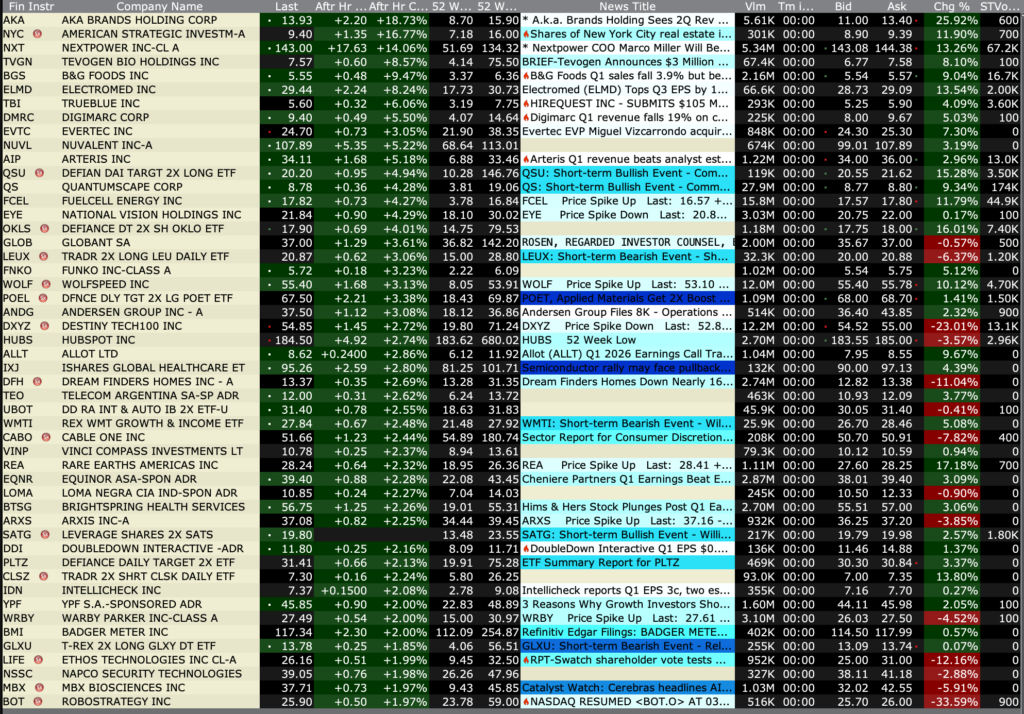

Tuesday’s After-Hours Advancers and Decliners

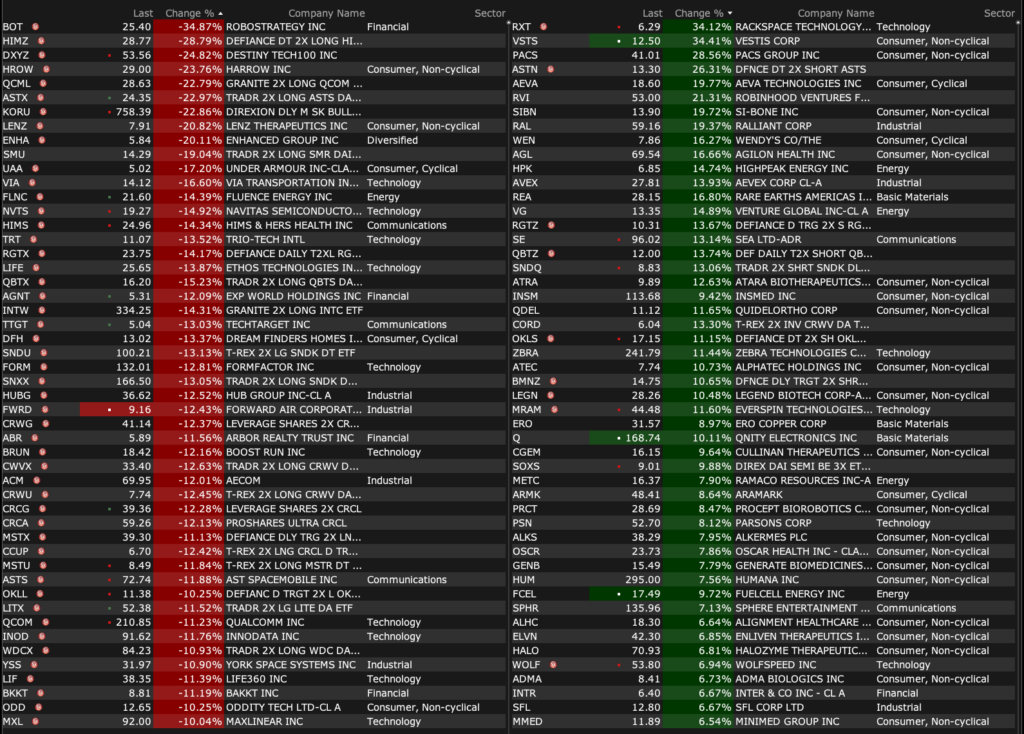

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · May 12, 2026, 4:45 PM EDT

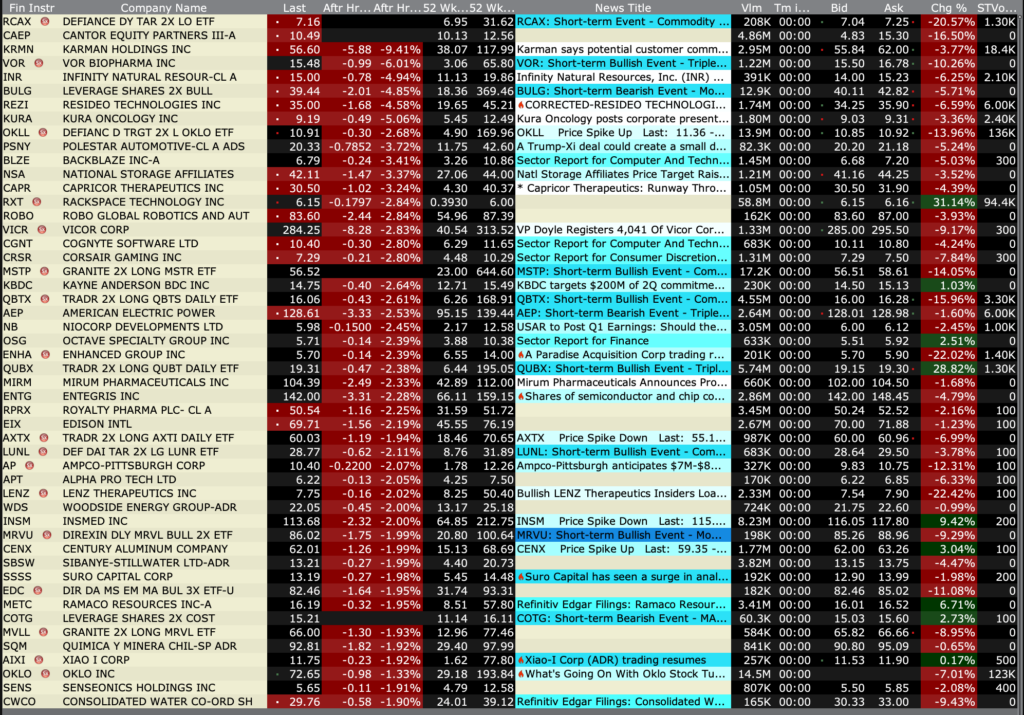

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · May 12, 2026, 4:45 PM EDT

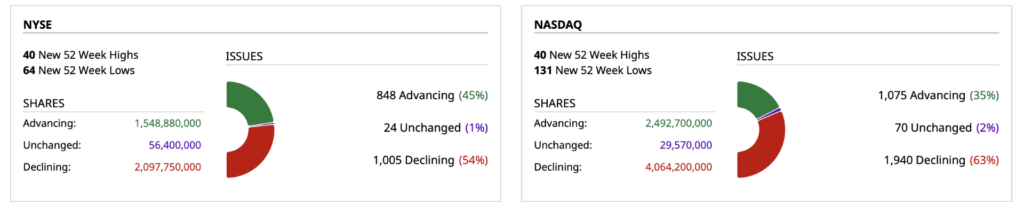

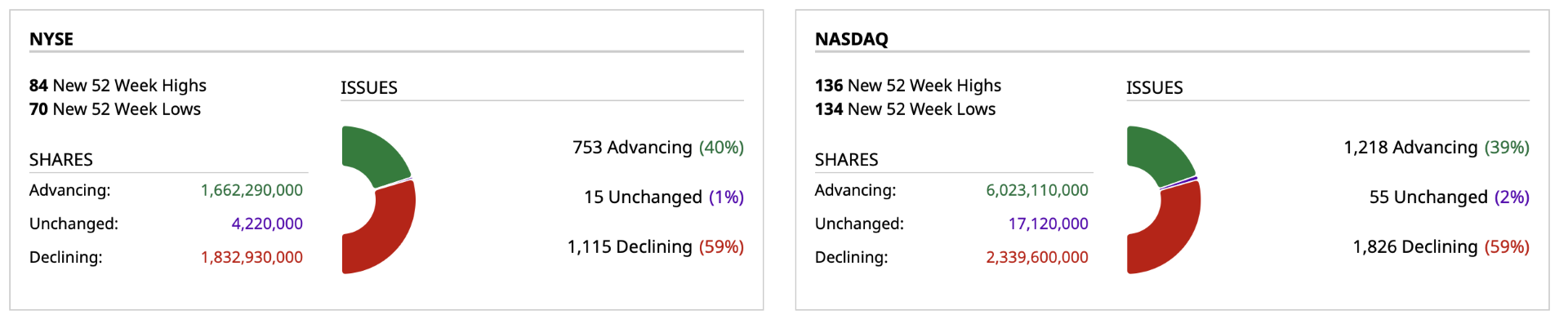

Closing Volume

– NYSE volume 12% above its one-month average

– NASDAQ volume 9% above its one-month average

– VIX index: down 2.29% to 17.96

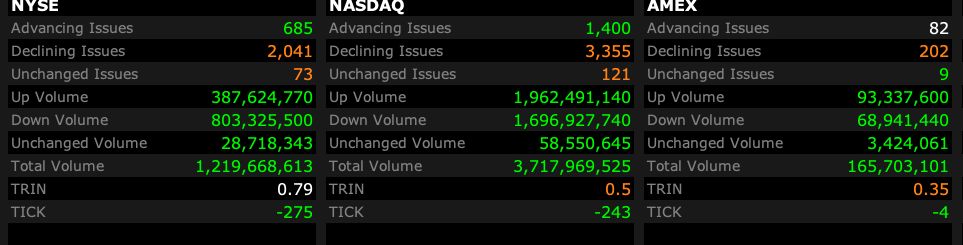

Breadth

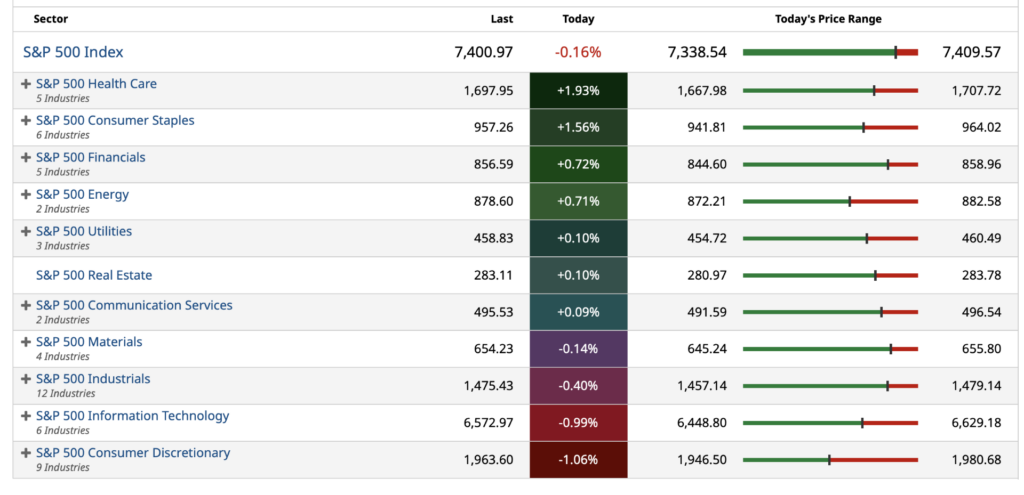

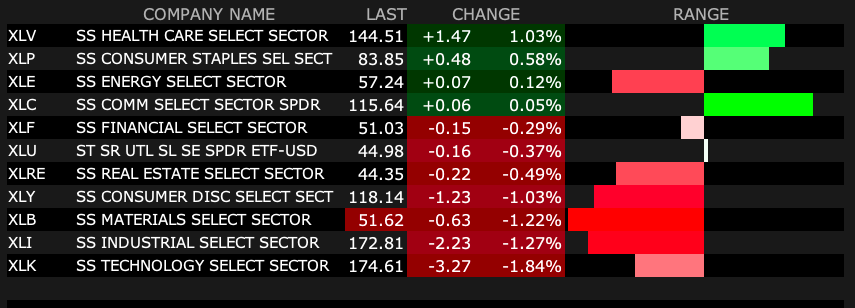

S&P 500 Sectors

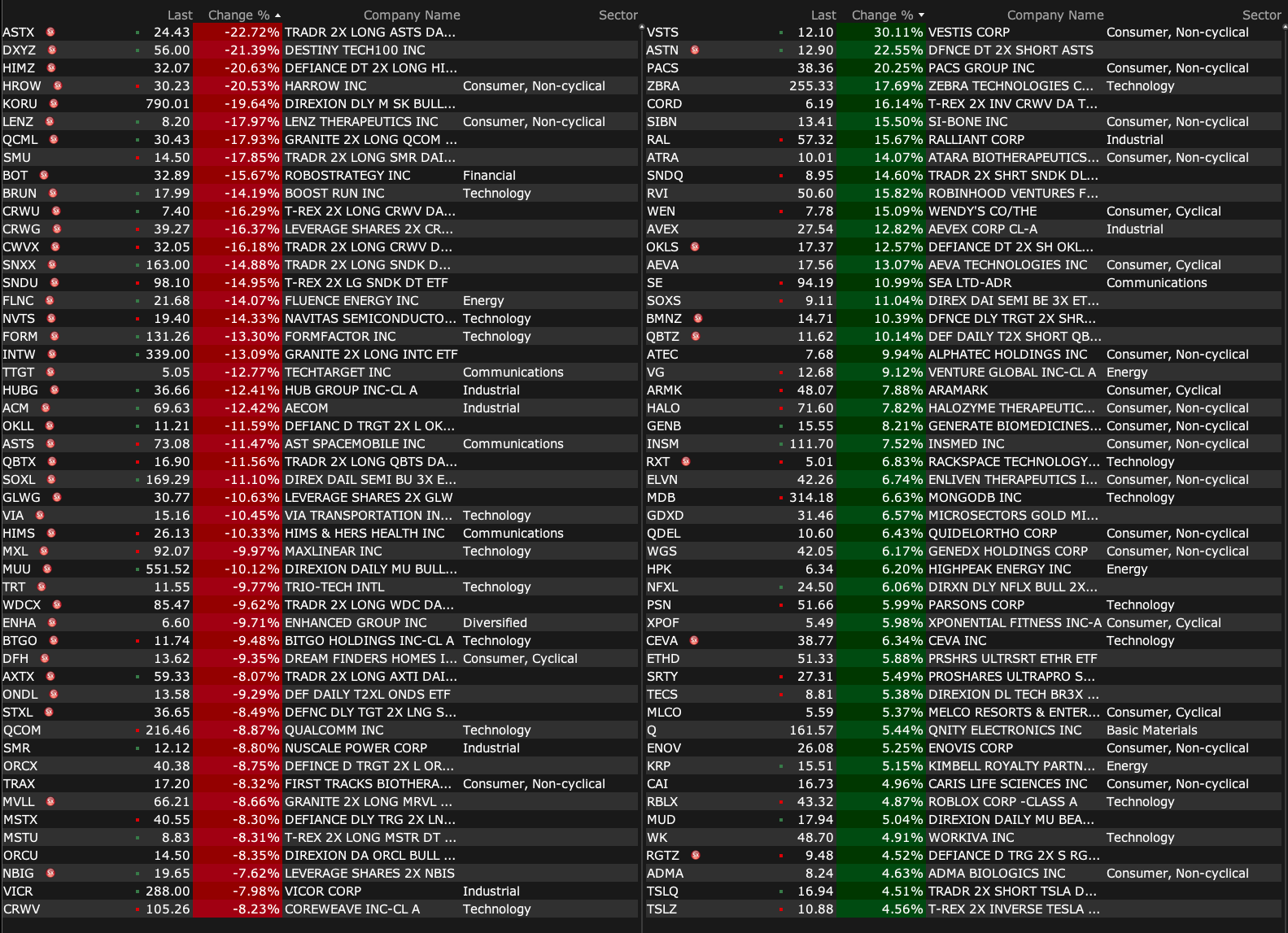

% Movers

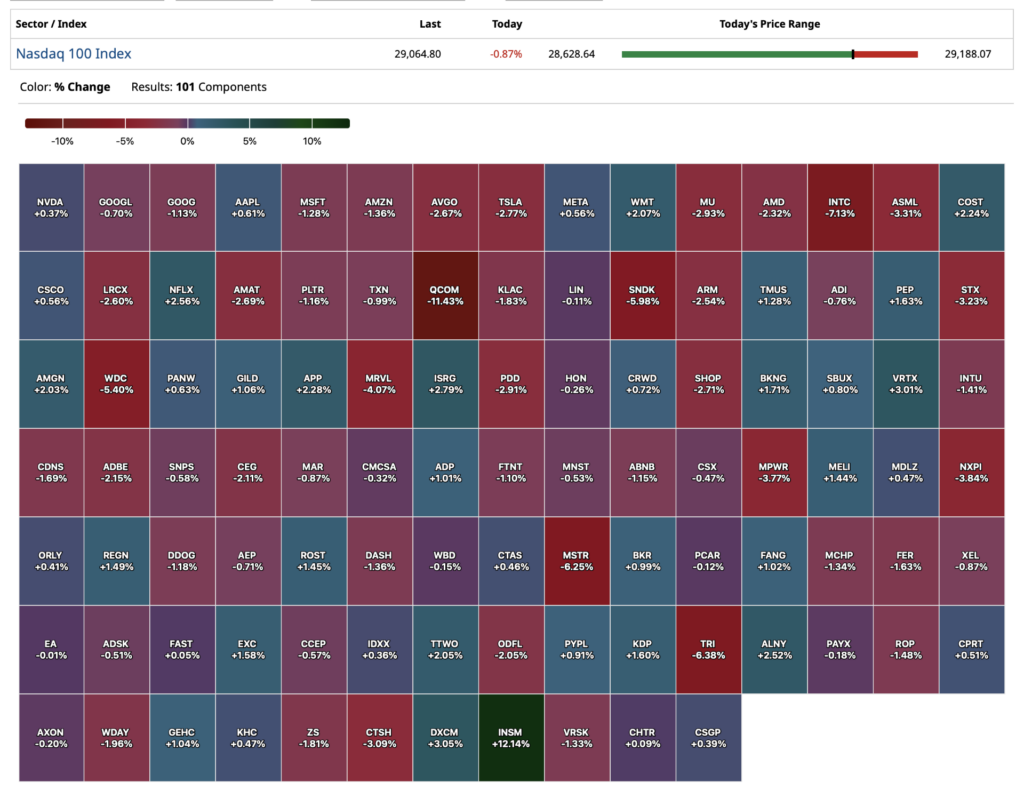

Nasdaq 100 Heat Map

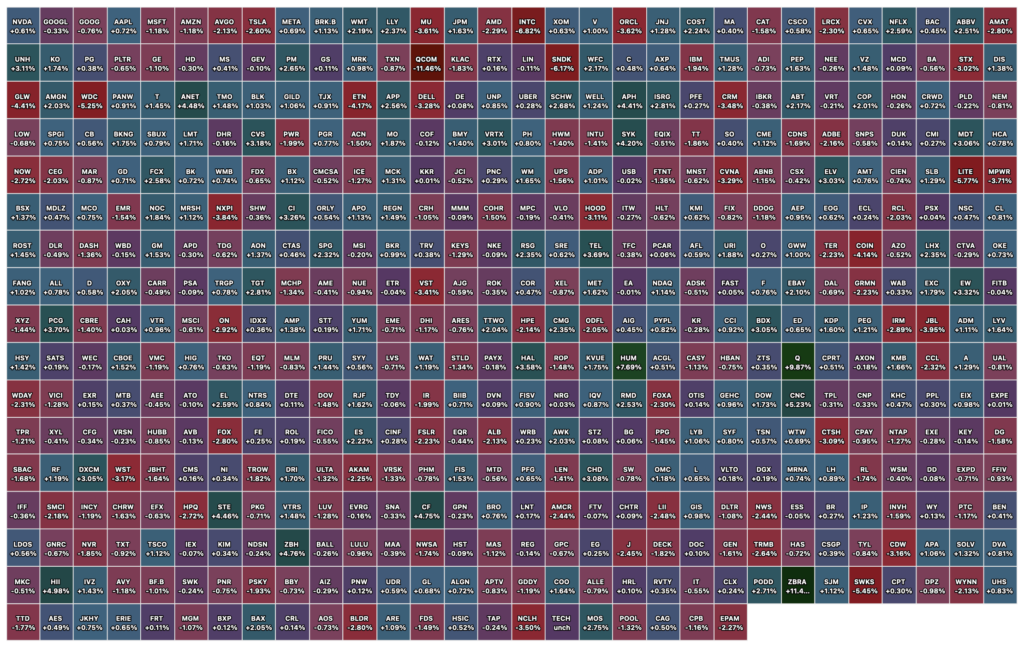

Closing S&P 500 Heat Map

Position: None

BY Doug Kass · May 12, 2026, 4:26 PM EDT

I was scaling up on strength in my short SPY, but I took my short in right after the close at $737.40 for a small gain.

I want a good night’s sleep!

Thanks for reading my Diary today.

Enjoy the evening.

Be safe.

Position: None

BY Doug Kass · May 12, 2026, 4:09 PM EDT

I am shorting SPY at $737.27

