$100 Oil Price in Play but Bulls Should Heed This Warning

Oil has avoided meaningful supply disruptions amid Middle East conflict. But headlines and seasonality will play a role in prices ahead.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Thus far, we haven’t seen any meaningful supply disruptions in crude oil due to recent events in the Middle East. The overreaction is likely more of a short-covering event than a fundamental game-changer.

The oil market and market participants adopted a sell-the-rally mentality in 2024; as prices fell into the mid-$60.00s, speculators held one of the most minor net-long positions in decades. Also, options traders had given up on the idea of a rally, leaving the implied volatility in the oil call options near multi-year lows. In essence, the market was unprepared for the surprise, and we are seeing FOMO now that prices are finally moving in favor of the bulls.

Crude oil futures are notorious for buy-the-rumor-sell-the-fact price action; more specifically, the track record for buying into Middle East tension after it has already occurred is subpar.

This is because market participants tend to hit the “buy” button first and ask questions about geopolitical risk later. With this in mind, we caution traders about chasing prices higher. Perhaps the best approach is to wait for a large dip patiently. The U.S. rig count has fallen to a two-and-a-half-year low, and the monthly chart is constructive; thus, we could see $90.00 To $100 oil again, but it probably won’t be until next year.

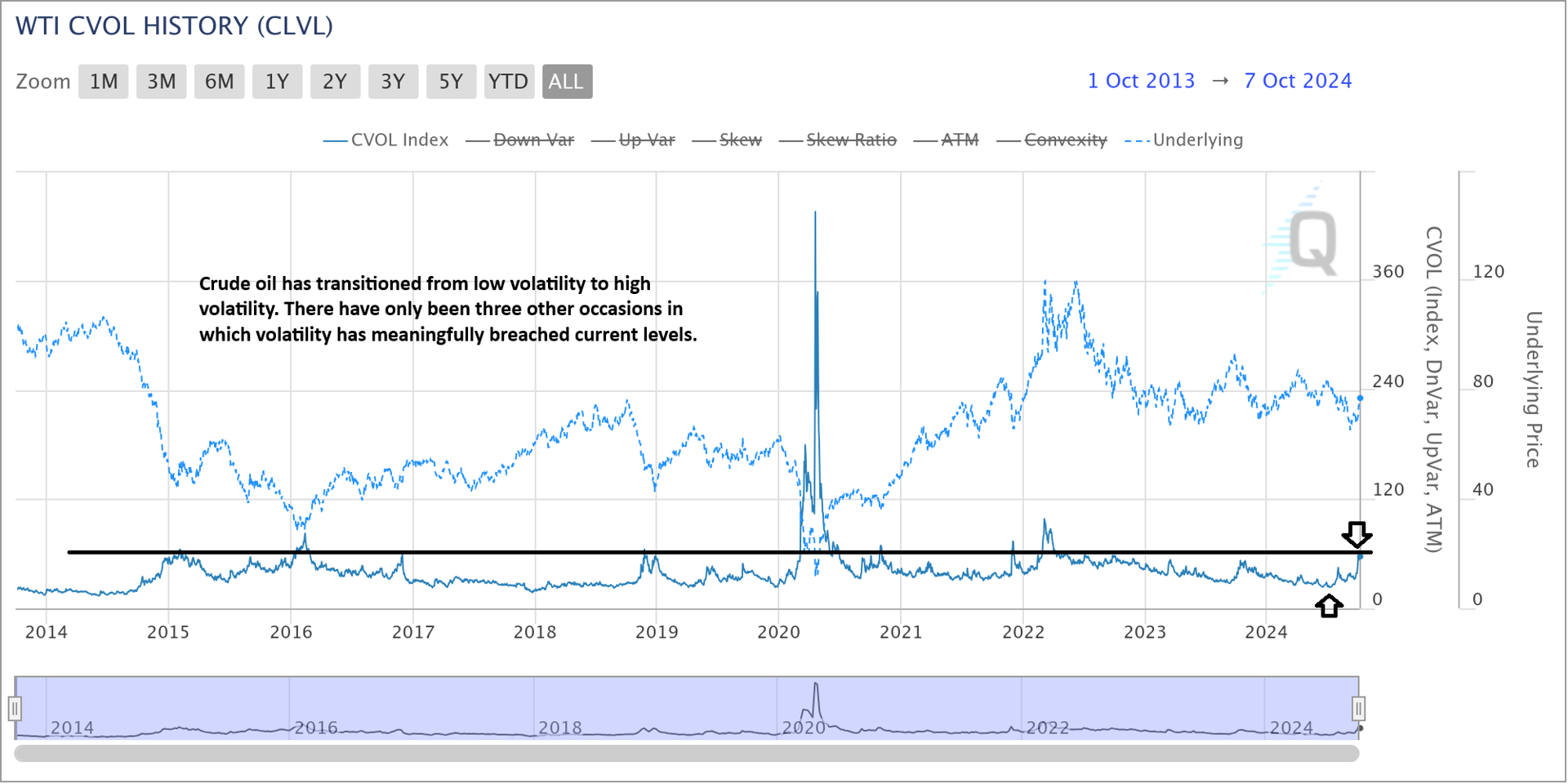

Oil Volatility

Earlier this year, we pounded the table to warn traders of historically-low volatility in the crude oil options market.

The implied volatility of oil options (the amount of premium priced into options by speculators to account for volatility risk) was near an all-time low. We thought this low-volatility environment made it an excellent time to be an option buyer, but it was one of the worst times ever to be an option seller.

With recent events, this has flipped. Implied volatility has increased from 25.00 to about 60.00, which has mostly been the ceiling on oil volatility. Throughout the last decade, oil volatility has only surpassed this level meaningfully on three occasions, one of those being the COVID shutdowns.

