Buffett By the 'Book': Berkshire Hathaway Is No Bargain

The Oracle of Omaha has always advised valuing Berkshire in terms of book value rather than reported earnings. Here's what our analysis reveals.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

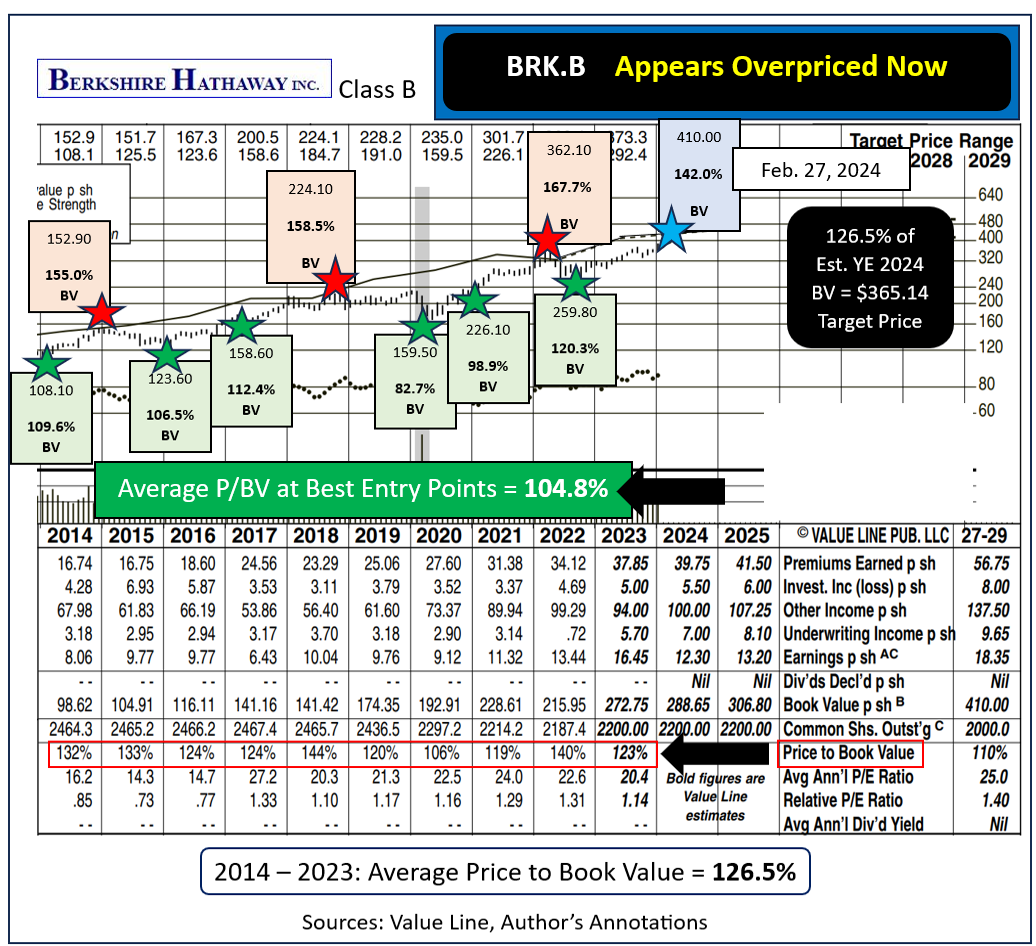

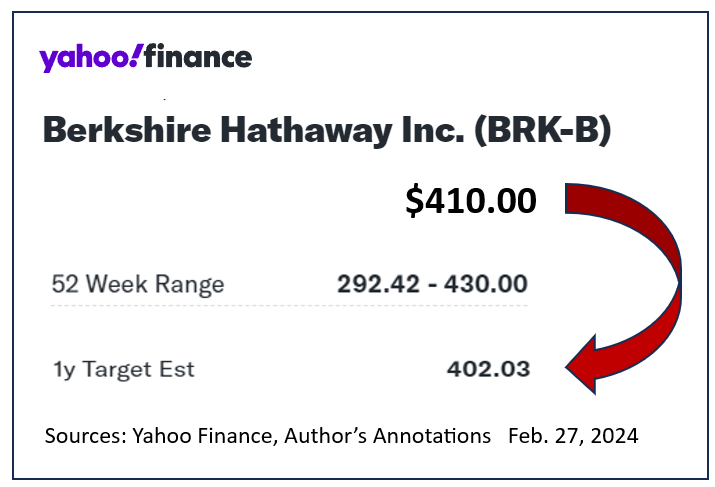

Berkshire Hathaway BRK.ABRK.B reported end-of-2023 results last Saturday. The class B shares shot up briefly to an all-time high of $430 before easing back to about $410 on the morning of February 27, 2024.

