BREAKING: President Trump announces that the US will be suspending attacks on Iran for a period of 2 weeks on the condition that Iran will be reopening the Strait of Hormuz.

Axios Reporter Barak Ravid Posts: "White House press secretary Karoline Leavitt tells me: 'The President has been made been aware of the proposal, and a response will come'"

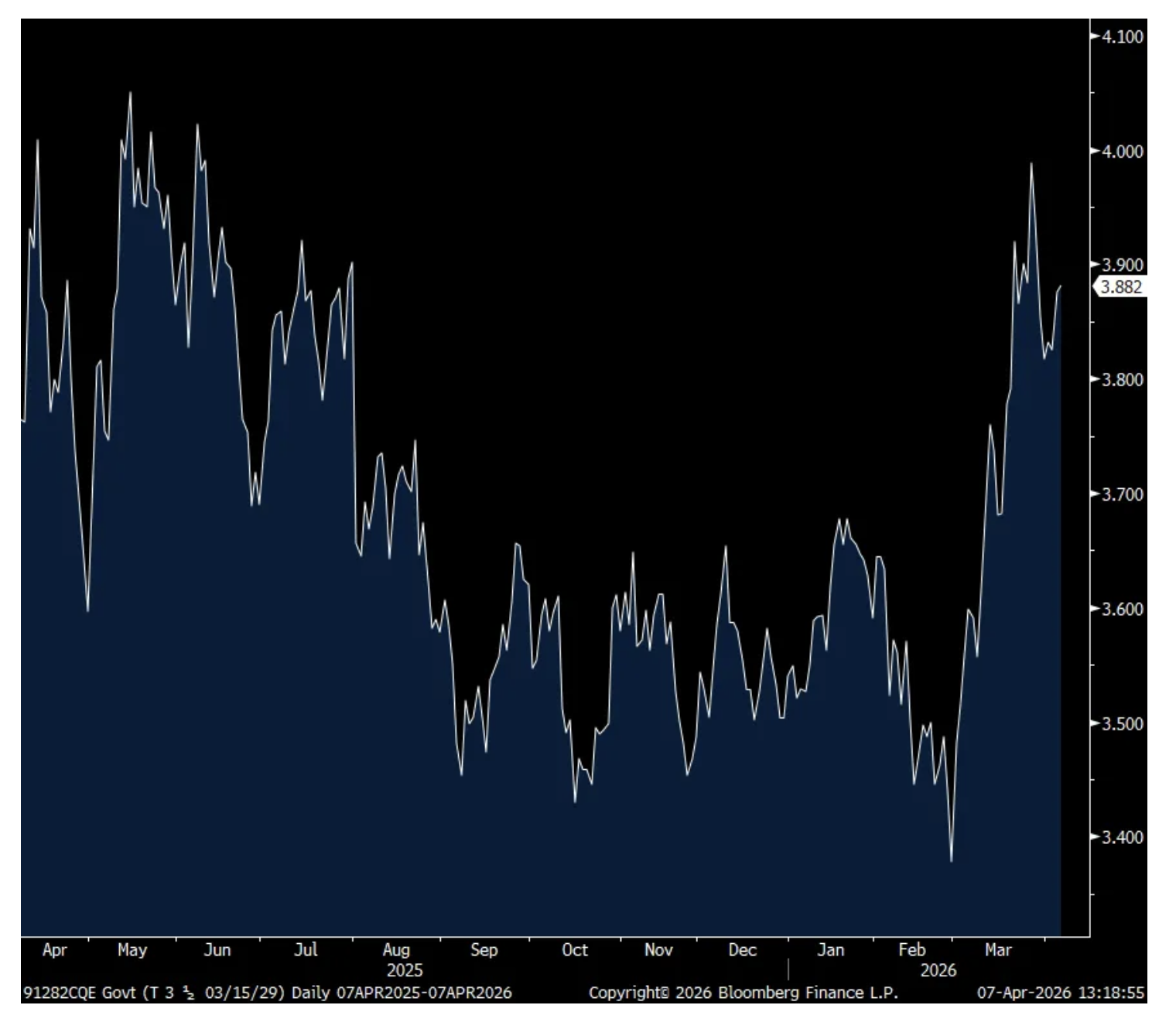

After a slew of bad auctions a few weeks ago, today's 3 yr was fine

Unlike the terrible 2 yr auction two weeks ago (along with a tough week in the 5s and 7s), today’s 3 yr note auction was fine. The yield at 3.897% was just below the when issued. The bid to cover of 2.68 was above the previous 12 month average of 2.61. And, direct and indirect bidders took down 87% of the auction which is about the same as the one year average.