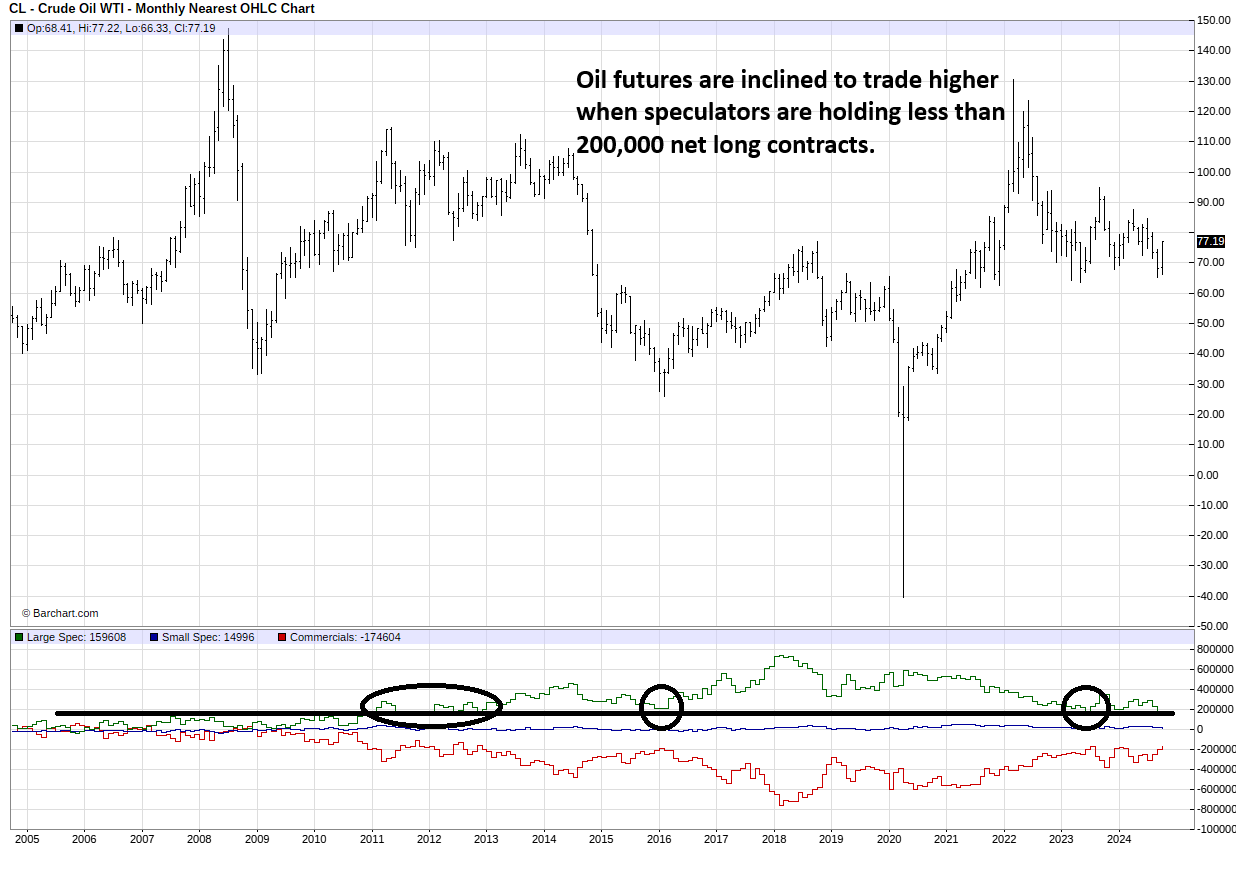

Traders Positioning

Going into fresh Middle East turmoil, large speculators had trimmed their long position to a net contract size of about 160,000. When this group holds less than 200,000, it tends to indicate that most of the sales have already occurred. Moreover, much buying power on the sidelines could be brought in on dips. This is precisely what has unfolded over the last week of trading.

