Doug Kass: I Remain Bearish, And I've Got Lots of Reasons

While I recognize I'm in a small minority in embracing a negative market view, my investment approach is consistent and doesn't change with the weather.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

What follows is a compilation of recent commentary in my Daily Diary on the TheStreet Pro and comments delivered to my investors at my hedge fund, Seabreeze Partners.

To me, the stock market's advance this year has represented a challenge to value investors and to rational thought and analysis.

Investors, in our view, have not been compensated properly for the economic, profit, valuation, political, geopolitical and market structure risks I have expressed in my Diary throughout this year. Moreover, the interaction of monetary and fiscal policy has now led to a toxic brew — contributing to a nation of (nearly unfinanceable) entitlements with a bloated balance sheet and an unsustainable budget.

It has been most surprising that investors have continued to ignore that equities are materially overvalued relative to interest rates — with the equity risk premium at a 20-year low.

I recognize that I am in a small minority in embracing a negative market view. I am accustomed to being outside the herd (when justified). It is not dissimilar to my pessimistic and non-consensus views expressed in the summer of 2007 or in the early winter of 2021.

That said and as previously noted (and until recently), I have done a poor job in forecasting the market. At the same time, I have been a good risk manager — as despite our positioning in 2024 (on average at about 15% net short), I have sidestepped losses in achieving modest but positive returns.

My investment approach is consistent and doesn't change with the weather. As always, a value-oriented investment process considers upside reward relative to downside risk with an eye towards achieving "a margin of safety."

There is nothing like price to change investor sentiment (h/t "The Divine Ms. M"). Both Warren Buffett (Berkshire Hathaway) and I (Seabreeze) question why investors today would prefer to buy high and sell low. Given the dominance of passive products and strategies we have seen even more price following and reverence.

I am dispassionate in the implementation of my strategy — viewing high stock prices as the enemy of the rational investor and low prices as our ally. I don't worship at the altar of price and chase equities (when climbing) for the sake of investment performance when the fundamentals do not justify ownership. Security analysis, when done properly, allows one to determine "intrinsic values" and gives one confidence in exploiting the sort of wild price swings that have become commonplace.

This approach, while it might be wrong during certain discrete periods of time, will likely prove quite correct through a market cycle. (At least that is my experience!)

"Rule No 1: never lose money. Rule No 2: never forget rule No 1."

— Warren Buffett

When I am wrong, as I have been this year, it is naturally reflected in weak relative performance. However, even when wrong I am always attentive to risk management. As a reflection of this, my hedge fund has not lost money in the face of a sharp market climb (and we have actually made some money). But, when I am correct, as was the case in 2022, it is reflected in strong relative performance. (See The Oracle's quote above!)

***

Most notably and since last month's commentary, the domestic economy's outlook has eroded and the prospects for U.S. corporate profit growth have deteriorated.

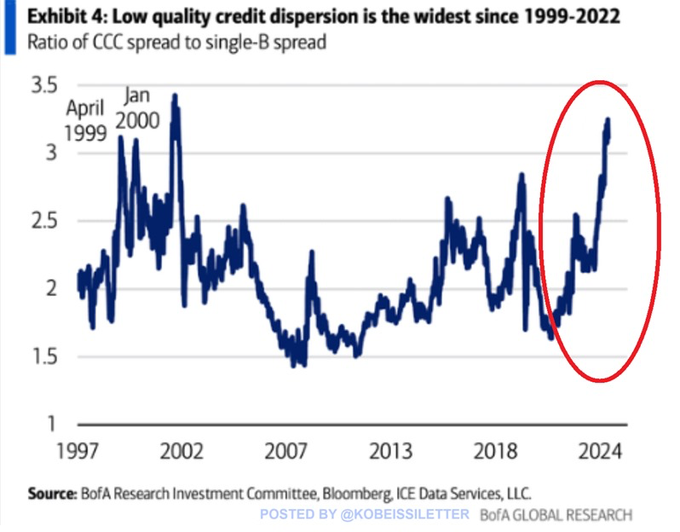

Corporate bond markets are flashing warning signs: Low-quality U.S. corporate bond credit spreads have spiked to the widest since 2001. In fact, the ratio of CCC-rated spread to B-rated spread has DOUBLED in the last 2 1/2 years. This difference is now even wider than the run up to the 2000 Dot.com bubble. Meanwhile, 346 large corporations have declared bankruptcy through June, 2024, the most since 2010:

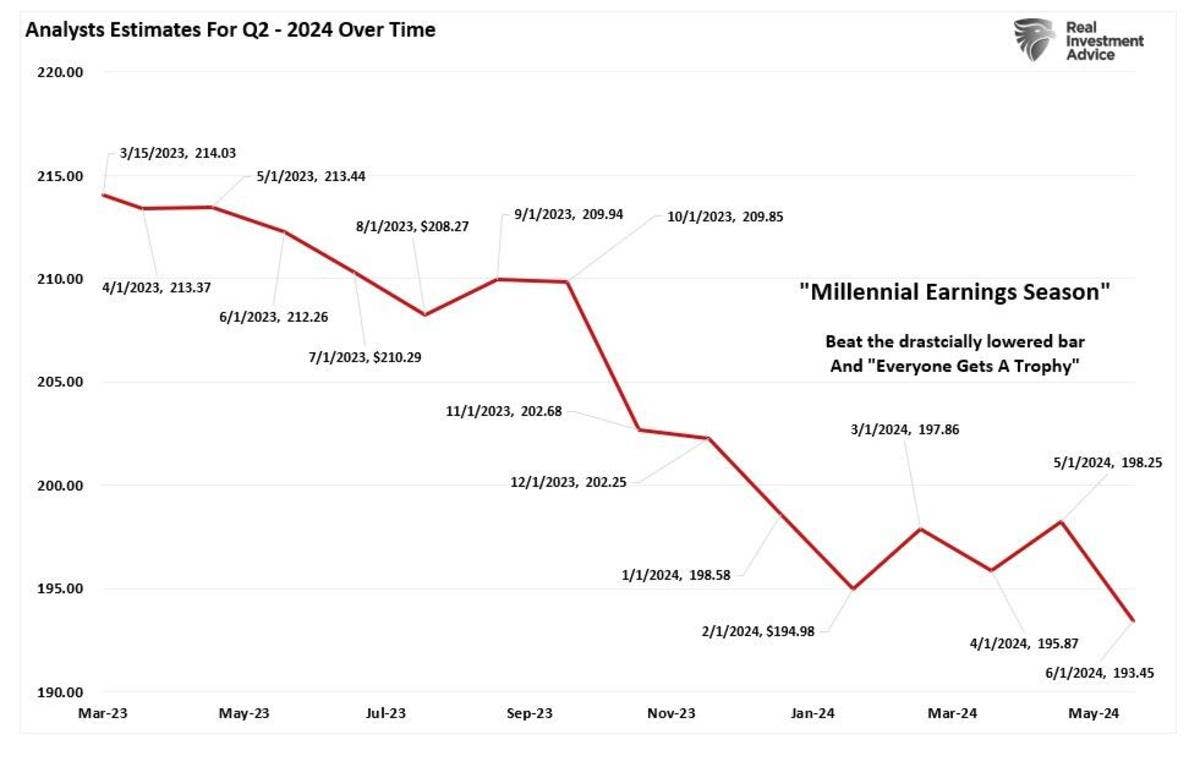

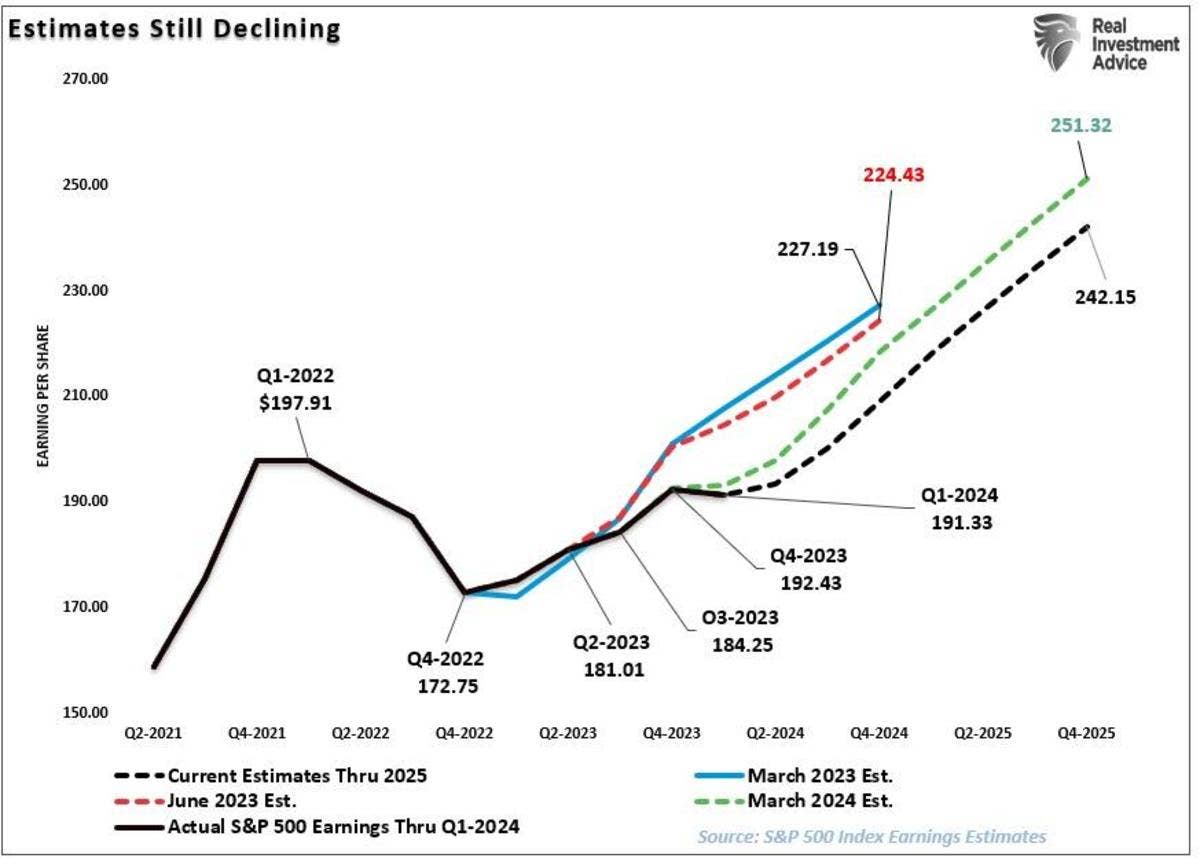

Optimism surrounding strong corporate profit growth in 2024-25 (used by many to rationalize today's high stock prices) seems unjustified.

As a reflection of this view, expectations for 2024 have recently fallen by $5/share and for next year consensus profit projections have declined by $9/share:

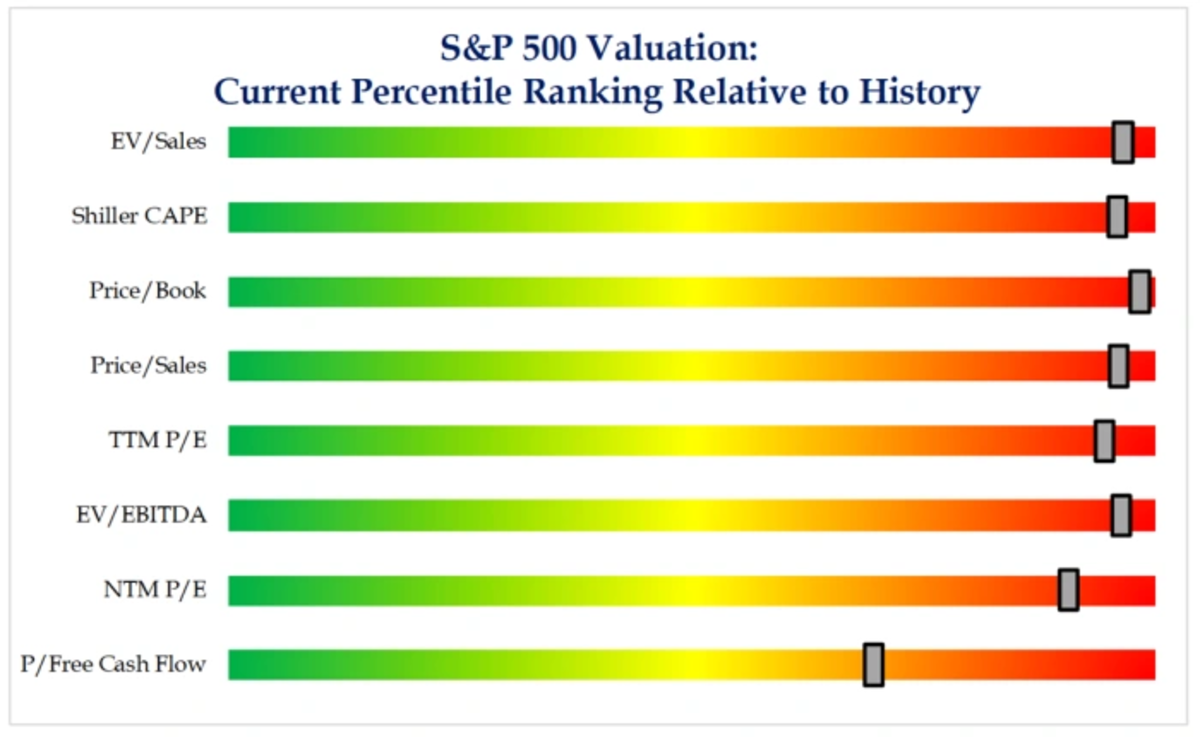

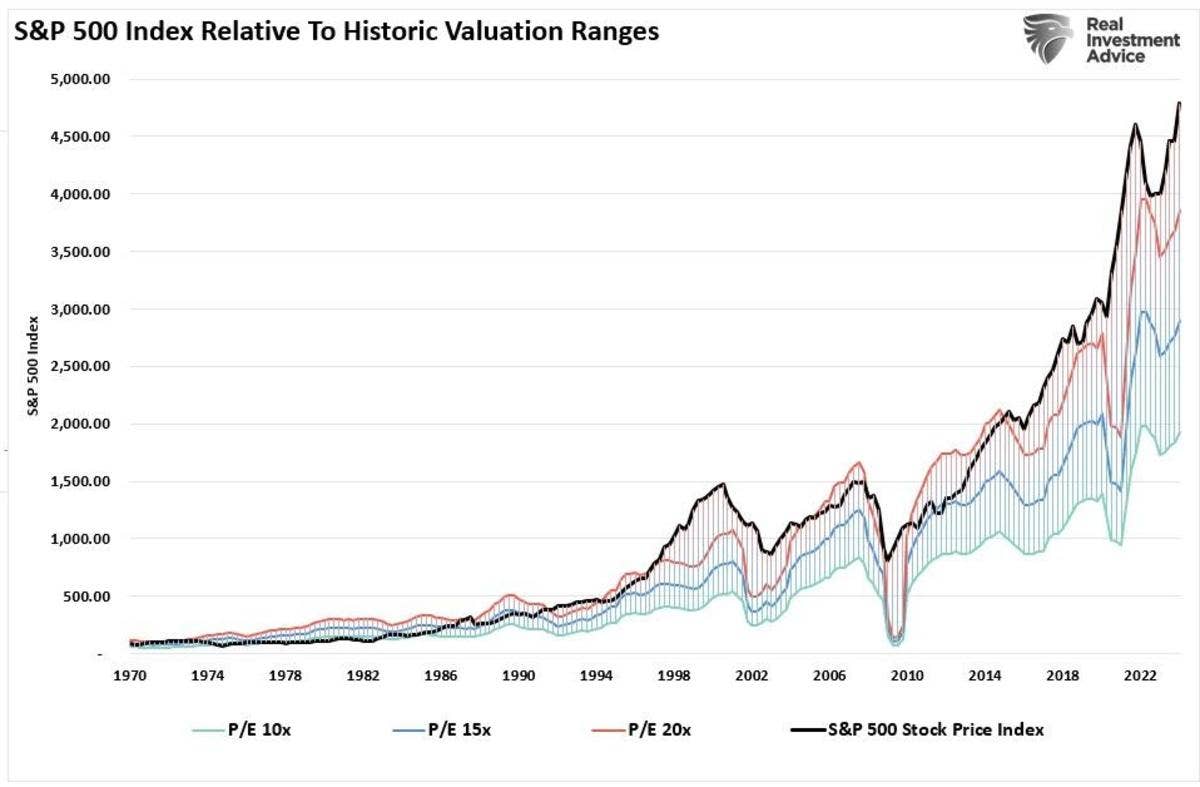

Importantly a too-optimistic consensus profits outlook comes at a time in which stocks are overvalued. Most traditional valuation metrics are in the 90%+ tile:

Why Are Strategists So Optimistic Given the Backdrop of Interest Rates and Inflation?

