A bunch of data but I tried to get to the most relevant points

It’s somewhat dated data but the January national home price index from S&P Cotality slowed to a .9% y/o/y price gain. I welcome a slowdown in home price increases and even believe that home price declines are what is needed in order to jump start the pace of transactions, especially as mortgage rates reverse higher again. On the flip side of course, no homeowner, including myself, wants to see a drop in the value of their biggest asset for many and this is the market dilemma right now.

The worst markets were those that have had the most amount of building over the past few years, Tampa, Denver, Dallas, Phoenix and Miami. The best market was New York City with prices up 4.9%, followed by Chicago, Cleveland, Minneapolis, and Boston.

Home Price Index y/o/y

The March Chicago manufacturing index fell by 5 pts m/o/m but held above 50 at 52.8. The estimate for this very volatile data point was 55. I don’t have the press release yet to give any details under the hood. Overall, the regional manufacturing indices have been pretty mixed but of course now under another set of uncertainties with the war and rise in material costs, particularly energy. Tomorrow’s national ISM is expected to be little changed m/o/m at 52.3.

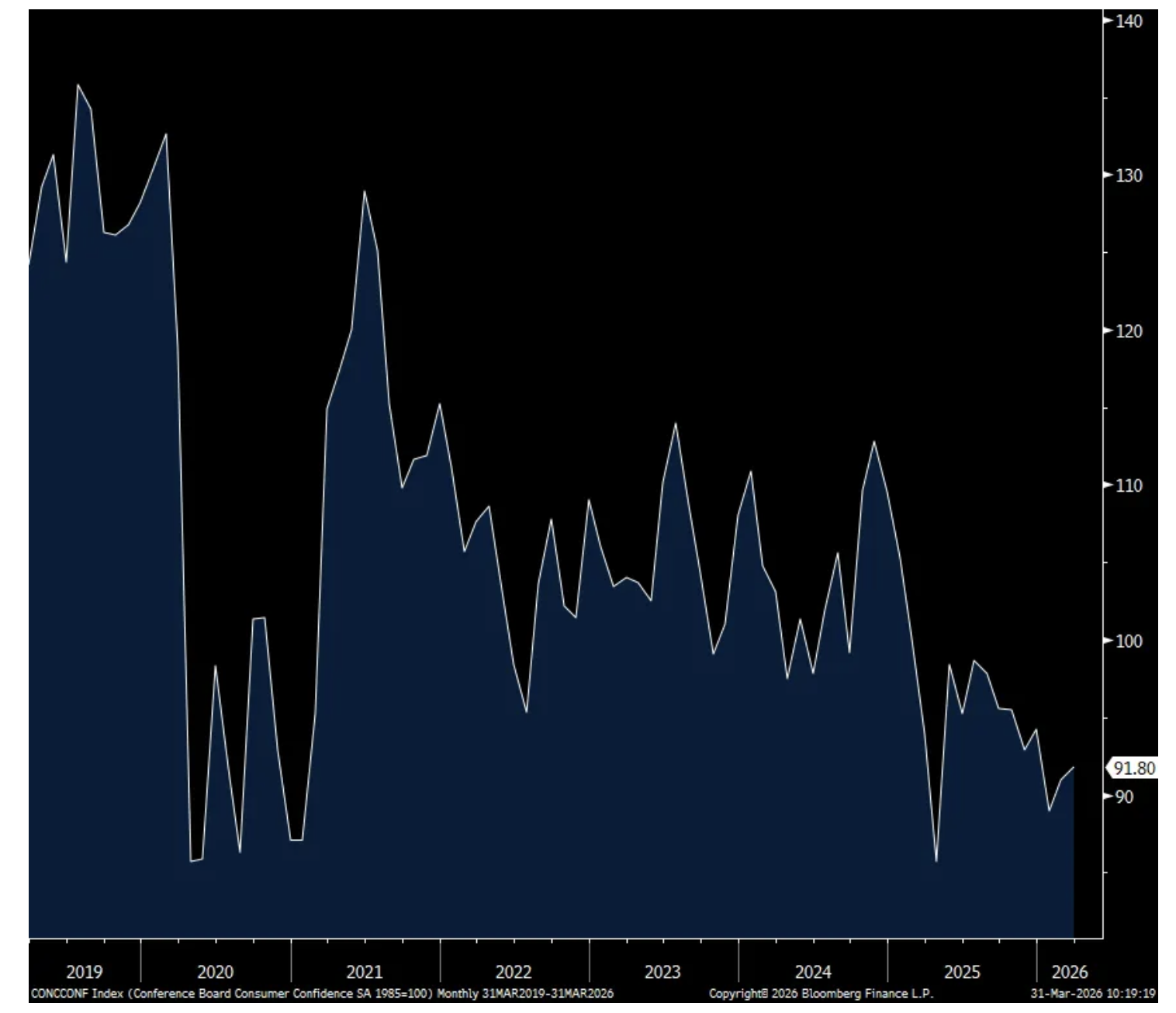

The March Conference Board consumer confidence index was steady at 91.8 relative to the February print of 91 but the internals were mixed as the Present Situation rose while Expectations fell. Overall, the level of confidence is still relatively depressed.

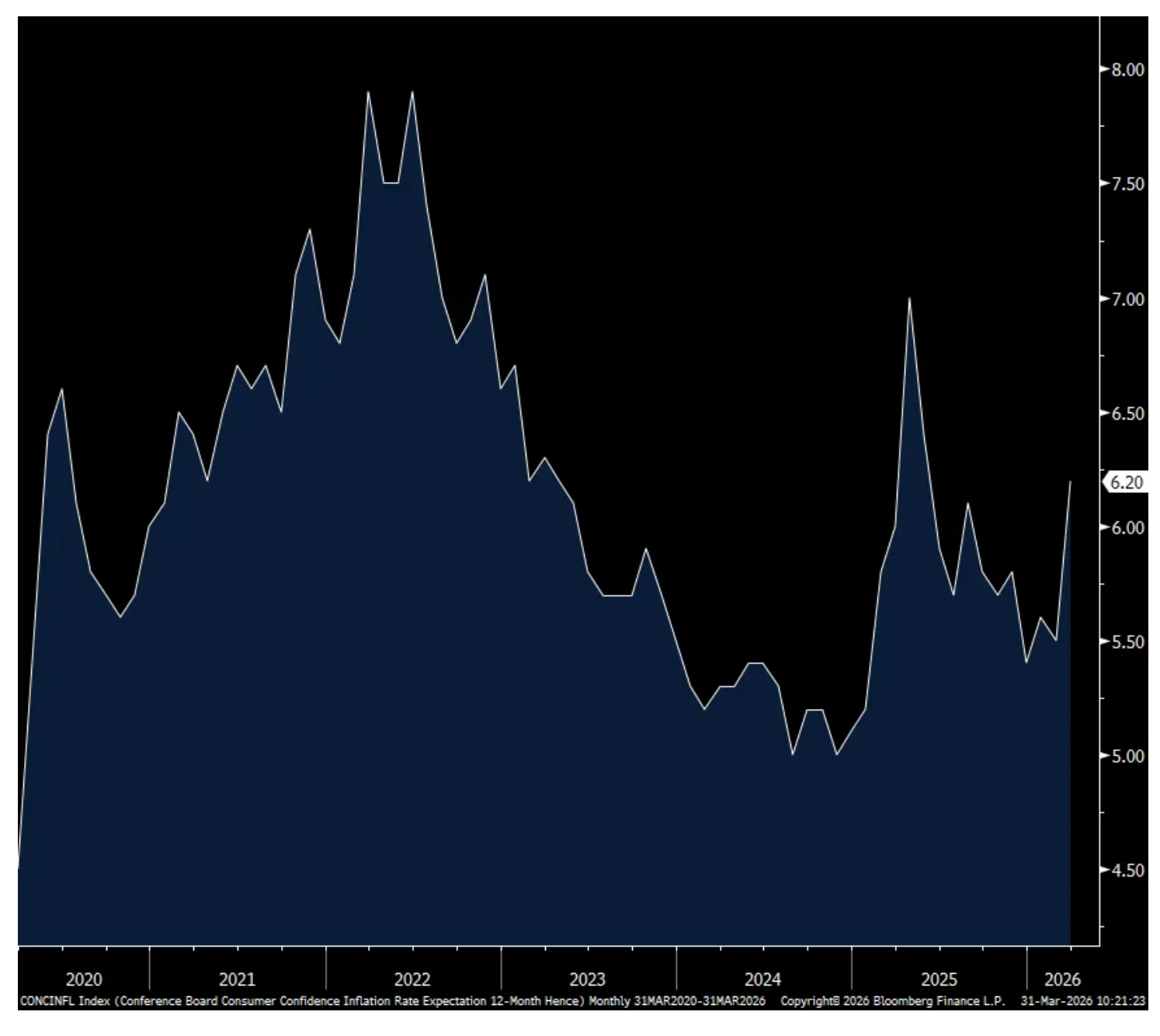

In the face of the jump in gasoline prices, one year inflation expectations rose to 6.2% from 5.5%, that’s the highest since last May.