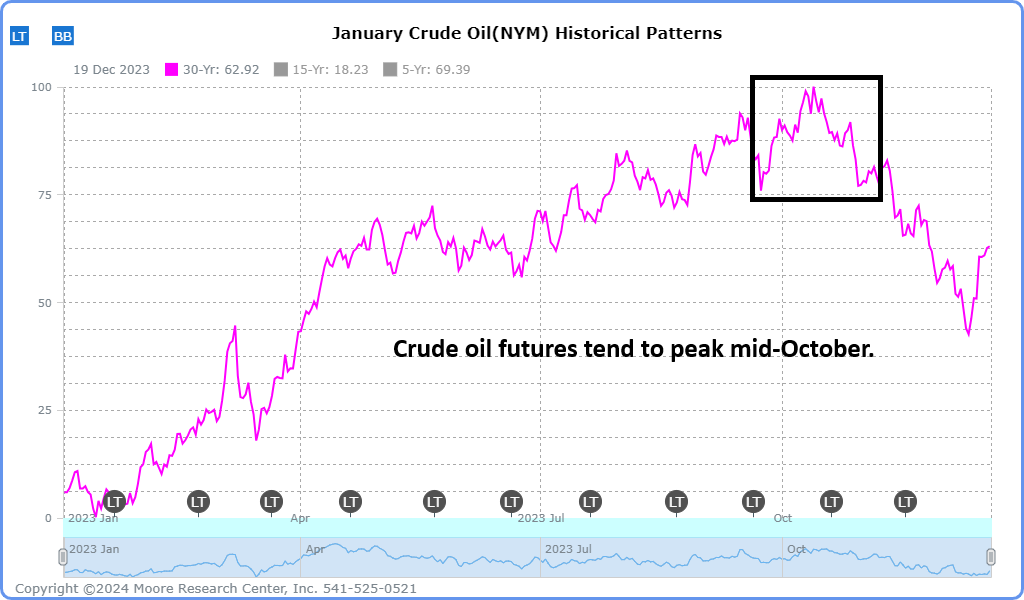

Seasonality

The oil market tends to run out of steam between October 12 and October 15. Thus, if history is a guide, this particular rally could be on its last leg (at least for now). Commodity market seasonality isn’t perfect, but it is generally a good idea not to go against the market’s tendencies.

