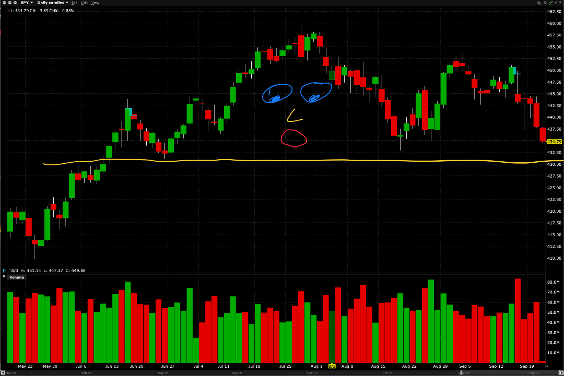

Chart of the Day Part: Small Caps, Big Trouble

Small caps now down on the year:

BY Doug Kass · Sep 21, 2023, 5:40 PM EDT

Small caps now down on the year:

BY Doug Kass · Sep 21, 2023, 5:40 PM EDT

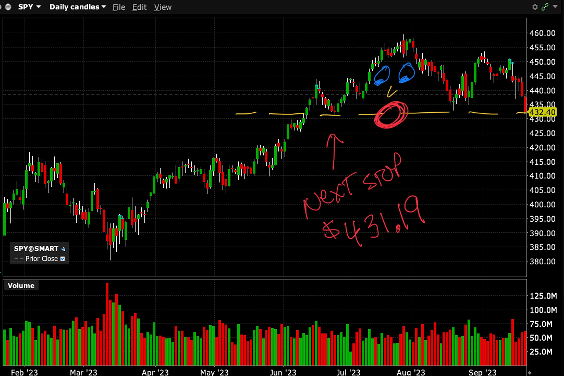

* For a head-and-shoulders top....

* Hat tip to Eigen Man!

BY Doug Kass · Sep 21, 2023, 3:57 PM EDT

I have covered my Apple AAPL short.

BY Doug Kass · Sep 21, 2023, 3:28 PM EDT

The housing markets have begun a fall:

And Wolf Street howls about the very subject: "Demand for Existing Homes Falters Further. Price Cuts, Days on Market, New Listings Rise. Prices Languish below 2022 Peak"

BY Doug Kass · Sep 21, 2023, 3:27 PM EDT

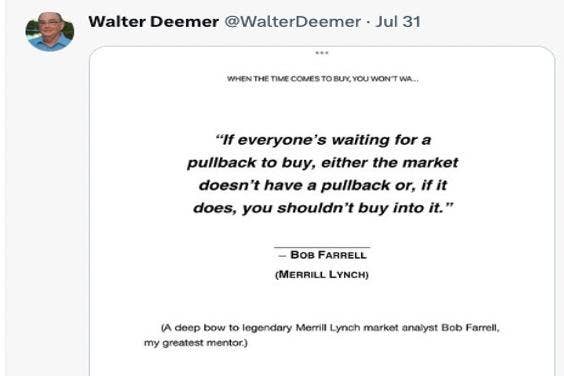

* or maybe the year... which includes comments from Wally Deemer and Bob Farrell:

1. I still have the below tweet from Walter pinned up from 7/31 that I think is in effect.

2. Dougie seeing Head & Shoulders on SPY and based on his friend Abie analysis of lower highs and lower lows playing out we could breach Aug low soon.

3. Carter yesterday points to Unfilled gaps with $SPX at 4231 which is also 9% decline from the July highs which he noted earlier in one of the risk reversal episodes as typical corrections for SPY within the uptrend from Oct'22.

4. TechNova indicated without an Event he sees VIX resistance at 19 and also had indicated before that $SPX is still in uptrend and while he thinks we get a visit towards $4200 while still maintaining the uptrend.

5. S&P Oscillator still not deeply oversold.

6. Helene not seeing the true whoosh lower which are typically seen with oversold conditions and believes complacency is still out there.

7. Tier1 Alpha dealers continue selling into weakness as Gamma is negative.

8. Sell Rosh Hashanah and Buy Yom Kippur still in play.

9. Negative Sep Seasonality has been self-fulfilling.

10. Dave Jerbos on CNBC yesterday talks about M2 supply and ample Liquidity still in the system from 2020 QE and Stimulus which he believes is far more effective than Fed hikes and could still propel SPYs higher after this correction. We will just have to see where we end up won't we.

BY Doug Kass · Sep 21, 2023, 3:22 PM EDT

From my bestie, Tony "Dwyerama" Dwyer:

The zombie is chasing Goldilocks

Regardless of today's Fed decision, Jerome Powell is likely to suggest rates are going to remain higher for longer due to the resilience of the consumer and full employment backdrop ("Goldilocks"). We have long said that a perceived soft landing now driven by lower inflation and full employment may be the worst-case scenario because it reinforces the Fed's idea of "higher for longer" in a generationally levered system. In our view, this monetary backdrop creates a zombie economy by not allowing for an improved outlook for money via the stimulative effect of lower rates. Indeed, it has become very popular to envision the 1995 "Goldilocks" environment as a similar period, but we now have a very different backdrop than in 1995.

