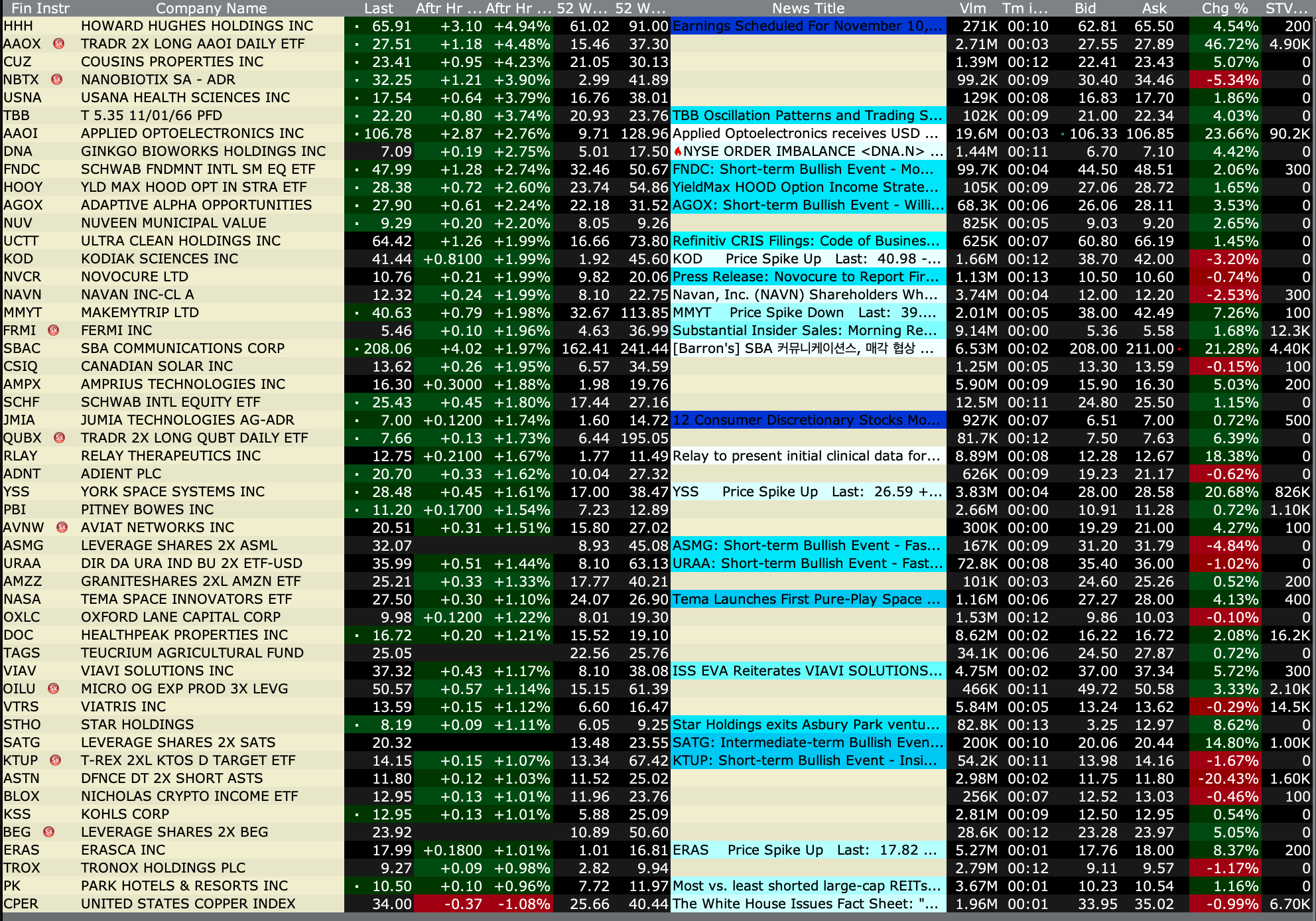

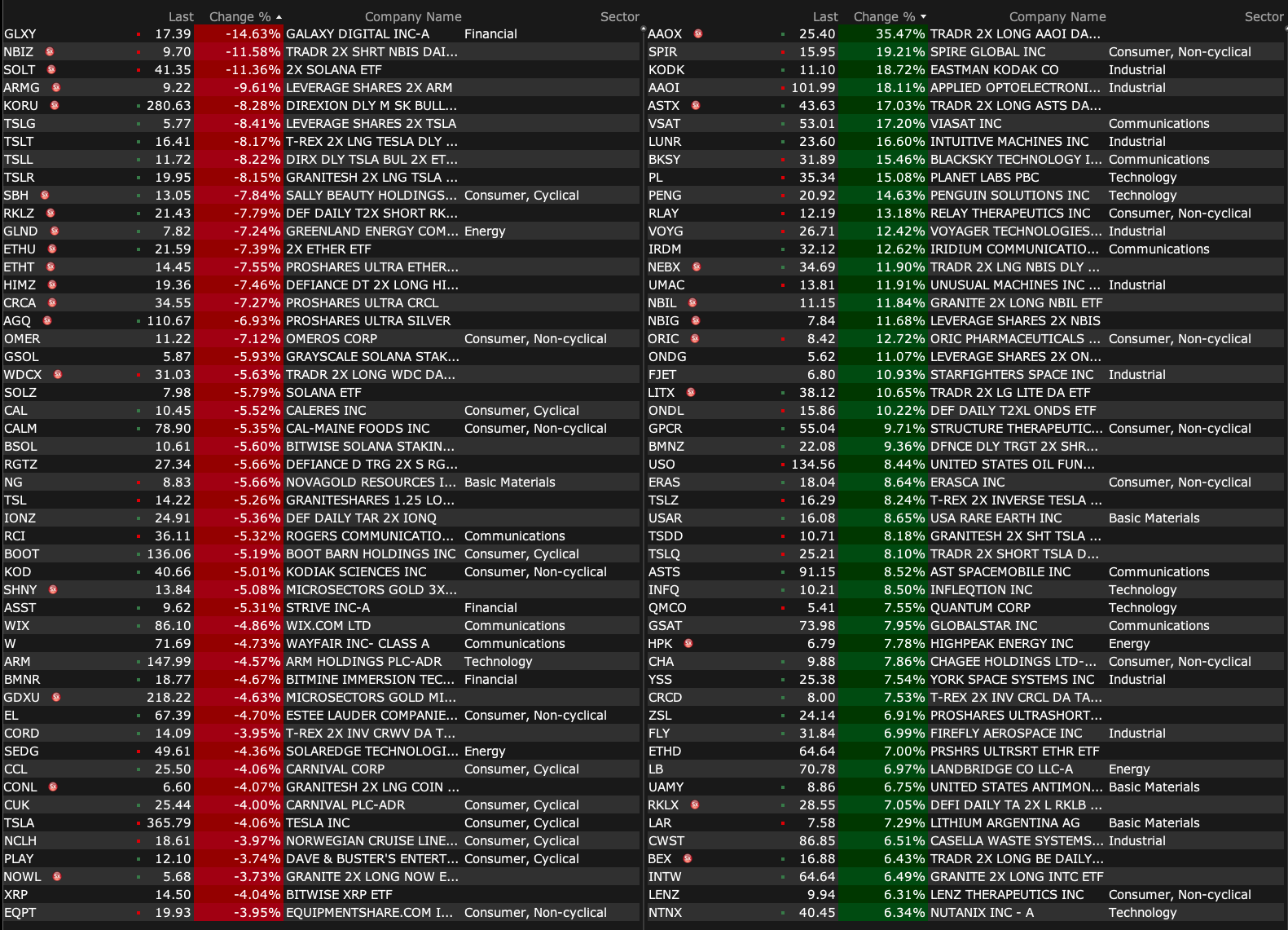

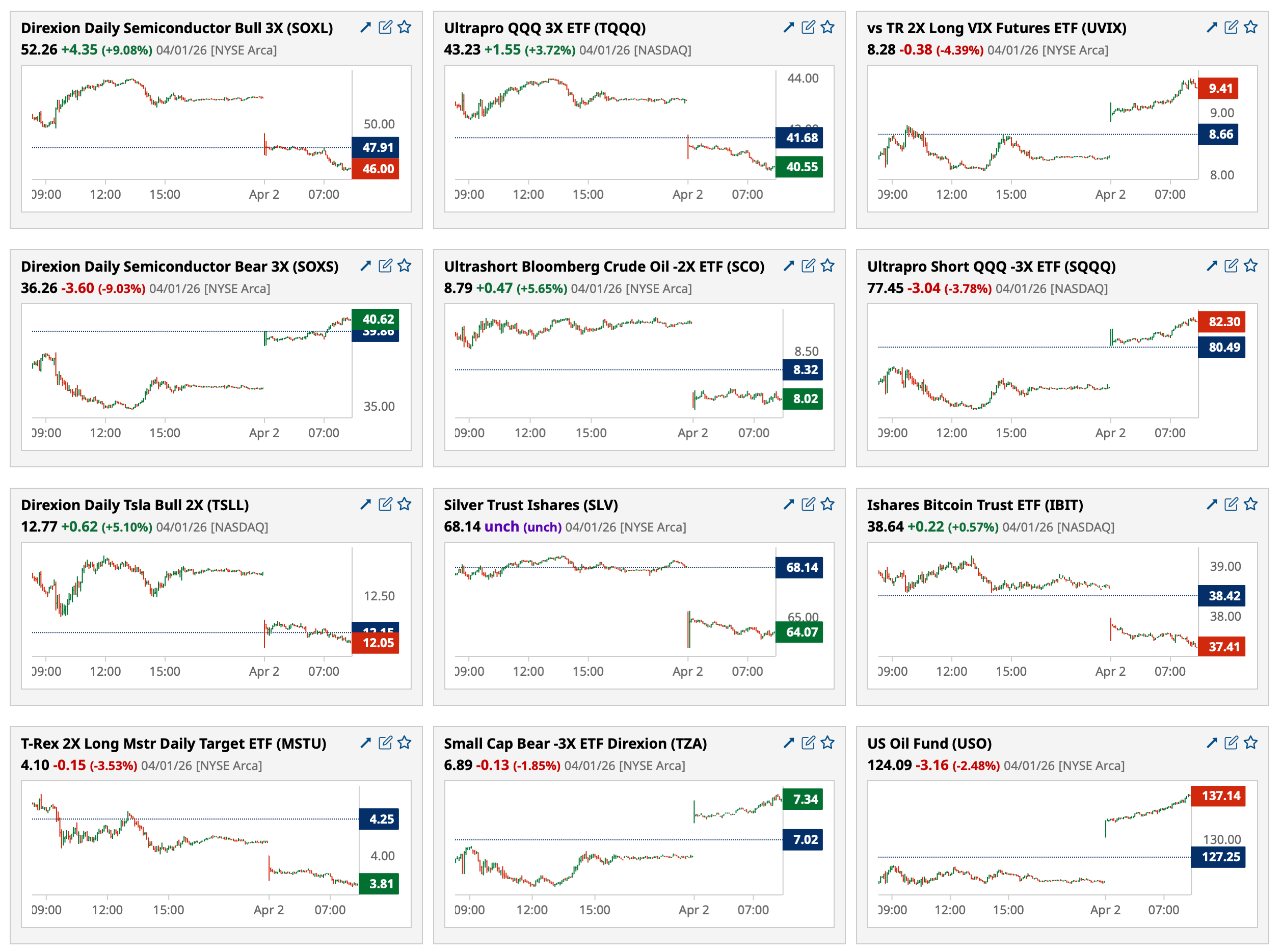

Thursday's After-Hours Advancers and Decliners

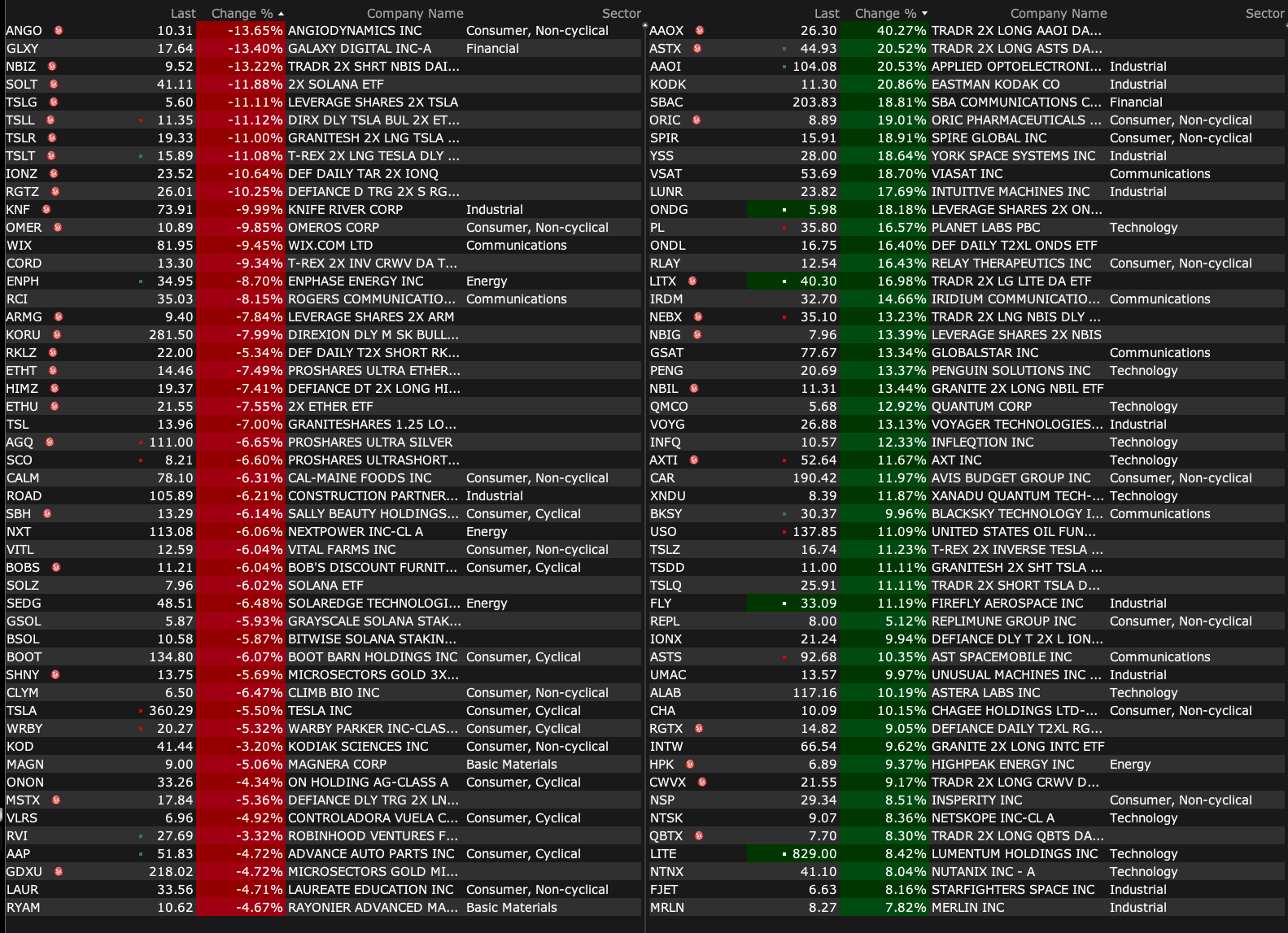

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Apr 2, 2026, 4:40 PM EDT

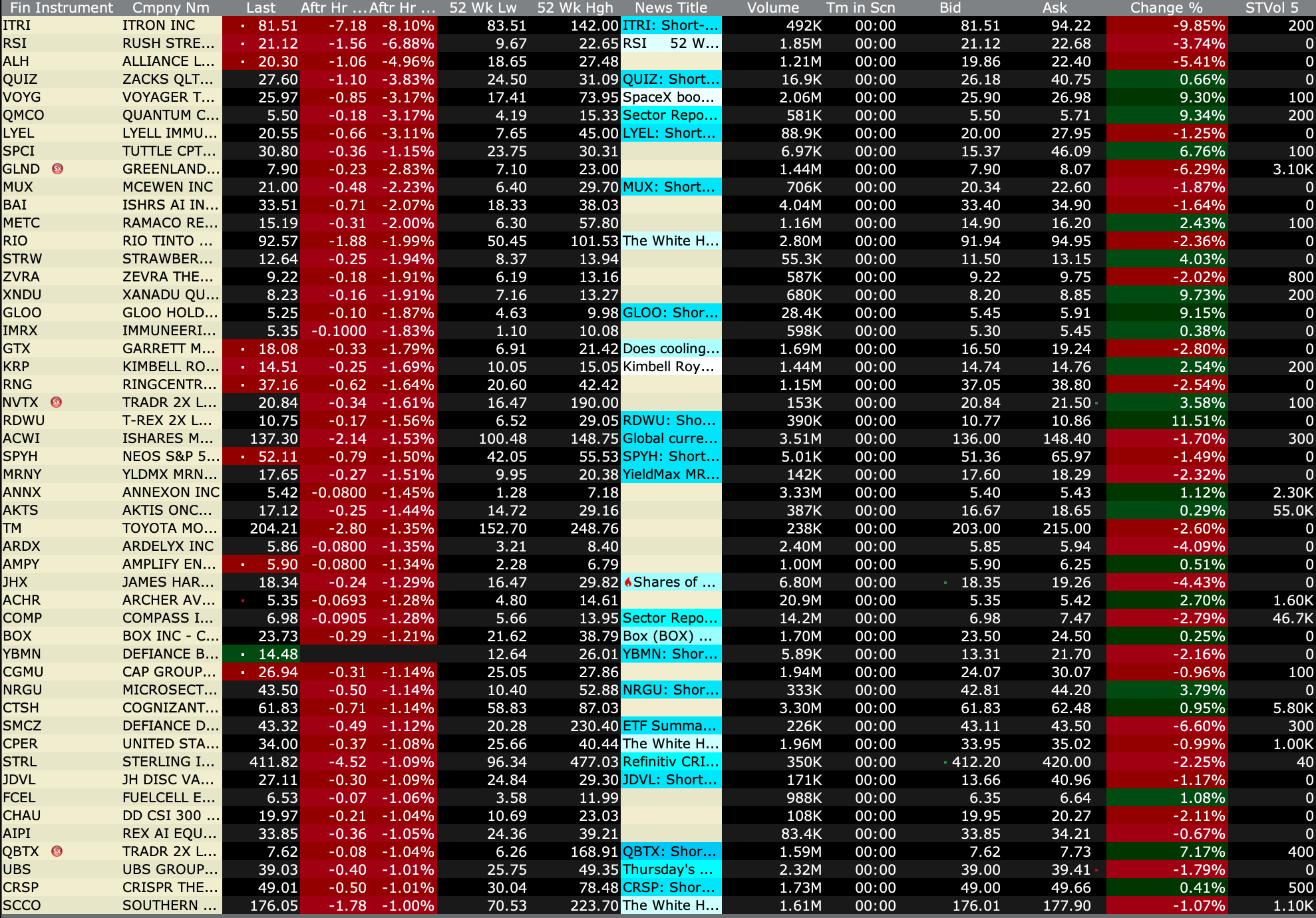

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Apr 2, 2026, 4:40 PM EDT

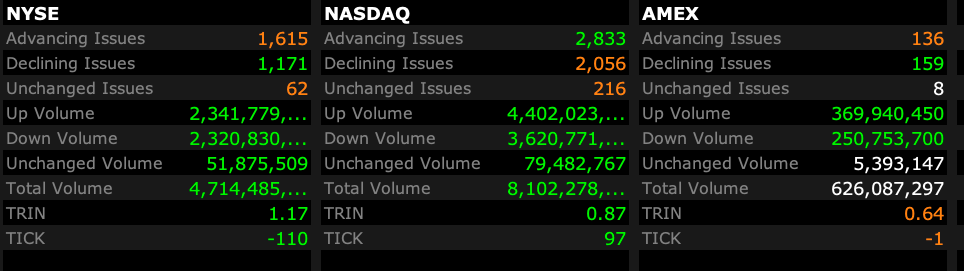

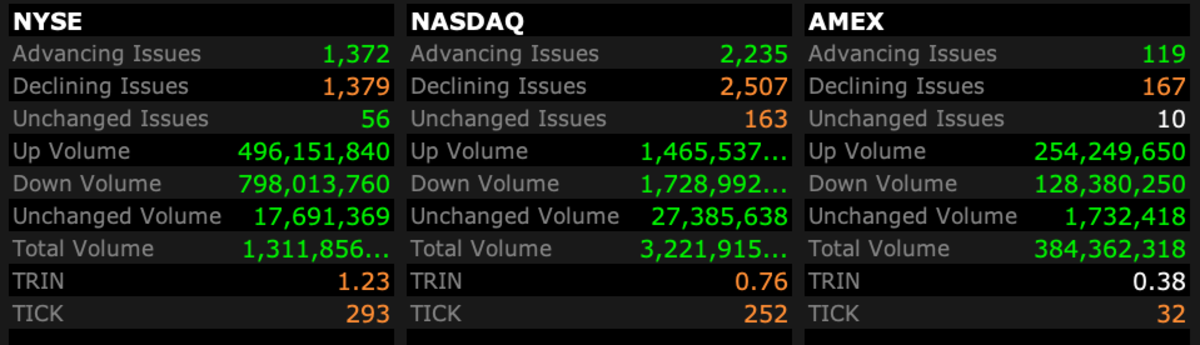

Closing [Low] Volume

- NYSE volume 16% below its one-month average

- NASDAQ volume 7% below its one-month average

- VIX index: down 1.92% to 24.07

Breadth

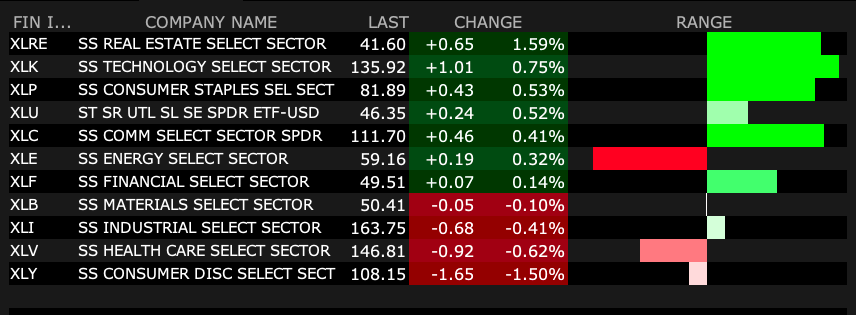

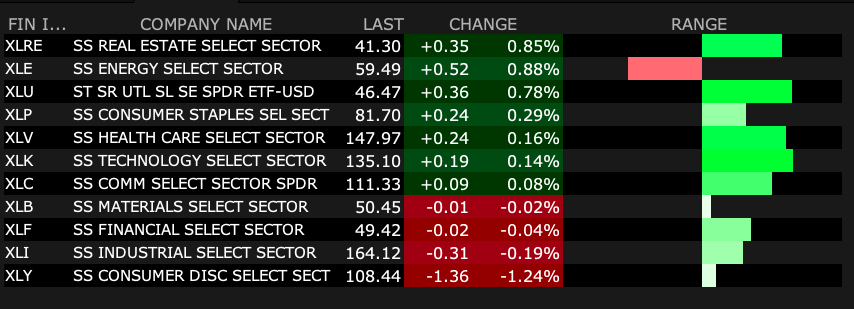

S&P 500 Sector ETFs

% Movers

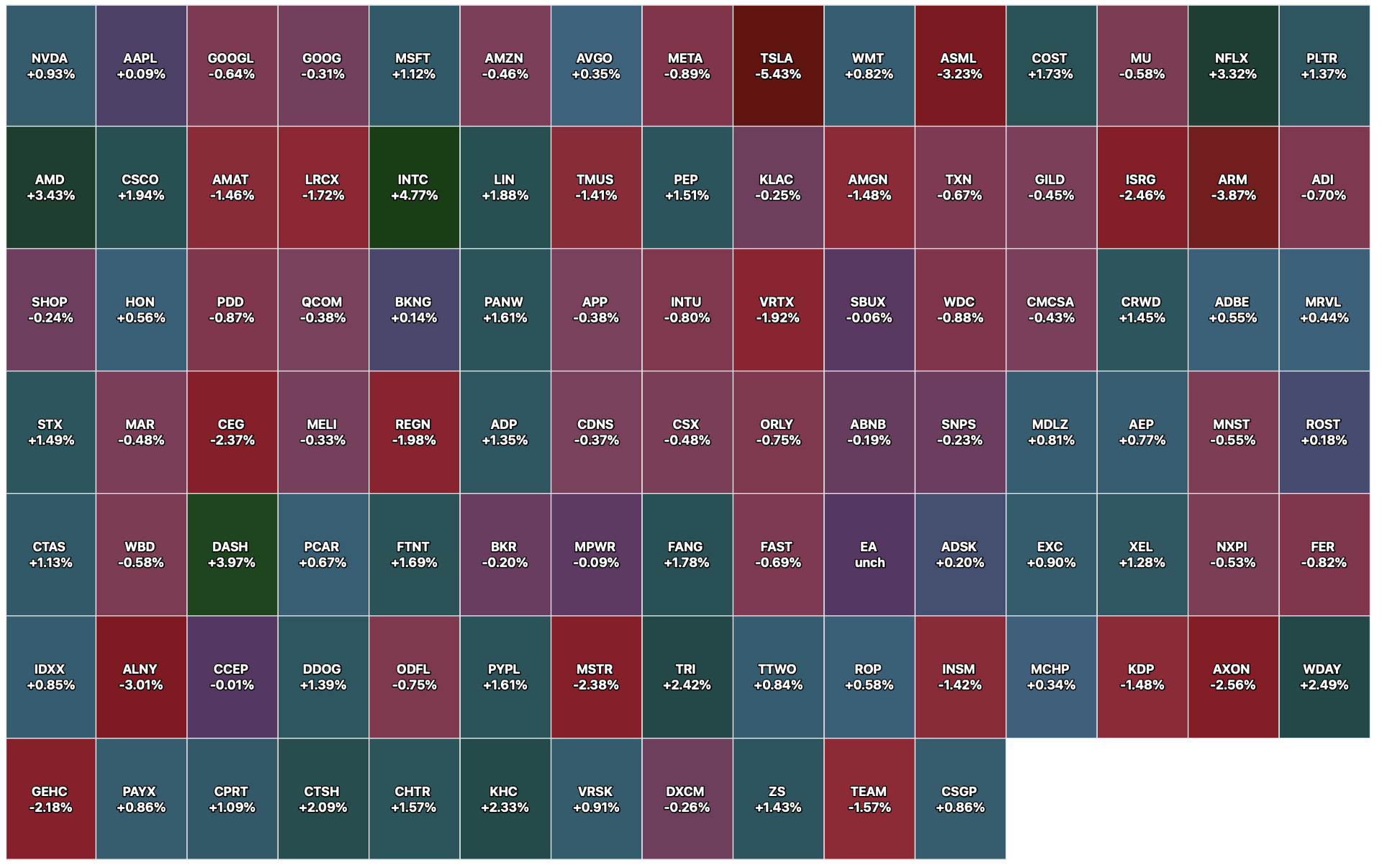

Nasdaq 100 Heat Map

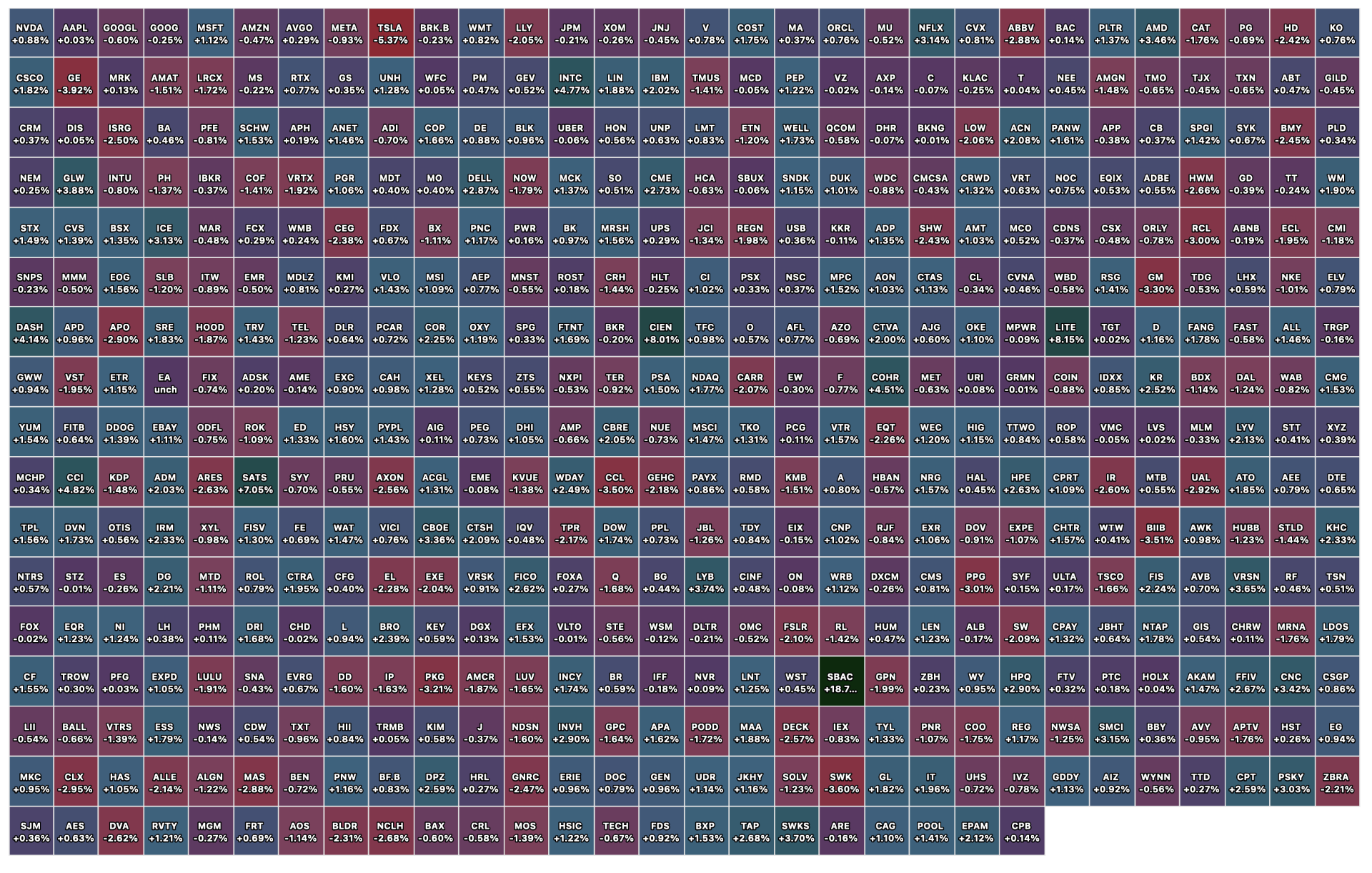

Closing S&P 500 Heat Map

BY Doug Kass · Apr 2, 2026, 4:23 PM EDT

* Nike faces a long (3-4 year) path until overall results recover

* Despite the sharp fall in price it may be too early to "bottom fish" in Nike's shares...