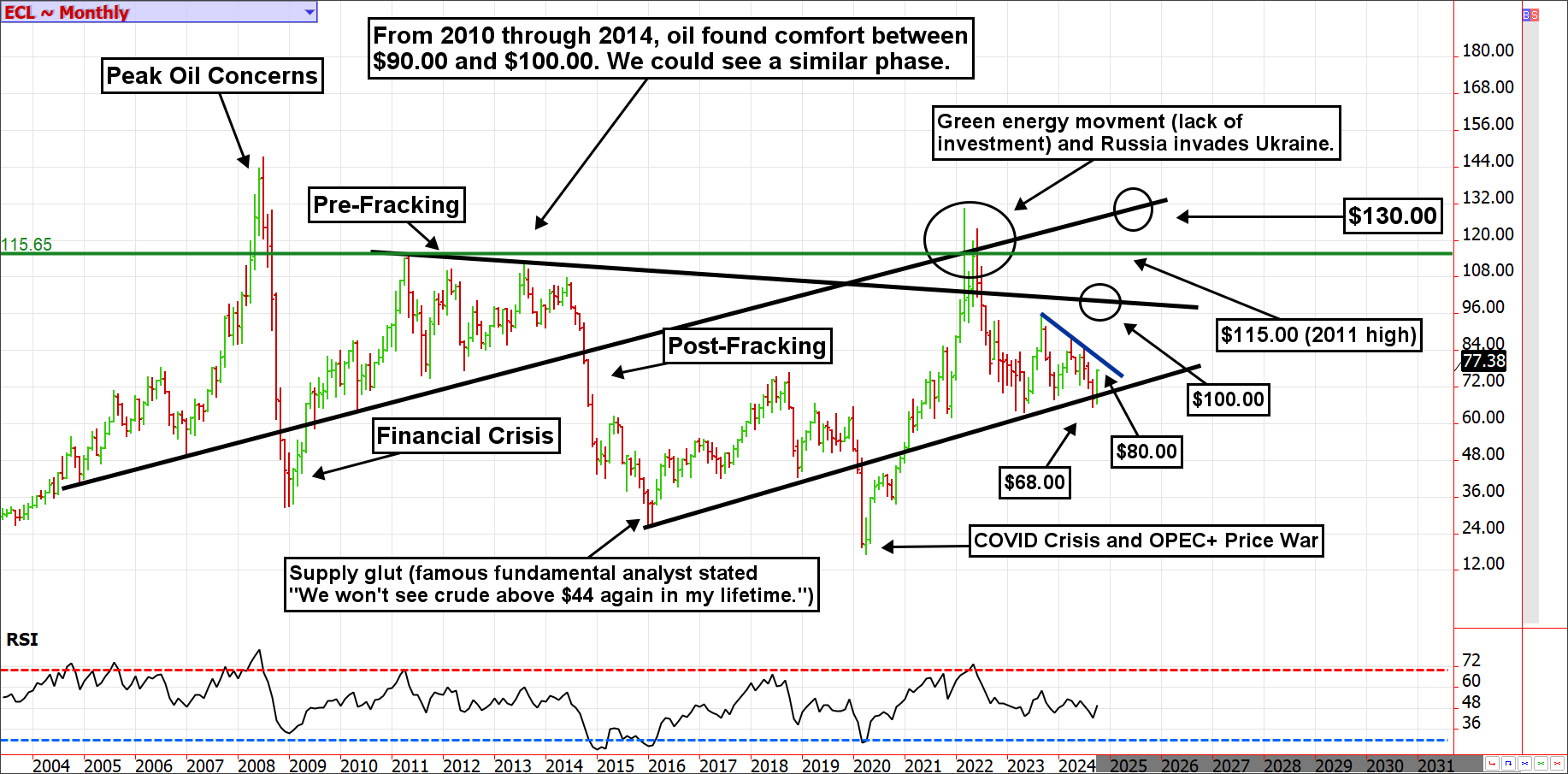

Monthly Chart

The long-term charts suggest $100 is eventually in play, but in the short run, we would likely run out of steam near $80.00, where the market has been most comfortable since the 2022 boom and 2023 bust.

Conclusion

These are not your grandparents' commodity markets. Central bank and government market interferences and political violence are working overtime to influence prices. Further, although the monthly chart of oil and trading positioning suggests the path of least resistance is higher for black gold, seasonality and headlines could work against the commodity in the near term.

If you are a bull wanting to pull the trigger, be patient. If you are a bull sitting on profits, protect them; immediately higher oil prices is far from a guarantee. There is a lot of game left to be played.

At the time of publication, Garner had no positions in any securities mentioned.