Position: Short SPY (VS)

BY Doug Kass · May 12, 2026, 3:26 PM EDT

Wolf Street howls about the Fed’s “real rates” being negative.

Position: None

BY Doug Kass · May 12, 2026, 3:03 PM EDT

I plan to give the market a relatively wide berth this afternoon before I re-short the indices and individual equites.

But short I will.

That will be my message contained in tomorrow's opening missive.

Position: None

BY Doug Kass · May 12, 2026, 2:04 PM EDT

It is interesting to note that VIX is now down on the day at 18.35 — down from 19.10 at the day's high...

Position: None

BY Doug Kass · May 12, 2026, 1:36 PM EDT

Tomorrow I have a lengthy (multi-part) discussion of the markets.

Positions: None.

BY Doug Kass · May 12, 2026, 11:50 AM EDT

Positions: None.

BY Doug Kass · May 12, 2026, 11:15 AM EDT

I covered the balance of my semiconductor shorts:

* (MU) $747.70

* (AMD) $442.42

* (INTC) $118.20

I will reshort on strength.

Positions: None.

BY Doug Kass · May 12, 2026, 11:13 AM EDT

This is exactly the sort of day that you should run (don't walk!) to watch MRKT CALL with Carter, Dan and Guy.

Honest, action-oriented and even amusing - they deliver non consensus views with humilty and take ownership of both their winners and losers.