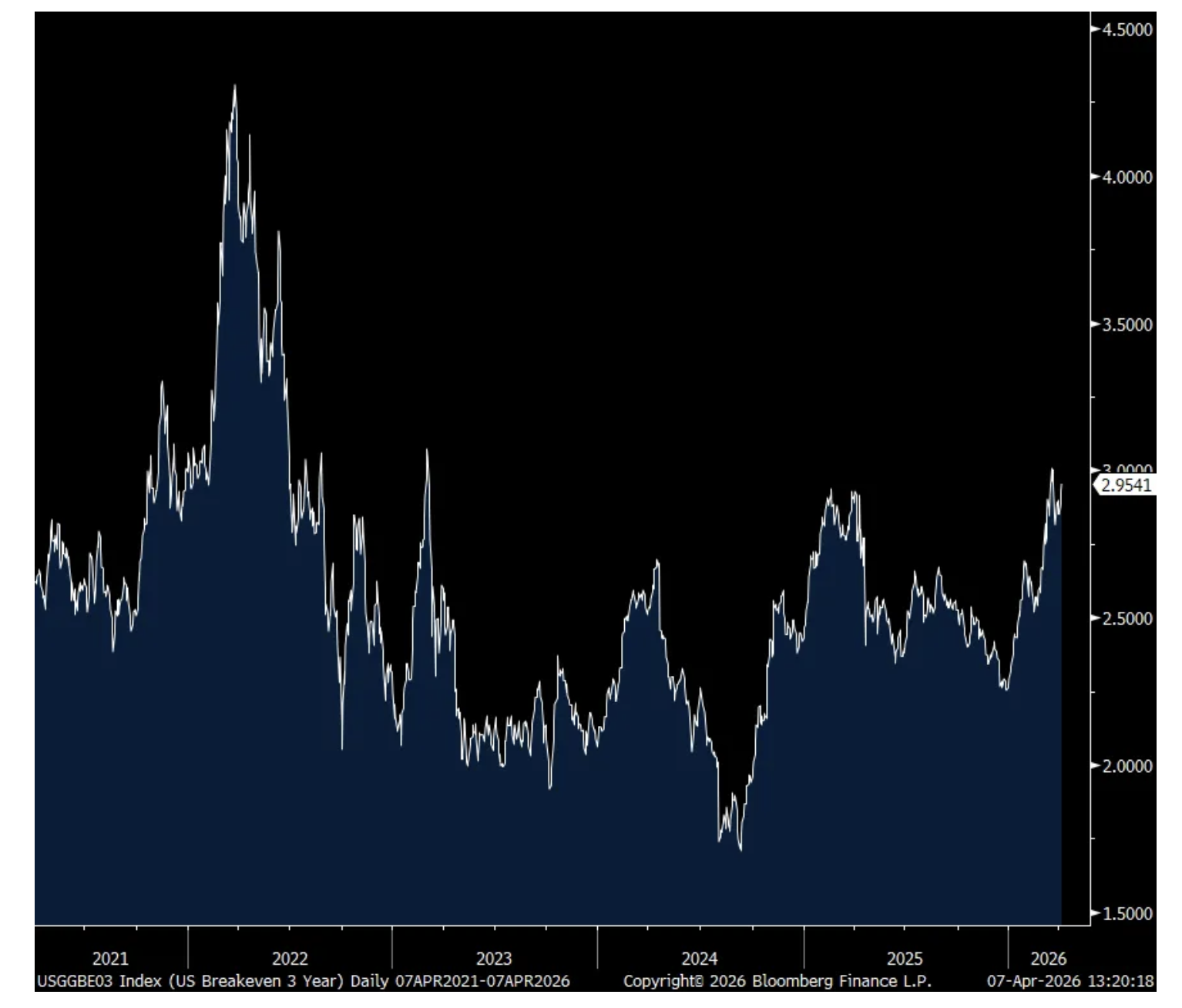

This yield compares with the 3 yr inflation breakeven currently at 2.95%, just off the highest level since March 2023.

Bottom line, a yield near the highest since last summer brought out a decent bid. With respect to those wanting to take more duration risk, tomorrow’s 10 yr and Thursday’s 30 yr will be more telling on risk appetite.

Boockvar on the Scramble for Oil, Coal Prices, China's Treasury/Gold Flip and More

From Peter Boockvar:

So, I guess we just sit and wait

So I guess we now just sit and wait to see what happens, if anything, up until 8pm est tonight and as I write this, I read about explosions on Kharg Island.

In the meantime, countries continue to do what they can do to keep the lights on and transportation moving. Japanese refineries, which procures almost all of its crude from the Middle East, and where the PM is trying to have talks with the Iranian president, are now relying on “ship-to-ship transfers far from the Middle East to secure crude supplies while keeping its tankers out of a conflict zone that has become too risky for crews and vessels” according to a Bloomberg News article. “The Kisogawa, a very large crude carrier (VLCC), is en route to Hokkaido after receiving about 1.2 million barrels of Murban oil from Rio De Janeiro Energy while at sea off Linggi on Malaysia’s west coast on Sunday, ship tracking data show.”https://www.bloomberg.com/news/articles/2026-04-07/japan-relies-on-offshore-oil-transfers-as-middle-east-risks-rise

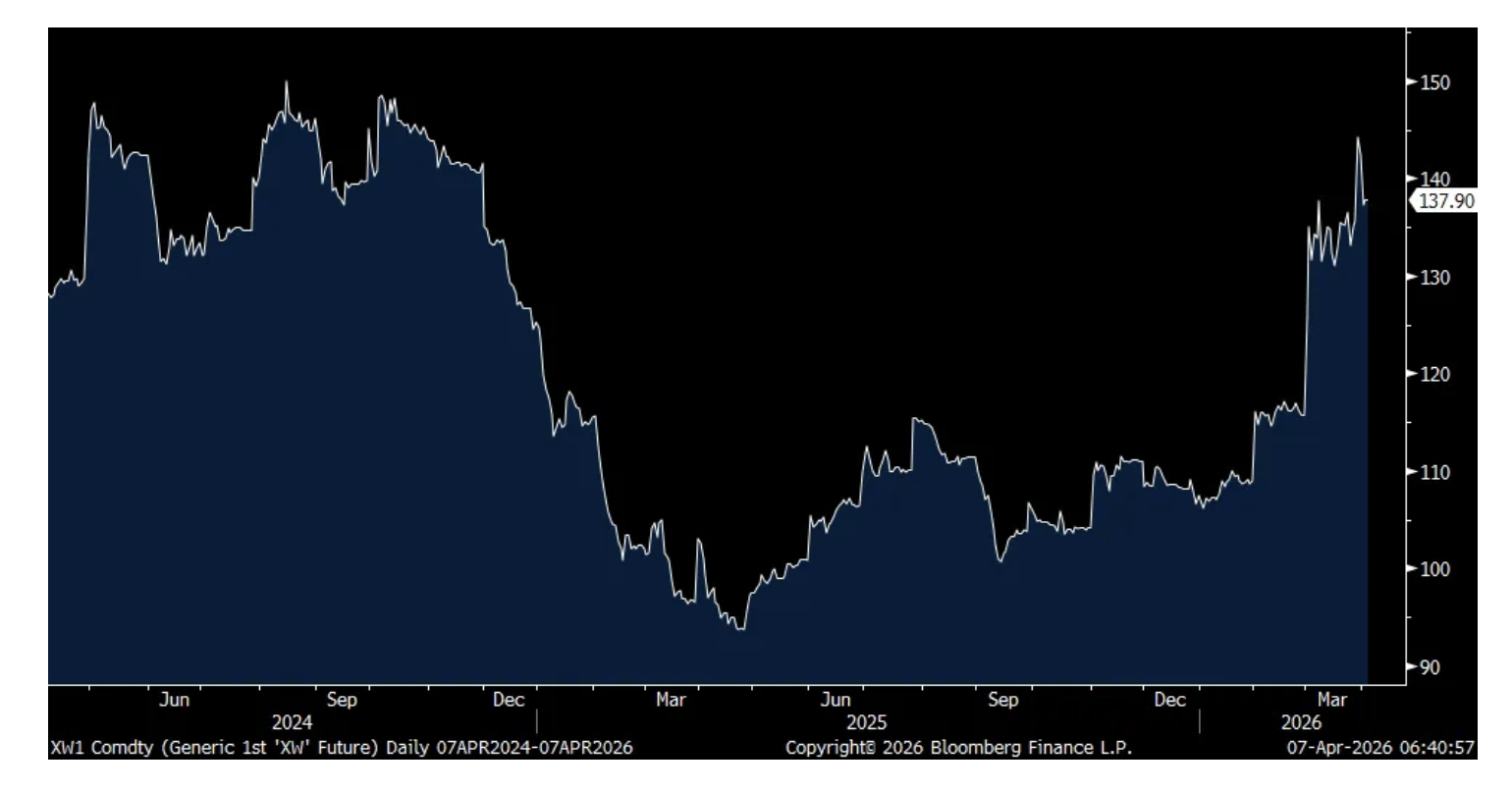

Last week we heard that Germany is turning back on some of its coal plants. Today I read that Taiwan is doing the same, along with other countries ramping up coal plants. Prior to the bombing of the Qatar Ras Laffan LNG facility, Taiwan got about 1/3 of its LNG needs from them and where LNG makes up about half its electricity needs. We’ve been buying shares in more US natural gas companies as their market share will only grow in the coming years via LNG exports and the possibility that Henry Hub natural gas prices catch up to the global price rather than the global price catching down to US prices.