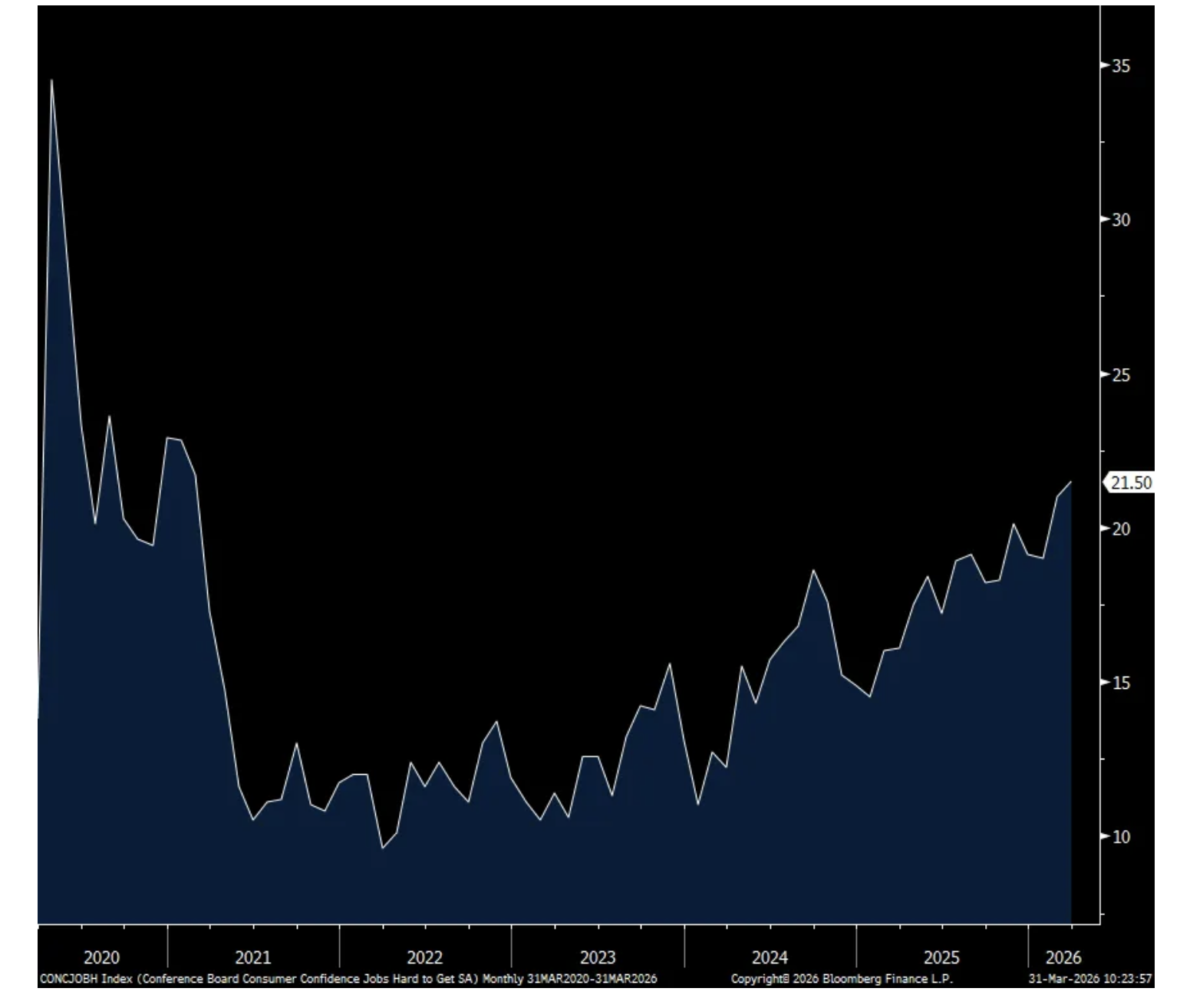

The labor market responses were also mixed. Those that said jobs were Plentiful rose .6 pts to a 3 month high but those that said jobs were Hard to Get was up .5 pt to the highest since February 2021. With respect to expectations for ‘more jobs’ in the coming six months, it fell .6 pts after rising by 1.2 pts in the month before. Income expectations did though improve.

Spending intentions were little changed with autos up slightly, home buying down a bit and major appliances uneven. More on this from the Conference Board, “Consumers’ plans to buy big-ticket items over the next six months shifted from “yes” and “maybe” in February, to “no” in March. Nonetheless, the proportion saying “yes” remained well above the other responses. Used cars, furniture, TVs, and smartphones remained the most popular items within their respective categories for future purchases. Among all expensive items, furniture persists as the top expected purchase.”

With respect to services, “Consumers planning more spending on services over the next six months also shifted from “yes” and “maybe” to “no.” Consumer spending trends in 2026 remain focused on “cheap thrills” and necessary services, and away from expensive and highly discretionary activities…Despite dipping in the month, restaurants/bars/take-out remained the top category for expected spending ahead, still followed by streaming/internet/mobile services and beauty and personal care.”

To the obvious change in the macro, the Conference Board said this, “While not obvious in the headline or its component indexes, the weight of rising costs due to tariff passthrough and spiking oil prices was evident among other measures in the survey like inflation expectations.”

Also, “Consumers’ write-in responses on factors affecting the economy continued to skew towards pessimism. Comments about prices and the cost of goods suggest that the cost of living remained at the top of consumers’ minds. As the war in Iran overlapped significantly with the survey sample period, comments about oil/gas and war/conflict spiked, while specific mentions of trade and tariffs decreased notably.”

Bottom line, nothing market moving here and not a surprising response to what is going on, particularly at the pump.