Let's go to the tape (at 11 a.m.): MRKT Call - Tuesday, May 12th

Positions: None.

BY Doug Kass · May 12, 2026, 10:59 AM EDT

I covered some of my semi shorts:

* (MU) $748.19

* (AMD) $444.04

* (INTC) $119.02

I plan to reshort on strength.

Positions: None.

BY Doug Kass · May 12, 2026, 10:49 AM EDT

With S&P cash -49 handles I have covered all of my index shorts:

* (SPY) $734.23

* (QQQ) $704.87

I plan to reshort on strength.

Positions: None.

BY Doug Kass · May 12, 2026, 10:47 AM EDT

I covered the balance of my (SNDK) short at $1421.45.

Shorted yesterday at $1,566.

From earlier this morning:

I am covering half of my SanDisk (SNDK) short at $1,477.From yesterday:* Initiated a very small short in (SNDK) at $1,569.28.

Positions: Short SNDK VS

BY Doug Kass · May 12, 2026, 9:41 AM EDT

BY Doug Kass · May 12, 2026, 10:38 AM EDT

Chart from 9:45 a.m. ET

Positions: None.

BY Doug Kass · May 12, 2026, 10:35 AM EDT

From my friend Peter Boockvar:

Bottom line, it certainly could have been worse though the trend remains higher for inflation for now. And in response to the about in line data, the 2 yr yield is down 1.5 bps to 3.97-.98%, the 10 yr is off by 1 bp to 4.43% from 8:29am est and the 30 yr is still at 5.00%.