Yesterday Nike (NKE) reported mixed fiscal third-quarter performance against low expectations.

The fourth-quarter guidance was awful and, looking out to next year, management suggested a longer-than-expected path to recovery.

NIKE, Inc. - Investor Relations - NIKE, Inc. Reports Fiscal 2026 Third Quarter Results

While Nike's Win Now program and Sports Offense Strategy is likely to yield good results, the inflection point in the company's fundamentals (likely one to two years away) is beyond my investing timeframe.

Though the company's North American operations are already starting to show modest improvement, other channels and geographies (particularly China and EMEA) have a lot of work in front of them before stabilization will be seen.

Significantly, macroeconomic headwinds are likely moving in the wrong direction and could further delay Nike's sales and profit recovery (particularly in the sportswear division and to direct to consumer channels).

The bottom line is that I don't see reported EPS beating fiscal (May) 2025 returns until 2029.

From Goldman Sachs:

The Positives

NKE management signaled improving confidence in the progress made against its Win Now Strategy and Sport Offense repositioning. North America commentary was incrementally constructive, with NKE highlighting a sequential improvement in digital performance throughout the quarter with improvements in average retail discounts, improved sell-throughs in February, and positive growth in all channels in the geography for the first time in several years.

NKE also signaled confidence in a return to balanced growth in NA for both the direct and wholesale channels in the near-term, and suggested they are not seeing a change in consumer trends as a result of recent macro trends. Beyond NA, management called out growing order books, strong wholesale partnerships, and shelf space recapture.

Management also indicated that Spring 2027 will be the first quarter in which products developed under the Sport Offense framework flow into the marketplace.

The Negatives

Management acknowledged that their comeback is taking longer than they would like. Momentum sequentially weakened in EMEA, with management calling out weaker sell-through trends and elevated promotions across the marketplace.

Franchise management actions continue to weigh on results (-MSD% headwind in F3Q),and NKE signaled that they still have work to do to reposition the Dunk. Sportswear remains a significant headwind to revenue growth, markdowns remain elevated, and digital remains too promotional, per management. China repositioning remains in the early days, and management signaled that profitability would improve before sales as actions take root.

Revenues are set to decline as a result of intentional sell-in reductions and marketplace management.

As demonstrated below, Wall Street's EPS forecasts and price targets — though markedly reduced after results were announced — still remain far too optimistic:

Nike price target lowered to $57 from $69 at Evercore ISI Evercore ISI analyst Michael Binetti lowered the firm's price target on Nike to $57 from $69 and keeps an Outperform rating on the shares. Nike's turnaround is proving "tougher and slower than hoped," with new headwinds pushing any real EPS inflection further out and "well into" FY27 or FY28, the analyst tells investors in a post-earnings note.

