A Presidential Headlock, Pivotal Day for Tesla's Chart, Lululemon Annihilation

A pro-wrestling-style spat between Trump and Musk hits Tesla and boosts ... Rocket Lab. Also, a rare breadth tie and ... today's jobs day.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I still can't believe what we all witnessed on Thursday afternoon.

When I was a kid, I mean a small kid, like early elementary school aged, I used to watch professional wrestling. I couldn't understand how these guys could take such a serious beating and do it over and over again. My favorites were the long-time champ, Bruno Sammartino and Chief Jay Strongbow. Much to my chagrin, later on, as I approached adolescence, I found out that Chief Strongbow wasn't even Native American but was really an Italian-American fellow named Joe Scarpa. So, the wrestling was not real, nor were the personas. I got over it and stuck to team sports where I thought I could better trust the competition.

On Thursday, former DOGE head Elon Musk and Pres. Trump ran an hours-long social media battle that sunk into the theater of the ridiculous, making both men look foolish. Was this just some kind of show? For the sake of both men, I'd like to think so. The president appeared to vent his frustrations with Tesla's TSLA CEO as a meeting with the press from the Oval Office with German Chancellor Friedrich Merz present and looking a little bewildered. Seemingly all day long, Musk attacked the "big, beautiful bill" and attacked the president on his X (formerly Twitter) social media platform, while the president attacked Musk on his Truth Social platform.

The back and forth slinging of nonsense and pure drivel hit a crescendo with Musk accusing Trump of not releasing the Epstein files because he's supposedly mentioned in them and suggesting that the president should be impeached. The president, for his part, mentioned taking actions that would pull government funding or contracts or both from Musk's businesses. This is why Tesla shares were down more than 14% on the day and the very idea of seeing SpaceX do less federal business is why Rocket Lab USA RKLB is up more than 4% overnight.

Cooling Off?

That's the rumor, anyway. After Musk had threatened to decommission his SpaceX Dragon spacecraft immediately, which after the Boeing BA debacle, may be the only way to ferry NASA astronauts back and forth between planet Earth and the International Space Station, tempers appeared to cool off a bit. Politico reported on Thursday evening, that a call had been scheduled between the world's richest man and its most powerful.

After neither side had taken any shots at the other for a bit, Musk mentioned that he would not be decommissioning the Dragon spacecraft and publicly allowed (on X) that maybe it would be "good advice" to step back and cool off for a bit. Tesla shares are up more than 5% overnight on the very idea that the two may have gotten carried away and could potentially overlook the absurdity that was Thursday.

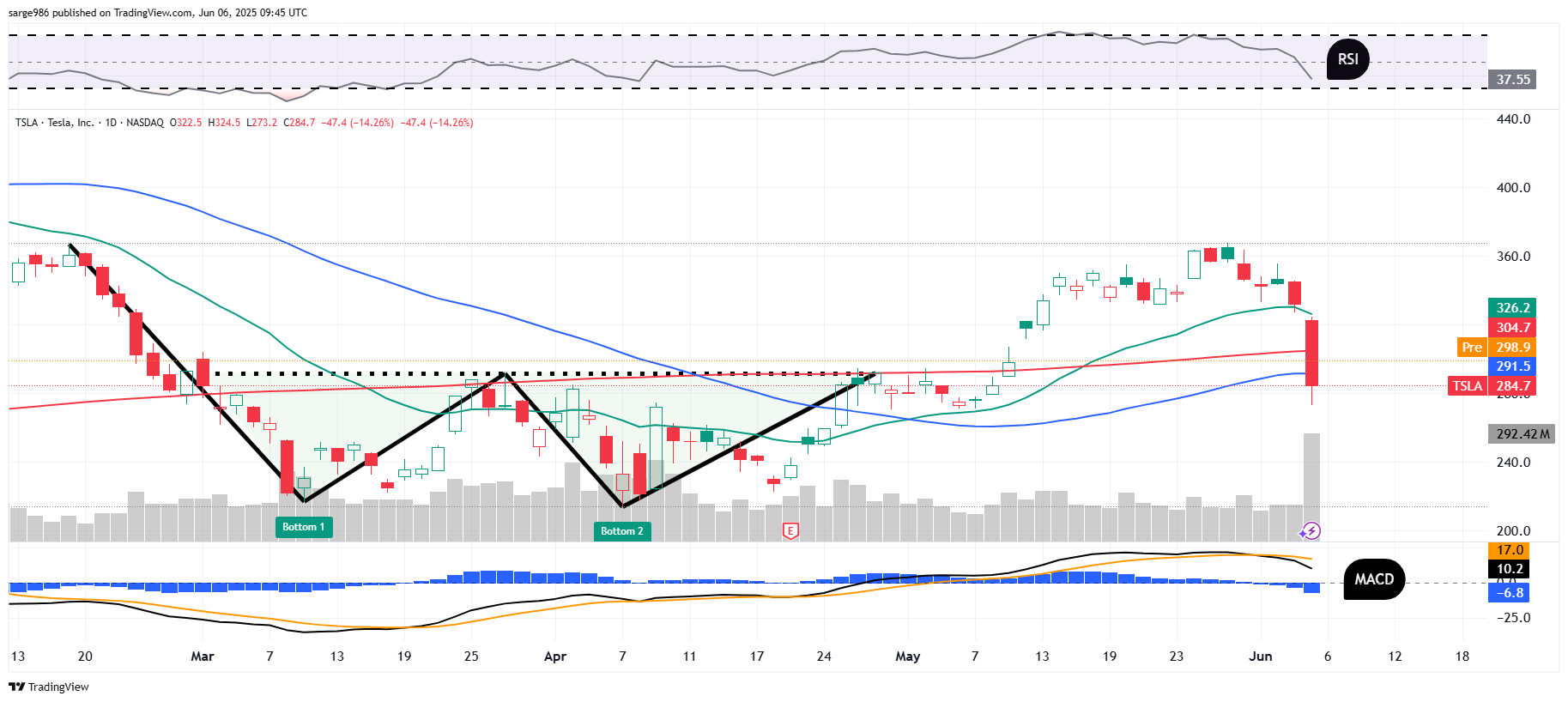

Serious Day for Tesla?