Here is chart of coal prices with Newcastle futures as of yesterday’s close on per metric ton basis:

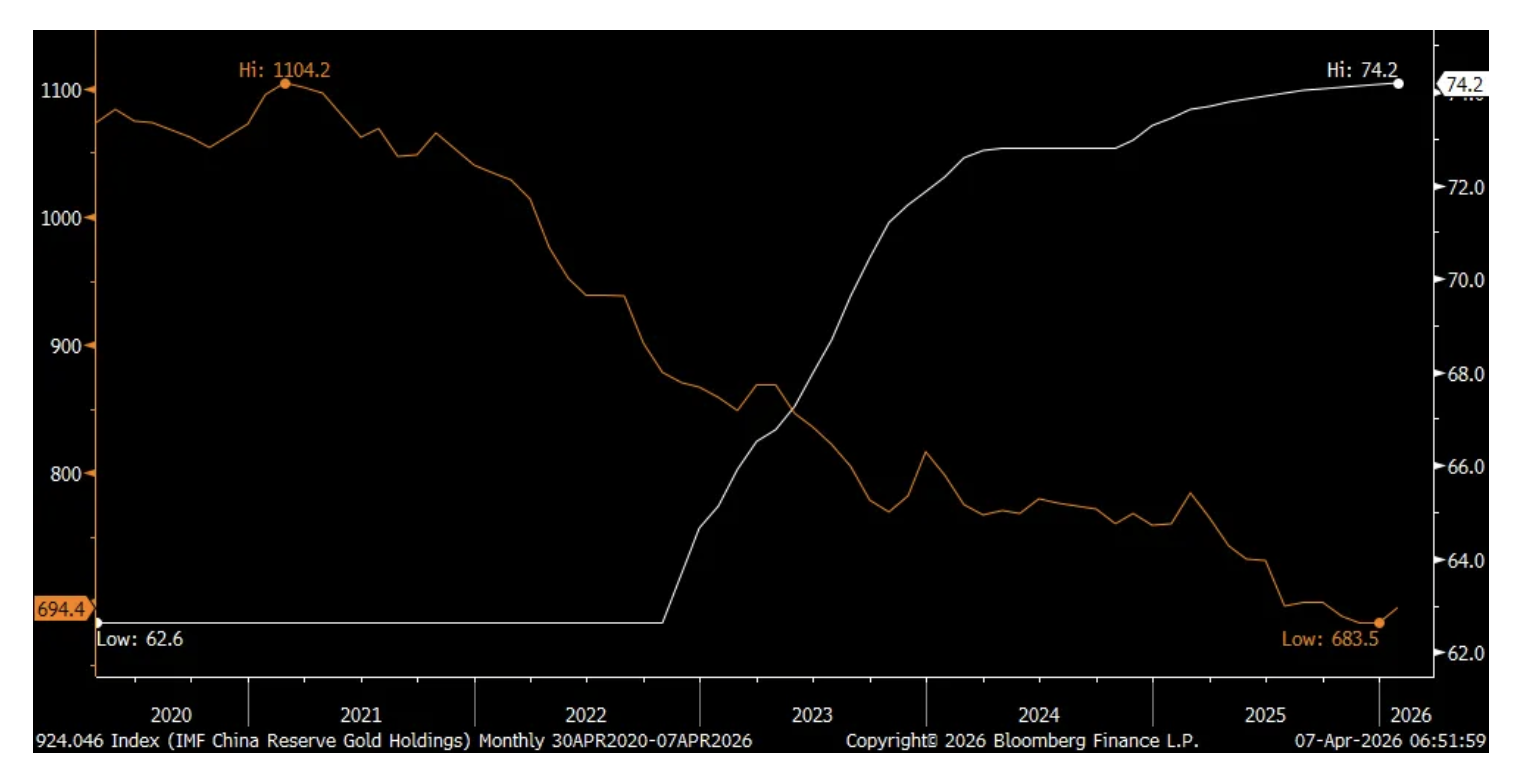

What does China buy as they reduce their holdings of US Treasuries? They continue to buy gold. In March, they took their holdings to 74.38 million troy ounces from 74.22 million in the month before. Notice in the chart how buying picked up steam in 2022. That was in response to the EU and US freezing half of Russia’s central bank reserves. And as foreign official holdings of US Treasuries are around the lowest level since 2012, China has not been the only one making this swap.

China US Treasury holdings in orange in US$ & physical holdings in gold tonnage per ounce in white as of Feb

The final March Eurozone services PMI was left little changed at 50.2 vs 50.1 in the initial print and down from 51.9 in February. S&P Global said “At the national level, economic activity trends were mixed. Spain was the fastest growing country in March, registering an accelerated upturn. Ireland followed closely behind, despite the rate of expansion easing to a six month low. The Eurozone’s largest economy - Germany - continued to see activity growth at the end of the first quarter, albeit with its rate of increase slowing to the weakest in the year to date. Meanwhile, France and Italy recorded contractions.”

Some more, “The encouraging signs of growth seen earlier in the year have been eradicated thanks to surging energy prices, choked supply chains, financial market volatility and a renewed downturn in demand. The accompanying surge in prices raises the unwelcome spectre of stagflation, or worse, in the near term.”

The final UK services PMI for March was 50.5 vs 53.9 in February. S&P Global said “UK service providers experienced a marked slowdown in output growth in March as the war in the Middle East encouraged greater risk aversion among clients and postponed investment decisions.”

Nothing market moving on either as it highlights the obvious changed business environment.

* Though the negatives are accumulating, a few stocks are approaching buyable levels

* "Slugflation" is more likely than ever — with economic growth prospects moderating the pressured part of the K-shaped economy might move into the upper middle class (if equities fall and the negative wealth effect takes hold) just as inflationary pressures are mounting (and the knock-on effect of higher oil prices is felt)

* The equity risk premium has turned into an equity risk discount — portending weak equities ahead

* Improvisational U.S. foreign policy will have a destabilizing impact on our alliances (trade and political)

* For the next few months we see a broadening trading range with a negative bias lower

* But opportunities could emerge in this year's second half, setting up the stage for a good market in 2027

What follows is a compilation of commentary from my Daily Diary on TheStreet Pro and from communications to my hedge fund investors at Seabreeze Partners...

As noted in my commentary of the last few months we have been prepared for the market downdraft by building up our cash reserves.