Consumer Confidence

One Yr Inflation Expectations

Jobs Hard to Get

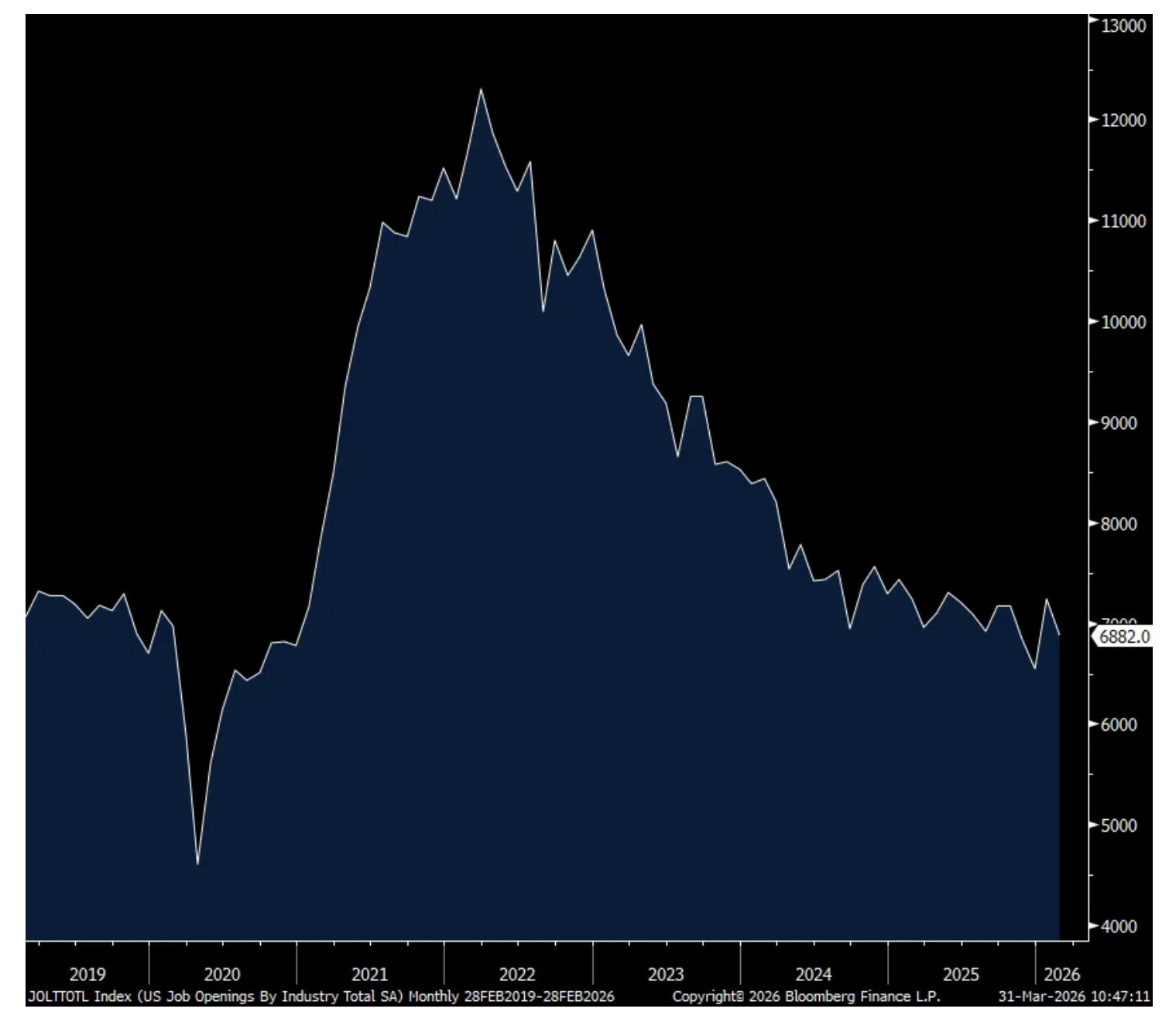

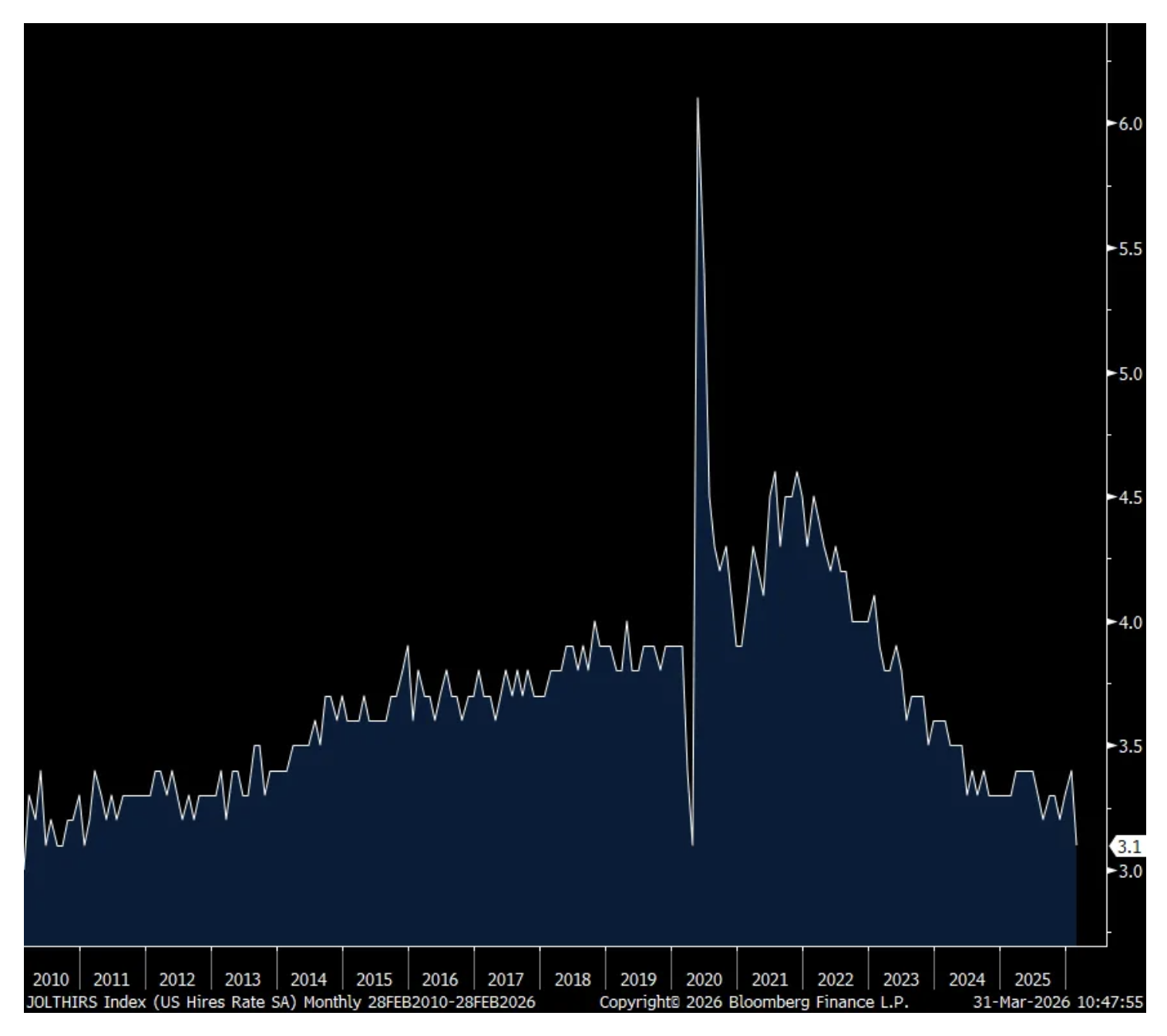

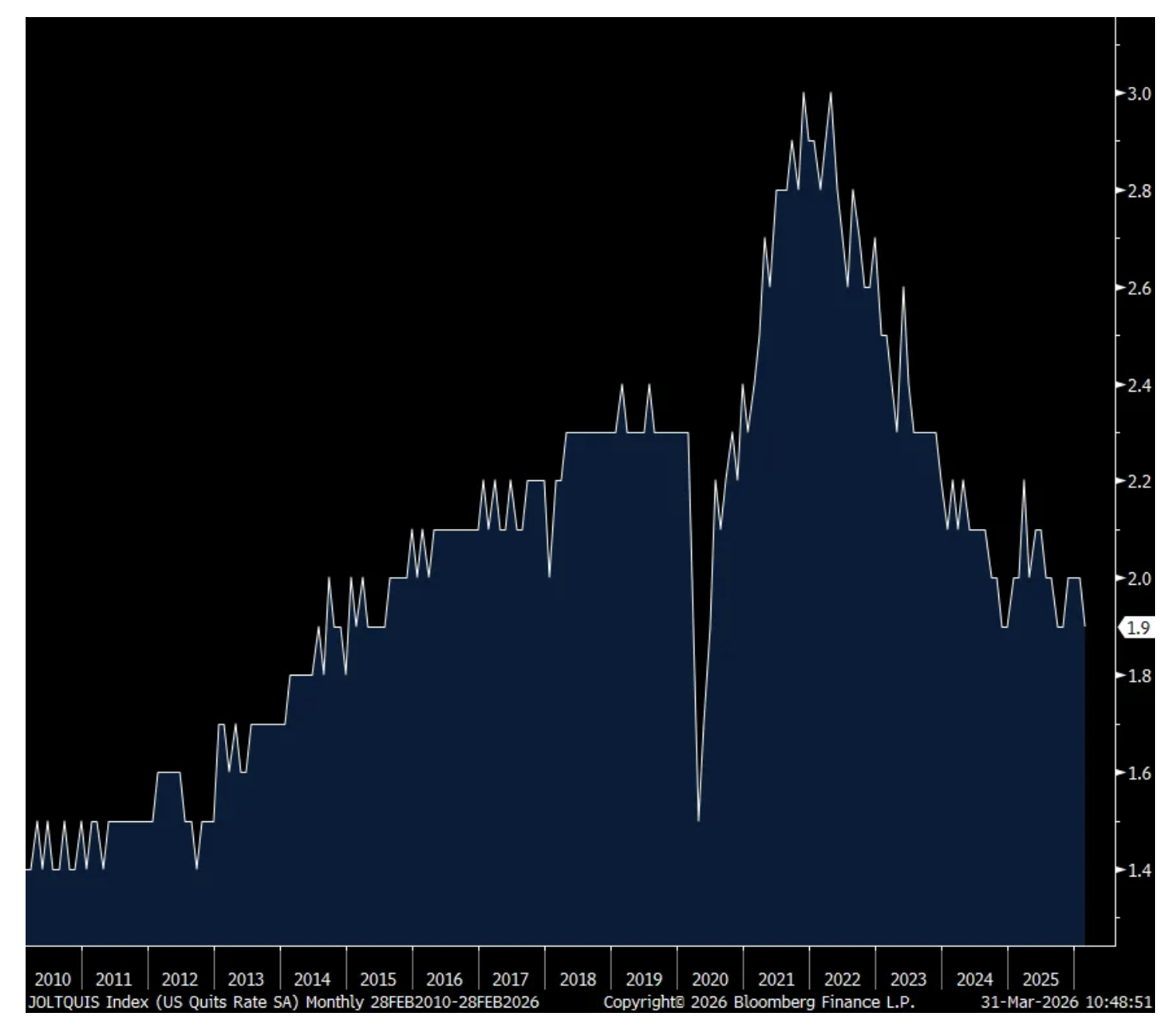

Lastly, with respect to the labor market in February right before the war began, job openings totaled 6.882mm, down from 7.24mm in January which was revised up by about 300k. Of particular note, the hiring rate fell to just 3.1%, down from 3.4% in the month before and that is the lowest since February 2010 not including Covid. The quit rate fell to the lowest since 2015, also not including Covid, at 1.9%, down one tenth m/o/m.

Bottom line, further evidence of the slowdown in the demand for labor.

In the first real precedent of tobacco companies taking an equity stake in cannabis — BAT has elected to convert its debenture into CWEB common (and is investing an additional $10 million — which will take its ownership to 40%).

Who in his/her right mind thinks that the prospects for 2026-7 S&P EPS gains are now higher than before the Iranian conflict (and after the rapid increase in energy and other related costs - which will impede demand and raise the costs of goods, adversely impacting margins)?…

All Too Often Missed Opportunities Are in Plain Sight

* The potential rewards in cannabis equities now dwarf the possible risks.... that asymmetry is being overlooked by investors

"Our greatest regrets in life tend not to be the things we did wrong or failed to achieve; but rather the missed opportunities or things we didn't do that we wish we had."

- Anoir Ou-chad

More than any time in history, the cannabis industry's potential investment setup may be providing an unprecedented investor opportunity (7) X as the upcoming developments in the sector could mark the most exciting period that the major multi state operators and investors have faced in years.

It is underappreciated that as we move ever closer to rescheduling ... that we will likely move ever closer to merger and acquisition activity in the cannabis space, where compelling "merger of equal" (within the cannabis industry) will deliver sizable cost saves. As well, consumer products, pharmaceutical, tobacco companies as other industries may view the ridiculously low cannabis enterprise values as takeover fodder and an inexpensive way of capturing cannabis' sizable addressable market.

Of greater importance, the improving legal outlook (rescheduling, followed by uplistings and freeing up of custodian issues) coupled with (as noted two weeks ago) the recently successful scaling of the "refinancing cliff" (at very attractive interest rates and maturities) are being incorrectly dismissed by worn out cannabis investors - providing potentially large asymmetry in the upside reward relative to the downside risk:

MAR 13, 2026 9:30 AM EDT

Multi-State Cannabis Operators Have Successfully Overcome a Potential 'Refinancing Cliff'

The largest financial hurdle (that I previously feared) facing the cannabis industry has been successfully leapt over by most of the multi-state operators.