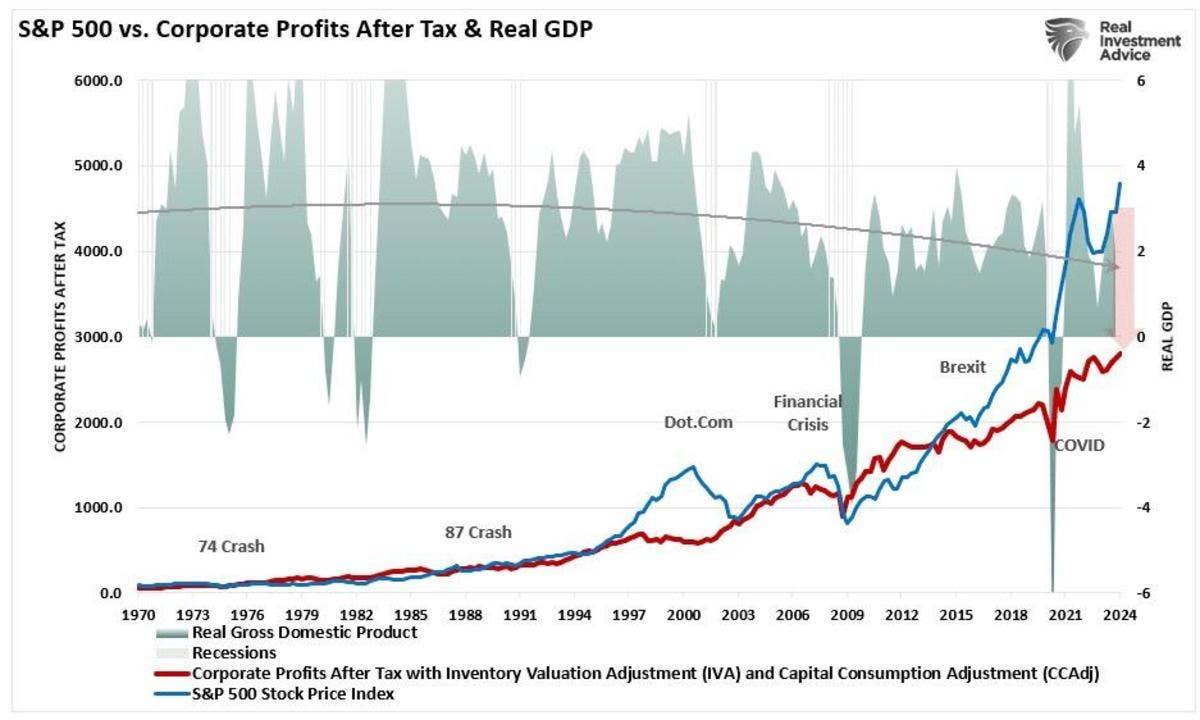

Equity prices generally (and over long period of time) tend to track economic growth and earnings. Over the last 7-8 decades the economy has expanded by a 6.4% growth rate, EPS have compounded by 7.7% annually and stock prices have risen by 9.3%/year.

The chart below demonstrates how overvalued equities are relative to Real Domestic Product and after tax profits:

Most strategists are expecting about a 10% rise in S&P profits in 2024 and near 15% again next year.

How is this possible given the following backdrop?

* The economic bounce back from Covid is over. The rate of growth in U.S. GDP is likely moderating toward about +1.5% over the next few quarters.

* Inflation has dropped dramatically to around 2.5%-3.0%. With economic growth decelerating and inventories no longer scarce, companies have likely far less pricing power today than at any point in the last two to three years. The impact of "stacked" or cumulative inflation is already being felt on reported profits by a number of consumer-oriented companies like Home Depot HD, McDonald's MCD, Starbucks SBUX, Winnebago WGO and many others (some of which we are short!).