Shares of Tesla surrendered their 21-day exponential moving average, 200-day simple moving average and 50-day simple moving average in that order, on Thursday. This would be incredibly bearish for the stock if those levels could not be quickly retaken.

Overnight, the shares have been trading above both the 50-day and 200-day lines. That should keep portfolio managers invested. But this will likely be a very serious day.

Back To Reality...

Friday Morning. Today is May jobs day. Jobs day is, under normal circumstances, among the most high-profile macroeconomic events of any month. This month, this is perhaps truer than ever as the ADP Employment Report on May private sector job creation so badly disappointed economists on Wednesday. Wall Street is looking for a non-farm payrolls print close to 120,000 this morning. Readers will see below that I am up around 130,000 for this number.

It's been a tough week for domestic macroeconomic data so far, which puts more pressure on Fed Chair Jerome Powell to start cutting short-term interest rate targets, despite the inflationary signals visible in both the manufacturing and service sector ISM surveys for May. Earlier this week, May construction spending surprised with a negative print, its second contractionary month in a row. This was followed by the grotesque ADP print on Wednesday and horrific revisions to data covering first-quarter unit labor costs and first quarter productivity.

In short, this morning's survey results will matter and could push the central bank one way or the other. Especially with the Bank of England, the European Central Bank and now the Reserve Bank of India all now getting increasingly dovish.

Bearish Day One?

Weren't we just talking about having confirmed a bullish change in trend? Yes, we were. That said, I did tell you that this was a tough one to trust. I was referring to the expected exchange between Presidents Trump and Xi, which so far has not amounted to more than an agreement to keep talking and not a fight between Pres. Trump and Elon Musk. I was also wary of this morning's data release by the Bureau of Labor Statistics. Thursday's selloff occurred on increased trading volume. So, yet another "Day One"? Not so fast, my friend. Let's explore.

On Thursday, the S&P 500 lost 0.53%, as the Nasdaq Composite gave up 0.83%. The small to mid-cap indexes all showed very slight losses for the session. With the exception of a few names, such as Palantir Technologies PLTR, there was no market-wide beat-down. Ten of the 11 S&P sector SPDR ETFs shaded into the red on Thursday. That said, only Consumer Discretionaries XLY gave back more than 1% for the session and that was largely due to a 12.9% thrashing suffered by the Dow Jones U.S. Automobile Index.

That index was lower, thanks to the TSLA beating. Among large caps, Stellantis STLA suffered the second worst beating at -2.32%, so this was a Tesla thing. Communication Services XLC was the only fund among those eleven to finish the day in the green.

Breadth

Here's why there was no bearish Day One on Thursday. Winners and losers tied at the NYSE for the day. Tied? You're kidding me. I kid you not. Across the NYSE on Thursday, there were 1,376 winners, and 1,376 losers with 82 stocks closing unchanged. In the era of decimalized, electronic trading, do readers understand how hard it is to actually have a tie? The odds of such an event actually happening must be incredible. Losers beat winners at the Nasdaq by a 7-to-5 margin which is hardly overwhelming.

Advancing volume took a 45.9% share of composite NYSE-listed trade, and a 36.7% share of composite Nasdaq-listed activity. Aggregate trade was indeed higher on a day over day basis, across NYSE-listings, across Nasdaq-listings and across the membership of the S&P 500. That said, the breakdown of winners and losers was not decisive. We have no "Day One" bearish reversal.

That said, I am unsure right now, and I guess the market reaction to the jobs data will let me know if we still have a burgeoning uptrend in place. We still do have a series of higher-lows in place and that is a positive.

Anyone See Lululemon, DocuSign Bloodshed?

Lululemon LULU and DocuSign DOCU are simply getting annihilated overnight as comp sales were awful for LULU and both firms provided weak guidance. Broadcom AVGO, on the other hand, provided stronger-than-expected guidance last night, but after trading higher is now also trading lower as night melts into morning.

May Employment Situation (08:30 ET)

Non-Farm Payrolls: Expecting 130K, Last 177K.

Unemployment Rate: Expecting 4.2%, Last 4.2%.

Underemployment Rate: Expecting 7.8%, Last 7.8%.

Participation Rate: Expecting 62.7%, Last 62.6%.

Average Hourly Earnings: Expecting 3.7% y/y, Last 3.8% y/y.

Average Weekly Hours: Expecting 34.3, last 34.3 hours.

Other Economics (All Times Eastern)

1:00 p.m. - Baker Hughes Total Rig Count (Weekly): Last 563.

1:00 - Baker Hughes Oil Rig Count (Weekly): Last 461.

3:00 - Consumer Credit (May): Last $10.17B.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: ABM (.86)

At the time of publication, Guilfoyle was long RKLB, PLTR equity.