Many stocks are already down in excess of 25%. As reported in March, we are ready (as individual equities justify purchase) to return to the land of the living and we are open to building up our long exposure.

We expect a very volatile "two-way" market going forward — something we relish as it provides numerous trading and investing opportunities for the opportunistic and dispassionate who have a sense of (intrinsic) value in the averages, in sectors and in individual stocks. This likely market backdrop will be far different than the runaway bull market experienced since late 2022. To quote my Grandma Koufax, a great philosopher, businesswoman and money manager... "the coming market conditions will likely demonstrate the difference (in performance) between 'the men and the boys.'"

Though we still think there is more to go on the downside, selected equities have grown attractive and (as suggested last month) we have moved from a net short exposure to a modest net long exposure in the last two weeks.

Our current gross exposure stands at 80%. Our net exposure (gross longs (45%) less gross shorts (35%)) is about 10% net long. We envision taking our net long exposure higher over the balance of the year.

We remain broadly and conservatively diversified with no individual stock position accounting for more than five percent of our portfolio. Both our longs and shorts generally consist of actively traded (liquid) stocks with large market capitalizations.

Recent new portfolio additions (made in the move lower in the averages) include Fannie Mae (FNMA) , Freddie Mac (FMCC), Meta (META) , Alphabet (GOOGL) , Amazon (AMZN) , Microsoft (MSFT) and Disney (DIS) .

Strategy

While we are of the view that some stocks have reached buyable levels, we are skeptical about the violence of the initial upside move (which was likely exacerbated by short-covering). The breakneck speed in which stocks rose reduced the reward vs. risk opportunities and took away some "margin of safety."

There is still downside risk to economic and corporate profit growth and valuations — and to equity prices.

We will stay patient in building up our long book — waiting for the right pitches.

President Trump's speech last Thursday evening underscored a likely lengthier and drawn-out conflict in Iran (and, with it, heightened and adverse economic ramifications). Indeed, in some ways it bolstered my medium-term economic and investment concerns.

While the war in Iran will eventually will be "resolved," the impact will be to have knock-on consequences to economic growth (weaker), inflation (stronger and more persistent), tighter-than-expected (Fed) monetary policy (so interest rates will be "higher for longer") and produce something of a supply shock (for a vast array of critical materials and products).

Oil is the spark, but inflation is the fire. And once it spreads, it's much harder to contain:

With inflation already elevated before the Iran conflict, "slugflation" (sluggish economic growth and persistent inflation) is now almost guaranteed to be a semi-permanent condition.

Oil is a tax on consumption and the problem is that we now have to get comfortable with the notion of higher oil prices for longer.

"I have written for years that oil prices act like a tax on the economy, both on the US and globally. It is actually simply the price paid, but the effect on the economy is similar to a tax. If the price goes up, it takes more money from individual consumers that would otherwise be saved or spent somewhere else. Just like taxes.

The growth of the global economy is really the growth in energy and how we use it. When energy become scarce or high-priced it is necessarily going to reduce global GDP. It will reduce GDP much more in some countries than others, depending on their need for both energy and its related products like fertilizers, plastics, and all the things that energy produces.

The Strait of Hormuz is a big deal. About 20% of the world's oil consumption, 20% of LNG and 25% of seaborne oil trade passes through the Strait of Hormuz."

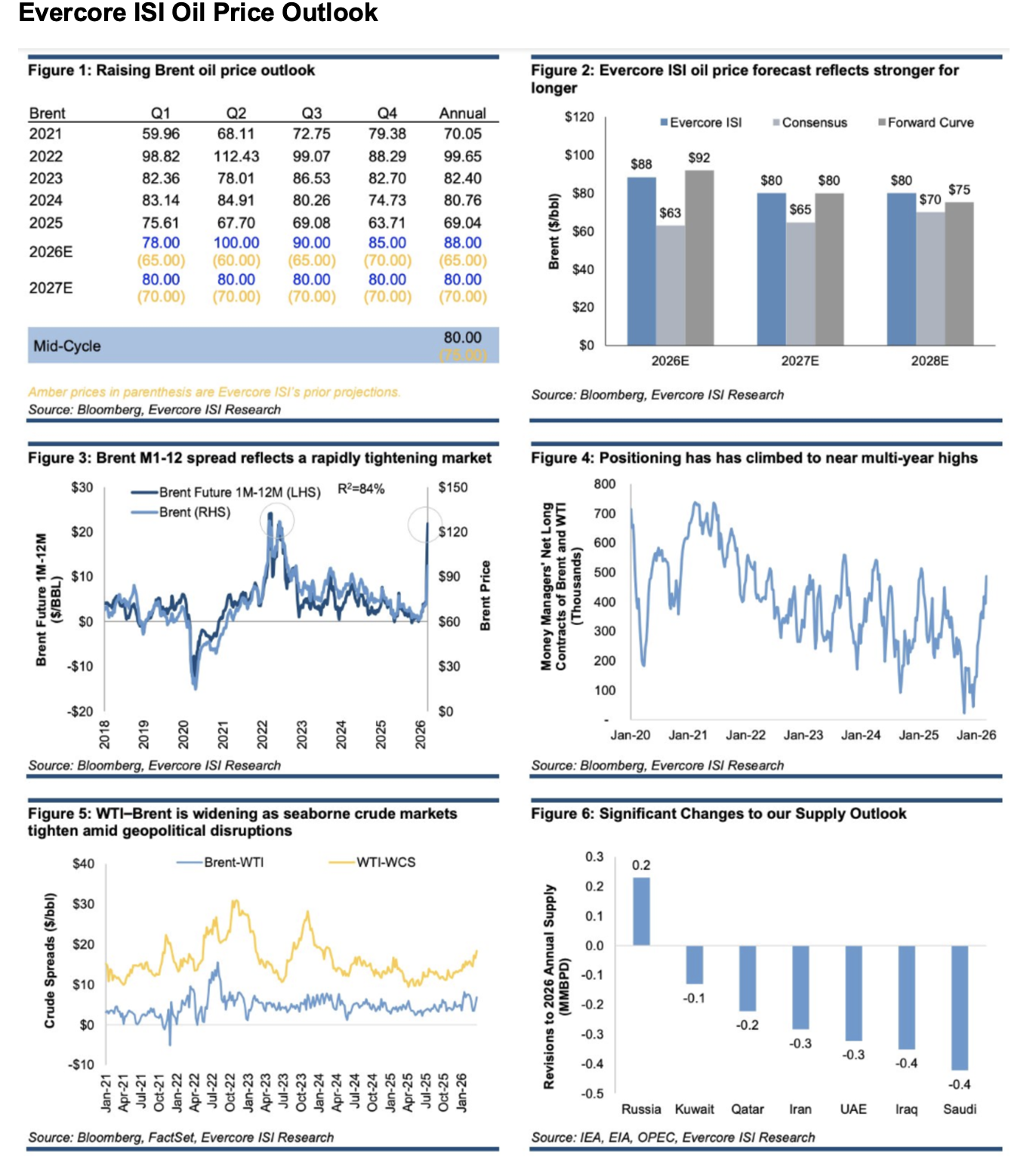

Here is Evercore ISI's oil price forecast:

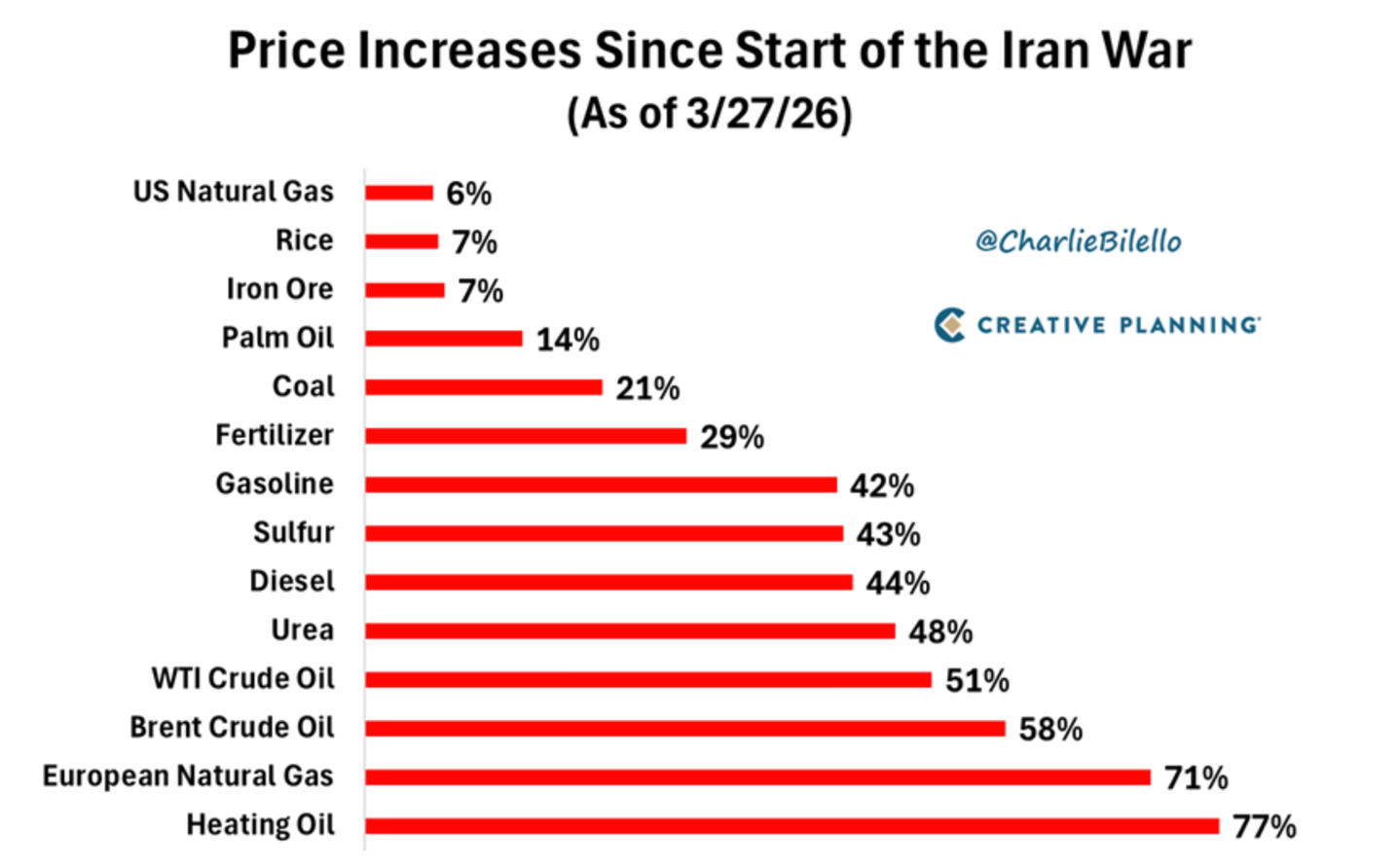

Since the beginning of the conflict with Iran on February, 28 2026, American drivers have paid an additional $8.4 billion in fuel costs — representing an additional $240 million per day. The average cost of a gallon of gas in the U.S. is now up to $4.10/gallon, the highest since June 2022. This puts the cost of gas up +$1.30/gallon since January 2026.

The bottom and the middle of the K-shaped U.S. economy are bound to be even more pressured in the months ahead as general affordability is materially threatened by a weakening jobs market and stubbornly higher costs (and inflation). Should stocks continue to fall, the negative wealth effect will begin to impact the upper middle class and the rich.

Importantly, consensus corporate profit growth expectations (of about +15% year over year) will likely have to be ratcheted down despite protestations from the cabal of (ostrich-like) perma-bulls.

With interest rates staying above previous expectations and S&P profits below elevated and unrealistic consensus forecasts — the equity risk discount has grown ever deeper — providing a possible backdrop for a future greater-than-expected contraction in valuations.

We continue to remain concerned about the systemic risks associated with the private equity and credit industries. For three years I was a member of the Board of Directors of a business development company listed on the New York Stock exchange where I saw what everyone knows is going on now — that private equity/credit are remarkably proficient at kicking the can down the road (as assets are marked to model and myth but not to reality and market). However, it looks (to me and to others) that the likely the end of the road is near.

I also remain concerned about the destabilizing impact of improvisational U.S. foreign policy and what it means for our alliances (trade and political).

While some stocks have become attractive, the factors listed above are not valuation friendly and, at the very least, will likely constrain the enthusiasm and upside that was demonstrated in the middle of the past week.

Bottom Line

As noted earlier, Seabreeze is modestly net long in exposure.

Given the rapidly changing reward vs. risk prospects, which are an outgrowth of a near +4% advance in the broader averages (from recent lows), our investment strategy will be to stay vigilant, flexible and opportunistic.

If forced to make a forecast for the next six months, I would suggest that we are likely in a broadening trading range with a slightly negative bias. This anticipated backdrop will be fertile with both trading and investing opportunities.

Despite the emergence of individual equity opportunities, I continue to see 2026 as a negative year for the broad averages — with most rally attempts failing or being constrained by persistent inflation, moderating corporate profit expectations, relatively tight Fed policy (and higher for longer interest rates), a ballooning U.S. debt load, inconsistent leadership and poorly framed and impromptu policy (without previous thought and analysis) and declining valuations.

Depending on the nature of the emerging economic fundamentals and the direction of stock prices, we might be setting up for an excellent buying opportunity during the second half of this year — setting the stage for a much better stock market in 2027.