In this short video we highlight the differences:

1. Inflation was in secular decline while today it remains stubbornly high.

2. U.S. Treasury, corporate, and mortgage interest rates were moving sharply lower rather than today's cycle high.

3. Unemployment was declining and not close to full employment, while today the opposite is true.

Summary - Higher for longer keeps the zombie alive and chasing Goldilocks. We are in a seasonally weak period for equities, our tactical indicators are still neutral, our core fundamental thesis remains on recession watch, and we are fast approaching earnings season. We simply don't feel the need to jump into this guessing game and would stay "light and tight" until there is either a more severe oversold condition or significant clarity in the macro backdrop and outlook for money, especially with the risk-free rate on the 6-month U.S. Treasury Bill Yield of 5.53% roughly equivalent to the SPX Earnings Yield of 5.4% using the current 2024 Refinitiv consensus estimate of $247/share. When driving on a muddy road, we still don't want to jerk the wheel.

BY Doug Kass · Sep 21, 2023, 3:06 PM EDT

BY Doug Kass · Sep 21, 2023, 2:48 PM EDT

Here is a realistic analysis (that explains the bill's challenges -- some of which I discussed in my previous analysis) of The SAFER Act, by Cowen:

BY Doug Kass · Sep 21, 2023, 2:39 PM EDT

I speak to Jason often and TerrAscend TSNDF is the only cannabis stock I am buying:

Randy36 minutes ago edited

This is like every day lately

Form 4 TerrAscend Corp. For: Sep 20 Filed by: Wild Jason G.

http://archive.fast-edgar.c...

Filed on: September 21, 2023

Executive Chairman

Common Shares 09/20/2023 P shares 27,450 price $ 2.0118 total owned 90,187,476

BY Doug Kass · Sep 21, 2023, 2:23 PM EDT

Out of all of my short SPY calls now.

BY Doug Kass · Sep 21, 2023, 1:30 PM EDT

I just covered my UPS trading short for a gain and shorted moreFDX (still small, though).

BY Doug Kass · Sep 21, 2023, 1:05 PM EDT

As you all know about 10% of my investing/trading process is technical.

I use basic stuff like support and resistance lines to help me time purchases/sales/short.

And gaps:

So close to filling the gap. 20 cents more. I may be interested now.

BY Doug Kass · Sep 21, 2023, 1:03 PM EDT

I am placing JOE on my "Best Ideas" List now.

BY Doug Kass · Sep 21, 2023, 12:41 PM EDT

* As I have been suggesting over the last two months....

Sourece: Hedgeye

BY Doug Kass · Sep 21, 2023, 12:00 PM EDT

First buy of the day - JOE at $55.45.

BY Doug Kass · Sep 21, 2023, 11:56 AM EDT

I have covered the following shorts on the gaps lower and at excellent prices this morning: TOL , DHI , BX , ABNB , BRKB , TSLA .

I have not yet made any long purchases.

Please note that I still have many investment shorts in our portfolio (over 20 remaining) - but the stocks that I covered this morning were considered more trading sardines (and short term trading rentals).

BY Doug Kass · Sep 21, 2023, 11:30 AM EDT

Break in:

Microsoft MSFT to roll out AI Copilot on Sept 26 on Windows. The shares are flying higher.

In Comments Section this morning I highlighted that this could happen:

Probably nothing.

But watch MSFT at around 1PM.

Intel has alluded to copilot project.

If MSFT's progress on copilot accelerated and revealed at their analyst meeting - MSFT could skyrocket, helping the markets.

I have no edge here, but pay attention.

Dougie

BY Doug Kass · Sep 21, 2023, 10:29 AM EDT

* Caution and stock market congestion may lie ahead...as interest rates stay higher for longer

* The stock market decline has now assumed a global character

* More lessons from Howard Marks

"Risk control is still number one at Oaktree. Seventy-plus years ago, UCLA football coach Henry Russell "Red" Sanders said, "Winning isn't everything, it's the only thing." (The saying is also attributed to Vince Lombardi, legendary football coach of the Green Bay Packers.) While I haven't figured out exactly what that phrase means, I'm firmly convinced that for Oaktree, risk control isn't everything; it is the only thing."

-- Howard Marks, Fewer Losers, or More Winners?

A tentative Fed Chair has admitted to the uncertainties that I have highlighted repeatedly in my Diary over the last few months.

It may no longer matter what a feckless and fatuous Fed's near-term interest rate (policy) intention is -- as bond market participants are doing their own tightening, with the yield on the 10-Year Treasury +43 basis points and the yield on the 30-Year Treasury +49 basis points since the July FOMC meeting.

Stated simply, the breakout in the real yield (late yesterday and today) is market unfriendly. And the prospects for this condition to continue well into 2024 could be even more challenging to equities.

Assessing the equity risk premium (which, to me, is the foundation of assessing value), with the S&P earnings yield (inverse of the P/E) likely to decline and the risk-free rate of return rising (and staying higher for longer), the odds that we have seen a peak in the S&P Index (which I had at 75%) is increasing.

As I have also repeatedly written, short-dated Treasuries provide equity-like returns with limited risk and volatility in these uncertain times. (That uncertainty was admitted to by Chair Powell yesterday afternoon -- but we already know that their forecasts have been wrong footed for several years and that the only certainty is the lack of certainty).

We are moving rapidly into a period of slugflation (sluggish economic growth and prickly inflation) unfriendly to our markets.

What was essential for money managers to own in the last few years -- an arguably over-owned FAANG + M -- may not thrive in a "higher for longer" interest-rate backdrop.