Over the last several months Verrano, Green Thumb (GTBIF) , Trulieve (TCNNF) , TerrAscend, Curaleaf (CURLF) and others have refinanced their debt with credit facilities at very attractive interest rates (9.5% to 11.5%) and have extended maturities:

I view the refinancings above as an underappreciated factor facing cannabis investors — suggesting that the industry's share price outlook has measurably improved.

I have added to my cannabis exposure every day over the last two weeks.

In investing and is in life: All too often missed opportunities are in plain sight.

Position: Long MSOS (L), MSOX (M), Long Trulieve, Curaleaf, Green Thumb, TerrAscend, Verano, Glass House

Boockvar on Gas Prices, Iran Rumors, German Jobless Rate

From Peter Boockvar:

Never a dull moment

More signaling, this time from the WSJ, that the President wants to be done with this war with the only question being what can be declared as a victory and what control of the Strait will look like. The S&P futures immediately reversed higher last night when the story hit but the Strait needs to be reopened, completely, for the global economy to breathe easier and oil prices are up again today.

Was the global rally in sovereign bonds and drop in yields yesterday a pivot for the market from ‘inflation worries and capital raising needs’ to ‘the global economy is about to slow, I need to own some bonds’? Maybe.

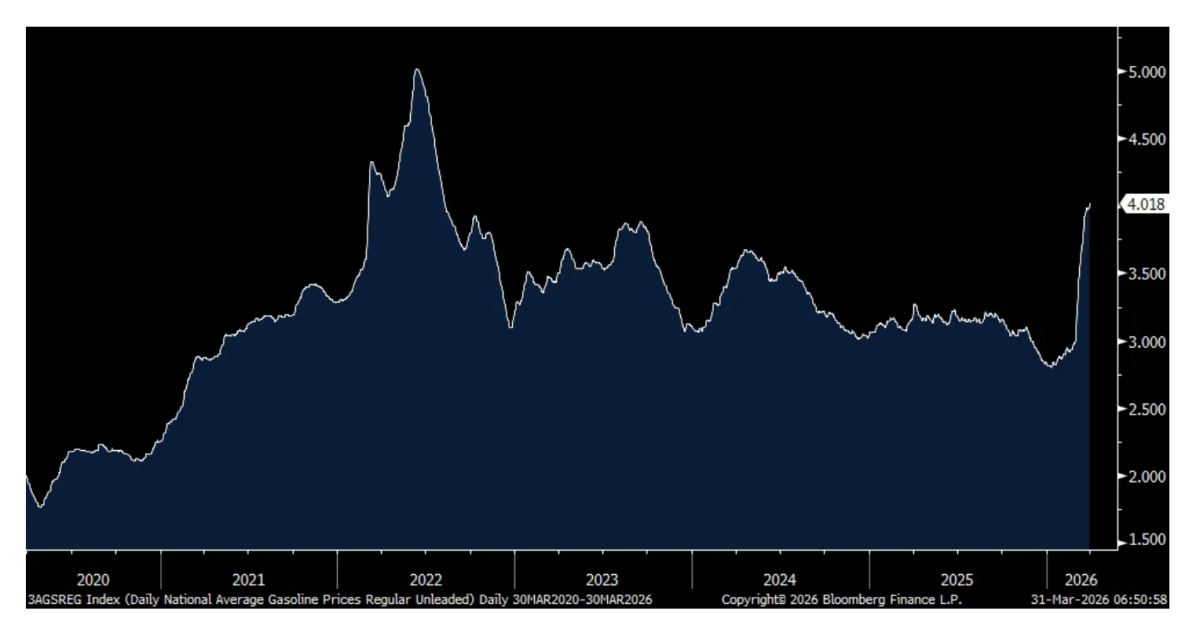

The average gallon of gasoline in the US is officially above $4, according to AAA as of yesterday as it rose from $3.99 (close enough) to $4.02.

Average Gallon Price

More surveys have come out for March that reflect our new economic reality. This was from the Dallas Banking Conditions Survey out yesterday:

“Loan volume and demand notably accelerated in March. The upward momentum was driven by real estate loans, especially commercial real estate. Credit standards and terms tightened slightly, but loan pricing continued to decline. Overall loan performance deteriorated. Bankers reported slight declines in general business activity. Outlooks were a bit less optimistic overall than the prior survey. Survey respondents still expect growth in loan demand and business activity six months from now but also expect worsening loan performance.”

Here were some comments from some of the banks surveyed and to be expected:

It’s imperative that the stabilization of the price of oil occurs quickly (30 to 60 days) so that it doesn’t create a long-term economic drain on businesses and consumers.

There is a tremendous amount of uncertainty in the economy at the moment. It is difficult for customers to have a positive business attitude. The partisan politics, spiking energy cost, international conflict, uncertainty at the Federal Reserve due to political pressure all add to an economic decision stagnation. Some stability on some fronts would be helpful to grow this economy.

Recent events in Iran and surrounding countries have created uncertainty in the domestic economy while dramatically increasing the price of fuel. Persistent personal consumption expenditures reports above 2.5 percent make it difficult to determine what the Federal Open Market Committee will do in the short term.

Loan demand has been increasing due to a major project in the Monroe market. Commercial loan nonperformance seems to have leveled out. Consumer, residential real estate and consumer nonperformance are increasing. We will plan to tighten underwriting and hold rates due to liquidity pressure on the balance sheet.

We are seeing some opportunities for commercial real estate and commercial and industrial lending in some of our markets. All of our commercial customers are now wanting floating rate loans in anticipation of continued rate cuts. I am not so optimistic because of inflation pressures associated with oil and gas due to the Iran conflict.

The March Dallas manufacturing index out yesterday too remaining about flat at -.2 vs +.2 in February. Here is what was said from a variety of companies in different industries with many adjusting to the current environment, some better than others and with one unfortunately ready to close the doors:

Beverage and tobacco product manufacturing

We have seen decreases in some of our costs, in particular agricultural raw materials. We have seen increases in the costs of our packaging materials, some of this related to increase in energy costs. We expect the Iran war to cause increases in energy costs for a period extending at least six months and potentially longer. This has increased our uncertainty for the rest of the year.

Chemical manufacturing

The Iran war and bottleneck in the Strait of Hormuz has caused significant supply chain disruption from China, allowing the U.S. chemicals sector to benefit from the supply bottleneck. We believe this to be short-lived and the situation to return to the lower demand levels in the latter half of 2026.

Computer and electronic product manufacturing

I am thinking about recommending to our board to close the company. I bolded to highlight.

We have seen no impact yet from higher fuel prices. However, we expect to see this very soon, as our vendors will increase raw materials prices to include the increased cost for transportation.

We would like to see lower interest rates throughout this year.

Food manufacturing

Continuing confusion at the federal level, illiquid consumer base and falling federal government spending are not helping the food industry.

High density Hispanic channels are down. Costs are up, and freight is increasing fast. Tariff chaos has wreaked havoc with all of our export customers and seasoning suppliers.

We are worried about costs increasing due to fuel price increases. We are worried about a slowdown in the economy due to geopolitics.

Furniture and related product manufacturing

The Iran war and impact on energy prices are concerns as consumers have to deal with the rapid increase in energy cost. Hopefully it will moderate as the conflict curtails. That said, the more demoralizing impact of the constant circus out of Washington and inability to fund critical infrastructure like TSA is killing the animal spirits of our economy.

Machinery manufacturing

We are beating our competition due to the continued vertical integration plans that we are focused on implementing and improving. This requires a great deal of planning and money, but the payout is very sound.

Spring has sprung. It’s truly like the balm of Gilead. After an extended period of ailment and woe, the healing has occurred and we are on our way to greater things. Our business growth thus far in 2026 is like a sweet fragrance that is healing our loss and hardship from prior years.

We are still seeing strong business activity with our backlog increasing.

Our company is seeing an increase in activity totally unrelated to the current geopolitical conditions. The effect of uncertainty delayed the start of a new manufacturing project in the U.S. (tariffs, capital expenditures) in 2025. Project 2025 is underway with a six-month delay and scaled back to accommodate a less ambitious picture for 2026. We are still recovering from 2025 plus a more conservative outlook for 2026. Things are trending upward in our field but at a much slower pace.

Miscellaneous manufacturing

Many external factors contributing to an unstable market.

If we could get our tariff reimbursement back, that would put us in a position to invest in growth. Without it, though, we don’t have the capital to invest in growth.

Nonmetallic mineral product manufacturing

We are waiting for home building activity to pick up, which is dependent upon interest rates.

Paper manufacturing

Overall business still slow. Have achieved limited price reductions in some raw materials that are in an oversupply condition but not enough to keep up with the decline in selling prices of our products. We still see upward pressure on labor and benefits cost. Margins are reduced from 12 months ago.

Plastics and rubber products manufacturing

Importing from China is precarious. The costs of product and freight are higher and slower. Suppliers are apprehensive. Their costs are increasing, especially a certain raw material plastic impacted by petrochemicals affected by cost of oil.

Printing and related support activities

We have been stupid slow recently, slower than we can recall in many years. We continue to believe it’s from the chaos and confusion coming out of Washington. In addition, now with the Iran war, prices are going to shoot up due to shipping costs, and tariffs are still in effect. So, there is no telling when business will start to improve. We have some nice work coming in soon, but it’s work we knew was coming. We are seeing some improvement in our estimating backlog, which is a good sign of better days to come. The war is causing a disruption of raw materials prices as we are producing plastic-based products, virtually all of our raw materials are hydrocarbon based. Fifteen percent increases are normal.

