (also via an ETF, though I haven’t decided which one, yet).

At the time of publication, Tchir was building a position in FXI and looking to do the same for India-related ETFs.