Non-rigorous equity selection without a serious investment process will now become more costly without "the wind of a bull market at our backs" -- and investors better understand what they own and why. Importantly, our calculator (and process) becomes more valuable in answering what the likely reward vs. risk ratio is.

Like the $100k forecasts for bitcoin, the many confident forecasts of imminent new highs in the S&P Index will likely fade away.

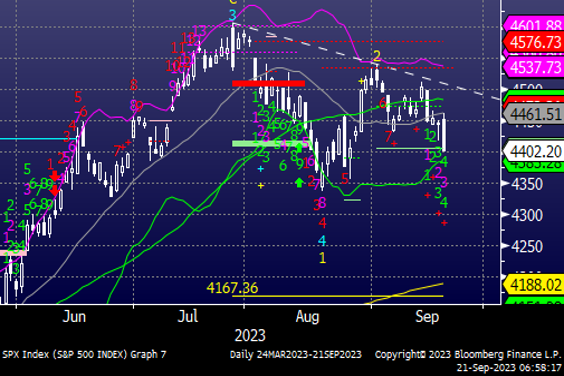

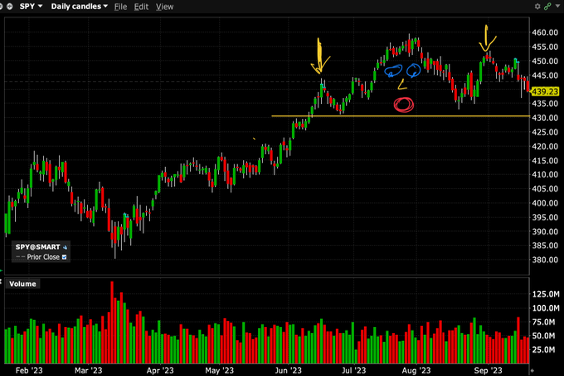

Technically, as previously mentioned I see rollovers and breakdowns everywhere -- with a clear pattern of a head-and-shoulder top in the senior averages -- the S&P Index:

This is all about to get real.

----------------

I started today's opening missive with a quote from my pal, Oaktree's Howard Marks.

As it relates to today's theme of balancing reward against risk, I also want to end my opener with some more important lessons from Howard:

One of my favorite quotes is attributed to Albert Einstein and Yogi Berra, among others: "In theory, there is no difference between theory and practice. In practice, there is." If markets are efficient and securities are always priced correctly, there can be no value in active investing. The truth is that many active managers, especially in developed market equities, have failed to demonstrate the ability to add value, or to add enough value to justify their management fees. This is largely why index funds were created and why a significant amount of equity capital has migrated to index and passive investing in recent decades.

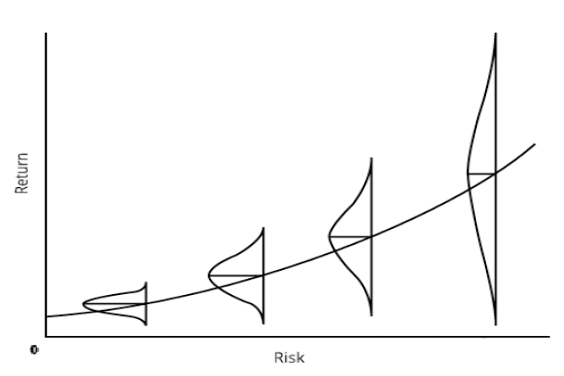

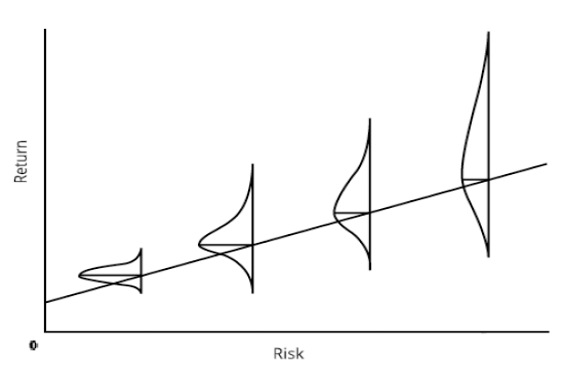

And yet, I firmly believe there are times when the markets are overpriced and times when they're underpriced. There are also times when particular markets or sectors are overpriced or underpriced relative to others. In these instances, some securities can be priced too high or too low, and thus some positions on the risk curve can offer better bargains than others.

The theory assumes investors are rational and objective, but psychological excesses violate that assumption. Take, for example, the investment environment during the Global Financial Crisis. As I described in my July memo Taking the Temperature, in late 2008, investors were so worried about a financial sector meltdown that they panicked and sold securities aggressively as their prices collapsed. Excessive risk aversion causes the risk/return line to steepen (increasing the return for each incremental unit of risk borne) and perhaps even to curve upward (rendering the compensation for making investments at the risky end of the spectrum disproportionately generous). Thus, in periods of excessive risk aversion, the riskier part of the curve can be the smarter place to be (and in periods when risk bearing is too eagerly embraced, the safer part can offer a superior proposition).

View Chart »View in New Window »

The last element I want to touch on is what I call "alpha," or individual investing skill. The reason the EMH disdains efforts to beat the market is its conviction that since securities are always priced correctly, the ability to identify bargains to buy and over-pricings to avoid can't exist. Theory's assertion that there's no such thing as mastery of markets implies that no one has the skill to assemble portfolios that outperform. This is why I depict the bell-shaped curves above as symmetrical: In an efficient market, investors can only take what the market gives them.