I forgot to mention this yesterday but there is still not much of a drilling reaction from US producers in response to the spike in oil prices. As of Friday, the US crude oil rig count fell by 5 rigs, giving back almost all of the 7 rig increase over the prior three weeks, capturing the month of March and after the war began. I’ll argue again, that when this war is over and the Strait is fully reopened without threat, crude oil is not going back to the $65 range it was before it started. At around $65 I believed it was one of the cheapest assets in the world and US oil production was no longer a growth story and that remains the case.

Crude Oil Rig Count

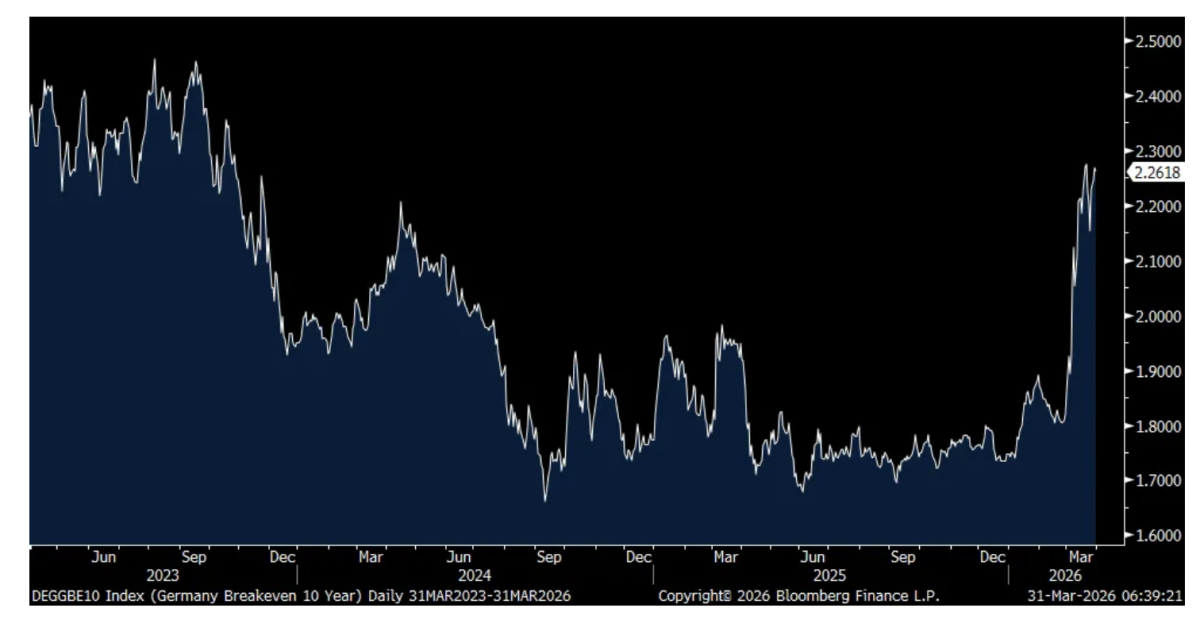

Capturing the jump in energy prices, the March Eurozone CPI was higher by 2.5% y/o/y, up from 1.9% in February but one tenth below what was expected. The core rate, where higher energy will eventually bleed into, was little changed, up by 2.3% vs 2.4% in the month before. Energy prices in particular rebounded by 4.9% y/o/y after falling over the prior six months. Services inflation, which will also soon feel the impact of higher energy prices via transportation, airfares, etc..., was up 3.2% y/o/y vs 3.4% in February.

As the data was about as anticipated, the breakevens are little changed but they did lift yesterday after Germany reported its inflation stats that jumped a lot. Its 10 yr breakeven is at a still modest level of 2.26%, though at the highest since October 2023.

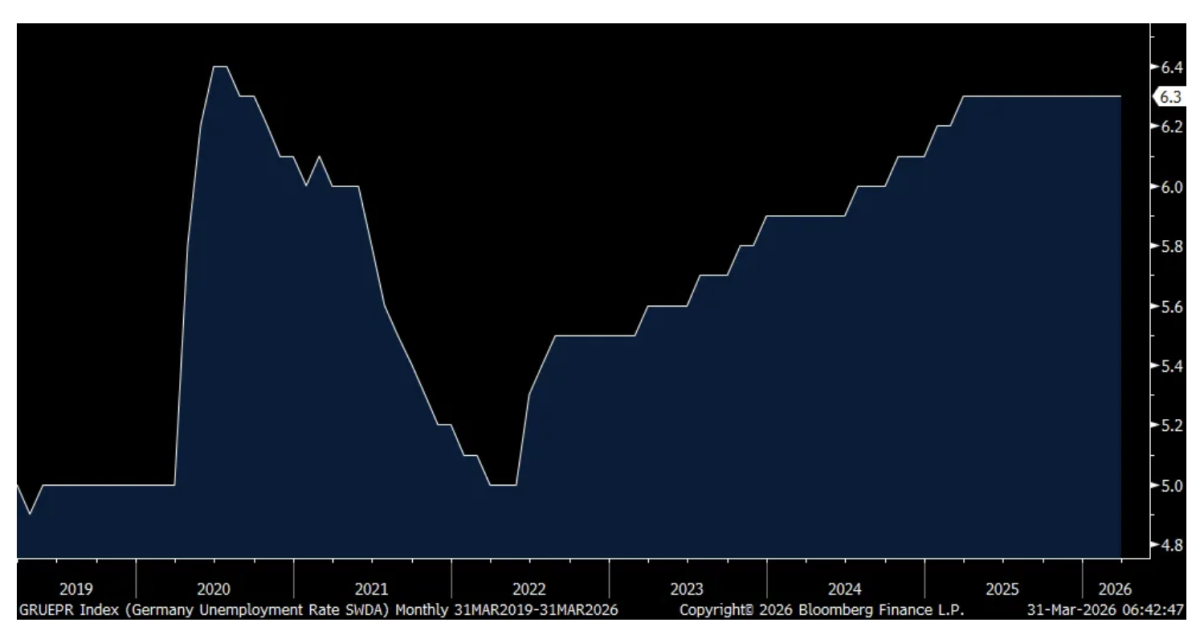

Also of note out of Europe was the German March jobs report where there was no change in unemployment, a touch better than the estimate of an increase of 2k and their unemployment rate held at 6.3%, the highest since the Covid shutdowns and vs 5% before Covid as the German economy remains challenged by uncompetitive energy costs (even before the war), and the intense competition from China in a variety of manufactured goods, particularly autos.