Position: Long FNMA (VS), FMCC (VS), META (S), GOOGL (S), AMZN (S), MSFT (S), DIS (S)

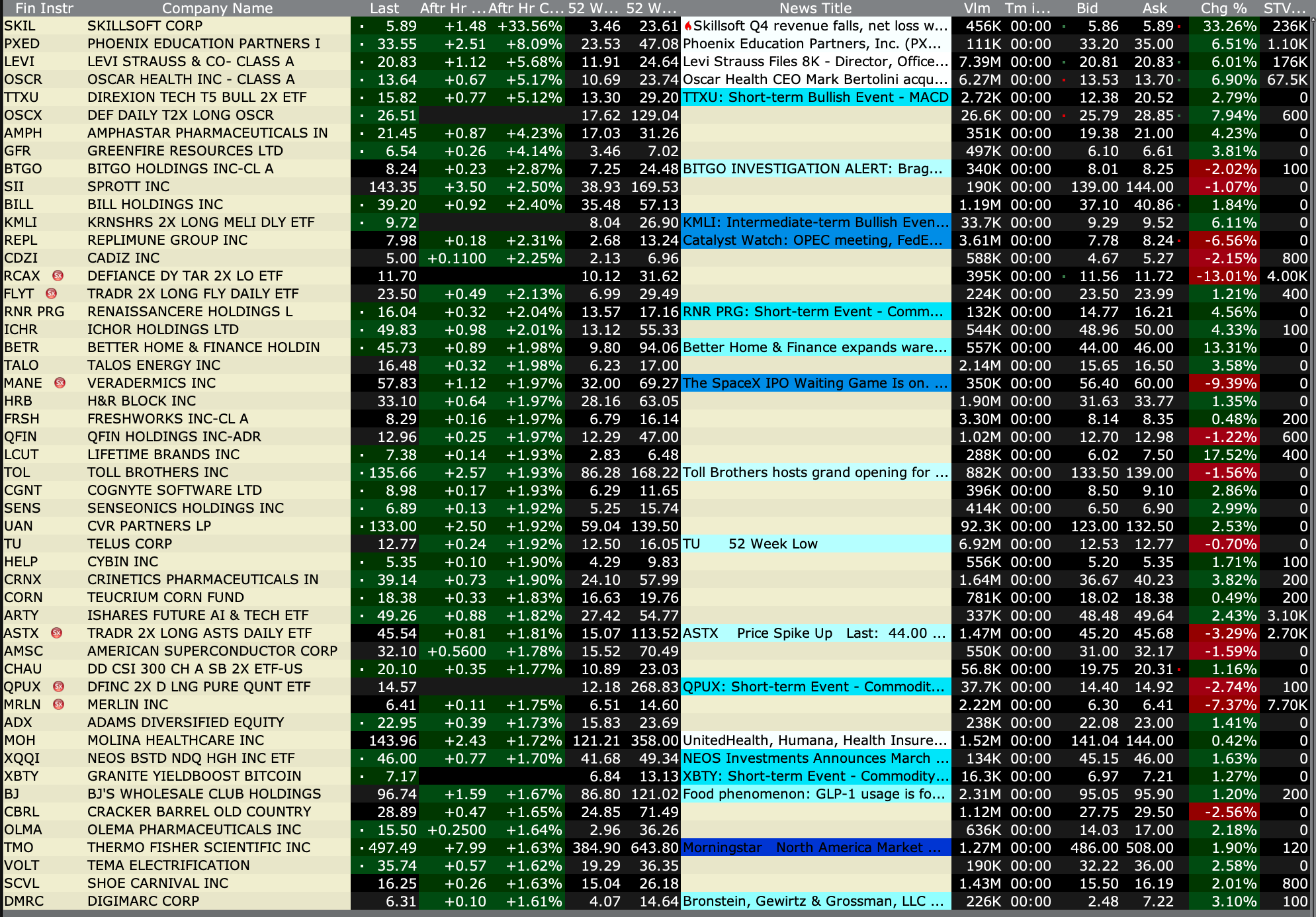

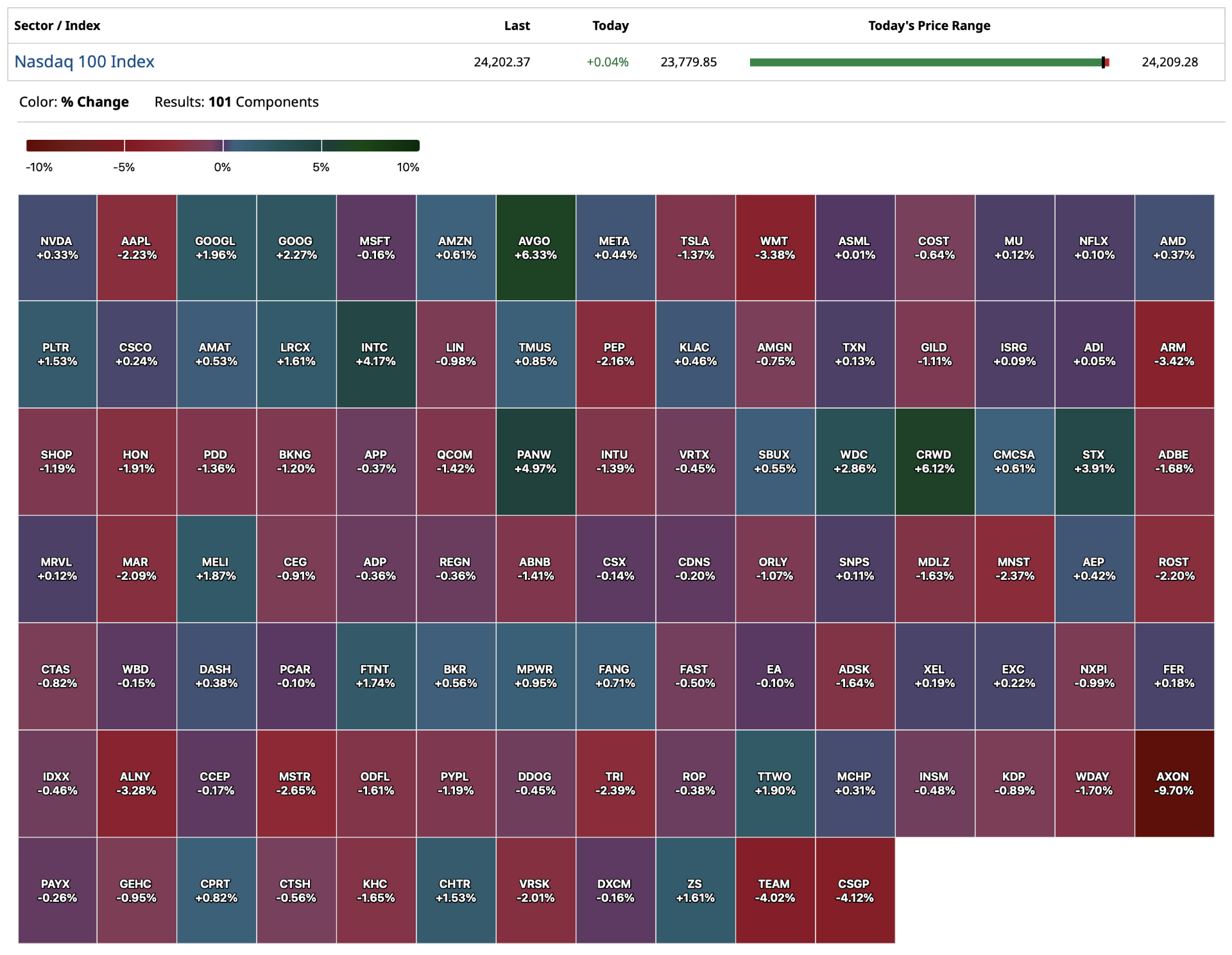

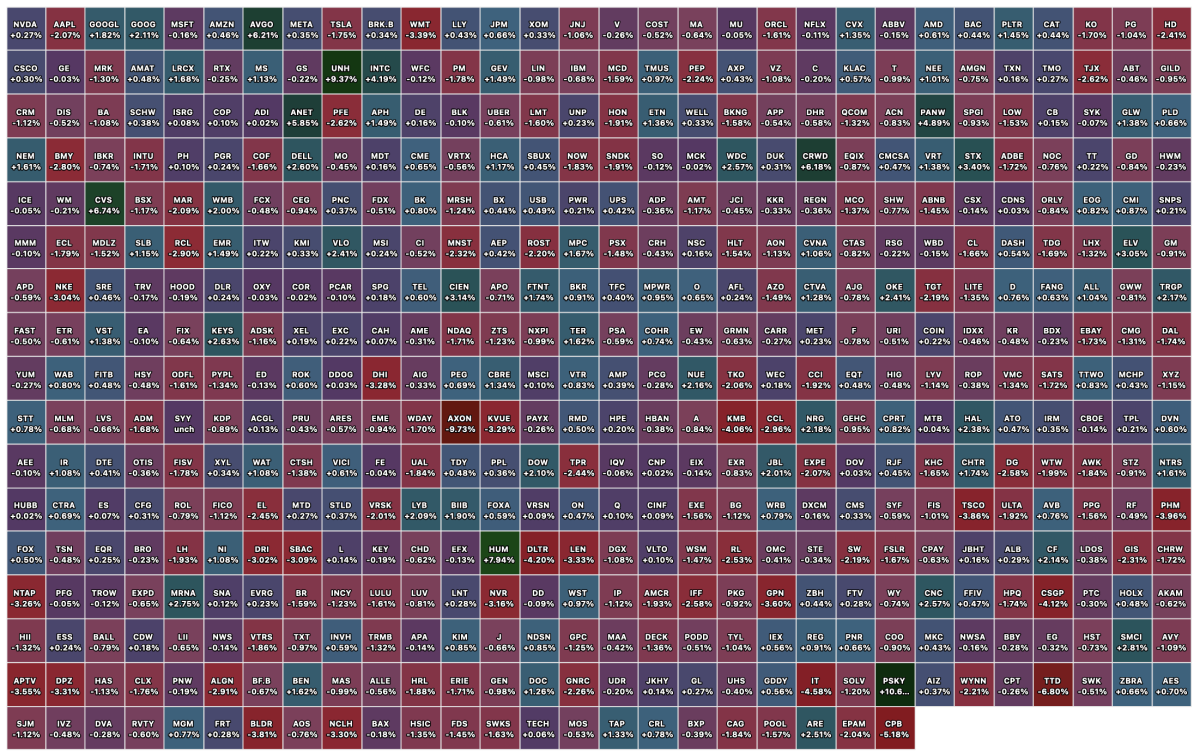

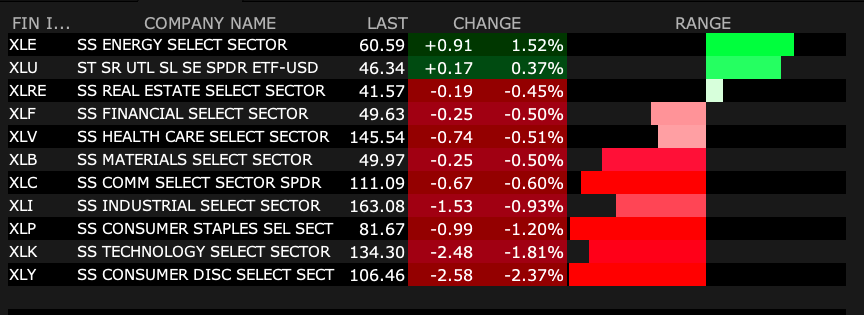

-UNH +6.9% (CMS completes 2027 Medicare Advantage and Part D payment policies; health insurers higher on higher MA payments)

-CVS +6.7% (CMS completes 2027 Medicare Advantage and Part D payment policies; health insurers higher on higher MA payments)

-FUBO +5.5% (hearing Barrington Research upgrade)

-ACIU +3.7% (amended 2018 license and collaboration agreement with Lilly to continue research and development of Tau aggregation inhibitor small molecules for Alzheimer's disease and other neurodegenerative diseases, covering new lead Tau Morphomer candidates and potential back-up compounds)

-AVGO +2.6% (expands Google and Anthropic AI agreements)

Downside:

-XXII -11% (announces update on advancement of a 100Mm VLN reduced nicotine content cigarette)

-MNR -9.4% (prices 9M secondary public offering of common units at $13.05/share)