But I'm convinced the potential to improve on that through skill does exist in some markets and some people. Investors who possess alpha have the ability to alter the shape of the distributions in the graphs above so that they're not symmetrical, in that the portion of the distribution representing the less desirable outcomes is smaller than the portion representing the better ones. In fact, that's what alpha really means: Investors with alpha can go into a market and, by applying their skill, access the upside potential offered in that market without taking on all the downside risk. In my memo What Really Matters? (November 2022), I said the key characteristic of superior investing is asymmetry - having more upside than downside. Alpha enables exceptional investors to modify the probability distributions such that they are biased toward the positive, resulting in superior risk-adjusted returns.

View Chart »View in New Window »

If alpha is the ability to earn return without taking fully commensurate risk, investors possessing it can do so by either reducing risk while giving up less return or by increasing potential return with a less-than-commensurate increase in risk. In other words, skill can enable some investors to outperform by emphasizing aggressiveness and some by emphasizing defensiveness. The choice between these approaches depends on the type of alpha an investor possesses: Is it the ability to produce stunning returns with tolerable risk, or the ability to produce good returns with minimal risk? Almost no investors possess both forms of alpha, and most possess neither. Investors who lack alpha shouldn't expect to be able to produce either version of asymmetry - that is, to be able to generate superior risk-adjusted returns. However, most believe they do have it.

The proper choice between the two approaches - fewer losers or more winners - depends on each investor's skill, return aspiration, and risk tolerance. As with many of the things I discuss, there's no right answer here. Just a choice.

BY Doug Kass · Sep 21, 2023, 10:18 AM EDT

Now out of these shorts: TSLAABNB and BRK.B

Dougie

BY Doug Kass · Sep 21, 2023, 10:02 AM EDT

From Art Cashin:

By the end of Wednesday's trading day, many equity traders could probably mistake Jay Powell, Chairman of the Fed with one of the Duryea Brothers. You know - expecting to hear from a bright inventive guy with some creative ideas talk about something that many people had thought was going to be positive and by the end of it, they were at the point of fully rethinking where things were going and was the device or at least direction moving in the wrong order. When Powell began to speak at 2:30 p.m., equity prices were solid, by the time he was finished, they were headed to the lows of the day and managed to move even lower and closing pretty much on the bottom and sending yields off in a confusing pattern, but of course, the Fed Chair would disagree with that assessment, but then again, probably so would one of the Duryea Brothers. The equity day started out reasonably well for the stock market and things moved along. Not anywhere near a super rally or a run for the roses, but a quiet, solid performance and some occasional re-think of the relationship between bond yields, particularly the yield on the ten-year treasury and equity prices. A matter we had discussed several times over the last couple of days and saying its validity may come into question on a Fed decision day and, boy did it ever. We started out okay and it looked like the bulls were going to move along and at least solidify their position, if not manage to move ahead, but we started to see some shifting in those ten-year bond yields and we had mentioned that in the pre-opening commentary and saw fit to come back and revisit it in this late morning update:

Late Morning Update 09.20.23 Yields tick down off the morning highs and stocks go up. That sounds like a pretty familiar theme, however, today that may be as much coincidental as it may be causative and again, I think, that probably is because it is the FOMC announcement day. As I had suggested in the pre-opening commentary, traders were marginally deemphasizing yields and, once again, they touched on the high end of the testing range and pulled back. So, they are becoming a bit of a recently familiar reflex. The market will continue to double check itself. Yields will matter but the bulls will have to be a bit more dramatic to get the full attention of the equity crowd. Again, do not dismiss the Fed Drift, which is the tendency for equities to drift higher in the 24-hours before the Fed announcement. On a day like today, it is probably somewhat foolish to try to be too predictive of where things may go, and it is all about the Fed and what comes out. Again, we believe the dot plot will be the absolute high point, barring the fact that if Powell goes off on a diversion of some kind. So, watch the yields, but only react if the movements are a bit more dramatic than those we have seen so far. In the meantime, stay safe and see you at 2:45 p.m. The movement in the yields and their relationship to stocks were tried again and again throughout the day and waxed and waned even when the Fed Chair spoke.

As I said earlier, the stock market was reasonably solid when Powell came to the podium at 2:30 and, by the time he had finished, stocks were in tatters and were coming apart only to wind up closing pretty much at the lows of the day. Of further import was that late in the day, as things were moving around after people were assessing what Powell's intent was in some of things he said, the yield on the ten year wound up snapping smartly higher with the yield on the ten-year touching and virtually closing at a relative new high, which takes it through the upside of the testing area and, more importantly, takes it through there for a closing print. Technically, that would have rather strong implications and it might mean a breakout to the upside and all of that may have been mitigated by the Fed day as we said, but we will have to get out our slide rule and protractor and see if the push through was enough of a test as to strongly hint a breakout to the upside, which insightful professionals like the great Katie Stockton have said that an upside breakout in those yields could take the next higher upside target up into the 5% range, which is clearly something the stock market is not ready for. So, we will take all that with a grain of salt you can carry around in a wheelbarrow and try to review with bond professionals like Rick Santelli and others how much that high close meant on a technical basis. In the meantime, as is customary, we should now look and see what our cousins offshore did in reaction to the New York action and the Powell press conference and what they hear and think about central banks in their own area. Overnight, global equity markets are positively reeling in response to the reaction to the U.S. markets to the FOMC press conference. In Asia, Japan closed down the equivalent of 500 points in the Dow. Hong Kong was off about 450 points. Mainland China was relatively quiet, down only about 280 Dow points. India had a somewhat similar performance. In Europe, as we go to press, London is down about 170 Dow points, but Paris is off close to 420 Dow points. Frankfurt is down a little bit less.