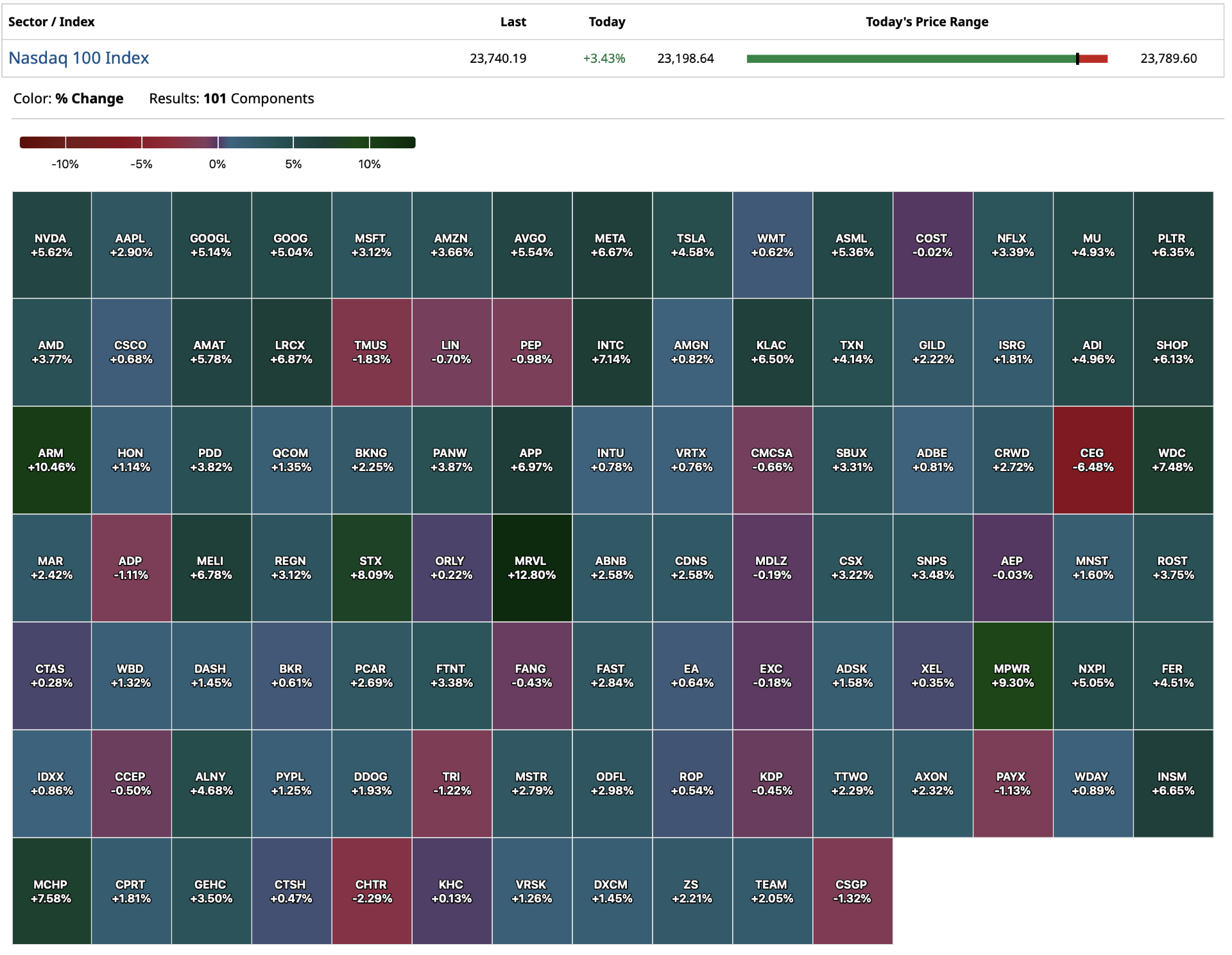

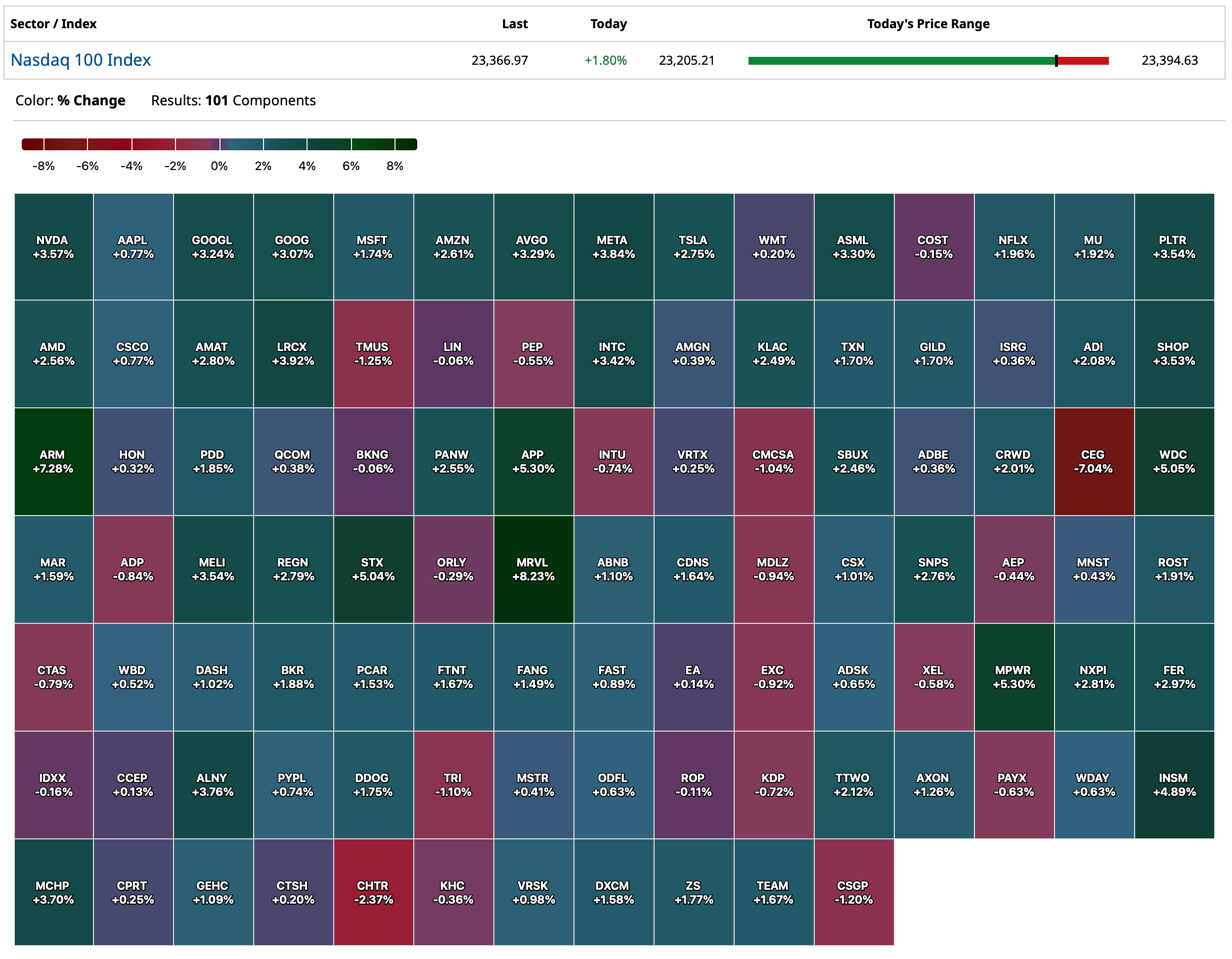

With S&P cash +90 handles I am taking down my Mag7 longs (most are experiencing sharp gains - like (META) (Trade of the Week) +$19!) from medium-sized to small-sized.

@jimcramer@carlquintanilla Jim I respectfully disagree with your upbeat assessment (as it relates to equities) of the new strategy to cede control of the Strait. The knock on consequences of this new strategy are broad, inflationary and economic dulling. The policy leads to…