What is bothered however by the big picture trend are the inflation breakevens. The 2 yr breakeven is up by 5 bps to 2.94%, the 5 yr by 2 bps to 2.71% and the 10 yr is up by almost 2 bps to 2.50%, just 2 bps from the highest since March 2023.

Positions: None.

BY Doug Kass · May 12, 2026, 10:10 AM EDT

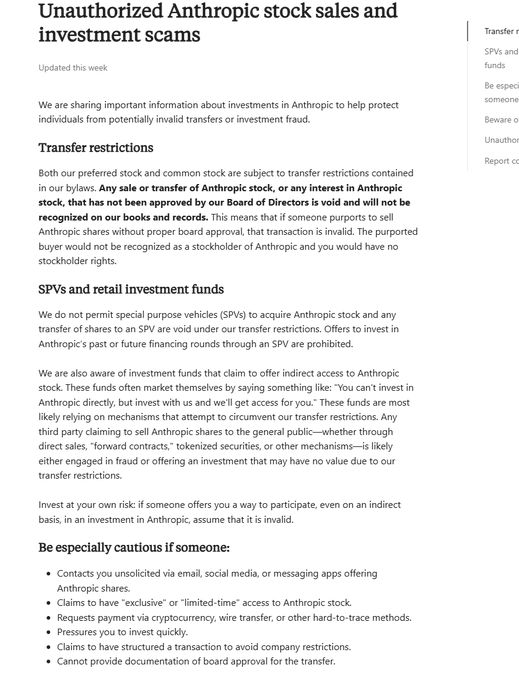

This is weird and I suspect will lead to a lower value in the secondary market:

Anthropic just published a support page that should terrify anyone holding its shares on the secondary market.

— TFTC (@TFTC21)

"Any sale or transfer of Anthropic stock, or any interest in Anthropic stock, that has not been approved by our Board of Directors is void and will not be recognized on… pic.twitter.com/4EKGpeJryJ

Positions: None.

BY Doug Kass · May 12, 2026, 9:49 AM EDT

I am covering half of my SanDisk (SNDK) short at $1,477.

From yesterday:

* Initiated a very small short in (SNDK) at $1,569.28.

Positions: Short SNDK VS

BY Doug Kass · May 12, 2026, 9:41 AM EDT

From Peter Boockvar:

The April CPI rose .6% m/o/m headline as expected while the core rate was higher by .4% m/o/m, one tenth above the estimate. Versus last year, CPI was up 3.8% headline and 2.8% core vs 3.3% and 2.6% in the month before. Energy prices jumped 3.8% m/o/m after the 11% rise in March and 18% y/o/y for obvious reasons with gasoline mostly driving that. Electricity prices jumped by 2.1% in the month alone and up by 6.1% y/o/y and we assume data center power demand as the key factor. Food prices bounced by .5% m/o/m and now by 3.1% y/o/y, if we include beverages too. Food at home prices were up by .7% m/o/m and 2.9% y/o/y. Helping to drive this was the 1.8% m/o/m and 6.1% y/o/y rise in fruits and vegetables (see my previous note and comment from Fresh Del Monte). Also, beef/veal prices spiked by another 2.7% in April and higher by 15% y/o/y. For those costs away from home, prices were up .2% m/o/m and 3.6% y/o/y.

Services inflation ex energy was up .5% m/o/m and 3.3% y/o/y. Owners equivalent rent rose .5% m/o/m and 3.3% y/o/y (real world is up more like 2-3% with respect to blended rates, less in sunbelt states and a bit higher for coastal ones). Rent of Primary Residence also saw a .5% m/o/m rise and by 2.8% y/o/y (closer to reality). Medical care costs were down for a 2nd month, by one tenth, though up 2.5% y/o/y. Not reality at all, the BLS said health insurance costs fell .4% m/o/m and down 6.1% y/o/y as they measure health insurance company profit margins rather than actual costs to consumers. Airline fares keep spiking, by another 2.8% m/o/m and by 20.7% y/o/y. The cost to fix a vehicle fell .2% m/o/m but only after jumping by 1.3% in March and they are higher by 5.1% y/o/y. Vehicle insurance costs are finally calming down, up .1% m/o/m and by just .2% y/o/y.

Goods prices were unchanged m/o/m and higher by 1.1% y/o/y. Keeping a lid on things was the no change in used vehicle prices and .2% drop for new ones. Apparel prices though did increase by .6% m/o/m and 4.2% y/o/y with tariffs having an impact along with issues with petrochemical costs that go into polyester, as heard from Under Armour this morning. With household furnishings and supplies saw prices down .5% m/o/m but up 2.8% y/o/y.

Bottom line, it certainly could have been worse though the trend remains higher for inflation for now. And in response to the about in line data, the 2 yr yield is down 1.5 bps to 3.97-.98%, the 10 yr is off by 1 bp to 4.43% from 8:29am est and the 30 yr is still at 5.00%.

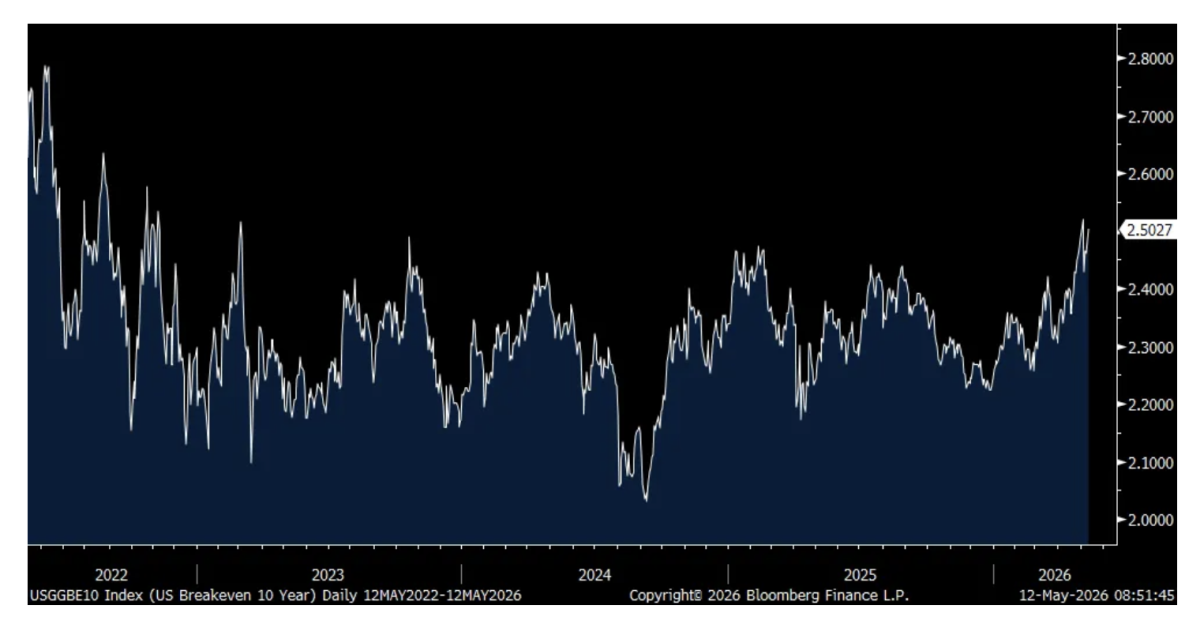

What is bothered however by the big picture trend are the inflation breakevens. The 2 yr breakeven is up by 5 bps to 2.94%, the 5 yr by 2 bps to 2.71% and the 10 yr is up by almost 2 bps to 2.50%, just 2 bps from the highest since March 2023.

10 yr Inflation Breakeven

Positions: None.