In the pre-dawn hours, I sent an email to my friend, the exceedingly thorough, Becky Quick, noting that several of the TV pundits were doing gymnastic turns in trying to pull out the nuances in the Fed statement that caused the market reactions. I noted to Becky what floor traders were talking about at their respective watering holes and that was that in response to the prepared statements, both the official one from the FOMC and Powell's own prepared statements, equity markets were neutral to actually rallying slightly and, it was only when we got into the randomness of the Q&A that equity prices turned lower and then sharply lower. So, it was hardly some linguistic nuance, in which, the Fed modified a modifier. It was more the fact that Powell basically admitted the Fed still had some difficulty with controlling things and that they might, in fact, have to tighten further and continue the Quantitative Tightening longer than many had thought. As I say, self-style pundits will look for gems where there is nothing but ordinary rocks. The post-FOMC calendar is reasonably moderate. It being Thursday, we will get Initial Jobless Claims and then also pre-opening, the Philly Fed Index and the Current Account data. At midmorning, we get Existing Home Sales and Leading Indicators and the Natural Gas Inventories. After the close, everybody will rush to look at the Fed Balance Sheet and see how Quantitative Tightening is going and how much tightening we are actually seeing.

Those who wonder why I keep repeating that the Stock Traders Almanac is so valuable are reminded of this quote from it by Jeff Hirsch, which we cited earlier in the week: September quarterly options expiration treacherous, week after awful. SP500 down 10 of last 11 September quarterly OPEX Fridays and down 26 of last 33 weeks after. Some of the swings in bond trading on the FOMC day brought even further attention to some of the inverted yield curves that I have been talking about for weeks, and weeks, and weeks. They may be hinting a bit more strongly that a possible recession could be within sight. We will need to get our abacus re-strung and maybe dig into that next week. In the meantime, you know the current drill.

With all the geopolitical nuances, stay close to the newsticker. Keep your seatbelt fastened. Stay nimble and alert. Keep your eye on those yields. If they stay at, or more importantly, push higher than Wednesday's relative high closing level, watch carefully to see how the market reacts. They will not have Fed Day as an excuse. Stay safe.

BY Doug Kass · Sep 21, 2023, 9:54 AM EDT

From Peter Boockvar:

Market rates are tightening policy further

So when you hear the concept of r* further debated and where the Fed is targeting the fed funds rate relative to inflation, this is how Jay Powell defined it yesterday, "You only know when you get there." And as to when monetary policy is restrictive, "you know you're overly restrictive only when you see it."

I will say this about the prospect of another Fed rate hike, all of a sudden the long end of the yield curve is doing it for them and by almost 50 bps since the July FOMC meeting. The 10 yr yield as risen now by 43 bps since that July get together.

The Fed pause was followed by an unexpected Swiss National Bank pause. They were expected to hike by 25 bps by kept rates unchanged at 1.75%. Remember they started hiking from a level of -.75% so in their eyes they've done a lot already, amazingly. Governor Jordan in fact called the tightening so far as "significant" but left door open for more. He said "The significant tightening of our monetary policy over recent quarters is countering remaining inflationary pressure. It cannot be ruled out that a further tightening of monetary policy may become necessary."

The Bank of England took the less than expected CPI seen this week and got them to do nothing today too, leaving rates at 5.25% but they are increasing the pace of QT to 100b pounds over the next 12 months vs their previous pace of 80b pounds. The vote was tight as it was 5-4 with the 4 wanting to hike by 25 bps. As the Fed did, they left open the possibility of another hike and higher for longer either way. "Monetary policy will need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with the Committee's remit. Further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures."

The Bank of Indonesia, the Taiwanese central bank and the one in the Philippines also all left rates unchanged as expected.

In contrast, the Swedish Riksbank and the Norges Bank in Norway both increased rates by 25 bps as expected. The Riksbank said "inflationary pressures in the Sweden economy are still too high" but "Inflation is also falling in Sweden. The rate of increase in energy and food prices has slowed significantly." They also are not happy with the weakness in the Swedish Krona. As for what comes next, "To ensure that inflation continues downwards and stabilizes around the target within a reasonable period of time, monetary policy needs to be tightened further."

The Norges bank said to both expect another in December and higher for longer as the Governor said "There will likely be one additional policy rate hike, most probably in December. There will likely be a need to maintain a tight stance for some time ahead."

This global move higher in rates comes with a global debt level of $307 trillion according to the Institute of International Finance which updated this figure on Tuesday as of June 30th. As a percent of global GDP it's 336%, up from 334% at yr end 2022 but down from 360% during Covid. This debt includes governments, businesses and households. Bottom line, we're talking about an extraordinary increase in the amount now being paid out in interest expense relative to where we were just a few years ago that will only grow as more and more debt matures in the coming years.