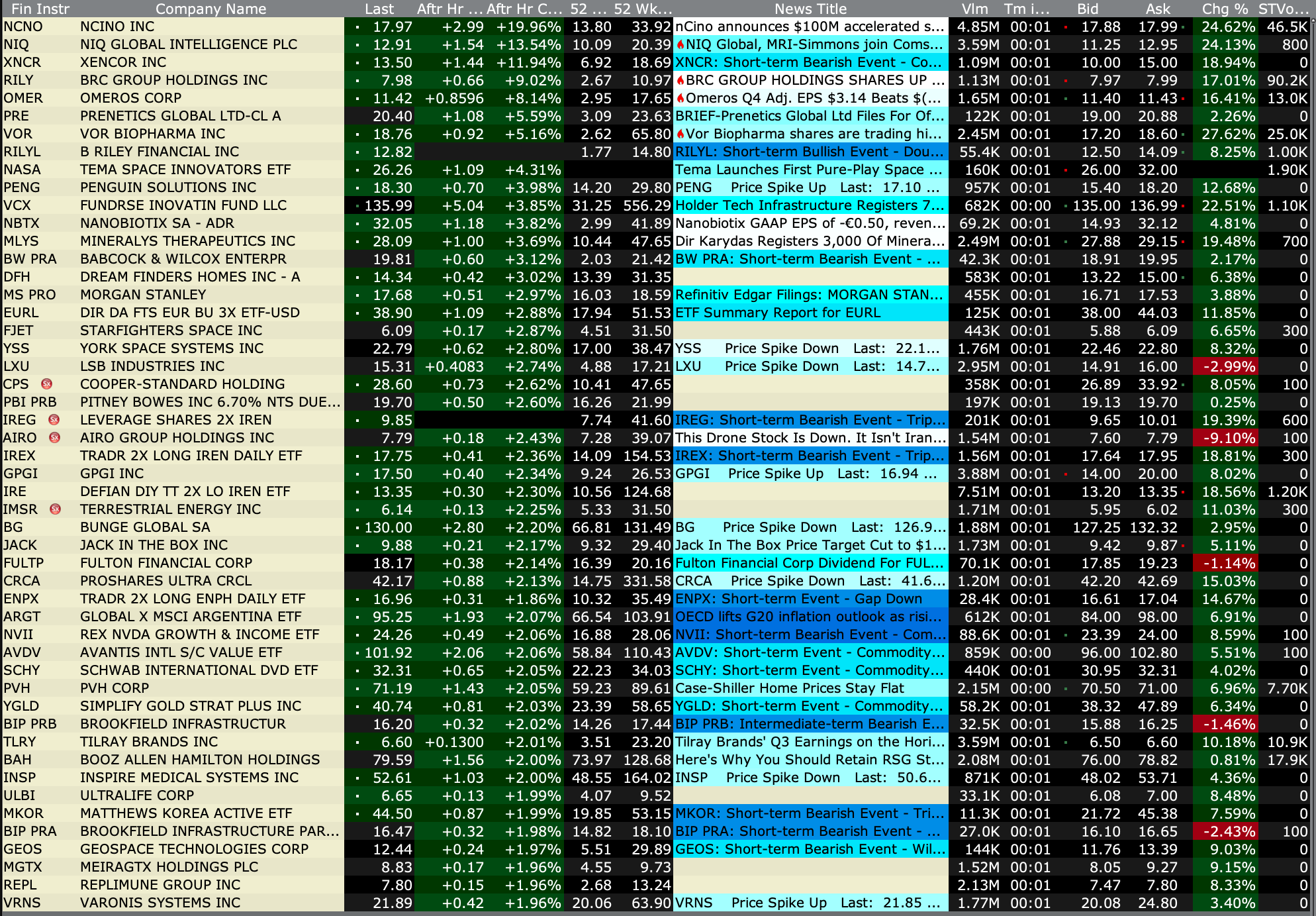

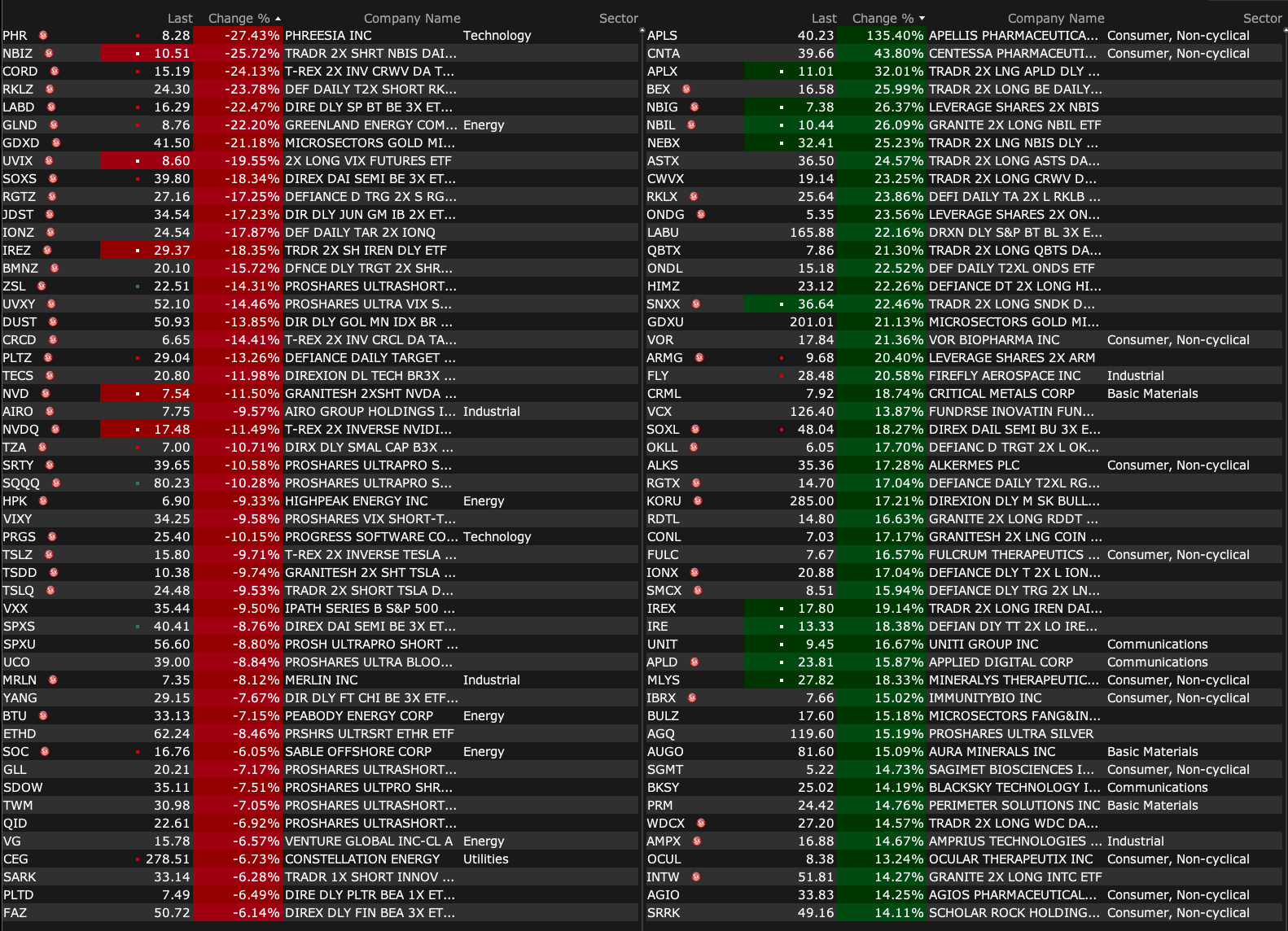

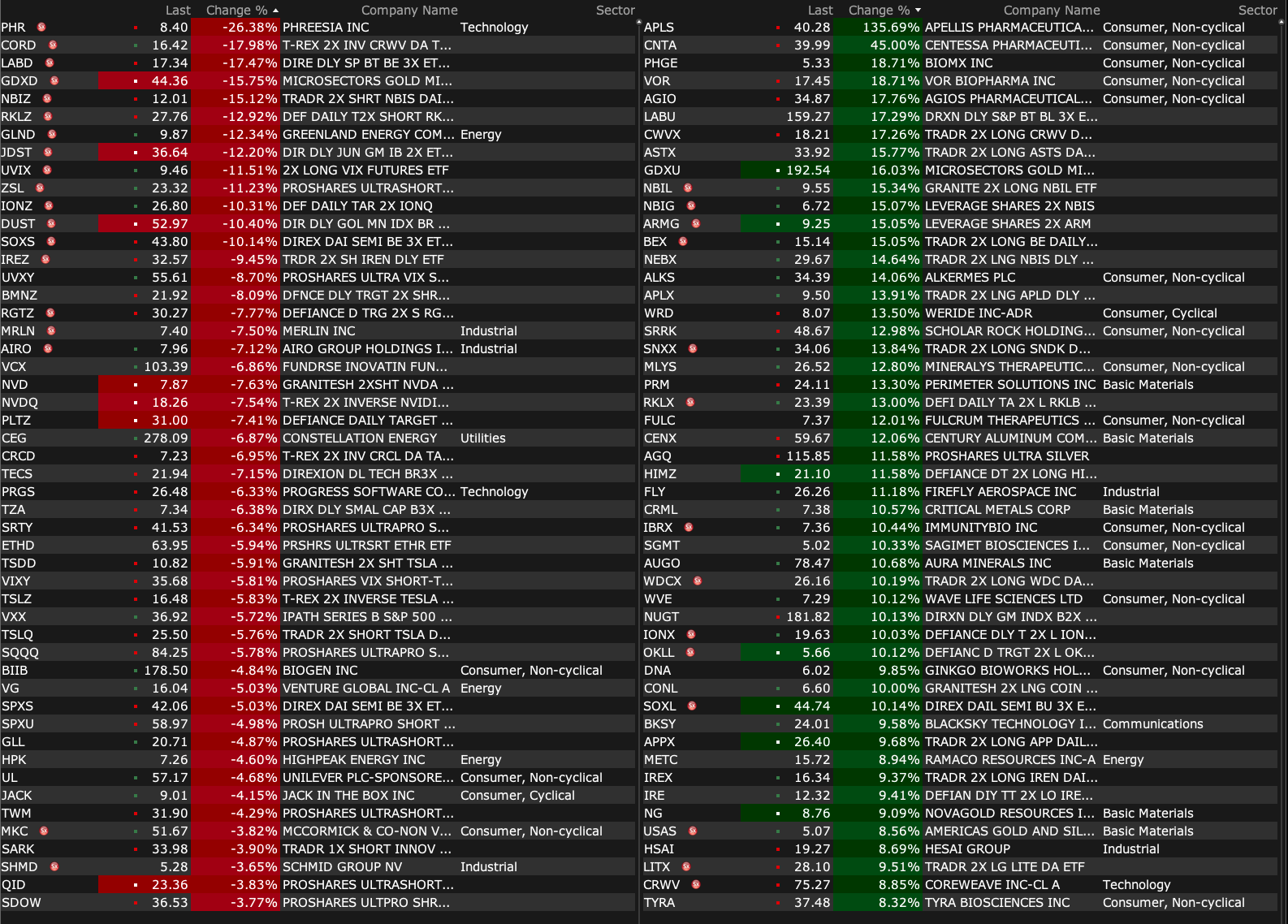

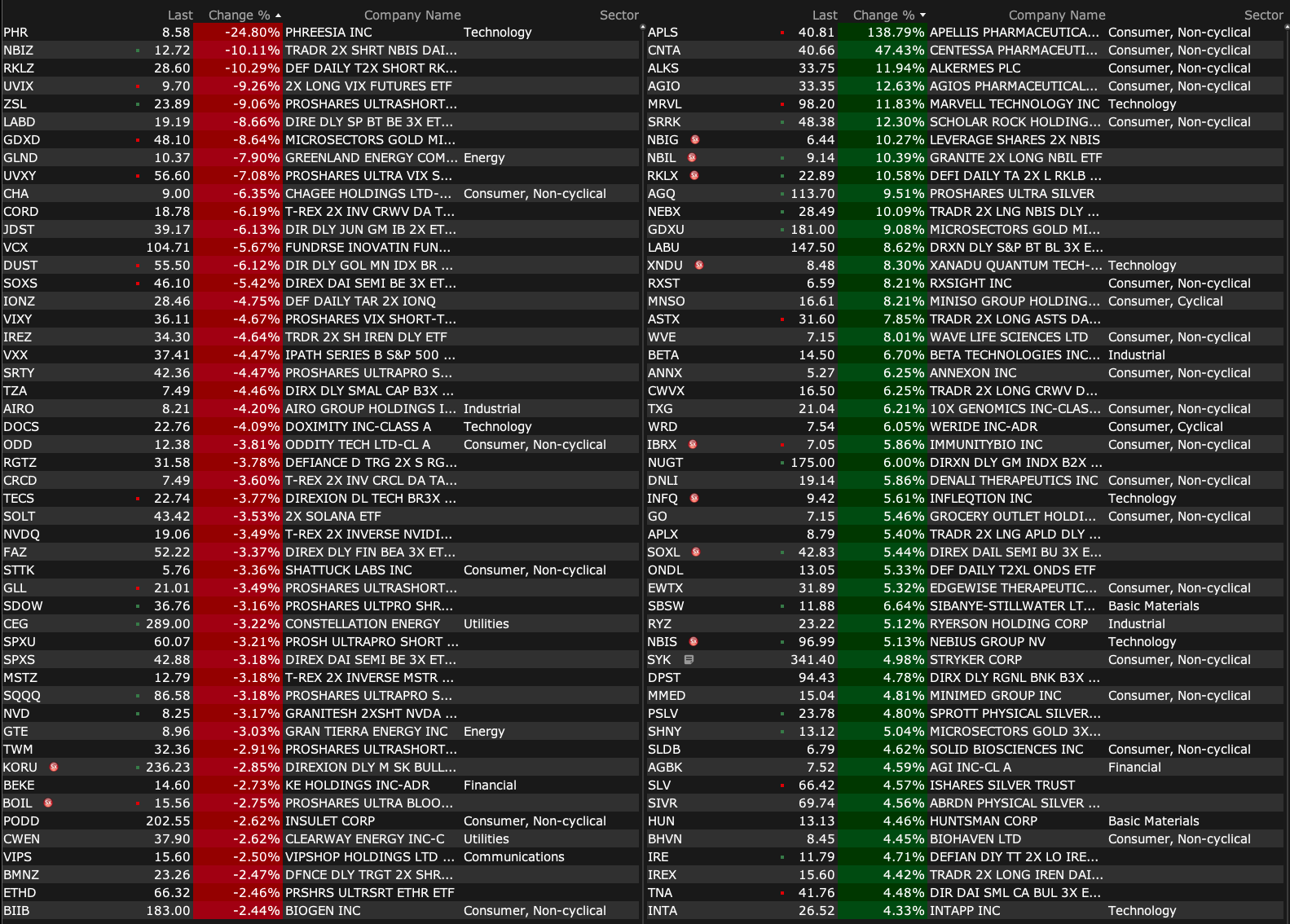

-APLS +137% (Biogen confirms to Acquire Apellis for $41/shr plus CVR or $5.6B)