-ARM -4.1% (Morgan Stanley Cuts ARM to Equal Weight from Overweight, price target: $150 from $135)

-MRVL -3.1% (COO sells 10K shares)

-HIMS -2.0% (CFO plans to sell ~$5M in stock)

-LEN -2.0% (Seaport Global Securities Cuts LEN to Sell from Buy, price target: $74)

1:45PM: Fed Bank of Chicago President Goolsbee (Non-Voter) Radio Appearance -- WJR-AM;

5:50PM: Fed Vice Chair Jefferson (Voter) speaks on the economic outlook and the labor market before the University of Detroit Mercy College of Business Administration Charlton Center for Responsible Investing Speaker Series, Detroit, MI (Text available. Audience Q&A expected. No webcast);

7:00PM: Fed Bank of San Francisco President Daly (Non-Voter) participates in Fox Business interview

.. US budget deficits likely “grow to ~7% of GDP for 2026. Even if the amount of the supplemental request were halved to $100bn, deficits could grow to ~6.6% ..” pic.twitter.com/fVC6QpbqzB

For the many reasons I have mentioned in columns on @thestreetpro... the "cash on the sidelines" is a B.S. argument that often surfaces during maturing Bull Markets as Bulls run out of arguments... @dougkasshttps://t.co/LwDUn0DsCp