I heard the CFO of Bank of America yesterday at a conference say "It's difficult to see a US recession when the consumer is spending 4% more y/o/y." He apparently though is talking in nominal terms as that growth rate is mostly inflation.

Here are some key points FedEx (a stock we own) made in their call last night as they executed well in a tougher macro environment, "we really did feel good about how we executed within the quarter, but the macro did not help. As we're thinking about the domestic market specifically from a parcel perspective, if you look at calendar year '23, total volume for the whole year will be down .5%...That's a little bit lower than we anticipated the full year...Like I said, the market is not helping."

Some more, "when I look at the macro, a couple of things, trade is growing at 1.7%, that's down vs 2.2% the previous year. As we look at inventory, they're in a pretty good place from a retailer's perspective. I think the retailers have done a good job, they're not carrying a lot of extra inventory; wholesalers are. But the net takeaway is that inventory restocking is not going to help us."

These are some important comments from General Mills after earnings:

"In our North America Retail segment, we continued to see elevated retail sales growth for at-home food in the first quarter vs the pre-pandemic period, though the pace moderated from the double digit growth rates we saw in fiscal 2023, reflecting less impact from inflation driven pricing and a shift toward value for some consumers."

With regards to their pet food business, it "moderated in Q1 for some of the same reasons as human food: less of an impact from pricing, and increased value seeking behavior from consumers - or in this case, pet parents. With pet parents feeling increasingly uncertain about their economic outlook, we saw some shifting to more value oriented products and channels, as well as smaller pack sizes. In addition, with pet parents spending more time in the office or otherwise away from home, we're seeing incremental headwinds for the treats and wet food segments of the category."

KB Home is doing their part in filling the needed supply of new home inventory as seen in their earnings release. They said "Demand was healthy across our markets enabling us to raise prices in 65% of our communities while decreasing prices in only 10%. We offered mortgage concessions as we needed primarily in cases where the buyer did not qualify. Anecdotally, we hear from our teams in the field that buyers are compelled by the combination of the best price and value, not just the best interest rates which is aligned with our business model and our culture of selling built to order homes." As supply chains have improved, they can make a house in about 6 months vs the historical level of between 4 and 5 months.

In terms of cadence of business throughout the quarter, "Although interest rates rose as the quarter progressed our net orders remained fairly consistent month to month. The combination of an acute shortage of homes together with the demographic factors I just referenced (Millennials and Gen Z buyers) led to strong absorption and a cancellation rate that has returned to historical levels."

I'll say, with interest rates now approaching 7.75%, it will be really interesting to see how sustainable this demand will be. I question it.

Overseas, French business confidence in September was unchanged m/o/m but that was 2 pts better than expected and August was revised up by 1 pt.

Finally with stock market sentiment, Investors Intelligence said the mood is still pretty bullish but a bit less so. Bulls fell to 48.6 from 50.7 while Bears rose a touch to 22.8 from 22.5. AAII is not as much as Bulls fell by 3.1 pts to 31.3, the lowest since June 1st while Bears rose by 5.4 pts to above the level of Bulls at 34.6, a 5 week high. The CNN Fear/Greed index is still in Neutral territory at 47 vs 54 one week ago. Overall, a mixed bag of conviction.

BY Doug Kass · Sep 21, 2023, 9:36 AM EDT

Good stuff from Jefferies:

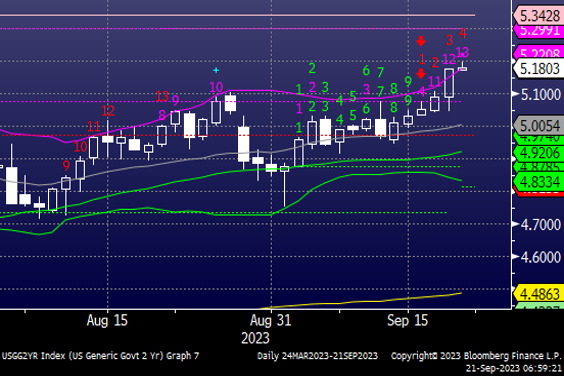

TECHNICALS & MARKETS...JEFFERIES Technicals & Markets...FED, S&P, US 2 Yr, DAX, HSI

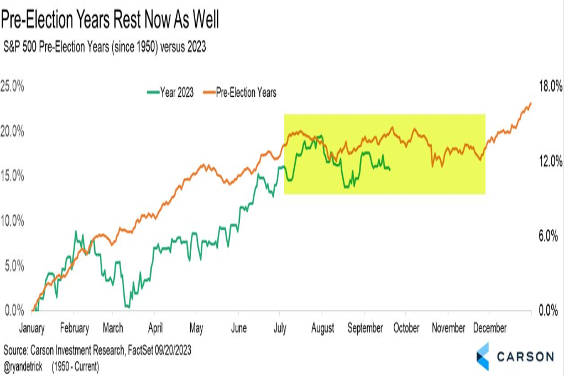

Our expectation for a dovish surprise from the FED yesterday did not even remotely come to fruition. The higher for Longer mantra and the substantially raised dot plots for 2024 were pretty much as hawkish as it gets, considering where we are in the cycle. Although we would have expected this to be priced in, markets still reacted pretty negatively to this hawkish message with stocks and bonds both selling off further. It is certainly not ideal and will increase the fear by a large margin, that the FED is on its path to break something and cause a volatility spike. But this further souring sentiment will also provide the background for a major recovery in Q4. Markets do need their Wall of Worries in order to recover, and that Wall has gotten quiet a bit bigger after yesterday's FED meeting. Eventually the FED will back pedal as they do pretty often. And it is also worth remembering, that many times the market reaction of the actual FED day gets reversed a few days later.