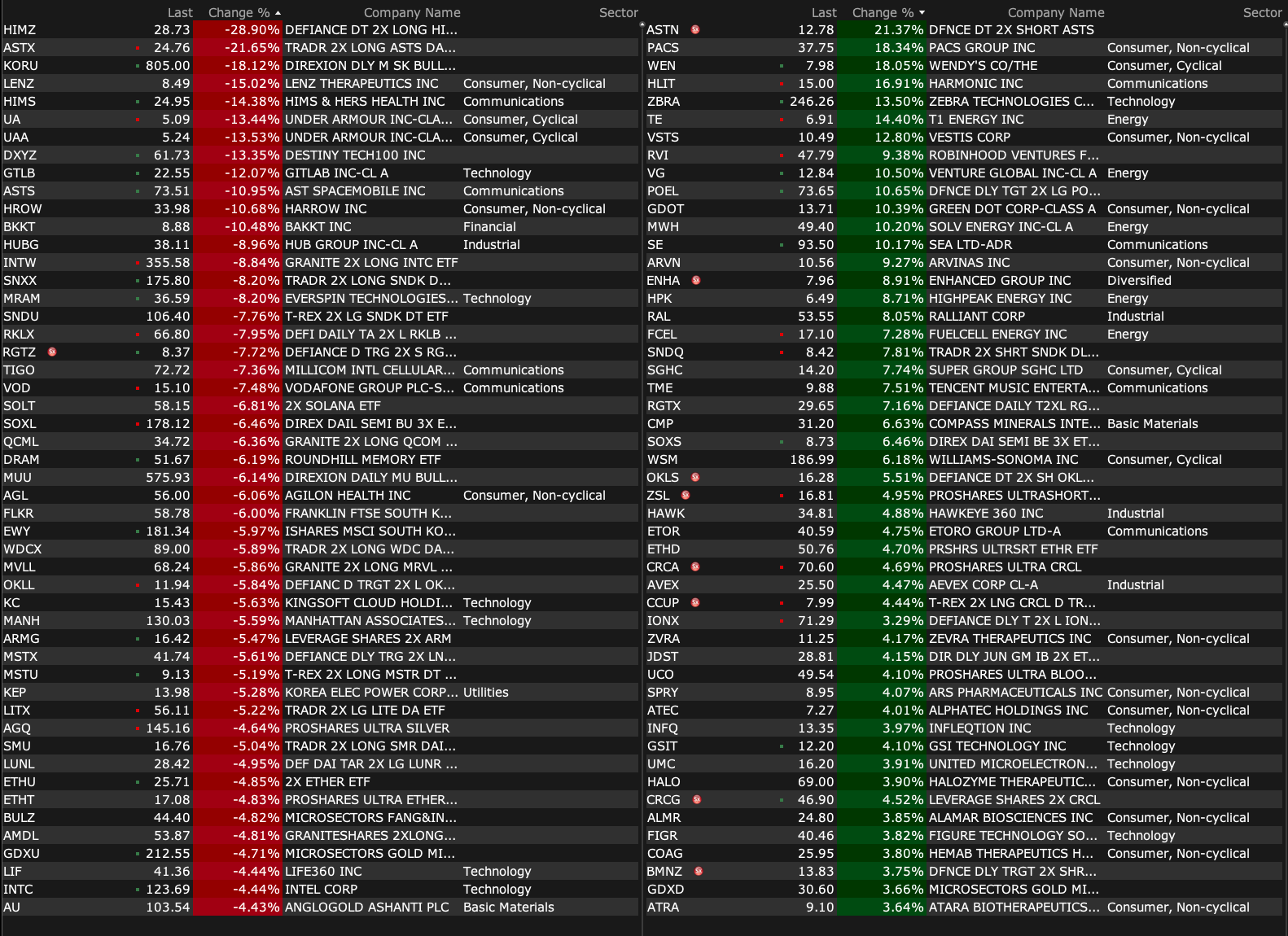

BY Doug Kass · May 12, 2026, 9:25 AM EDT

-VSTS +22% (earnings, guidance)

-VPG +21% (earnings, guidance)

-PACS +17% (earnings, guidance; Board approves $250M share buyback program)

-WEN +16% (Nelson Peltz's Trian Fund Management said to be in talks to raise funds for go-private bid)

-ZBRA +15% (earnings, guidance)

-HLIT +14% (earnings, guidance)

-PLUG +13% (earnings, color)

-AMBQ +12% (earnings, guidance)

-SE +11% (earnings, guidance)

-VG +11% (earnings, guidance; signs LNG deals with TotalEnergies and Vitol)

-RAL +9.6% (earnings, guidance)

-MWH +9.3% (earnings, guidance)

-ARMK +6.6% (earnings, guidance)

-RIGL +6.6% (Arvinas and Pfizer enter transaction with Rigel Pharmaceuticals for Exclusive Global Rights of VEPPANU)

-TME +6.2% (earnings, color)

-AI +2.3% (reports prelim Q4 revenue; Thomas Siebel resume CEO role)

-TE +2.2% (earnings, guidance)

-MVST -39% (earnings, color)

-HIMS -15% (earnings, guidance)

-GTLB -13% (announces job cuts while affirming FY27 forecast; Raymond James Cuts GTLB to Market Perform from Outperform)

-ASTS -12% (earnings, color)

-UA -12% (earnings, guidance)

-QBTS -8.0% (earnings, color)

-HUBG -7.2% (files to delay 10Q)

-GME -2.3% (eBay rejects unsolicited proposal from GameStop)

Positions: None.

BY Doug Kass · May 12, 2026, 9:12 AM EDT

Positions: None.

BY Doug Kass · May 12, 2026, 8:58 AM EDT

From Peter Boockvar:

It is not just urea (nitrogen) that is in short supply as about one third of it is sourced from the Middle East. About 20% of phosphate is produced there too, along with a quarter of ammonia and half of seaborne sulfur volumes where these two raw materials are used to produce phosphate. Mosaic, a fertilizer producer stock we own, making phosphate and potash, is curbing the production of phosphate because the current price of it is not high enough to offset the higher cost of ammonia and sulfur. They can source ammonia and sulfur mostly in North America but the margins have gotten squeezed and will be until phosphate prices rise further which they will upon these cuts. But, they can only rise so much from an affordability standpoint until the price of corn, soybeans, wheat and other products increase too so farmers can afford the price increases of their inputs.

From the Mosaic earnings call yesterday:

“Compressed margins and limited raw material availability have forced producers to curb production. For example, China has banned phosphate exports through August, and other competitors have significantly curtailed production primarily due to sulfur availability. To put it simply, there is not going to be enough phosphate to meet global demand.”

“There are real agronomic consequences caused by persistent under application. There is no substitute for phosphate, and when application rates are reduced too far or for too long, soil nutrient balances drop and yields are impacted. While those effects may not appear immediately, they have historically been an important driver of demand normalization as growers respond.”

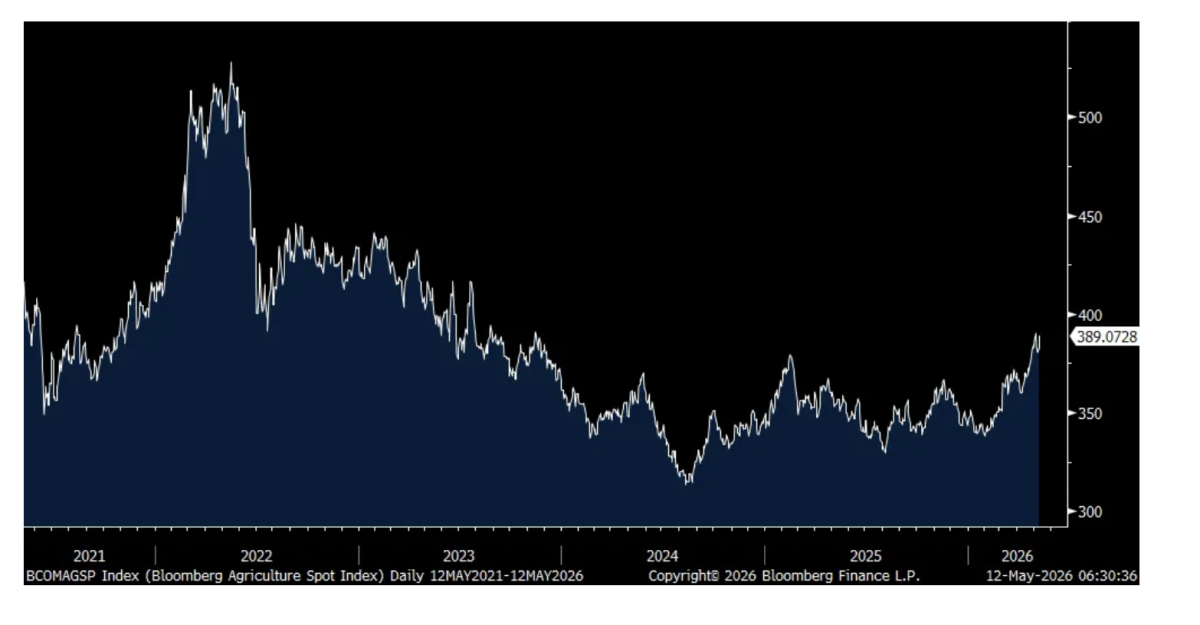

As for the broad ag sector which also includes coffee and cocoa in addition to corn, wheat and soybeans among others, the Bloomberg Agriculture Spot Index is within one point of its highest since 2023 and as seen in the chart, there is a lot of runway higher, a negative for the world that eats but positive for the farmers that farm.