* Inflation remains prickly, which means the Fed will be less easy and stimulative. Expectations of six rate cuts (as recently as five months ago) has been reduced to one to two cuts for this year.

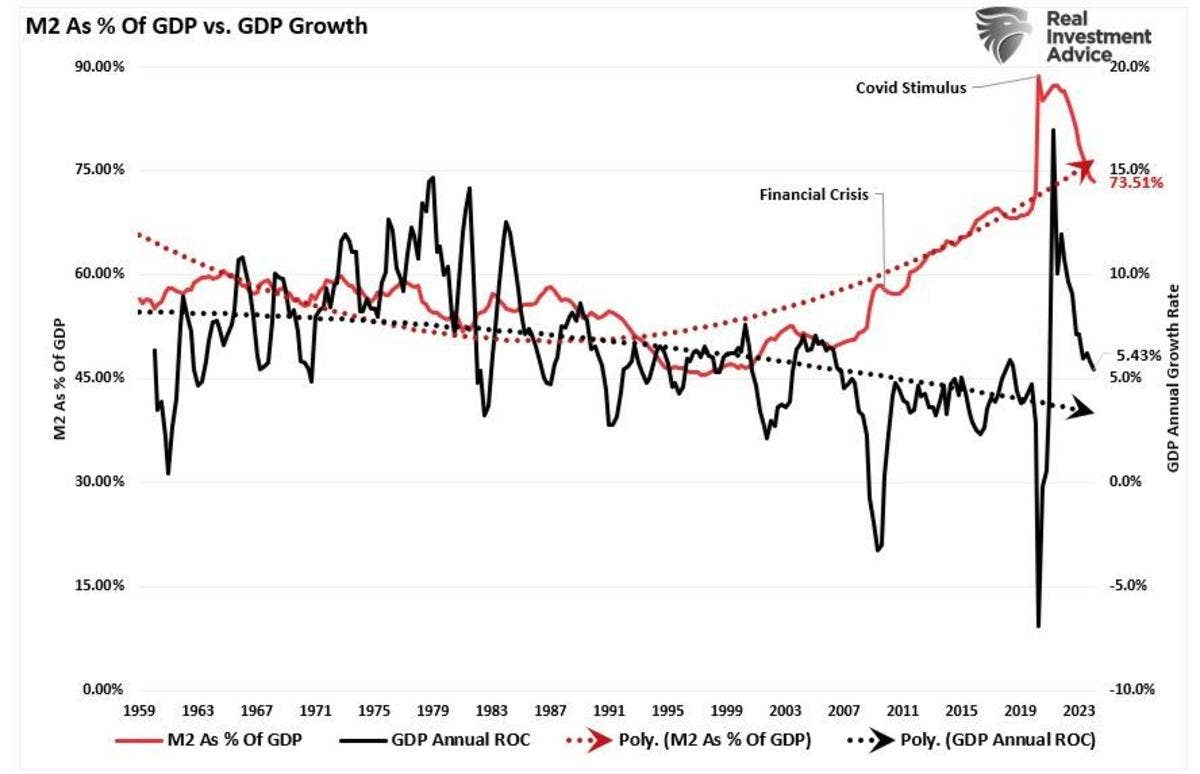

* The surge in liquidity/money supply is over:

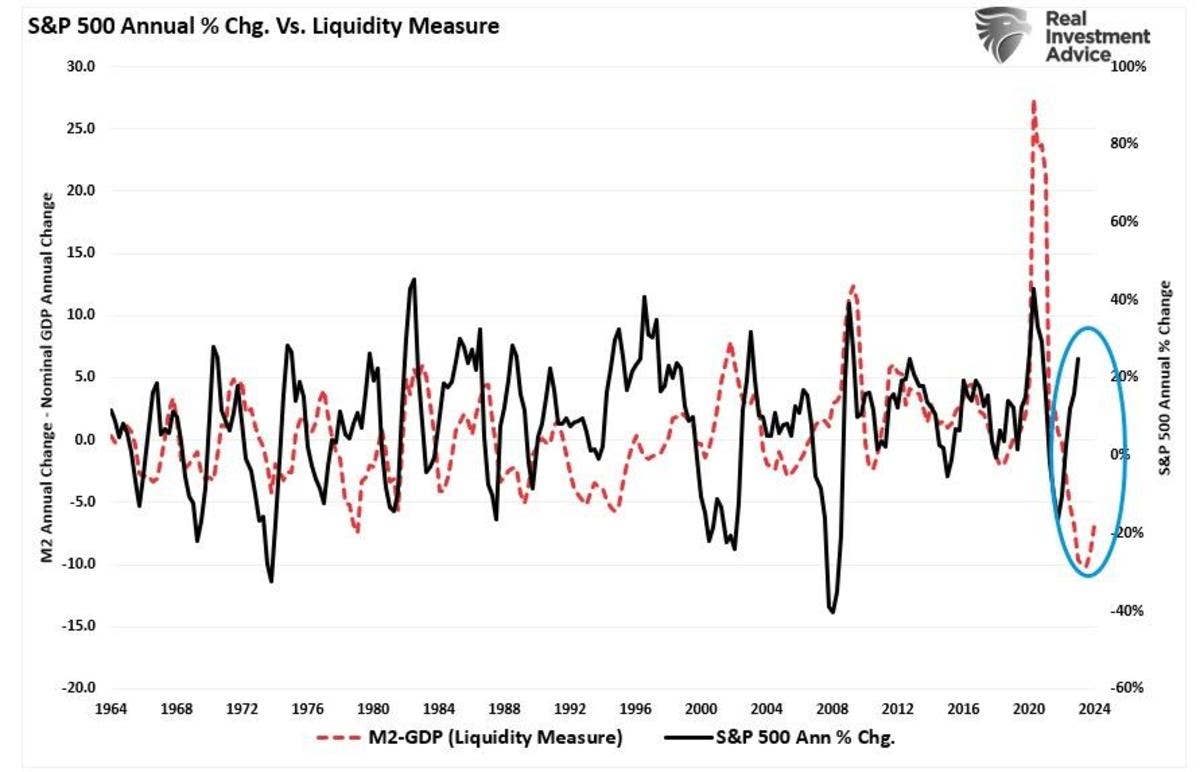

While the media often states that “stocks are not the economy,” as noted, economic activity creates corporate revenues and earnings. As such, stocks cannot grow faster than the economy over long periods. A decent correlation exists between the expansion and contraction of M2 less GDP growth (a measure of liquidity excess) and the annual rate of change in the S&P 500 index.

Currently, the deviation seems unsustainable. More notably, the current percentage annual change in the S&P 500 is approaching levels that have preceded a reversal of that growth rate:

So, either the annualized rate of return from the S&P 500 will decline due to repricing the market for lower-than-expected earnings growth rates, or the liquidity measure is about to turn sharply higher.

More TheStreet Pro:

- Investing Is a Marathon. Trading Is a Sprint.

- How the Darvas Box Method Can Help Today's Investors Stick With Winners

- Everything You Ever Wanted to Know About the CNN Fear & Greed Index

Other Issues

* Not only won't monetary policy stimulate much growth, but with fiscal policy out of hand, there is a limit to further expansion in fiscal stimulation. It is almost certain that fiscal outlays will not be as stimulative over the next 18 months as in the past several years.

* Though currently ignored by authorities and investors, the U.S. deficit and debt load are out of hand and must be addressed. Former President Trump's tax cuts expire next year. More tax cuts will be inflationary, lowering growth. Should the incumbent prevail, tax increases are likely — this will also dampen economic growth.

* Following the pandemic, consumption has been pulled forward. The consumer has reduced/eliminated excess savings and has taken on loads of debt — the consumer is now spent up not pent up. And, as mentioned previously, cumulative inflation is now taking its toll.