Nike price target lowered to $56 from $65 at Stifel Stifel lowered the firm's price target on Nike to $56 from $65 and keeps a Hold rating on the shares. The fiscal Q3 report makes the firm "incrementally cautious" on the timing and magnitude of Nike's turnaround, the analyst tells investors. While Q4 revenue and EPS guidance "appear beatable," investor aspirations for a mid-single digit percent year-over-year top-line algorithm "appear to be pushed to FY28," the analyst added.

Nike price target lowered to $75 from $90 at BTIG BTIG lowered the firm's price target on Nike to $75 from $90 and keeps a Buy rating on the shares after its Q3 results. Within North America, Sportswear remains challenging and gross margin declined 130 basis points, pressured again by tariff costs, the analyst tells investors in a research note. The firm adds that Q4 revenues are expected to decline in China by 20% as the company is managing sell-in tightly. BTIG further notes that with the turnaround taking longer than anticipated, it is reducing its EPS estimates for Nike for FY26 to $1.52 from $1.70 and for FY27 to $1.90 from $2.50.

Goldman 'incrementally cautious' on Nike post results, downgrades shares Goldman Sachs downgraded Nike to Neutral from Buy with a price target of $52, down from $76. JPMorgan this morning also downgraded the shares. The stock in premarket trading is down 10% to $47.30. Goldman left the company's fiscal Q3 report "incrementally cautious" on the timeline of its recovery. Nike's momentum in sportswear "remains muted," its inventory reset actions are ongoing, and China remains under "particular pressure," the analyst tells investors in a research note. The firm believes "more patience will be needed" as Nike executes its strategic plan with macro headwinds pick up. As such, it sees a balanced risk/reward for the shares.

Nike price target lowered to $53 from $65 at Citi Citi analyst Paul Lejuez lowered the firm's price target on Nike to $53 from $65 and keeps a Neutral rating on the shares. The company reported a fiscal Q3 earnings beat but the earnings call brought "disappointment" on the pace of Nike's around, the analyst tells investors in a research note. Citi sees a balanced risk/reward at current share levels.

Position: Long C (VS)

BY Doug Kass · Apr 2, 2026, 3:15 PM EDT

On rescheduling, Blanche said during his Senate confirmation hearing he would give the issue "careful consideration". Blanche will eventually be replaced with Lee Zeldin, pending Senate approval. Zeldin has backed cannabis banking and protecting state medical cannabis laws.

— Anthony Martinelli (@AMartinelliWA)

BY Doug Kass · Apr 2, 2026, 2:30 PM EDT

tommyPA

Just saw Josh Brown give incredible insight about why he's buying his new Best Stocks in the Markets - QSR (near the 52-week high $76.00) "BECAUSE PEOPLE HAVE TO EAT" ... okay sounds logical. But then why are restaurants WEN, BLMN, CBRL near 52-week lows??

BY Doug Kass · Apr 2, 2026, 1:45 PM EDT

President Trump has ousted Pam Bondi as Attorney General.

BY Doug Kass · Apr 2, 2026, 1:32 PM EDT

Apropos to

Lee Zeldin is a possible replacement.

BY Doug Kass · Apr 2, 2026, 1:02 PM EDT

Break in.

Amazon (AMZN) to impose a 3.5% fuel and logistics surcharge on fulfillment services for third-party sellers.

Amazon to apply 3.5% fuel and logistics surcharge on fulfillment | Supply Chain Dive

Position: Long AMZN (S)

BY Doug Kass · Apr 2, 2026, 12:16 PM EDT

BY Doug Kass · Apr 2, 2026, 11:40 AM EDT

Equities ripped right before the public announcement of a possible drafting of a deal in which Iran and Oman may be establishing protocol to "monitor" the Strait of Hormuz's traffic.

Iran and Oman drafting protocol to 'monitor' Hormuz Strait traffic: IRNA

Iran must have joined the ranks of insider traders!

With "everyone" now trading on inside information... what a confidence builder for the markets. (Tongue in cheek!)

BY Doug Kass · Apr 2, 2026, 11:30 AM EDT

From Peter Boockvar:

Reading between the lines, we did not hear about progress on the negotiations with Iran last night and thus no further insight on when the Strait will fully reopen without threat. Thus, the war trade is back on. I am growing more and more concerned about growing global supply shortages, particularly with refined products, that we’re going to hear about in the coming weeks and over the month.

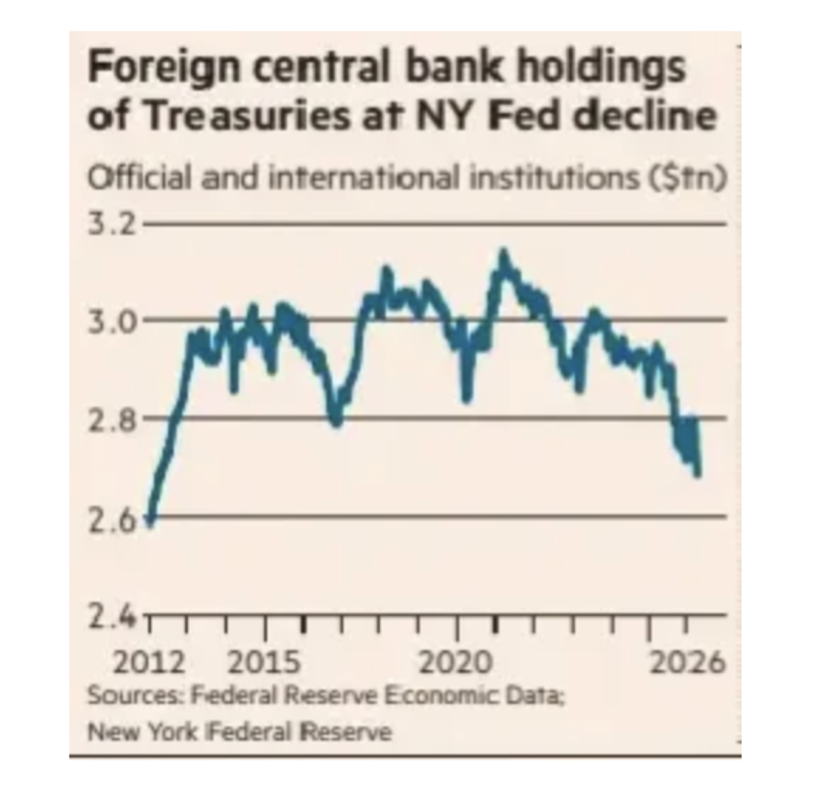

I mentioned Monday that because foreigners own so much of US assets, that our markets are a source of funds for them. Here is a chart from the FT of foreign official holdings (central banks and governments) of US Treasuries that hit their lowest level since 2012.

I mentioned also Monday the depressed market sentiment in the CNN Fear/Greed index that was a good set up for the two day rally we had to almost the 200 day moving average in the S&P 500. That was confirmed by the Investors Intelligence survey (as of last Friday) seen yesterday that saw Bulls fall to 35.2, the least since May 2025, from 39.3 while Bears jumped to 31.5 from 25. It was just February when this spread was north of 45. Today, the AAII retail index had Bulls at 33.6, up1.5 pts but Bears at 51.4, higher by 1.6 with the balance Neutral.

Bottom line, after an almost 4% rally to near the 200 day, I no longer have confidence in any further upside for now until the war ends.

Auto sales in March totaled 16.34mm, better than the estimate of 15.86mm but below the 17.77mm in March 2025 and 17.5mm in March 2019. The Car Dealership Guy said “Last year’s tariff driven pull-ahead inflated the comparison baseline, but the results still reinforce a split market, with many mainstream brands contending with softer sales, while demand for profitable trucks and SUVs continues to hold up.”

Wards on Tuesday, ahead of the March data on car sales, said “history shows that while gas prices can change quickly, it can take several months before consumer behavior gets seriously affected.”

MSC Industrial Direct, the large distributor of many things that go to the manufacturing and industrial sector, is a go to earnings call for me on the state of things. They said this of note yesterday:

“I would describe the current state as a tale of two realities. On one hand, signs of a potential industrial recovery are encouraging...the IP readings across most of our top manufacturing end markets are beginning to form more favorable trends. Customer sentiment has been improving also as seen by recent MBI readings, which have produced consecutive monthly readings above 50 for the first time in a multi year period.”

“However, on the other hand, geopolitical tensions, the war with Iran and rising fuel costs present heightened uncertainty. While we haven’t seen any meaningful disruption yet, we are in constant communication with customers and are taking proactive steps to secure supply.”