Bloomberg Ag Spot Index

Staying on the ag theme, I read through the Fresh Del Monte earnings call from last Tuesday, the maker of fresh fruit and vegetables and whose stock is down 12% since the day before earnings. They said this of note:

“The conflict in the Middle East has introduced a meaningful shock across key inputs fundamental to food production, energy, fertilizers, packaging and transportation. There is no part of agriculture that is not energy dependent, from inputs to packaging to transportation. As a result, movements and energy costs do not remain isolated. They cascade through the entire system.”

“Agriculture does not operate in real-time. The timing of impact varies meaningfully by category. In crops like pineapples, for instance, where production cycles extend to approximately 18 months, the impulse being deployed today will be reflected in cost and pricing later this year. Bananas, by contrast, move more quickly through the system and therefore, respond more immediately to changes in input costs.”

“As a result, the pressures that emerged during the quarter are now embedded in the system and will continue to move through the value chain in the periods ahead, regardless of how conditions in the Middle East evolve from here.”

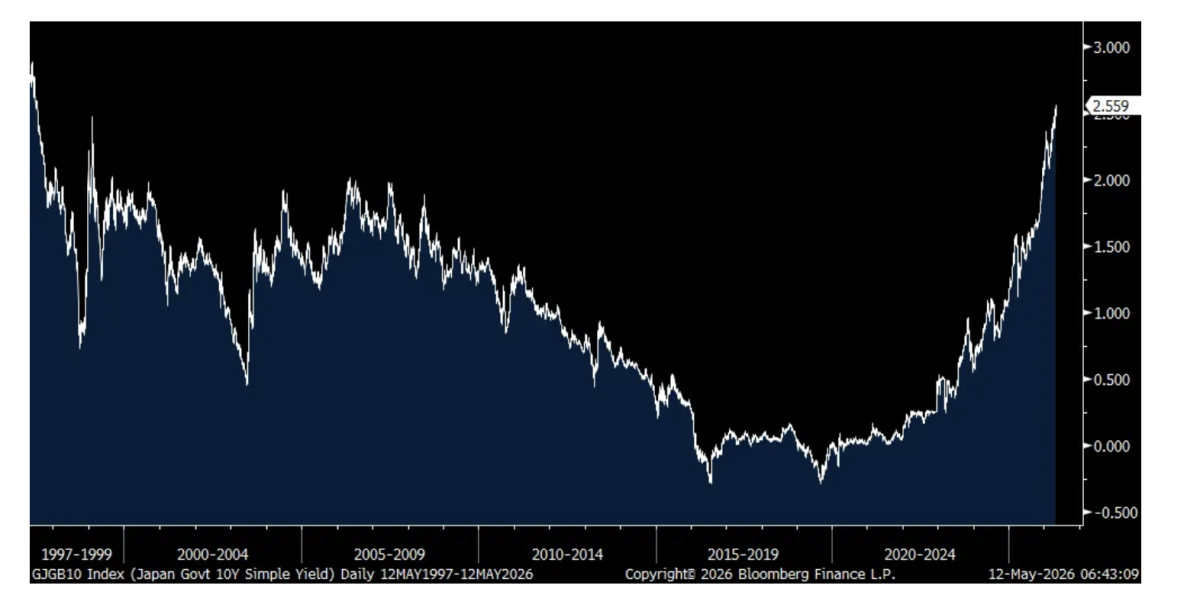

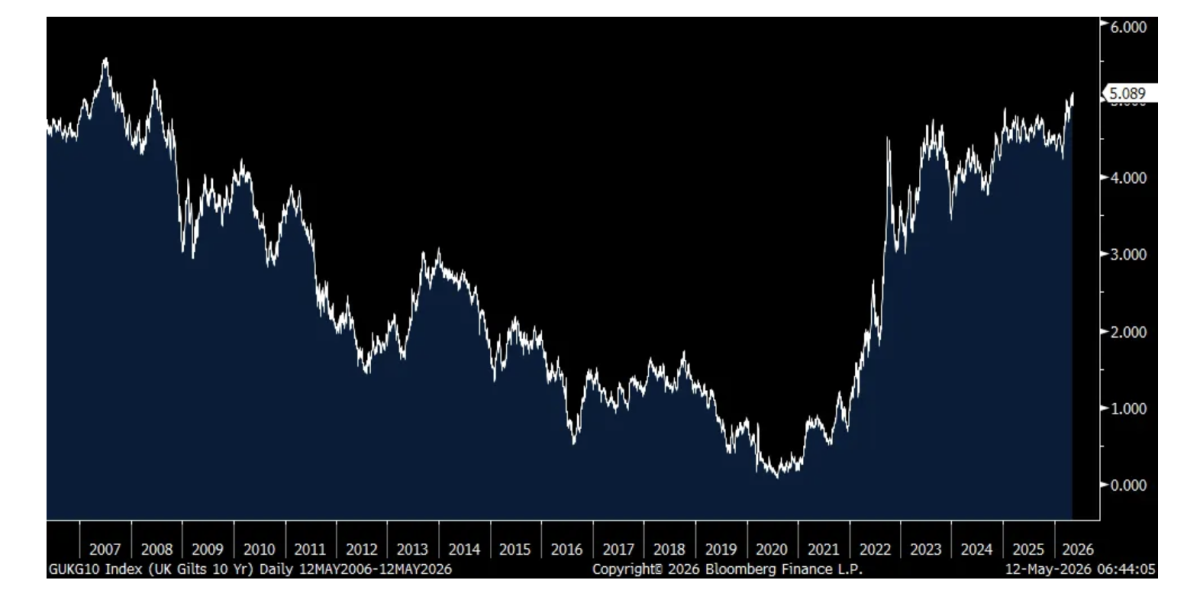

We have another day of rising bond yields globally. A fresh 29 year high in Japanese JGB 10 yr yield at 2.56%. A fresh 18 yr high in the UK 10 yr gilt yield at 5.09%. German and French 10 yr yields are just below their 15 yr highs at 3.08% and 3.71% respectively. Yields are up too throughout the Euro region and in Asia outside of China where yields were little changed. The US 30 yr yield is back to 5% and with the 10 yr yield, at 4.43%, keep your eye on 4.48% as that was intraday high seen in late March which was previously matched in July 2025.

We are not just dealing with the rise in commodity prices but in the cost of money too.