But it also shows us again how powerful seasonality is and that betting against it does not work very often. With that in mind, it is worth pointing out, that we are still in the middle of a very typical seasonal soft patch, that has historically always led to weeks and months of patchy and volatile trading. And whatever the current reasons are for that, we are still right in that period. The average chart pattern for the S&P of all the pre election years since 1950 shows pretty well, how markets still have to endure a period of uncertainty for a while. On top of that, the worst week of the year is doing its bit to get sentiment down again. Although we were hoping that the FED could break this historic pattern this year, it did not happen and we will have to continue to wait for some type of indication, that the seasonal low has been reached.

S&P...still in the typical seasonal soft patch

We have highlighted the fact for some time now, that the S&P still has uncompleted DeMark counts to the downside, that could potentially complete at some point and deliver a convincing Buy and entry level. There is no way to predict if it will do so and print new lows below the August lows or not. But after days like yesterday, the possibility of that scenario still to unfold, increases. It is hard to assess where and when this typical Q3 low will be reached or if it has already been printed. But right now we still do not have enough evidence, that the autumn correction is over. In an ideal setup we would want to see some of the major benchmarks at least produce buy signals or for volatility indices to show sell signals. None of those are present yet.

S&P...still with uncompleted Buy counts to the downside ( pink 8 out of 13)

But despite all that we still have a high conviction, that into year end markets will be substantially higher, then where they are right now. We highlighted the charts of Bonds and Yields yesterday. Obviously Yields rose even more after the FED, but they are in such stretched territory, that we see very little upside for them. The FED was as hawkish as it could be, and there is now little left to move them much higher from here. This should eventually turn into a tailwind for markets. That the current months would be much harder to navigate then the first half of the year, was always a given. But that period will pass as well and the outlook will get clearer again.

US 2 year yield with Sell signal ( pink 13)...upside limited

European indices won't escape the negative impact from the US today. But their ability to bounce over the last few days has created some room for them not to threaten the major supports, that held last week, even on a down day like today. They are driven mainly by the moves in the US, but if they can continue to hold the lows form August, we would still expect them to recover within their current trading range. We clearly do not expect a major rally, as the seasonal setup is still too shaky. But we are hopeful, that European markets can get through the next few weeks by moving along within their ranges without breaking the supports at 4180 on the Estoxx and 15,500 on the DAX. As long as that is the case, we do not see the need for any major action.

DAX...still holding 200d MA and August low support

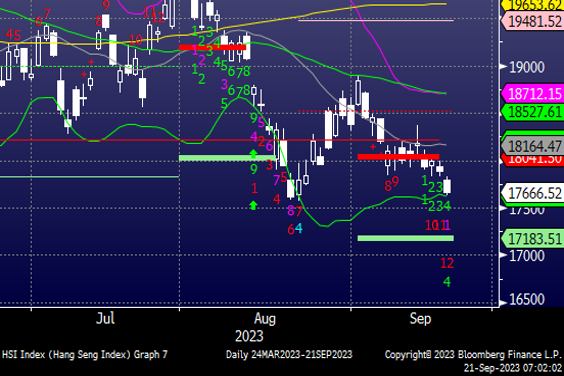

Asian markets on the other hand are so far not showing any signs of a bounce, as we had hoped for. Despite a buy signal earlier in the week on the HSTECH index and the CSI 300 both got ignored. The Hang Seng is pretty much back at its low from August at 17,500. That creates a risk of a new low going forward. But both, the Hang Seng and the HSTECH will lock in another buy signal potentially by tomorrow. It is not the strongest of signals and one more indicator is still uncomplete. But there is a good chance, that the Hang Seng could bounce of that support with the presence of that buy signal. That would be our expectation for now, as long as the 17,500 low does not get broken.

Hang Seng...with potential Buy signal tomorrow ( red 13) just above August low at 17,500

BY Doug Kass · Sep 21, 2023, 9:08 AM EDT

BY Doug Kass · Sep 21, 2023, 8:53 AM EDT

BY Doug Kass · Sep 21, 2023, 8:33 AM EDT

Upside:

-ALGS +8.8% (announces IND Clearance for NASH lead, ALG-055009)

-FDX +4.7% (earnings, guidance)

-MRVL +3.9% (earnings, guidance)

-CRWD +2.5% (earnings, guidance)

-OPRA +2.2% (earnings, guidance)

-SPLK - Halted following news of acquisition by CSCO (to resume trading at 815a ET)

Downside:

-TVTX -37% (announces confirmatory data from the Phase 3 PROTECT Study of FILSPARI demonstrating long-term kidney function preservation in IgA Nephropathy; narrowly misses eGFR total slope endpoint versus active control, Irbesartan)

-AVGO -6.5% (Google's executives have extensively discussed dropping Broadcom as a supplier of AI chips as early as 2027)

-CSCO -4.9% (to acquire SPLK for $157/shr in cash)

-KBH -3.3% (earnings, guidance)

BY Doug Kass · Sep 21, 2023, 8:18 AM EDT

There will be no "Futures" column because I am too busy trading this morning.

Market thoughts coming up.