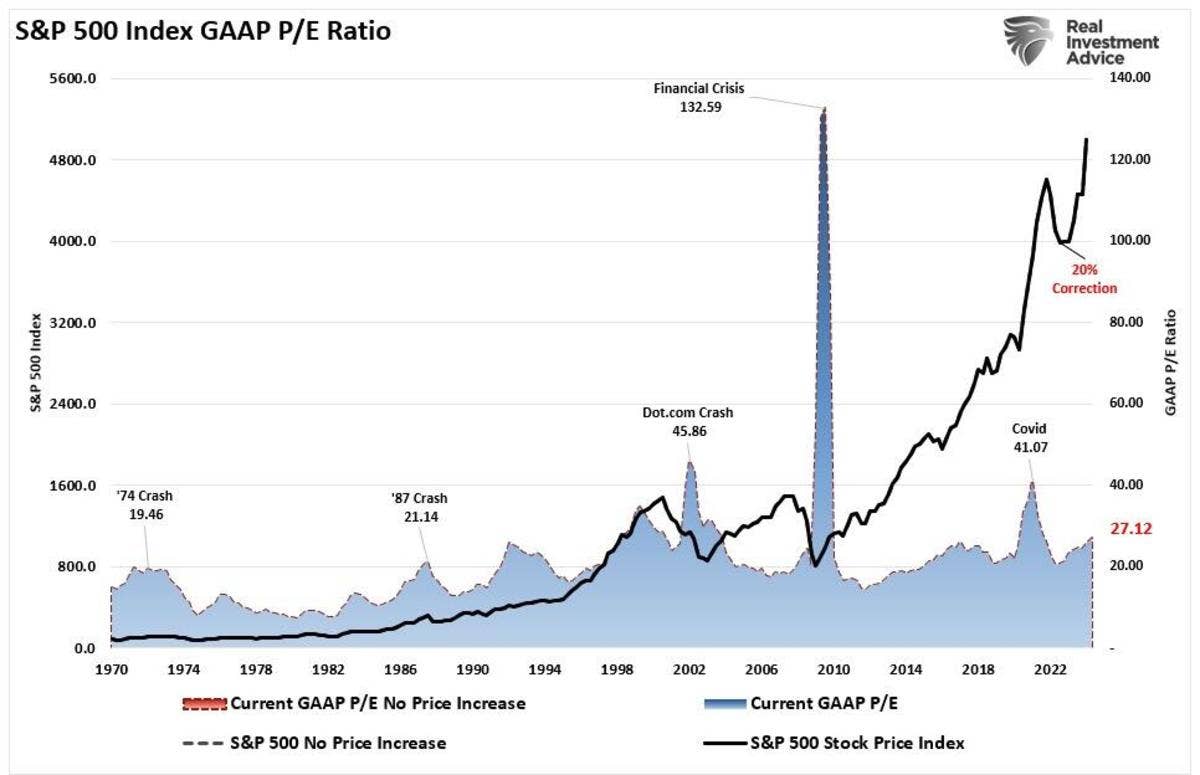

* The quality of earnings remains suspect. Most companies report “operating” earnings, which obfuscate profitability by excluding all the “bad stuff.” A significant divergence exists between operating (or adjusted) and GAAP earnings. When such a wide gap exists, investors should question the “quality” of those earnings:

The chart below uses GAAP earnings. If we assume current earnings are correct, then such leaves the market trading above 27-times earnings. (That valuation level remains near previous bull market peak valuations.)

Bottom Line

I remain a disciplined investor, selecting equities (long and short) through hard-hitting analysis, with a calculator in hand. I refuse to chase equities, particularly when valuations based on historical metrics, are at or above the 90%-tile.

I plan to continue to be patient in continuing to pursue a risk-averse strategy (concentrating on a conservative approach thru pairs investing) over the near term.

Importantly I fully recognize that wealth is generated by being long equities — but there is a time and place to be defensive. Large cash positions and/or shorting stocks protect wealth as most learned just two years ago.

The bottom line is that we are growing more confident that equities will finally fall back to an area that represents value — perhaps sooner than later.

Representative longs include Trulieve, Green Thumb Industries, Glass House Brands, St. Joe Company, Draftkings, Valvoline, Freshpet, Elanco Animal Health, Walt Disney and Procter & Gamble.

Representative shorts include McDonald’s, Medical Properties Trust, Winnebago, Sleep Number, B. Riley Financial, Freedom Holding Corp, Petco Health and Wellness, Warner Bros. Discovery, Chegg, FIGS, Walgreens, Boot Barn and Blackstone Mortgage Trust.