10 yr JGB Yield

10 yr UK Yield

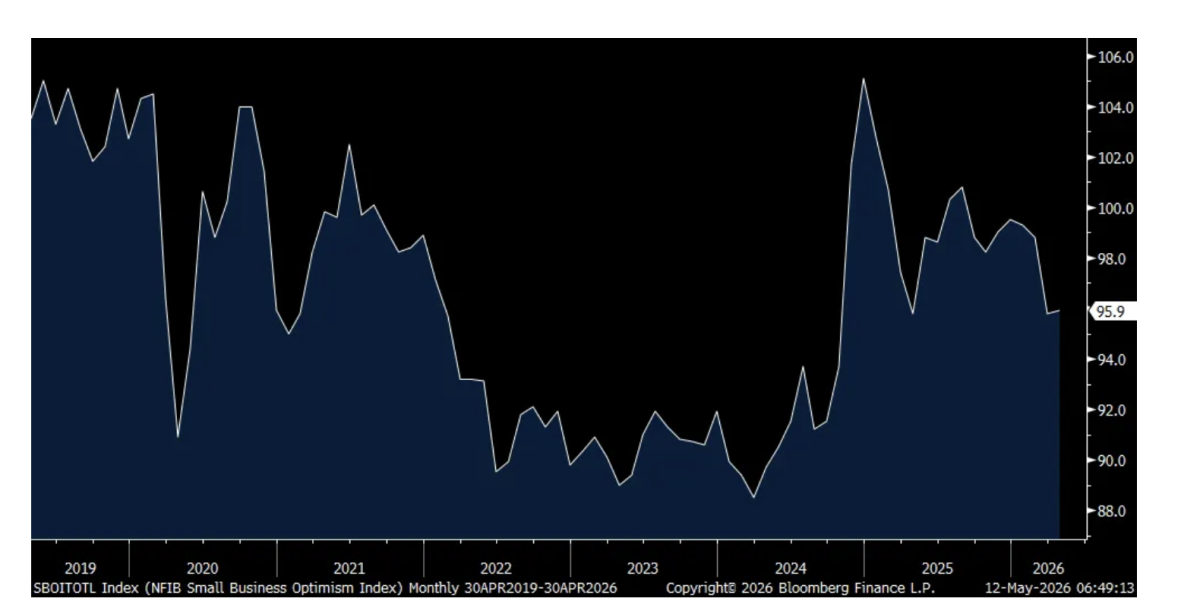

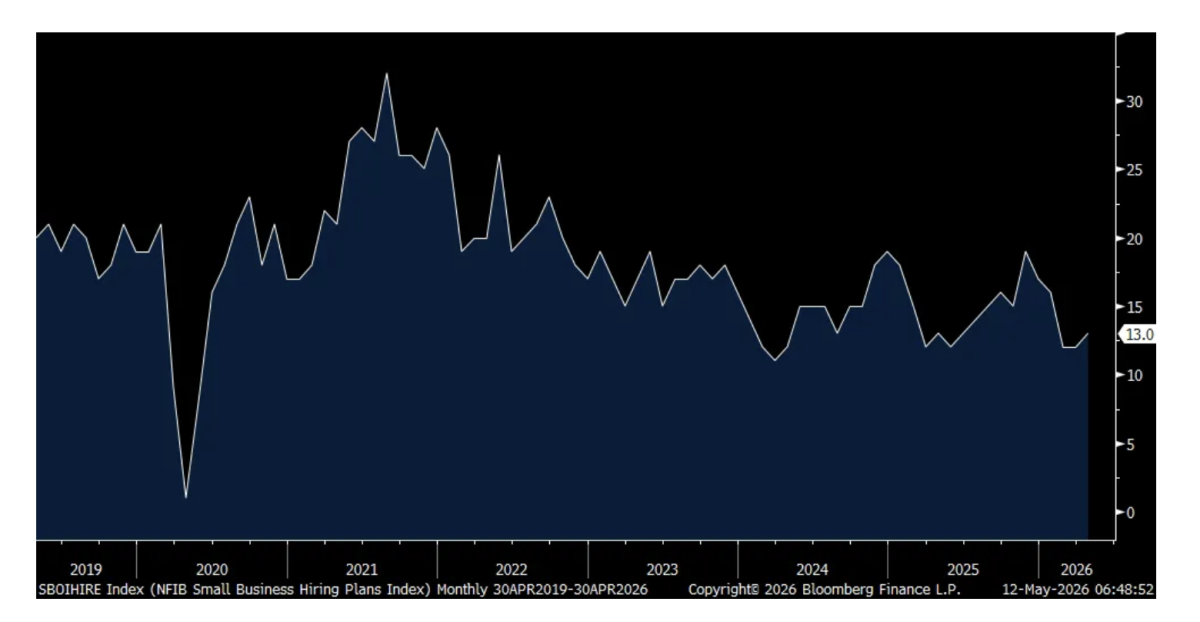

The April NFIB Small Business Optimism index was little changed at 95.9 vs 95.8 in March. Plan to Hire rose 1 pt off a one year low. Positions Not Able to Fill were up 2 pts m/o/m and to about where the 6 month average is. Compensation slipped 3 pts to 30% and vs 31% for the half yr average. Comp plans were unchanged at 18% but that is 3 pts below the 6 month average.

Off the lowest level since 2009, Capital Spending rose 1 pt while Plan to Increase Inventory was 3 pts less negative. Those that Expect a Better Economy fell to just 4% from 11% in March, 18% in February, 21% in January and vs 24% in December. Those that Expect Higher Sales fell 4 pts m/o/m to 3% vs the 6 month average of 10%. Good Time to Expand was down 4 pts to 7% vs the 6 month average of 12%.

After falling by 11 pts in March, Positive Earnings Trends rose 6 pts but to a still negative 19%. With inflation, Higher Selling Prices rose 5 pts to 30%, matching a 5 month high and 2 pts above its six month average. Those that plan to hike prices over the coming three months rose 3 pts.

To the point above about rising interest rates, the average rate paid on a loan rose to 8.3% from 7.9% in March but still remaining below the 10.1% touched in September 2024.

The NFIB’s bottom line, “Inflationary pressures continue to be a challenge for Main Street. While small business optimism is currently fragile, the benefits of the Working Families Tax Cut Act should start to feed into the private sector over the next few months.”

NFIB

Plan to hire

Expect Better Economy

Average Rate Paid on a Loan

Higher Selling Prices

Positions: None.

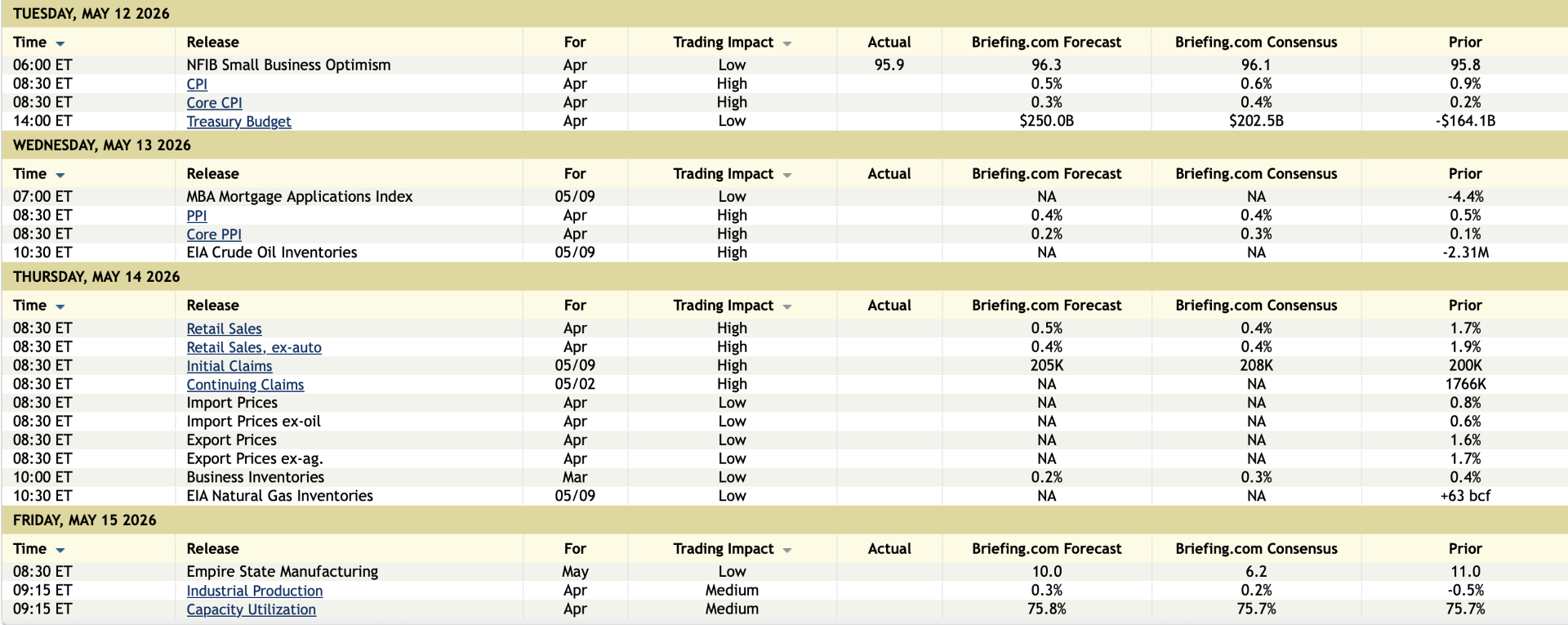

BY Doug Kass · May 12, 2026, 8:30 AM EDT

Positions: None.

BY Doug Kass · May 12, 2026, 8:13 AM EDT

Fed Speakers

9:10AM: Fed Bank of Chicago President Goolsbee (Non-Voter) Radio Appearance -- NPR Morning Edition

1:00PM: Fed Bank of Chicago President Goolsbee (Non-Voter) participates in moderated question-and-answer session before the Greater Rockford Chamber of Commerce, Rockford, IL (Livestream available. Embargoed text TBD)

Treasury Auctions:

11:00AM: Treasury Announces a 4 and 8 and 17 Week Bill Auction

11:00AM: Treasury buyback announcement (liq support)

11:30AM: Treasury hosts a $50B 52-Week Bill Auction

11:30AM: Treasury hosts a $80B6-Week Bill Auction

1:00PM: Treasury hosts a $42B 10-Year Note Auction

2:00PM: Federal Budget Balance (April)

Economic Calendar

Position: None

BY Doug Kass · May 12, 2026, 7:44 AM EDT

Monday's market advance had some conspicuous and worrisome divergences:

* Market breadth was poor and leadership continued to narrow (even more noticeably than in the past few days):

* The VIX strengthened to 18.38 (+1.19).