-CNTA +46% (acquired by Eli Lilly for up to $7.8B)

-BIRD +16% (entered definitive agreement for American Exchange Group to acquire all intellectual property and certain other assets and liabilities for an estimated transaction value of $39M)

-AEHR +15% (wins silicon photonics order for data center transceivers)

-SRRK +13% (resubmits Biologics License Application (BLA) to FDA for Apitegromab for Treatment of Children and Adults with Spinal Muscular Atrophy (SMA) with March 3, 2026 Type C meeting)

-NTRA +9.7% (Signatera MRD Identifies Breast Cancer Patients Who Can Forgo Surgery)

-MRVL +9.4% (receives $2B investment from Nvidia amid partnership on AI infrastructure and silicon photonics)

-SPCE +9.2% (earnings, guidance)

-IBRX +7.8% (secures non-dilutive funding and debt conversion)

11:30 a.m.: Treasury hosts a $75B 6-Week Bill Auction

Fed Speakers:

12 p.m.: Fed Bank of Chicago President Goolsbee (Non-Voter) gives opening remarks before the "Human Capital in a Time of Low Real Rates" event hosted by the Federal Reserve Bank of Chicago, Chicago, IL (Livestream available. Embargoed text TBD);

1:10 p.m.: Fed Bank of Kansas City President Schmid (Non-Voter) speaks on monetary policy and the economic outlook at the Rotary Club of Oklahoma City, Oklahoma City, OK (Text and audience Q&A expected);

3:00 p.m.: Fed Governor Barr (Voter) speaks on "Stablecoins" at The Federalist Society’s The GENIUS Act in Practice: Key Questions for Stablecoin Regulation, Virtual (Text expected. Q&A from moderator and audience);

5:10 p.m.: Fed Vice Chair for Supervision Bowman (Voter) speaks on "Small Business" at CBA Live 2026, San Diego, CA (Text expected. Q&A from moderator. Livestreamed at https://www.cbalive.info/livestream)

* You can't make up what happened last night in futures trading

* A confusing statement by the Administration on abandoning the strategy of taking the Strait of Hurmuz makes little sense to this observer

* Here is my play by play...

Practicing on our night moves Trying to lose the awkward teenage blues Workin' on out night moves Oh I wonder Hey we felt the lightning yeah And we waited on the thunder Waited on the thunder

I woke last night to the sound of thunder How far off I sat and wondered Started humming a song from nineteen sixty-two Ain't it funny how the night moves When you just don't seem to have as much to lose Strange how the night moves With autumn closing in

Night moves (Night moves) oh (Night moves) I remember (Night moves) sure do remember those night moves

Follow the stock futures dots since the close of trading yesterday:

Cliff Notes

"You can't make this up: Iran's trading advice to US investors actually worked. At 4:12 PM ET on Sunday, Iran's Speaker of the Parliament said pre-market news is a "reverse indicator" and if they "dump" the market, then "go long." At 6:00 PM ET, S&P 500 futures opened nearly -1% lower and fell just 30 points away from correction territory. By 11:00 PM ET, S&P 500 futures had reversed all losses and turned green. Then, at 7:25 AM ET today, President Trump posted that "great progress" is being made on Iran peace talks. Now, the S&P 500 is trading +100 points above its low seen just hours ago, adding +$900 billion in market cap. We are in the most unusual times in market history."

🚨 Do you understand what happened in the last 24 hours..

> the US dropped a HIGH VOLUME of 2,000-pound bunker-busters on Isfahan.. directly on top of 400 kilograms of highly enriched uranium.. creating a mushroom-cloud fireball..

Last night (as noted above), the equity futures market was clearly breaking down. S&P futures were down by nearly -40 handles and Nasdaq futures were down by well over -100 handles.

I purchased (SPY) and (QQQ) common at some very low prices (see my post from the Comments Section — adding to my growing index long position.

I fell asleep near 9 PM with futures at the low in the evening session.

I awoke about two hours later to see a total reversal to the upside of nearly +100 S&P points:

S&P 500 futures bid up 100 points off the lows on this latest TACO.

After I observed only a slight downdraft in oil prices, I instinctively sold out what I had purchased only 180 minutes earlier with gains of between +$8 to +$10.

Abandoning the objective of "freeing" the Strait of Hormuz made no sense to me as it would likely continue to put pressure on oil prices to remain elevated and rekindle the "affordability" issue. This then stops being an oil price shock story and becomes a global oil supply shock. This strategy would have a consequential knock-on consequences for derivative petroleum products (e.g. fertilizers) and other products (e.g. helium).

Oil prices could surge to $150–$200 a barrel if the Strait of Hormuz remains largely shut for weeks, as the Iran war disrupts global supply.

Analysts warn ongoing losses of millions of barrels are tightening the market, and physical…

— *Walter Bloomberg (@DeItaone)

The messaging from the White House seems conflicted:

bbfreak

more contradiction.

Fresh Monday statements from Treasury Secretary Scott Bessent continue to signal a longish timeframe for US operations in Iran (far beyond the mere 'days' mentioned in late February at the start). Speaking somewhat ambiguously, he said "over time" the US will "retake" control of the Strait of Hormuz.

Given my interpretation of the news (and that the WSJ story might be a "stretch"/hyperbolic or even may not be totally accurate), I (reluctantly) sold down some more of my index common longs, purchased during Monday's trading session. (I am now delta equivalent neutral with my short index calls.)

Position: Long SPY common (S), QQQ common (S); Short SPY calls (S), QQQ calls (S)

$MSOS Reporter: Do you think that there's something that coincides with rescheduling that hints at uplisting taking place? Marc: Yes, I mean I couldn't disagree. R: Is that speculation or is that truth? M: Im not gonna get my sources in trouble. I'm not looking to burn any… pic.twitter.com/gX5Kc0UMDL

Just sold Indices I bought earlier in the evening:

SPY $638.22

QQQ $563.96

Better Jewish luck than Christian Science!

Wow.

1131:M

Dougie Kass

Dougie Kass

The more I think about it, the less I believe the WSJ story.

And even it is true, think about the ramifications for the price of oil and second order impact on inflation. I am taking a loss in some of my Index positions and, reluctantly, reducing from M sized to S sized SPY and QQQ.

With my short SPY and QQQ calls against the long common I am delta neutral in the Indices.

The + 100 handle rise in S and P futures just seems absurd (currently +60 handles after being -40 handles earlier in the evening, when I bought.

kdog

Just to be clear, are you currently long or short the indices? Just saw this, Sorry

Dougie Kass

sold the gap in the middle of the night... long common short calls delta equivalent neutral

Position: Long SPY common (S), QQQ common (S); Short SPY calls (S), QQQ calls (S).

BREAKING: Iran's Foreign Minister Araghchi just now on potential peace talks with the US:

"We do not have any faith that negotiations with the US will yield any results. The trust level is at zero."

OIL COULD HIT $200 IF HORMUZ STAYS CLOSED

Oil prices could surge to $150–$200 a barrel if the Strait of Hormuz remains largely shut for weeks, as the Iran war disrupts global supply.

Analysts warn ongoing losses of millions of barrels are tightening the market, and physicalShow more

“.. Trump told aides he’s willing to end the U.S. military campaign against Iran even if the Strait of Hormuz remains largely closed .. likely extending Tehran’s firm grip on the waterway and leaving a complex operation to reopen it for a later date.”

@WSJ

BREAKING: There is now a 37% chance that the US economy enters a recession by the end of 2026, per Polymarket.

US oil prices are officially up +$50/barrel from their December 2025 low.

Every time this line turns negative, stocks have entered a bear market

We saw this in the 1970s, 1999, 2007, 2022

And it’s about to happen again…

A Thread 🧵

@jimcramer@carlquintanilla Jim I respectfully disagree with your upbeat assessment (as it relates to equities) of the new strategy to cede control of the Strait.

The knock on consequences of this new strategy are broad, inflationary and economic dulling.

The policy leads toShow more

$MSOS Reporter: Do you think that there's something that coincides with rescheduling that hints at uplisting taking place? Marc: Yes, I mean I couldn't disagree.

R: Is that speculation or is that truth? M: Im not gonna get my sources in trouble. I'm not looking to burn anyShow more

Who in his/her right mind thinks that the prospects for 2026-7 S&P EPS gains are now higher than before the Iranian conflict (and after the rapid increase in energy and other related costs - which will impede demand and raise the costs of goods, adversely impacting margins)?Show more