PVH, the owner of Calvin Klein, Tommy Hilfiger, and Heritage Brands, jumped 10% yesterday and said this on their call:

“In the fourth quarter, we exceeded our guidance across revenue, operating profit, and EPS...Despite the choppy consumer and macroeconomic environment, we delivered a non-GAAP operating margin of 8.8% for the full year, above our guidance, including the impact of tariffs.”

“Looking ahead, while the macroeconomic environment remains uncertain, we have started 2026 with positive momentum and higher spring season sell through trends across both brands and all three regions. While wholesalers remain cautious and the consumer macro environment continues to be uneven, our fall 2026 order books for Europe are positive.

Specifically with their North American business, “The consumer backdrop has been uneven and in stores, industry traffic trends were increasingly challenged, resulting in our total D2C business down low-single digits for the year.”

From Lamb Weston, the maker of french fries, and whose stock fell 9% yesterday:

“Volume increased 7%, led by solid execution in North America, including customer wins, share gains, and strong retention. This more than offset softer demand in key markets in our international segment...as well as increased competitive export dynamics, which most notably affected our EMEA business.”

“Let me provide context on what we are seeing in traffic trends. In the US, QSR traffic turned positive for the first time since fiscal 2024, up 1% for the quarter. QSR burger traffic grew in February, although it was down 1% for the full quarter. QSR chicken remained a bright spot with continued growth. Internationally, most markets saw low single digit declines in restaurant traffic. In the UK, our largest international market, QSR traffic declined approximately 1%, showing improvement versus recent quarters.”

“Outside of EMEA, volume grew in China and Latin America, and year-to-date volume is up across every region outside of EMEA.” For overall international, “we anticipate y/o/y declines in the second half as we lap unusually strong performance last year and as the fourth quarter is further pressured by the evolving conflict in the Middle East. For reference, sales to the Middle East represents a high single digit percentage of the international segment’s volume year-to-date.”

None.

BY Doug Kass · Apr 2, 2026, 11:15 AM EDT

From Peter Boockvar:

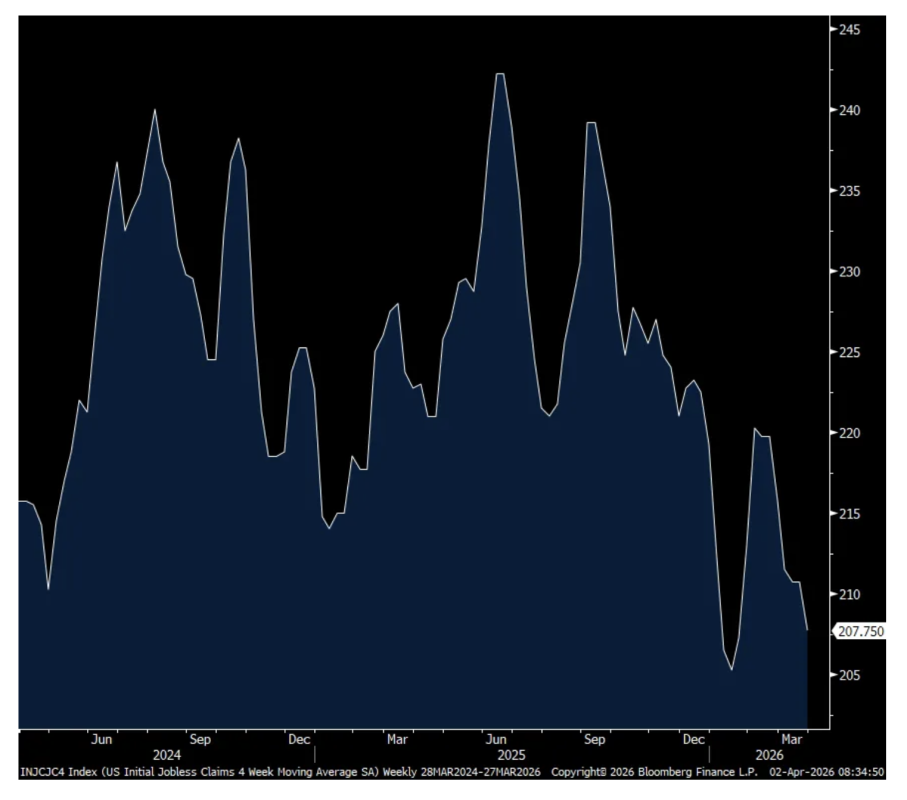

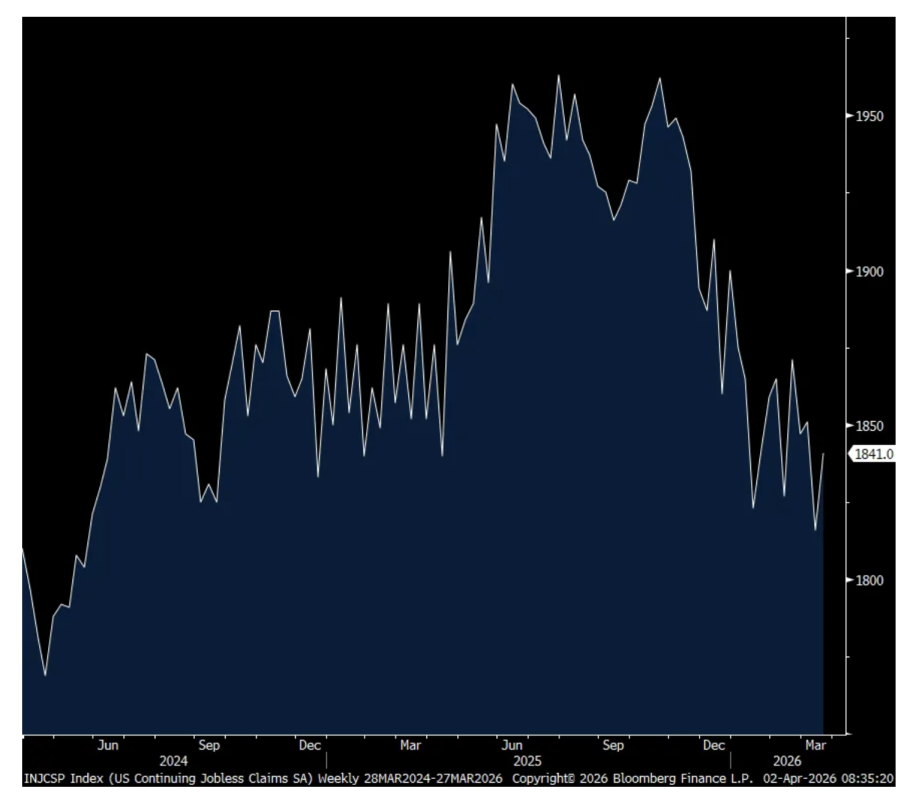

The pace of firing’s as measured by the weekly claims data remains muted with new unemployment filings totaling just 202k, 10k below expectations and down from 211k in the week before. This brings the 4 week average down to 208k from 211k last week. Continuing claims were 1.841mm, up from 1.816mm in the week prior but still remaining below 1.9mm. Is that because benefits are running out or people are slowly finding new jobs or both. I’m leaning on the first choice just based on the modest hiring data we’re seeing outside of healthcare.

4 week avg Initial Claims

Continuing Claims

Challenger today said that there were 60,620 announced job cuts in March, up 25% sequentially but lower by 78% y/o/y. They said, “Removing the wave of federal layoffs announced in February and March of last year, job cut announcements in 2026 are closely following the pattern of 2025. Last year it was Government, Retail, and Technology. This year, it’s Technology, Transportation, and Healthcare.” Interesting on that last category, healthcare, since it seems to be the main source of hiring, especially seen in yesterday’s ADP report.

Specifically with tech, Challenger said “Companies are shifting budgets toward AI investments at the expense of jobs. The actual replacing of roles can be seen in Technology companies, where AI can replace coding functions. Other industries are testing the limits of this new technology, and while it can’t replace jobs completely, it is costing jobs.”

Year to date, these have been the reasons given for job cuts, “So far in 2026, Market and Economic Conditions lead all reasons year-to-date with 45,103 cuts, followed by Restructuring with 37,916, Closings with 37,405, and Contract Loss with 31,817. AI ranks fifth year-to-date with 27,645 cuts, or roughly 13% of all job cut plans.”

Positively, hiring plans jumped 157% in March from February and up 149% y/o/y. Though, year to date, hiring is down 6% y/o/y.

None.