* Financials were noticeably weak. Homebuilders, restaurants (Shake Shack (SHAK) down by another -$6) and retailers (Walmart (WMT) -$3), hit by another boost in yields, suffered. Consumer staples and private-equity stocks, in particular, got taken to the woodshed with three-to five-dollar losses commonplace.

* Healthcare was strong and technology, of course, was led by memory and semiconductors (though software slipped with Oracle (ORCL) , Adobe (ADBE) , Salesforce (CRM) , IBM (IBM) all lower after recent strength).

* Nonetheless, a divergence in large-cap tech vs. rising indices, evidenced by the weakness in several components of the Mag 7, was probably the key feature of the day — with sizeable declines for Amazon (AMZN) (-$4), Google (GOOGL) (-$12), Microsoft (MSFT) (-$3) and Meta (META) (-$10).

I expanded my net short exposure by adding to technology and index shorts.

We took a new trading short rental (with a tight stop) in SanDisk (SNDK) (at $1,596) off the eye-popping overbought (RSI).

Position: Short SPY (S/M), QQQ (S/M), SNDK (VS)

BY Doug Kass · May 12, 2026, 7:05 AM EDT

BY Doug Kass · May 12, 2026, 6:45 AM EDT

⚠️Speculation in the US market is skyrocketing:

— Global Markets Investor (@GlobalMktObserv)

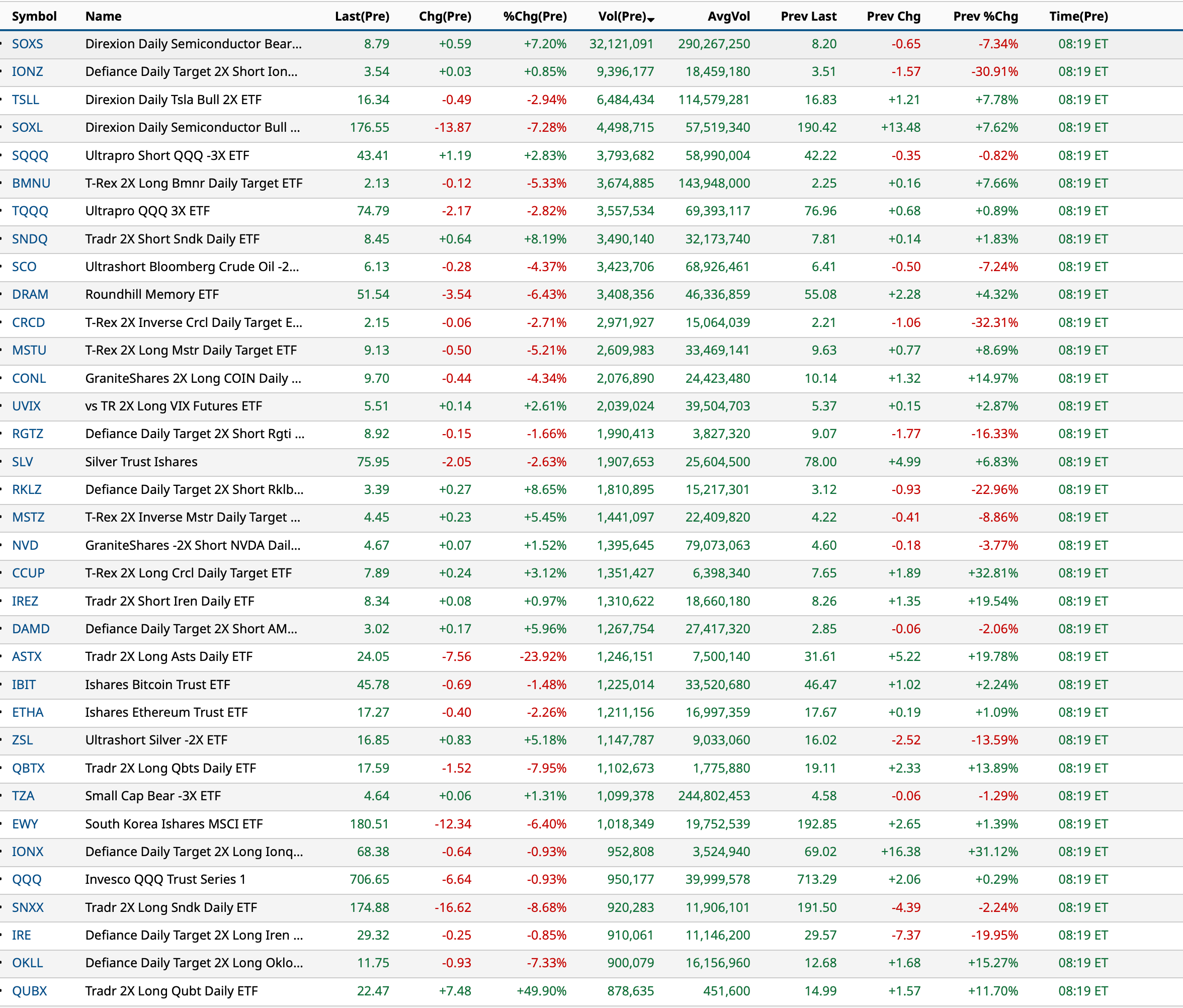

Assets under management (AUM) in leveraged and inverse single-stock ETFs have surged to a record ~$38 billion.

This has QUADRUPLED since 2024.

These products allow investors to bet on individual stocks moving up or down by 2 or 3… pic.twitter.com/cLyt1KZWlT

Position: None

BY Doug Kass · May 12, 2026, 6:35 AM EDT

These are insane numbers.

— zerohedge (@zerohedge)

Over the past month:

levered ETF rebal total: +$115B of Buying;

LevETF TECH +$46.9B of Buying;

LevETF SEMIS +$43.8B of Buying;

LevETF Mag7 +$13.2B of $Buying

Insane in the brain.

Position: None

BY Doug Kass · May 12, 2026, 6:25 AM EDT

Cathie Wood literally missed the AI bubble. pic.twitter.com/6lMR7jjPhb

— Alexander Stahel 🌻 (@BurggrabenH)

Position: None

BY Doug Kass · May 12, 2026, 6:15 AM EDT

The 16% gain in the S&P 500 over the last 6 weeks is the 11th biggest 6-week gain for the index since 1950.

— Charlie Bilello (@charliebilello)

What's unique about this rally?

It's the only example in the top 20 that did not occur either during a bear market or soon after a bear market low. pic.twitter.com/VDCUtiTpGR

Position: None

BY Doug Kass · May 12, 2026, 6:06 AM EDT

The S&P Short Range Oscillator is modestly overbought at 1.01% vs. 1.65%.

Position: Short SPY (S/M), QQQ (S/M)

BY Doug Kass · May 12, 2026, 5:55 AM EDT

In watching the shows yesterday, it appears that everyone will "know" when to sell tech/semis... before the others:

Semiconductor Stocks are now trading 63% above their 200-day moving average, the largest margin since the Dot Com Bubble Burst 🚨🚨🚨 pic.twitter.com/mZZhJLFiKX

— Barchart (@Barchart)

More on technology stocks in Wednesday's opening missive.

Position: None

BY Doug Kass · May 12, 2026, 5:45 AM EDT

Anthropic just published a support page that should terrify anyone holding its shares on the secondary market. "Any sale or transfer of Anthropic stock, or any interest in Anthropic stock, that has not been approved by our Board of Directors is void and will not be recognized on Show more

These are insane numbers. Over the past month: levered ETF rebal total: +$115B of Buying; LevETF TECH +$46.9B of Buying; LevETF SEMIS +$43.8B of Buying; LevETF Mag7 +$13.2B of $Buying

⚠️Speculation in the US market is skyrocketing: Assets under management (AUM) in leveraged and inverse single-stock ETFs have surged to a record ~$38 billion. This has QUADRUPLED since 2024. These products allow investors to bet on individual stocks moving up or down by 2 or 3Show more

Semiconductor Stocks are now trading 63% above their 200-day moving average, the largest margin since the Dot Com Bubble Burst 🚨🚨🚨

The 16% gain in the S&P 500 over the last 6 weeks is the 11th biggest 6-week gain for the index since 1950. What's unique about this rally? It's the only example in the top 20 that did not occur either during a bear market or soon after a bear market low.