BY Doug Kass · Sep 21, 2023, 7:35 AM EDT

Repeating for emphasis...

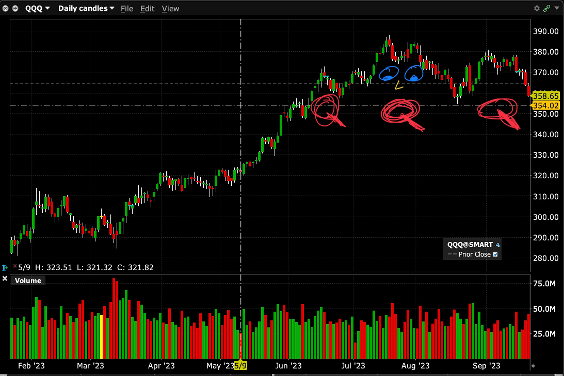

I see head-and-shoulder tops everywhere:

BY Doug Kass · Sep 21, 2023, 7:22 AM EDT

This table is a valuable resource for momentum-based short-term traders:

Themes and Sectors

BY Doug Kass · Sep 21, 2023, 7:16 AM EDT

BY Doug Kass · Sep 21, 2023, 7:01 AM EDT

From JPMorgan:US: Futs are weaker, seeing follow-up selling after the Fed's hawkish pause. Longer-dated bond yields are 2-4bps higher, aiding USD appreciation. Cmdtys are coming for sale and WTI again begins the day sub-$90. Some non-Fed headlines come from BAC's CFO who says, "It's difficult to see a US recession when the consumer is spending 4% more year-over year." Axios reports that the US Chamber of Commerce's Small Business Index, a confidence indicator, has reached its highest level since COVID struck US markets in early 2020. The survey includes 751 business, each that have fewer than 500 people; 71% say they expect revenue to increase next year. Today's macro data focus is on Jobless Claims, Existing Home Sales, Leading Index, and Philly Fed.

And...EQUITY AND MACRO NARRATIVE: Following the Fed's decisions, here are my immediate comments yesterday (in BBG chat/blast): The Fed is predicting stronger growth while inflation expectations are essentially unchanged. By 2026, the economy will have reverted to its long-term average of 1.8% GDP growth with 2% inflation. Equities are clearly reacting to moves in the yield curve but taking a step back, the Fed expects growth without inflation despite (their own prediction) a materially looser labor market. Let's wait for the press conference but this is about as hawkish as we could reasonably expect and this does nothing to change the investment hypothesis ... my view (tactically cautious through month-end) is still constructive longer-term ... GDP growth will continue to surprise to the upside, earnings improve from here, disinflation trend continues, and Fed is done. This is bullish for risk assets despite it likely being a bumpy ride into year-end.

BY Doug Kass · Sep 21, 2023, 6:49 AM EDT

On the gap lower this morning (with stock futures falling further) I am covering my short positions in ABNB , TSLA and BRK.B for quick and nice profits.

BY Doug Kass · Sep 21, 2023, 6:38 AM EDT

BY Doug Kass · Sep 21, 2023, 6:29 AM EDT

From my friends at Miller Tabak:

Wednesday, September 20, 2023

The Fed Is Overpromising: Upcoming Data Will Disappoint

While the Fed's decision to hold rates steady was a forgone conclusion, the new Summary of Economic Projections (SEP) surprised us by being overly optimistic about the U.S. outlook. The Fed now projects that the real GDP growth will meet its 1.8% long-term average between 2023-25, with 2.1% growth in 2023 making up for 1.5% growth in 2024. The Fed is thus predicting that the current tightening cycle will be completely pain free rather than leading to below-trend growth. This is not realistic. The previous SEP's forecast of 1.1% GDP growth in 2024 (with sub-1% growth early in the year) is far more likely.

The FOMC now expects 2.1% GDP growth in 2023, corresponding roughly to 2.5% in 3Q and 1.8% in 4Q (the FOMC does not provide quarterly forecasts). Like most analysts, the FOMC is misunderstanding why recent growth has beaten expectations. It is not because rate hikes have mostly passed through the economy. Rather, it is because of an unexpected and temporary productivity spike, captured by a 3.4% annualized increase in 2Q2023. This results from the resolution of pandemic-era disruptions, particularly to the labor market, but it will be exhausted by the end of the year. Better productivity has boosted growth and led to excellent June and July inflation readings, but it should not have major effects on the 2024 outlook. Non-residential investment, including capital expenditures, will stall over the next two quarters. The end of pandemic savings should lower consumption growth back to trend. This adds up growth slightly below 1% growth in 4Q2023 and 1Q2024.

The new dot-plot shows a 12-7 majority of FOMC members expecting one more rate hike this year, although there appears little chance of the Fed going above 550-575 bps. We see a 75% chance, however, that the Fed is done raising rates. Weaker data should soon cause at least three FOMC members to switch to no more rate hikes. Powell also described recent strong growth as coming from stronger demand: "growth has come in higher than expected and that requires higher rates." By December, however, the Fed should better understand that because recent growth comes from better productivity, it has been disinflationary.

BY Doug Kass · Sep 21, 2023, 6:20 AM EDT

Wolf Street howls about Powell and the repeated use of "carefully" at his press conference.

BY Doug Kass · Sep 21, 2023, 6:09 AM EDT

BY Doug Kass · Sep 21, 2023, 5:49 AM EDT