BY Doug Kass · Apr 2, 2026, 10:45 AM EDT

BY Doug Kass · Apr 2, 2026, 10:45 AM EDT

A reminder (from a tweet I made two weeks ago):

Remember, nearly EVERY opinion that was confidentally delivered on @cnbc over the last two months were totally wrong:

— Dougie Kass (@DougKass)

1. There is economic risk. (The threat to global economic growth is obvious)

2 There is geopolitical risk (Duh!)

3. There is interest rate and inflation risk.… https://t.co/Y4IUT026N1

None.

BY Doug Kass · Apr 2, 2026, 10:15 AM EDT

Here are today's things:

* Bought indexes: (SPY) $645.37 and (QQQ) $573.03.

* Added back to following technology stocks: (AMZN) $205.93, (GOOGL) $289.92, (META) $561.99, (MSFT) $365.02.

* Bought (VRNOF) $1.07.

Long SPY common M QQQ common M VRNOF VS AMZN S GOOGL S META S MSFT S

BY Doug Kass · Apr 2, 2026, 10:03 AM EDT

* Yesterday's obsequious Squawk Box interview with Cathie Wood underscored the failure of FinTV journalism

* Good god, man (host) - do your homework and stop bootlicking the egos of "talking heads" that have not earned the privilege of appearing on your platform...

Yesterday Cathie Wood was interviewed on Squawk Box about ARK's (ARKK) investment in OpenAI.

Here is the tape: Cathie Wood on OpenAI: We continue to serve as a bridge between private and public markets

The CNBC host, Joe Kernen, started out by cherry picking Wood's investment returns by indicating how well ARKK has performed over the last 12 months but failing to state that the exchange-traded fund has lost more money (estimated at $13 billion last year) than any actively managed exchange traded fund in history (as most of the money came into ARKK near or at the top of ARKK's share price).

Moreover, and not surprisingly, the interviewer also failed to go beyond the surface in his interview. Cathie Wood started out by stating that ARK provides a bridge between the private and public markets.

To that I say... B.S.!

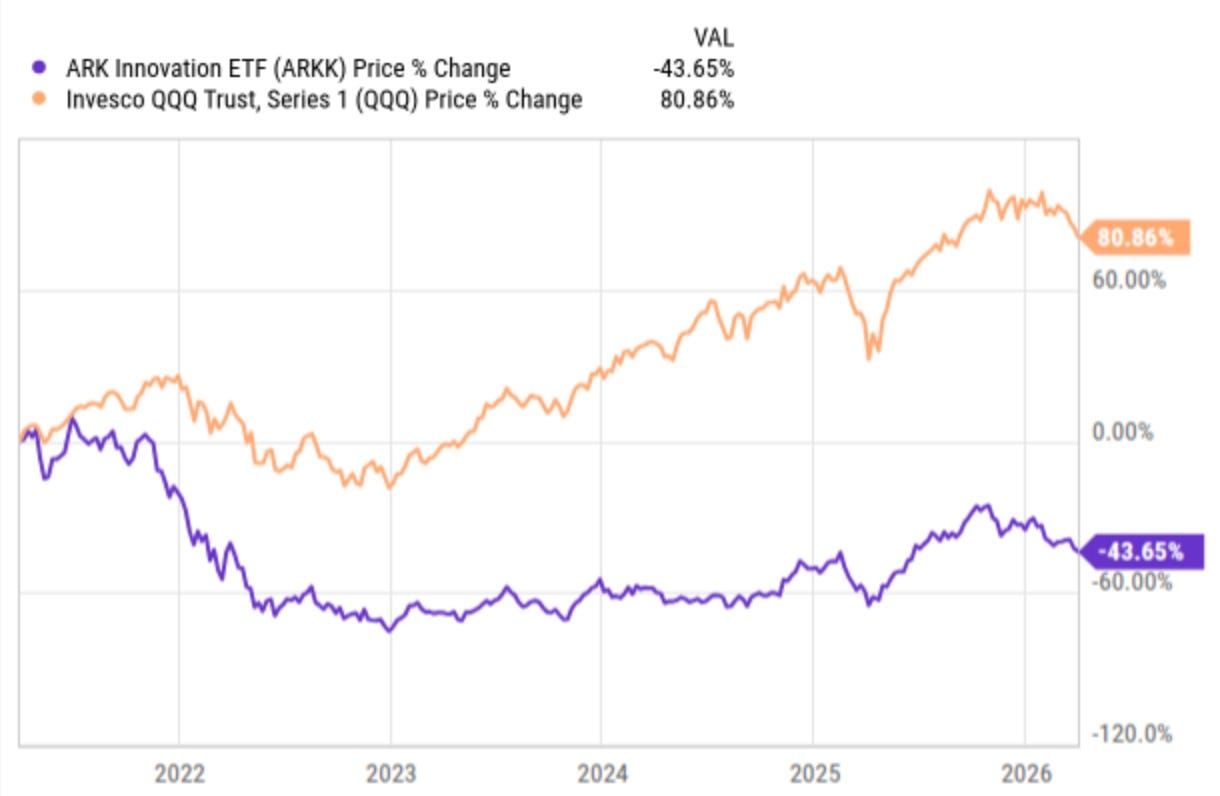

In reality, as seen in Quoth The Raven's column this morning (see quote at the beginning of the column), the percentage of the ARK exchange traded funds have invested in Open AI is de minimis and doesn't move the performance needle of those funds.

From Quoth The Raven: The OpenAI Trade Without The Baggage - by Quoth the Raven

"The latest development making headlines is that OpenAI is set to gain exposure across several ETFs run by Ark Investment Management, according to reporting from Bloomberg.

The exposure will come through funds including the ARK Innovation ETF, ARK Fintech Innovation ETF, and ARK Next Generation Internet ETF, each expected to hold roughly a three percent stake. For retail investors, this is being framed as a rare opportunity to gain access to one of the most sought-after private AI companies in the world. On the surface, that sounds compelling.

In reality, it is far less attractive than it appears and I believe there are far better ways to get exposure to OpenAI (and Anthropic).

The key issue with ARK is that investors are not actually buying OpenAI by itself. They are buying an actively managed ETF with a small allocation to OpenAI embedded within a much larger portfolio driven by the decisions of Cathie Wood.

That distinction matters, especially when you look at the track record. Over the past five years, the ARK Innovation ETF has declined roughly 43.65%, while the Invesco QQQ Trust, a proxy for the Nasdaq-100, has risen about 80.86%.

Even more telling, by 2024 ARKK was estimated to have destroyed around $14 billion in shareholder value despite its explosive run during 2019 through 2021, a period largely driven by its heavy exposure to Tesla (TSLA) .

The implication is straightforward: When you buy these ETFs, you are making a bet on the manager as much as, if not more than, the underlying theme.

If the goal is to gain exposure to leading AI companies, there are cleaner and more rational ways to do it, as I noted days ago. Microsoft (MSFT) and Amazon (AMZN) already sit at the center of this ecosystem, with deeply embedded relationships that function as economic call options on the success of OpenAI and Anthropic.

Microsoft has invested more than $10 billion into OpenAI and is widely understood to hold roughly a quarter to a third of its economic upside following its restructuring. More importantly, OpenAI’s models are integrated across Microsoft’s core products, from Azure to Office to Windows. This means that as OpenAI grows, Microsoft benefits not only from equity appreciation but also from increased cloud usage and software monetization."

- Quoth The Raven

Memo to Fin TV:

* Your viewers are your most important stakeholders.

* Do your homework better.

* Engage your guests (whether it is company managements, strategists or investment managers - selling themselves, their services and trying to gather assets) in more thoughtful, value-added and hard-hitting analysis.

And stop fawning over guests (based on the apparent need for access) some of whom, based on investment returns, have not earned the privilege of appearing on a leading business network

Long MSFT VS AMZN VS.

BY Doug Kass · Apr 2, 2026, 9:45 AM EDT

None.