S and P futures -20 handles, Nasdaq futures -99 handles Back buying and moving from delta equivalent short to delta equivalent long: SPY $657.13 QQQ $586.12 910 PM

From earlier this afternoon: Profits From Opportunistic Trading Can Add Up! I just sold off the indices I bought less than two hours for a small profit — moving me slightly net short (from slightly net long) indices:

Sale prices:

* (SPY) $658.18 * (QQQ) $588.06

Position: Long SPY common (M), QQQ common (M); Short SPY calls (M), QQQ calls (M)

Vice President JD Vance reportedly is advising President Trump to accept Iran's surprisingly reasonable 10-point peace plan and end the Iran war. Trump responded by sending Vance to Hungary on the eve of the expiration of his deadline to re-open the Strait of Hormuz. https://t.co/bp3b2OCJrT

#Iran War Update No. 38 (focus on Iranian strategic narrative):

🔹Iran has rejected a U.S.-backed temporary ceasefire proposal and instead outlined its conditions for a permanent end to the war. This is consistent with Iran’s position since the beginning of the conflict, whereby…

— Hamidreza Azizi (@HamidRezaAz)

and...

BREAKING: President Trump might delay his Tuesday 8 PM ET deadline on Iran “if he sees a deal is coming together,” per Axios.

This would mark the 5th time President Trump has delayed his ultimatum.

— The Kobeissi Letter (@KobeissiLetter)

and...

BREAKING: Negotiators are “pessimistic” Iran will bend to meet President Trump’s demand to reopen the Strait of Hormuz before his Tuesday-night deadline, per WSJ.

This is “paving the way” for the US to target Iranian bridges and power plants in a fresh escalation of the war.…

PIMCO:

.. US budget deficits likely “grow to ~7% of GDP for 2026. Even if the amount of the supplemental request were halved to $100bn, deficits could grow to ~6.6% ..”

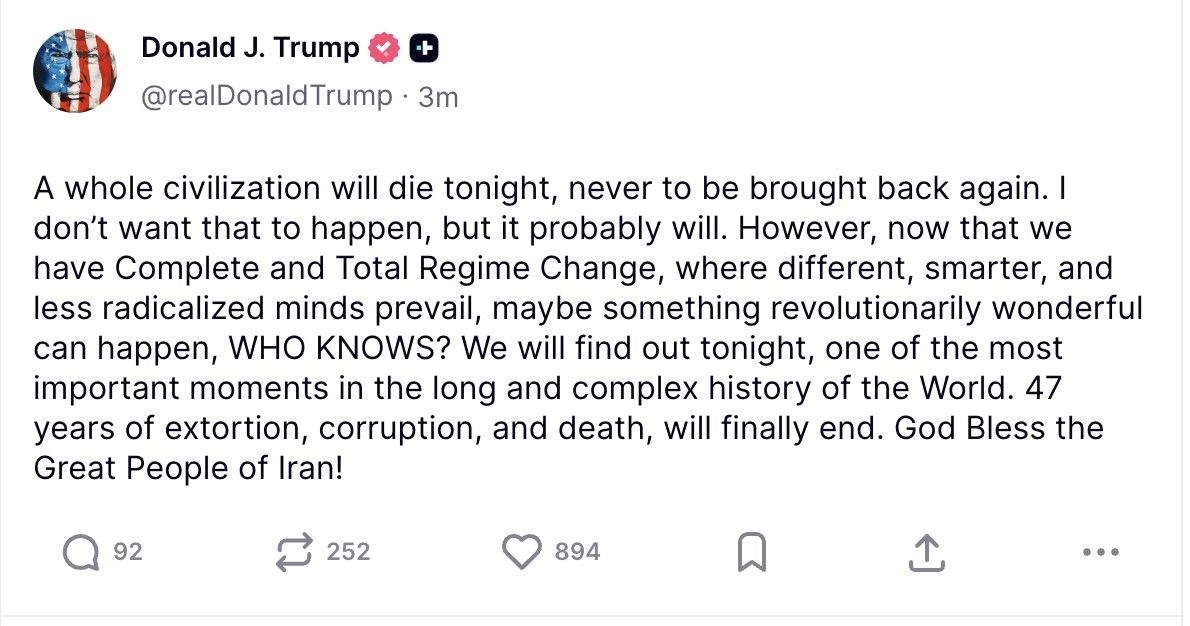

BREAKING: President Trump announces that the US will be suspending attacks on Iran for a period of 2 weeks on the condition that Iran will be reopening the Strait of Hormuz.

"This will be a double sided ceasefire," Trump says.

BREAKING: A deal is "expected to be closed" between the US and Iran tonight, per CNN.

Details include:

1. A "regional source" has informed CNN that "some good news is expected from both sides soon"

2. Discussions are being steered directly by Pakistan’s army chief, FieldShow more

$SPX up 4.5% off last week's lows, but has anything changed yet? 6600-6650 an area for potential sellers to load up and push the bulls back.

@SchwabTrading@SchwabNetwork#SchwabCoaching

*not a recommendation

BREAKING: President Trump might delay his Tuesday 8 PM ET deadline on Iran “if he sees a deal is coming together,” per Axios.

This would mark the 5th time President Trump has delayed his ultimatum.

BREAKING: Negotiators are “pessimistic” Iran will bend to meet President Trump’s demand to reopen the Strait of Hormuz before his Tuesday-night deadline, per WSJ.

This is “paving the way” for the US to target Iranian bridges and power plants in a fresh escalation of the war.Show more

#Iran War Update No. 38 (focus on Iranian strategic narrative):

🔹Iran has rejected a U.S.-backed temporary ceasefire proposal and instead outlined its conditions for a permanent end to the war. This is consistent with Iran’s position since the beginning of the conflict, wherebyShow more

Re: the S&P 500, what a mess.

A primary uptrend can't resume until new ATH's.

A downtrend can't emerge until < 6,316.

Not jumping above last week's high today is a bit ominous.

T-Bill & chill looks pretty to me - paying up (opportunity loss) for a degree of directionalShow more

For the many reasons I have mentioned in columns on @thestreetpro... the "cash on the sidelines" is a B.S. argument that often surfaces during maturing Bull Markets as Bulls run out of arguments... @dougkass

Barchart

@Barchart

$8.2 Trillion is now sitting in money market funds, an all-time high 🚨🤑

Vice President JD Vance reportedly is advising President Trump to accept Iran's surprisingly reasonable 10-point peace plan and end the Iran war. Trump responded by sending Vance to Hungary on the eve of the expiration of his deadline to re-open the Strait of Hormuz.

Mario Nawfal

@MarioNawfal

WOW...

Vance, Witkoff, and Kushner are reportedly now pushing Trump to take a deal with Iran, according to Axios.

On the other side? Surprise, surprise: Netanyahu and Lindsey Graham.