Should investors be chasing momentum here?

All data and past trading history is shouting "No."

Warren Buffett has always advised valuing the stock in terms of its book value rather than reported earnings. That is because earnings per share vary widely based on both market sentiment, which influences its portfolio value, as well as insurance claims, which often swing sharply depending on disasters insured or calm years for losses.

Buffett's old rule of thumb was to only have the firm buy back shares when the price-to-book value ratio (P/BV) was under 120%. Recently, though, he has been violating that parameter. Berkshire retired approximately $2.2 billion of its own shares in Q4 2023 when the P/BV was well above 120%.

Each share bought back at above book value is dilutive to the book value on all remaining shares.

Berkshire's price to year-end book value has varied from as low as 82.7% during the Covid crisis, to 167.7% of BV early in 2022.

Crunching the numbers over the past decade shows Berkshire's average P/BV was 126.5%. The best six entry points (green-starred below) saw BRK.B at less than a 5% premium to projected year-end BV. Buying Berkshire Hathaway near one-time forward book value has always been a smart move.

The three previous "should have sold" moments for BRK.B (red-starred) averaged 160.4% of projected year-end BV. The December 2014 peak led to a 12-month, 21.7% decline. The fall of 2018 top preceded a 28.8%, 16-month selloff. The March 2022 peak of $362.10 led to a six-month, 28.3% decline.

Buying above 150% of forward BV has always meant "dead money" at best for the stock's foreseeable year ahead.

Berkshire Hathaway has never paid cash dividends. Avoiding predictable large declines like those three allowed for better employment of cash and the ability to buy back later at significantly cheaper prices.

Who would not have sold if they knew for sure, or highly suspected, that the shares were set up for bad news?

At the recent all-time high BRK.B was selling for 149% of Value Line's Dec. 31, 2024 estimated book value.

I am not alone is calling Berkshire's current price unattractive.

Yahoo Finance sees $402.03 as their 12-month target price on the class B shares. Even that appears to be somewhat optimistic. It represents greater than 139% of expected Dec. 31, 2024 book value.

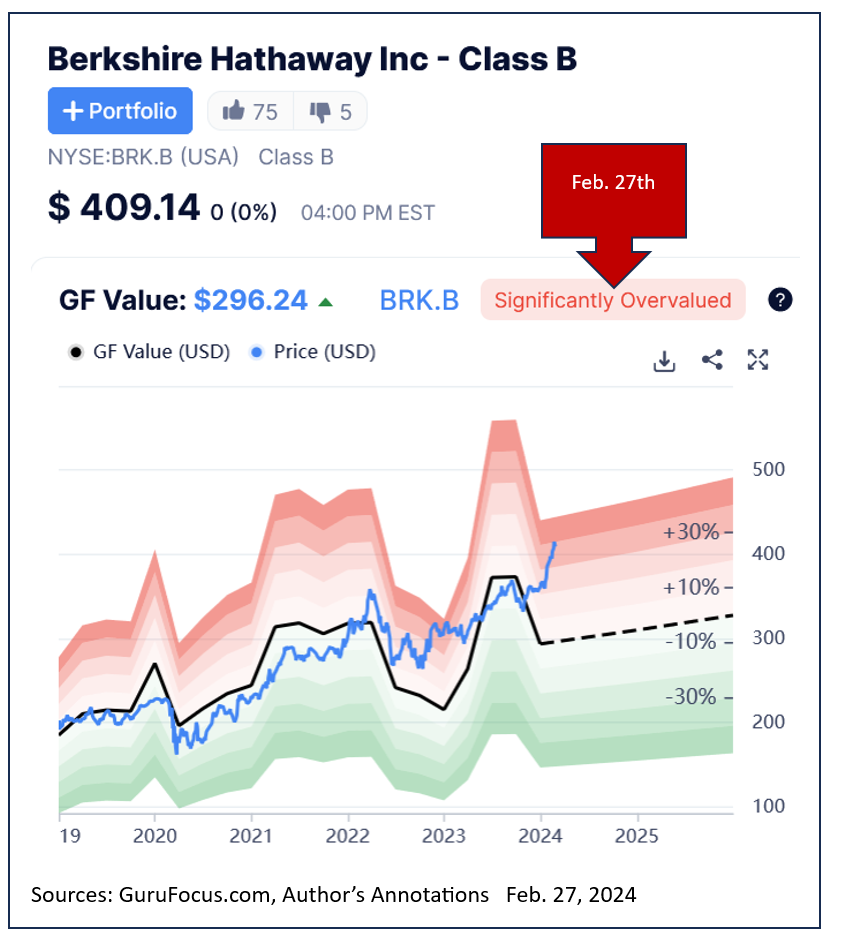

Research from GuruFocus, conversely sees present-day fair value for BRK.B as just $296.24 per share.

