Investing in Berkshire Hathaway Is Like Hedging Against Your Overall Portfolio

Berkshire is really a Warren Buffett/Charlie Munger driven value-focused ETF.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Saturday morning, Berkshire Hathaway BRK.B reported third quarter operating earnings that popped 41% on a year over year basis, as the strongest performance came from its insurance businesses. The Railroad, Energy and Utility businesses dragged on that performance as the firm beefed up its cash position by adding almost $10B to its stash over three months' time. That doesn't necessarily mean that Berkshire was profitable, just that its businesses are doing well. Let's explore.

In full disclosure, I am long the "B" stock as in BRK.B, and that's where my focus will be for this article as I am just guessing that a lot more readers might be able to afford investing in a stock trading in the $350's per share than in the "A" stock BRK.A , which trades close to $535K a share.

Digging In

As far as generation of operating earnings are concerned, Insurance-underwriting improved to $2.422B from the year ago comp of $-1.072B. Insurance-investment income improved by 75.4% to $2.47B. Beyond that, the railroad (BNSF - formerly Burlington Northern Santa Fe) produced operating income of $1.221B (-15.3%) as the Utilities & Energy business wrapped up in one category, generated an operating income of $498M (-68.9%).

Moving on to the Statement of Earnings, for the three month period ended September 30th, Berkshire's total revenue added up to $93.21B, but investment and derivative contract gains/losses came to $-29.778B. Total costs and expenses amounted to $80.653B. That left EBIT of $-17.221B. Once accounting for interest and taxes, net income/loss attributable to Berkshire Hathaway shareholders landed at $-12.767B for a GAAP EPS of $-5.88 per B share (or $-8,824.00 per A share).

Fundamentally Speaking...

Over the first nine months of the year, Berkshire Hathaway generated operating cash flow of $34.796B (+28.7%). Out of that came CapEx spending of $13.701B (+25.6%). This left free cash flow of $21.095B (+30.8%). Out of this number, the firm has repurchased $6.978B worth of common stock for the firm's treasury. The firm does not return capital to shareholders in the form of cash dividends.

As of September 30th, Berkshire had a cash position of $157.241B inclusive of cash, cash equivalents and holdings of US T-Bills. The firm also holds investments of $22.435B in fixed maturity securities and $318.621B in equity investments, so the firm has cash and liquid investments that total a whopping $498.297B. Total assets amount to $1.019.933T including $115.147B in goodwill and other intangibles, as well as inventories of $24.755B. At 11% of total assets, intangibles are not an issue here.

Total liabilities less equity comes to $485.206B. This includes $124.781B in total debt. which can easily be paid off out of pocket without touching liquid assets meant to be longer term investments. This balance sheet as you already knew or at least suspected, is in fine shape.

My Thoughts

The businesses are up, thanks to a year where the insurers did not get whacked, at least not yet. The investments have gone sideways, which makes sense, as AppleAAPL is by far the firm's largest equity holding and Apple is down 5% over three months, while being up just 2% over six months. Berkshire's second and third largest holdings at least as of late June were Bank of America BAC and American Express AXP . Those two names are down by 16% and 12%, respectively, over the past three months. If you believe in the financials going into year's end and if you see the recent dip in Apple as a bottom, then, this is well set up.

I remain long the stock (BRK.B) and it has been good to me. I don't necessarily believe in the financials (or the rails) going into a recession. I do believe that insurance will continue to do well, for now. Overall, I like investing in a conglomerate like Berkshire which is really its own Warren Buffett/Charlie Munger driven value-focused ETF.

It's sort of a hedge against my own performance which can at times be aggressive or shorter-term in horizon than in the thinking of these two gentlemen. I'd rather allocate a slice of my overall equity exposure in their direction than just walk on by. Best part is they have to reveal just what it is that they are doing every quarter.

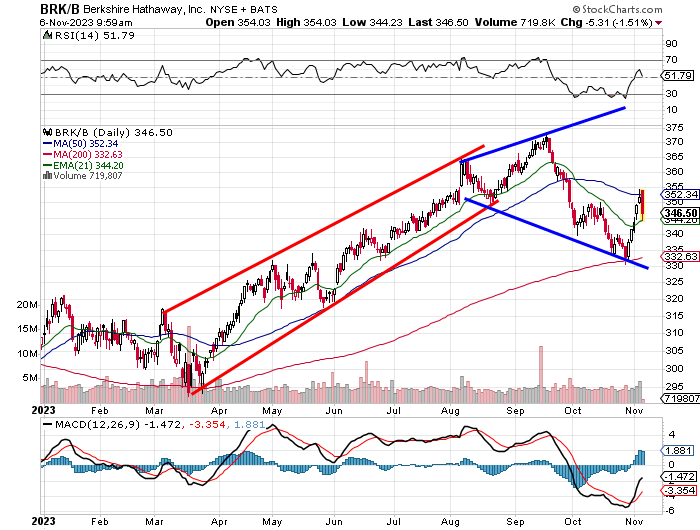

What was an ascending price channel for most of the year, has broken and looks to potentially be developing into a broadening asymmetric wedge. That pattern simply means that volatility is on the rise and doesn't help much with signaling direction.

Relative strength is once again neutral despite this morning's sell-off after having been oversold as recently as late October. The daily MACD (moving average convergence/divergence) is still in a wonky looking position, but has experienced a crossover by the 12 day EMA (exponential moving average) over the 26 day EMA (bullish), even though both are still in negative territory. At least the histogram of the nine day EMA is still hanging onto the positive side of the football.

The stock has shown support at the 200 day SMA (simple moving average), which is solid, but also resistance at the 50 day SMA. That's not so positive. This morning we are looking for support to show up at the 21 day EMA in order to get the swing traders on the side of the bulls. That would set up a second chance at that 50 day line.

For now, for the bulls, the 50 day SMA (currently $362) is the pivot. That puts our target at a lofty $416. Of course, this depends on the broader market as this firm's holdings have underperformed its businesses of late.

Panic? That's easy. This stock loses that 200 day line (currently $332), they'll lose me and a whole lot of portfolio managers.

(AAPL and BAC are holdings in the Action Alerts PLUS member club. Want to be alerted before AAP buys or sells these stocks? Learn more now.)

At the time of publication, Stephen Guilfoyle was long BRK-B equity.