BY Doug Kass · Apr 2, 2026, 9:25 AM EDT

-GSAT +13% (reportedly Amazon considers bidding for Globalstar to compete with Musk's Starlink at a valuation of ~$9B)

-EOG +4.1% (strength in oil and gas producers)

-IRDM +3.4% (higher in sympathy with GSAT)

-CVX +2.5% (CitiGroup Reiterates CVX with Buy, price target: $235 from $210; broad strength in oil and gas)

-LPCN -78% (LPCN 1154 misses Phase 3 primary endpoint in postpartum depression)

-ELAB -63% (announces $4.6M common stock issuance to Streeterville Capital)

-INO -25% (prices 12.5M shares at $1.40/shr in $17.5M underwritten public offering)

-ADAG -14% (updated Data from Phase 1b/2 Study of Muzastotug in Combination with KEYTRUDA (pembrolizumab) in Late-line Patients with Microsatellite Stable Colorectal Cancer Demonstrate Improved Durability of Response; prices 18.7M ADDs at $3.75 per ADS in $70M offering)

-ANRO -10% (ALTO-101 misses primary endpoint)

-OWL -9.1% (caps private credit funds redemptions at 5%)

-IMVT -8.4% (Batoclimab Phase 3 Thyroid Eye Disease (TED) studies miss primary endpoint)

-NAVN -5.9% (Audit Engine adds 45+ compliance checks)

-APO -5.2% (private equity weakness in sympathy with OWL investor redemptions)

-DOCN -4.4% (acquires Katanemo Labs, focused on infrastructure for agentic AI)

-KKR -4.1% (private equity weakness in sympathy with OWL investor redemptions)

-TSLA -4.1% (reports Q1 deliveries, production)

-ARES -4.0% (private equity weakness in sympathy with OWL investor redemptions)

-BX -4.0% (private equity weakness in sympathy with OWL investor redemptions)

-AVGO -2.8% (chip stock weakness)

-NVDA -2.7% (chip stock weakness)

-EL -2.3% (reportedly Estee Lauder is an advanced talks for a stock deal with Puig)

None.

BY Doug Kass · Apr 2, 2026, 9:24 AM EDT

None.

BY Doug Kass · Apr 2, 2026, 9:10 AM EDT

Starting to buy back (AMZN) , (MSFT) , (META) and (GOOGL) in the premarket.

Long AMZN S MSFT S META S GOOGL S

BY Doug Kass · Apr 2, 2026, 8:55 AM EDT

Last night I tweeted out that Attorney General Pam Bondi might be replaced:

bondi likely to be replaced as attorney general by lee zeldin….

— Dougie Kass (@DougKass)

This morning there has been some confirmation that this is being considered.

Trump has discussed ousting Attorney General Pam Bondi, sources say

If accurate it could be a positive for the cannabis space:

The NYT is reporting that Trump is considering firing Bondi, which tracks with what our sources said in March. Bondi may be replaced with Lee Zeldin, who has voted in favor of cannabis banking and backed protections for state medical marijuana programs.https://t.co/pjllQ4XQ4D

— Anthony Martinelli (@AMartinelliWA)

🌿 Every cannabis investor needs to read this headline carefully.

— Denis Rudev (@DenisRudev)

AG Bondi was personally directed by Trump’s Dec 18 executive order to finalize marijuana rescheduling from Schedule I → Schedule III.

A new AG means the rescheduling timeline resets — or accelerates.

Zeldin’s… https://t.co/frQildEZI6

None.

BY Doug Kass · Apr 2, 2026, 8:52 AM EDT

Average cost of my buys in the indexes in premarket:

* (SPY) $645.37

* (QQQ) $573.03

Long SPY common M QQQ common M; Short SPY calls M QQQ calls M

BY Doug Kass · Apr 2, 2026, 8:33 AM EDT

11 a.m.: Fed Bank of Dallas President Logan (Voter) participates in fireside chat before the Eleventh District Banking Conference hosted by the Federal Reserve Bank of Dallas, Dallas, TX (Other details TBA)

11 a.m.: Treasury announces a 6-Week and 3 and 6 Month Bill Auction;

11 a.m.: Treasury's Note Announcement;

11:30 a.m.: Treasury hosts an $80B 4 and a $75B 8 Week Bill Auction

None.

BY Doug Kass · Apr 2, 2026, 8:28 AM EDT

* President Trump's speech rang hollow and fell short relative to market expectations — it was flat, contracted some of his previous comments, tone deaf (ignoring the war's direct consequences of higher inflation and dampened economic demand), raised affordability concerns for the average American and was uneventful (providing few new details regarding the end of the conflict in Iran)

* The almost immediate response was for oil futures (now +$6.35) to rise and stock futures to fall

* The president's speech will likely "fuel" and encourage a rising probability and view of future "slugflation" (a valuation killer)

* Trump's intrusive and disruptive gaming of the markets is probably now over

In yesterday's opener, God Only Knows I expressed some skepticism about the violence of the upside move over the last two days (which was likely exacerbated by short covering). While some values emerged earlier in the week, the breakneck speed in which stocks rose on Tuesday and Wednesday (and that I aggressively sold into — see my multiple Diary posts) reduced the reward vs. risk opportunities and took away some "margin of safety."

The president's speech underscored a likely lengthier and drawn-out conflict in Iran (and, with it, heightened and adverse economic ramifications). Indeed, in some ways it bolstered my medium-term economic and investment concerns.

From Wednesday's column:

My greatest concerns are that the war in Iran (which eventually will be "resolved") will have knock-on consequences to economic growth (weaker), inflation (stronger and more persistent), tighter-than-expected (Fed) monetary policy (so interest rates will be "higher for longer") and produce something of a supply shock (for a vast array of critical materials and products).

The bottom and the middle of the K-shaped U.S. economy are bound to be even more pressured in the months ahead as general affordability is materially threatened by a weakening jobs market and stubbornly higher costs (and inflation).

Importantly, corporate profit growth expectations (of about +15% year over year) will have to be ratcheted down despite protestations from the cabal of (ostrich-like) perma-bulls:

Who in his/her right mind thinks that the prospects for 2026-7 S&P EPS gains are now higher than before the Iranian conflict (and after the rapid increase in energy and other related costs - which will impede demand and raise the costs of goods, adversely impacting margins)?…

— Dougie Kass (@DougKass)

With interest rates staying above consensus expectations and S&P profits below elevated consensus forecasts — the equity risk discount will grow ever larger — providing a backdrop for future greater-than-expected valuation contraction.

I also remain concerned about U.S. foreign policy and what it means for our alliances (trade and political).

These above factors are not valuation friendly and, at the very least will likely constrain the enthusiasm and upside that was demonstrated Tuesday.

While I remain modestly net long in exposure but I start (and, to update, ended) Wednesday much less long than I started Tuesday — given the rapidly changing reward vs. risk prospects, which are an outgrowth of a near +4% advance in the broad averages.My investment strategy will be stay vigilant and to be flexible and opportunistic.

If you put a gun to my head I would say we are in a broadening trading range with a negative bias over the intermediate term (measured in months).

I continue to see 2026 as a negative year for the broad averages— with most rally attempts failing or being constrained by persistent inflation, moderating corporate profit expectations, relatively tight Fed policy (and higher than longer interest rates), inconsistent and poorly framed U.S. leadership/policy and declining valuations.

Position: Long SPY common (M), QQQ common (M); Short SPY calls (M), QQQ calls (M)

BY Doug Kass · Apr 2, 2026, 6:30 AM EDT

The S&P Short Range Oscillator is less oversold at -1.53% vs. -3.92%.

Position: Long SPY common (M), QQQ common (M); Short SPY calls (M), QQQ calls (M)

BY Doug Kass · Apr 2, 2026, 5:45 AM EDT

On rescheduling, Blanche said during his Senate confirmation hearing he would give the issue "careful consideration". Blanche will eventually be replaced with Lee Zeldin, pending Senate approval. Zeldin has backed cannabis banking and protecting state medical cannabis laws.

🌿 Every cannabis investor needs to read this headline carefully. AG Bondi was personally directed by Trump’s Dec 18 executive order to finalize marijuana rescheduling from Schedule I → Schedule III. A new AG means the rescheduling timeline resets — or accelerates. Zeldin’s Show more

*TRUMP HAS DISCUSSED FIRING ATTORNEY GENERAL BONDI: NYT *TRUMP HAS FLOATED REPLACING BONDI WITH EPA CHIEF ZELDIN: NYT

A senior advisor to President Trump tells us the president is “very disappointed with Bondi’s inaction on cannabis rescheduling.” According to the advisor, Bondi says the delay is due to the DEA’s need to ensure everything is done in a legally valid manner, while continuing to

bondi likely to be replaced as attorney general by lee zeldin….

bondi likely to be replaced as attorney general by lee zeldin….

Who in his/her right mind thinks that the prospects for 2026-7 S&P EPS gains are now higher than before the Iranian conflict (and after the rapid increase in energy and other related costs - which will impede demand and raise the costs of goods, adversely impacting margins)? Show more

Remember, nearly EVERY opinion that was confidentally delivered on @cnbc over the last two months were totally wrong: 1. There is economic risk. (The threat to global economic growth is obvious) 2 There is geopolitical risk (Duh!) 3. There is interest rate and inflation risk. Show more

@TheStreet @TheStreetPro The Business Media Has Failed You * Not providing two way discourse/debate (and relying on formulaic programming) has prepared investors poorly for when the halcyon days are over and the tides starts going out... "So much for objective journalism.