That number seems too low as it implies just 102.6% of projected year-end BV. I agree that Berkshire class B is overpriced but see about $347 as a more reasonable present-day valuation based on 126.5% of today's book value.

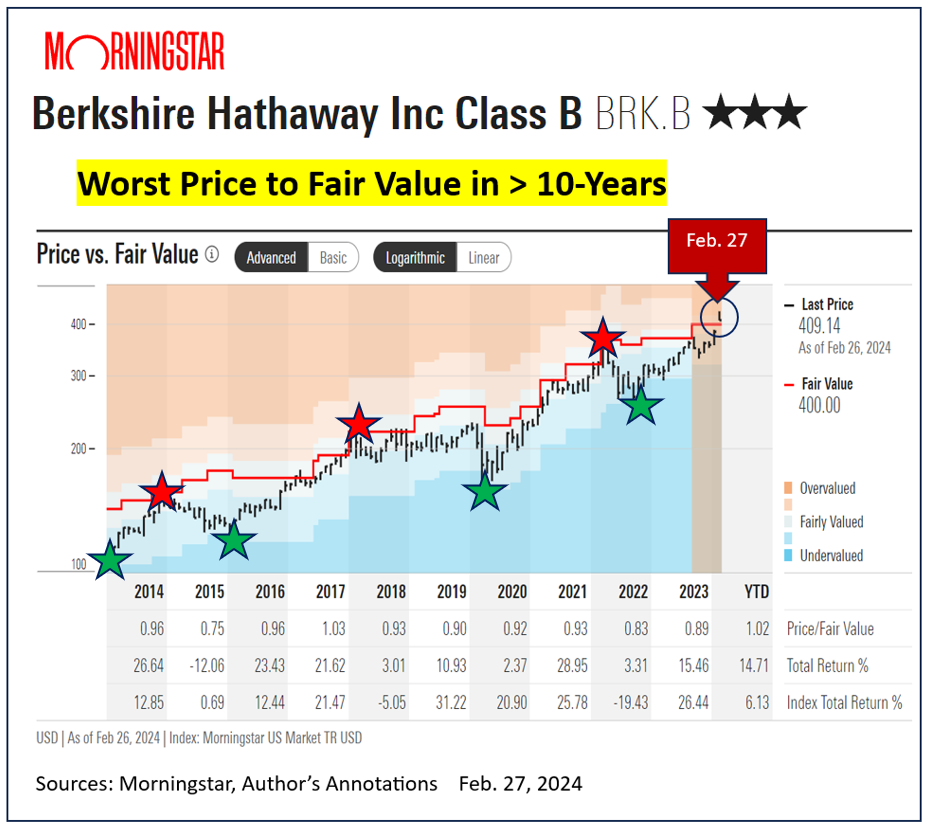

Independent opinion from Morningstar calls BRK.B's present-day fair value as $400 on the nose.

Its estimated price-to-fair value graph shows BRK.B has never been pricier over the previous decade. Why then, do they rate it as 3-star, neutral, HOLD?

There is no doubt that Berkshire Hathaway is a fine company which should continue to prosper under Warren Buffett and beyond. But no matter which opinion you think is most accurate, there is little to no chance of making significant gains from owning the stock over the coming year.

Berkshire's huge, and growing cash hoard was a drag on performance since the Covid panic period. If Buffett believes the market offers little value right now its own portfolio of stocks is unlikely to do well going forward. If he continues to be wrong on that view he would admit that he should have been putting that enormous cash pile to work years ago when almost everything was much cheaper, including Berkshire's own shares which were available around $160 during March 2020.

If you own Berkshire Hathaway A or B consider selling into strength. If you were thinking about buying on the pullback from $430, think again.

At the time of publication, Price had no positions in any class of Berkshire Hathaway and no option exposure to Berkshire Hathaway.